Abstract

This article provides a conceptual and exploratory examination of Scope 3 greenhouse gas (GHG) emissions, focusing on the complexities associated with their nature, measurement, reporting, and verification. It examines the emerging role of artificial intelligence (AI) in addressing these complexities, particularly considering the fragmented, opaque, and often inaccessible nature of Scope 3 data. The paper introduces Critical Systems Thinking (CST) as a foundational framework for considering the practicality of utilization of AI in this context. CST emphasizes three key principles: critical awareness of assumptions and contexts, emancipation through attention to power dynamics and continuous improvement, and methodological pluralism, to engage with complexity through diverse analytical approaches. Due to the complex nature of GHG emissions reporting and assurance, AI application for this purpose remains limited. While Scope 3 reporting has made progress in certain sectors and regions, overall maturity remains uneven—particularly in developing and emerging markets. Although AI applications in Scope 3 reporting are still at an early stage, they hold significant potential to enhance both reporting quality and assurance processes. A key factor that needs to be addressed in the future utilization of AI for Scope 3 emissions reporting and assurance is the integration of CST into the development and implementation of AI tools. This paper proposes such integration as a necessary step forward. At present, there are substantial gaps in Scope 3 emissions measurement and reporting due to the inherently highly complex, distributed, and fragmented nature of value chain emissions. This gap poses risks to data quality and consistency, which in turn can hinder the implementation of reporting legislation and informed decision making by management and stakeholders. Systemic fragmentation, power asymmetries in data access, and methodological inconsistencies present substantial challenges to traditional forms of validation. Rather than offering a predictive model or finalized solution, the paper aims to lay a conceptual foundation for future empirical research and highlights the importance of systems-based approaches in advancing the credibility and utility of Scope 3 GHG disclosures. This is a key limitation relating to this paper, as it mainly focuses on the CST framework and the potential incapacities of artificial intelligence in relation to the implementation of CST, rather than applications of CST, as they are limited at present.

1. Introduction

The recently introduced international climate reporting standard, the International Financial Reporting Standards (IFRS) S2 “Climate-related Disclosures” issued by the International Sustainability Standards Board (ISSB), requires an entity to disclose information about climate-related risks and opportunities that could reasonably be expected to affect the entity’s financial performance [1]. Among its key requirements, IFRS S2 requires companies to disclose their greenhouse gas (GHG) emissions, including Scope 1, 2, and 3 emissions. Scope 3 emissions result from sources or assets not owned or directly controlled by the reporting organization and relate to indirect impacts across both upstream and downstream segments in the value chain [2]. To accurately report on Scope 3 emissions, a comprehensive emissions inventory approach, which provides a structured framework for identifying, quantifying, and disclosing indirect emissions throughout the value chain, is useful [2], but, in practice, data limitations, low supplier engagement, and methodological inconsistencies have constrained reporting.

Despite growing regulatory pressure, companies are finding it difficult to capture, measure, report, and assure Scope 3 emissions, yet Scope 3 emissions account for up to seventy-five percent of total emissions for most companies [3], and, in some cases, even more. For financial institutions, financed emissions alone can account for over 90%, and often more than 99%, of a financial institution’s total emissions [4]. Prior research has found that there is a general lack of knowledge, capacity, and consistent methodology in this space [5,6,7]. As such, many organizations struggle to produce reliable or decision-useful Scope 3 disclosures. These challenges are amplified in developing and emerging markets, where data infrastructure, regulatory enforcement, and supply chain transparency are often less mature.

This paper responds to a key contradiction: the rising demand for Scope 3 emissions disclosures, potentially accompanied by assurance requirements, contrasted with the systemic complexity that prevents most organizations from fulfilling this obligation meaningfully. It aims to provide a comprehensive understanding of Scope 3 emissions within the Greenhouse Gas (GHG) Protocol, with a particular focus on the challenges of measurement, reporting, and assurance. It also offers a conceptual and exploratory examination of this gap, focusing on how artificial intelligence (AI) can support improvements in the measurement, reporting, and assurance of Scope 3 GHG emissions.

Although AI is frequently cited as a tool to automate and enhance sustainability reporting, its application to Scope 3 remains limited and fragmented. The effective use of AI in this space requires more than technical capability—it demands a systems-oriented approach that can navigate data fragmentation, accountability gaps, and stakeholder complexity. To this end, the paper proposes Critical Systems Thinking (CST) as a foundational framework to guide the development and deployment of AI in the Scope 3 value chain context. CST emphasizes three principles:

- Critical awareness of assumptions and contexts;

- Emancipation, which involves addressing power asymmetries and promoting systemic improvement;

- Methodological pluralism, which encourages the use of multiple tools and perspectives to manage complex problems.

To illustrate current applications of AI in practice, the article presents multiple examples of AI-enabled ESG platforms. These examples demonstrate the limitations of AI applications and gaps relating to alignment with regulatory expectations due to systemic complexities.

Finally, the paper also discusses why empirical testing of such frameworks remains limited. It applies a critical systems perspective to explain the barriers, fragmented supply chain data, limited assurance methodologies, and inconsistent practices across jurisdictions, that hinder robust testing and validation. Rather than offering a predictive model or finished solution, this study lays a conceptual foundation for future empirical research and practice. It contributes to an emerging body of work that recognizes the need for systems-based approaches to ensure credible, scalable, and decision-useful Scope 3 disclosures. The paper proceeds with Section 2, which reviews the current state of Scope 3 reporting and assurance and provides an overview of Scope 3 emissions under the Greenhouse Gas (GHG) Protocol. It outlines key challenges in measurement, reporting, and verification of Scope 3 emissions data. This section is followed by a discussion of Critical Systems Thinking as a theoretical framework to navigate the multifaceted issues involved. Artificial intelligence tools that are being utilized for capturing and critically analyzing Scope 3 emissions are illustrated through multiple examples of ESG platforms covered in Section 4, while Section 5 discusses the findings and implications. Section 6 concludes with reflections and future research directions.

2. Scope 3 Greenhouse Gas Emissions: Conceptual Foundations and Methodological Challenges

2.1. Scope 3 Emissions—An Overview

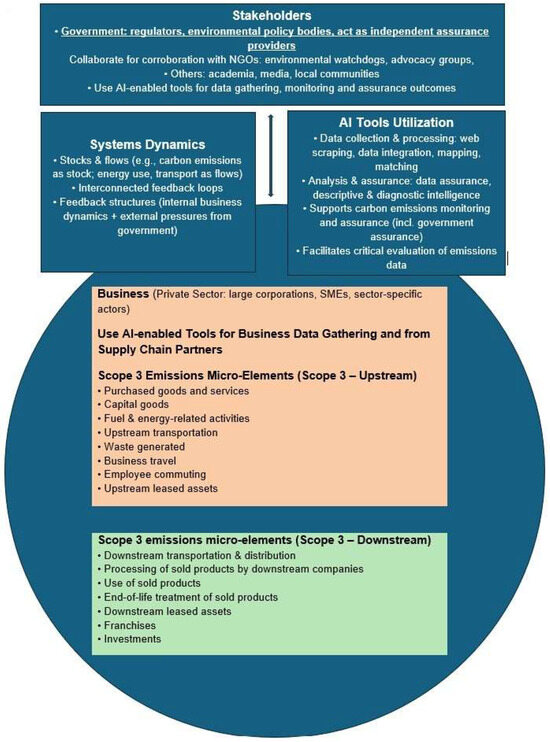

There are two types of GHG emissions, direct and indirect. Direct emissions are the result of sources directly related to a reporting company. Indirect emissions are emissions that are a result of the activities of the company; they occur at sources not owned or controlled by the company [8]. Emissions are further divided into Scope 1 (direct emissions) and Scope 2 emissions, which relate to purchased electricity, steam, heating, and cooling used by the company [8]. Scope 3 emissions are all other emissions not accounted for under Scope 1 and 2 emissions. These include emissions from upstream activities (indirect GHG emissions related to purchased or acquired goods and services until the point of receipt by the company). Examples of upstream activities include purchased goods and services, transportation and distribution, business travel, and employee commute. Downstream activities are indirect GHG emissions related to sold goods and services and emissions related to activities after sale or transfer of control from the company. Examples include emissions relating to the use of sold products, end of life treatment of sold products, franchises, and investments [8]. A complete GHG inventory includes Scope 1, 2, and 3 emissions [8].

The GHG Protocol has established a global framework to measure and manage greenhouse gas emissions from operations and value chains [9]. It is the GHG Protocol’s Corporate Value Chain (Scope 3) Accounting and Reporting Standard (hereinafter referred to as the GHG Scope 3 Standard) that provides detailed guidance for Scope 3 Emissions reporting [8]. This standard, and the other globalized standard GHG Protocol frameworks, were developed collaboratively by the World Business Council for Sustainable Development (WBCD) and the World Resources Institute (WRI). The standard provides requirements and guidance for companies to report on their GHG emissions inventory, including indirect emissions from value chains (Scope 3) [8]. A Scope 3 inventory requires reporting of emissions from multiple partners in the value chain, especially from suppliers [8]. A reporting entity (company) is required to work closely with supply chain partners to create a common understanding of emissions information; a company can also provide information on the progress of engagement in the supply chain towards measuring and reporting Scope 3 emissions [8].

2.2. Upstream Scope 3 Emissions

Under the standard, various categories [8,10] of upstream Scope 3 emissions are defined as follows [8]:

Category 1—Purchased goods and services: Extraction, production, and transportation of goods and services, including all upstream emissions (cradle-to-gate) of purchased goods and services not otherwise included in Categories 2–8.

Category 2—Capital goods (such as machinery and equipment, raw materials, vehicles): Extraction, production, and transportation of capital goods purchased or acquired by the company, including all upstream (cradle-to-gate) emissions of purchased capital goods.

Category 3—Fuel and energy activities (not included in Scope 1 or 2): These include extraction, production, and transportation of fuels and energy purchased by the company in the reporting year not already accounted for in Scope 1 or 2. For upstream emissions of purchased fuels, all emissions from cradle to gate need to be recorded from raw material extraction to the point of combustion. It also includes upstream emissions related to purchased electricity, from raw material extraction to the point of combustion and the generation of purchased electricity.

Category 4—Upstream transportation and distribution: Transportation and distribution of purchased products in the reporting period between the company’s tier 1 suppliers and the company’s operations in vehicles and facilities not owned or controlled by the company, inbound logistics, outbound logistics, and transportation and distribution between the company’s facilities (in vehicles not owned by the company).

Category 5—Waste generated in operations: Disposal and treatment of waste generated in the reporting company’s operations (in facilities not owned or controlled by the company).

Category 6—Business travel: Transportation of employees for business-related activities during the reporting period (in vehicles not owned or operated by the company).

Category 7—Employee commuting: Transportation of employees between dwellings and worksites during the reporting period (in vehicles not owned or operated by the company).

Category 8—Upstream leased assets: Operation of leased assets by the reporting company (lessee) in the reporting year and emissions not included in Scope 1 or 2.

2.3. Downstream Scope 3 Emissions

Similarly, there are various categories for downstream Scope 3 emissions [10], which include the following:

Category 9—Downstream transportation and distribution: Transportation and distribution of products sold by the company between the reporting company’s operations and the end consumer (if not paid for by the reporting company), including retail and storage (in vehicles and facilities not owned by the company).

Category 10—Processing of sold products: Processing of intermediate products sold in the reporting year by downstream companies (e.g., manufacturers).

Category 11—Use of sold products: End use of goods and services sold by the reporting company, which include direct use-phase emissions of sold products over their expected useful life.

Category 12—End of life treatment of sold products: Waste disposal and treatment of products sold by the reporting company (in the reporting year) at the end of their life, including Scope 1 and 2 emissions of waste management companies during disposal or treatment of sold products.

Category 13—Downstream leased assets: Operation of assets owned by the reporting company (lessor) and leased to other entities in the reporting year.

Category 14—Franchises: Operation of franchises in the reporting year, not included in Scope 1 or 2, reported by the reporting company (franchisor).

Category 15—Investments: Operation of equity and debt investments categorized as downstream Scope 3 as capital or financing is provided by the reporting company and the associated emissions are not recognized as part of Scope 1 or 2.

As identified in the detailed coverage of Scope 3 emissions (upstream and downstream), the amount of data that needs to be collected is extensive, complex, and laborious. Data collection processes need to cover the most significant GHG emissions, data collected need to highlight the most significant GHG reduction opportunities, and high-quality data need to be ensured [8]. Assurance plays a critical role in ensuring high-quality data.

2.4. Scope 3 Emissions: Quantitative Approaches for Data Collection

Screening methods are employed to identify and prioritize relevant activities; they are supported by robust quantitative approaches [8]. These approaches involve the use of GHG estimation methodologies to estimate and rank Scope 3 emissions across the value chain. Emissions estimates can be generated using industry average data, environmentally extended input–output data (models used to estimate energy use and/or GHG emissions from upstream supply chain activities of different sectors and products), proxy data, or rough estimates. However, the preferred sources for more accurate estimation include site-specific energy use or emissions data from suppliers and waste management companies and grid-specific transmission and distribution (T&D) loss rates, as they provide a more precise representation of actual emissions [8]. The T&D loss rate refers to the loss of electricity as heat across the network of poles and wires [11].

The T&D loss rate plays a critical role in determining the cost of electricity for consumers and indicates to generators how much power is lost during transportation [11]. These losses are influenced by several factors, including the distance between generators and end users (customers), the voltage and resistance of transmission lines, and the amount of power transmitted through the line. More heavily loaded lines tend to generate more heat, resulting in increased T&D loss [11]. Understanding these dynamics is essential for improving grid efficiency and minimizing energy waste.

Companies can also use financial significance analysis to rank upstream activities based on their economic impacts. For downstream emissions, a company’s revenue can be utilized as a proxy for ranking. However, care must be undertaken to ensure that high-emitting products or services are not overlooked solely due to their lower revenue contribution. It is essential to consider GHG intensity alongside financial metrics to avoid underestimating the environmental impact of such products [8].

In addition to financial criteria, other criteria for selecting which Scope 3 emissions to report on include the degree of influence a company has over an activity, the extent to which an activity increases the company’s risk exposure, the importance of activities deemed critical by stakeholders, and whether the activity meets other materiality thresholds [8]. Moreover, a company may also engage with its customers either directly or through intermediaries, such retailers, marketers, or advertisers, by providing guidance on product use and disposal, educating consumers on efficient use of a product, or encouraging recycling practices as effective strategies to reduce Scope 3 downstream emissions [8].

Primary Data Versus Secondary Data

Primary data, such as supplier-specific data, provide a more accurate representation of a company’s value chain activities. These data enable performance tracking and evaluation of reduction targets and strengthen GHG awareness, transparency, and management throughout the value chain [8]. However, key disadvantages of primary data collection include costs and difficulty relating to verification of data collected by respective value chain partners [8]. Measuring instruments for primary data collection include meter readings, purchase records, utility bills, engineering models, direct monitoring, mass balance, stoichiometry (measurement of elements within a reaction), and other instruments relating to specific activities in the value chain [8].

Secondary data, such as industry averages, can serve as a practical alternative when primary data are not available. These data are particularly useful for estimating emissions from minor activities due to their lower cost and greater accessibility, and they can help engage suppliers operating in emission-intensive hot spots [8]. However, secondary data present several limitations. They may not accurately represent the activities of specific suppliers or account for emission reduction initiatives undertaken by suppliers. Furthermore, they often lack traceability to actions implemented by specific facilities or undertaken by specific partners within the value chain, which could potentially limit their effectiveness in monitoring and tracking progress towards GHG reduction targets [8].

A comprehensive data management plan needs to be developed and implemented for collecting Scope 3 emissions data. Key elements of the data management plan include the following:

- Description of Scope 3 categories and activities included in the Scope 3 inventory.

- Entities responsible for measuring and data collection procedures.

- Data collection procedures.

- Data sources and data quality assessments.

- Calculation methodologies.

- Timeframe for data archiving.

- Data transmission, storage, and back-up procedures;

- Quality control and quality assurance procedures [8].

2.5. Current State of Scope 3 Emissions

Between 1995 and 2015, global Scope 1, 2, and 3 emissions increased by 47%, 78%, and 84%, respectively, reflecting a significant rise in GHG emissions across direct and indirect sources [12]. More broadly, global GHG emissions increased by approximately 51% from 1990 to 2021 [13]. In response, companies worldwide are looking for techniques to decarbonize their global supply chains. Nevertheless, Scope 3 emissions, which refer to indirect emissions across a company’s value chain, remain particularly challenging to address. Due to the complexity and nature of Scope 3 reporting, disclosure remains highly fragmented and is not yet a common practice among most companies. The limited visibility of firms over their value chains and their data collection capacity raise questions about the reliability of indirect emissions inventories and companies’ ability to manage these emissions [14]. This is especially concerning given that Scope 3 emissions can account for up to 70% of a company’s total carbon footprint, making them both significant and difficult to manage [15,16]. While corporate disclosure of Scope 3 emissions has been on the rise, increasing from 50% in 2010 to 56% in 2021, reporting remains highly fragmented and is still not a consistent practice across most companies [17].

Scope 3 emissions related data collection faces multiple challenges, and companies so far have not been able to implement accounting and reporting frameworks specifically for Scope 3 emissions [18,19]. There is a limited amount of Scope 3 emissions reporting, and the majority of it is not assured [18]. Evidence of a lack of capturing of Scope 3 emissions has been found more recently by [20]. A main issue that remains is the lack of coherence in the application of the GHG Protocol by companies.

Key obstacles to effective Scope 3 emissions reporting include lack of data consolidation, limited availability of complex calculative models, inadequate logistics data management, poor supplier collaboration, and the absence of integration of digital tools [21]. This absence also reflects a broader systemic issue in sustainability reporting—namely, the fragmentation of digital infrastructures across organizations and value chains. Many companies still rely on siloed data systems that do not interface seamlessly with one another, making it difficult to trace emissions data across multiple tiers of suppliers, partners, and operational processes [22,23]. This lack of interoperability complicates the task of aggregating, verifying, and analyzing emissions data in real time. Moreover, many small and medium-sized enterprises (SMEs), which make up a significant portion of global supply chains, lack access to sophisticated digital platforms for environmental data tracking. Even when tools exist, they are often underutilized due to high costs, insufficient training, or a lack of alignment with evolving global reporting frameworks, such as the International Financial Reporting Standards (IFRS), the Sustainability Disclosure Standards (ISSB Standards), and the Corporate Sustainability Reporting Directive (CSRD) of the European Union.

Industry perspectives suggest that the absence of scalable, user-friendly digital ecosystems hinders the widespread adoption of sustainability reporting, effective emissions tracking, and assurance practices [22,24,25,26,27]. Academic research not only echoes these concerns but also reveals that digital immaturity in sustainability reporting is not just a technological issue, as it is also underpinned by broader socio-organizational factors. For instance, studies highlight that the lack of integration of digital tools reflects governance gaps, unclear accountability structures, and competing reporting priorities within organizations (e.g., [28,29,30,31,32]). This fragmentation and lack of integration not only impact data accuracy and completeness but also reduce the potential for advanced analytics and predictive insights that could support decarbonization strategies.

It is within this context that artificial intelligence (AI) has been promoted as one of the critical solutions to address weaknesses and gaps associated with sustainability reporting. Nevertheless, associated risks have been identified, such as use of AI for greenwashing purposes [33]. AI is also alleged to be overhyped as a way to support global improvements in sustainability reporting [34]. We further expand on this point by approaching Scope 3 emissions reporting and assurance from the frame of reference of systems thinking and by critically analyzing the limitations of AI (based on its current state) as a facilitator of better-quality Scope 3 emissions reporting. This critical analysis of AI utilization is presented later in the article.

2.6. Scope 3 Emissions Assurance

Assurance promotes confidence that the emissions inventory is complete, accurate, consistent, transparent, relevant, and without material misstatements [8]. Although it is not compulsory, assurance of the Scope 3 inventory serves multiple benefits, including increased confidence in reported information, better-quality internal accounting and reporting practices, improved knowledge transfer, improved efficiency in inventory audit processes, and greater stakeholder confidence in the reported information [8].

Currently, according to the GHG Scope 3 Standard, there is flexibility relating to who can provide the assurance. It can also be undertaken by internal auditors. O’Dwyer [35] points out that sustainability report assurance has received increasing attention by the Big Four professional services firms. Nevertheless, as evidenced by the extensive detail in the Scope 3 standard document, which spans over 150 pages, assurance of Scope 3 emissions data remains a complex and resource-intensive undertaking. Francis [36] found that a typical financial statement audit costs 1/10th of 1 percent of aggregate client sales and that outright audit failures with material economic consequences rarely occur. This might not be the case for sustainability information including Scope 3 emissions data audits, mainly due to the complexity associated with the data. Audits in this domain are likely to be more challenging and resource-intensive than those of traditional financial statements.

Each of the fifteen categories of Scope 3 emissions reporting involves extensive and complex underlying processes, which become increasingly complicated as the boundary/scope of the data coverage increases. In the absence of primary data, there is significant reliance on the use of estimates and industry averages. Griffith et al. [37] have identified audits of estimates as being problematic, especially if the auditor focuses on the management process rather than critical analysis of the overall estimates. Other issues related to the lack of quality assurance may include the failure to detect inconsistencies in estimates, other internal data, or external conditions, as well as overreliance on specialists to identify, evaluate, and challenge the assumptions underlying data [37]. The lack of quality data provided by suppliers has been identified as a critical limitation of the GHG Scope 3 Standard. Scope 3 emissions assurance is still in its very early stage, especially due to its voluntary nature; thus, audit expertise in relation to Scope 3 emissions reporting remains limited.

Another issue contributing to the high risk of low-quality assurance is the lack of auditors’ critical thinking abilities. According to Bucaro [38], complex processes, such as those involved in Scope 3 emissions data capture processes, require thoughtful analysis, research, and inspection. On the contrary, auditors have the habit of making mechanistic audit decisions, frequently relying on a checklist approach and following a series of rules or perceived rules and tick boxes [38]. Bucaro suggests a systems thinking perspective as a means to enhance auditors’ critical thinking, particularly in the context of Scope 3 emissions assurance [38]. Auditors who apply systems thinking are better equipped to recognize the complexity involved in developing accounting estimates and to evaluate associated risks of material misstatements more effectively [38]. System thinking has the potential to give auditors the necessary tools to think more critically and engage in deeper analysis [38].

3. Theoretical Underpinnings of Systems Thinking

Systems thinking has been especially influential in the fields of ecology and management, as well as in areas of systems evaluation, critical systems thinking (CST), and heuristics [39]. In spite of the varied understandings of systems thinking, there are a few common elements. According to Cabrera and Cabrera [39], systems thinking encompasses the following:

- A holistic orientation towards systemic phenomena rather than a focus on constituent parts (reductionism) and the idea of emergence (that the complexity of systems cannot be understood by merely focusing on the physical or tangible parts alone).

- An understanding of complex network structures.

- An understanding of roles of perspectives (mental models) to attain a comprehensive conception of all phenomena.

- An understanding of interrelated phenomena and dynamic relationships of systems and non-linear webs of causality.

- Application of multivariate logic.

Building on this foundation, the systems dynamic approach requires defining problems as they evolve over time, with a focus on system characteristics that contribute to the problem. A system dynamics approach models the system through interconnected feedback loops and non-linear causality; it identifies stocks and flows in the system, and it employs computer-based simulation models to visualize the stocks, flows, and feedback structures of the system [39]. This approach is well-suited for developing a Scope 3 inventory, as it effectively captures the complexity and interconnectivity of value chain elements, along with the multiple stocks and flows involved in the data collection process.

The system dynamics approach emphasizes modeling complex systems through feedback loops, stocks, flows, and simulation, and it largely encompasses a positivist and expert-driven perspective. In contrast, a CST approach requires a departure from this positivist, functionalist “expert” orientation, instead advocating for increasing participation of stakeholders and affected parties [40]. This inclusive orientation aligns with methodological pluralism, which embraces the integration of multiple perspectives and methods [39].

The CST has three fundamental underlying principles. First, critical awareness involves ongoing and repetitive examination of underlying assumptions and contextual origins. Second, emancipation involves evaluating potential improvements over time while accounting for the influence and impacts of power dynamics. Third is methodological pluralism, which is the use of a variety of methods and techniques to assess and analyze complex issues and create a comprehensive understanding of their respective strengths, weaknesses, and associated challenges [41,42,43].

Jackson [44] further elaborates on the pluralist meta-theory, which balances both quantitative modeling and qualitative debate [42]. Quantitative modeling methods typically assume that there is agreement regarding problem definition or goals, whereas qualitative approaches operate under the assumption of disagreements [42]. These approaches need to work in a complementary manner [42]. This approach is particularly relevant in the context of measuring and reporting of Scope 3 emissions. This is referred to as a meta paradigmatic approach [45].

The GHG Protocol highlights that third-party assurance of Scope 3 emissions enhances objectivity, while first-party assurance requires transparent disclosure of potential conflicts of interest and mitigation mechanisms [8]. However, internal disagreements, such as conflicts between management and internal auditors, can hinder transparent debate [46].

The underlying epistemological theory, or theory of knowledge, is referred to as the theory of knowledge of constitutive interests [47]. Jackson’s interpretation of Habermas’ knowledge of constitutive interests within the context of CST highlights two key dimensions: work, focused on technical prediction and control of social phenomena, and interaction, which aims at mutual understanding among stakeholders [47]. Importantly, disagreements between groups may pose challenges or threats to the processes of prediction and control [47].

The framework of constitutive interests not only informs how knowledge is pursued but also highlights the role of social power dynamics in shaping that pursuit. In particular, Habermas emphasizes the necessity of critically analyzing the exercise of power and the historical as well as contemporary social arrangements within which it operates [42,47]. When power is exercised unduly, it can prevent an open, inclusive, and free discussion [47]. Consequently, emancipatory interest becomes essential in situations of constraints imposed by asymmetrical power relations [47].

Hard systems approaches, such as the Scope 3 emissions reporting framework and the use of artificial intelligence (AI) tools, primarily support technical interests. They focus on modeling as the central activity to enable prediction and control of environmental variables [42]. In contrast, soft systems methodologies are oriented towards facilitating and managing debate and dialogue among people, enabling and facilitating learning, critical evaluation of ideas, and collaborative planning. These approaches serve practical interests by fostering mutual understanding. Meanwhile, critical systems heuristics are aligned with emancipatory interests [41], as they aim to subject underlying assumptions in planning processes to ethical critique [42]. They require addressing questions concerning whose views should be considered and how this decision should be made [42]. Ultimately, this heuristic challenges and transforms restrictive power relations with the goal of achieving freedom and emancipatory interest [41]. The CST is inherently dedicated to human emancipation, with the overarching goal of enabling individuals to fully realize their potential by raising quality of life in societies [48]. Emancipation can only be achieved by addressing all three elements: prediction and control, mutual understanding, and freedom from oppressive power relations [48].

Critical awareness is developed through a comprehensive understanding of the strengths and weaknesses of various system methodologies, including their theoretical foundations, techniques and methodologies, application contexts, and possible consequences [45,49]. A critical examination of the assumptions and values embedded in existing systems’ designs or proposed systems’ designs is also important [48].

The GHG Scope 3 Standard emphasizes boundary setting in identifying relevant Scope 3 emissions sources—an essential aspect of systems thinking. The boundary of analysis is crucial [50]. Churchman [50,51] also clarifies that boundaries are constructs and that expanding these boundaries can also entail broadening the scope of who is legitimately included in decision making processes. The process of boundary setting inherently determines what knowledge is considered relevant and whose perspectives are valued. For example, supply chain partners who have a stake become key stakeholders in efforts to improve the overall system [42]. In relation to improvements, Churchman [50] suggests that foundational assumptions, such as those underlying Scope 3 emissions calculations, should be subjected to critiques. The process should be followed by rational argumentation to assess the robustness of the assumptions [42]. Improvements should only be implemented if they withstand this rigorous scrutiny and survive assurance providers’ views [42]. However, the undue exercise of power, particularly by management, can inhibit open and transparent discussion between the assurer and other stakeholders, including management, thereby compromising the integrity of the process [47].

From a Scope 3 emissions reporting perspective, a CST approach, particularly one that includes robust assurance mechanisms for all Scope 3 emissions data, is highly relevant if the data are to meet the qualitative requirements of quality assurance, as identified in the GHG Scope 3 Standard [8].

Key competencies required of assurers, whether internal or external, include expertise in assurance methodologies, experience with assurance frameworks, and proficiency in corporate GHG accounting and/or life cycle assessments (LCAs). Additionally, assurers must be familiar with Scope 3 inventory processes, possess a solid understanding and knowledge of the company’s operations and sectoral contexts, and have the ability to assess emission sources and degrees of potential errors, omissions, and misrepresentations [8]. According to the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD) [8], assurers should demonstrate credibility, independence, and professional skepticism, attributes required to critically evaluate the accuracy and integrity of data and information provided by reporting entities or the company. In this context, a CST approach aligns well with the requirement to exercise professional skepticism.

The main assurance processes outlined by [8] include planning and scoping to determine risks and potential material misstatements, identifying emission sources, performing assurance activities, including evidence gathering, evaluation of results, and determination, and reporting of conclusions. The concept of evidence gathering maps [45,49] as a part of critical awareness promotes a deeper understanding of both strengths and weaknesses in emissions data, particularly regarding the identification of emission sources and the degree of potential errors, omissions, and misrepresentations.

The undertaking of the assurance process prior to public release of the GHG inventory report should allow for identification and correction of material misstatements, as well as overall improvements to the inventory itself [8]. This fits with the concept of qualitative debate [42]. Within the CST approach, the correction of errors can lead towards achieving practical interests and securing mutual understandings among all of those involved [47].

Materiality is an important concept in the context of Scope 3 emissions reporting. According to the GHG Scope 3 Standard, a material misstatement occurs when errors, omissions, or misrepresentations, whether individually or in aggregate, can have a significant impact on the accuracy or credibility of GHG inventory disclosures [8]. Materiality can be defined in both quantitative and qualitative terms. Quantitative materiality is measured as a percentage of the Scope 3 inventory, and appropriate materiality thresholds must be established accordingly [8]. In determining these thresholds, assurers need to consider the likelihood of potential misstatements based on risk assessments and historical patterns of prior misstatements [8]. The process of setting quantitative materiality benchmarks represents what [42] describes as a “hard systems” approach centered on modeling as the central activity, with an emphasis on predictions and technical precision, as also defined in the standard. This approach aims to serve the technical interest and to predict material misstatements by systematically identifying and mitigating the risks of material misstatements in emissions reporting [42].

Qualitative misstatements, while potentially immaterial in quantitative terms, may nonetheless lead to significant impacts on a reporting entity’s emissions in the future [8]. From the perspective of critical systems heuristics [42], the assurer will need to subject its underlying assumptions to ethical critique during the assurance planning process to ensure that independence and objectivity are maintained in the design of the audit. The audit process includes addressing normative questions, such as whose views should be considered, which aligns with a qualitative understanding of materiality [42].

Having established the foundational key concepts of Scope 3 reporting and assurance, the subsequent section discusses AI and analyzes AI tools currently available to support sustainability reporting and assurance. This includes an evaluation of the extent to which these tools are adequate and fit to apply CST. The AI tools assessed were identified through a systematic search using Google search, the predominant search engine globally [52], which has been utilized and cited in a large amount of academic literature as a key platform, especially for problem-specific information seeking and retrieval [53].

4. Artificial Intelligence Applications for Sustainability Reporting and Assurance

Artificial intelligence (AI) is defined as a set of technologies that enable computer systems to perform advanced functions, including large-scale data analysis, predictive simulations, and the generation of actionable feedback and insights, as well as the delivery of data-driven recommendations [54]. These technologies can process and interpret data at a scale and speed that exceed human capabilities. AI technologies typically incorporate machine learning, deep learning, predictive analytics, natural language processing, recommendation algorithms, and intelligent data retrieval [54] that can enhance the accuracy and efficiency of sustainability reporting. Prior studies [55,56,57,58,59,60] have explored and examined the role of such advanced technologies, including advanced big data analytics and artificial intelligence, in promoting, facilitating, and accelerating sustainable development efforts, while related research has emphasized the importance of integrated approaches across accounting, management, and governance in addressing sustainability challenges [61].

A range of ESG platforms have been analyzed to ensure the generalizability of the findings across industries. Top ESG (sustainability management software) providers, such as Key ESG, allow users to select regulation-based sustainability metrics from an extensive database. The software also supports automated data validation, interactive visualizations, and performance tracking [62]. Workiva focuses on processing large and complex ESG datasets, offering automation in both data collection and management, which is particularly valuable in data-intensive industries [62]. SustainIQ provides tracking for over 200 ESG metrics and, while it enables data gathering, it assumes integration with external information system, highlighting a broader challenge of interoperability in ESG software environments [62]. Sector-specific tools also offer insights into how ESG platforms adapt to different operational contexts. Osapiens integrates carbon accounting across the value chain and supports supplier relationship management and procurement auditing, reflecting a deep focus on supply chain transparency [62]. Diligent serves multiple sectors, including healthcare, retail, real estate, and government. In industries with domestic supply chains, such as healthcare and real estate, the usual problem of limited data from developing economies becomes less critical [62]. SAP Sustainability Tower and Sphera emphasize data analytics and full value chain coverage, aiming to deliver measurable results in emissions reductions and compliance outcomes [62]. Meanwhile, Novisto handles complex ESG data infrastructures for regulatory compliance, and Novata targets private equity and venture capital firms, supporting due diligence and investor reporting [62]. Finally, Apiday is explicitly designed for alignment with emerging regulatory frameworks, such as the EU Taxonomy and the CSRD, underscoring the growing role of software in meeting legal ESG obligations [62]. This range of platforms—from generalist tools to sector-specific solutions—demonstrates the functional and contextual diversity of ESG software and provides a more robust foundation for evaluating sustainability management systems. The platforms described below are leading platforms that utilize global reporting frameworks, such as GRI and the United Nations Global Compact [63].

4.1. Sustain.Life (Now Workiva)

Sustain.Life, now acquired by Workiva (Ames, IA, USA), has a comprehensive and extensive emissions factor library, which is integral to the development of an emissions inventory for its clients. In the past, Sustain.Life engaged a software consulting firm to provide independent assurance of the emissions factor library. The purpose of the assurance is to ensure the accuracy and reliability of the emissions factor library [63]. A limited assurance of the emission factors was undertaken, and the outcome was deemed successful. The assurance firm noted that, as with any internal control systems, inherent risk and limitations exist, including the possibility of undetected fraud, errors, or non-compliance. Nevertheless, the firm has affirmed that it undertook rigorous assurance processes and procedures and concluded that there was no evidence of material inaccuracies in the emissions factor dataset [63].

According to Sustain.Life, its products demonstrate potential to facilitate supplier engagement and supply chain decarbonization. Sustain.Life has identified several challenges and complexities related to the capabilities of suppliers to accurately measure and manage their emissions, noting that in many instances, primary emissions data are not available. As a result, representative datasets, such as industry averages, have to be utilized [64]. Furthermore, [64] highlights that requests for emissions-related information from suppliers can strain the relationships if not managed carefully. Hence, the integration of technologies like AI within collaborative platforms, such as Sustain.Life, can promote more cooperative efforts and efficient data sharing.

Manual data collection has proven sub-optimal for many of Sustain.Life’s clients, as it often leads to issues of inconsistency and incomparability [64]. To address these limitations, the platform utilizes AI to access publicly available emissions data, which are data already available in relation to supply chains, and AI is used to automate the extraction of the data. AI can also be used to integrate multiple data sources, such as LCA datasets [64]. AI capabilities also extend to accurately mapping procurement data against relevant GHG Protocol categories, while simultaneously enabling assurance processes through automated data quality check and anomaly detection [64]. Nevertheless, anomaly detection with the use of AI is not explained adequately, including why or how the anomaly has occurred. This limitation is common to many AI anomaly detection methods, which often operate in an unsupervised manner and identify anomalies based on statistical deviations without being able to utilize explicit contextual information. The complexity and high dimensionality of emissions data further complicate interpretation, causing these models to function as “black boxes” that prioritize detection accuracy over explainability [65,66,67,68].

Additional AI-driven functionalities identified by Sustain.Life include automated data requests and data matching, which link uploaded suppliers’ data with entities already captured in the Sustain.Life database [64]. The system also uses AI to scrape sustainability reports and extract relevant information from other publicly available databases. Moreover, AI is also used to develop alternative supplier selection strategies and to establish emissions mitigation pathways based on supplier-specific emissions profiles [64].

4.2. Cority

Cority purports to provide “total impact visibility” [69] and has multiple features, such as the ability to measure air pollutants and GHG emissions through automation. AI utilization is described to promote data extraction from multiple sources, including texts, videos, PDF documents, and social media, as well as data consolidation through natural language processing (NLP)s [62]. High-quality data collection is stressed as an important element. AI is also promoted to provide forecasts based on historical averages and assumptions [62]. Industry averages do not capture the divergence of data. Predictions for non-reporting businesses have high absolute errors, and utilization of machine models cannot improve data accuracy.

4.3. Aryza

Aryza is a U.K.-based consulting firm. Aryza’s ESG platform also provides interactive dashboards, predictive modeling, and automated alerts [70]. The platform has the ability to define business activities by country, business segment, or policy, making it potentially useful for compliance-related applications. However, its reliance on integration with third-party systems presents a significant limitation. In many economically developing countries, such systems are either lacking or underdeveloped, which limits the platform’s applicability in these settings. This raises concerns about design assumptions that may not account for infrastructural disparities across different markets.

For further sustainability reporting, AI-enabled features are defined as below.

- Key ESG

The software allows for selection of regulation-based sustainability metrics from an extensive database. It can also be used to send data requests, and it automates and validates data calculations, produces interactive charts, and allows for target setting and tracking.

- Workiva

The software allows for advanced data processing of large and complex ESG datasets, automating data collection and data management [62].

- SustainIQ

This software, while utilizing the ESG principles, allows for tracking of over 200 metrics [62]. While it allows for gathering of ESG data, the underlying assumption is that the software communicates with other information systems for this purpose.

- Osapiens

This is advanced sustainability management software for businesses to track, analyze, and reduce environmental impacts. It is stated that the software integrates carbon accounting in the entire value chain to manage supplier relationships and for auditing procurement processes [62].

- Diligent

This platform caters to the ESG reporting requirements of multiple industries, including retail, technology, manufacturing, energy, healthcare, real estate, and government [62]. A limited number of these industries, including healthcare and real estate (compared to the construction industry), are domestic-focused value chains, and thus the issue of lack of data from economically developed countries is not relevant.

- SAP Sustainability Tower

This software focuses on data analytics to track the environmental and social impacts of a business [62].

- Sphera

It is stated that this platform allows ESG management tools, which span the entire value chain, to promote “measurable” results for greenhouse gas emissions reduction and environmental compliance [62].

- Novisto

This platform enables handling of complex ESG data infrastructures and compliance with industry regulations [62].

- Novata

This ESG software is focused on private equity and venture capital firms and enables data collection, project management, due diligence, and regulatory compliance [62].

- Apiday

It supports compliance with ESG regulations, including the CSRD and the EU taxonomy [62].

As suggested by the examples of ESG platforms provided above, utilization of AI is currently limited to data extraction, data mining, and analysis, with a heavy reliance on secondary data, such as publicly available data. The underlying assumption is that these software solutions require multiple data sources, including internal systems, external data systems, and manual inputs [62]. The platforms are as effective as the data fed into them. Based on the analysis of ESG platforms, key applications of AI are recapped below.

4.4. AI Applications for Scope 3 Emissions Reporting and Assurance

Key applications of AI, as illustrated in the examples above and including those more broadly relevant to Scope 3 emissions reporting, include the following:

- Web scraping;

- Data integration;

- Data mapping;

- Data matching;

- Data assurance;

- Limited strategizing.

It appears that downstream activities, which are directly related to customers, have not received much attention for estimation of Scope 3 emissions. The following section discusses key applications relevant to Scope 3 emissions reporting.

4.4.1. Web Scraping

The main function of an AI-powered web scraper is to extract data [71]. Compared to traditional web scrapers, AI-based tools offer faster and more effective performance to process websites that rely heavily on JavaSscripts [71]. An AI web scraper can analyze website structure and behavior, and it can identify patterns and extract data even when content is loaded asynchronously [71]. In addition, AI web scraping tools can facilitate automated quality assurance testing, a point further explored and discussed in the later section on AI and assurance [71].

Web scraping, including that conducted AI-based tools, is generally considered legal, but such tools need to comply with relevant laws and regulations [71]. Some AI web scrapers can bypass anti-scraping mechanisms implemented by websites, such as reCAPTCHA and other access controls [71].

Web scraping is increasingly being used to collect sustainability-related industry data and to compare the data with internal datasets [72]. Web scraping can scan and extract publicly available data, such as permits, standards, regulations, policies, guidance materials, and corporate disclosures. In doing so, web scraping can support greater transparency around corporate sustainability performance [72], particularly in relation to Scope 3 emissions disclosures. Additionally, web scraping is being used for supply chain monitoring, enabling the collection of information on suppliers’ and vendors’ sustainability policies and environmental impact, information that can be used to assess supply chain sustainability performance [72].

4.4.2. Data Integration and Data Matching

In addition to web scraping, other AI technologies, such as natural language processing (NLP) and computer vision, can streamline data from multiple sources, such as websites, documents, and multimedia [73]. AI-powered data integration tools automate tasks like data matching, cleansing, and transformation efficiently [74]. These tools can be combined with sensors and Internet of Things (IoT) devices to enhance data collection and integration [74]. Furthermore, AI-enabled tools can be integrated with IoT-based blockchain systems to analyze and match multi-domain data from multiple locations, thereby enabling secure, transparent, and intelligent blockchain-powered solutions for supply chain management [56,75].

AI accelerates each stage of the data integration process, starting with data extraction; advanced AI algorithms analyze the structure and content of various data sources and automatically extract relevant information [74]. AI-powered data integration tools can use machine learning (ML) to adapt to new data sources over time while applying NLP techniques to recognize patterns in language and identify keywords and phrases within unstructured content [74]. Computer vision is utilized to extract data from images and videos [74]. In relation to data quality, AI-powered data integration tools can automatically profile data sources to identify patterns, relationships, and anomalies, as well as automatically correct errors in datasets and perform data cleaning [74].

4.4.3. Data Mapping

Data mapping refers to the process of matching fields from one database with corresponding fields in another [76]. It serves as the preliminary step to facilitate data migration, data integration, and other data management tasks [76]. Data mapping bridges the structural differences between two systems, and it ensures that when data are moved from a source they remain accurate, consistent, and usable at their destination [76]. The complexity of mapping increases with large datasets, such as those related to Scope 3 emissions, thus requiring automated tools [76]. Leveraging the application of ML algorithms, AI-based systems can analyze large volumes of data and generate intelligent mapping suggestions based on historical data, patterns, and relationships [74].

Data warehousing represents one of the most appropriate uses of AI for measuring Scope 3 emissions. It involves pooling data from multiple sources into a central repository for analysis and reporting, where the data have already been migrated, integrated, and transformed [76].

An example of a generative AI-driven data mapping tool is Amazon Connect, which provides customers with data mapping capabilities to support more personalized customer experiences [77]. The primary objective of this tool is to personalize and enhance interactive voice response and chatbots to improve customer satisfaction and AI agents’ productivity [77].

As this example demonstrates, the current use of AI-enabled data mapping remains largely confined to marketing applications. However, there is significant potential to extend these capabilities to sustainability contexts, for instance, to track and capture downstream Scope 3 emissions from downstream transportation and distribution, customers’ processing/use of products, end of life treatment of sold products, as well as emissions from leased assets by the reporting company and emissions relating to franchises and investments. AI-enabled data mapping tools could facilitate the integration and analysis of such data, thereby supporting more accurate and comprehensive Scope 3 emissions reporting.

An example of AI application in Scope 3 emissions measurement is the ENERGY STAR Scope 3 Use of Sold Products Analysis Tool in the United States, which allows retailers to measure and quantify Scope 3 GHG emissions associated with the use of sold products [2]. This tool estimates and quantifies emissions associated with sales of ENERGY STAR-certified products and forecasts potential emissions reductions based on increases in sales of these products. AI-enabled data mapping could serve as an efficient tool to measure emissions related to the use of sold products, a significant component of downstream Scope 3 emissions.

4.4.4. Strategizing

AI, with its advanced and powerful analytical capabilities, can transform data into actionable insights through machine learning, statistical analysis, and optimization [73]. By uncovering patterns, AI can provide actionable recommendations for sustainability improvements, such as optimizing the selection of suppliers [73].

Altman points out that AI tools can help executives in avoiding biases in decision making process while gaining insights from large datasets and supporting ad hoc strategic choices [78]. Altman describes six stages of AI development in strategic contexts, starting with descriptive intelligence, which comprises simple analytics involving the use of dashboards for comparative analysis or performance evaluation using data automatically uploaded and integrated from multiple business departments. The second stage is diagnostic intelligence, which enables the ability to analyze retrospective data to identify and understand performance drivers. The next stage is predictive intelligence, which enables anticipation of future scenarios or options [78]. Diagnostic and predictive intelligence currently represent AI’s most significant contributions, particularly in enhancing analytical efficiency, although these stages require human involvement [79]. Fully autonomous AI decision making without human interaction remains unrealized [79].

Regarding AI’s predictive capabilities, they might not be very accurate in highly volatile and vulnerable environments susceptible to external events [79], such as forecasting future Scope 3 emissions in supply chains, which might be impacted by multiple external factors, including the environmental policies of the relevant jurisdictions. In relation to bias, Atsmon [79] points out that AI can identify situations prone to inherent biases, including, for example, situations where there is a lack of a critical voice against leadership choices, which may potentially perpetuate business-as-usual practices. Another benefit of AI-enabled analysis is to reduce confirmation bias [79] by introducing greater objectivity in the decision making process. Real-time AI assurance can detect data anomalies and prevent data manipulation, thereby enhancing the integrity of the decision making process [79].

In the context of measuring and reporting Scope 3 emissions, the objectivity AI provides in supplier selection is both notable and valuable. Without the availability of upstream data, in spite of the utilization of AI, there is a high risk that managers may fail to undertake required changes in suppliers’ choices due to inadequate awareness and insufficient understanding of high-level upstream emissions related to purchases from certain suppliers. Prior research has documented evidence of management bias; for example, procurement managers have been found to prioritize low-cost sourcing regions without adequate consideration of other factors [80,81]. This suggests that sustainability criteria are often excluded from the procurement decision making process. AI-system-enabled sustainability-related criteria assessments can be effective if systematic changes are implemented and driven by government pressure for data in economically developing countries, where the majority of manufacturing occurs.

AI can facilitate partnerships for generating more inclusive data with the private sector [82]. Data engineering, understood as the monitoring of emissions, can be enhanced through AI-powered data engineering tools that automatically track carbon emissions and footprints [83]. The process of automation involves collecting data from operational activities, such as corporate travel, and across the entire value chain, including suppliers, transporters, and downstream use of the company’s products [83]. Predictive AI models can be used to forecast future emissions based on current reduction initiatives, new carbon reduction methodologies, and anticipated future demand, thereby facilitating the setting, adjustment, and achievement of reduction targets [83]. On the other hand, prescriptive AI can help improve efficiency in production and transportation, thus promoting reduced carbon emissions [83]. If AI is embedded in national collaborative systems (networks), which also involve partnerships between government departments and the private sector (business), then more comprehensive data can be generated for carbon emission monitoring purposes.

4.4.5. AI for Data Assurance

As identified earlier in the article, assurance by third-party assurance providers, such as audit firms, is potentially problematic due to the complex nature of data and potential power relationships between businesses and assurance providers. We therefore propose that assurance of carbon emissions data can be better provided by government bodies specifically set up for the purpose of business carbon emissions assurance. Multiple departments, for example, specifically relating to each SDG can be set up within the Auditor General’s office. In the context of assurance, AI offers limited capabilities, such as automating audit data collection tasks [84]. Through the analysis of information, the technology learns to improve judgements and problem solving in subsequent tasks, a process called machine learning (ML) [84]. Critical thinking, which involves emancipation, repetitive interactions with stakeholders, and handling of power relationships to ensure quality audits, are not current features of AI-enabled assurance tools.

AI can support the collection of quality Scope 3 emissions data. Data quality encompasses attributes like accuracy, completeness, consistency, reliability, and validity [85]. It is an important aspect of advanced data analytics and fundamental to an organization’s data governance strategy and framework [85]. AI contributes to data quality assurance by automating data cleaning processes and detecting and correcting errors within large datasets [85]. Techniques like ML and NLP further enhance data precision and the efficiency of data cleaning, thereby supporting more precise analytics and informed decision making [85]. At best, AI can identify gaps in relation to supply chains and upstream and downstream carbon emissions data, or it can identify anomalies in data that might suggest a lack of data reliability.

Regarding specific audit functions, AI can facilitate processes like sampling, identification of outliers, detection of patterns and trends, and improved risk management by harnessing audit intelligence and machine learning techniques to generate high-risk samples for detailed analysis [86]. From an assurance perspective, these high-risk samples, with missing data or abnormal performance data, can lead to limited assurance and qualified opinions (which refers to material issues within the assured data).

The key issues with conventional auditing methods include time-consuming manual processes and high risk of errors [87]. The integration of advanced AI technologies into the audit engagement management process thus streamlines and simplifies audit analysis and increases efficiency [87]. AI-enabled audit technologies enable the examination of all transactions, allowing auditors to focus on high-risk areas. These tools can improve audit quality by identifying unusual transactions, providing streamlined access to relevant documentation, and enabling customization of techniques and criteria specific to each engagement [87]. They also enable easy access to client data and automate critical audit processes, such as the generation of working papers [87].

A significant beneficial feature of AI-enabled audit technologies lies in their sophisticated algorithms that identify risks, facilitate better understanding of data, and contribute to more accurate and efficient audits, as well as allowing auditors to allocate more time towards strategic planning [87]. AI-enabled technologies continuously improve as they process increasing volumes of data, further enhancing effectiveness [87].

AI’s capability to process large volumes of data and reconcile accounts [84] is particularly useful in the context of Scope 3 emissions, which involves multiple and distributed data sources across the value chain. Auditors (assurance providers) can leverage AI technology to request and analyze complete datasets, enabling them to refine the audit’s scope and focus on actual high-risk elements [84].

However, one of the issues raised by assurance providers regarding the use of AI is cost [84]. It has been suggested that these costs should be passed on to the client. The potential for increased fees or the refusal of an assurance provider to undertake an engagement may motivate clients to standardize their data collection process, potentially through the use of AI, to ensure the collection of relevant and high-quality data [87]. Thus, the government serving as an assurance provider is potentially a better option. Governments can push businesses to collect upstream and downstream carbon emissions data.

Use of AI for Scope 3 emissions assurance is still in its infancy. As identified in this section and as Kokina et al. [88] found with financial statement audits, current applications are limited to basic AI technologies. Current applications include data extraction from documents and automation of repetitive tasks, while more complex and advanced AI tools for assurance purposes are still under development. Robotic process automation (RPA) facilitates data-oriented processes, such as the automation of evidence collection, automated report generation, the aggregation of data and evidence from multiple sources, and the execution of tests [88]. When RPA is combined with ML, this approach is referred to as intelligent automation [88].

As highlighted in this section, the theoretical concepts mentioned earlier, including critical awareness, analysis of complex issues, understandings of social power dynamics, and provision of critiques, are not currently possible solely by utilizing AI. AI, in its current state, is being used for data extraction, identification of patterns and anomalies, and to create interactive platforms and chatbots. Human intervention remains necessary to undertake analyses of complex data, interpret nuanced contexts, and make informed decisions that AI alone cannot fully address. Human interactions are required to question clients regarding gaps in data, such as those relating to upstream (purchase) activities. There are severe limitations regarding data availability, especially from economically developing countries, where more than 50% of global manufacturing takes place. These regions do not have adequate infrastructure in place to allow for accurate data collection, data analysis, data assurance, or utilization of AI to enhance the integrity of Scope 3 emissions reporting. Several initiatives are underway to address these challenges, such as the United Nations Environment Programme’s Initiative for Climate Action Transparency (ICAT) [89], which provides technical assistance and capacity building, and digital traceability platforms like KOLTIVA [90] that combine monitoring with on-the-ground verification.

Our data gathering exercise through the market leader search engine, Google, confirmed what has been identified in this section and earlier by sustainability reporting platforms, including Sustain.Life, that sustainability reporting on Scope 3 emissions is generated based on secondary data, especially industry averages. Thus, assurance of Scope 3 GHG emissions reporting is also purported to be undertaken with secondary data. It has also been established earlier in the article that secondary data, especially industry averages, are not an accurate source of data. Thus, the lack of availability of primary data, especially in economically developing countries, acts as a main barrier to critically engaged assurance. Governments need to play a more active role in requiring carbon emissions data from businesses, applying a system-based approach for carbon emissions monitoring and reporting, and acting as carbon emissions (reporting) assurers. By implementing this approach, with the utilization of AI to handle complex data, governments would be able to improve national-level reporting and undertake more impactful stakeholder engagement for SDG implementation.

4.5. Upstream Scope 3 Emissions: AI Resource Consumption

Despite the significant benefits that AI offers for Scope 3 emissions management and reporting, it also presents some negative effects, but these can be addressed. Exponential growth of artificial intelligence applications has led to massive increases in energy consumption and associated carbon emissions, mainly due to the intensive computational demands of AI processes [91,92]. Deep learning models, in particular, require even greater computational resources, which are provided by AI-enabled data centers with high-performance servers and cooling systems [91]. The continuous processes of training, inference, and optimization within AI systems result in prolonged utilization of server infrastructure and increased electricity consumption and carbon emissions [91]. For entities utilizing AI technologies, a significant portion of Scope 3 emissions can be traced to the data centers and server infrastructure that support these AI applications [92].

Mitigating these emissions involves several strategic approaches. One is engaging with server suppliers to assess and understand their energy sources, infrastructure efficiency, and overall carbon footprint, encouraging the adoption of energy-efficient technologies and renewable energy [91]. Another approach is to undertake LCAs of server infrastructure to identify inefficiencies and emission hotspots and impacts throughout the hardware life cycle, including production, data centers’ operations, and end of life disposal, thereby recognizing opportunities for optimization and emissions reduction [91]. In addition, stakeholders can also put pressure on server companies to invest in renewable energy and carbon offsetting initiatives [91]. Governments are well-positioned not only to implement renewable energy projects but also to support AI-enabled data gathering, monitoring, and assurance.

5. Critical Discussion

This article has provided a comprehensive understanding of the network structure requirements relating to GHG Scope 3 emissions according to the Standard [39]. It started with a simplified explanation of the GHG Scope 3 emissions Standard, emphasizing the interrelated phenomena and processes [39] within the value chains. Scope 3 emissions encompass both upstream and downstream activities; however, to date, downstream activities have received comparatively less attention than upstream suppliers’ related activities. Nevertheless, data related to upstream activities are also limited, largely due to the unavailability of data from regions where most manufacturing takes place.

Adopting a systems approach requires clear problem identification [39], which in this instance relates to the challenge of achieving accurate and transparent reporting of Scope 3 emissions [8]. Such accuracy and transparency is important, as both social and environmental impacts are increasingly central to corporate social responsibility (CSR) (sustainability) reporting [93,94]. From this perspective, the GHG Protocol currently focuses on emissions and does not extend to capture broader social and environmental impacts. Nevertheless, recent developments, such as forthcoming IFRS and GRI reporting, are expected to expand sustainability reporting to include topics like biodiversity, water, human capital, and social issues [95,96]. Similarly, the European Sustainability Reporting Standards (ESRS), based on double materiality, require disclosures of both environmental metrics and social impacts, such as workforce reskilling and community effects related to climate transition plans [97,98]. While these developments may not alter the GHG Protocol directly, they will complement it by broadening the scope of sustainability reporting. Accurately measuring, accounting, and reporting Scope 3 emissions hold immense potential to provide information about the complex interconnections between environmental impacts and humans systems, including businesses [99]. As highlighted in the context of the Anthropocene, environmental changes, partially driven by Scope 3 emissions, both influence and are influenced by social and economic systems [99].

The complexity of Scope 3 emissions measurement, reporting, and assurance stems from the networked nature of value chains and the demand for detailed, often complicated or obscure information that needs to be better connected to global environmental changes [99,100]. Addressing this complexity requires careful setting of analytical boundaries and specific determination of the scope and boundary of material considerations relevant to Scope 3 emissions [50]. Accounting, understood as both measurement and reporting, serves an important function of integrating internal and external entities, even as organizational fragmentation persists [101].

Setting the boundary of materiality is a rational approach, as it helps specify which transactions and activities should be governed [101]. The formation of such boundaries inherently implies the design of governance to align activities with adequate structural forms [101]. Inter-firm planning becomes essential when activities between firms are either complementary (inter-dependent) or dissimilar in nature or when capabilities are distributed across firms or in separate firms [101]. In this context, the application of AI for Scope 3 emissions measurement and reporting, both within and across firms, has the potential to promote better governance of transactions and activities. AI can facilitate the identification and coordination of material, interdependent, and heterogeneous activities, thereby acting as an adequate structural form for Scope 3 emissions reporting [101]. Nevertheless, significant challenges arise in supply chains, particularly in upstream activities relating to purchases from economically developing countries, as well as in downstream activities, such as waste tracing after product use and other related processes. A critical assumption in leveraging AI for these purposes is the availability of primary data to ensure quality reporting and assurance. However, in many cases, such primary data are missing. The CDP reports that nearly 60% of companies globally either failed to disclose or provided minimal information on their supply chain Scope 3 emissions in recent reporting cycles [102]. Initiatives like the Science-Based Targets Initiative (SBTi) and the UNEP Finance Initiative further emphasize the ongoing disclosure challenges in developing regions, where limited access to data, complex supply chains, and institutional constraints hinder accurate reporting. The probability of complexities relating to data collection on energy consumption by suppliers, relating, for example, to T&D loss, and thus the absence of such data, especially for the large number of SME suppliers, is also very high.

While more than 50% of global manufacturing occurs in economically developing countries, sustainability reporting in these regions remains limited. According to CDP, nearly 60% of companies globally did not disclose any supply chain (Scope 3) emissions category in their recent reporting cycles [102]. Reports from initiatives like the Science-Based Targets Initiative (SBTi) [103] and the UNEP Finance Initiative [104] further highlight that companies in many developing regions, including Africa, face persistent challenges with Scope 3 reporting due to data unavailability, complex supply chains, and limited institutional capacity. These gaps in primary emissions data significantly restrain the effective application of AI, even for the rudimentary purpose of data extraction and analysis.