Sustainability Reporting as a Governance Tool for Sustainable Development Goals (SDGs): A Bibliometric and Content Analysis

Abstract

1. Introduction

2. Methodology

2.1. Data Extraction and Inclusion and Exclusion Criteria

2.2. Data Analysis

3. Findings

3.1. Publication Trend

3.2. Most Impactful Publications and Authors Based on Citations

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Article | Source | Article Title | Citation |

|---|---|---|---|

| [26] | Journal of Cleaner Production | Addressing the SDGs in sustainability reports: The relationship with institutional factors | 428 |

| [27] | Corporate Social Responsibility and Environmental Management | Business contribution to the Sustainable Development Agenda: Organizational factors related to early adoption of SDG reporting | 209 |

| [32] | Corporate Social Responsibility and Environmental Management | New challenges for corporate sustainability reporting: United Nations’ 2030 Agenda for Sustainable Development and the Sustainable Development Goals | 129 |

| [30] | Accounting, Auditing & Accountability Journal | Conceptualizing the contemporary corporate value creation process | 387 |

| [33] | Journal of Cleaner Production | Corporate involvement in sustainable development goals: Exploring the territory | 92 |

| [34] | Finance and Credit | The role of accounting in providing sustainable development and national safety of Ukraine | 54 |

| [28] | Business Strategy and the Environment | Do institutional investors drive corporate transparency regarding business contribution to sustainable development goals? | 61 |

| [35] | Sustainability | Mapping the sustainable development goals relationships | 112 |

| [29] | Journal of Cleaner Production | “Sell” recommendations by analysts in response to business communication strategies concerning the Sustainable Development Goals and the SDG compass. | 47 |

| [31] | Sustainability | The challenge of sustainable development goal reporting: The first evidence from Italian-listed companies | 67 |

3.3. Most Significant Sources and Publishers

3.4. Country Collaborations

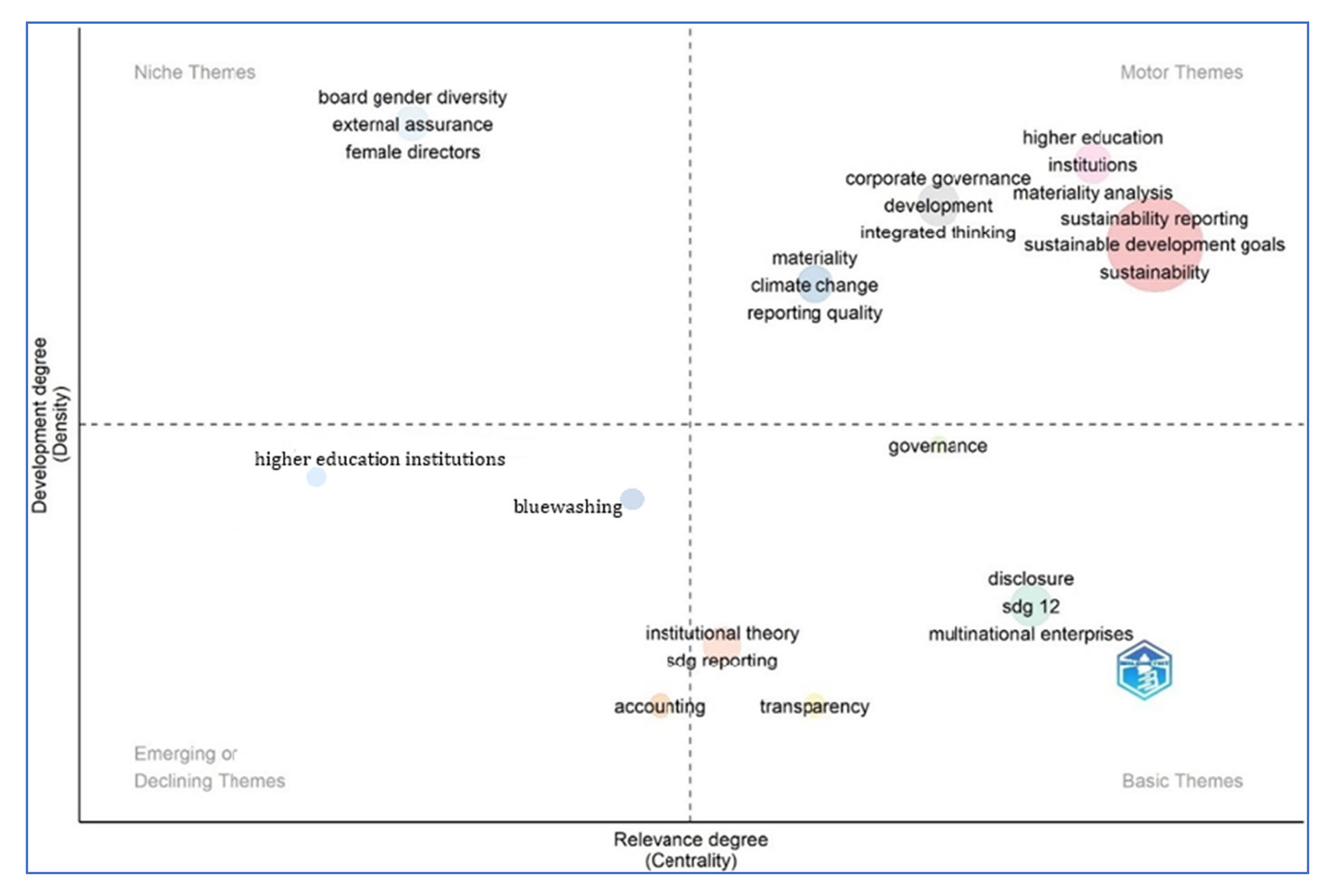

3.5. Thematic Map

- (1)

- The motor theme—high centrality and density, in the upper right quadrant;

- (2)

- The core theme—low density but high centrality, in the lower right quadrant;

- (3)

- The niche theme—high density but low centrality, in the upper left quadrants;

- (4)

- The emerging or disappearing theme—low density and centrality, in the bottom left quadrant.

3.6. Network Visualization—Critical Analysis of Key Themes

3.6.1. Sustainability Reporting as a Governance Mechanism

3.6.2. The Intersection of Sustainable Development Goals (SDGs) and Corporate Sustainability

3.6.3. The Performance-Accountability Paradox in Sustainability Disclosure

- (1)

- Comparative studies between emerging and developed countries on the mechanisms used to integrate SDGs into companies’ strategic plans and how effectively it is reported. The results could shed light on the possibilities of sustainability reporting acting as a governance tool across diverse markets.

- (2)

- Studies on how artificial intelligence, big data analytics, and machine learning could be leveraged to enhance the availability and accuracy of sustainability reporting and the challenges faced throughout the supply chain. This could facilitate corporate sustainability efforts and alignment with the SDGs.

- (3)

- Examine how cultural norms, diversity, equity, and inclusion (DEI) across different economies shape the integration of SDGs into their strategic planning framework and what governance mechanisms are set in place to ensure the execution of such plans and their eventual sustainability reporting.

- (4)

- Identify industry-specific challenges companies face when integrating SDGs within organizational frameworks and sustainability reporting in different economic contexts.

- (5)

- Determine factors contributing to greenwashing in sustainability reporting in different industries, economic contexts, and cultural settings, and propose strategies to mitigate such circumstances.

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Awuah, B.; Yazdifar, H.; Elbardan, H. Corporate reporting on the Sustainable Development Goals: A structured literature review and research agenda. J. Account. Organ. Change 2024, 20, 617–646. [Google Scholar] [CrossRef]

- Guarini, E.; Mori, E.; Zuffada, E. Localizing the Sustainable Development Goals: A managerial perspective. J. Public Budg. Account. Financ. Manag. 2022, 34, 583–601. [Google Scholar] [CrossRef]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development. 2015. Available online: https://sdgs.un.org/ (accessed on 16 May 2025).

- Zyznarska-Dworczak, B. Corporate governance in ensuring the quality of financial and sustainability reporting in times of uncertainty. Theor. J. Account. 2023, 47, 99–119. [Google Scholar] [CrossRef]

- Rizzato, F.; Tonelli, A.; Fiandrino, S.; Devalle, A. Analysing SDG disclosure and its impact on integrated thinking and reporting. Meditari Account. Res. 2024, 32, 803–831. [Google Scholar] [CrossRef]

- Diab, A.; Eissa, A.M. ESG performance, auditor choice, and audit opinion: Evidence from an emerging market. Sustainability 2023, 16, 124. [Google Scholar] [CrossRef]

- Shahrour, M.H.; Arouri, M.; Rao, S. Linking Climate Risk to Credit Risk: Evidence from Sectorial Analysis. J. Altern. Invest. 2024, 27, 118–135. [Google Scholar] [CrossRef]

- Moussa, A.S.; Elmarzouky, M. Sustainability reporting and market uncertainty: The moderating effect of carbon disclosure. Sustainability 2024, 16, 5290. [Google Scholar] [CrossRef]

- Wang, Y.; Lu, Y.; He, G.; Wang, C.; Yuan, J.; Cao, X. Spatial variability of sustainable development goals in China: A provincial level evaluation. Environ. Dev. 2020, 35, 100483. [Google Scholar] [CrossRef]

- Moussa, A.S.; Elmarzouky, M.; Shohaieb, D. Green Governance: How ESG Initiatives Drive Financial Performance in UK Firms? Sustainability 2024, 16, 10894. [Google Scholar] [CrossRef]

- Idowu, S.O.; Dragu, I.M.; Tiron-Tudor, A.; Farcas, T.V. From CSR and sustainability to integrated reporting. Int. J. Soc. Entrep. Innov. 2016, 4, 134–151. [Google Scholar] [CrossRef]

- Permatasari, I.; Tjahjadi, B. A closer look at integrated reporting quality: A systematic review and agenda of future research. Meditari Account. Res. 2024, 32, 661–692. [Google Scholar] [CrossRef]

- Turzo, T.; Marzi, G.; Favino, C.; Terzani, S. Non-financial reporting research and practice: Lessons from the last decade. J. Clean. Prod. 2022, 345, 131154. [Google Scholar] [CrossRef]

- Sarkar, S.; Moolearambil Sukumaran Nair, M.; Datta, A. Role of Environmental, Social, and Governance in achieving the UN Sustainable Development Goals: A special focus on India. Environ. Prog. Sustain. Energy 2023, 42, e14204. [Google Scholar] [CrossRef]

- Raman, R.; Nair, V.K.; Shivdas, A.; Bhukya, R.; Viswanathan, P.K.; Subramaniam, N.; Nedungadi, P. Mapping sustainability reporting research with the UN’s sustainable development goal. Heliyon 2023, 9, e18510. [Google Scholar] [CrossRef]

- Effah, N.A.A.; Wang, Q.; Owusu, G.M.Y.; Otchere, O.A.S.; Owusu, B. Contributions toward sustainable development: A bibliometric analysis of sustainability reporting research. Environ. Sci. Pollut. Res. 2023, 30, 104–126. [Google Scholar] [CrossRef]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E.; et al. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 2021, 372, n71. [Google Scholar] [CrossRef]

- Ansari, Y.; Arwab, M.; Subhan, M.; Alam, M.S.; Hashmi, N.I.; Hisam, M.W.; Zameer, M.N. Modeling socio-economic consequences of COVID-19: An evidence from bibliometric analysis. Front. Environ. Sci. 2022, 10, 941187. [Google Scholar] [CrossRef]

- Ejaz, H.; Zeeshan, H.M.; Ahmad, F.; Bukhari, S.N.A.; Anwar, N.; Alanazi, A.; Sadiq, A.; Junaid, K.; Atif, M.; Abosalif, K.O.A.; et al. Bibliometric analysis of publications on the omicron variant from 2020 to 2022 in the Scopus database using R and VOSviewer. Int. J. Environ. Res. Public Health 2022, 19, 12407. [Google Scholar] [CrossRef]

- Khan, O.; Daddi, T.; Iraldo, F. The role of dynamic capabilities in circular economy implementation and performance of companies. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 3018–3033. [Google Scholar] [CrossRef]

- Dumay, J.; Bernardi, C.; Guthrie, J.; Demartini, P. Integrated reporting: A structured literature review. Account. Forum 2016, 40, 166–185. [Google Scholar] [CrossRef]

- Aria, M.; Cuccurullo, C. bibliometrix: An R-tool for comprehensive science mapping analysis. J. Informetr. 2017, 11, 959–975. [Google Scholar] [CrossRef]

- Van Eck, N.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [PubMed]

- Cobo, M.J.; Martínez, M.A.; Gutiérrez-Salcedo, M.; Fujita, H.; Herrera-Viedma, E. 25 years at knowledge-based systems: A bibliometric analysis. Knowl.-Based Syst. 2015, 80, 3–13. [Google Scholar] [CrossRef]

- Bellucci, M.; Marzi, G.; Orlando, B.; Ciampi, F. Journal of Intellectual Capital: A review of emerging themes and future trends. J. Intellect. Cap. 2021, 22, 744–767. [Google Scholar] [CrossRef]

- Rosati, F.; Faria, L.G. Addressing the SDGs in sustainability reports: The relationship with institutional factors. J. Clean. Prod. 2019, 215, 1312–1326. [Google Scholar] [CrossRef]

- Rosati, F.; Faria, L.G.D. Business contribution to the Sustainable Development Agenda: Organizational factors related to early adoption of SDG reporting. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 588–597. [Google Scholar] [CrossRef]

- Garcia-Sanchez, I.M.; Aibar-Guzmán, B.; Aibar-Guzmán, C.; Rodriguez-Ariza, L. “Sell” recommendations by analysts in response to business communication strategies concerning the Sustainable Development Goals and the SDG compass. J. Clean. Prod. 2020, 255, 120194. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Rodríguez-Ariza, L.; Aibar-Guzmán, B.; Aibar-Guzmán, C. Do institutional investors drive corporate transparency regarding business contribution to the sustainable development goals? Bus. Strategy Environ. 2020, 29, 2019–2036. [Google Scholar] [CrossRef]

- Adams, C.A. The Sustainable Development Goals, Integrated Thinking and the Integrated Report; ICAEW Thought Leadership: London, UK, 2017. [Google Scholar]

- Izzo, M.F.; Ciaburri, M.; Tiscini, R. The challenge of sustainable development goal reporting: The first evidence from Italian listed companies. Sustainability 2020, 12, 3494. [Google Scholar] [CrossRef]

- Tsalis, T.A.; Malamateniou, K.E.; Koulouriotis, D.; Nikolaou, I.E. New challenges for corporate sustainability reporting: United Nations’ 2030 Agenda for sustainable development and the sustainable development goals. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1617–1629. [Google Scholar] [CrossRef]

- Van der Waal, J.W.; Thijssens, T. Corporate involvement in sustainable development goals: Exploring the territory. J. Clean. Prod. 2020, 252, 119625. [Google Scholar] [CrossRef]

- Akimova, L.M.; Levytska, S.O.; Pavlov, K.V.; Kupchak, V.R.; Karpa, M.I. The role of accounting in providing sustainable development and national safety of Ukraine. Financ. Credit Act. Probl. Theory Pract. 2019, 3, 54–61. [Google Scholar] [CrossRef]

- Fonseca, L.; Carvalho, F. The reporting of SDGs by quality, environmental, and occupational health and safety-certified organizations. Sustainability 2019, 11, 5797. [Google Scholar] [CrossRef]

- Rao, P.K.; Shukla, A. Sustainable strategic management: A bibliometric analysis. Bus. Strategy Environ. 2023, 32, 3902–3914. [Google Scholar] [CrossRef]

- Callon, M.; Courtial, J.P.; Turner, W.A.; Bauin, S. From translations to problematic networks: An introduction to co-word analysis. Soc. Sci. Inf. 1983, 22, 191–235. [Google Scholar] [CrossRef]

- Adams, C.A. The ethical, social and environmental reporting-performance portrayal gap. Account. Audit. Account. J. 2004, 17, 731–757. [Google Scholar] [CrossRef]

- Kolk, A. Trajectories of sustainability reporting by MNCs. J. World Bus. 2010, 45, 367–374. [Google Scholar] [CrossRef]

- Milne, M.J.; Gray, R. W(h)ither ecology? The triple bottom line, the Global Reporting Initiative, and corporate sustainability reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Sundarasen, S.; Zyznarska-Dworczak, B.; Goel, S. Sustainability reporting and greenwashing: A bibliometrics assessment in G7 and non-G7 nations. Cogent Bus. Manag. 2024, 11, 2320812. [Google Scholar] [CrossRef]

- Lyon, T.P.; Montgomery, A.W. The means and ends of greenwash. Organ. Environ. 2015, 28, 223–249. [Google Scholar] [CrossRef]

- Boiral, O. Sustainability reports as simulacra? A counter-account of A and A+ GRI reports. Account. Audit. Account. J. 2013, 26, 1036–1071. [Google Scholar] [CrossRef]

- Cho, C.H.; Laine, M.; Roberts, R.W.; Rodrigue, M. Organized hypocrisy, organizational façades, and sustainability reporting. Account. Organ. Soc. 2015, 40, 78–94. [Google Scholar] [CrossRef]

- Lozano, R. A holistic perspective on corporate sustainability drivers. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 32–44. [Google Scholar] [CrossRef]

- Dyllick, T.; Muff, K. Clarifying the meaning of sustainable business: Introducing a typology from business-as-usual to true business sustainability. Organ. Environ. 2016, 29, 156–174. [Google Scholar] [CrossRef]

- European Commission. Corporate Sustainability Reporting Directive (CSRD). 2022. Available online: https://ec.europa.eu/ (accessed on 12 January 2025).

- Spangenberg, J.H. Hot air or comprehensive progress? A critical assessment of the SDGs. Sustain. Dev. 2017, 25, 311–321. [Google Scholar] [CrossRef]

- Bebbington, J.; Unerman, J. Achieving the United Nations Sustainable Development Goals: An enabling role for accounting research. Account. Audit. Account. J. 2018, 31, 2–24. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The impact of corporate sustainability on organizational processes and performance. Manag. Sci. 2012, 60, 2835–2857. [Google Scholar] [CrossRef]

- Hahn, T.; Figge, F.; Pinkse, J.; Preuss, L. A paradox perspective on corporate sustainability. Organ. Stud. 2014, 35, 697–727. [Google Scholar]

- Stubbs, W.; Higgins, C. Integrated reporting and internal mechanisms of change. Account. Audit. Account. J. 2014, 27, 1068–1089. [Google Scholar] [CrossRef]

- Andrew, J.; Cortese, C. Accounting for climate change and the self-regulation of carbon disclosures. Account. Forum 2011, 35, 130–138. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Gray, R.; Owen, D.; Adams, C. Accounting & Accountability: Changes and Challenges in Corporate Social and Environmental Reporting; Prentice Hall: London, UK, 1996. [Google Scholar]

- Deegan, C. Introduction: The legitimizing effect of social and environmental disclosures–a theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

| Sources | ABDC Ranking | ABS Ranking | SJR Ranking | Publisher |

|---|---|---|---|---|

| Journal of Cleaner Production | A | 3* | Q1 | Elsevier (Amsterdam, The Netherlands) |

| Journal of Business Ethics | A | 3* | Q1 | Springer (Berlin/Heidelberg, Germany) |

| Corporate Social Responsibility and Environmental Management | B | 2* | Q1 | Wiley-Blackwell Publishing (Hoboken, NJ, USA) |

| Accounting, Auditing and Accountability Journal | A | 3* | Q1 | Emerald Group Publishing Ltd. (Leeds, UK) |

| Sustainability | - | - | Q2 | MDPI (Basel, Switzerland) |

| Business Strategy and the Environment | B | 3* | Q1 | Wiley-Blackwell Publishing |

| Sustainability Accounting, Management and Policy Journal | C | - | Q2 | Emerald Group Publishing Ltd. |

| Accounting, Organizations, and Society | A* | 4* | Q1 | Elsevier Ltd. |

| Academy of Management Review | A* | 4* | Q1 | Academy of Management (Valhalla, NY, USA) |

| Meditari Accountancy Research | A | 1* | Q1 | Emerald Group Publishing Ltd. |

| Critical Perspectives on Accounting | A | 3* | Q1 | Emerald Group Publishing Ltd. |

| Accounting Forum | B | 3* | Q2 | Emerald Group Publishing Ltd. |

| Country | Total Citations | Average Article Citations | Country | Total Citations | Average Article Citations |

|---|---|---|---|---|---|

| USA | 1662 | 20.02 | Canada | 295 | 12.83 |

| Spain | 1544 | 11.35 | Brazil | 271 | 8.21 |

| Italy | 971 | 13.87 | Romania | 269 | 8.97 |

| China | 658 | 10.12 | Belgium | 268 | 38.29 |

| Australia | 656 | 17.26 | Switzerland | 251 | 22.82 |

| The Netherlands | 641 | 35.61 | Austria | 249 | 19.15 |

| Germany | 583 | 17.15 | Ireland | 245 | 24.50 |

| France | 519 | 37.07 | India | 236 | 6.21 |

| Sweden | 335 | 20.94 | Denmark | 224 | 20.36 |

| Japan | 296 | 29.60 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sundarasen, S.; Rajagopalan, U.; Zyznarska-Dworczak, B. Sustainability Reporting as a Governance Tool for Sustainable Development Goals (SDGs): A Bibliometric and Content Analysis. Sustainability 2025, 17, 4784. https://doi.org/10.3390/su17114784

Sundarasen S, Rajagopalan U, Zyznarska-Dworczak B. Sustainability Reporting as a Governance Tool for Sustainable Development Goals (SDGs): A Bibliometric and Content Analysis. Sustainability. 2025; 17(11):4784. https://doi.org/10.3390/su17114784

Chicago/Turabian StyleSundarasen, Sheela, Usha Rajagopalan, and Beata Zyznarska-Dworczak. 2025. "Sustainability Reporting as a Governance Tool for Sustainable Development Goals (SDGs): A Bibliometric and Content Analysis" Sustainability 17, no. 11: 4784. https://doi.org/10.3390/su17114784

APA StyleSundarasen, S., Rajagopalan, U., & Zyznarska-Dworczak, B. (2025). Sustainability Reporting as a Governance Tool for Sustainable Development Goals (SDGs): A Bibliometric and Content Analysis. Sustainability, 17(11), 4784. https://doi.org/10.3390/su17114784