Understanding the dynamics between customer loyalty metrics and brand perception is pivotal in contemporary marketing research. This chapter examines two critical constructs: the Net Promoter Score (NPS) and brand image. The former serves as a gauge for customer loyalty and potential business growth, while the latter encapsulates consumers’ perceptions and associations with a brand. By exploring existing literature, we aim to elucidate the individual dimensions of these constructs and their interrelationship, providing a foundation for subsequent empirical analysis.

2.1. The Net Promoter Score

The Net Promoter Score (NPS) has become one of the most widely adopted metrics in customer experience and relationship marketing, particularly for its purported simplicity and predictive value. Introduced by

Reichheld (

2003), NPS is based on a single question that asks customers how likely they are to recommend a company, product, or service to others. Responses are given on an eleven-point scale from 0 (not at all likely) to 10 (extremely likely), with respondents then categorized as promoters (scores of 9–10), passives (7–8), or detractors (0–6). The final NPS is calculated by subtracting the percentage of detractors from the percentage of promoters.

The original appeal of NPS stemmed from its intuitive design and the argument that it served as a strong predictor of business growth.

Reichheld (

2003) claimed that NPS could explain variances in company performance better than traditional customer satisfaction metrics, especially when applied consistently over time. As a result, many organizations adopted NPS not only as a tool for monitoring customer loyalty but also as a key performance indicator linked to employee bonuses, strategy, and product development (

Reichheld et al., 2021). Its widespread implementation across sectors (including banking, telecommunications, retail, and healthcare) has further contributed to its perceived legitimacy and utility in both academic and practitioner circles (

Zolkiewski et al., 2017).

Despite its popularity, NPS has not been without criticism. Scholars have pointed to several conceptual and methodological limitations that challenge its validity.

Keiningham et al. (

2007) were among the first to question the metric’s ability to predict growth, demonstrating that alternative satisfaction and loyalty measures often outperform NPS in explanatory power. Furthermore, the categorization of responses into promoters, passives, and detractors has been criticized for discarding valuable information and oversimplifying consumer sentiment (

Kristensen & Eskildsen, 2014). This reductionist approach may obscure the nuances of customer experience, especially in industries with complex service offerings, such as financial services or healthcare. Another point of contention is the assumption that the likelihood to recommend is universally understood and valued across different cultural and demographic contexts. Research indicates that cultural norms affect how likely individuals are to make recommendations, leading to possible systematic biases in NPS results across markets (

Baehre et al., 2021). Moreover, the scale itself has been debated. Some researchers argue that treating the 11-point scale as categorical, as in the traditional NPS model, limits its usefulness for advanced statistical analysis. Treating NPS as a continuous variable, instead, can reveal more nuanced insights through correlation or regression analysis (

N. A. Morgan & Rego, 2006).

Nonetheless, NPS continues to be widely used, in part due to its ease of implementation and the strategic clarity it provides for managers. Its application as a proxy for customer advocacy, loyalty, and overall satisfaction makes it an attractive option for businesses seeking actionable feedback. The ongoing academic debate highlights the need for organizations to interpret NPS within context, potentially supplementing it with additional qualitative or quantitative measures to gain a more comprehensive understanding of customer perceptions.

2.2. Image

Brand image is a pivotal concept in marketing, referring to the collective perceptions and associations that consumers hold about a brand (

Keller, 1993). It encompasses the beliefs, ideas, and impressions that are formed through direct and indirect experiences with a company and its products or services. One of the most influential definitions comes from

Keller (

1993), who describes brand image as the set of brand associations held in consumer memory. These associations can be shaped by various touchpoints, including advertising, customer service interactions, peer recommendations, and personal experiences.

Brand image is multifaceted, consisting of cognitive, emotional, and symbolic components. On a cognitive level, consumers evaluate functional attributes such as reliability, performance, or convenience. Emotional components relate to how the brand makes the consumer feel, whether it evokes trust, excitement, or security. Symbolic aspects reflect the degree to which a brand aligns with a consumer’s identity or values (

Aaker, 1996). Collectively, these components influence not only how consumers perceive the brand but also how they behave toward it, impacting purchase intentions, loyalty, and advocacy. The significance of brand image lies in its effect on consumer decision-making. A positive brand image enhances perceived value, reduces perceived risk, and increases customer satisfaction and loyalty (

Nguyen & Leblanc, 2001). Consumers often rely on brand image as a heuristic when making purchasing decisions, especially in low-involvement or complex product categories. For instance, in financial services, where product differentiation is minimal, brand image can serve as a key differentiator and a source of competitive advantage (

Bravo et al., 2009). In these cases, attributes such as trustworthiness, corporate social responsibility, and customer care become critical elements of brand perception.

From a strategic perspective, managing brand image is essential for maintaining strong brand equity.

Aaker (

1991) posits that brand image contributes to brand equity by influencing consumer preferences, purchase behavior, and the willingness to pay a price premium. In this sense, brand image is not only a reflection of current market perceptions but also a driver of future brand performance. Companies invest heavily in shaping brand image through marketing communication, visual identity, customer experience, and public relations, aiming to create consistent and favorable brand associations over time.

Measuring brand image presents methodological challenges due to its abstract and subjective nature. Common approaches include the use of structured surveys employing Likert-type or semantic differential scales to assess perceptions across a range of attributes, such as reliability, friendliness, or modernity (

Rio et al., 2001). Factor analysis is often employed to identify underlying dimensions of brand image from observed attributes, thereby simplifying interpretation and enabling comparison across brands. Additionally, qualitative techniques such as brand personality profiling or projective methods can be used to capture deeper, symbolic meanings associated with brands (

Zhang, 2015). As markets become increasingly saturated and competitive, brand image plays a central role in differentiating offerings and fostering customer loyalty. It acts as a psychological shortcut in consumer decision-making and serves as a key asset in long-term brand management. The continuous monitoring and strategic development of brand image are therefore vital for sustaining competitive advantage in today’s dynamic marketing environment.

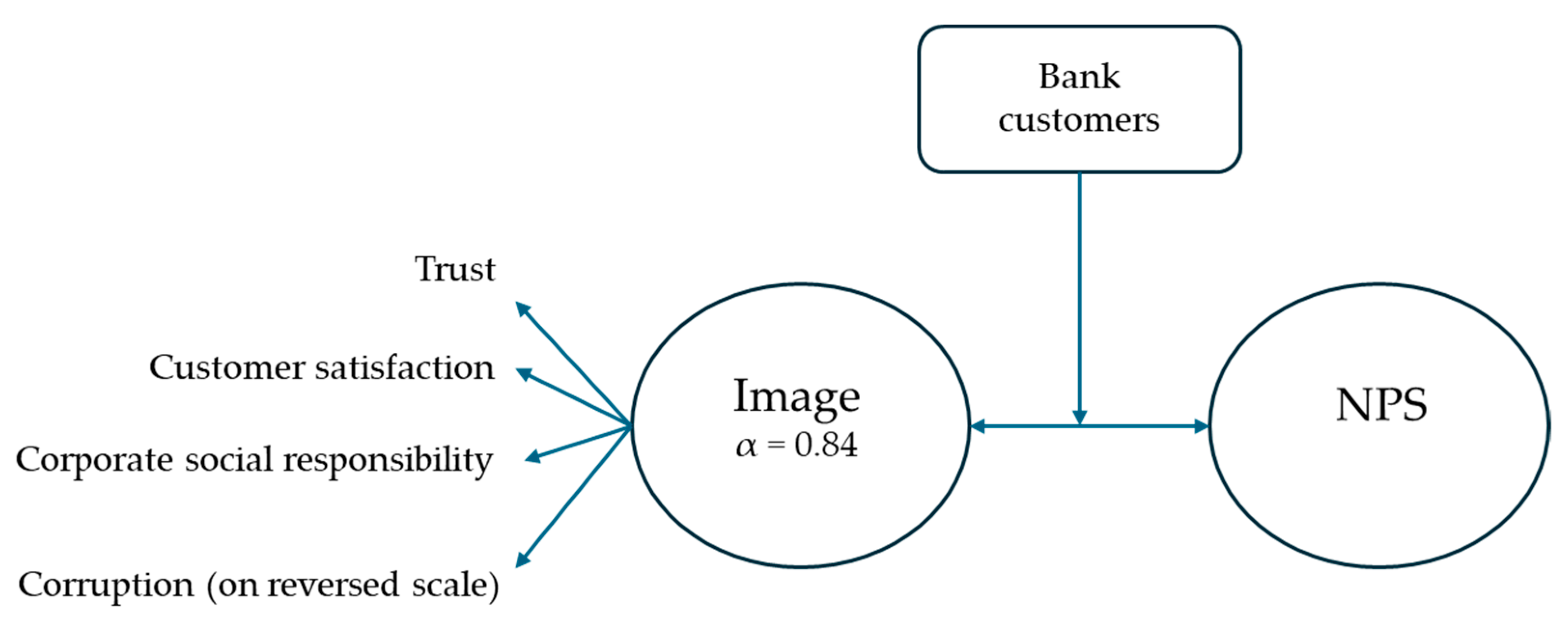

This study is part of a research project that has been ongoing since 2004 and uses the perceptual mapping method for measuring image or position of the brand in the mind of customers (

Lilien & Rangasqamy, 2004). Perceptual mapping is a strategic tool widely used in marketing to visually represent consumer perceptions of brands relative to one another across selected attributes which are considered important for the industry. The attributes used here were defined in a detailed preparatory study in 2004 and included, among others, trust, CSR, customer satisfaction, and corruption, which were considered important for the banking sector. These attributes have been assessed regularly since 2004.

Trust is a core determinant of long-term customer relationships and loyalty (

Chaudhuri & Holbrook, 2001). In perceptual mapping, trust functions as a critical axis that differentiates brands not merely on performance, but on relational quality. Consumers are more likely to exhibit brand commitment and word-of-mouth advocacy when trust is high, making it a non-negotiable factor in brand evaluation (

R. M. Morgan & Hunt, 1994).

Corporate social responsibility has emerged as a significant factor influencing consumer perceptions and brand evaluations, particularly among socially conscious demographics. CSR initiatives, such as environmental stewardship, community engagement, and ethical sourcing, signal a brand’s alignment with broader societal values (

Du et al., 2010). Including CSR in perceptual mapping allows firms to position themselves in terms of moral capital, which can drive differentiation and consumer goodwill (

Luo & Bhattacharya, 2006). Furthermore, CSR perceptions are known to interact with brand trust and emotional attachment, amplifying their impact on brand loyalty (

Pivato et al., 2008).

Customer satisfaction remains a robust predictor of repurchase intention, brand loyalty, and profitability (

Anderson et al., 1994). As a perceptual attribute, it captures consumers’ cumulative evaluation of brand performance and experience. Measuring customer satisfaction enables organizations to understand where they stand in delivering value compared to competitors, which is essential for identifying areas requiring operational or experiential improvements (

Oliver, 1997). Moreover, satisfaction levels often mediate the relationship between other brand attributes, such as CSR or trust, and behavioral outcomes (

Homburg et al., 2006).

Corruption is actually the opposite of trust and when using perceptual mapping it is necessary to have attributes that are opposite (

Lilien & Rangasqamy, 2004). While often overlooked in traditional marketing models, perceived corruption or lack of integrity can substantially damage brand equity, especially in industries where trust is paramount (

Rodriguez et al., 2006) which is the case in banking. In emerging markets or highly regulated industries, consumers’ perceptions of ethical conduct, including transparency, honesty, and fairness, can be as influential as product quality. Incorporating corruption as a perceptual dimension helps map negative space in brand positioning, highlighting reputational risks and informing crisis communication strategies. Research suggests that even indirect associations with unethical behavior can harm consumer trust and reduce brand legitimacy (

Chang, 2011).

Integrating trust, CSR, customer satisfaction, and corruption when measuring image provides a multidimensional view of brand equity that is more aligned with contemporary stakeholder expectations. Such an approach supports more socially attuned and ethically grounded branding strategies. From a research standpoint, it encourages the application of stakeholder theory and signaling theory to perceptual analysis, expanding traditional consumer-centric paradigms (

Freeman, 1984;

Spence, 1973). As brands navigate complex consumer expectations and an increasingly transparent digital landscape, traditional positioning based solely on price or quality is no longer sufficient. The inclusion of trust, CSR, customer satisfaction, and perceived corruption when measuring image offers a powerful framework for understanding brand equity through a moral and experiential lens. This approach not only enhances strategic clarity but also supports ethical brand management and stakeholder alignment in a socially conscious marketplace. For these reasons, it is very interesting and important to examine the relationship between image, which is composed of the above-mentioned attributes, and NPS.

2.3. The Relationship Between NPS and Image

The relationship between the Net Promoter Score (NPS) and brand image has become increasingly relevant in the context of brand performance measurement and strategic customer management. While NPS is primarily used as a metric for customer loyalty and advocacy (

Reichheld, 2003), brand image encompasses the perceptions and associations that shape how consumers evaluate and relate to a brand (

Keller, 1993). Understanding the intersection of these constructs is crucial for organizations seeking to foster long-term relationships, enhance reputation, and drive sustainable growth (

Baehre et al., 2021). Although both concepts originate from different theoretical backgrounds—NPS from customer experience management and brand image from consumer psychology—their convergence reflects the broader evolution of marketing toward a customer-centric paradigm. Several scholars have investigated the empirical and conceptual ties between brand image and NPS, identifying multiple pathways through which they may influence one another (

Baehre et al., 2021;

de Haan et al., 2015;

Keiningham et al., 2008). These studies show that factors like trust, perceived value, and overall satisfaction, which are integral components of brand image, play a critical role in shaping customers’ willingness to recommend a brand, as measured by NPS.

On a basic level, a favorable brand image enhances the likelihood of a customer becoming a promoter. As NPS directly measures customers’ willingness to recommend, it is logical that such advocacy stems from positive brand experiences and strong emotional or symbolic associations with the brand. According to

de Haan et al. (

2015), customer satisfaction and brand perceptions are significant antecedents of NPS ratings. In their study across several industries, they found that improvements in brand image attributes, such as trust, innovativeness, and social responsibility, positively influenced NPS outcomes, highlighting a direct link between perceived image and willingness to recommend. This relationship can be further explained through the lens of brand equity and customer-based brand strength. Brand image, as part of the overall brand equity framework (

Keller, 1993), contributes to brand value by shaping customer attitudes, satisfaction, and loyalty. These constructs are highly predictive of NPS, which acts as a proxy for customers’ emotional and rational attachment to the brand.

Baehre et al. (

2021) argue that when NPS is treated not as a strict performance indicator but as a brand health metric, it reflects the cumulative effects of various image-related components, including service quality, corporate reputation, and consumer trust.

Empirical studies in sectors such as banking, telecommunications, and hospitality support these theoretical claims. Recent studies from outside the banking sector also support this connection. For instance,

Harrigan et al. (

2018) found that brand image significantly influenced customer advocacy in both hospitality and telecom contexts. Similarly,

Xie et al. (

2022) demonstrated strong links between brand trust and advocacy across several industries, including e-commerce and transportation, reinforcing the relevance of these dynamics beyond financial services. In a study on retail banking,

Bravo et al. (

2012) demonstrated that brand image factors (particularly trust and corporate social responsibility) significantly influenced customers’ loyalty behaviors, including their likelihood to recommend the bank. These behaviors align closely with how NPS is operationalized, suggesting that image and NPS are not independent constructs, but rather mutually reinforcing. Similarly,

Keiningham et al. (

2007) highlighted that satisfaction and perceived image quality were strong predictors of recommendation behavior, further supporting the idea that brand image can explain variations in NPS. Beyond direct influence, brand image also moderates the interpretation and strategic use of NPS data. In markets where trust and reputation are essential, such as financial services, a high NPS score may not be achievable without a strong underlying image. This point is particularly important in comparative studies across industries or regions.

Kristensen and Eskildsen (

2014) noted that differences in national culture and brand familiarity can affect both brand perceptions and NPS evaluations, potentially confounding their relationship. Therefore, analyzing NPS without accounting for brand image may lead to incomplete or misleading conclusions about customer sentiment and future behavior.

At the same time, it is important to acknowledge that the relationship between brand image and NPS is not entirely linear. Some customers may have favorable perceptions of a brand yet be unlikely to recommend it, due to personal preferences, switching costs, or social dynamics.

Reichheld et al. (

2021) suggest that while promoters are often emotionally connected to the brand, not all satisfied or loyal customers become advocates. This asymmetry suggests that while brand image is a necessary condition for high NPS, it may not be sufficient on its own. Other factors, such as customer effort, recent service experiences, or emotional triggers, may mediate or moderate the image–NPS link.

From a managerial perspective, integrating brand image analysis with NPS tracking offers several strategic benefits. Organizations can identify which dimensions of image, such as trust, innovation, or environmental responsibility, are most predictive of advocacy and prioritize investment accordingly (

Bravo et al., 2012;

Keller, 1993). Moreover, using image-based segmentation in NPS analysis allows for more nuanced interpretation of results, helping firms distinguish between passive satisfaction and active enthusiasm (

Baehre et al., 2021). As brands seek to build long-term customer relationships and differentiate themselves in competitive markets, this integrated approach enables more targeted, effective brand and experience management (

Zolkiewski et al., 2017). In conclusion, the relationship between NPS and brand image is both conceptually coherent and empirically supported. NPS reflects the outcome of accumulated brand perceptions, while brand image shapes the emotional and cognitive foundation for customer loyalty and advocacy (

de Haan et al., 2015). The interplay between these constructs reinforces the importance of managing customer experience and brand equity in tandem. As research in this area evolves, future studies may benefit from exploring longitudinal dynamics, industry-specific variations, and cross-cultural contexts to deepen understanding and enhance practical application.

Figure 1 shows a hypothetical model exploring the relationship between image and NPS and whether there are differences depending on the banks’ customer groups.

To investigate these relationships empirically, the following chapter outlines the methodological approach used in this study. It describes the research design, data collection procedures, sample characteristics, and the analytical techniques employed to examine the connection between brand image and NPS across multiple measurement periods.

{kind=link}