1. Introduction

Let

be a one-dimensional standard Brownian motion starting at zero for

, and let

be a Poisson process with rate

. The three stochastic processes are assumed to be independent. We define

where

are independent random variables that are distributed as the continuous random variable

Z with the probability density function

and are independent of the Poisson process. The functions

,

and

,

, are such that

is a two-dimensional jump-diffusion process.

If

and

is a non-negative or non-positive deterministic function, then

could serve as a model for the wear or the remaining lifetime, respectively, of a device. The model would be a generalization of the one proposed by Rishel [

1] and considered by Lefebvre in various papers (see, for instance, [

2]).

Suppose that

, and let

be the

first-exit time defined by

Generalizing the results in [

3,

4] (see also [

5]), we can state that the moment-generating function

of

, where

, satisfies the partial differential–integral equation (PDIE)

In this paper, we assume that

Z has an exponential distribution with parameter

. It follows that Equation (

5) becomes

Since the jumps are positive, the boundary conditions are

if

or

.

Similarly, the mean

of

satisfies the PDIE

and is such that

if

or

.

Finally, let

This function, which is the probability of first exit at

, is a solution of the PDIE

The boundary conditions are

if

and

if

.

In one dimension, and when there are no jumps, obtaining exact analytical expressions for the functions corresponding to

,

, and

is generally rather straightforward. When jumps are added to the model, the problem becomes much more difficult. Papers on problems of this type have been written by Abundo (see [

6,

7,

8,

9]). In [

8], the first-passage area of one-dimensional jump-diffusion processes was computed. In addition to his papers on jump-diffusion processes, Lefebvre has also considered stochastic control problems for these processes. Jump-diffusion processes are especially important in financial mathematics; see the seminal paper by Merton [

10], as well as [

11]. Other papers on this subject are those by Cai [

12], Peng and Liu [

13], Yin et al. [

14], Zhou and Wu [

15], Gapeev and Stoev [

16], Herrmann and Zucca [

17], Song [

18], and Ai et al. [

19].

In the next section, we will compute the function

explicitly and exactly in three particular cases. First, taking advantage of the symmetry in the problems considered, we will make use of the method of similarity solutions to reduce Equation (

9) to an integro-differential equation (IDE). Then, we will transform the IDE into an ordinary differential equation (ODE) of the third order. In

Section 3, the problem of computing the mean

and the moment-generating function

of

will be studied. We will end this paper with a few remarks in

Section 4.

2. Computation of the Probability

Case I. The first particular case that we consider is the following:

where

c,

, and

are positive constants. Then,

is an Ornstein–Uhlenbeck process with Poissonian jumps. Moreover, if we let

decrease to zero, then

is an integrated Ornstein–Uhlenbeck process, which is multiplied by the constant

c.

Now, based on the definition of the first-exit time

, we will look for a solution of the form

where

. This is an application of the method of similarity solutions to solve partial differential equations, and

u is the similarity variable. For the method to work, we must be able to express (after simplification) all elements of Equation (

12) in terms of

u, as well as the boundary conditions. Here, the boundary conditions reduce to

Furthermore, Equation (

12) can be rewritten as follows:

Next, differentiating the above equation with respect to

u, we deduce from the Leibniz integral rule that

Moreover, from Equation (

15), we have

Substituting this expression into Equation (

16), we find that

Notice that this is a second-order linear ODE with constant coefficients for

. Its general solution is

where

is an arbitrary constant for

, and

For the sake of simplicity, let us take

,

, and

. Then,

The unique solution of Equation (

18) that satisfies the conditions

,

, and

is given by

where

If we substitute the above function into Equation (

15), we find that this equation is satisfied if we take

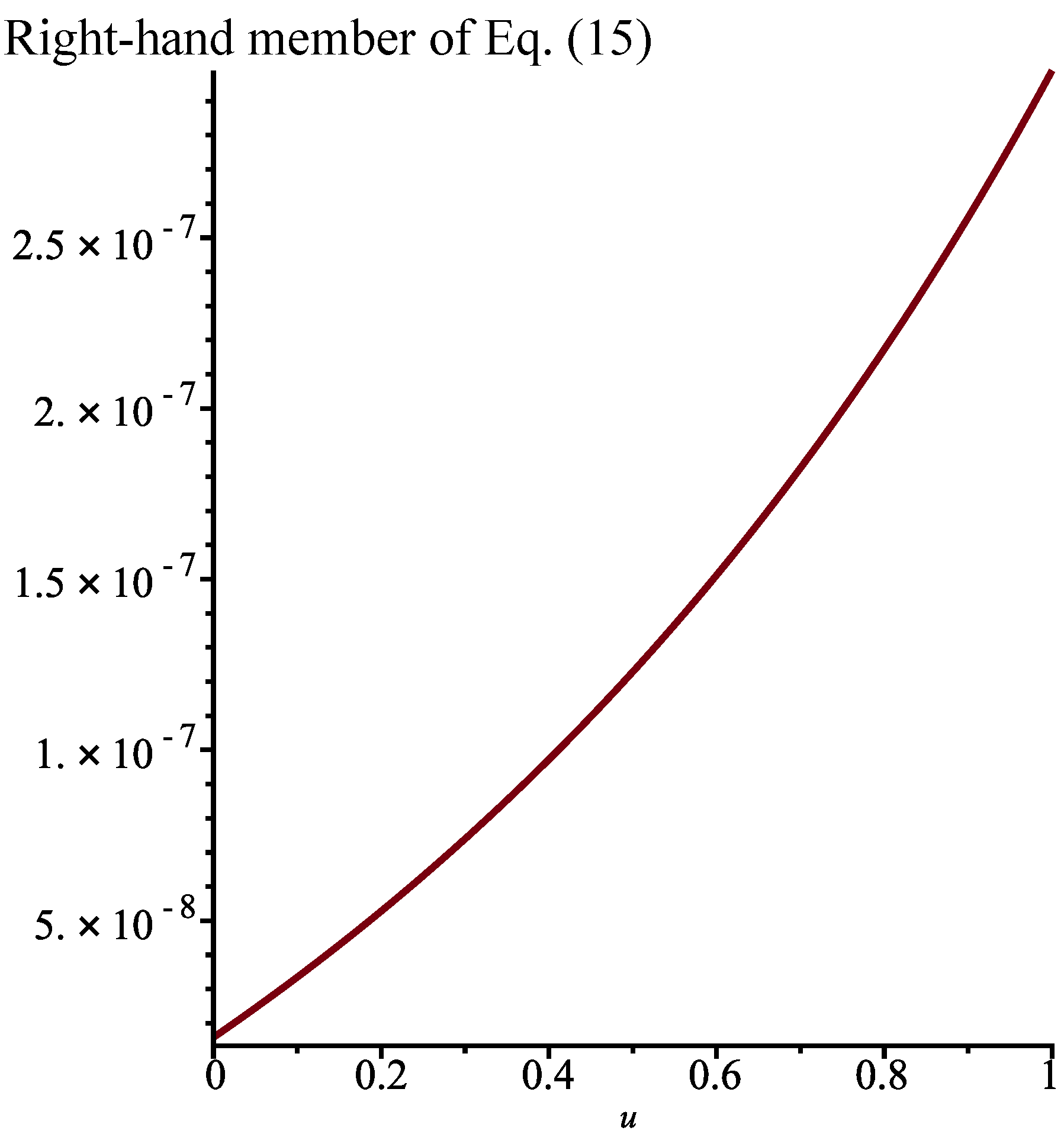

. Indeed, as can be seen in

Figure 1, the right-hand member of Equation (

15) is then practically equal to 0.

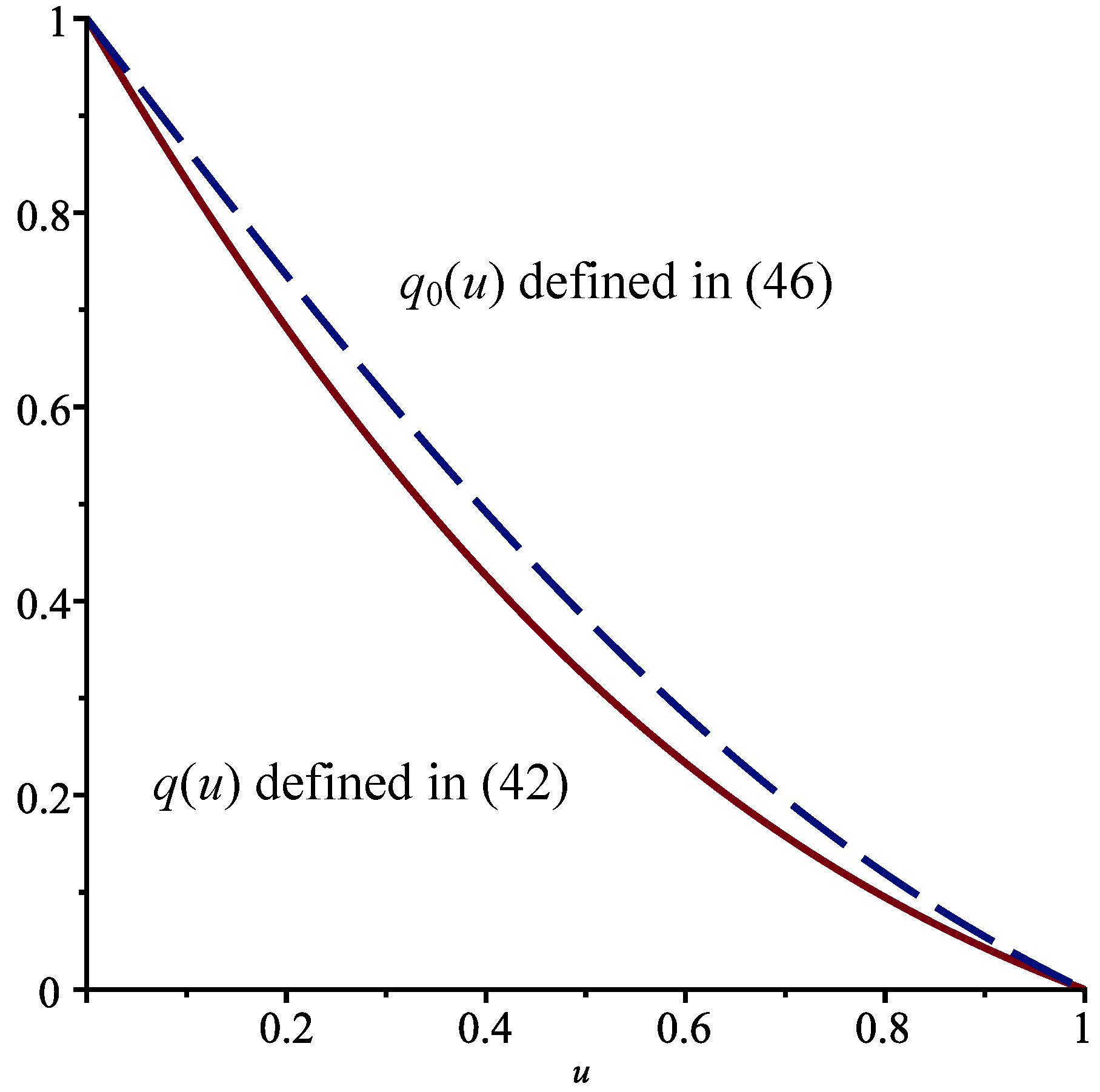

Proposition 1. When , , and , the probability is given by , where is defined in Equation (22) and . We havefor . Remark 1. We can calculate the function for any admissible values of the parameters γ, σ, λ, and θ, as well as for any constants and . However, the general solution is rather cumbersome. Moreover, to determine the value of the constant r, it is almost mandatory to choose particular values for all the quantities mentioned above.

When

so that there are no jumps, the function

that corresponds to

can be written as

, where

satisfies the elementary ODE

The solution that satisfies the boundary conditions

and

is

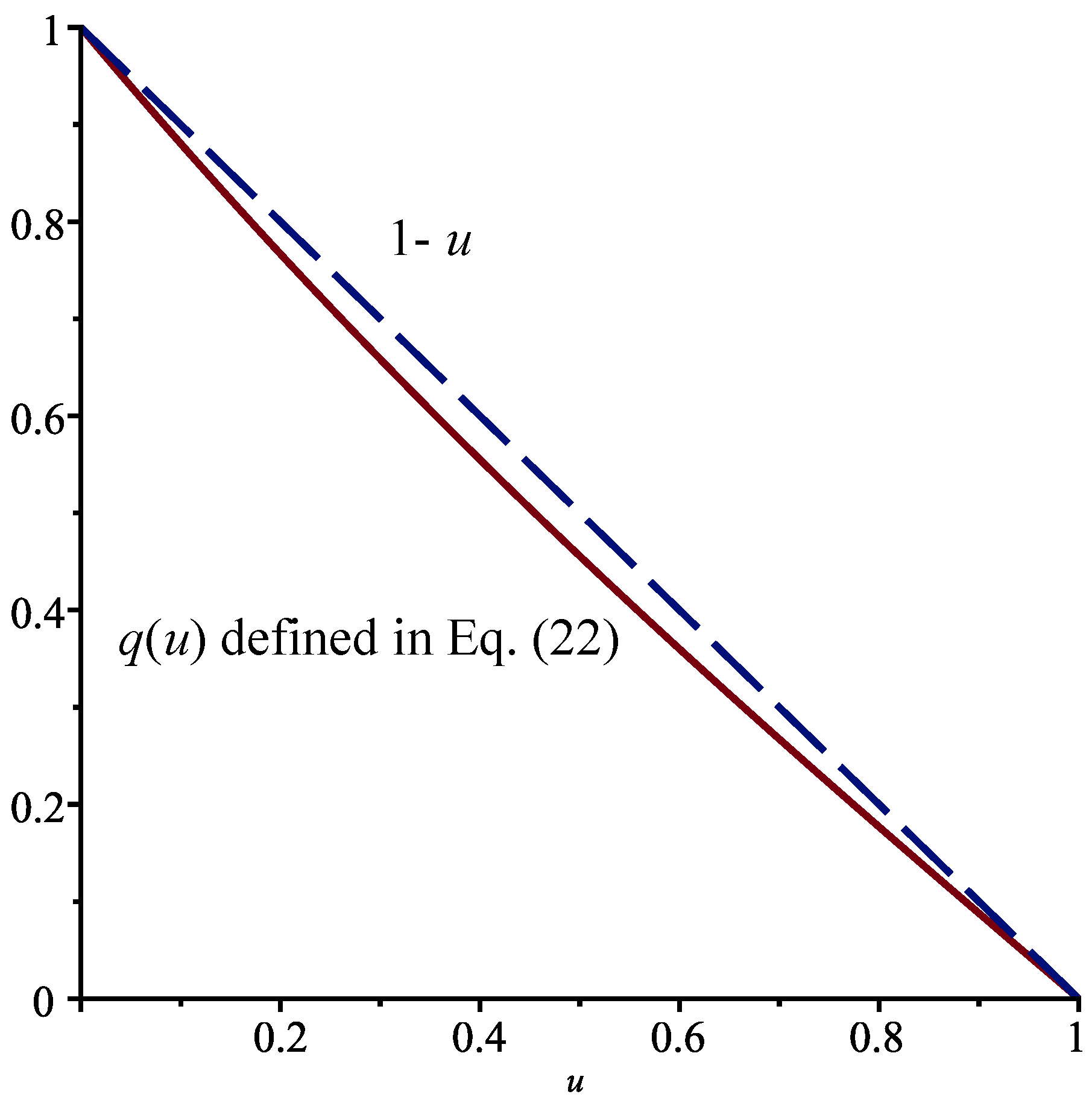

. In

Figure 2, the functions

and

are shown in the interval

. Notice the effect of the jumps on the probability of absorption at

. The effect would be more pronounced if we increased the value of the parameter

and/or decreased

.

Case II. Next, we consider the case when

where

. This time,

is a jump-diffusion process whose continuous part is a geometric Brownian motion, which is used extensively in financial mathematics.

We need to solve the following PDIE (see (

9)):

As in Case I, we set

, where

. The boundary conditions are the same as those in Equation (

14), and the PDIE becomes the IDE

Proceeding as above, we find that Equation (

29) is transformed into

which is again a second-order linear ODE for

but with non-constant coefficients. When

, the general solution of (

30) can be written as follows:

where

is an

exponential integral. The function

is defined by

We take

and

. The solution for

,

, and

is

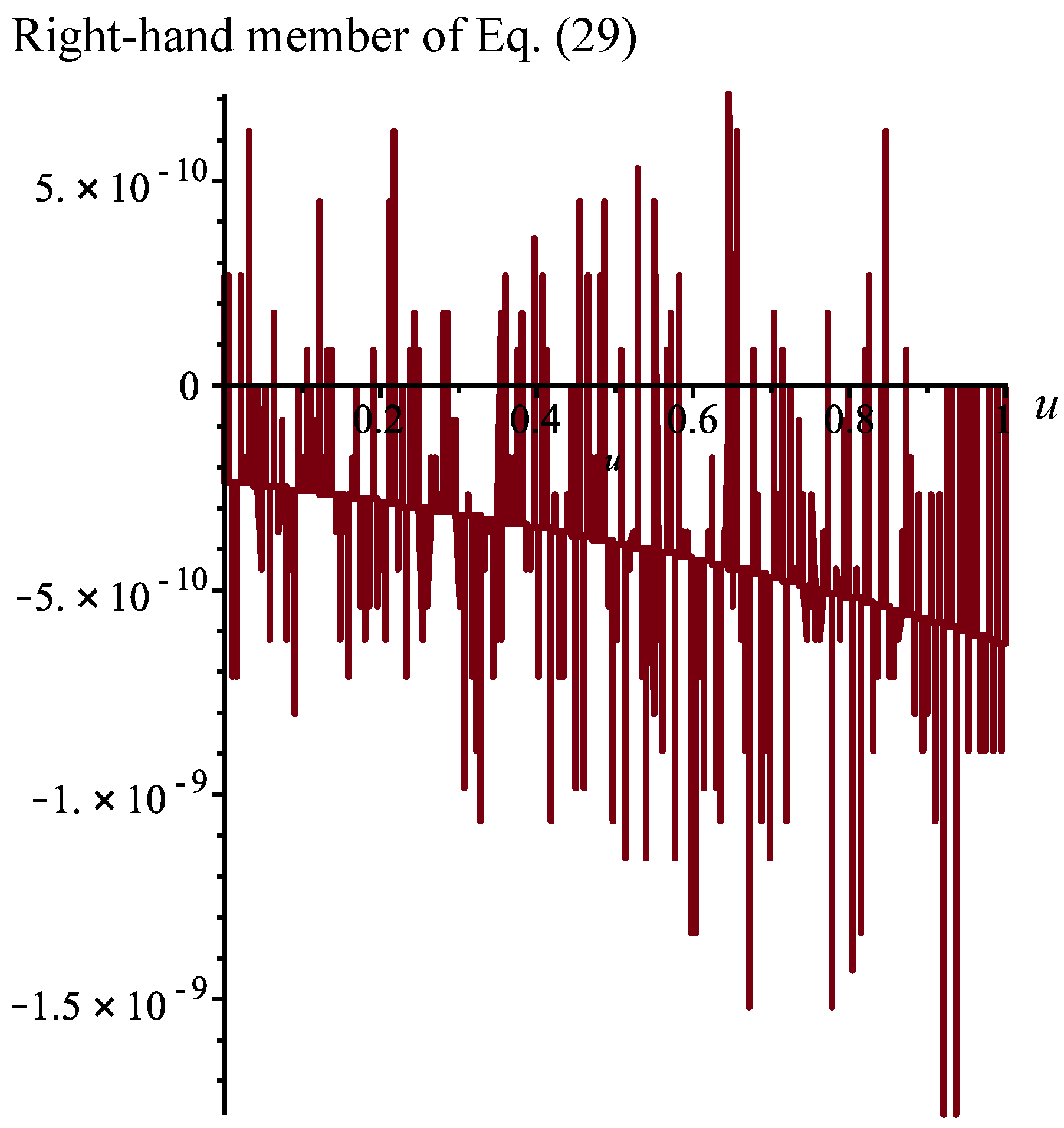

In order for the function defined in Equation (

33) to satisfy the PDIE (

29), we must take

. In

Figure 3, we present the value of the right-hand member of Equation (

29) that we obtain with the function

.

We can state the following proposition.

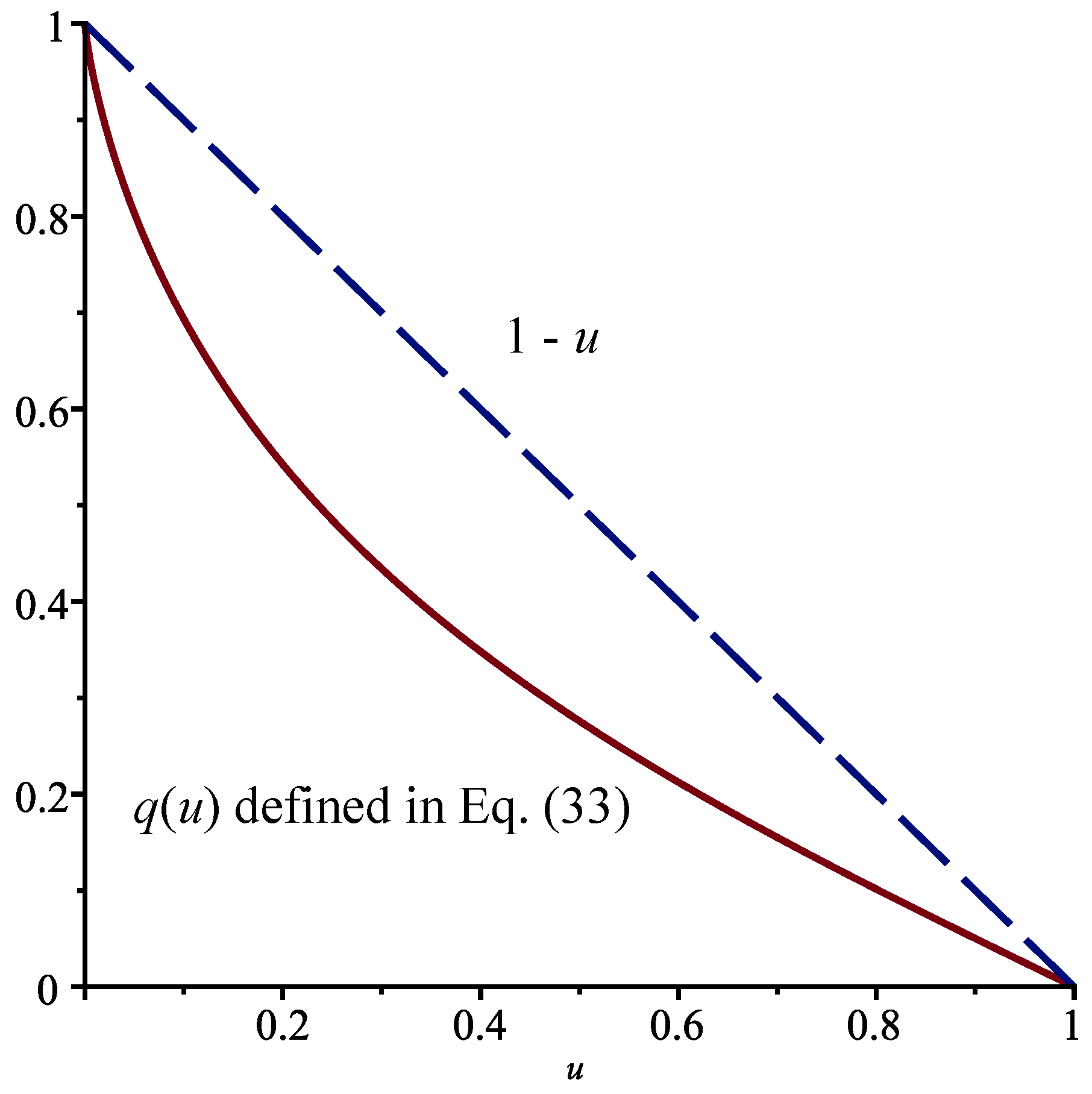

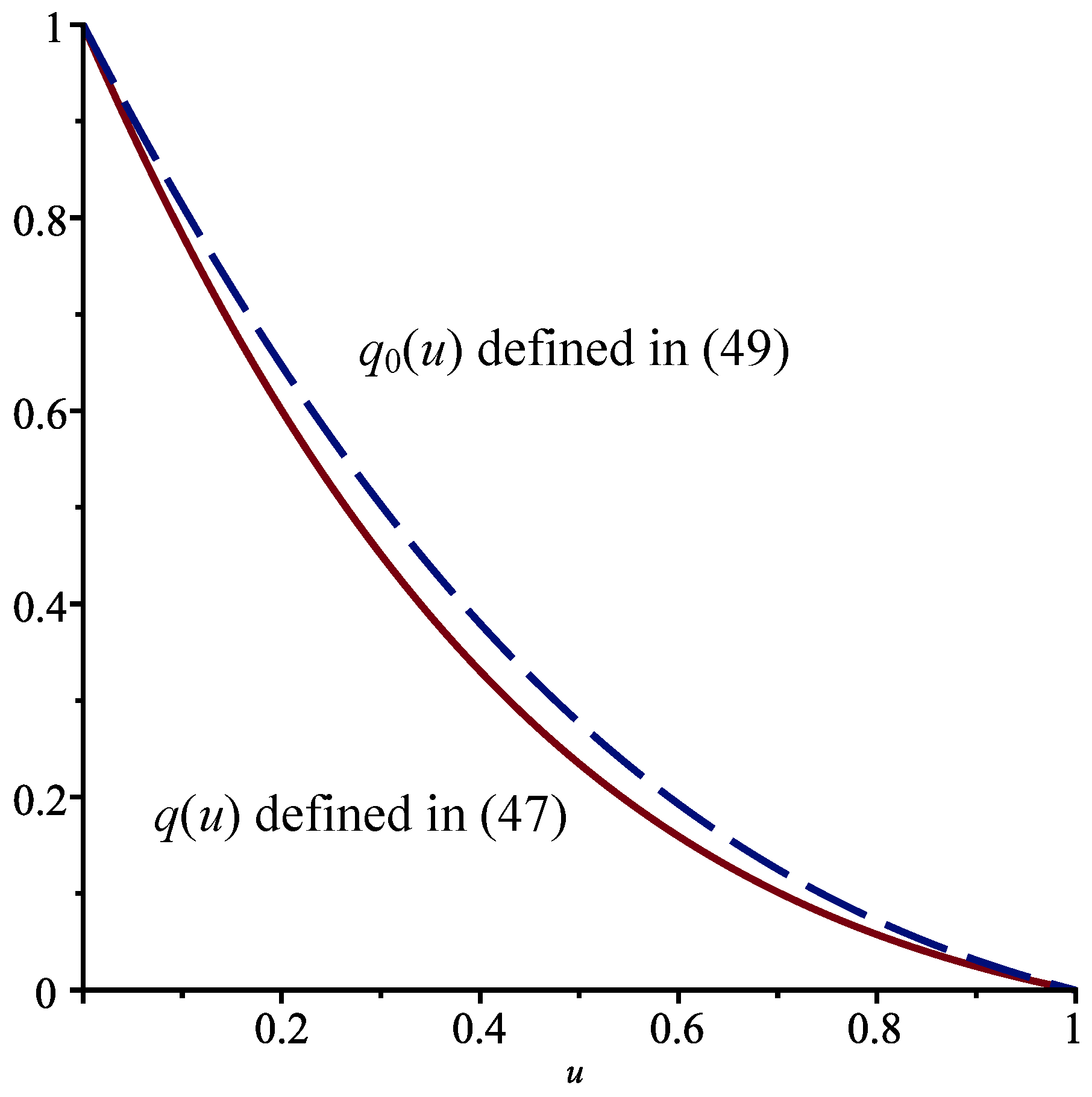

Proposition 2. When , , and , the function is equal to , where is defined in Equation (33) and . We computefor . When there are no jumps, the function

is equal to

, as in Case I, so that

. The functions

and

are displayed in

Figure 4 for

. The effect of the jumps is more pronounced than in Case I.

Case III. Finally, we define

The continuous part of the process

is a Wiener process (or Brownian motion) with drift

and dispersion parameter

, which is the basic diffusion process. Note that there is a single Brownian motion in the above system so that

is a degenerate two-dimensional jump-diffusion process. Moreover, as mentioned in Case I, this type of process is important in reliability theory to model the wear or remaining lifetime of devices.

We deduce from Equation (

9) that the function

satisfies the PDIE

Assuming that

, with

, the above equation reduces to

As in the previous cases, the boundary conditions are those in Equation (

14).

With

, we obtain the ODE

The general solution of this ODE is

where

is the

error function, which is defined by

When

,

, and

, we find that the solution such that

,

, and

is

where

Proceeding as in the previous cases, we find that if

, then the above function satisfies the PDIE in (

38). The right-hand member of Equation (

38) obtained with this function is shown in

Figure 5.

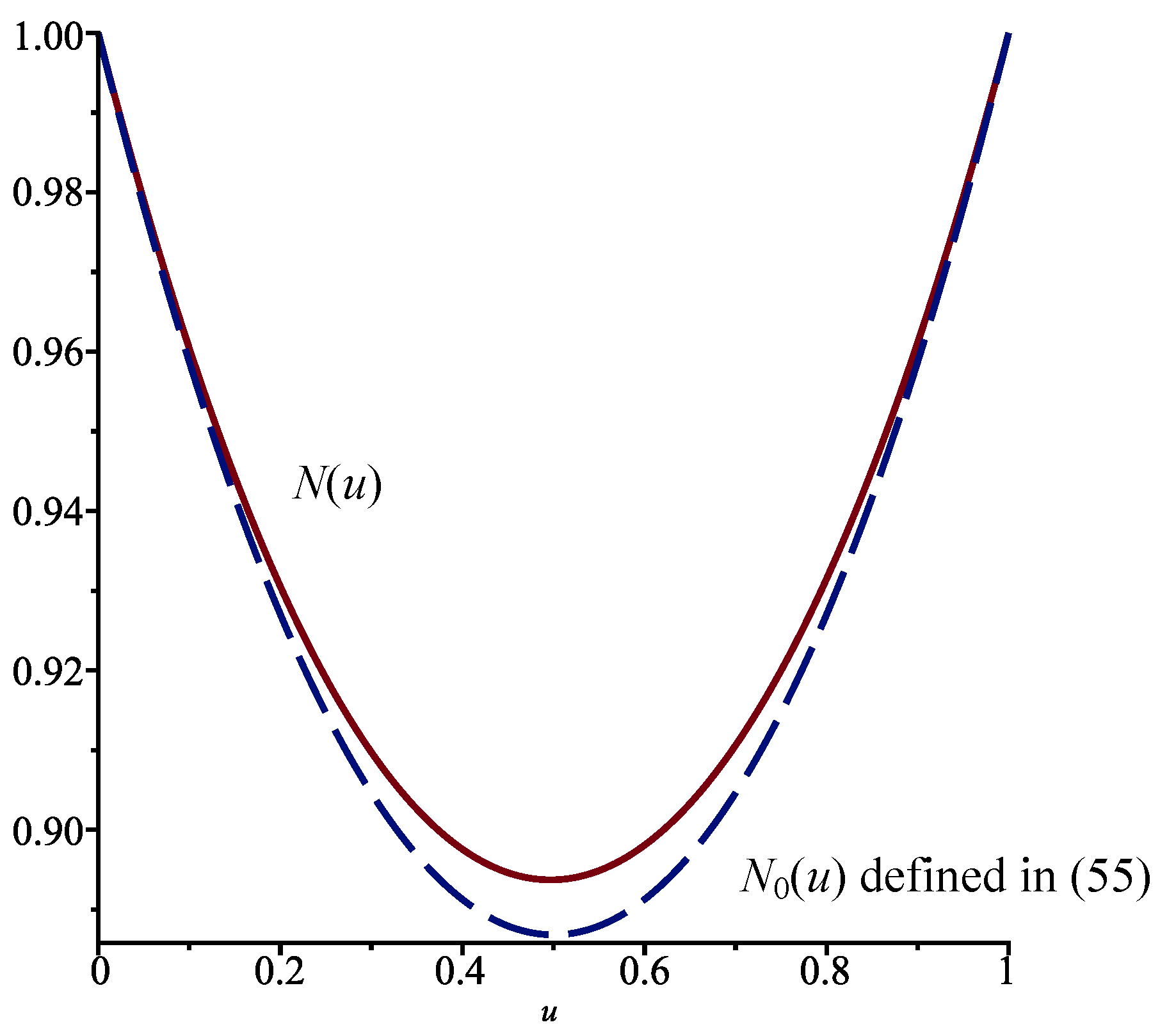

Proposition 3. When , , , and , we have , where is defined in Equation (42) with . We can write thatfor . Without the jumps, we consider the function

, which satisfies the ODE

Making use of the boundary conditions

and

, we find that

See

Figure 6.

Finally, with

, we obtain that

and

The function

is the unique solution of the ODE

such that

and

. We have

The functions

and

are presented in

Figure 7.

3. Computation of the Mean and the Moment-Generating Function

In this section, we will first compute the functions

and

for the process considered in Case I of

Section 2. Because the coefficients of the equations that we need to solve are constants, the task is much easier than when these coefficients depend on

, as in Cases II and III. We will also obtain the function

in Case II.

First, the PDIE satisfied by the function

in Case I is (see Equation (

6))

subject to the boundary conditions

if

or

.

We look for a solution of the form

, with

. This leads to the following equation:

Differentiating the above equation with respect to

u, we obtain (after some work) that

satisfies the linear third-order ODE

Let us take

so that

We can find the general solution of the above equation. We choose

and

, and we seek the unique solution for which

and

. Proceeding as in

Section 2, we are able to find the value of the constant

r. The resulting expression for the function

is rather long and will not be reproduced here.

With

, the function

that corresponds to

is a solution of the simple ODE

The unique solution such that

is

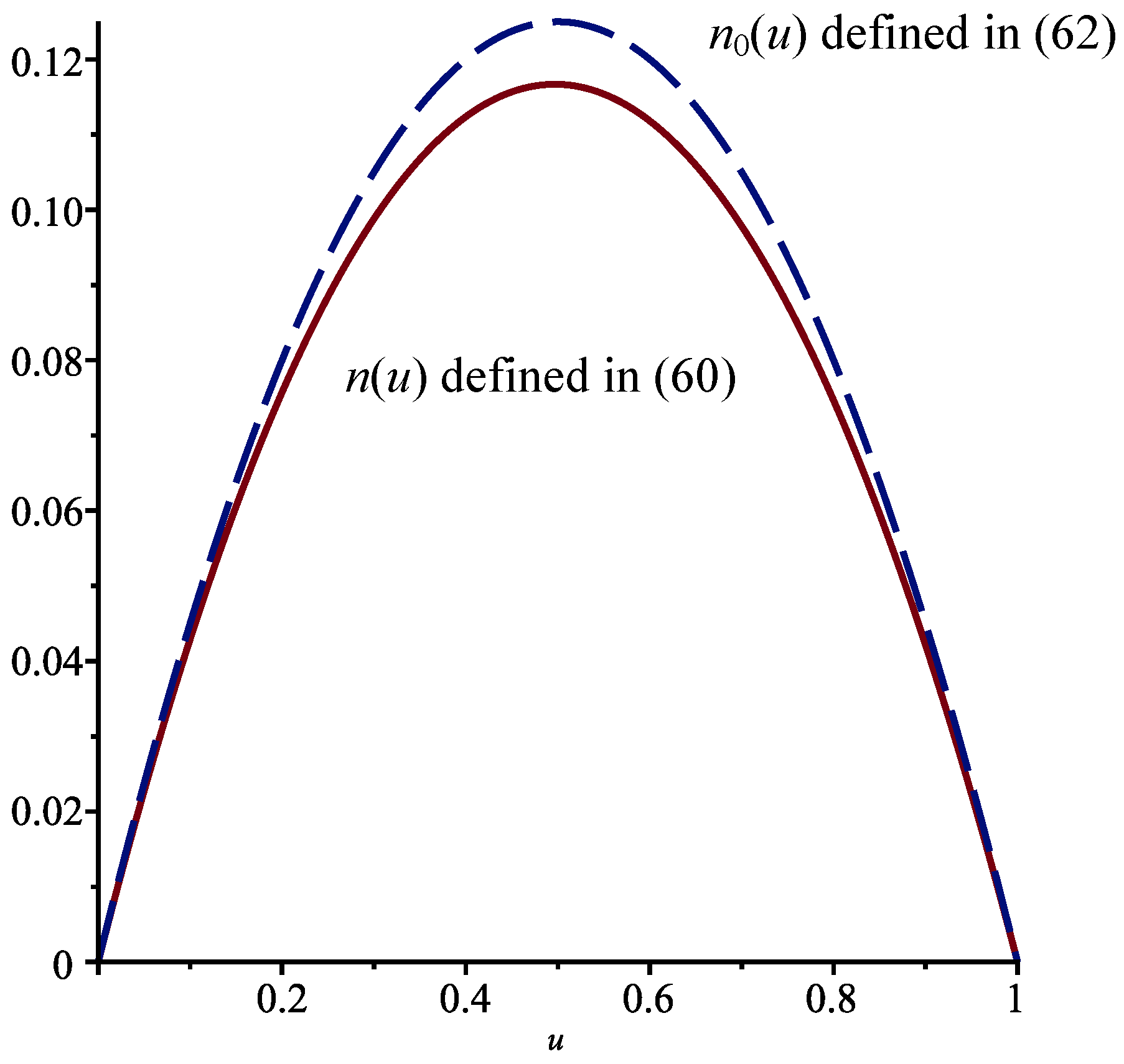

The functions

and

are shown in

Figure 8.

Next, in the case of the function

, the PDIE is (see Equation (

7))

and we must have

if

or

. We define

, which yields the following ODE:

Letting

, the above equation simplifies to the ODE

whose general solution is

As previously, we can first find the constants

,

, such that

and

, and then the constant

r for which the PDIE is satisfied. The constant is

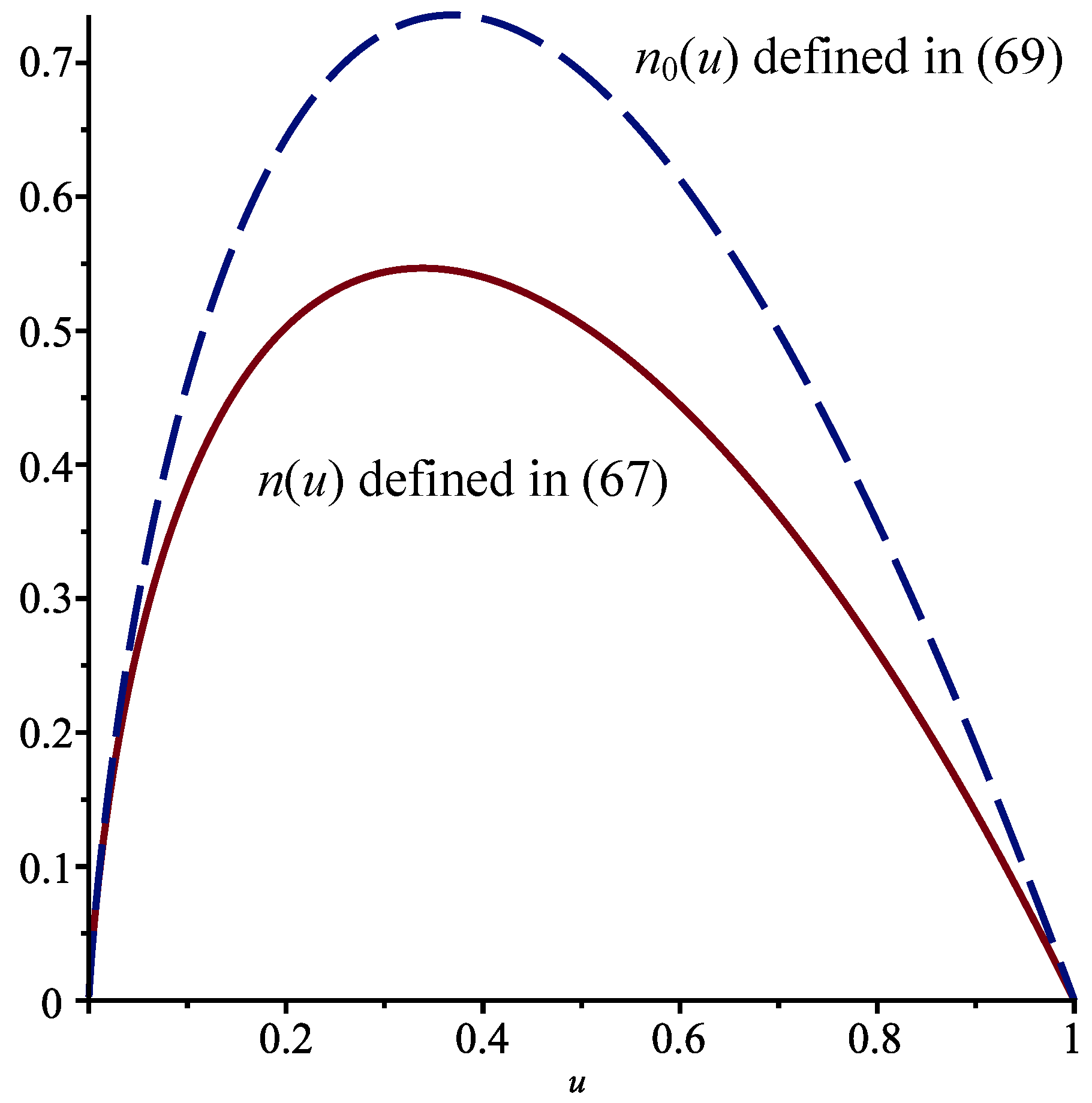

and

The corresponding function

is the unique solution of

such that

. We easily find that

See

Figure 9.

Finally, in Case II, the PDIE that we need to solve to obtain

is

This equation is transformed into the ODE

Choosing

, we obtain

With the help of the software program

Maple, we find that the general solution of the above equation is

Once again, we impose the conditions

and

. We find that we must take

. We have

In the absence of jumps, we compute the function

. It satisfies the ODE

With the conditions

, we find that

Figure 10 presents the functions

and

, which are quite different.

4. Discussion

In several fields, notably, financial mathematics, many authors are now proposing diffusion processes with jumps as models. Moreover, random variables known as first-hitting times are important in various applications. In two or more dimensions, when there are no jumps, to obtain the quantities of interest, such as the mean of these random variables, we need to solve partial differential equations. These equations become partial differential–integral equations when continuous jumps are added.

In this paper, we have considered problems of this type. Owing to the symmetry in these problems, we were able to reduce the PDIEs to (ordinary) integro-differential equations. For the distribution of the random jumps that we used, we succeeded in transforming the IDEs into ODEs.

We have obtained exact analytical solutions to problems involving important diffusion processes. In cases where it is not possible to find analytical solutions, numerical methods can be used to obtain solutions to problems for fixed values of the various parameters in the models.

To generalize the results obtained in this paper, we could add random jumps to the stochastic process as well. Furthermore, other distributions for the random jumps could be used. For discrete distributions, the equations to be solved would be partial differential–difference equations.

Finally, we could try to solve optimal control problems for these jump-diffusion processes in two or more dimensions. To find the optimal control, in the case of random jumps with a continuous distribution, we generally need to obtain the value function, which would then satisfy a nonlinear PDIE.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}