On a Measure of Tail Asymmetry for the Bivariate Skew-Normal Copula

Abstract

1. Introduction

2. Preliminaries

2.1. Tail Order and Tail Order Parameter

2.2. The Skew-Normal Copula

3. Tail Asymmetry of the Skew-Normal Copula

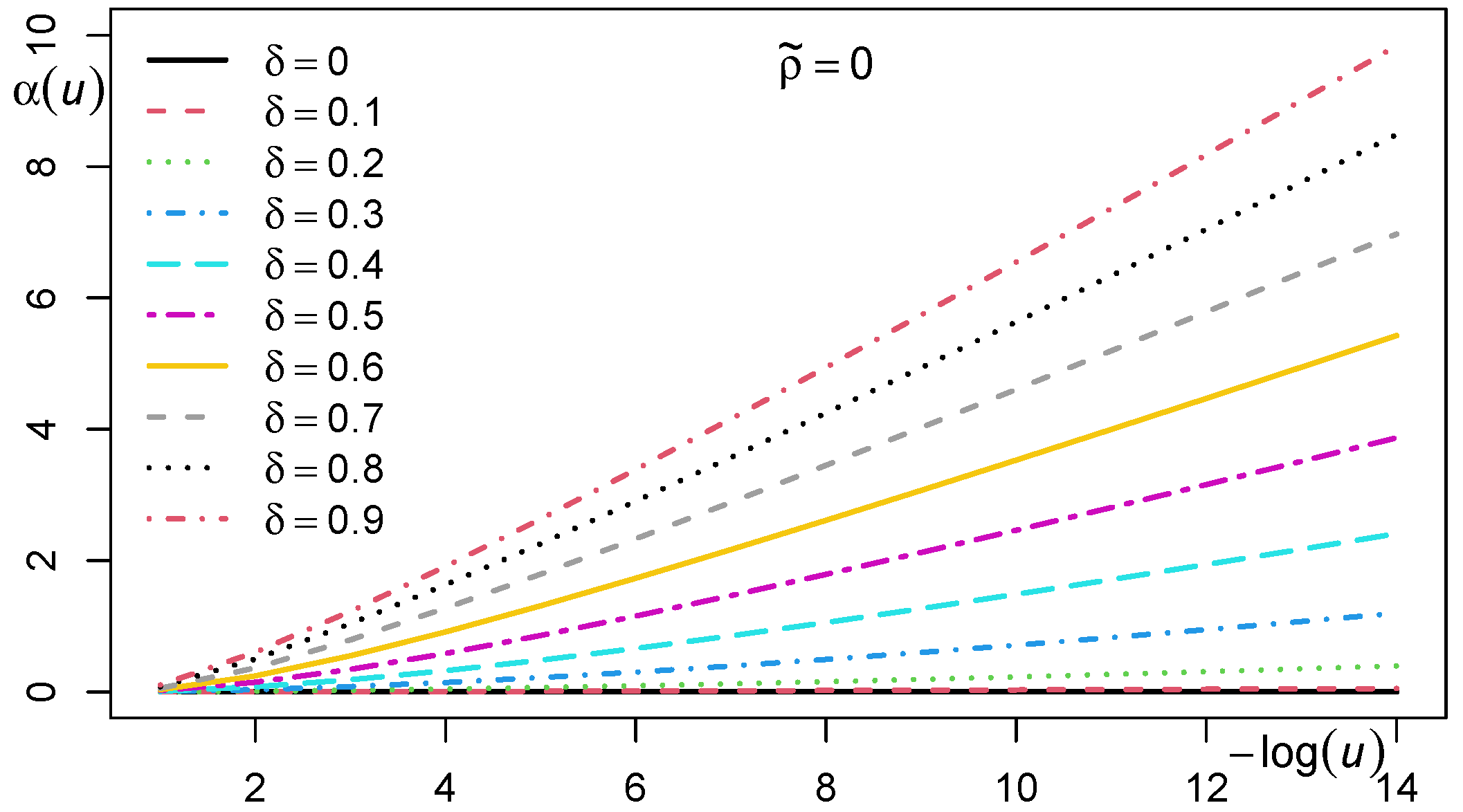

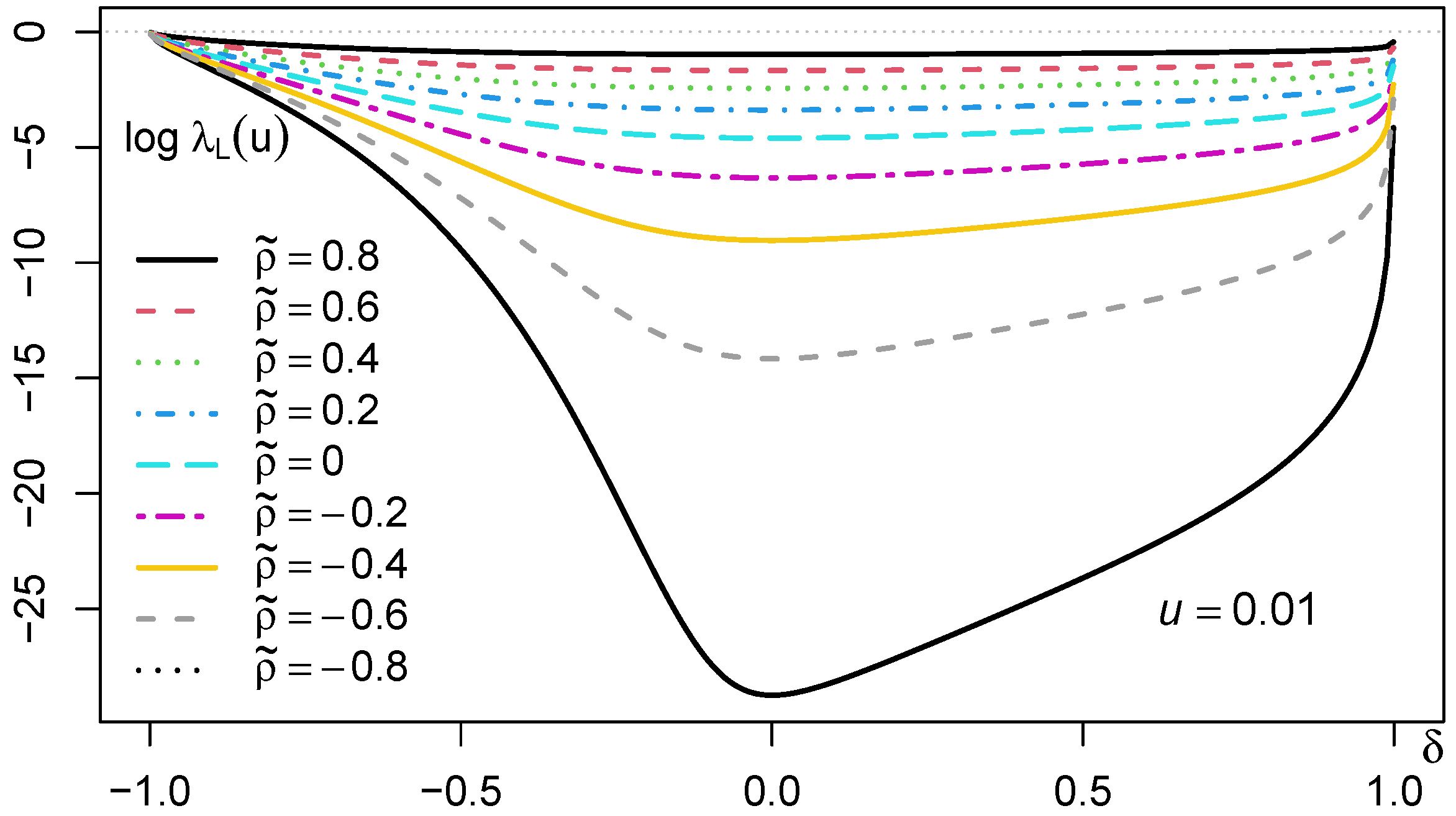

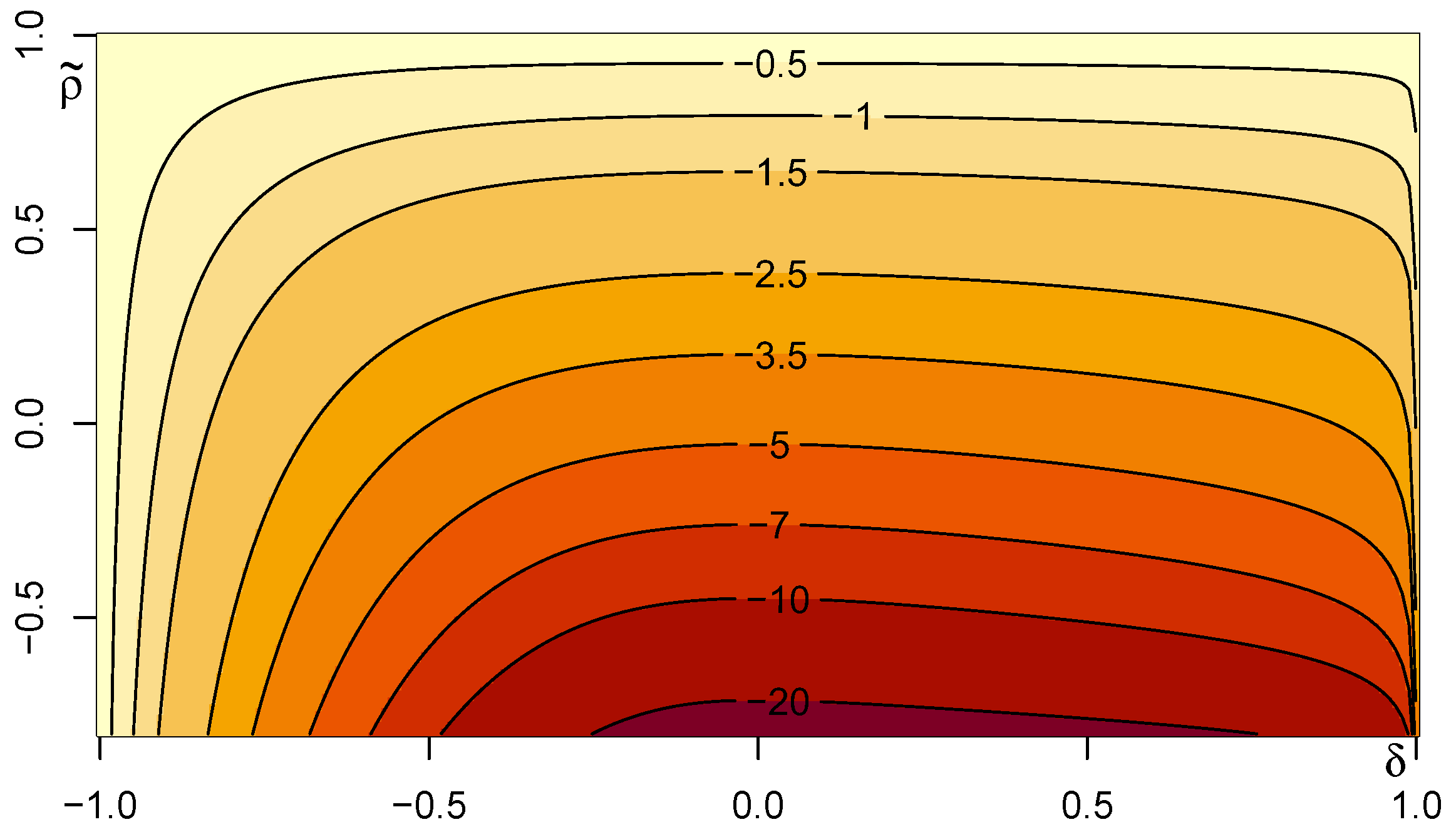

3.1. Measure of Tail Asymmetry and Tail Order

3.2. Measure of Tail Asymmetry of the Skew-Normal Copula

4. Accuracy of the Asymptotic Formulas

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Detailed Calculations

Appendix A.1. Parameters of the Bivariate Skew-Normal Copula

Appendix A.2. Tail Orders of the Bivariate Skew-Normal Copula

- Case I: δ1 = δ2 = δ

- Case III: δ1, δ2 < 0

- Case II: δ1, δ2 < 0

- Case IV: One of δ1 and δ2 Is Zero and the Other Is Negative

- Case V: One of δ1 and δ2 Is Zero and the Other Is Positive

Appendix B. Proofs

References

- Ang, A.; Chen, J. Asymmetric correlations of equity portfolios. J. Financ. Econ. 2002, 63, 443–494. [Google Scholar] [CrossRef]

- Azzalini, A. The Skew-Normal and Related Families; Cambridge University Press: Cambridge, UK, 2014. [Google Scholar] [CrossRef]

- Azzalini, A.; Dalla Valle, A. The multivariate skew-normal distribution. Biometrika 1996, 83, 715–726. [Google Scholar] [CrossRef]

- Azzalini, A.; Capitanio, A. Distributions generated by perturbation of symmetry with emphasis on a multivariate skew t-distribution. J. R. Stat. Soc. Ser. B 2003, 65, 367–389. [Google Scholar] [CrossRef]

- Nikoloulopoulos, A.K.; Joe, H.; Li, H. Vine copulas with asymmetric tail dependence and applications to financial return data. Comput. Stat. Data Anal. 2012, 56, 3659–3673. [Google Scholar] [CrossRef]

- Dobric, J.; Frahm, G.; Schmid, F. Dependence of Stock Returns in Bull and Bear Markets. Depend. Model. 2013, 1, 94–110. [Google Scholar] [CrossRef]

- Rosco, J.; Joe, H. Measures of tail asymmetry for bivariate copulas. Stat. Pap. 2013, 54, 709–726. [Google Scholar] [CrossRef]

- Krupskii, P. Copula-based measures of reflection and permutation asymmetry and statistical tests. Stat. Pap. 2017, 58, 1165–1187. [Google Scholar] [CrossRef]

- Kato, S.; Yoshiba, T.; Eguchi, S. Copula-based measures of asymmetry between the lower and upper tail probabilities. Stat. Pap. 2022, 63, 1907–1929. [Google Scholar] [CrossRef]

- Azzalini, A.; Capitanio, A. Statistical applications of the multivariate skew normal distribution. J. R. Stat. Soc. Ser. (Stat. Methodol.) 1999, 61, 579–602. [Google Scholar] [CrossRef]

- Adcock, C.; Azzalini, A. A selective overview of skew-elliptical and related distributions and of their applications. Symmetry 2020, 12, 118. [Google Scholar] [CrossRef]

- Azzalini, A. An overview on the progeny of the skew-normal family—A personal perspective. J. Multivar. Anal. 2022, 188, 104851. [Google Scholar] [CrossRef]

- Hua, L.; Joe, H. Tail order and intermediate tail dependence of multivariate copulas. J. Multivar. Anal. 2011, 102, 1454–1471. [Google Scholar] [CrossRef]

- Fung, T.; Seneta, E. Tail asymptotics for the bivariate skew normal. J. Multivar. Anal. 2016, 144, 129–138. [Google Scholar] [CrossRef]

- Sibuya, M. Bivariate extreme statistics, I. Ann. Inst. Stat. Math. 1960, 11, 195–210. [Google Scholar] [CrossRef]

- Joe, H. Parametric Families of Multivariate Distributions with Given Margins. J. Multivar. Anal. 1993, 46, 262–282. [Google Scholar] [CrossRef]

- Fung, T.; Seneta, E. Tail asymptotics for the bivariate skew normal in the general case. arXiv 2022, arXiv:2210.01284. [Google Scholar]

- Lao, X.; Peng, Z.; Nadarajah, S. Tail Dependence Functions of Two Classes of Bivariate Skew Distributions. Methodol. Comput. Appl. Probab. 2023, 25, 10. [Google Scholar] [CrossRef]

- Fung, T.; Seneta, E. Tail dependence for two skew t distributions. Stat. Probab. Lett. 2010, 80, 784–791. [Google Scholar] [CrossRef]

- Fung, T.; Seneta, E. Tail dependence and skew distributions. Quant. Financ. 2011, 11, 327–333. [Google Scholar] [CrossRef]

- Fung, T.; Seneta, E. Convergence rate to a lower tail dependence coefficient of a skew-t distribution. J. Multivar. Anal. 2014, 128, 62–72. [Google Scholar] [CrossRef]

- Ling, C.; Peng, Z. Tail dependence for two skew slash distributions. Stat. Interfaces 2015, 8, 63–69. [Google Scholar] [CrossRef]

- Tian, W.; Li, H.; Gupta, A.K. Tail Dependence of Generalized Modified Skew Slash Distribution. J. Stat. Theory Pract. 2022, 16, 4. [Google Scholar] [CrossRef]

- Ning, J.; Yi, W. Tail dependence for skew Laplace distribution and skew Cauchy distribution. Commun. Stat. Theory Methods 2016, 45, 5224–5233. [Google Scholar] [CrossRef]

- Genz, A. Numerical computation of rectangular bivariate and trivariate normal and t probabilities. Stat. Comput. 2004, 14, 251–260. [Google Scholar] [CrossRef]

- Coles, S.; Heffernan, J.; Tawn, J. Dependence measures for extreme value analyses. Extremes 1999, 2, 339–365. [Google Scholar] [CrossRef]

- Li, X.; Joe, H. Estimation of multivariate tail quantities. Comput. Stat. Data Anal. 2023, 185, 107761. [Google Scholar] [CrossRef]

- Nelsen, R.B. An Introduction to Copulas; Springer: New York, NY, USA, 2006. [Google Scholar] [CrossRef]

- Resnick, S.I. Heavy-Tail Phenomena: Probabilistic and Statistical Modeling; Springer Series in Operations Research and Financial Engineering; Springer: New York, NY, USA, 2007. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yoshiba, T.; Koike, T.; Kato, S. On a Measure of Tail Asymmetry for the Bivariate Skew-Normal Copula. Symmetry 2023, 15, 1410. https://doi.org/10.3390/sym15071410

Yoshiba T, Koike T, Kato S. On a Measure of Tail Asymmetry for the Bivariate Skew-Normal Copula. Symmetry. 2023; 15(7):1410. https://doi.org/10.3390/sym15071410

Chicago/Turabian StyleYoshiba, Toshinao, Takaaki Koike, and Shogo Kato. 2023. "On a Measure of Tail Asymmetry for the Bivariate Skew-Normal Copula" Symmetry 15, no. 7: 1410. https://doi.org/10.3390/sym15071410

APA StyleYoshiba, T., Koike, T., & Kato, S. (2023). On a Measure of Tail Asymmetry for the Bivariate Skew-Normal Copula. Symmetry, 15(7), 1410. https://doi.org/10.3390/sym15071410