Intermediate Effect of the COVID-19 Pandemic on Prices of Housing near Light Rail Transit: A Case Study of the Portland Metropolitan Area

Abstract

:1. Introduction

2. Literature Review

2.1. Property Value Premium

2.2. Impacts of COVID-19 Pandemic

2.2.1. Transit Ridership

2.2.2. Real Estate Market

2.3. Research Gaps

3. Research Design

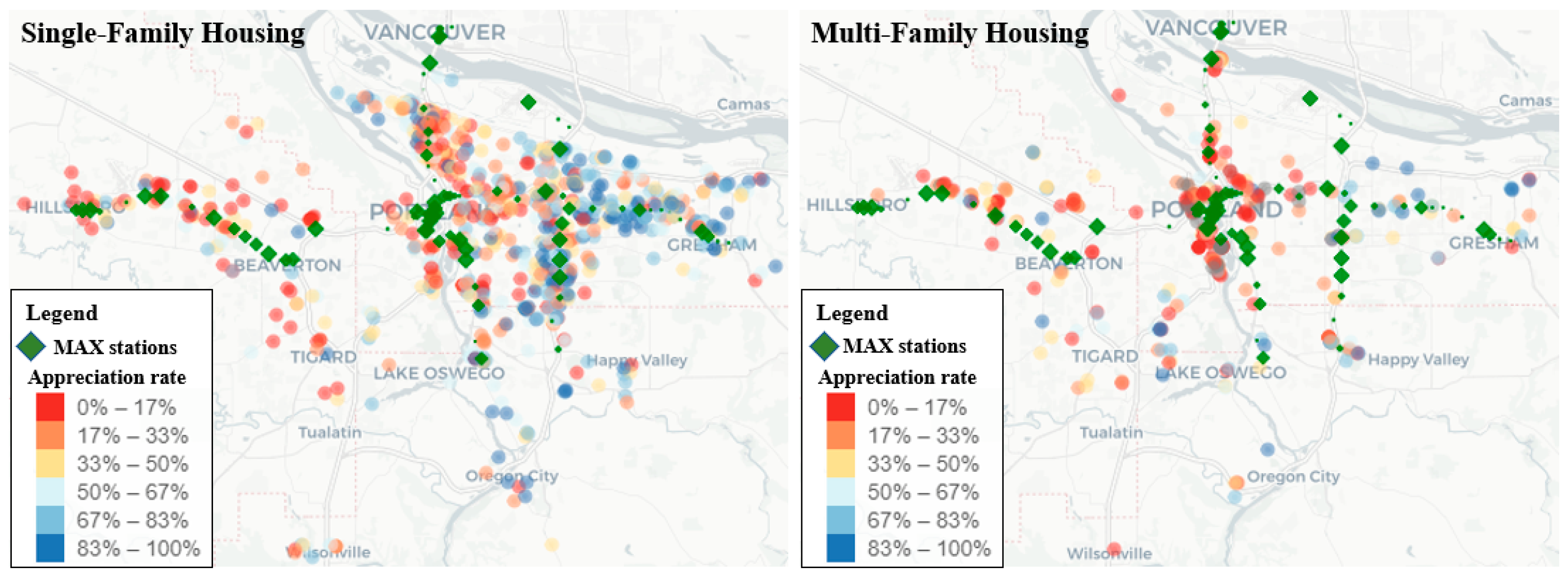

3.1. Study Area

3.1.1. Portland Metropolitan Area

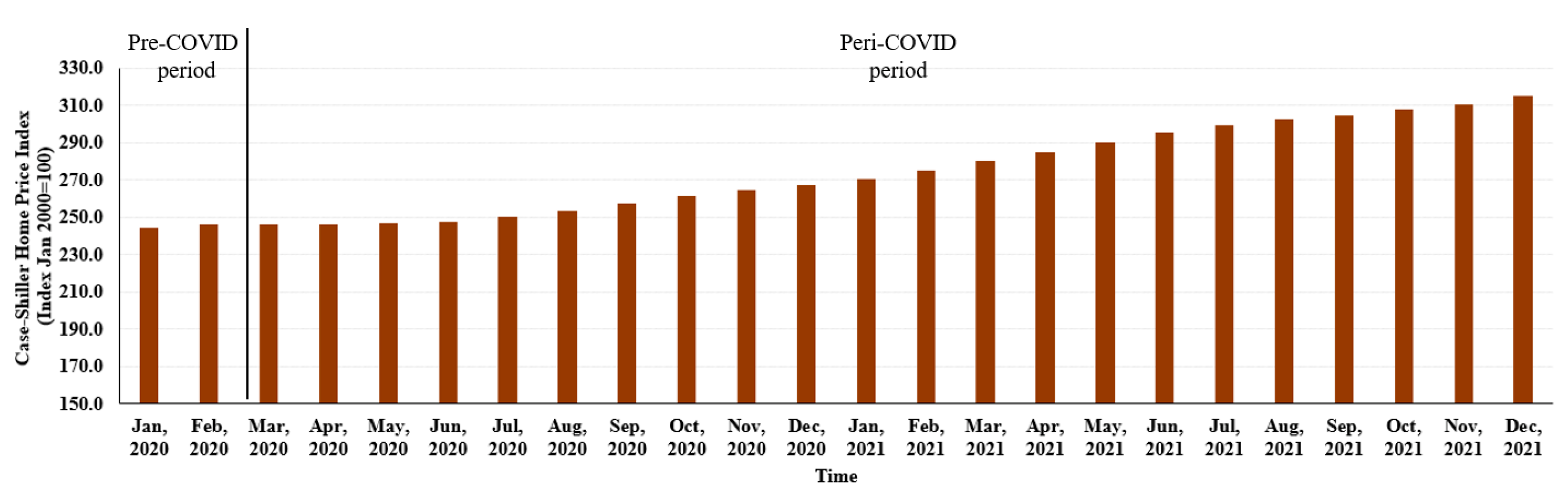

3.1.2. Timeline

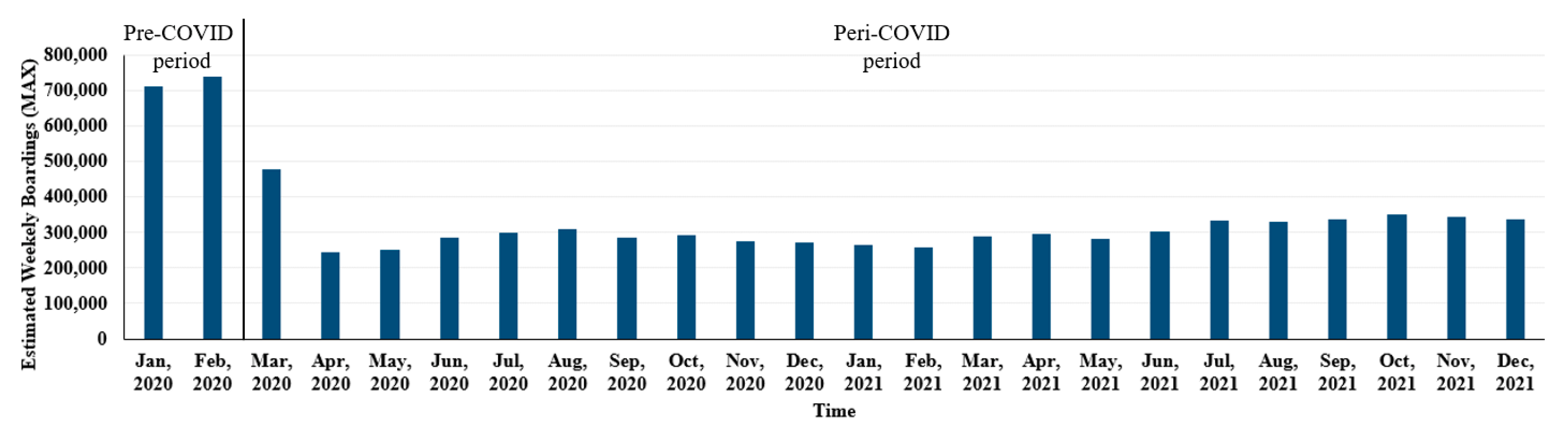

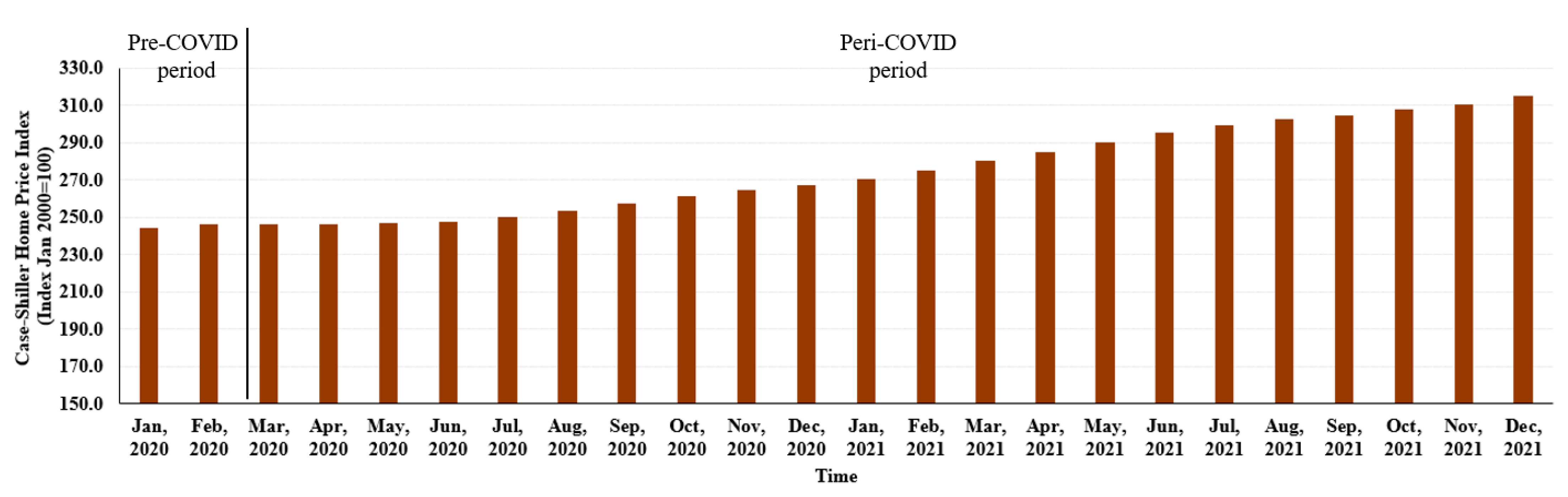

3.1.3. Broad Trends in Transit Ridership and Residential Property Values in Portland

3.2. Methodological Approach

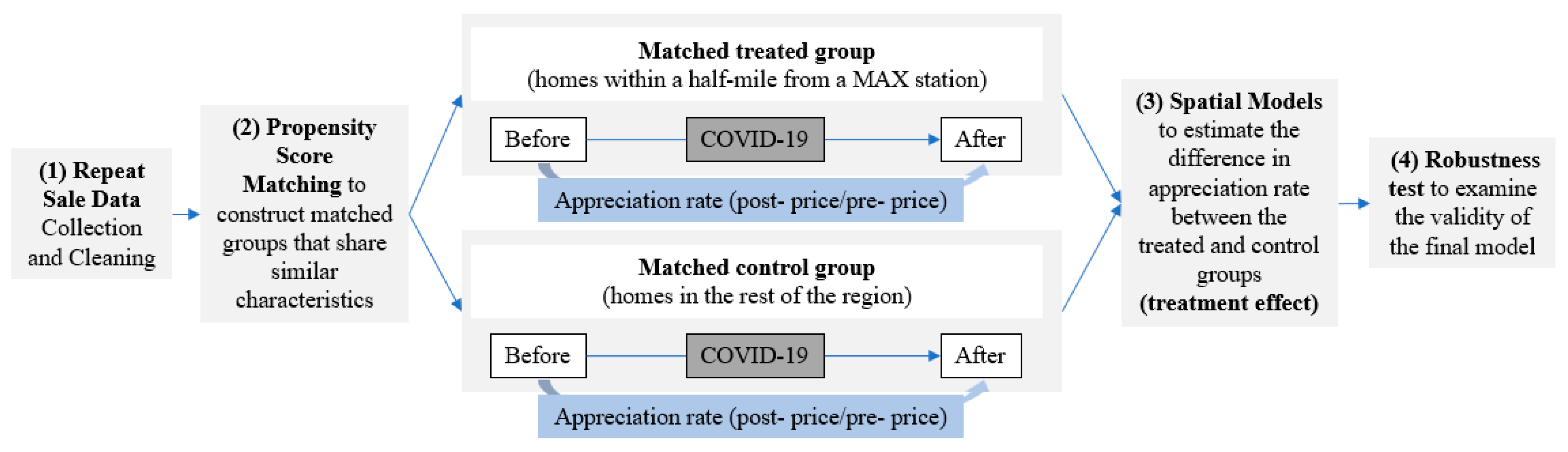

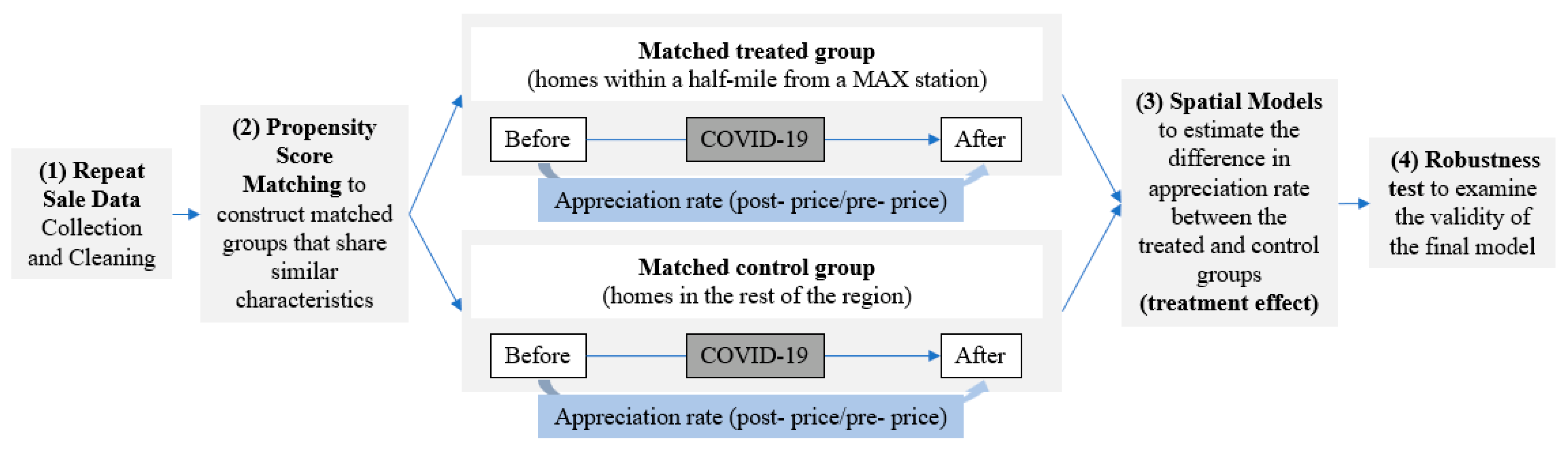

3.2.1. Overview of the Four-Step Process

3.2.2. Step 1: Repeat Sales Data Collection and Cleaning

3.2.3. Step 2: Propensity Score Matching

3.2.4. Step 3: Spatial Econometrics Model

3.2.5. Step 4: Robustness Test

4. Results

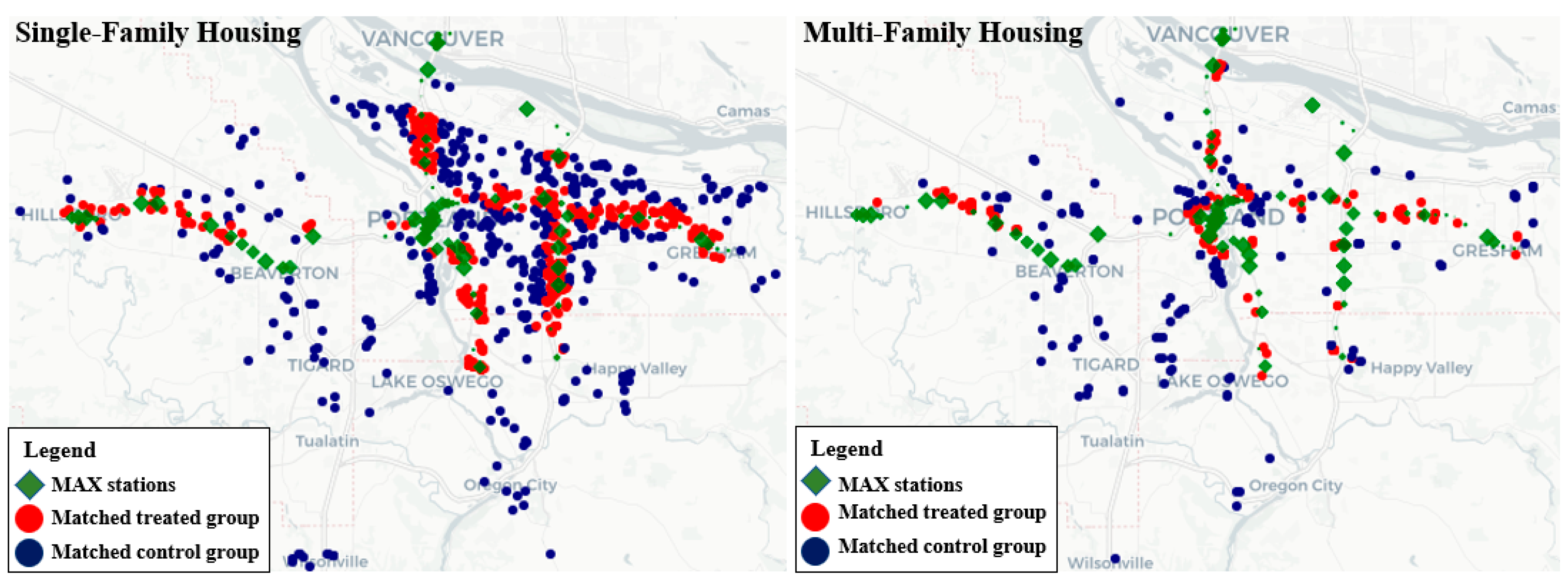

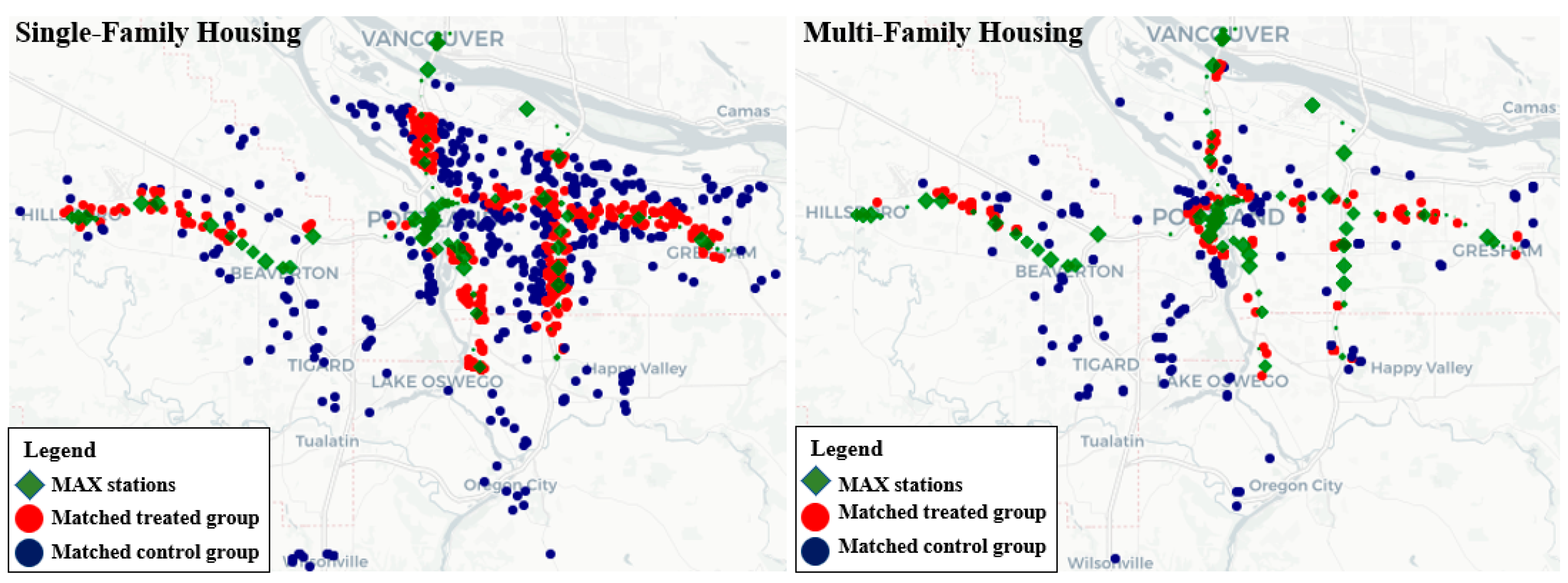

4.1. Propensity Score Matching

4.1.1. Balance Diagnostics

4.1.2. Descriptive Statistics of Matched Treated and Control Groups

4.2. Spatial Econometrics Model

4.2.1. Final Model Specification

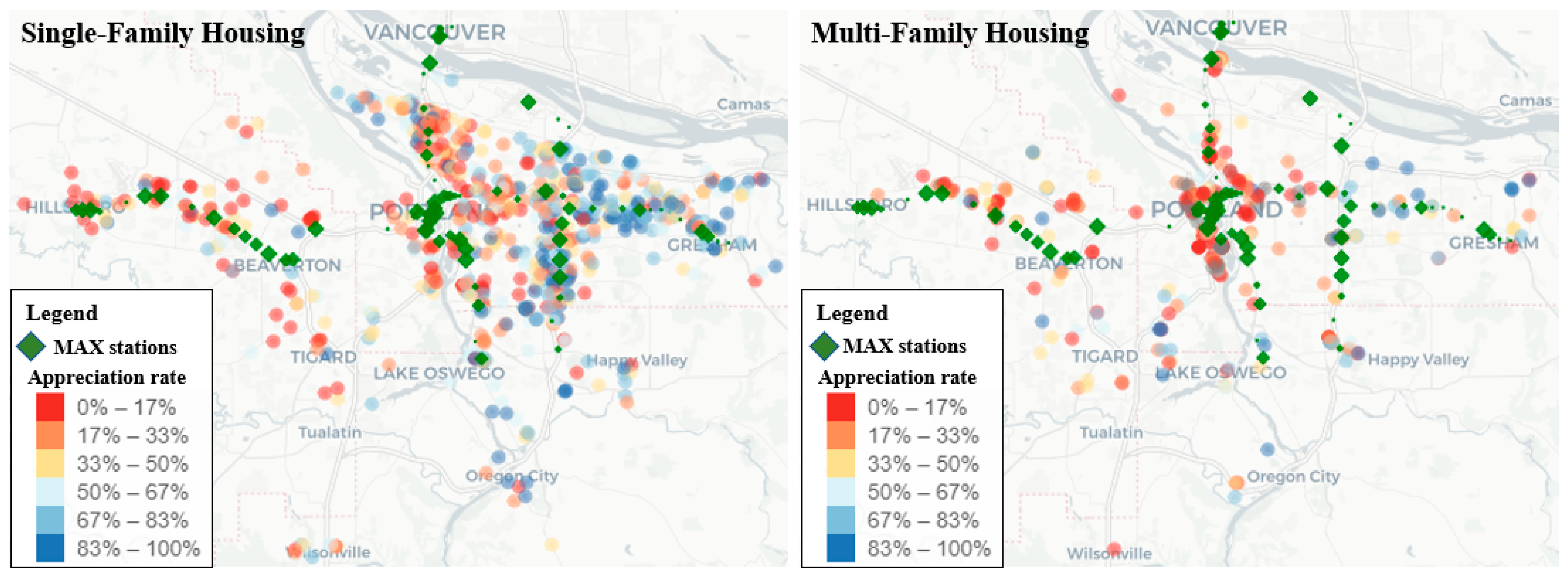

4.2.2. Treatment Effect

4.3. Robustness Test

5. Discussions

5.1. Single-Family Housing Market

5.2. Multi-Family Housing Market

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Tanrıvermiş, H. Possible Impacts of COVID-19 Outbreak on Real Estate Sector and Possible Changes to Adopt: A Situation Analysis and General Assessment on Turkish Perspective. J. Urban Manag. 2020, 9, 263–269. [Google Scholar] [CrossRef]

- Yin, Y.; Li, D.; Zhang, S.; Wu, L. How Does Railway Respond to the Spread of COVID-19? Countermeasure Analysis and Evaluation Around the World. Urban Rail Transit 2021, 7, 29–57. [Google Scholar] [CrossRef] [PubMed]

- Honey-Rosés, J.; Anguelovski, I.; Chireh, V.K.; Daher, C.; Bosch, C.K.; van den Litt, J.S.; Mawani, V.; McCall, M.K.; Orellana, A.; Oscilowicz, E.; et al. The Impact of COVID-19 on Public Space: An Early Review of the Emerging Questions–Design, Perceptions and Inequities. Cities Health 2020, 5, S263–S279. [Google Scholar] [CrossRef]

- Nanda, A.; Thanos, S.; Valtonen, E.; Xu, Y.; Zandieh, R. Forced Homeward: The COVID-19 Implications for Housing. Town Plan. Rev. 2021, 92, 25–31. [Google Scholar] [CrossRef]

- Zhang, D.; Jiao, J. How Does Urban Rail Transit Influence Residential Property Values? Evidence from An Emerging Chinese Megacity. Sustainability 2019, 11, 534. [Google Scholar] [CrossRef] [Green Version]

- Siripanich, A.; Rashidi, T.H.; Moylan, E. Interaction of Public Transport Accessibility and Residential Property Values Using Smart Card Data. Sustainability 2019, 11, 2709. [Google Scholar] [CrossRef] [Green Version]

- Gong, W.; Li, J.; Ng, M.K. Deciphering Property Development around High-Speed Railway Stations through Land Value Capture: Case Studies in Shenzhen and Hong Kong. Sustainability 2021, 13, 12605. [Google Scholar] [CrossRef]

- Dawkins, C.; Moeckel, R. Transit-Induced Gentrification: Who Will Stay, and Who Will Go? Hous. Policy Debate 2016, 26, 801–818. [Google Scholar] [CrossRef]

- Bartholomew, K.; Ewing, R. Hedonic Price Effects of Pedestrian- and Transit-Oriented Development. J. Plan. Lit. 2011, 26, 18–34. [Google Scholar] [CrossRef]

- Alonso, W. A Theory of the Urban Land Market. In Urban and Regional Economics; 1960; pp. 83–91. Available online: http://lib.cufe.edu.cn/upload_files/other/4_20140526030430_59_A%20theory%20of%20the%20urban%20land%20market.pdf (accessed on 19 June 2022).

- Mills, E.S. Studies in the Structure of the Urban Economy; John Hopkins Press: Baltimore, MD, USA, 1972. [Google Scholar]

- Muth, R.F. Cities and Housing; the Spatial Pattern of Urban Residential Land Use; University of Chicago Press: Chicago, IL, USA, 1969. [Google Scholar]

- Wingo, L. Transportation and Urban Land, 1st ed.; Routledge: London, UK, 1961; ISBN 978-1-138-96267-5. [Google Scholar]

- Bowes, D.R.; Ihlanfeldt, K.R. Identifying the Impacts of Rail Transit Stations on Residential Property Values. J. Urban Econ. 2001, 50, 1–25. [Google Scholar] [CrossRef]

- Duncan, M. Comparing Rail Transit Capitalization Benefits for Single-Family and Condominium Units in San Diego, California. Transp. Res. Rec. 2008, 2067, 120–130. [Google Scholar] [CrossRef]

- Pan, Q. The Impacts of an Urban Light Rail System on Residential Property Values: A Case Study of the Houston METRORail Transit Line. Transp. Plan. Technol. 2013, 36, 145–169. [Google Scholar] [CrossRef]

- Cervero, R.; Duncan, M. Benefits of Proximity to Rail on Housing Markets: Experiences in Santa Clara County. J. Public Transp. 2002, 5, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Hess, D.B.; Almeida, T.M. Impact of Proximity to Light Rail Rapid Transit on Station-Area Property Values in Buffalo, New York. Urban Stud. 2007, 44, 1041–1068. [Google Scholar] [CrossRef]

- Hamidi, S.; Kittrell, K.; Ewing, R. Value of Transit as Reflected in U.S. Single-Family Home Premiums: A Meta-Analysis. Transp. Res. Rec. 2016, 2543, 108–115. [Google Scholar] [CrossRef]

- Chatman, D.G.; Tulach, N.K.; Kim, K. Evaluating the Economic Impacts of Light Rail by Measuring Home Appreciation: A First Look at New Jersey’s River Line. Urban Stud. 2012, 49, 467–487. [Google Scholar] [CrossRef]

- McIntosh, J.; Trubka, R.; Newman, P. Can Value Capture Work in a Car Dependent City? Willingness to Pay for Transit Access in Perth, Western Australia. Transp. Res. Part A Policy Pract. 2014, 67, 320–339. [Google Scholar] [CrossRef]

- He, S.Y. Regional Impact of Rail Network Accessibility on Residential Property Price: Modelling Spatial Heterogeneous Capitalisation Effects in Hong Kong. Transp. Res. Part A Policy Pract. 2020, 135, 244–263. [Google Scholar] [CrossRef]

- Kim, K.; Lahr, M.L. The impact of Hudson-Bergen Light Rail on residential property appreciation. Pap. Reg. Sci. 2014, 93, S79–S97. [Google Scholar] [CrossRef] [Green Version]

- Cao, X.; Lou, S. When and How Much Did the Green Line LRT Increase Single-Family Housing Values in St. Paul, Minnesota? J. Plan. Educ. Res. 2018, 38, 427–436. [Google Scholar] [CrossRef]

- Song, Z.; Cao, M.; Han, T.; Hickman, R. Public Transport Accessibility and Housing Value Uplift: Evidence from the Docklands Light Railway in London. Case Stud. Transp. Policy 2019, 7, 607–616. [Google Scholar] [CrossRef]

- Lee, S.; Wang, L.; Dong, H.; Yang, H. Temporal Dynamics of the Effects of Light Rail on the Housing Prices: A Case Study of Portland, Oregon. Available online: http://wstlur.org/symposium/2021/documents/WSTLUR_2021_Abstract_Book_June24.pdf (accessed on 10 June 2021).

- Knaap, G.J.; Ding, C.; Hopkins, L.D. Do Plans Matter?: The Effects of Light Rail Plans on Land Values in Station Areas. J. Plan. Educ. Res. 2001, 21, 32–39. [Google Scholar] [CrossRef]

- Agostini, C.A.; Palmucci, G.A. The Anticipated Capitalisation Effect of a New Metro Line on Housing Prices. Fisc. Stud. 2008, 29, 233–256. [Google Scholar] [CrossRef]

- Jayantha, W.M.; Lam, T.I.; Chong, M.L. The Impact of Anticipated Transport Improvement on Property Prices: A Case Study in Hong Kong. Habitat Int. 2015, 49, 148–156. [Google Scholar] [CrossRef]

- Golub, A.; Guhathakurta, S.; Sollqpuram, B. Spatial and Temporal Capitalization Effects of Light Rail in Phoenix: From Conception, Planning, and Construction to Operation. J. Plan. Educ. Res. 2012, 32, 415–429. [Google Scholar] [CrossRef]

- Pearson, J.; Muldoon-Smith, K.; Liu, H.; Robson, S. How Does the Extension of Existing Transport Infrastructure Affect Land Value? A Case Study of the Tyne and Wear Light Transit Metro System. Land Use Policy 2022, 112, 105811. [Google Scholar] [CrossRef]

- Yan, S.; Delmelle, E.; Duncan, M. The Impact of a New Light Rail System on Single-Family Property Values in Charlotte, North Carolina. J. Transp. Land Use 2012, 5, 60–67. [Google Scholar] [CrossRef] [Green Version]

- Ke, Y.; Gkritza, K. Light Rail Transit and Housing Markets in Charlotte-Mecklenburg County, North Carolina: Announcement and Operations Effects Using Quasi-Experimental Methods. J. Transp. Geogr. 2019, 76, 212–220. [Google Scholar] [CrossRef]

- Liu, L.; Miller, H.J.; Scheff, J. The Impacts of COVID-19 Pandemic on Public Transit Demand in the United States. PLoS ONE 2020, 15, e0242476. [Google Scholar] [CrossRef]

- Brough, R.; Freedman, M.; Phillips, D. Understanding Socioeconomic Disparities in Travel Behavior during the COVID-19 Pandemic; Social Science Research Network: Rochester, NY, USA, 2020. [Google Scholar]

- Hu, S.; Chen, P. Who Left Riding Transit? Examining Socioeconomic Disparities in the Impact of COVID-19 on Ridership. Transp. Res. Part D Transp. Environ. 2021, 90, 102654. [Google Scholar] [CrossRef]

- WMATA. Metro and COVID-19: Steps We’ve Taken | WMATA. Available online: https://www.wmata.com/service/covid19/COVID-19.cfm (accessed on 26 May 2021).

- Jung, H. The Impact of an Epidemic on Transit Ridership. J. Public Transp. 2020, 22, 1. [Google Scholar] [CrossRef]

- Ramani, A.; Bloom, N. The Donut Effect: How COVID-19 Shapes Real Estate; Standford Institute for Economic Policy Research: Standford, CA, USA, 2021; p. 8. [Google Scholar]

- Liu, S.; Su, Y. The Impact of the COVID-19 Pandemic on the Demand for Density: Evidence from the U.S. Housing Market; Social Science Research Network: Rochester, NY, USA, 2021. [Google Scholar]

- TriMet. TriMet Service and Ridership Information. Available online: https://trimet.org/about/pdf/trimetridership.pdf (accessed on 30 November 2020).

- D’Lima, W.; Lopez, L.A.; Pradhan, A. COVID-19 and Housing Market Effects: Evidence from U.S. Shutdown Orders; Social Science Research Network: Rochester, NY, USA, 2020. [Google Scholar]

- Yoruk, B. Early Effects of the COVID-19 Pandemic on Housing Market in the United States; Social Science Research Network: Rochester, NY, USA, 2020. [Google Scholar]

- Sun, W.; Zheng, S.; Wang, R. The Capitalization of Subway Access in Home Value: A Repeat-Rentals Model with Supply Constraints in Beijing. Transp. Res. Part A Policy Pract. 2015, 80, 104–115. [Google Scholar] [CrossRef]

- Concato, J.; Shah, N.; Horwitz, R.I. Randomized, Controlled Trials, Observational Studies, and the Hierarchy of Research Designs. N. Engl. J. Med. 2000, 342, 1887–1892. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Dong, H. Rail-Transit-Induced Gentrification and the Affordability Paradox of TOD. J. Transp. Geogr. 2017, 63, 1–10. [Google Scholar] [CrossRef]

- Ali, M.S.; Prieto-Alhambra, D.; Lopes, L.C.; Ramos, D.; Bispo, N.; Ichihara, M.Y.; Pescarini, J.M.; Williamson, E.; Fiaccone, R.L.; Barreto, M.L.; et al. Propensity Score Methods in Health Technology Assessment: Principles, Extended Applications, and Recent Advances. Front. Pharmacol. 2019, 10, 973. [Google Scholar] [CrossRef]

- Dong, H. Were Home Prices in New Urbanist Neighborhoods More Resilient in the Recent Housing Downturn? J. Plan. Educ. Res. 2015, 35, 5–18. [Google Scholar] [CrossRef] [Green Version]

- Zhang, L.; Yi, Y. Quantile House Price Indices in Beijing. Reg. Sci. Urban Econ. 2017, 63, 85–96. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The Central Role of the Propensity Score in Observational Studies for Causal Effects. Biometrika 1983, 70, 41–55. [Google Scholar] [CrossRef]

- Landis, J.; Guhathakurta, S.; Huang, W.; Zhang, M.; Fukuji, B. Rail Transit Investments, Real Estate Values, and Land Use Change: A Comparative Analysis of Five California Rail Transit Systems. 1995. Available online: https://escholarship.org/uc/item/4hh7f652 (accessed on 19 June 2022).

- Wang, Y.; Cai, H.; Li, C.; Jiang, Z.; Wang, L.; Song, J.; Xia, J. Optimal Caliper Width for Propensity Score Matching of Three Treatment Groups: A Monte Carlo Study. PLoS ONE 2013, 8, e81045. [Google Scholar] [CrossRef] [Green Version]

- Austin, P.C. An Introduction to Propensity Score Methods for Reducing the Effects of Confounding in Observational Studies. Multivar. Behav Res 2011, 46, 399–424. [Google Scholar] [CrossRef] [Green Version]

- Kelley, K.; Rausch, J.R. Sample Size Planning for the Standardized Mean Difference: Accuracy in Parameter Estimation via Narrow Confidence Intervals. Psychol. Methods 2006, 11, 363–385. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Hsu, H.; Lachenbruch, P.A. Paired t Test. In Encyclopedia of Biostatistics; American Cancer Society: Atlanta, GA, USA, 2005; ISBN 978-0-470-01181-2. [Google Scholar]

- Bhat, C.R.; Gossen, R. A Mixed Multinomial Logit Model Analysis of Weekend Recreational Episode Type Choice. Transp. Res. Part B Methodol. 2004, 38, 767–787. [Google Scholar] [CrossRef] [Green Version]

- Gehrke, S.R.; Wang, L. Operationalizing the Neighborhood Effects of the Built Environment on Travel Behavior. J. Transp. Geogr. 2020, 82, 102561. [Google Scholar] [CrossRef]

- Ewing, R.; Tian, G.; Goates, J.; Zhang, M.; Greenwald, M.J.; Joyce, A.; Kircher, J.; Greene, W. Varying Influences of the Built Environment on Household Travel in 15 Diverse Regions of the United States. Urban Stud. 2015, 52, 2330–2348. [Google Scholar] [CrossRef]

- Anselin, L. Spatial Econometrics. In A Companion to Theoretical Econometrics; Baltagi, B.H., Ed.; Blackwell Publishing Ltd.: Malden, MA, USA, 2003; pp. 310–330. ISBN 978-0-470-99624-9. [Google Scholar]

- Anselin, L. Spatial Econometrics: Methods and Models; Springer Science & Business Media: Berlin, Germany, 2013; ISBN 978-94-015-7799-1. [Google Scholar]

- LeSage, J.P. An Introduction to Spatial Econometrics. Revue D’économie Industrielle 2008, 123, 19–44. Available online: https://econpapers.repec.org/article/caireidbu/rei_5f123_5f0019.htm (accessed on 19 June 2022). [CrossRef] [Green Version]

- Conway, D.; Li, C.Q.; Wolch, J.; Kahle, C.; Jerrett, M. A Spatial Autocorrelation Approach for Examining the Effects of Urban Greenspace on Residential Property Values. J. Real. Estate. Financ. Econ. 2010, 41, 150–169. [Google Scholar] [CrossRef]

- Liu, J.H.; Shi, W. Impact of Bike Facilities on Residential Property Prices. Transp. Res. Rec. 2017, 2662, 50–58. [Google Scholar] [CrossRef] [Green Version]

- Rubin, D.B. Using Propensity Scores to Help Design Observational Studies: Application to the Tobacco Litigation. Health Serv. Outcomes Res. Methodol. 2001, 2, 169–188. [Google Scholar] [CrossRef]

- Moran, P.A.P. Notes on Continuous Stochastic Phenomena. Biometrika 1950, 37, 17–23. [Google Scholar] [CrossRef]

- Anselin, L. Lagrange Multiplier Test Diagnostics for Spatial Dependence and Spatial Heterogeneity. Geogr. Anal. 1988, 20, 1–17. [Google Scholar] [CrossRef]

- Florida, R.; Rodríguez-Pose, A.; Storper, M. Cities in a Post-COVID World. Urban Stud. 2021, 23. [Google Scholar] [CrossRef]

- Tan, L.; Ma, C. Choice Behavior of Commuters’ Rail Transit Mode during the COVID-19 Pandemic Based on Logistic Model. J. Traffic Transp. Eng. Engl. Ed. 2021, 8, 186–195. [Google Scholar] [CrossRef]

- Cooper, T.; Faseruk, A. Strategic risk, Risk Perception and Risk Behaviour: Meta-Analysis. J. Financ. Manag. Anal. 2011, 24, 20–29. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Periods | Description | Dates |

|---|---|---|

| The pre-COVID period | before the COVID-19 outbreak | January 2016~February 2020 |

| The peri-COVID period | after the COVID-19 outbreak | March 2020~December 2021 |

| Name | Description | Data Source |

|---|---|---|

| Treated | Dummy variable for whether the home is in the treated group, located within a half-mile from the nearest MAX (light rail transit system in the Portland metropolitan area) station | GIS |

| Structural Characteristics | ||

| Bldg Area | The building area of a home in square feet | RLIS |

| Lot Area | The lot area of a home in square feet | RLIS |

| Year Built | The year that a home was built | RLIS |

| Locational Factors | ||

| Freeway | Log-transformed distance in feet between each home and the nearest freeway at sale year during the pre-COVID period | GIS |

| Ramp | Log-transformed distance in feet between each home and the nearest ramp at sale year during the pre-COVID period | GIS |

| Bus | Log-transformed distance in feet between each home and the nearest bus stop at sale year during the pre-COVID period | GIS |

| CBD | Log-transformed distance in feet between each home and downtown (the City Hall of Portland) at sale year during the pre-COVID period [46] | GIS |

| Neighborhood Characteristics | ||

| Pop Den | The total population per acre at the census block group level at sale year during the pre-COVID period | ACS |

| White | The proportion of the residents who are non-Hispanic white at sale year during the pre-COVID period | ACS |

| HH Income | The median household income at the census block group level at sale year during the pre-COVID period | ACS |

| Education | The proportion of the population 25 years and over who attain less than high school at the census block group level at sale year during the pre-COVID period | ACS |

| Land Mix | The evenness in the spatial footprint of three land uses at census block group level at sale year during the pre-COVID period: residential, commercial/industrial, and others at sale year during the pre-COVID period | GIS |

| Net Den | The total length of roads in feet per acre at the census block group level [57] | SLD |

| Intersect Den | The total length of street intersection per square mile at the census block group level [58] | SLD |

| School | The total number of schools per acre at the census block group level at sale year during the pre-COVID period | GIS |

| Access Auto | The number of jobs within 45 min auto travel time at the census block group level | SLD |

| Access Transit | The number of jobs within 45 min transit travel time at the census block group level | SLD |

| Name | Single-Family Housing | Multi-Family Housing | ||||

|---|---|---|---|---|---|---|

| N | Mean | Std. Dev | N | Mean | Std. Dev | |

| Treated | 4482 | 0.11 | 0.31 | 1319 | 0.27 | 0.44 |

| Bldg Area | 4482 | 1740.17 | 683.14 | 1319 | 1110.19 | 427.31 |

| Lot Area | 4482 | 5420.81 | 2268.88 | 1319 | 467.88 | 415.13 |

| Year Built | 4482 | 1976.68 | 33.58 | 1319 | 1986.70 | 24.06 |

| Freeway | 4482 | 12,350.99 | 13,784.36 | 1319 | 6696.87 | 11,124.49 |

| Ramp | 4482 | 29,708.26 | 23,426.22 | 1319 | 20,036.30 | 21,398.93 |

| Bus | 4482 | 4130.57 | 10,051.20 | 1319 | 1937.19 | 10,545.16 |

| CBD | 4482 | 49,321.33 | 28,259.63 | 1319 | 33,089.20 | 27,039.27 |

| Pop Den | 4482 | 5530.79 | 3332.20 | 1319 | 7810.15 | 6127.20 |

| White | 4482 | 80.38 | 12.06 | 1319 | 80.71 | 12.07 |

| HH Income | 4482 | 75,952.90 | 29,306.83 | 1319 | 73,756.83 | 27,919.97 |

| Education | 4482 | 8.21 | 7.26 | 1319 | 5.49 | 6.76 |

| Land Mix | 4482 | 0.42 | 0.20 | 1319 | 0.55 | 0.19 |

| Net Den | 4482 | 20.36 | 8.67 | 1319 | 25.09 | 10.23 |

| Intersect Den | 4482 | 125.96 | 79.70 | 1319 | 155.96 | 91.19 |

| School | 4482 | 1.15 | 1.47 | 1319 | 1.14 | 1.40 |

| Access Auto | 4482 | 63,692.91 | 29,062.29 | 1319 | 84,329.47 | 32,269.66 |

| Access Transit | 4482 | 46,730.84 | 88,329.29 | 1319 | 87,232.67 | 114,657.22 |

| Name | Description | Data Source |

|---|---|---|

| Dependent variable | ||

| ln(appreciation rate) | Log-transformed appreciation rate The appreciation rate was calculated as the sale price of a residential property during the COVID-19 pandemic (sold between March 2020 and December 2021) divided by the price of the same property before the COVID-19 outbreak (sold between January 2016 and February 2020). | RLIS |

| Independent variable | ||

| Treated | The dummy variable for a property located within a half-mile from the nearest MAX (light rail transit system in the Portland metropolitan area) station | RLIS |

| Length of time | Length of time between two transactions in months | RLIS |

| Name | Single-Family Housing | Multi-Family Housing | ||||

|---|---|---|---|---|---|---|

| N | Mean | Std. Dev | N | Mean | Std. Dev | |

| ln(appreciation rate) | ||||||

| Total sample | 860 | 0.251 | 0.159 | 376 | 0.141 | 0.157 |

| Matched Treated Group | 430 | 0.249 | 0.153 | 188 | 0.127 | 0.155 |

| Matched Control Group | 430 | 0.253 | 0.165 | 188 | 0.156 | 0.158 |

| Appreciation rate | ||||||

| Total sample | 860 | 1.302 | 0.223 | 376 | 1.166 | 0.192 |

| Matched Treated Group | 430 | 1.300 | 0.213 | 188 | 1.150 | 0.182 |

| Matched Control Group | 430 | 1.310 | 0.233 | 188 | 1.180 | 0.202 |

| Length of time | ||||||

| Total sample | 860 | 42.5 | 12.5 | 376 | 41.5 | 12.7 |

| Matched Treated Group | 430 | 42.7 | 11.7 | 188 | 42.1 | 12.4 |

| Matched Control Group | 430 | 42.3 | 13.2 | 188 | 40.9 | 13.1 |

| Variables | Single-Family Housing | Multi-Family Housing | ||

|---|---|---|---|---|

| Standardized Difference | p-Value of Paired t-Test | Standardized Difference | p-Value of Paired t-Test | |

| Bldg Area | 0.021 | 0.748 | 0.027 | 0.783 |

| Lot Area | 0.063 | 0.323 | 0.112 | 0.306 |

| Year Built | 0.015 | 0.798 | 0.056 | 0.475 |

| Freeway | 0.065 | 0.309 | 0.007 | 0.949 |

| Ramp | 0.019 | 0.714 | 0.013 | 0.878 |

| Bus | 0.026 | 0.769 | 0.024 | 0.846 |

| CBD | 0.088 | 0.182 | 0.019 | 0.825 |

| Pop Den | 0.015 | 0.828 | 0.039 | 0.481 |

| White | 0.036 | 0.571 | 0.121 | 0.250 |

| HH Income | 0.014 | 0.817 | 0.139 | 0.129 |

| Education | 0.010 | 0.876 | 0.040 | 0.740 |

| Land Mix | 0.091 | 0.225 | 0.137 | 0.170 |

| Net Den | 0.080 | 0.162 | 0.052 | 0.430 |

| Intersect Den | 0.062 | 0.325 | 0.059 | 0.339 |

| School | 0.041 | 0.5793 | 0.096 | 0.404 |

| Access Auto | 0.088 | 0.127 | 0.081 | 0.405 |

| Access Transit | 0.058 | 0.357 | 0.103 | 0.258 |

| Sample Size | 860 (430 pairs) | 376 (188 pairs) | ||

| Moran’s I | Lagrange Multiplier (LM) Tests | |||||

|---|---|---|---|---|---|---|

| LM Test for Spatial Lag (LMlag) | LM Test for Spatial Error (LMerror) | Robust LM Test for Spatial Lag (RLMlag) | Robust LM Test for Spatial Error (RLMerror) | Portmanteau Test (SARMA) | ||

| Single-Family Housing | 0.14 *** | 27.34 *** | 706.09 *** | 1.19 | 679.90 *** | 707.28 *** |

| Multi-Family Housing | 0.26 *** | 0.21 | 1611.80 *** | 125.07 *** | 1736.60 *** | 1736.80 *** |

| Housing Market | Single-Family Housing | Multi-Family Housing | ||||

|---|---|---|---|---|---|---|

| Final Model | No | No | Yes | No | No | Yes |

| Models | OLS | SAR | SEM | OLS | SAR | SEM |

| Estimate (Std. Error) | Total Impact (Std. Error) | Estimate (Std. Error) | Estimate (Std. Error) | Total Impact (Std. Error) | Estimate (Std. Error) | |

| Constant | 0.059 *** (0.019) | 0.046 ** (0.018) | 0.046 ** (0.018) | 0.039 ** (0.028) | 0.065 ** (0.029) | 0.067 *** (0.025) |

| Treated | −0.006 (0.010) | −0.014 (0.010) | −0.008 (0.010) | −0.032 ** (0.016) | −0.031 ** (0.016) | −0.030 ** (0.013) |

| Length of time | 0.005 *** (0.0004) | 0.004 *** (0.0004) | 0.005 *** (0.0004) | 0.003 *** (0.001) | 0.003 *** (0.001) | 0.005 *** (0.001) |

| Model statistics | ||||||

| Observations | 860 | 860 | 860 | 376 | 376 | 376 |

| Adjusted R2 | 0.128 | 0.057 | ||||

| Rho | 0.003 *** | −0.004 | ||||

| Lambda | 0.013 *** | 0.011 *** | ||||

| Wald Statistics | 19.846 *** | 548.201 *** | 4.403 ** | 907.491 *** | ||

| LR Test | 20.538 *** | 85.775 *** | 1.196 | 156.509 *** | ||

| Log-likelihood | 429.949 | 462.567 | 175.485 | 253.142 | ||

| AIC | −831.360 | −849.898 | −915.135 | −341.770 | −340.970 | −496.283 |

| Housing Market | Single-Family Housing | Multi-Family Housing | ||||

|---|---|---|---|---|---|---|

| Final Model | No | No | Yes | No | No | Yes |

| Models | OLS | SAR | SEM | OLS | SAR | SEM |

| Estimate (Std. Error) | Total Impact (Std. Error) | Estimate (Std. Error) | Estimate (Std. Error) | Total Impact (Std. Error) | Estimate (Std. Error) | |

| Constant | 0.314 *** (0.044) | 0.218 *** (0.053) | 0.253 *** (0.050) | 0.103 * (0.061) | 0.082 * (0.065) | 0.152 ** (0.060) |

| Treated | 0.023 (0.033) | 0.018 (0.032) | 0.020 (0.032) | 0.027 (0.038) | 0.028 (0.037) | 0.031 (0.034) |

| Length of time | −0.004 ** (0.001) | −0.003 * (0.001) | −0.003 * (0.001) | 0.001 (0.002) | 0.001 (0.002) | 0.002 (0.002) |

| Model statistics | ||||||

| Observations | 194 | 194 | 194 | 78 | 78 | 78 |

| Adjusted R2 | 0.023 | 0.011 | ||||

| Rho | 0.012 *** | 0.017 | ||||

| Lambda | 0.020 ** | 0.070 *** | ||||

| Wald Statistics | 8.020 *** | 10.374 *** | 0.749 | 145.620 *** | ||

| LR Test | 8.862 *** | 5.345 ** | 0.601 | 14.521 *** | ||

| Log-likelihood | 17.806 | 16.047 | 30.341 | 37.301 | ||

| AIC | −18.749 | −25.611 | −22.094 | −52.080 | −50.681 | −64.601 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, S.; Wang, L. Intermediate Effect of the COVID-19 Pandemic on Prices of Housing near Light Rail Transit: A Case Study of the Portland Metropolitan Area. Sustainability 2022, 14, 9107. https://doi.org/10.3390/su14159107

Lee S, Wang L. Intermediate Effect of the COVID-19 Pandemic on Prices of Housing near Light Rail Transit: A Case Study of the Portland Metropolitan Area. Sustainability. 2022; 14(15):9107. https://doi.org/10.3390/su14159107

Chicago/Turabian StyleLee, Sangwan, and Liming Wang. 2022. "Intermediate Effect of the COVID-19 Pandemic on Prices of Housing near Light Rail Transit: A Case Study of the Portland Metropolitan Area" Sustainability 14, no. 15: 9107. https://doi.org/10.3390/su14159107

APA StyleLee, S., & Wang, L. (2022). Intermediate Effect of the COVID-19 Pandemic on Prices of Housing near Light Rail Transit: A Case Study of the Portland Metropolitan Area. Sustainability, 14(15), 9107. https://doi.org/10.3390/su14159107