Women’s Entrepreneurship and Government Policy: Facilitating Access to Credit through a National Program in Chile

Abstract

:1. Introduction

2. Materials and Methods

2.1. Literature Review

2.2. CreceMujer Emprendedora Program

2.3. Research Design

2.4. Data

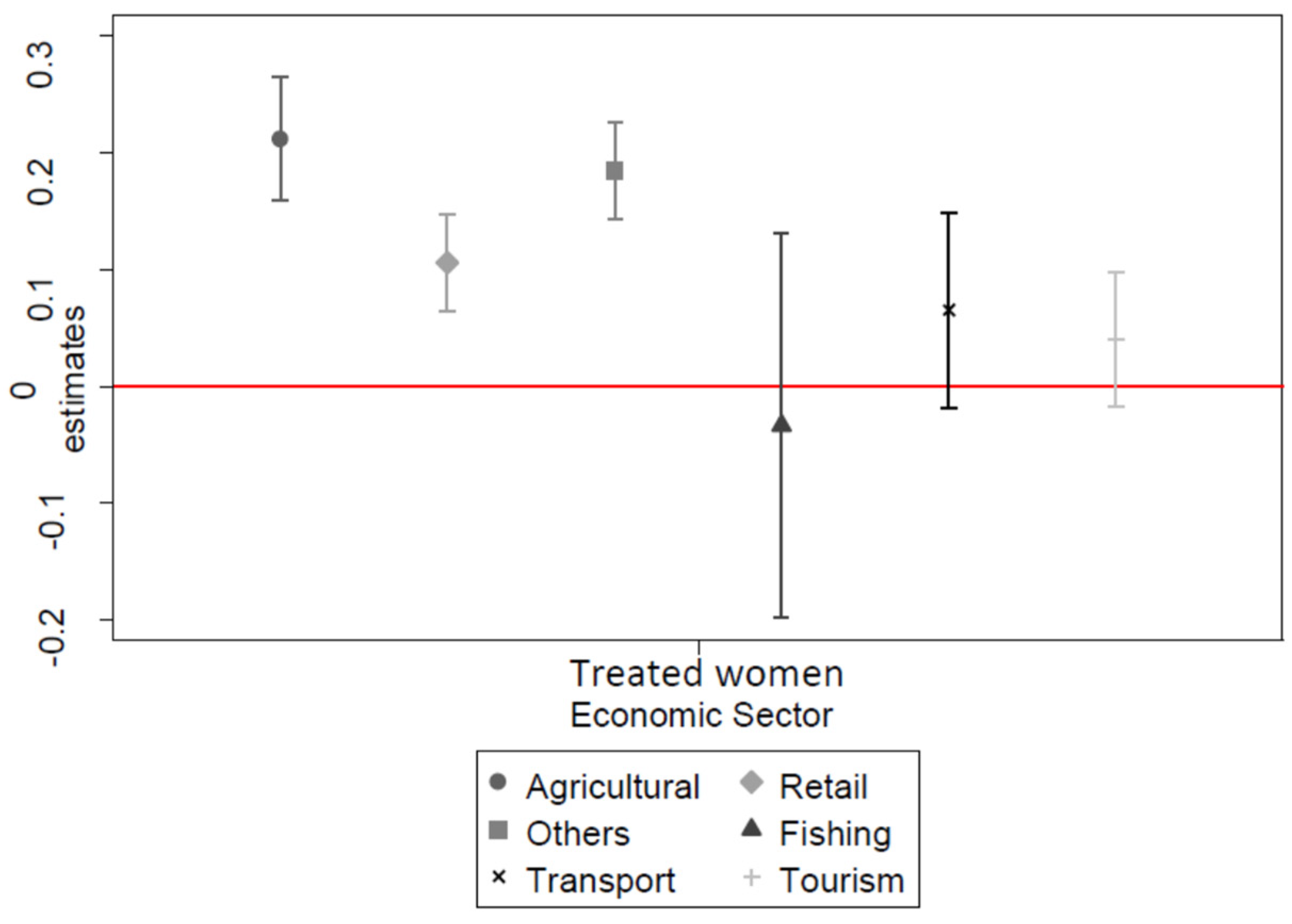

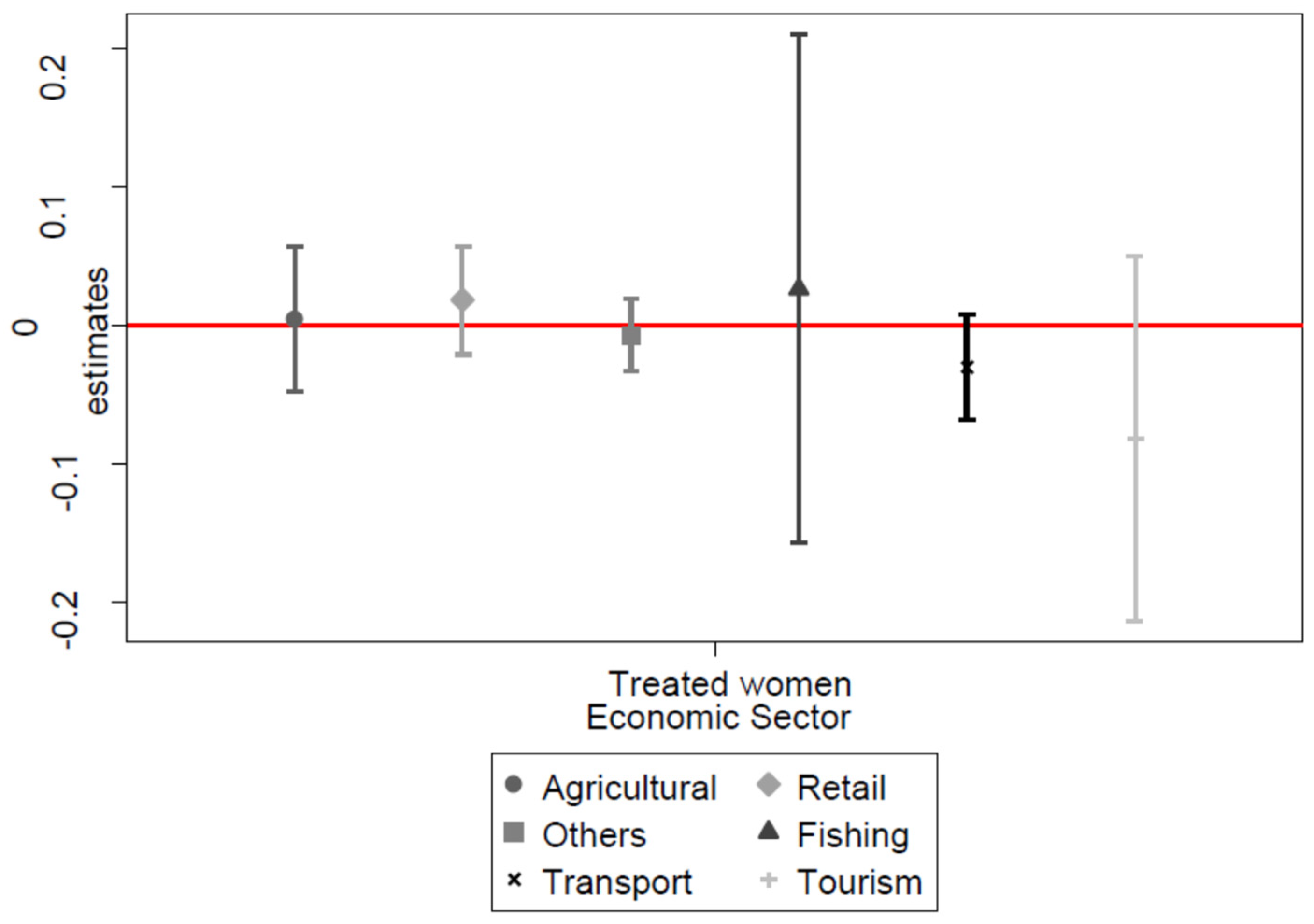

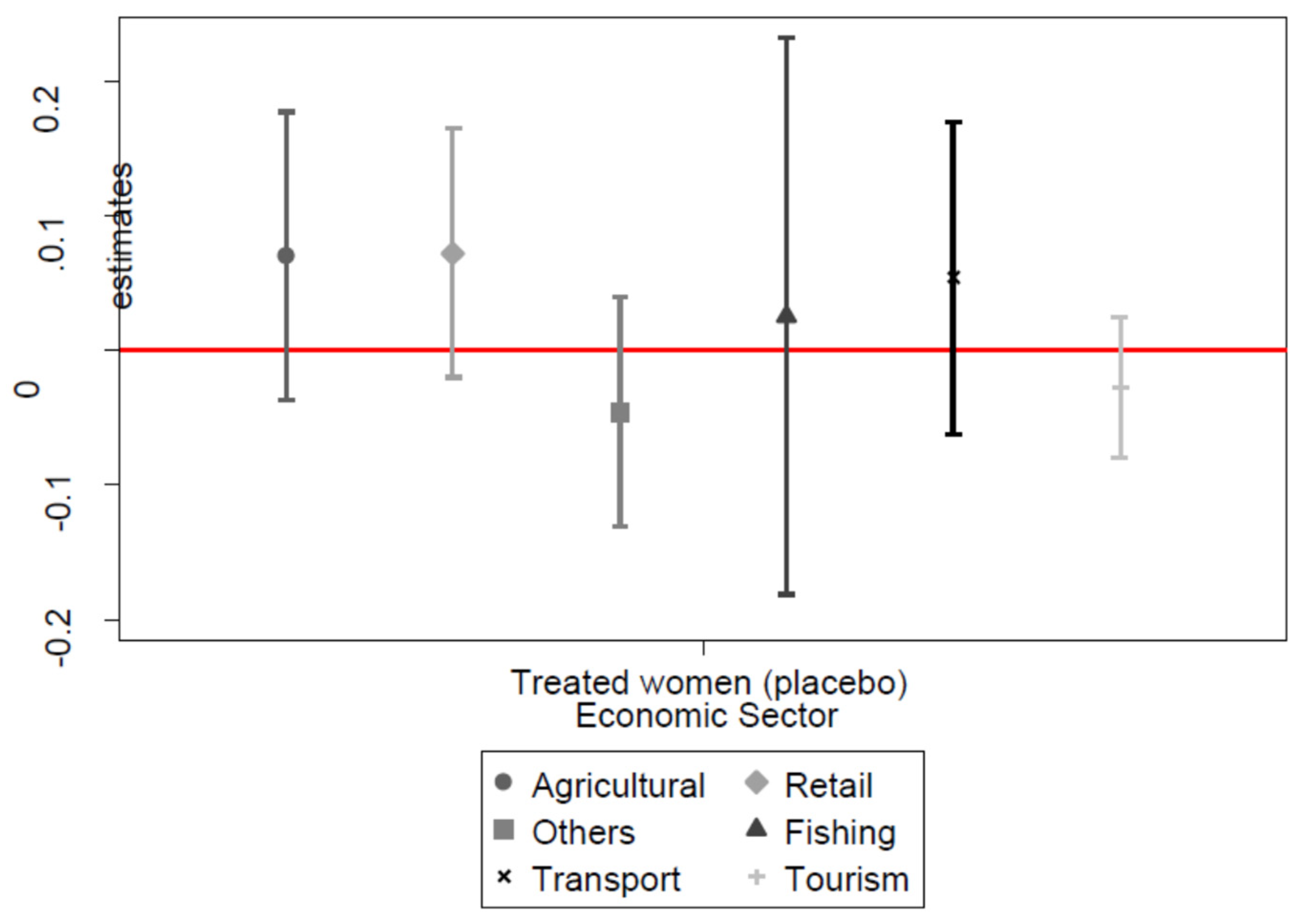

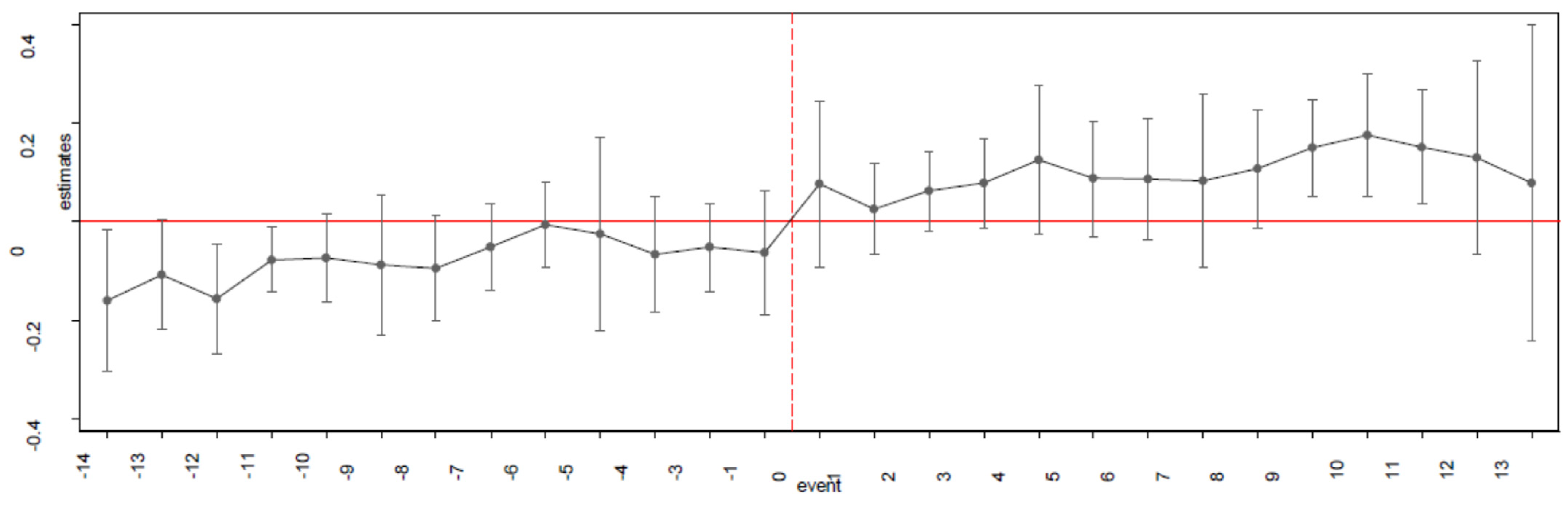

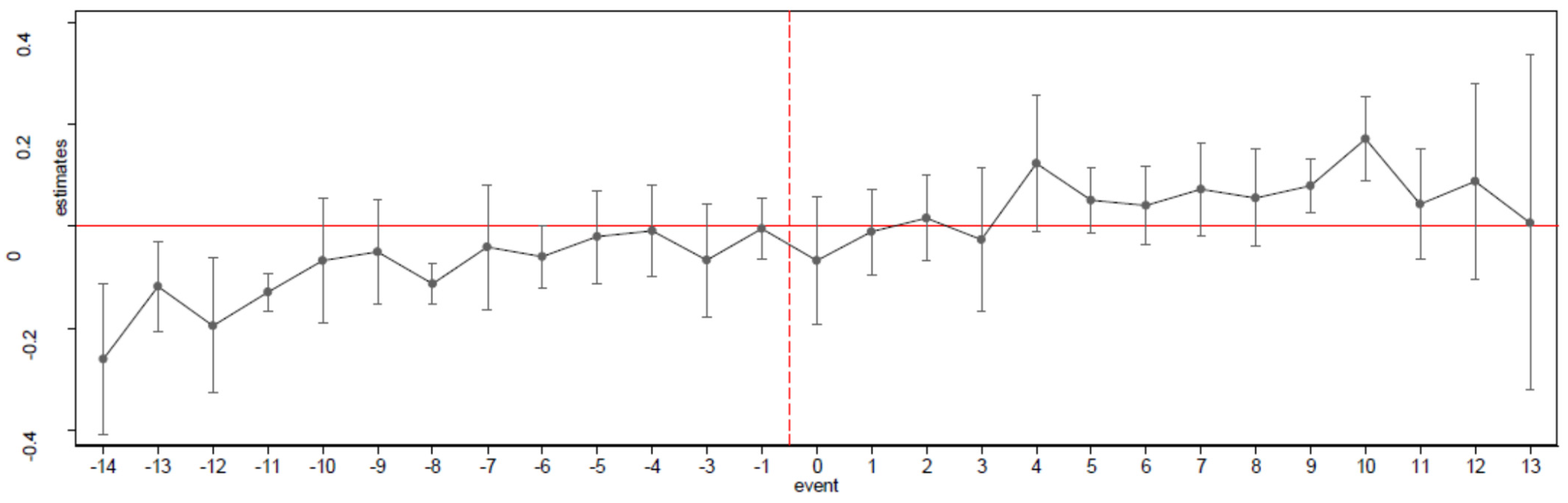

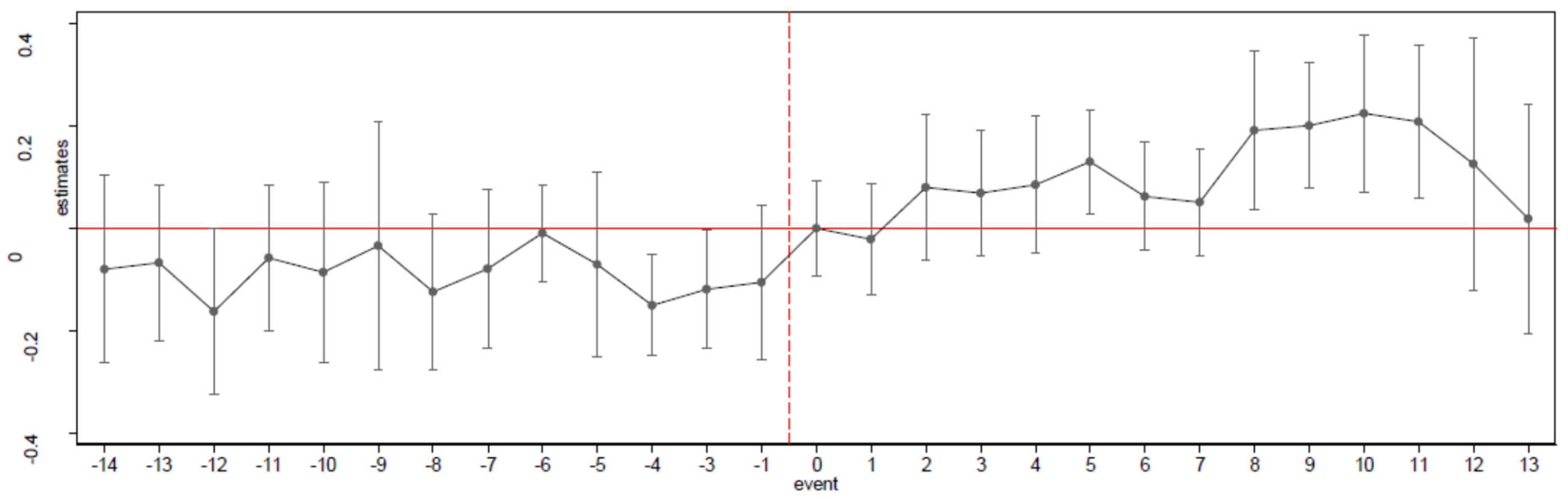

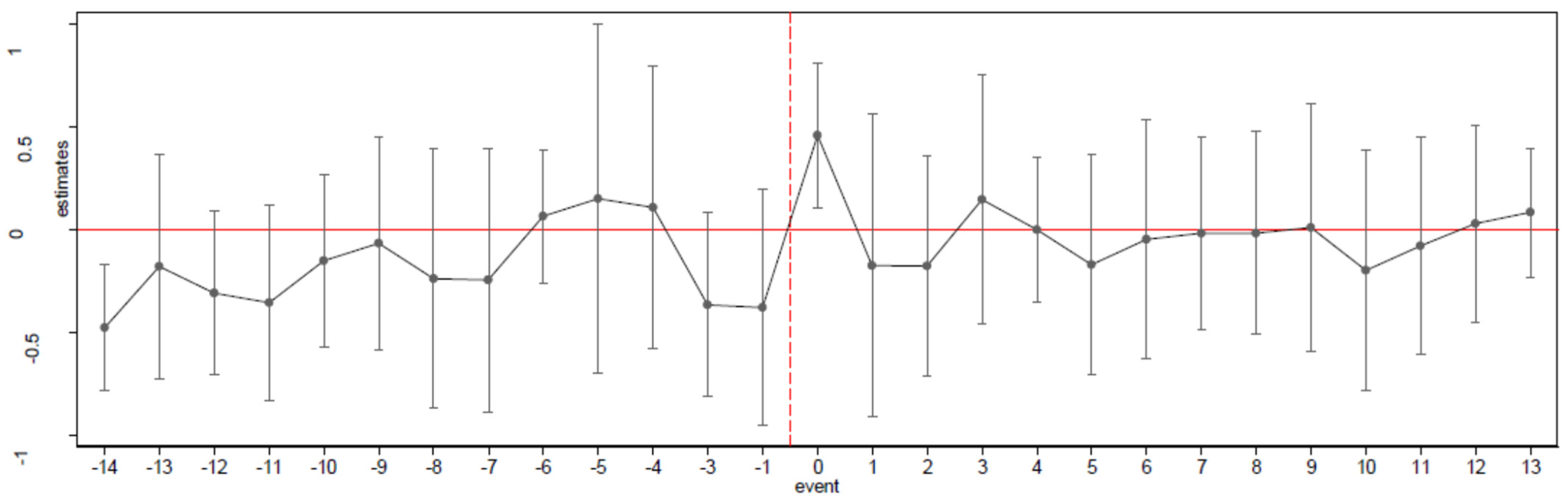

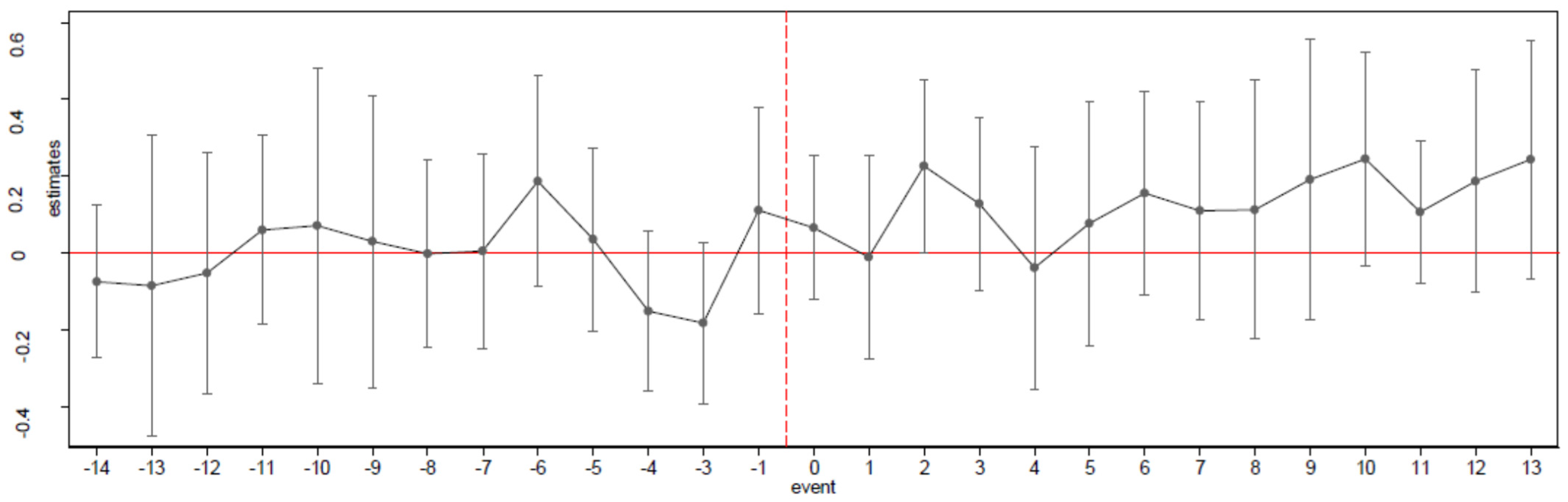

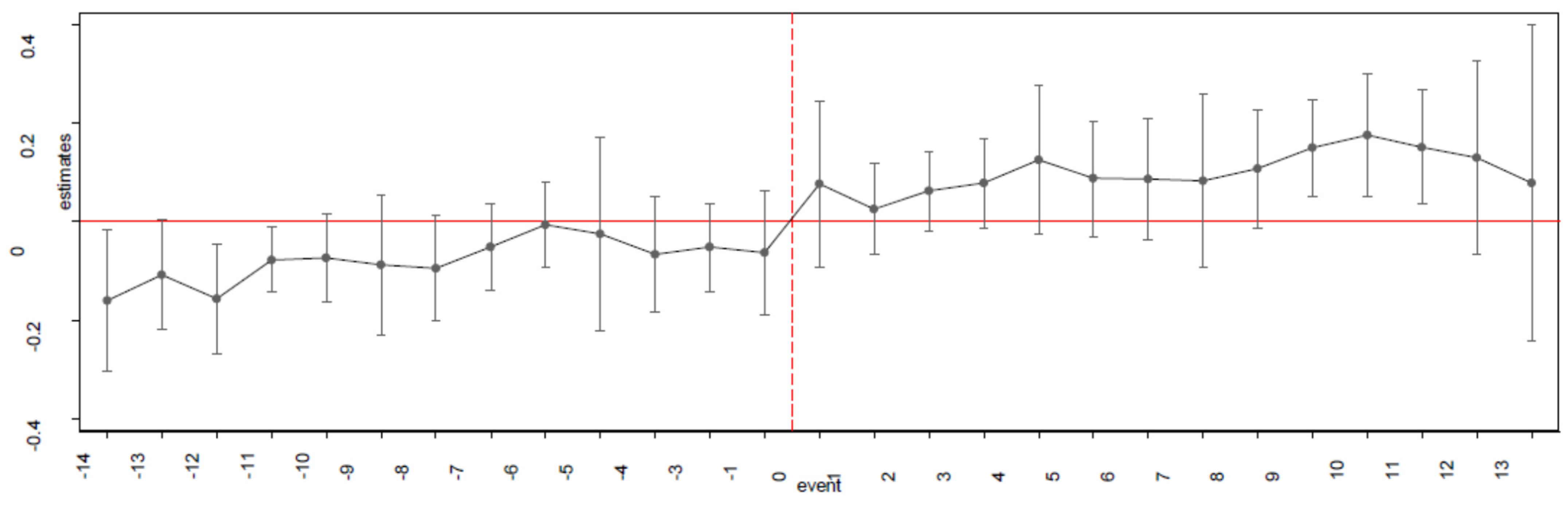

3. Results

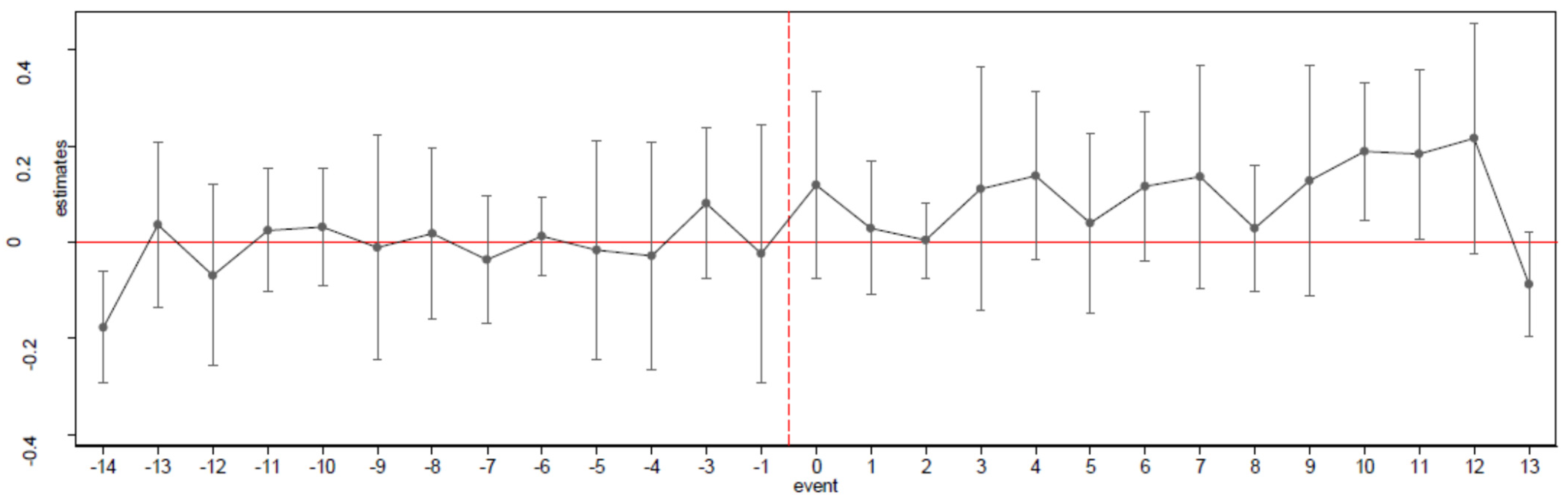

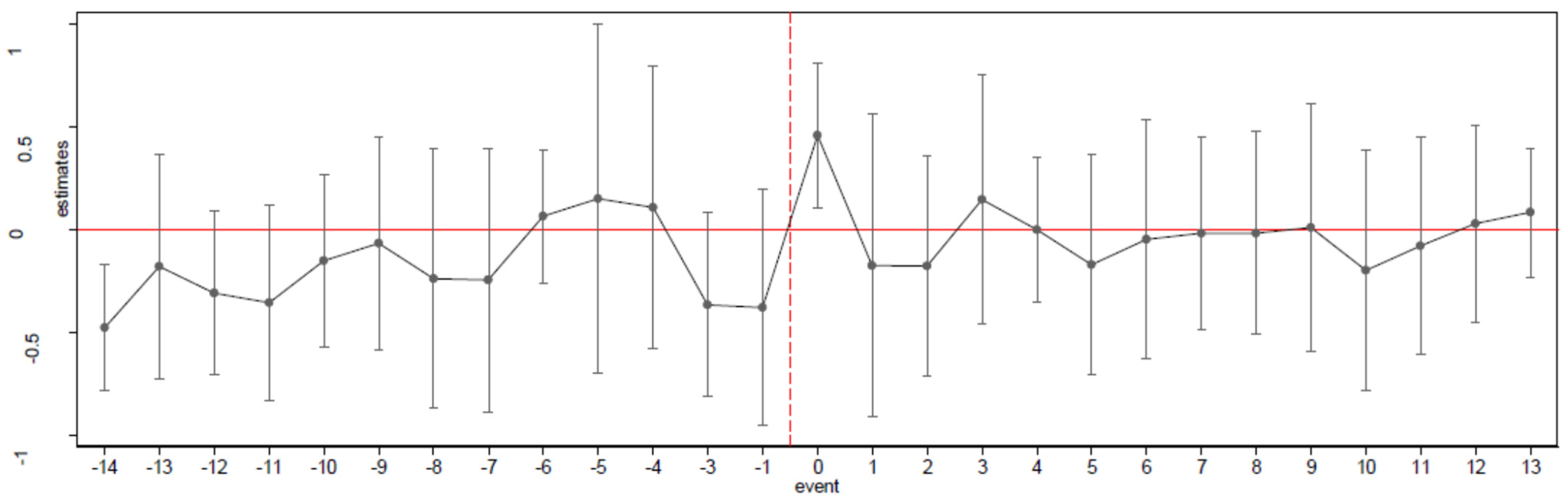

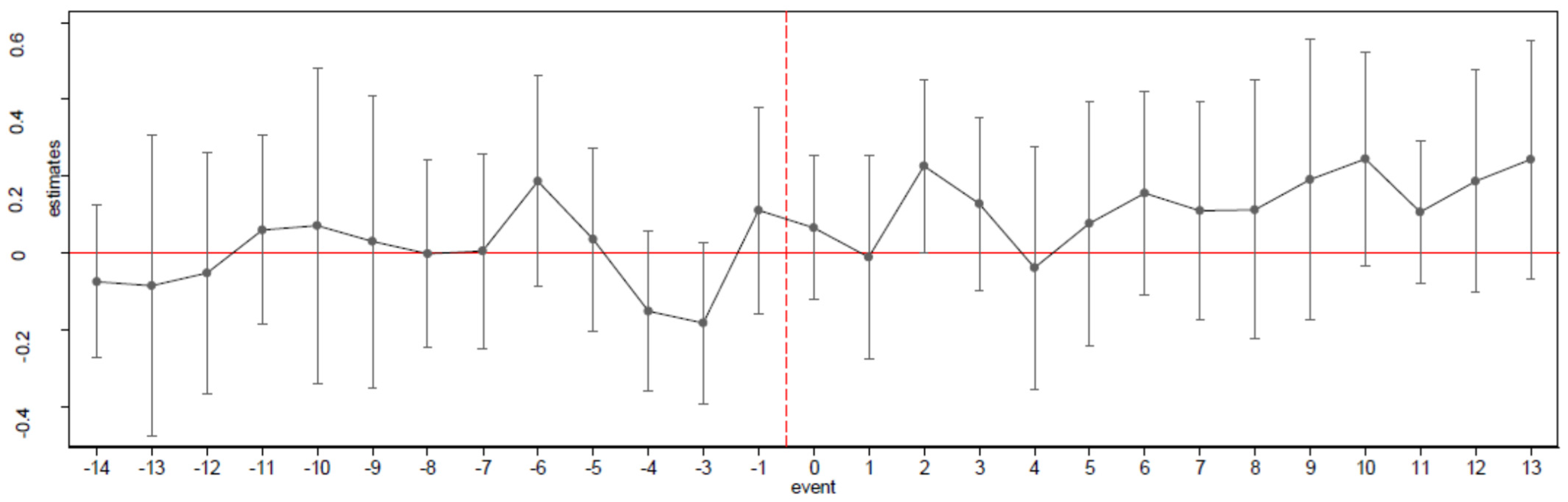

4. Discussion

5. Conclusions

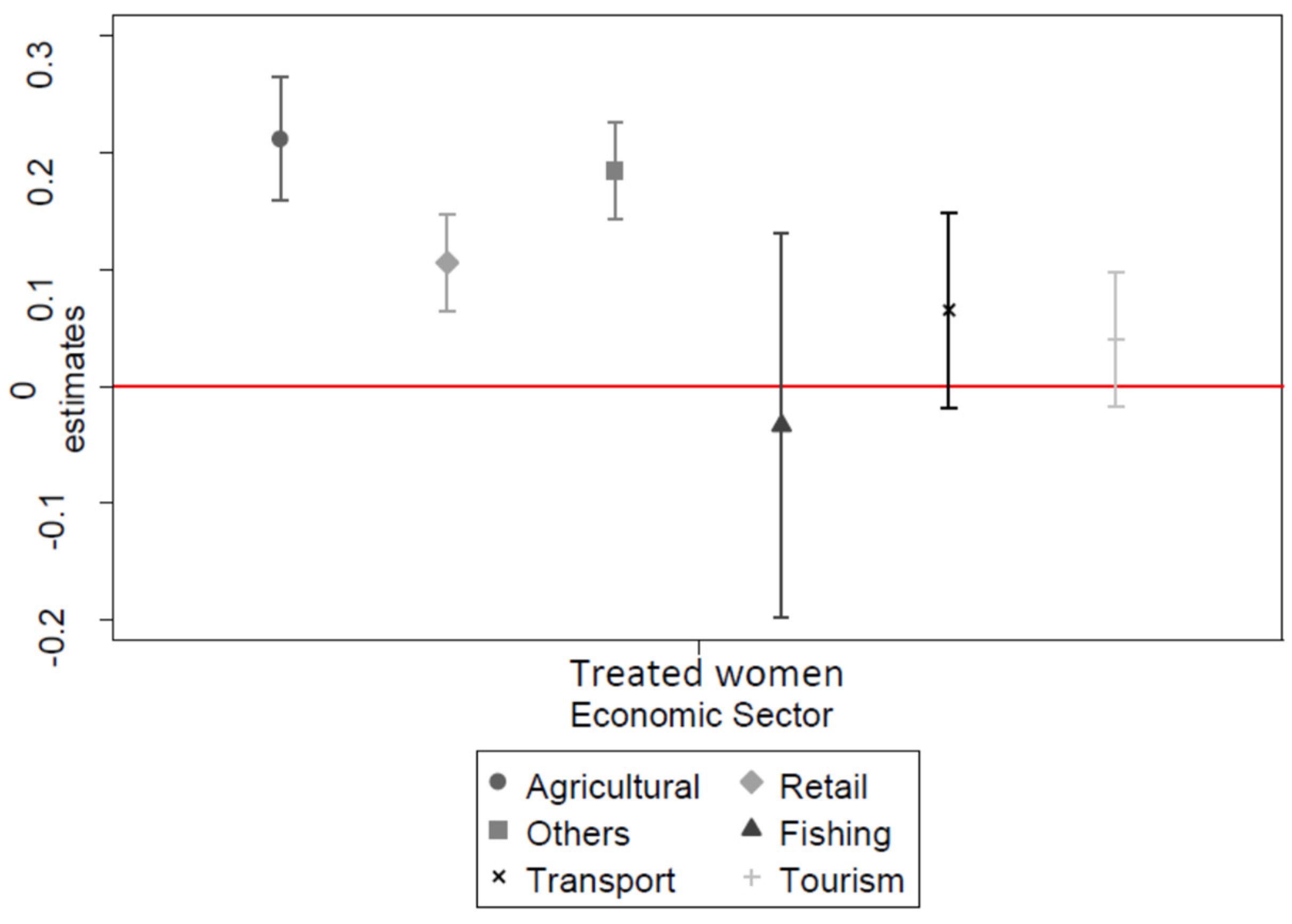

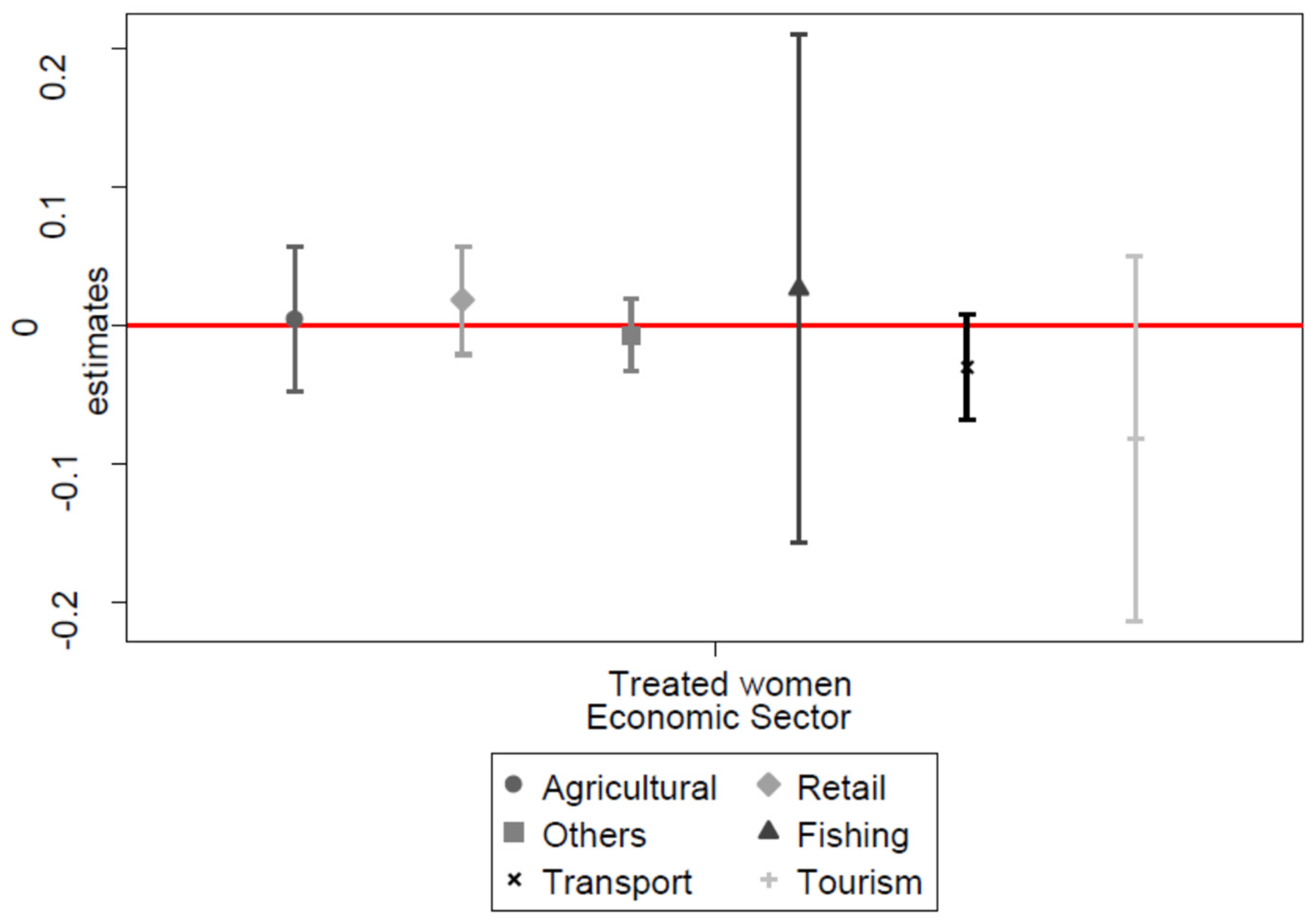

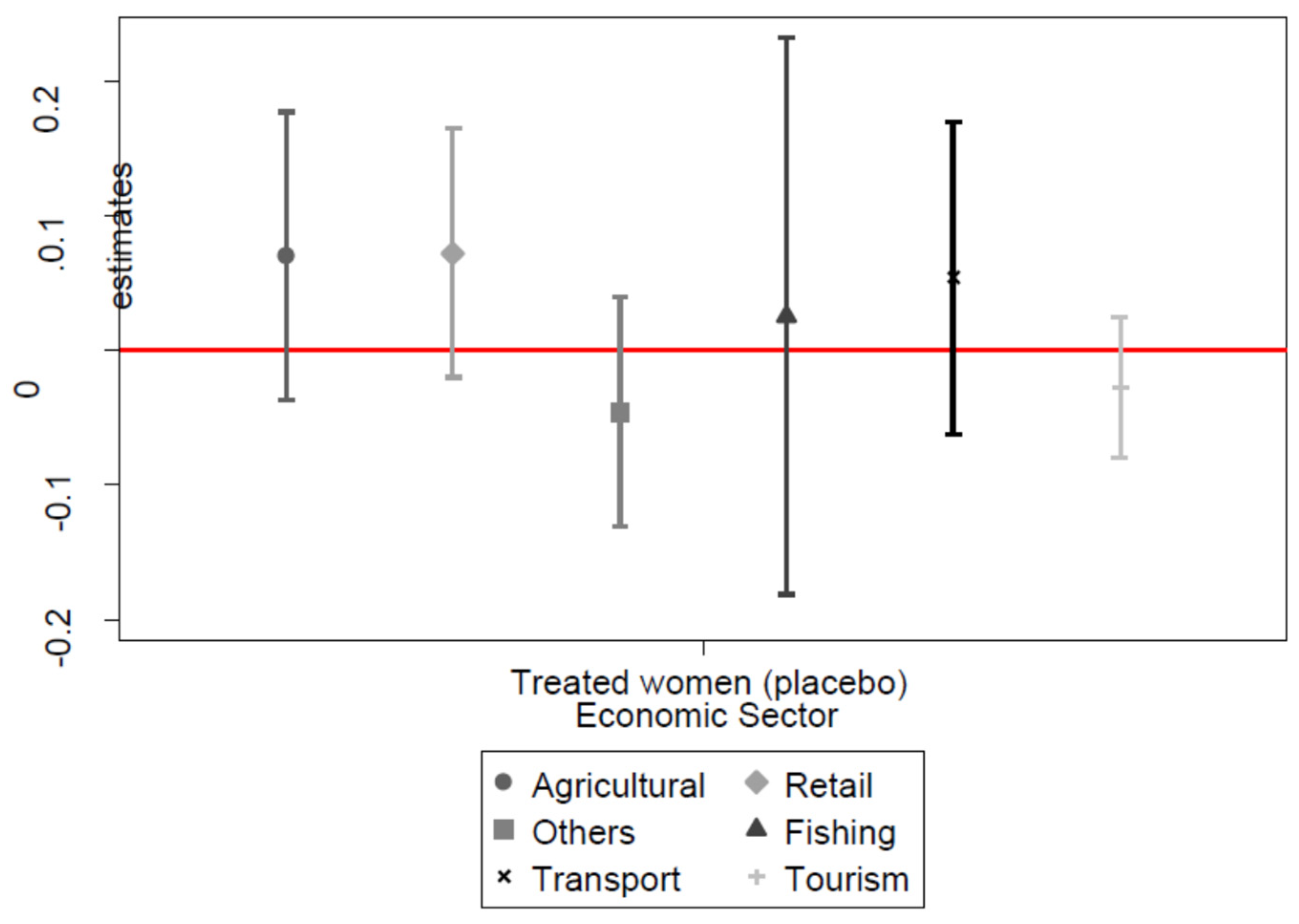

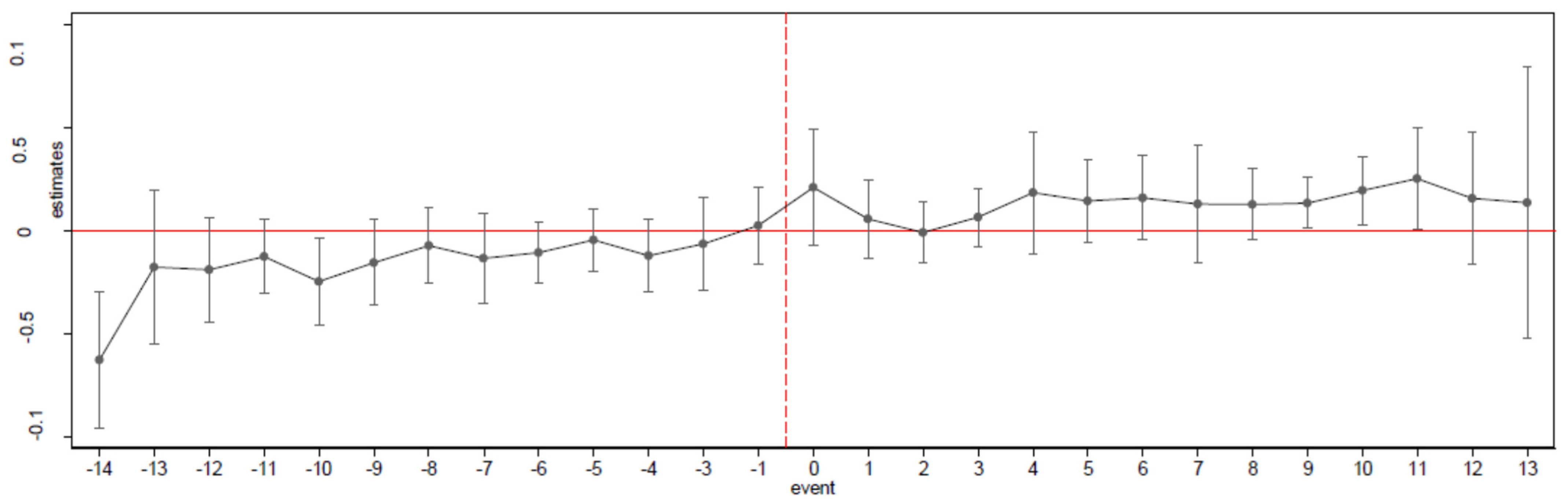

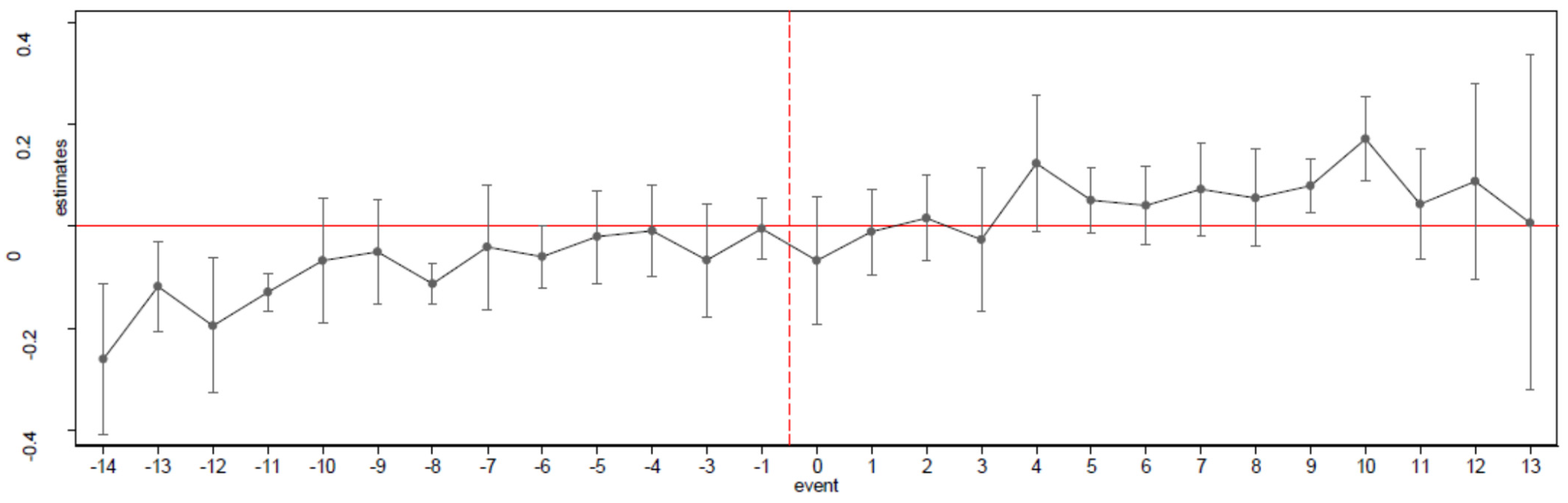

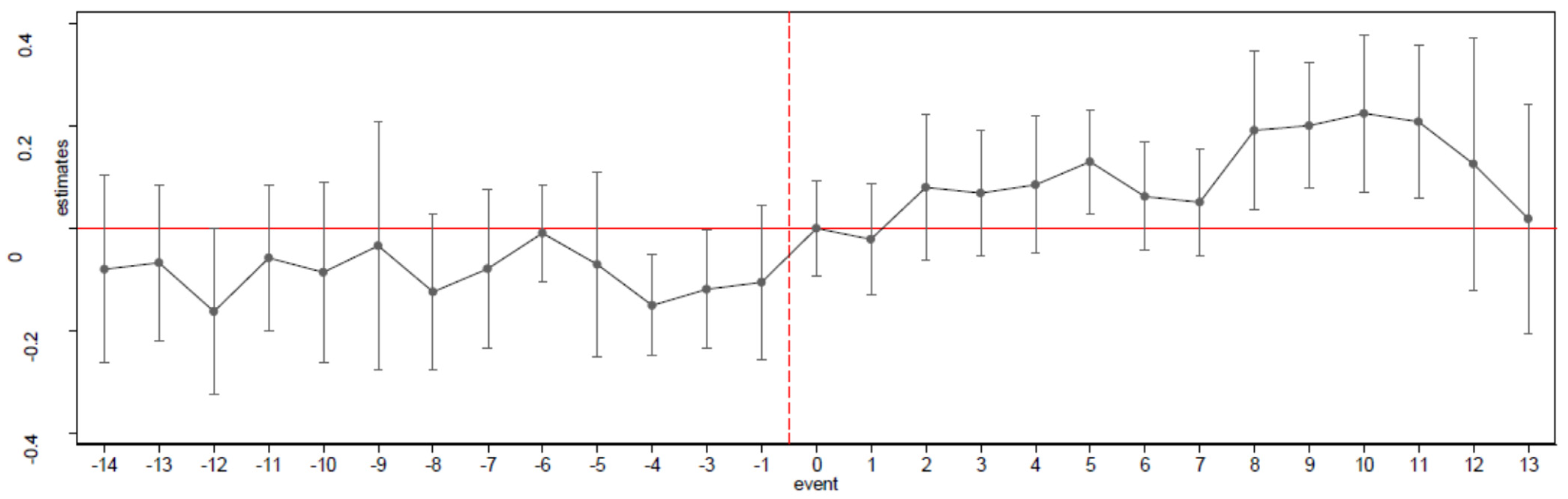

6. Annexe: Event Studies by Economic Sector

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | There is evidence of gender differences in the impact of banking services on low-income clients in Mexico (Bruhn and Love 2011). |

| 2 | Focus groups and extended interviews with customers were carried out, supporting those findings. Such evidence is consistent with Eddleston et al. (2014), whose results document that women entrepreneurs are less likely to obtain the same levels of bank financing than men. Moreover, they are consistent with the Mujeres del Pacífico (2018) collection of evidence. Banks refuse female entrepreneurs’ loan requests, arguing that their payment capacity is insufficient. |

| 3 | Langowitz and Minniti (2007) found that women perceive themselves in less favourable terms than men across the 16 countries where the Global Entrepreneurship Monitor (GEM) Project data were collected. |

| 4 | Consistent with McGowan et al. (2012). |

| 5 | From north to south of Chilean territory, those regions were: Arica y Parinacota, Tarapacá, Antofagasta, Atacama, Coquimbo, Valparaíso, Metropolitana de Santiago, Libertador General Bernardo O’Higgins, del Maule, de Ñuble, Biobío, Araucanía, Los Ríos, Los Lagos, Aysén, and Magallanes. |

| 6 | Kast and Pomeranz (2014) carried out a study in Chile that does not have the advantage of analysing a quasi-experimental national experience covering the whole country. Instead, they analyse the impact of a financial inclusion program that promotes access to saving accounts through an experiment that randomises interested people in treated and control groups. |

| 7 | The total amount lent by BEM and the average monthly loans are in Chilean pesos, considering inflation to express both in the pesos of July 2018. We use indices reported by the Central Bank of Chile. |

| 8 | Non-treated and treated periods change depending on the area. For instance, for the first area (Libertador Bernardo O’Higgins Region), the non-treated period extends from January 2012 to December 2014, while the treated period goes from January 2015 to July 2018. |

| 9 | In this case, the analysis considered branch-specific linear trends; the same graphs exposing estimates without those controls are available upon request. |

| 10 | (Sewing and clothing, shoes, handicrafts, clothing, and jewellery, among others). |

References

- Acs, Zoltan, Elena Bardasi, Saul Estrin, and Jan Svejnar. 2011. Introduction to special issue of Small Business Economics on female entrepreneurship in developed and developing economies. Small Business Economics 37: 393–96. [Google Scholar] [CrossRef]

- Adkins, Cheryl, Steven Samaras, Sally Gilfillan, and Wayne McWee. 2013. The Relationship between Owner Characteristics, Company Size, and the Work-Family Culture and Policies of Women-Owned Businesses. Journal of Small Business Management 51: 196–214. [Google Scholar] [CrossRef]

- Bardasi, Elena, Shwetlena Sabarwal, and Katherine Terrell. 2011. How Do Female Entrepreneurs Perform? Evidence from Developing Regions. Small Business Economics 37: 417–41. [Google Scholar] [CrossRef]

- Beck, Thorsten, and Asli Demirguc-Kunt. 2006. Small and Medium-size Enterprises: Access to Finance as a Growth Constraint. Journal of Banking and Finance 30: 2931–43. [Google Scholar] [CrossRef]

- Bertrand, Marianne, Esther Dufflo, and Sendhil Mullainathan. 2004. How Much Should We Trust Differences-In-Differences Estimates? The Quarterly Journal of Economics 119: 249–75. [Google Scholar] [CrossRef] [Green Version]

- Bruhn, Miriam, and Inessa Love. 2011. Gender Differences in the Impact of Banking Services: Evidence from Mexico. Small Business Economics 37: 493–12. [Google Scholar] [CrossRef]

- Carrillo, Paul, Nestor Gandelman, and Virginia Robano. 2014. Sticky Floors and Glass Ceilings in Latin America. The Journal of Economic Inequality 12: 339–61. [Google Scholar] [CrossRef]

- Coleman, Susan, Henry Colette, Barbara Orser, Lene Foss, and Friederike Welter. 2019. Policy Support for Women Entrepreneurs’ Access to Financial Capital: Evidence from Canada, Germany, Ireland, Norway, and the United States. Journal of Small Business Management 57: 296–322. [Google Scholar] [CrossRef]

- Craig, Ben, William Jackson II, and James Thomson. 2007. Small Firm Finance, Credit Rationing, and the Impact of SBA-guaranteed Lending on Local Economic Growth. Journal of Small Business Management 45: 116–32. [Google Scholar] [CrossRef]

- Cuberes, David, and Marc Teignier. 2014. Gender Inequality and Economic Growth: A Critical Review. Journal of International Development 26: 260–76. [Google Scholar] [CrossRef] [Green Version]

- Deere, Carmen, and Cheryl Doss. 2006. The Gender Asset Gap: What Do We Know and What Does it Matter? Feminist Economics 12: 1–50. [Google Scholar] [CrossRef]

- Deere, Carmen, and Magdalena Leon. 2003. The Gender Asset Gap: Land in Latin America. World Development 31: 925–47. [Google Scholar] [CrossRef]

- Del Pacífico, Mujeres. 2018. Primer Informe: Programas de Apoyo al Emprendimiento Femenino en la Alianza del Pacífico. Available online: https://home.mujeresdelpacifico.org/uploads/library/5b96f4d0a1270_1er-Informe-MdP-ASELA-OAP.pdf (accessed on 12 December 2021).

- Demirguc-Kunt, Asli, Leora Klapper, and Dorothe Singer. 2013. Financial Inclusion and Legal Discrimination against Women: Evidence from Developing Countries. Policy Research Working Paper Series 6416. Washington: The World Bank. [Google Scholar]

- Doss, Cheryl, Carmen Deere, Abena Oduro, Hema Swaminathan, Zachary Catanzarite, and J. Y. Suchitra. 2019. Gendered Paths to Asset Accumulation? Markets, Savings, and Credit in Developing Countries. Feminist Economics 25: 36–66. [Google Scholar] [CrossRef]

- Drori, Israel, Ronny Manos, Estefania Santacreu-Vasut, Oded Shenkar, and Amir Shoham. 2018. Language and Market Inclusivity for Women Entrepreneurship: The Case of Microfinance. Journal of Business Venturing 33: 395–415. [Google Scholar] [CrossRef]

- Economic Commission for Latin America and the Caribbean. 2018. Participation Rate by Sex. Available online: http://interwp.cepal.org/sisgen/ConsultaIntegrada.asp?idIndicador=120&idioma=i (accessed on 12 December 2021).

- Eddleston, Kimberly, Jamie Ladge, Cheryl Mitteness, and Lakshmi Balachandra. 2014. Do You See What I See? Signalling Effects of Gender and Firm Characteristics of Financing Entrepreneurial Ventures. Entrepreneurship Theory and Practice 40: 489–514. [Google Scholar] [CrossRef]

- Elborgh-Woytek, Katrin, Monique Newiak, Kalpana Kochhar, Stefania Fabrizio, Kangni Kpodar, Philippe Wingender, Benedict Clements, and Gerd Schwartz. 2013. Women, Work, and the Economy: Macroeconomic Gains from Gender Equity. IMF Staff Discussion Note. SDN/13/10. Available online: https://www.imf.org/external/pubs/ft/sdn/2013/sdn1310.pdf (accessed on 12 December 2021).

- Escobar, Bernardita. 2015. Female entrepreneurship and participation rates in 19th century Chile. Estudios de Economía 42: 67–91. [Google Scholar] [CrossRef]

- Escobar, Bernardita. 2016. Women in Business in Late Nineteenth-Century Chile: Class, Marital Status, and Economic Autonomy. Feminist Economics 23: 33–67. [Google Scholar] [CrossRef]

- Foss, Lene, Colette Henry, Helene Ahl, and Geir Mikalsen. 2018. Women’s Entrepreneurship Policy Research: A 30-year Review of Evidence. Small Business Economics 53: 409–29. [Google Scholar] [CrossRef] [Green Version]

- Fossen, Frank. 2012. Gender Differences in Entrepreneurial Choice and Risk Aversion—A Decomposition Based on Microeconometric Model. Applied Economics 44: 1795–812. [Google Scholar] [CrossRef] [Green Version]

- Friedmann, Enav, and Oded Lowengart. 2016. The Effect of Gender Differences on the Choice of Banking Services. Journal of Service Science and Management 9: 361–77. [Google Scholar] [CrossRef] [Green Version]

- Global Entrepreneurship Monitor. 2013. Reporte Nacional de Chile 2013. Santiago de Chile: GEM, Available online: https://negocios.udd.cl/gemchile/files/2014/10/Reporte-GEM-Chile-2013-web.pdf (accessed on 12 October 2021).

- Global Entrepreneurship Monitor. 2019. Reporte Nacional de Chile 2019. Santiago de Chile: GEM, Available online: https://negocios.udd.cl/gemchile/files/2020/07/GEM-Nacional-de-Chile-2019baja-1.pdf (accessed on 12 October 2021).

- Johan, Sofia, and Patricio Valenzuela. 2020. Business Advisory Services and Female Employment in an Extreme Institutional Context. British Journal of Management 32: 1082–96. [Google Scholar] [CrossRef]

- Kast, Felipe, and Dina Pomeranz. 2014. Saving More to Borrow Less: Experimental Evidence from Access to Formal Savings Accounts in Chile. NBER Working Papers 20239. Cambridge: NBER Inc. [Google Scholar]

- Langowitz, Nan, and Maria Minniti. 2007. The Entrepreneurial Propensity of Women. Entrepreneurship Theory and Practice 31: 323–39. [Google Scholar] [CrossRef]

- Leitch, Claire, Friederike Welter, and Colette Henry. 2018. Women Entrepreneurs’ Financing Revisited: Taking Stock and Looking Forward. Venture Capital 20: 103–14. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, and Olivia Mitchell. 2008. Planning and Financial Literacy: How Do Women Fare? American Economic Review 98: 413–17. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, and Olivia Mitchell. 2014. The Economic Importance of Financial Literacy: Theory and Evidence. Journal of Economic Literature 52: 5–44. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Malapit, Hazel Jane. 2012. Are Women More Likely to be Credit Constrained? Evidence from Low-Income Urban Households in the Philippines. Feminist Economics 18: 81–108. [Google Scholar] [CrossRef] [Green Version]

- Marlow, Susan, and Janine Swail. 2014. Gender, risk and finance: Why can’t a woman be more like a man? Entrepreneurship & Regional Development 26: 80–96. [Google Scholar]

- Mazzarol, Tim. 2014. Growing and Sustaining Entrepreneurial Ecosystems: What They are and the Role of Government Policy. SEAANZ White Paper. Melbourne: SEAANZ, Available online: https://smallbusiness.report/Resources/Whitepapers/28ea2090-9f50-4220-a098-a9435a2dbe20_iicie.pdf (accessed on 12 October 2021).

- McGowan, Pauric, Carol Lewis Redeker, Sarah Cooper, and KKate Greenan. 2012. Female Entrepreneurship and the Management of Business and Domestic Roles: Motivations, Expectations and Realities. Entrepreneurship and Regional Development 24: 53–72. [Google Scholar] [CrossRef] [Green Version]

- OECD. 2012. Closing the Gender Gap. Act Now. Paris: OECD Publishing. [Google Scholar]

- OECD. 2015a. The Missing Entrepreneurs 2015: Policies for Self-Employment and Entrepreneurship. Paris: OECD Publishing. [Google Scholar]

- OECD. 2015b. Entrepreneurship at a Glance 2015. Paris: OECD Publishing. [Google Scholar]

- OECD. 2016. OECD Employment Outlook 2016. Paris: OECD Publishing. [Google Scholar]

- OECD. 2018. Participation Rate by Sex. Available online: https://stats.oecd.org/ (accessed on 12 October 2021).

- Parker, Simon. 2005. The Economics of Entrepreneurship: What We Know and What We Don’t. Foundations and Trends in Entrepreneurship 1: 1–54. [Google Scholar] [CrossRef]

- Rodríguez, Paola, Mar Fuentes-Fuentes, and Lazaro Rodríguez. 2013. Strategic Capabilities and Performance in Women-Owned Businesses in Mexico. Journal of Small Business Management 52: 541–54. [Google Scholar] [CrossRef]

- Roodman, David, James MacKinnon, Morten Orregard, and Matthew Webb. 2018. Fast and Wild: Bootstrap Inference in Stata Using Boottest. Wording Papers 1406. Kingston: Department of Economics, Queen’s University. [Google Scholar]

- Sabarwal, Swetlena, and Katherine Terrell. 2009. Access to Credit and Performance of Female Entrepreneurs in Latin America (Summary). Frontiers of Entrepreneurship Research 29: 6. [Google Scholar]

- Superintendencia de Bancos e Instituciones Financieras. 2014. Género en el Sistema Financiero. Santiago de Chile: Superintendencia de Bancos e Instituciones Financieras Publishing. [Google Scholar]

- Terjesen, Siri, and Ainsley Lloyd. 2014. The 2015 Female Entrepreneurship Index. Analysing the Conditions that Foster High-Potential Female Entrepreneurship in 22 Countries. Washington: The Global Entrepreneurship and Development Institute. [Google Scholar]

- Thébaud, Sarah. 2015. Business as Plan B: Institutional Foundations of Gender Inequality in Entrepreneurship across 24 Industrialised Countries. Administrative Science Quarterly 60: 671–711. [Google Scholar] [CrossRef]

- Verheul, Ingrid, and Roy Thurik. 2001. Start-Up Capital: ‘Does Gender Matter? ’ Small Business Economics 16: 329–46. [Google Scholar] [CrossRef]

- World Bank. 2011. Gender Equality and Development, World Development Report 2012. Washington: The International Bank for Reconstruction and Development. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Month | Region |

|---|---|

| January 2015 | Libertador Bernardo O’Higgins (Red) |

| March 2015 | Magallanes y la Antártica Chilena, Aysén del General Carlos Ibáñez del Campo y Región de los Lagos (Green) |

| April 2015 | Los Ríos y Araucanía (Yellow) |

| May 2015 | Bio Bio y Maule (Orange) |

| June 2015 | Valparaíso y Coquimbo (Purple) |

| July 2015 | Antofagasta, Tarapacá, y Arica y Parinacota (Apple green) |

| September 2015 | Atacama y Metropolitana (White) |

| Source: BancoEstado Microempresas | |

| January 2012 | July 2018 | |||||||

|---|---|---|---|---|---|---|---|---|

| Area | Branches | Loans Granted | The Total Amount of Money Lent /1 | Average Amount Lent by Loan /2 | Branches | Loans Granted | The Total Amount of Money Lent /1 | Average Amount Lent by Loan /2 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| 1 | 10 | 333 | 1514 | 4,665,885 | 17 | 479 | 2563 | 5,042,594 |

| 2 | 19 | 648 | 2270 | 3,420,075 | 27 | 883 | 3171 | 3,535,649 |

| 3 | 27 | 881 | 2602 | 3,433,318 | 39 | 1231 | 3963 | 3,756,844 |

| 4 | 38 | 1177 | 4185 | 3,321,303 | 57 | 1895 | 7765 | 3,915,905 |

| 5 | 23 | 880 | 3148 | 3,534,383 | 43 | 1449 | 5376 | 4,064,795 |

| 6 | 11 | 465 | 1950 | 3,799,510 | 15 | 552 | 2172 | 3,700,371 |

| 7 | 62 | 1975 | 7376 | 3,761,649 | 71 | 3234 | 12,212 | 4,244,989 |

| 190 | 6359 | 23,046 | 3,705,160 | 269 | 9723 | 37,222 | 4,037,307 | |

| Summary Statistics | |||

|---|---|---|---|

| Non-Treated | Treated | /2 | |

| Panel A: National | |||

| Total amount lent monthly at branch level /1 | CLP 24.0 | CLP 25.4 | *** |

| Average amount lent by loan at branch level /1 | CLP 4.1 | CLP 4.2 | *** |

| n | 53,078 | 61,387 | |

| Panel A: National—Men | |||

| Total amount lent monthly at branch level /1 | CLP 30.0 | CLP 30.8 | *** |

| Average amount lent by loan at branch level /1 | CLP 4.4 | CLP 4.6 | *** |

| n | 28,542 | 32,452 | |

| Panel A: National—Women | |||

| Total amount lent monthly at branch level /1 | CLP 17.0 | CLP 19.4 | *** |

| Average amount lent by loan at branch level /1 | CLP 3.7 | CLP 3.8 | *** |

| n | 24,536 | 28,935 | |

| T (months) | 36 | 43 | |

| Loans Granted | Average Loan | |||

|---|---|---|---|---|

| Area 1 | 0.175 *** | 0.121 | −0.063 | 0.211 |

| (0.036) | (0.119) | (0.037) | (0.127) | |

| Area 2 | 0.132 *** | −0.057 | −0.005 | 0.016 |

| (0.025) | (0.081) | (0.027) | (0.078) | |

| Area 3 | 0.126 *** | 0.137 * | 0.021 | 0.138 |

| (0.022) | (0.067) | (0.025) | (0.076) | |

| Area 4 | 0.092 *** | 0.252 *** | 0.004 | 0.249 *** |

| (0.019) | (0.059) | (0.021) | (0.062) | |

| Area 5 | 0.203 *** | 0.225 ** | 0.007 | 0.222 ** |

| (0.022) | (0.070) | (0.023) | (0.074) | |

| Area 6 | 0.077 * | 0.122 | −0.030 | 0.073 |

| (0.035) | (0.111) | (0.033) | (0.100) | |

| Area 7 | 0.123 *** | 0.227 *** | 0.004 | 0.246 *** |

| (0.016) | (0.053) | (0.015) | (0.051) | |

| Loans Granted | Average Loan | |||

|---|---|---|---|---|

| Specification (1) | Specification (2) | Specification (1) | Specification (2) | |

| 0.127 *** | 0.126 *** | −0.016 | −0.015 | |

| (0.016) | (0.016) | (0.120) | (0.149) | |

| −0.027 | −0.036 | −0.008 | −0.005 | |

| (0.023) | (0.023) | (0.545) | (0.571) | |

| −0.365 *** | −0.365 *** | −0.285 *** | −0.286 *** | |

| (0.030) | (0.029) | (0.003) | (0.005) | |

| Branch-specific linear trends | X | X | ||

| N | 114,465 | 114,465 | 114,465 | 114,465 |

| R2 | 0.359 | 0.365 | 0.217 | 0.224 |

| Loans Granted | ||

|---|---|---|

| Specification (1) | Specification (2) | |

| 0.028 | 0.025 | |

| (0.023) | (0.024) | |

| −0.052 | −0.018 | |

| (0.028) | (0.020) | |

| −0.376 *** | −0.376 *** | |

| (0.029) | (0.029) | |

| Branch-specific linear trends | X | |

| n | 46,449 | 46,449 |

| R2 | 0.399 | 0.365 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bentancor, A. Women’s Entrepreneurship and Government Policy: Facilitating Access to Credit through a National Program in Chile. Soc. Sci. 2022, 11, 14. https://doi.org/10.3390/socsci11010014

Bentancor A. Women’s Entrepreneurship and Government Policy: Facilitating Access to Credit through a National Program in Chile. Social Sciences. 2022; 11(1):14. https://doi.org/10.3390/socsci11010014

Chicago/Turabian StyleBentancor, Andrea. 2022. "Women’s Entrepreneurship and Government Policy: Facilitating Access to Credit through a National Program in Chile" Social Sciences 11, no. 1: 14. https://doi.org/10.3390/socsci11010014

APA StyleBentancor, A. (2022). Women’s Entrepreneurship and Government Policy: Facilitating Access to Credit through a National Program in Chile. Social Sciences, 11(1), 14. https://doi.org/10.3390/socsci11010014