Challenges and Responses of Agri-Food Activities under COVID-19 Pandemic: The Case of the Spanish Territories Producing Wine and Olive Oil

Abstract

:1. Introduction

2. Theoretical Background

2.1. The Territorial Approach

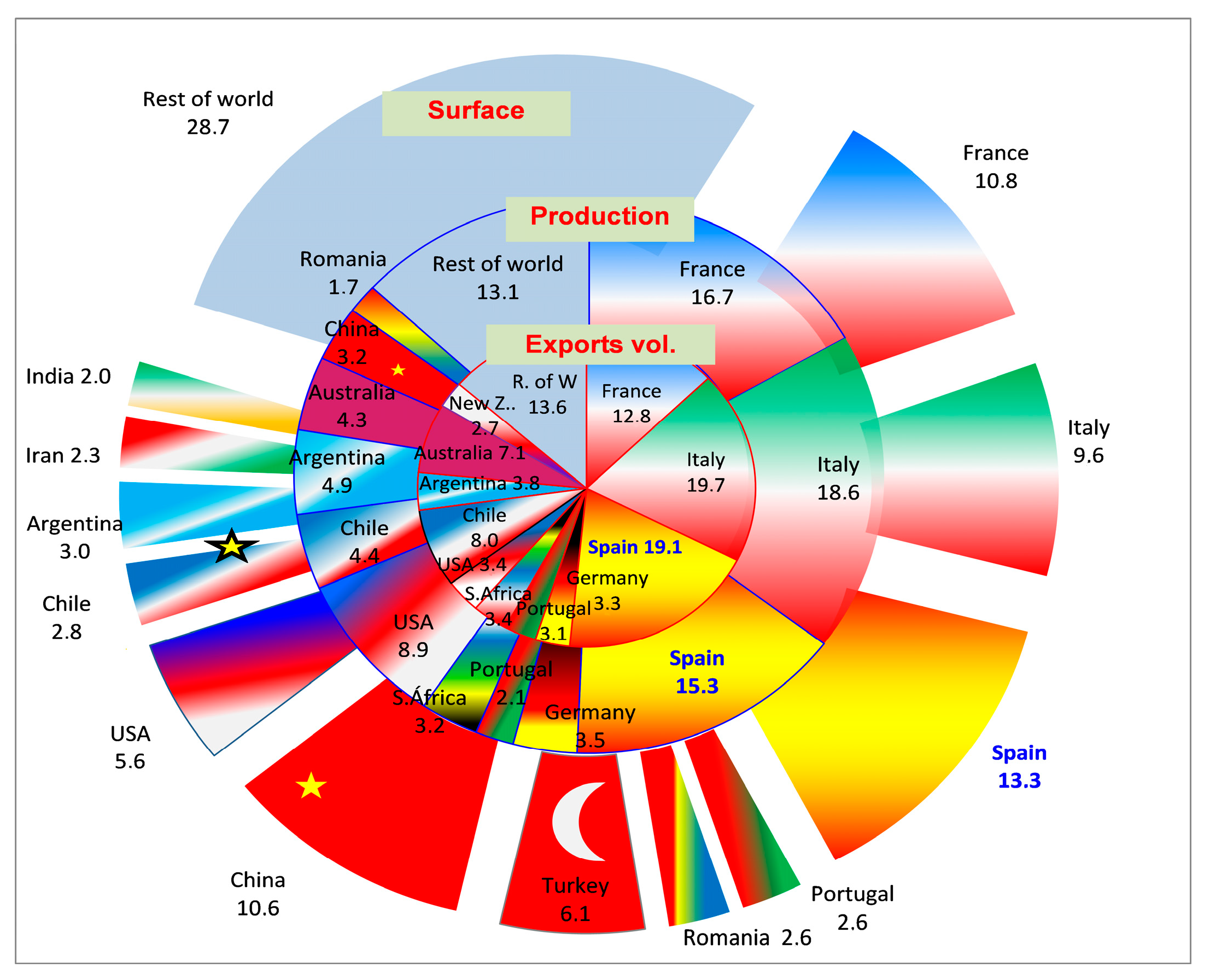

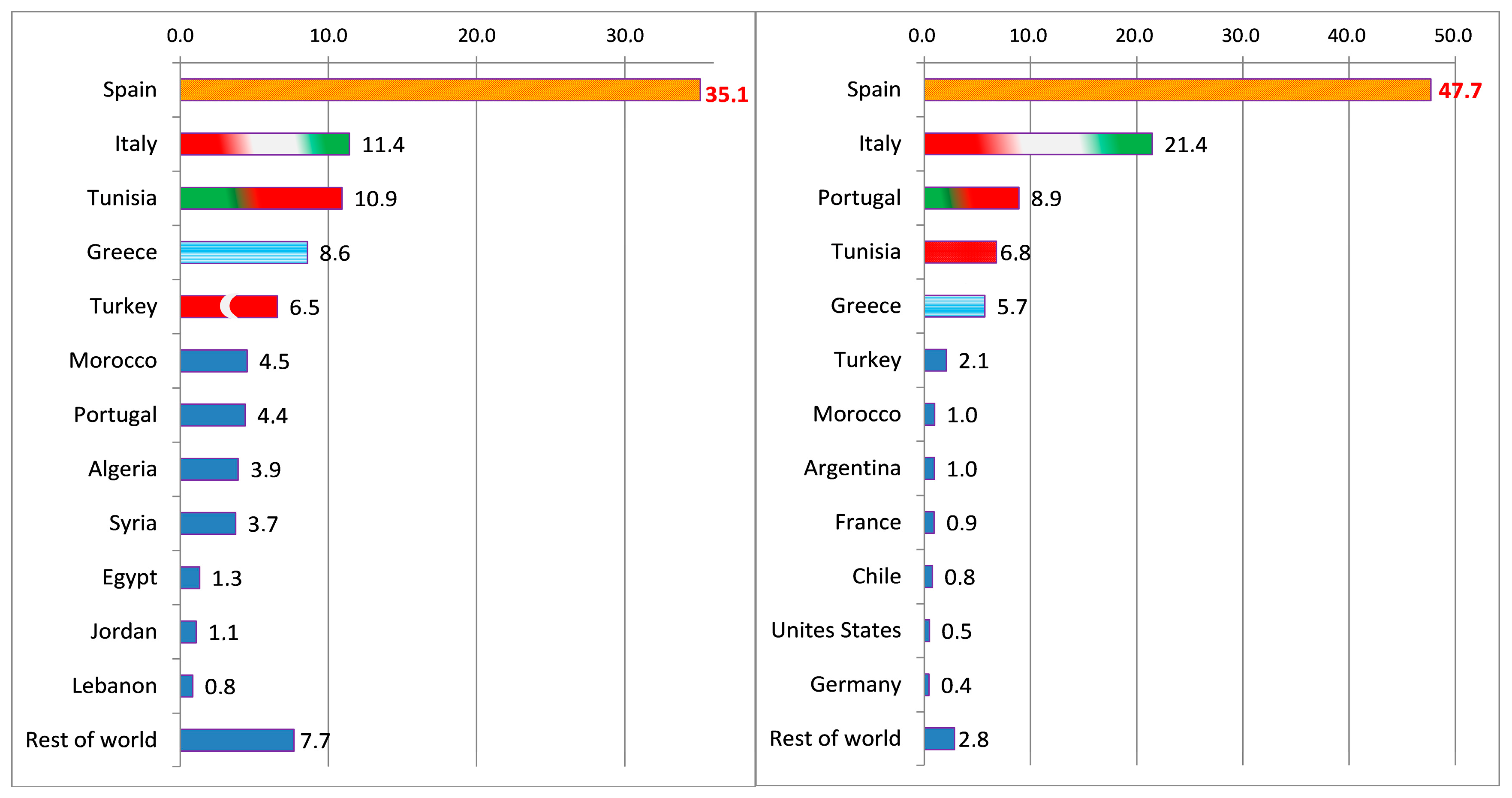

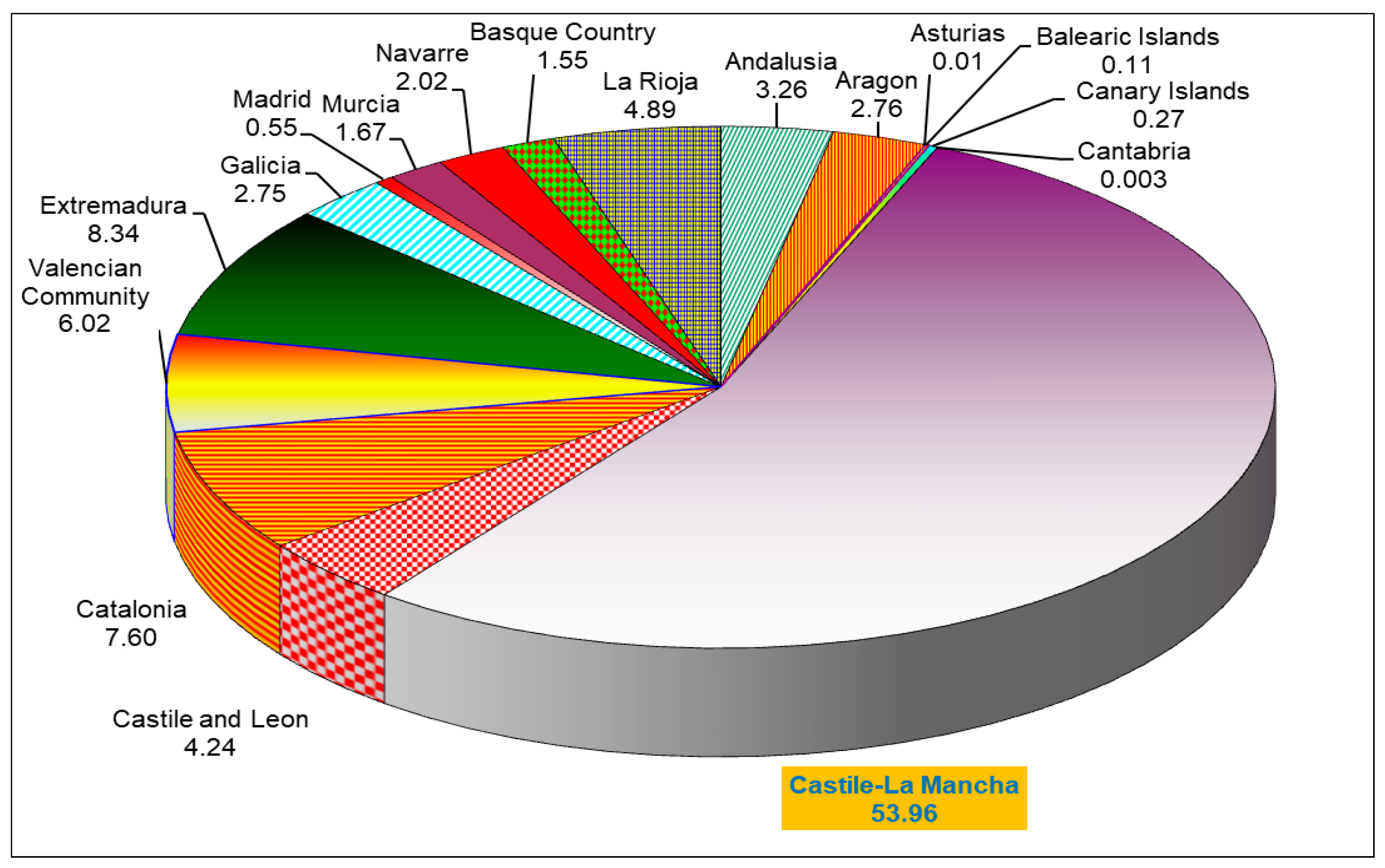

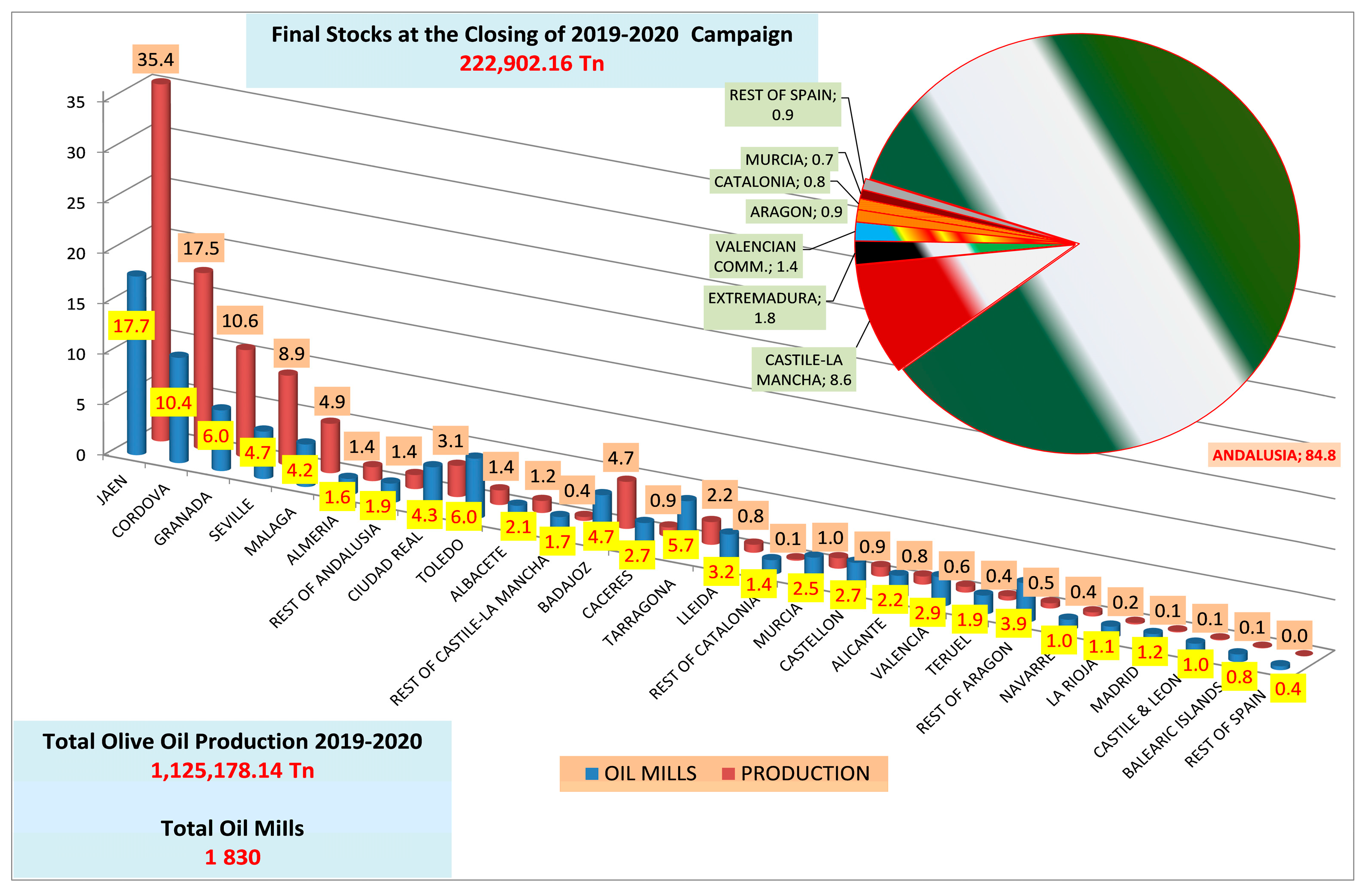

2.2. Description of Olive Oil and Wine Activities in Spain

3. Materials and Methods

4. Results

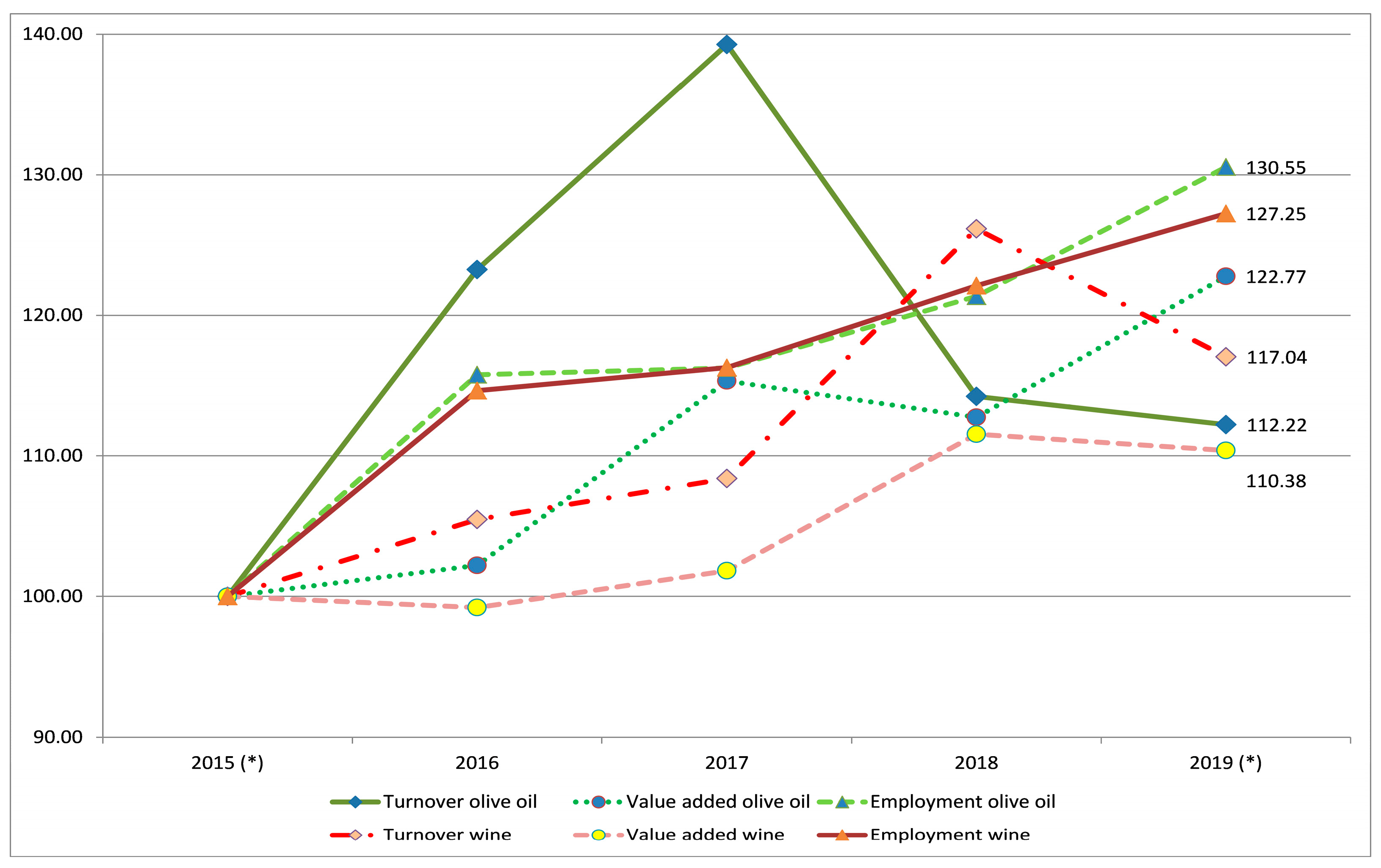

4.1. Spanish Wine and Oil Activities in the Face of the COVID-19 Crisis: The Effects of the Confinement

“Our firm sold a lot in restaurants. Now they are closed. It’s frustrating because our products aren’t interesting for retailers.”

“We have hardly been affected by the confinement. In fact, the harvest is sold out.”

4.2. Organizational Changes

“Some of our employees has been moved from production to the new department of online sales we have opened.”

“People look for new ways for consuming high-quality products for less money.”

4.3. Strategies in the Value Chain

“You can’t tell a big chain that your stocks are sold out. That business is for bigwineries.”

“We had touristic visits for a while, but the costs…guides, catering service, cleaning … were higher than revenues.”

4.4. The Role of Territorial Public Bodies

“Our intention supporting tourism within agri-food activities is to create a package for enjoying the territory.”

“Local firms had to maintain the relation with the final market, but the smaller companies couldn’t. Local public bodies knew that we had to step forward to create it.”

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Rodríguez-Cohard, J.C.; Juste-Carrión, J.J.; Vázquez-Barquero, A. Local Development Policies: Evolution and Challenges for Post-COVID-19 Recovering in Spain. Symphonia. Emerg. Issues Manag. 2020, 2, 41–54. [Google Scholar] [CrossRef]

- EIT Food. EIT Food Foresight: Impact of Covid-19 on the Food Sector in Southern Europe; Lantern: Madrid, Spain, 2020. [Google Scholar]

- OECD-FAO. OECD-FAO Agricultural Outlook 2020–2029; FAO, Rome/OECD Publishing: Paris, France, 2020. [Google Scholar] [CrossRef]

- FAO; IFAD; UNICEF; WFP; WHO. The State of Food Security and Nutrition in the World 2020. Transforming Food Systems for Affordable Healthy Diets; FAO: Rome, Italy, 2020. [Google Scholar] [CrossRef]

- FoodDrink Europe. Data & Trends EU Food & Drink Industry; FoodDrink Europe: Brussels, Belgium, 2020. [Google Scholar]

- Rastoin, J.-L. Stratégies D’entreprises Agroalimentaires Dans un Contexte de Globalisation; Séminaire agroalimentaire, Université Laval: Québec, QC, Canada, 2003. [Google Scholar]

- Rodríguez-Cohard, J.C.; Parras, M. The olive growing agri-industrial district of Jaén and the international olive oils cluster. Open Geogr. J. 2011, 4, 55–72. [Google Scholar] [CrossRef] [Green Version]

- Belis-Bergouignan, M.C. Bordeaux Wines: An Archetypal Terroir Cluster? Open Geogr. J. 2011, 4, 73–90. [Google Scholar] [CrossRef]

- Porter, M.E.; Bond, G.C. The California Wine Cluster. Harv. Bus. Sch. Case 1999, 799-124, (Revised February 2013). [Google Scholar]

- Sanz-Cañada, J.; Macías Vázquez, A. Quality certification, institutions and innovation in local agro-food systems: Protected designations of origin of olive oil in Spain. J. Rural. Stud. 2005, 21, 475–486. [Google Scholar] [CrossRef]

- Donthu, N.; Gustafsson, A. Effects of COVID 19 on business and research. J. Bus. Res. 2020, 117, 284–289. [Google Scholar] [CrossRef] [PubMed]

- Kristiana, Y.; Pramono, R.; Brian, R. Adaptation Strategy of Tourism Industry Stakeholders During the COVID-19 Pandemic: A Case Study in Indonesia. J. Asian Financ. Econ. Bus. 2021, 8, 213–223. [Google Scholar] [CrossRef]

- Serbulova, N.; Morgunova, T.; Persiyanova, G. Innovations during COVID-19 pandemic: Trends, technologies, prospects. E3S Web Conf. 2020, 210, 02005. [Google Scholar] [CrossRef]

- Popa, N.; Pop, A.N.; Marian-Potra, A.C.; Cocean, P.; Hognogi, G.G.; David, N.A. The Impact of the COVID-19 Pandemic on Independent Creative Activities in Two Large Cities in Romania. Int. J. Environ. Res. Public Health 2021, 18, 7674. [Google Scholar] [CrossRef] [PubMed]

- Trump, B.D.; Linkov, I. Risk and resilience in the time of the COVID-19 crisis. Environ. Syst. Decis. 2020, 40, 171–173. [Google Scholar] [CrossRef] [PubMed]

- Willy, D.K.; Diallo, Y.; Affognon, H.; Nang’ayo, F.; Waithaka, M.; Wossen, T. COVID-19 Pandemic in Africa: Impacts on Agriculture and Emerging Policy Responses for Adaptation and Resilience Building. TAATaat Policy Compact Working Paper no. wp01/2020. Available online: https://www.farm-d.org/document/covid-19-pandemic-in-africa-impacts-on-agriculture-and-emerging-policy-responses-for-adaptation-and-resilience-building/ (accessed on 17 November 2021).

- Zimmerer, K.S.; de Haan, S. Informal food chains and agrobiodiversity need strengthening—not weakening—to address food security amidst the COVID-19 crisis in South America. Food Secur. 2020, 12, 891–894. [Google Scholar] [CrossRef] [PubMed]

- Morton, J. On the susceptibility and vulnerability of agricultural value chains to COVID-19. World Dev. 2020, 136, 105132. [Google Scholar] [CrossRef]

- Toffolutti, V.; Stuckler, D.; McKee, M. Is the COVID-19 pandemic turning into a European food crisis? Eur. J. Public Health 2020, 30, 626–627. [Google Scholar] [CrossRef] [PubMed]

- Galanakis, C.M. The Food Systems in the Era of the Coronavirus (COVID-19) Pandemic Crisis. Foods 2020, 9, 523. [Google Scholar] [CrossRef] [PubMed]

- Laborde, D.; Martin, W.; Swinnen, J.; Vos, R. COVID-19 risks to global food security. Science 2020, 369, 6503. [Google Scholar] [CrossRef] [PubMed]

- Coluccia, B.; Agnusdei, G.P.; Miglietta, P.P.; De Leo, F. Effects of COVID-19 on the Italian agri-food supply and value chains. Food Control 2021, 123, 107839. [Google Scholar] [CrossRef] [PubMed]

- Mili, S.; Bouhaddane, M. Forecasting Global Developments and Challenges in Olive Oil Supply and Demand: A Delphi Survey from Spain. Agriculture 2021, 11, 191. [Google Scholar] [CrossRef]

- Rebelo, J.; Compés, R.; Faria, S.; Gonçalves, T.; Pinilla, V.; Simón-Elorz, K. Covid-19 lockdown and wine consumption frequency in Portugal and Spain. Span. J. Agric. Res. 2021, 19, e0105R. [Google Scholar] [CrossRef]

- Marco-Lajara, B.; Seva-Larrosa, P.; Ruiz-Fernández, L.; Martínez-Falcó, J. The Effect of COVID-19 on the Spanish Wine Industry. In Impact of Global Issues on International Trade; Özer, A.C., Ed.; IGI Global: Hershey, PA, USA, 2021; pp. 211–232. Available online: http://doi:10.4018/978-1-7998-8314-2.ch012 (accessed on 17 November 2021).

- Barca, F. An Agenda for a Reformed Cohesion Policy. A Place-Based Approach to Meeting European Union Challenges and Expectations. Independent Report; European Union: Brussels, Belgium, 2009. [Google Scholar]

- Beccatini, G. Dal Settore industriale al distretto industriale: Alcune considerazione sull’unita‘ diindagine dell’economia industriale. Riv. Di Econ. E Politica Ind. 1979, 1, 7–21. [Google Scholar]

- Fuà, G. L’industrializzazione nel nord est e nel centro. In Industrializzazione Senza Fratture; Fuà, G., Zacchia, C., Eds.; Mulino Il: Bologna, Italy, 1983; pp. 7–46. [Google Scholar]

- Garofoli, G. Endogenous Development and Southern Europe; Avebury: Aldershot, UK, 1992. [Google Scholar]

- Stöhr, W.B.; Taylor, D.R. Development from below: The bottom-up and periphery inward development paradigm. In Development from Above or Below? Stöhr, W.B.; Taylor, D.R. Wiley and Sons: Chichester, UK, 1981; pp. 39–72. [Google Scholar]

- Vázquez-Barquero, A. Local development and regional state in Spain. Pap. Reg. Sci. Assoc. 1987, 61, 65–78. [Google Scholar] [CrossRef]

- Aydalot, P. Milieux Innovateurs en Europe; Economica: Paris, France, 1986. [Google Scholar]

- Friedmann, J.; Weaver, C. Territory and Function: The Evolution of Regional Planning; University of California Press: Berkeley, CA, USA, 1979. [Google Scholar]

- Sachs, I. Stratégies de L’écodéveloppement; Les Éditions Ouvriéres: Paris, France, 1980. [Google Scholar]

- Vázquez-Barquero, A. Endogenous Development: Networking, Innovation, Institutions and Cities; Routledge: London, UK, 2002. [Google Scholar]

- Vázquez-Barquero, A.; Rodríguez-Cohard, J.C. Endogenous development and institutions: Challenges for local development initiatives. Environ. Plan. C Gov. Policy 2016, 34, 1135–1153. [Google Scholar] [CrossRef]

- FAO. Food Outlook. Biannual Report on Global Food Markets, June 2020; Food and Agriculture Organization of the United Nations: Rome, Italy, 2020. [Google Scholar] [CrossRef]

- Maudos, J.; Salamanca, J. Observatorio Sobre el Sector Agroalimentario Español en el Contexto Europeo; Cajamar Caja Rural: Almería, Spain, 2020. [Google Scholar]

- Caldentey, P. Nueva Economía Agroalimentaria; Editorial Agrícola Española: Madrid, Spain, 1998. [Google Scholar]

- Juste-Carrión, J.J. Producción y exportación de vino en España: El caso de Castilla y León. Estudios de Economía Aplicada 2017, 35, 153–188. [Google Scholar] [CrossRef]

- Juste Carrión, J.J. Industria agroalimentaria, desarrollo rural y sistemas productivos locales en Castilla y León. Cuadernos de Estudios Agroalimentarios 2011, 2, 219–252. [Google Scholar]

- OIV. Note de Conjoncture Vitivinicole Mondiale 2020; Organisation Internationale de la Vigne et du Vin: Paris, France, 2021. [Google Scholar]

- Alimarket. Informe 2021 del sector del Aceite de Oliva en España. Más Envasado Menos Precio; Publicaciones Alimarket: Madrid, Spain, 2021. [Google Scholar]

- IOC. World Olive Oil and Table Olive Figures; International Olive Council: Madrid, Spain, 2021; Available online: https://www.internationaloliveoil.org/what-we-do/economic-affairs-promotion-unit/#figures (accessed on 27 October 2021).

- INE (Instituto Nacional de Estadística). Estadística Estructural de Empresas: Sector Industrial; Instituto Nacional de Estadística: Madrid, Spain, 2019. [Google Scholar]

- Eurostat. Annual Enterprise Statistics for Special Aggregates of Activities (NACE Rev.2); Eurostat: Brussels, Belgium, 2021; Available online: https://ec.europa.eu/eurostat/databrowser/view/SBS_NA_SCA_R2__custom_1437860/default/table?lang=en (accessed on 27 October 2021).

- MERCASA. Alimentación en España. Producción, Industria, Distribución y Consumo; Mercasa-Distribución y Consumo: Madrid, Spain, 2021. [Google Scholar]

- Ministerio de Agricultura, Pesca y Alimentación. In Anuario de Estadística 2020; MAPA: Madrid, Spain, 2021.

- Ministerio de Agricultura, Pesca y Alimentación. In Avances de Superficies y Producciones de Cultivos, March 2021; MAPA: Madrid, Spain, 2021.

- SEVI. Balance de campaña del aceite de oliva a 30 de septiembre de 2020. La Sem. Vitivinícola 2021, 3578, 1795–1798. [Google Scholar]

- Ministerio de Agricultura, Pesca y Alimentación. In Datos de las Denominaciones de Origen protegidas de vinos (DOPs) campaña 2018/2019; MAPA: Madrid, Spain, 2020.

- Ministerio de Agricultura, Pesca y Alimentación. Datos de las Denominaciones de Origen Protegidas (D.O.P.), Indicaciones Geográficas Protegidas (I.G.P.) y Especialidades Tradicionales Garantizadas (E.T.G.) de Productos Agroalimentarios, año 2019; MAPA: Madrid, Spain, 2020. [Google Scholar]

- Bortolotti, T.; Boscari, S.; Danese, P. Successful lean implementation: Organizational culture and soft lean practices. Int. J. Prod. Econ. 2015, 160, 182–201. [Google Scholar] [CrossRef] [Green Version]

- Lisi, I.E. Translating environmental motivations into performance: The role of environmental performance measurement systems. Manag. Account. Res. 2015, 29, 27–44. [Google Scholar] [CrossRef]

- Neuman, W.L. Social Research Methods: Qualitative and Quantitative Approaches; Pearson: Boston, MA, USA, 2011. [Google Scholar]

- Carson, D.; Gilmore, A.; Perry, C.; Gronhaug, K. Qualitative Marketing Research; Sage: Thousand Oaks, CA, USA, 2001. [Google Scholar]

- Burns, N.; Grove, S.K. The Practice of Nursing Research: Appraisal, Synthesis and Generation of Evidence; Elsevier: St. Louis, MO, USA, 2009. [Google Scholar]

- Khan, S.H. Qualitative research method—Phenomenology. Asian Soc. Sci. 2014, 10, 298–310. [Google Scholar] [CrossRef] [Green Version]

- Juste Carrión, J.J. The Wine Industry in Spain: The case of Castile and Leon. In Proceedings of the American Association of Wine Economists (AAWE) 10th Annual Conference, Bordeaux, France, 21–25 June 2017. [Google Scholar]

- Rodríguez Cohard, J.C.; Sánchez Martínez, J.D.; Garrido Almonacid, A. Strategic responses of the European olive-growing territories to the challenge of globalization. Eur. Plan. Stud. 2020, 28, 2261–2283. [Google Scholar] [CrossRef]

- Rodríguez-Cohard, J.C.; Sánchez-Martínez, J.D.; Gallego Simón, V.J. Olive crops and rural development: Capital, knowledge and tradition. Reg. Sci. Policy Pract. 2019, 11, 935–949. [Google Scholar] [CrossRef]

- Rodríguez-Cohard, J.C.; Sánchez Martínez, J.D.; Gallego Simón, V.J. The upgrading strategy of olive oil producers in Southern Spain: Origin, development and constraints. Rural. Soc. 2017, 26, 30–47. [Google Scholar] [CrossRef]

- Sánchez-Martínez, J.D.; Rodríguez-Cohard, J.C.; Garrido-Almonacid, A.; Gallego Simón, V.J. Social Innovation in Rural Areas? The Case of Andalusian Olive Oil Co-Operatives. Sustainability 2020, 12, 10019. [Google Scholar] [CrossRef]

- Hristov, I.; Chirico, A.; Ranalli, F. Corporate strategies oriented towards sustainable governance: Advantages, managerial practices and main challenges. J. Manag. Gov. 2021, 1–23. [Google Scholar] [CrossRef]

- Glaser, B.G.; Strauss, A.L. The Discovery of Grounded Theory. Strategies for Qualitative Research; Aldine Transaction: New Brunswick, NJ, USA, 2012. [Google Scholar]

- Berelson, B. Content analysis in Communication Research; The Free Press: New York, NY, USA, 1952. [Google Scholar]

- Pool, J. Trends in Content Analysis; University of Illinois Press: Urbana-Champaign, IL, USA, 1959. [Google Scholar]

- Maxwell, J. Qualitative Research Design. An Interactive Approach; Sage: London, UK, 1996. [Google Scholar]

- Mayring, P. Qualitative content analysis. Forum Qual. Soc. Res. 2020, 1, 159–176. Available online: http://nbn-resolving.de/urn:nbn:de:0114-fqs0002204 (accessed on 17 November 2021).

- Braun, V.; Clarke, V. Using thematic analysis in psychology. Qual. Res. Psychol. 2006, 3, 77–101. [Google Scholar] [CrossRef] [Green Version]

- Trichopoulou, A.; Lagiou, P. Healthy traditional Mediterranean diet: An expression of culture, history, and lifestyle. Nutr. Rev. 1997, 55, 383–389. [Google Scholar] [CrossRef] [PubMed]

- Vázquez-Barquero, A.; Rodríguez-Cohard, J.C. Local development in a global world: Challenges and opportunities. Reg. Sci. Policy Pract. 2019, 11, 885–897. [Google Scholar] [CrossRef]

- Schumpeter, J.A. The Theory of Economic Development Harvard; University Press: Cambridge, MA, USA, 1934. [Google Scholar]

- Heijman, W.; Hagelaar, G.; van der Heide, M. Rural Resilience as a New Development Concept. In EU Bioeconomy Economics and Policies: Volume II. Palgrave Advances in Bioeconomy: Economics and Policies; Dries, L., Heijman, W., Jongeneel, R., Purnhagen, K., Wesseler, J., Eds.; Palgrave Macmillan: Cham, Switzerland, 2019. [Google Scholar] [CrossRef]

- Putnam, R.D. Bowling Alone: The Collapse and Revival of American Community; Simon and Schuster: New York, NJ, USA, 2000. [Google Scholar]

- Delgado Viñas, C. Depopulation processes in European rural areas: A case study of cantabria (Spain). Eur. Countrys. 2019, 11, 341–369. [Google Scholar] [CrossRef] [Green Version]

- Pérez, C. Technological revolutions and techno-economic paradigms. Camb. J. Econ. 2010, 34, 185–202. [Google Scholar] [CrossRef] [Green Version]

- Cohen, W.N.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Pérez, C. Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages; Edward Elgar: Cheltenham, UK, 2002. [Google Scholar]

- Arrow, K.J. The economic implications of learning by doing. Rev. Econ. Stud. 1962, 29, 155–173. [Google Scholar] [CrossRef]

- Dei Ottati, G. Social Concertation and Local Development: The case of Industrial Districts. Eur. Plan. Stud. 2002, 10, 449–466. [Google Scholar] [CrossRef]

- Teece, D.; Pisano, G. The dynamic capabilities of firms: An introduction. Ind. Corp. Chang. 1994, 3, 537–556. [Google Scholar] [CrossRef] [Green Version]

- MAPA (Ministerio de Agricultura Pesca y Alimentación). Digitisation Strategy for the Agri-Food and Forestry Sectors and Rural Areas; MAPA: Madrid, Spain, 2019. [Google Scholar]

- Elabed, G.; Lampieti, J.; Schroeder, K. What’s Cooking: Digital Transformation of the Agri-Food Systems; World Bank Group: Washington, DC, USA, 2021. [Google Scholar]

- Mazzucato, M.; Kattel, R. COVID-19 and public-sector capacity. Oxf. Rev. Econ. Policy 2020, 36, S256–S269. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Spain | EU-28 | |||||||

|---|---|---|---|---|---|---|---|---|

| Agriculture | Food, Beverages, and Tobacco | Agri-Food Sector | Expanded Agri-Food Sector | Agriculture | Food, Beverages, and Tobacco | Agri-Food Sector | Expanded Agri-Food Sector | |

| 2008 | 2.6 | 2.4 | 5.0 | 7.9 | 1.7 | 2.0 | 3.7 | 6.1 |

| 2009 | 2.4 | 2.4 | 4.8 | 7.9 | 1.6 | 2.1 | 3.6 | 6.2 |

| 2010 | 2.7 | 2.5 | 5.1 | 8.4 | 1.7 | 2.0 | 3.7 | 6.2 |

| 2011 | 2.6 | 2.6 | 5.2 | 8.6 | 1.7 | 2.0 | 3.7 | 6.2 |

| 2012 | 2.6 | 2.6 | 5.2 | 8.8 | 1.7 | 2.0 | 3.7 | 6.3 |

| 2013 | 2.9 | 2.6 | 5.5 | 9.2 | 1.9 | 2.1 | 4.0 | 6.5 |

| 2014 | 2.8 | 2.6 | 5.4 | 9.0 | 1.8 | 2.1 | 3.9 | 6.5 |

| 2015 | 3.0 | 2.5 | 5.5 | 9.2 | 1.8 | 2.1 | 3.9 | 6.4 |

| 2016 | 3.1 | 2.5 | 5.6 | 9.3 | 1.8 | 2.1 | 3.9 | 6.4 |

| 2017 | 3.1 | 2.4 | 5.5 | 9.3 | 1.9 | 2.1 | 3.9 | 6.5 |

| 2018 | 3.1 | 2.3 | 5.4 | 9.0 | 1.8 | 2.0 | 3.8 | 6.4 |

| 2019 | 2.9 | 2.4 | 5.3 | 8.9 | 1.8 | 2.0 | 3.8 | 6.3 |

| 2020 | 3.4 | 2.4 | 5.8 | 9.7 | 1.9 | 1.9 | 3.8 | 6.5 |

| Designation of Origin | Surface Hectares | Number Winegrowers | Number Wineries | Volume of Qualified Wine | Total Trade Hectoliters | Exports in Volume (%) | Total Trade EUR | Exports in Value (%) | Av. Price EUR/Liter |

|---|---|---|---|---|---|---|---|---|---|

| Rioja | 66,239 | 14,882 | 773 | 3,434,068 | 2,597,136 | 36.4 | 988,153,761 | 46.5 | 3.80 |

| Cava | 37,955 | 6582 | 357 | 2,154,267 | 1,834,248 | 66.8 | 733,100,903 | 49.9 | 4.00 |

| Ribera del Duero | 23,314 | 8060 | 316 | 334,901 | 625,532 | 11.9 | 287,919,443 | 28.0 | 4.60 |

| La Mancha | 156,840 | 14,843 | 246 | 375,272 | 426,495 | 48.9 | 114,855,170 | 38.3 | 2.69 |

| Cataluña | 41,427 | 6534 | 205 | 361,061 | 428,634 | 42.7 | 120,449,539 | 41.3 | 2.81 |

| Penedés | 16,500 | 2050 | 180 | 142,627 | 136,006 | 27.7 | 92,946,265 | 32.1 | 6.83 |

| Rías Baixas | 4051 | 5177 | 178 | 267,572 | 267,568 | 29.2 | 172,677,709 | 25.4 | 6.45 |

| Ribeiro | 1369 | 1658 | 110 | 85,460 | 91,502 | 9.1 | 77,252,394 | 15.8 | 8.44 |

| Priorat | 2041 | 531 | 109 | 11,011 | 29,776 | 52.6 | 27,479,200 | 50.8 | 9.23 |

| Utiel-Requena | 33,886 | 4977 | 107 | 486,324 | 231,476 | 66.1 | 70,417,462 | 66.8 | 3.04 |

| Valencia | 13,069 | 6150 | 103 | 468,415 | 424,177 | 62.6 | 109,879,654 | 56.7 | 2.59 |

| Navarra | 10,273 | 1859 | 97 | 483,545 | 333,816 | 30.4 | 69,240,342 | 36.3 | 2.07 |

| Ribeira sacra | 1236 | 2376 | 94 | 24,643 | 37,800 | 4.0 | 26,682,509 | 9.7 | 7.06 |

| Bierzo | 2450 | 1309 | 78 | 34,610 | 83,240 | 20.3 | 34,959,736 | 20.3 | 4.20 |

| Jerez-Xérès-Sherry | 7185 | 1591 | 73 | 506,720 | 234,289 | 78.3 | 70,286,700 | 78.3 | 3.00 |

| Gran Canaria | 219 | 311 | 71 | 1937 | 2730 | 4.5 | 2,652,699 | 3.3 | 9.72 |

| Rueda | 18,051 | 1579 | 69 | 766,394 | 767,712 | 10.7 | 214,959,360 | 10.7 | 2.80 |

| Toro | 5715 | 987 | 65 | 118,127 | 103,854 | 38.0 | 48,466,062 | 38.0 | 4.67 |

| Terra Alta | 6032 | 1244 | 59 | 77,107 | 44,383 | 15.7 | 12,738,533 | 26.6 | 2.87 |

| Montsant | 1810 | 602 | 57 | 48,365 | 42,191 | 30.7 | 15,426,856 | 26.4 | 3.66 |

| TOP 20 by n. Wineries | 449,662 | 83,302 | 3347 | 10,182,426 | 8,742,565 | 41.6 | 3,290,544,297 | 40.9 | 3.76 |

| Total Spain | 569,560 | 110,013 | 4133 | 13,574,234 | 11,209,086 | 41.3 | 3,985,946,504 | 40.1 | 3.56 |

| Top 20/Total Spain (%) | 78.95 | 75.72 | 80.98 | 75.01 | 78.00 | 82.55 |

| Designation of Origin | Surface Hectares | Number Farmers | Number of Mills | Packaging | Total Tons | Production | Trade | Exports | Av. Price | Economic |

|---|---|---|---|---|---|---|---|---|---|---|

| Trading Firms | Production | Protect. POD | Protect. POD | Value % | EUR/kg | Value (th. EUR) | ||||

| Baena | 60,000 | 8078 | 17 | 30 | 52,041 | 52,041 | 6938 | 55.2 | 5.50 | 38,160 |

| Priego de Córdoba | 29,628 | 6537 | 13 | 12 | 17,665 | 7066 | 2163 | 33.1 | 6.80 | 14,710 |

| Siurana | 9173 | 4922 | 29 | 29 | 2361 | 2356 | 2356 | 9.8 | 4.38 | 10,320 |

| Sierra de Cazorla | 37,700 | 11,200 | 10 | 20 | 6000 | 5000 | 3500 | 14.3 | 2.60 | 9100 |

| Les Garrigues | 16,107 | 2661 | 17 | 22 | 3286 | 3286 | 1606 | 1.7 | 5.24 | 8420 |

| Estepa | 40,039 | 4148 | 17 | 2 | 12,500 | 3159 | 3129 | 44.1 | 2.60 | 8140 |

| Aceite Bajo Aragón | 21,177 | 3289 | 33 | 5 | 7550 | 2098 | 2098 | 2.5 | 3.50 | 7340 |

| Montes de Toledo | 35,000 | 8500 | 29 | 29 | 23,000 | 15,000 | 1100 | 55.0 | 6.50 | 7150 |

| Sierra Mágina | 60,000 | 11,652 | 23 | 20 | 11,265 | 10,125 | 2140 | 2.7 | 3.10 | 6640 |

| Sierra de Segura | 35,064 | 9817 | 21 | 21 | 4654 | 4654 | 816 | 1.6 | 6.04 | 4930 |

| Aceite de Mallorca | 3872 | 994 | 13 | 22 | 464 | 252 | 293 | 16.1 | 11.85 | 3470 |

| Aceite de la Rioja | 688 | 1290 | 13 | 45 | 425 | 302 | 301 | 6.1 | 10.35 | 3120 |

| Campo de Montiel | 28,986 | 6690 | 11 | 8 | 3657 | 2717 | 875 | 45.4 | 3.00 | 2620 |

| Aceite de Terra Alta | 3320 | 1312 | 7 | 19 | 527 | 502 | 502 | 1.8 | 4.50 | 2260 |

| Antequera | 42,509 | 4934 | 13 | 2 | 2856 | 918 | 780 | 16.7 | 2.36 | 1840 |

| Sierra de Cádiz | 28,000 | 2160 | 4 | 4 | 3266 | 543 | 399 | 0.0 | 3.65 | 1460 |

| Aceite de L’Empordà | 800 | 303 | 5 | 2 | 182 | 182 | 182 | 0.0 | 5.58 | 1010 |

| Baix Ebre-Montsià | 12,111 | 3300 | 11 | 5 | 179 | 179 | 179 | 6.8 | 5.54 | 990 |

| Poniente de Granada | 27,013 | 5700 | 13 | 21 | 28,831 | 1065 | 318 | 0.0 | 2.60 | 830 |

| Aceite de la Alcarria | 28,335 | 543 | 4 | 4 | 1180 | 146 | 127 | 0.9 | 5.18 | 650 |

| Top 20 by Econ. Value Wineries | 519,522 | 98,030 | 303 | 322 | 181,888 | 111,590 | 29,801 | 26.9 | 4.47 | 133.160 |

| Total Spain | 709,501 | 128,834 | 361 | 370 | 255,767 | 112,758 | 30,318 | 26.5 | 4.45 | 134,950 |

| Top 20/Total Spain (%) | 73.22 | 76.09 | 83.93 | 87.03 | 71.11 | 98.96 | 98.30 | 99.9 | - | 98.67 |

| Attribute | Modality | Percentage |

|---|---|---|

| Gender | Male | 62.5 |

| Female | 37.5 | |

| Age | ≥50 | 43.75 |

| 41–44 | 37.5 | |

| ≤40 | 18.75 | |

| Job position | Top manager | 68.75 |

| Middle manager | 31.25 | |

| Experience in the activity | ≥10 years | 62.5 |

| 6–9 years | 25 | |

| ≤5 years | 12.5 | |

| Academic background | Doctoral studies | 12.5 |

| Bachelor’s | 68.75 | |

| Secondary | 18.75 |

| Countries | 2001 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | Cons.pc |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| France | 14.9 | 11.7 | 11.5 | 11.5 | 11.4 | 11.2 | 11.6 | 11.6 | 10.6 | 10.3 | 10.6 | 46.0 |

| Italy | 13.3 | 9.1 | 8.9 | 8.6 | 8.1 | 8.8 | 9.2 | 9.2 | 9.2 | 9.5 | 10.5 | 46.6 |

| Germany | 8.8 | 8.1 | 8.3 | 8.4 | 8.4 | 8.4 | 8.3 | 8.0 | 8.2 | 8.2 | 8.5 | 27.5 |

| Spain | 6.3 | 4.1 | 4.1 | 4.0 | 4.1 | 4.0 | 4.1 | 4.3 | 4.5 | 4.3 | 4.1 | 23.9 |

| Portugal | 2.1 | 2.0 | 2.1 | 1.7 | 1.8 | 2.0 | 1.9 | 2.1 | 2.1 | 1.9 | 2.0 | 51.9 |

| Romania | 2.1 | 1.7 | 1.8 | 1.9 | 1.9 | 1.6 | 1.6 | 1.7 | 1.6 | 1.6 | 1.6 | 23.5 |

| The Netherlands | 1.5 | 1.4 | 1.4 | 1.4 | 1.4 | 1.4 | 1.5 | 1.5 | 1.5 | 1.5 | 1.5 | 24.2 |

| Belgium | 1.1 | 1.2 | 1.2 | 1.2 | 1.1 | 1.2 | 1.1 | 1.1 | 1.1 | 1.1 | 1.1 | 26.9 |

| Austria | 1.0 | 1.0 | 1.1 | 1.2 | 1.2 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 29.9 |

| Sweden | 0.6 | 0.9 | 0.9 | 1.0 | 1.0 | 0.9 | 1.0 | 0.9 | 0.9 | 1.0 | 0.9 | 27.0 |

| Czechia | 0.4 | 0.9 | 0.7 | 0.7 | 0.7 | 0.8 | 0.9 | 0.9 | 0.9 | 0.9 | 0.9 | 23.2 |

| Others EU-27 | 6.7 | 6.9 | 6.7 | 7.6 | 6.8 | 5.6 | 6.7 | 6.0 | 4.7 | 6.8 | 5.3 | - |

| EU-27 | 58.6 | 49.0 | 48.7 | 49.1 | 47.8 | 47.2 | 48.7 | 48.4 | 46.2 | 47.9 | 47.9 | 22.1 |

| United Kingdom | 4.5 | 5.3 | 5.3 | 5.2 | 5.2 | 5.2 | 5.3 | 5.3 | 5.3 | 5.4 | 5.7 | 23.8 |

| Switzerland | 1.4 | 1.2 | 1.1 | 1.2 | 1.2 | 1.2 | 1.1 | 1.1 | 1.1 | 1.1 | 1.1 | 35.7 |

| Russia | 2.7 | 5.2 | 4.6 | 4.3 | 4.6 | 4.4 | 4.1 | 4.2 | 4.1 | 4.2 | 4.4 | 8.6 |

| United States | 9.3 | 12.0 | 12.3 | 12.7 | 12.7 | 12.7 | 12.8 | 12.8 | 13.3 | 13.7 | 14.1 | 12.2 |

| Canada | 1.2 | 1.9 | 2.0 | 2.0 | 1.9 | 2.0 | 2.0 | 2.0 | 2.0 | 2.0 | 1.9 | 13.9 |

| Argentina | 5.3 | 4.0 | 4.1 | 4.3 | 4.1 | 4.2 | 3.8 | 3.6 | 3.4 | 3.7 | 4.0 | 27.6 |

| Brazil | 1.4 | 1.5 | 1.3 | 1.4 | 1.3 | 1.4 | 1.3 | 1.3 | 1.4 | 1.5 | 1.8 | 2.6 |

| China | 4.8 | 6.8 | 7.6 | 7.7 | 7.2 | 7.5 | 7.9 | 7.9 | 7.2 | 6.2 | 5.3 | 1.0 |

| Japan | 1.2 | 1.1 | 1.3 | 1.4 | 1.5 | 1.4 | 1.4 | 1.4 | 1.4 | 1.5 | 1.5 | 3.1 |

| Australia | 1.7 | 2.2 | 2.2 | 2.2 | 2.2 | 2.3 | 2.2 | 2.4 | 2.5 | 2.4 | 2.4 | 27.8 |

| South Africa | 1.7 | 1.5 | 1.5 | 1.5 | 1.7 | 1.8 | 1.8 | 1.8 | 1.8 | 1.6 | 1.3 | 7.4 |

| Rest of the world | 6.1 | 8.2 | 8.0 | 6.7 | 8.6 | 8.8 | 7.5 | 7.6 | 10.6 | 8.8 | 8.5 | - |

| World Total (%) | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | - |

| World (million hl.) | 227.5 | 242.5 | 243.5 | 242.0 | 241.2 | 242.9 | 244.4 | 245.5 | 244.4 | 240.9 | 233.9 | - |

| Countries | 2001–2002 | 2011–2012 | 2012–2013 | 2013–2014 | 2014–2015 | 2015–2016 | 2016–2017 | 2017–2018 | 2018–2019 | 2019–2020 | 2020–2021 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Spain | 24.2 | 18.6 | 16.3 | 17.1 | 16.9 | 16.6 | 16.2 | 15.7 | 16.2 | 16.3 | 17.0 |

| Italy | 28.2 | 19.8 | 18.4 | 20.8 | 19.6 | 20.1 | 16.1 | 19.1 | 14.8 | 15.2 | 16.0 |

| France | 3.6 | 3.6 | 3.8 | 3.6 | 3.6 | 3.8 | 4.0 | 3.4 | 4.5 | 3.7 | 3.7 |

| Greece | 10.4 | 6.5 | 6.0 | 4.6 | 4.5 | 4.7 | 3.9 | 4.3 | 3.9 | 3.6 | 3.6 |

| Portugal | 2.4 | 2.5 | 2.5 | 2.4 | 2.4 | 2.3 | 2.6 | 2.5 | 1.8 | 2.5 | 2.5 |

| Germany | 1.5 | 2.0 | 2.0 | 2.1 | 2.2 | 2.1 | 2.2 | 2.0 | 2.1 | 1.7 | 1.8 |

| Others EU-27 | 1.8 | 3.3 | 3.4 | 3.6 | 3.7 | 3.9 | 3.9 | 3.5 | 3.8 | 3.3 | 3.8 |

| EU-27 | 72.1 | 56.3 | 52.4 | 54.3 | 52.9 | 53.5 | 48.9 | 50.4 | 47.2 | 46.3 | 48.5 |

| United States | 7.2 | 9.7 | 9.6 | 9.8 | 10.1 | 10.8 | 11.6 | 10.4 | 11.5 | 12.4 | 11.2 |

| Turkey | 2.1 | 4.9 | 5.0 | 3.4 | 4.3 | 3.9 | 5.5 | 5.8 | 5.3 | 5.4 | 5.3 |

| Morocco | 2.3 | 4.0 | 4.3 | 3.9 | 4.1 | 4.0 | 4.4 | 3.9 | 4.9 | 4.3 | 4.4 |

| Brazil | 0.9 | 2.2 | 2.4 | 2.4 | 2.3 | 1.7 | 2.2 | 2.5 | 2.8 | 3.2 | 3.0 |

| Syria | 3.3 | 4.4 | 5.4 | 5.5 | 4.3 | 3.5 | 3.6 | 2.6 | 2.5 | 2.8 | 2.7 |

| Algeria | 1.0 | 1.4 | 2.0 | 1.6 | 2.2 | 2.7 | 2.5 | 2.7 | 3.0 | 3.9 | 2.7 |

| Japan | 1.2 | 1.4 | 1.7 | 1.8 | 2.0 | 1.8 | 2.0 | 1.8 | 2.3 | 2.1 | 2.4 |

| China | 0.0 | 1.3 | 1.3 | 1.0 | 1.1 | 1.3 | 1.6 | 1.4 | 1.7 | 1.8 | 2.1 |

| Australia | 1.1 | 1.3 | 1.2 | 1.2 | 1.3 | 1.4 | 1.7 | 1.6 | 1.6 | 1.6 | 1.6 |

| United Kingdom | 1.0 | 1.9 | 2.1 | 2.0 | 2.2 | 2.2 | 2.6 | 2.1 | 2.2 | 0.7 | 1.6 |

| Canada | 0.9 | 1.3 | 1.2 | 1.3 | 1.3 | 1.4 | 1.4 | 1.5 | 1.5 | 1.8 | 1.5 |

| Egypt | 0.1 | 0.2 | 0.4 | 0.6 | 0.7 | 0.6 | 0.8 | 1.3 | 1.5 | 1.2 | 1.3 |

| Tunisia | 1.1 | 1.1 | 1.3 | 1.2 | 1.0 | 1.2 | 0.8 | 1.3 | 1.3 | 1.5 | 1.1 |

| Saudi Arabia | 0.2 | 0.5 | 0.7 | 0.7 | 0.9 | 0.8 | 1.0 | 1.1 | 1.2 | 1.2 | 1.1 |

| Israel | 0.6 | 0.5 | 0.7 | 0.7 | 0.7 | 0.7 | 0.8 | 0.7 | 0.8 | 0.9 | 0.9 |

| Jordan | 0.8 | 0.6 | 0.7 | 0.8 | 0.8 | 1.0 | 0.7 | 0.7 | 0.7 | 0.9 | 0.8 |

| Russia | 0.2 | 0.8 | 0.9 | 1.0 | 0.7 | 0.7 | 0.7 | 0.7 | 0.8 | 0.8 | 0.7 |

| Rest of the world | 4.2 | 6.3 | 6.6 | 6.8 | 7.2 | 7.0 | 7.4 | 7.3 | 7.3 | 7.2 | 7.2 |

| World Total (%) | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

| World (1.000 tn) | 2606.5 | 3085.5 | 2989.0 | 3075.5 | 2916.0 | 2979.5 | 2726.0 | 3039.0 | 3057.0 | 3234.0 | 3185.5 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rodríguez-Cohard, J.C.; Juste-Carrión, J.J.; Vázquez-Barquero, A. Challenges and Responses of Agri-Food Activities under COVID-19 Pandemic: The Case of the Spanish Territories Producing Wine and Olive Oil. Sustainability 2021, 13, 13610. https://doi.org/10.3390/su132413610

Rodríguez-Cohard JC, Juste-Carrión JJ, Vázquez-Barquero A. Challenges and Responses of Agri-Food Activities under COVID-19 Pandemic: The Case of the Spanish Territories Producing Wine and Olive Oil. Sustainability. 2021; 13(24):13610. https://doi.org/10.3390/su132413610

Chicago/Turabian StyleRodríguez-Cohard, Juan Carlos, Juan José Juste-Carrión, and Antonio Vázquez-Barquero. 2021. "Challenges and Responses of Agri-Food Activities under COVID-19 Pandemic: The Case of the Spanish Territories Producing Wine and Olive Oil" Sustainability 13, no. 24: 13610. https://doi.org/10.3390/su132413610

APA StyleRodríguez-Cohard, J. C., Juste-Carrión, J. J., & Vázquez-Barquero, A. (2021). Challenges and Responses of Agri-Food Activities under COVID-19 Pandemic: The Case of the Spanish Territories Producing Wine and Olive Oil. Sustainability, 13(24), 13610. https://doi.org/10.3390/su132413610