1. Introduction

One of the most pressing challenges confronting the US in the 21st century is water scarcity. Population growth, which will increase the demand for water throughout the US, has risen by nearly 7%, or approximately 22 million people, since 2010 (

Figure 1). Of course, there have been increases in water use efficiency that have somewhat counteracted the impact of population growth on demand. For example, in California, per capita daily use dropped from 244 to 178 gallons from 1995 to 2010 [

1]. Yet increased evapotranspiration from a warmer climate suggests a less available supply reaching our municipalities, agricultural lands, and water bodies, likely increasing the level of conflict among water sectors. Furthermore, while most climate change models suggest that the amount of precipitation may not change significantly over the next 50 to 100 years, precipitation events will become much more variable, intense, and infrequent, with more precipitation falling as rain than snow [

2,

3,

4,

5]. Combined, these characteristics suggest that conflicts over water scarcity will increase as the temporal distribution and form of supply deviates from what our infrastructure was designed to handle.

The objective of this review paper is to shed light on how water scarcity is changing in the Southwestern US, and the role water markets have and might play in addressing this scarcity. In particular, we focus on how the demand and supply of water are trending in representative states in the southwest—Arizona, California, and Texas—and the increasing role of water markets in helping states to address such scarcity. Two of these states—Texas and California—have accounted for nearly 1/3rd of the population growth in the US (

Figure 1). Relative to US averages, the southwestern states of Arizona, California, and Texas confront higher population growth (2.45% vs. 1.15% between 1920 and 2018), higher temperature (61.1 °F vs. 52.5 °F), and less precipitation (20.68 in vs. 30.48 in). Such differences increase water demand and decrease the supply of runoff from precipitation events resulting in rising water scarcity.

Since markets depend on differences in the marginal values across users to create incentives to trade, we differentiate between different types of water use (e.g., agricultural, environmental, municipal/city) to better understand which sectors will likely be driving the market, where scarcity might arise within a state, and the role of water markets in potentially assuaging such scarcity. After briefly describing some general climate and population statistics within each state that likely influence water scarcity, we introduce water supply and demand conditions by state, with a brief background of water use trends.

Following each state-level discussion, we provide data on water market trends and transactions within each state and discuss how those trends may relate to water scarcity characteristics within each state. Note that the effectiveness of water markets and growth in water demand, supply, and use is largely influenced by each state’s water rights laws and regulations. Given space limitations, we have opted to focus strictly on presenting the most recent data on water demand, supply, and markets but direct the reader to other sources for an in-depth understanding as to how water rights and regulations within each state influence the trends we identify. For example, for California, see Hanak, et al. [

6]; for Arizona, see Colby and Isaaks [

7]; for Texas, see Kaiser [

8].

Data are presented on the overall market size measured in total volume and value during 2009–2018 as well as the distribution of market activity across western states. We also review active sectors buying and selling water and discuss commonly traded types of water entitlements and transaction structures. In this paper, we use water markets data from Waterlitix

TM, the largest and most comprehensive database of water rights price and sales information in the United States. Waterlitix

TM is a proprietary database developed and maintained by WestWater Research. The data are the results of two decades of continuous, primary research of water right trading and leasing. Transaction information is compiled from state and local regulatory filings, public and private transaction documents such as leases and purchase and sale agreements, and through direct interviews with parties involved in transactions. The database is structured to include both water asset/water right details and transaction specific information. Water asset information includes details on the water asset type involved in the transaction such as authorized diversion volume, quantity of water approved for transfer (which may differ from the authorized diversion volume), other information on the water rights or assets such as priority date, authorized use, source and locational characteristics including water basin, administrative districts or water management boundaries such as a water district or ditch company. The database also includes specific transaction details such as buyer and seller information, previous and new use of the water, transaction structure such as single year lease, multi-year lease, permanent purchase or other complex exchanges where financial consideration is paid. Other transaction information includes financial consideration paid, financial and transaction terms, total payment, and unit price payment that has been normalized across all transactions to allow for comparisons of equivalent transactions and water asset types. All of the transactions within Waterlitix

TM are geo-referenced within a geospatial searchable data platform. Prior water market studies include comprehensive transactions from 1987 to 2009 in the Western US [

7,

9,

10,

11,

12]. Our analysis provides an update to these prior studies. We end with a discussion of how the role of water markets may be improved in the future to help states, and the US as a whole, better cope with future rising water scarcity.

3. Discussion

In this section, we first provide a comparison between the three states in terms of water demand and supply by sector and source. We then provide a discussion of notable water market characteristics—both similarities and differences—across the three states. We conclude with a brief discussion on the importance of developing more transparent and efficient markets to facilitate the usefulness of this tool in helping states confront rising water scarcity.

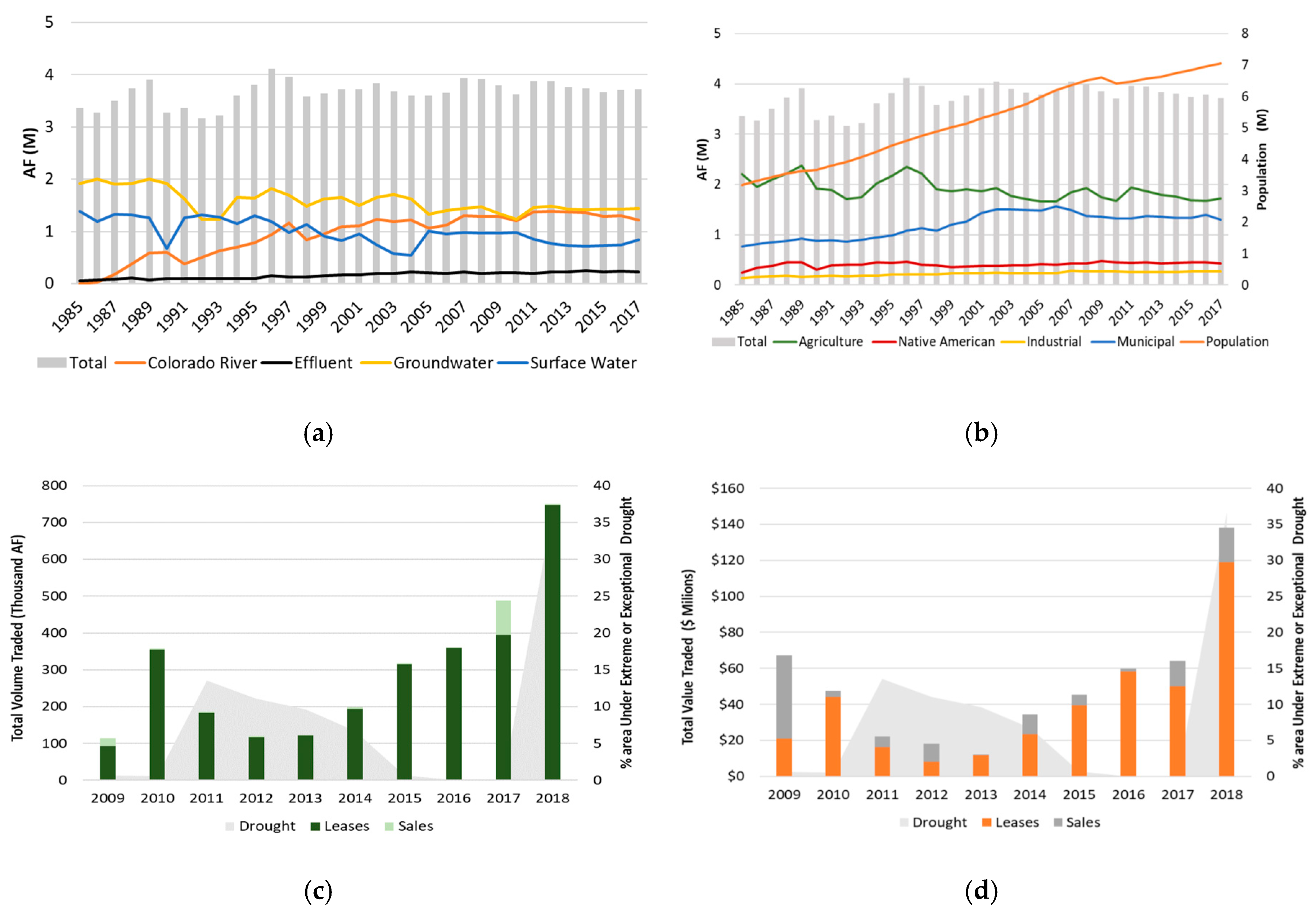

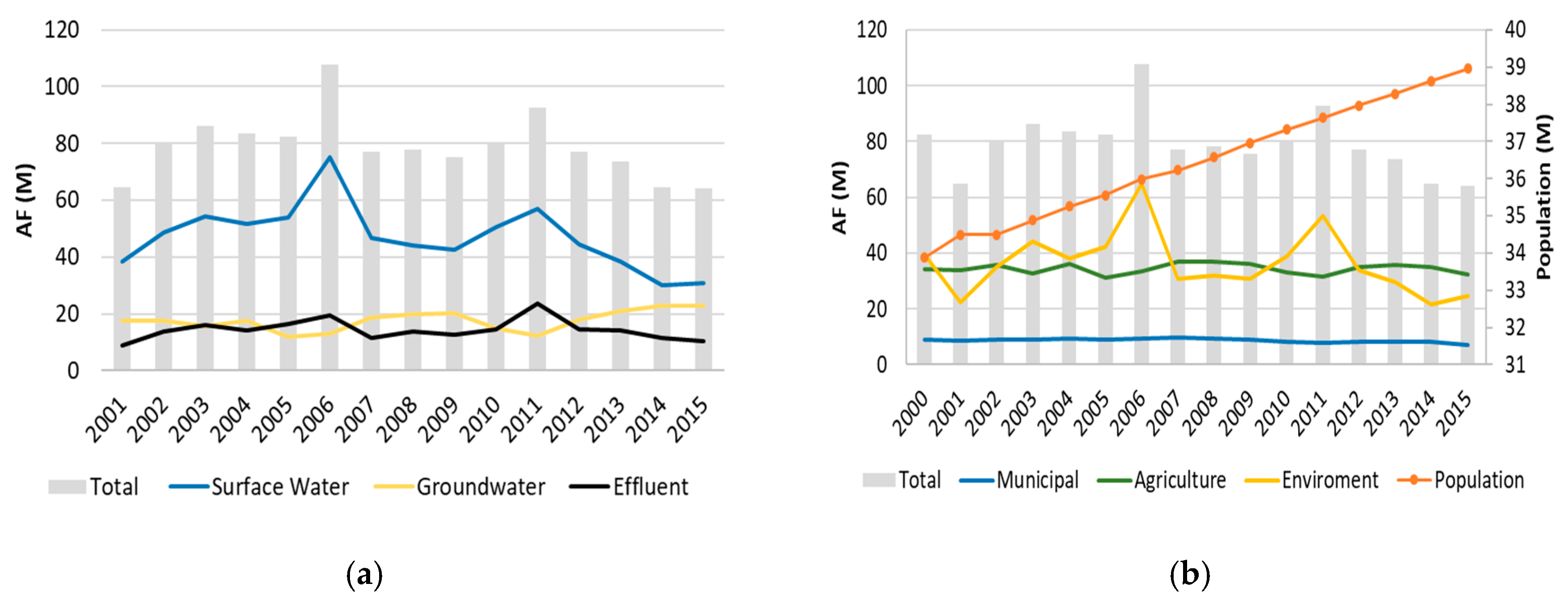

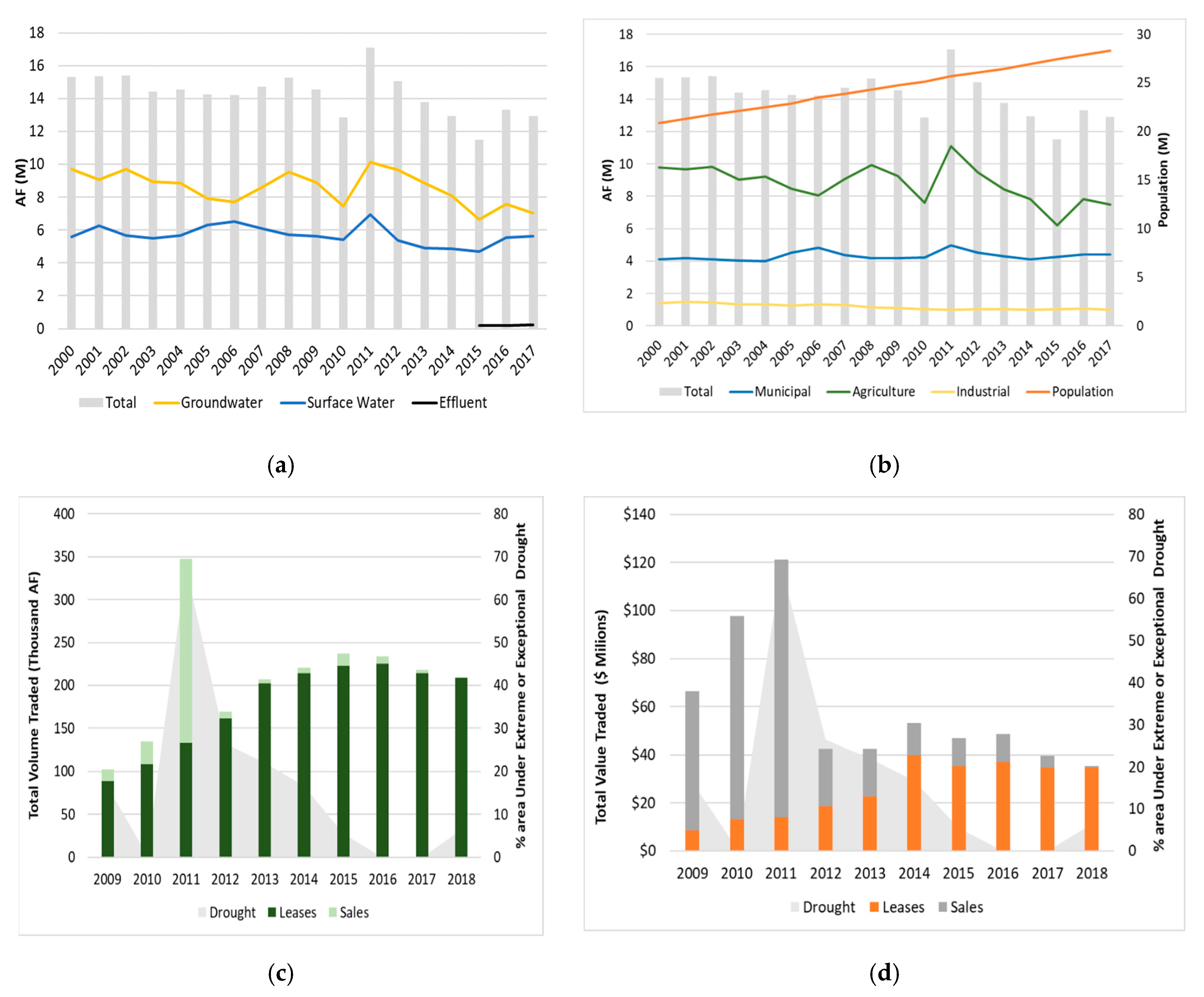

As illustrated in

Table 2, across all three states, the agricultural sector requires the highest volume of water, with it consuming 58% of the water in Texas, 51% in California, and 46% in Arizona. Note that while we use the term “consuming,” a more accurate term would be “diverting” since a fraction of the water not transpired or evaporated often returns to the system [

32]. However, while agriculture consumes the most water, its overall use has gone down over the past two to three decades, most notably in Arizona (~22%) and Texas (~12%). Improvements in irrigation efficiency are responsible for much of this decline. On the municipal side, demand is trending slightly up in Texas, is somewhat stable in Arizona, and trending slightly downward in California over the past two decades, with water efficiency measures again playing a significant role in counteracting significant population growth in all three states. As the agricultural and municipal sectors adopt more efficient water use behavior and technologies, demand hardening (i.e., as farmers/households become more efficient, it becomes more difficult to further reduce demand during a shortage or drought) will ensue thereby increasing the potential benefits of water markets as a tool to address increased future water scarcity.

In terms of source supply, surface water is the primary provider in Arizona (55%) and California (48%), but in Texas, groundwater is the primary source (54%). Unlike the role the Colorado River played for Arizona during the 1980s and 1990s, surface water sources are unlikely to provide any new volumes to these states moving forward, and groundwater supplies are in decline in all three states. Furthermore, with the enactment of new groundwater sustainability legislation in California in 2014, groundwater pumping is likely to decrease even more than it currently is. As such, water markets again can play an increasingly important role in responding to an increased level of water scarcity due to declining or less reliable water supplies in each state. Of course, effluent in the form of treated municipal wastewater may help assuage such scarcity in local markets, as is taking place in California, yet such efforts require significant infrastructure investments, along with other costs due to technological constraints [

33,

34], to play a more significant role.

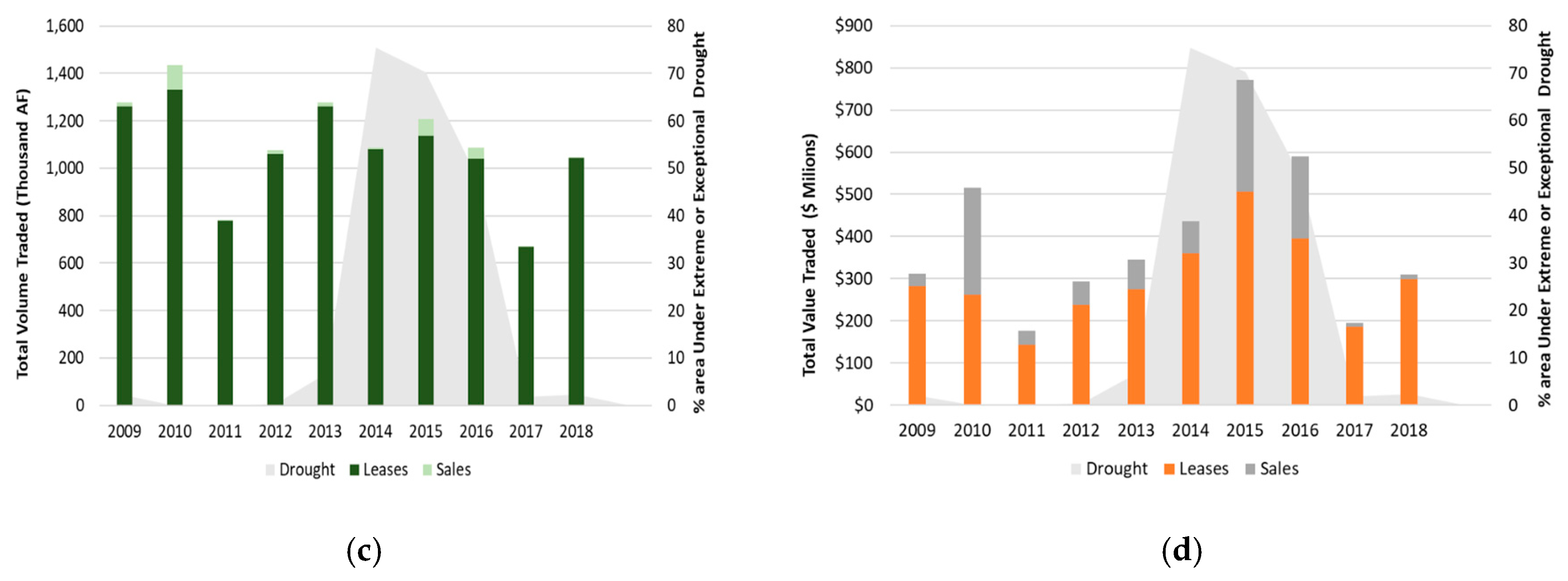

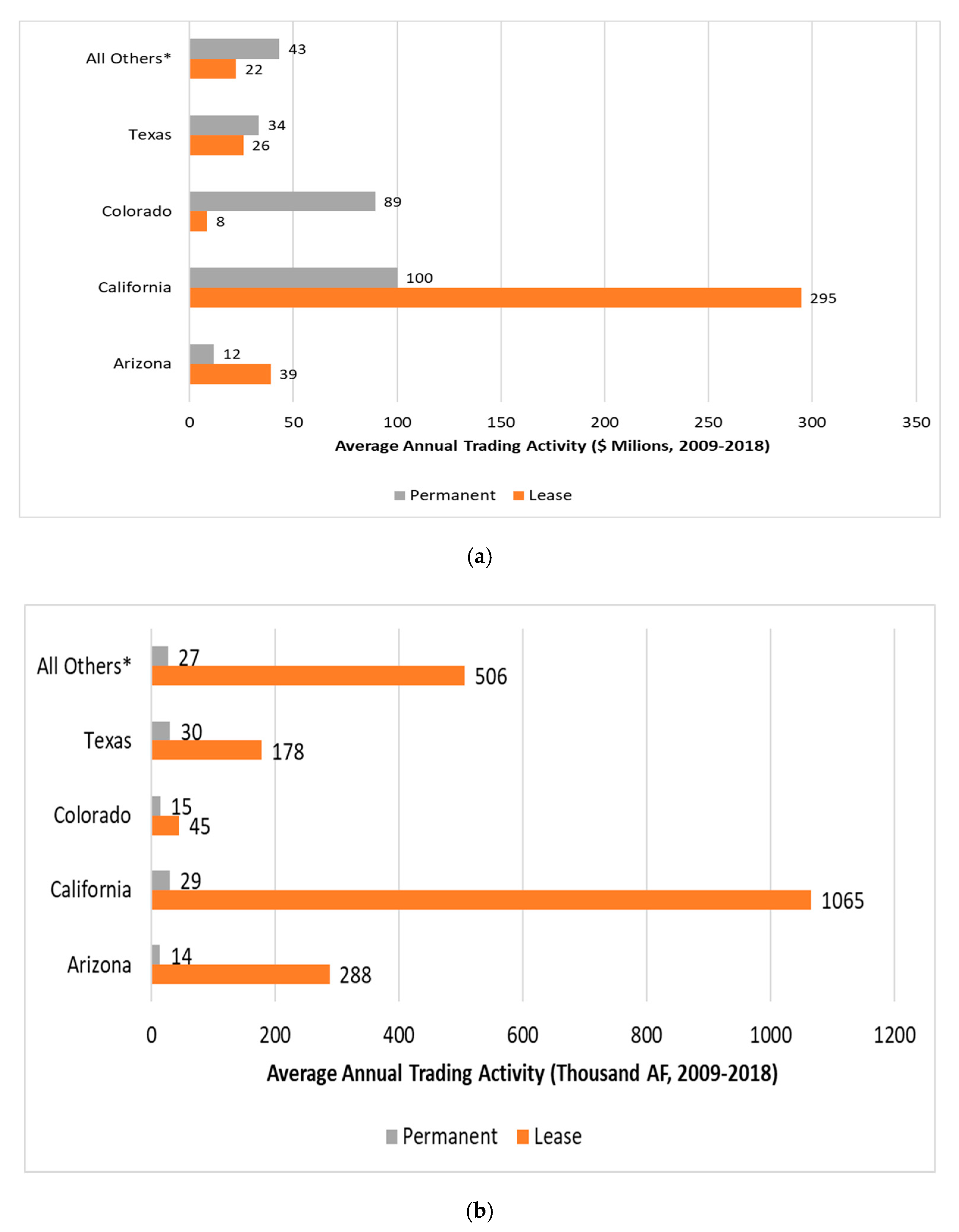

Since 2009, our data suggest that water markets in all three states are functioning to help address water scarcity, although there is likely plenty of opportunities for improvements and growth. While California has by far the highest amount of water trading—both in terms of volume and value—Arizona’s market transactions comprise approximately 4% of the overall water used in the state, double the approximate 2% that defines both California and Texas (

Figure 5a,b). However, even at 2%, approximately

$3.9 billion of water was exchanged in California over the past decade. Most of the activity and value is derived through temporary leases rather than permanent sales, on average. Exceptions to this include significant increases in the price of permanent water sales in California during its most recent drought, although trading activity did not change significantly, and permanent sales and the value of those sales in Texas during the drought in 2010 and 2011. Overall trading activity, though, has been on the rise in Arizona, somewhat stable in Texas, and quite variable in California over the past decade, highlighting the importance of the heterogeneous market, environmental, and institutional conditions across states, conditions that determine market performance.

In terms of who is selling and/or leasing the water,

Figure 6 provides a comparison of the sources of supply and demand for water trades and transfers in California (

Figure 6a,b), Texas (

Figure 6c,d), and the Western US (

Figure 6e,f) across the major sectors. In California, agricultural water rights holders provided most of the water to the market over the past ten years (

Figure 6a). Approximately 76% of the total volume transacted over this timeframe originated from the agricultural sector, followed by the municipal sector (19%). Agriculture’s market share as a supplier has increased over the last ten years by around 2%, although it should be recalled that overall traded volumes have gone down slightly.

In terms of major buyers in California, the municipal sector purchased/leased the most water, on average, over the past ten years, followed by agriculture and then the environment (

Figure 6b). While the municipal sector had a somewhat stable level of purchases from 2009 to 2016 (on average they comprise approximately 55% of the total market share), there was a slight decrease in 2017 and 2018 potentially due to (i) lower incentives to trade due to drought subsiding in 2017, and (ii) increased acreage of higher revenue perennial (e.g., tree and orchard) plantings whose significant capital investments increase the opportunity cost of fallowing land. While the agricultural sector has comprised approximately 25% of the market purchases over the past ten years, there was a noticeable and significant increase in the year 2018, as the drought eased and groundwater regulations were tightened under the recently passed Sustainable Groundwater Management Act of 2014. The environment, meanwhile, also plays a significant role in California water markets, comprising approximately 18% of total transactions by volume traded.

In Texas, similar to California, agricultural water rights holders provided most of the water to the market over the past ten years (

Figure 6c). Approximately 89% of the total volume transacted over this timeframe originated from the agricultural sector, followed by the industrial sector (8%). In terms of major buyers, the municipal sector purchased/leased the most water, on average, over the past ten years (84%), followed by agriculture (13%) (

Figure 6d).

The Western States in this figure include Arizona, California, Colorado, Idaho, Montana, Nevada, New Mexico, Oregon, Texas, Utah, Washington, and Wyoming. Not surprisingly, water is sourced primarily from the agriculture sector. Over the past ten years, approximately 73% of the total volume transacted in the Western US originated from the agricultural sector (

Figure 6e). The municipal sector is the second-largest supplier, comprising approximately 23% of the overall sourced supply in the Western US. The industrial sector is responsible for approximately 4% of the sourced water. Note that while in Texas the agricultural sector is responsible for typically around 90–95% of the overall water sales/leases in the state, in absolute terms it is relatively minor compared to California, where the municipal sector is responsible for around the same volume of water sales/leases compared with the agricultural sector in Texas.

On the demand side, participation remains relatively stable, with municipalities continuing to be the largest buyer with 46% of total market share over the past ten years (

Figure 6f), although it plays a much more significant role in percentage terms in California and Texas (

Figure 6b,d). Environmental buyers, usually comprised of private entities, conservation groups, but also state and federal agencies in efforts to maintain or meet obligations associated with environmental quality, instream-flows, and wildlife habitat [

35,

36], also play a significant role in western water markets—mostly arising in California—comprising approximately 26% of total transactions by volume traded, followed by agricultural (16%) and industrial (12%) sectors. As noted in Szeptycki, Forgie, Hook, Lorick, and Womble [

35], there is significant variation in how water transfers for the environment are regulated across western states, and these differences can significantly limit the type and scope of transfer. While all three states we considered have opportunities to reduce obstacles that are hindering environmental transfers, particularly the administrative burden buyers and sellers confront exercising such transactions, California and Texas are noted to confront fewer of the legal challenges than Arizona in terms of the scope, certainty, and permissibility of environmental water transfers.

In considering the year-to-year variation, we see that there were some significant volumes purchased by the agricultural sector in Texas during the drought years between 2011 and 2014, but on average, over 90% of the volume bought was by the municipal sector. While purchases of permanent water or leases by industrial users do happen, the percentage of the overall volume is quite small. Finally, and what perhaps California’s experience in 2018 forebodes for the rest of the West, water supply firming for agriculture associated with the increase in permanent cropping, especially in California, has prompted agriculture to participate in the demand side in higher proportions. As shown in

Figure 6b, California’s agriculture demand-side market participation has increased by 6% and 15% by value and volume traded, respectively, over the last ten years.

4. Concluding Remarks

Water markets at their core, as with any market, are intended to help reduce the impacts of scarcity by facilitating the transfer of water to its highest-valued uses. What this review has shown in evaluating three western states, is that water scarcity is likely to increase significantly moving forward, primarily due to population growth and the added water demand associated with such growth. Of course, improvements in water use efficiency, both in the agricultural and municipal sectors, have helped society respond to date (indeed, overall water use in California has decreased in the agricultural and municipal sectors). However, demand will harden, and thus such efficiency gains will be harder to come by, resulting in water demand rising with population growth. Scarcity will also heighten due to lower and/or more variable supplies coupled with increased regulation surrounding groundwater pumping and use. These conditions, increasing demand coupled with stagnating or declining and more variable supplies, which seem to characterize each of the three states we examined, suggest an increasingly important role for water markets.

Our analysis has also shown how water markets have played an essential role in water reallocation throughout the Western US. In the recent data we analyzed here, most of the transfers are associated with leases as opposed to permanent water sales. Nevertheless, the overall amount of water that is transferred is small relative to the total water used, between 2% and 4%. This suggests that plenty of opportunities exist for the market to expand, which will require attention from market developers, regulators, and stakeholder input. For instance, during California’s most recent drought, trading activity did not seem to respond in any appreciable manner, yet the price of both leases and permanent sales rose significantly (e.g., the price of permanent sales rose from $3797 per acre-foot in 2013 to over $9230 per acre-foot in 2014, yet actual trading activity in the state declined). There are multiple factors —that differ across states— that likely contribute to inhibiting the market from achieving its full potential, including high transaction costs associated with often multiple layers of approval, a lack of transparency, poor and incomplete information flows, along with conveyance and infrastructure limitations.. So while markets have been serving as a means to help change the temporal and spatial distribution of water allocations to their higher-valued uses, significant opportunities exist to both better understand the drivers that influence water market performance and expand the market through the creation of a more transparent, flexible, and user-friendly system.

While water transfers can lead to an overall increase in the net benefits water use from a social perspective, concerns of third-party effects and externalities on other users can create challenges and limit the full functioning of a water market [

37]. For instance, if water transferred out of a region results in impacts on local employment and income, such third-party effects can lead to transfers being politically unattractive (and lead to limits on transfers). Of course, if the transfers occur within a particular region, then such third-party effects will be minimal. In response to these third party effects, governments often respond by limiting out-of-region transfers via mandates or fees. Alternatively, if transfers incentivize greater groundwater pumping in agricultural-based communities, this may have impacts on the availability of municipal water for those communities dependent on groundwater for health and hygiene [

38]. Careful hydrological monitoring, or employment of a general water accounting framework, can help policy makers better understand the potential implications of transfers on groundwater levels and other users.

Note that the “water market” we describe in this paper is comprised of significantly different water trading and transfer schemes both within and across the three states analyzed. While our focus was on traded water entitlements, surface and groundwater rights are the most commonly traded asset class within the Western US market. However, there are other types of ownership interests in water that are also traded. For example, in Arizona and California, groundwater banking is also traded. Entitlement to use treated wastewater is traded in Arizona, California, and Colorado. Entitlement to store water for use in a surface reservoir, known as “Storage Water Rights”, is observed in California and Colorado [

39]. As such, there are many opportunities and forms of markets that can be used to help the Western US cope with rising water scarcity, but it requires significant planning, cooperation, collaboration, and evaluation by policymakers with stakeholders to facilitate the development and implementation of such markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}