Environmental Sustainability in Viticulture as a Balanced Scorecard Perspective of the Wine Industry: Evidence for the Portuguese Region of Alentejo

Abstract

:1. Introduction

2. Previous Research and New Directions on Balanced Scorecard

3. Research Methodology

- Quantitative research. In the present study, data were collected through a questionnaire survey. The questionnaire was developed based on the literature review and the strategic diagnosis of the AWI, as well as on the information collected from the interviews that were carried out and the subsequent qualitative content analysis. The questionnaire was sent electronically after its structure had been validated through a pre-test to a group of experts. The questionnaire was answered y 102 EAs, representing 25.56% of the target population. To identify the perspectives to be included in the BSC, a principal component analysis (PCA) with Varimax orthogonal rotation was performed using the SPSS (version 24.0). The quantitative analysis was complemented with other statistical analyzes.

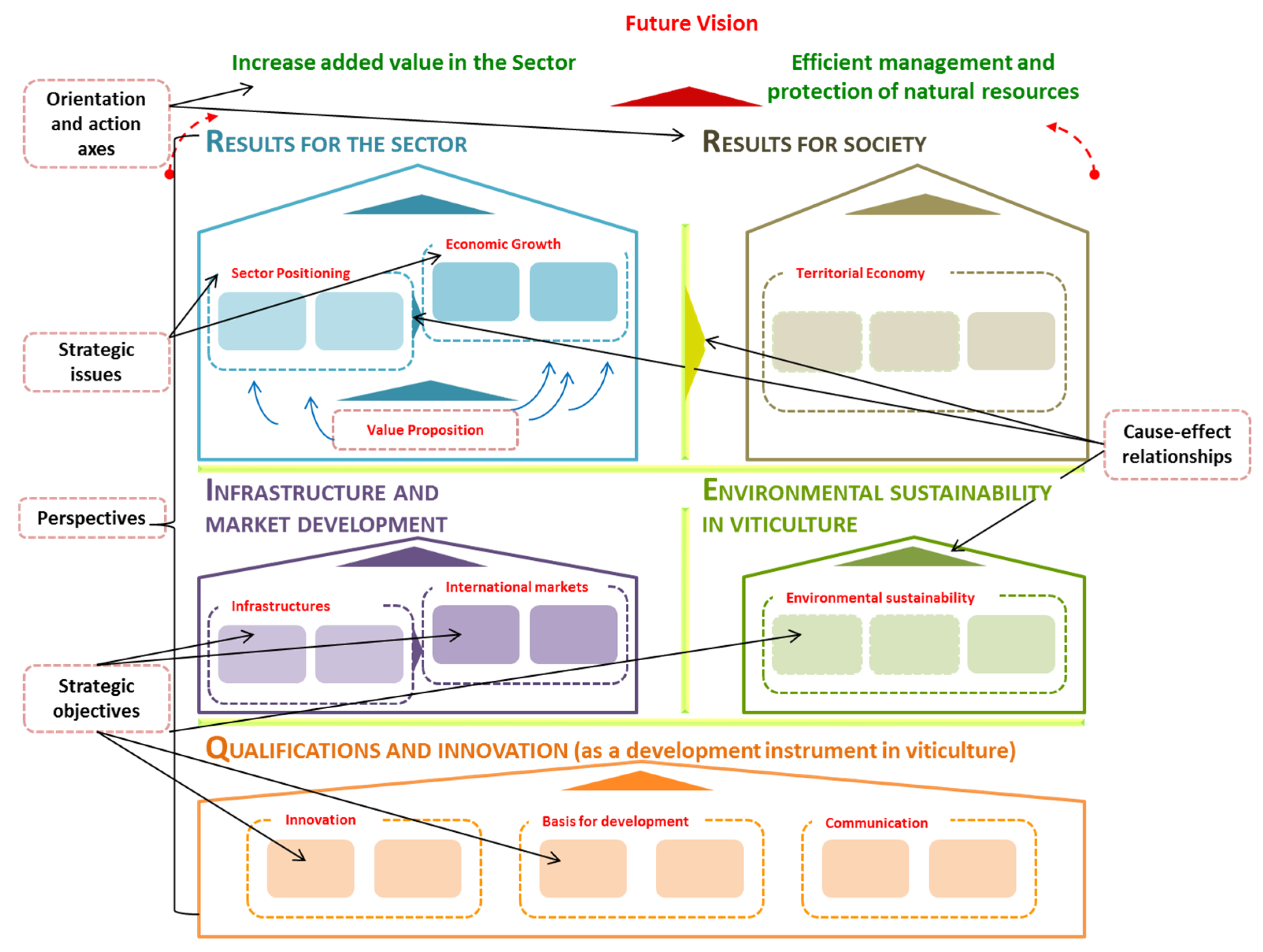

- The application of the PCA to question 14 of the questionnaire (What strategic themes/areas should be assessed in the AWI?), sought to support the identification of perspectives to consider in the development of the BSC for the AWI. That is, the items that constitute this question were included in the PCA to determine the components that would correspond to the perspectives to be considered in the BSC for the AWI. This is why there is an equivalence of the factors of the final PCA solution (five factors) to the BSC perspectives (five perspectives) considered in the development of the Strategic Map for the AWI.

4. Results and Discussion

- Improve communication (between players, for national and international markets, more and better promotion to recruit new consumers and markets and a strong connection to the territory and the ‘Alentejo’ brand) and quality (especially of certified products, working in the dimension of quality perceived by consumers);

- Increasing exports through internationalization (in volume and value), and improving the internationalization process, exploring new markets and products (diversifying the offer, differentiating the product and identifying global consumption trends);

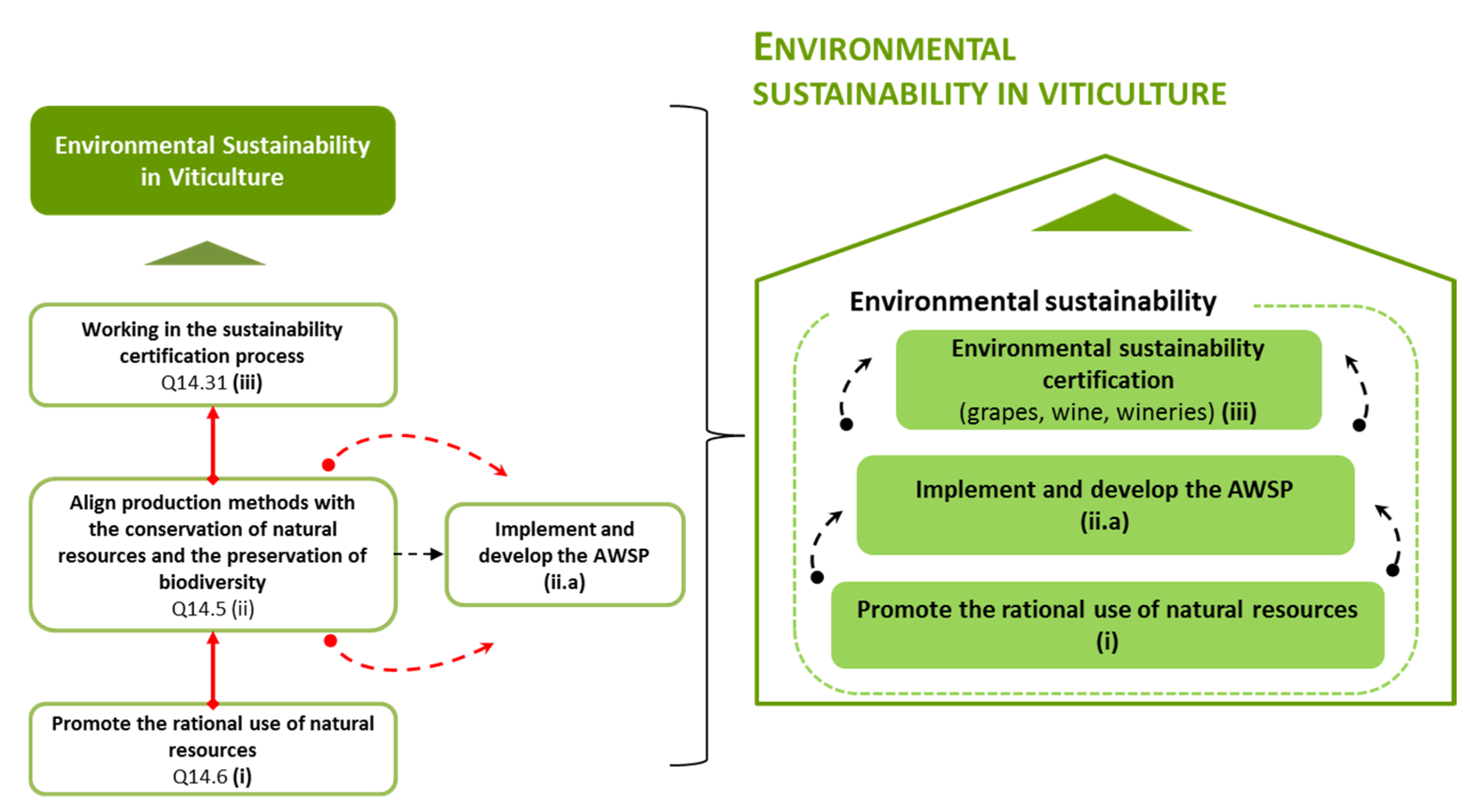

- develop sustainability in Alentejo viticulture (mobilizing producers throughout the industry to adhere to the AWSP and adopt strategies that ensure sustainability, highlighting a potential ‘environmental and social contract’ for future generations in this industry), with growing concern for climate change;

- increase the average value of ‘Alentejo Wineshor (better valuation of the product and the territorial brand).

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Objective | Indicator | Purpose |

|---|---|---|

| Environmental Sustainability Certification (iii) | Environmental Sustainability Certification Document for ‘Alentejo Wines’ | Compile the main rules needed to obtain the seal of environmental sustainability certification for ‘Alentejo Wines’. |

| Date of submission of the Manual to the EAs | ||

| Implement and develop AWSP (ii.a) | Adherence of EAs to AWSP (%) | Identifies the mobilization of EAs to the AWSP (%). |

| (Number of adherents/Total EAs working in the AWI Number of adherents/Total EAs working in the AWI) × 100 | ||

| Area of vineyard registered with the AWC that is covered by the AWSP (%) | Identifies the percentage of vineyard area in the Alentejo region registered in the AWSP. | |

| ∑ vineyard area included in PSVA | ||

| Wine production volume included in AWSP (%) | Inform the percentage of Alentejo wine production that is covered by the AWSP (volume). | |

| (Production volume entered in the AWSP/Production volume (total))/100 | ||

| Number of EAs visited by the AWC to support the self-assessment defined in the AWSP | Inform the number of visits made to the EAs who joined the AWSP and who are in the self-assessment phase, in a given period. | |

| ∑ number of EAs visited to support self-assessment | ||

| Number of EAs visited for validation of the self-assessment defined in the AWSP | Inform the number of visits made to the EAs to validate the self-assessment, in a given period. | |

| ∑ number of EAs visited for self-assessment validation | ||

| Number of EAs participating in workshops on AWSP topics | Inform the number of EAs participating in the AWSP-related workshops, in a given period (includes other partners). | |

| ∑ number of EAs participating in working sessions | ||

| Number of AWSP adherents by category | Identify the number of AWSP members by category (pre-initial, initial, intermediate, developed). | |

| ∑ number of members per category | ||

| Promote the rational use of natural resources (i) | Number of initiatives to promote the preservation of natural resources and biodiversity | Inform the number of EAs participating in initiatives aimed at promoting and preserving natural resources and biodiversity. These initiatives can be broken down into topics: Sustainability and environment; AWSP; Effects of climate change; Use of phytosanitary products; Energy efficiency in wineries, etc. This indicator can evolve to ‘number of sustainable processes’. |

| ∑ number of EAs participating in working sessions | ||

| Record of alternative energy consumption by EAs | Inform the consumption of alternative energy used by EAs in the production process. It allows, in association with the other indicators, to assess the industry’s contribution to the promotion of environmental management in wine-growing activities (greater efficiency in the use of resources). | |

| ∑ alternative energy consumption | ||

| Water recycling (%) | Present the relationship between the water recovered and the water consumed in the production process by the EAs. It allows, in association with the other indicators, to assess the industry’s contribution to promoting the environmental management of wine-growing activities (greater efficiency in the use of resources). | |

| ∑ water recycling (m3)/∑ water consumption (m3) | ||

| Quantity of recovered waste | Present the quantity of solid waste that is recovered through reuse, recycling or incineration in waste incineration facilities with energy recovery. It allows, in association with the other indicators, to assess the Sector’s contribution to the promotion of environmental management of wine-growing activities (greater efficiency in the use of resources). | |

| ∑ quantity of recovered waste | ||

| Environmental costs | Present the total environmental costs concerning the management of energy, water, waste and gaseous emissions. Allows EAs to identify the most sustainable processes for their activity, maintaining their competitiveness. Energy (costs associated with consumption); Water (treatment costs, fees, etc.); Waste (costs of transportation, disposal, treatment, etc.); Gaseous emissions (treatment costs, etc.). | |

| ∑ environmental costs related to treatment, transport, taxes, disposal, etc. (energy, water, waste and gaseous emissions). | ||

References

- Anthony, R.; Govindarajan, V. Management Control Systems; McGraw-Hill: New York, NY, USA, 2004. [Google Scholar]

- Kaplan, R.; Norton, D. The Execution Premium: Linking Strategy to Operations for Competitive Advantage; Harvard Business Press: Boston, MA, USA, 2008. [Google Scholar]

- Jordão, R.V.D.; Novas, J. A study on the use of the Balanced Scorecard for strategy implementation in a Large Brazilian Mixed Economy Company. J. Technol. Manag. Innov. 2013, 8, 98–107. [Google Scholar] [CrossRef]

- Jordão, R.V.D.; Novas, J. Knowledge management and intellectual capital in networks of small- and medium-sized enterprises. J. Intellect. Cap. 2017, 18, 667–692. [Google Scholar] [CrossRef] [Green Version]

- Jordão, R.V.D.; Sousa Neto, J.A.; Ferreira, E.P. Financial disclosure and corporate social environmental responsability. An empirical study on the Brazilian market. Contad. Adm. 2018, 63, 1–29. [Google Scholar] [CrossRef] [Green Version]

- Petera, P.; Wagner, J.; Šoljaková, L. Strategic management accounting and strategic management: The mediating effect of performance evaluation and rewarding. Int. J. Ind. Eng. Manag. 2020, 11, 116–132. [Google Scholar] [CrossRef]

- Kumar, S.; Sureka, R.; Lim, W.M.; Kumar Mangla, S.; Goyal, N. What do we know about business strategy and environmental research? Insights from Business Strategy and the Environment. Bus. Strategy Environ. 2021, (in press). [Google Scholar] [CrossRef]

- Epstein, M.; Manzoni, J. The Balanced Scorecard and Tableaux de Bord: A global perspective on translating strategy into action. Manag. Account. 1997, 79, 28–36. [Google Scholar]

- Kaplan, R.; Norton, D. A estratégia em Ação: Balanced Scorecard; Elsevier: Rio de Janeiro, Brazil, 1997. [Google Scholar]

- Niven, P. Balanced Scorecard Step-by-Step: Maximizing Performance and Maintaining results; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2002. [Google Scholar]

- Jordão, R.V.D.; Souza, A.A.; Avelar, E.A. Organizational culture and post-acquisition changes in management control systems: An analysis of a successful Brazilian case. J. Bus. Res. 2014, 67, 542–549. [Google Scholar] [CrossRef]

- Kaplan, R.; Norton, D. The Balanced Scorecard: Measures that Drive Performance. Harv. Bus. Rev. 1992, 70, 71–79. [Google Scholar] [PubMed]

- Kaplan, R.; Norton, D. Putting the Balanced Scorecard to Work. Harv. Bus. Rev. 1993, 71, 134–147. [Google Scholar]

- Kaplan, R.; Norton, D. Using the Balanced Scorecard as a Strategic Management System. Harv. Bus. Rev. 1996, 74, 75–85. [Google Scholar]

- Rafiq, M.; Maqbool, S.; Martins, J.; Mata, M.; Dantas, R.; Naz, S.; Correia, A. A Study on Balanced Scorecard and Its Impact on Sustainable Development of Renewable Energy Organizations: A Mediating Role of Political and Regulatory Institutions. Risks 2021, 9, 110. [Google Scholar] [CrossRef]

- Novas, J.; Alves, M.; Sousa, A. The role of management accounting systems in the development of intellectual capital. J. Intellect. Cap. 2017, 18, 286–315. [Google Scholar] [CrossRef]

- Jordão, R.V.D.; Almeida, V. Performance measurement, intellectual capital & financial sustainability. J. Intellect. Cap. 2017, 18, 643–666. [Google Scholar] [CrossRef]

- Jordão, R.V.D.; Novas, J.; Gupta, V. The role of knowledge-based networks in the intellectual capital and organizational performance of small and medium-sized enterprises. Kybernetes 2019, 49, 116–140. [Google Scholar] [CrossRef]

- Elkington, J. Towards the sustainable corporation: Win-win-win business strategies for sustainable development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Longoni, A.; Cagliano, R. Environmental and social sustainability priorities. Int. J. Oper. Prod. Manag. 2015, 35, 216–245. [Google Scholar] [CrossRef]

- Jordão, R.V.D.; Barbosa, C.R.; Resende, P.T. Domestic Inflation, Cost Management and Control: A Successful Experience at a Brazilian Multinational. J. Educ. Res. Account. 2018, 12, 93–114. [Google Scholar] [CrossRef]

- Peters, J.; Simaens, A. Integrating Sustainability into Corporate Strategy: A Case Study of the Textile and Clothing Industry. Sustainability 2020, 12, 6125. [Google Scholar] [CrossRef]

- United Nations (UN). Process of Preparation of the Environmental Perspective to the Year 2000 Beyond; United Nations: New York, NY, USA, 1983; Available online: http://www.un.org/documents/ga/res(38/a38r161.htm (accessed on 5 December 2020).

- Borowski, P.; Patuk, I. Environmental, social and economic factors in sustainable development with food, energy and eco-space aspect security. Pres. Environ. Sustain. Dev. 2021, 15, 153–169. [Google Scholar] [CrossRef]

- Gabinete de Planeamento, Políticas e Administração Geral do Ministério da Agricultura e do Mar (GPP). Agricultura, Silvicultura e Pesca. Indicadores 2012. O Programa de Desenvolvimento Rural do Continente 2014–2020. Diagnóstico. Ministério da Agricultura e do Mar—Gabinete de Planeamento, Políticas e Administração Geral: Lisbon, Portugal, 2012. Available online: https://www.gpp.pt/images/GPP/O_que_disponibilizamos/Publicacoes/Periodicos/Indicadores2012_agricultura.pdf. (accessed on 1 September 2021).

- Organisation Internationale de la Vigne et du Vin (OIV). Strategic Plan 2020–2024. Organisation Internationale de la Vigne et du Vin: Paris, France, 2019. Available online: https://www.oiv.int/public/medias/7156/en-oiv-strategic-plan-2020-2024-web.pdf. (accessed on 1 September 2021).

- Gonçalves, F.; Carlos, C.; Crespo, L.; Zina, V.; Oliveira, A.; Salvação, J.; Pereira, J.; Torres, L. Soil Arthropods in the Douro Demarcated Region Vineyards: General Characteristics and Ecosystem Services Provided. Sustainability 2021, 13, 7837. [Google Scholar] [CrossRef]

- Organisation Internationale de la Vigne et du Vin (OIV). Guidelines for Sustainable Vitiviniculture: Production, Processing and Packaging of Products; Organisation Internationale de la Vigne et du Vin: Paris, France, 2008; pp. 1–12. [Google Scholar]

- Viers, J.; Williams, J.; Nicholas, K.; Barbosa, O.; Kotzé, I.; Spence, L.; Webb, L.; Merenlender, A.; Reynolds, M. Vinecology: Pairing wine with nature. Conserv. Lett. 2013, 6, 287–299. [Google Scholar] [CrossRef]

- Richter, B.; Hanf, J. Cooperatives in the Wine Industry: Sustainable Management Practices and Digitalisation. Sustainability 2021, 13, 5543. [Google Scholar] [CrossRef]

- Brignall, S. The unbalanced scorecard: A social and environmental critique. In Performance Measurement and Management Conference; 2002; Available online: https://diblokdcma.files.wordpress.com/2009/08/unbalanced-scorecard.pdf (accessed on 5 March 2021).

- Butler, J.; Henderson, S.; Raiborn, C. Sustainability and the Balanced Scorecard: Integrating green measures in business reporting. Manag. Account. Q. 2011, 12, 1–10. [Google Scholar]

- Pravdic, P. Integration of environmental and social aspects into 4 perspectives of BSC. In Proceedings of the 6th International Quality Conference, Center for Quality, Faculty of Engineering, University of Kragujevac, Serbia, 2012. [Google Scholar]

- Quesado, P.; Rodrigues, L.; Guzmán, B. O Balanced Scorecard e a Gestão Ambiental: Um Estudo no setor público e privado português. Revista ABCustos 2013, 8, 30–69. [Google Scholar] [CrossRef]

- Fulop, G.; Hernadi, B.; Jalali, M.; Kavaliauskiene, I.; Ferreira, F. Developing of sustainability Balanced Scorecard for the chemical industry: Preliminary evidence from a case analysis. Inz. Econ.-Eng. Econ. 2014, 25, 341–349. [Google Scholar] [CrossRef] [Green Version]

- Hansen, E.; Schaltegger, S. The sustainability Balanced Scorecard: A systematic review of architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Monteiro, S.; Ribeiro, V. The Balanced Scorecard as a tool for environmental management: Approaching the business context to the public sector. Manag. Environ. Qual. Int. J. 2017, 28, 332–349. [Google Scholar] [CrossRef]

- Rafiq, M.; Zhang, X.; Yuan, J.; Naz, S.; Maqbool, S. Impact of a Balanced Scorecard as a Strategic Management System Tool to Improve Sustainable Development: Measuring the Mediation of Organizational Performance through PLS-Smart. Sustainability 2020, 12, 1365. [Google Scholar] [CrossRef] [Green Version]

- Kaplan, R.; Norton, D. The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment; Harvard Business School Press: Boston, MA, USA, 2000. [Google Scholar]

- Kaplan, R. Conceptual foundations of the Balanced Scorecard; Working Papers 10-074; Harvard Business School: Boston, MA, USA, 2010; pp. 1–36. [Google Scholar]

- Hoque, Z. 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps and opportunities for future research. Br. Account. Rev. 2014, 46, 33–59. [Google Scholar] [CrossRef]

- Confederação Nacional da Indústria (CNI). Mapa Estratégico da indústria, 2013–2022; Confederação Nacional da Indústria: Brasília, Brazil, 2013. [Google Scholar]

- Silva, N. Gestão Estratégica do Crescimento Económico em Portugal: Balanced Scorecard e Enfoque na Produtividade; Vida Económica-Editorial: Oporto, Portugal, 2010. [Google Scholar]

- Pinho, A.; Alves, S.; Pinto, F. A Contabilidade de Gestão nos Serviços Públicos numa perspetiva de Gestão Estratégica. Rev. Port. Contab. 2013, III, 501–528. [Google Scholar]

- Kaplan, R.; Norton, D. Commentary—Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part II. Account. Horiz. 2001, 15, 147–160. [Google Scholar] [CrossRef]

- Kaplan, R.; Norton, D. Strategy Maps: Converting Intangible Assets into Tangible Outcomes; Harvard Business School Press: Boston, MA, USA, 2004. [Google Scholar]

- Woods, M.; Grubnic, S. Integrated Performance management in UK Local Authorities: Is the balanced scorecard a suitable tool? In Proceedings of the 4th International Conference on Accounting, Auditing and Management in Public Sector Reforms, Siena, Italy, 7–9 September 2006. [Google Scholar]

- Saraiva, H.; Alves, M. The use of Balanced Scorecard in Portugal: Evolution and effects on management changes in Portuguese large companies. Rev. Appl. Manag. Stud. 2015, 13, 82–94. [Google Scholar] [CrossRef]

- Saraiva, H.; Alves, M. A evolução do Balanced Scorecard—Uma comparação com outros sistemas. Holos 2017, 33, 185–200. [Google Scholar] [CrossRef] [Green Version]

- Butler, A.; Letza, S.; Neale, B. Linking the balanced scorecard to strategy. Long Range Plan. 1997, 30, 242–253. [Google Scholar] [CrossRef]

- Wong-On-Wing, B.; Guo, L.; Wei, L.; Yang, D. Reducing conflict in balanced scorecard evaluations. Account. Organ. Soc. 2007, 32, 363–377. [Google Scholar] [CrossRef]

- Atkinson, A.; Epstein, M. Measure for Measure. CMA Manag. 2000, 74, 22–28. [Google Scholar]

- Cebrián, M.; Cerviño, E. El balanced scorecard o cuadro de mando integral y el cuadro de mando tradicional: Principales diferencias. Técnica Contab. 2005, 57, 13–17. [Google Scholar]

- Bohm, V.; Lacaille, D.; Spencer, N.; Barber, C. Scoping review of balanced scorecards for use in healthcare settings: Development and implementation. BMJ Open Qual. 2021, 10, 1–10. [Google Scholar] [CrossRef]

- Silva, M.; Callado, A. Balanced Scorecard sustentável. In Proceedings of the XVIII Congresso Brasileiro de Custos, Rio de Janeiro, Brazil, 7–9 November 2011. [Google Scholar]

- Oyaneder, L.; Valderrama, S. Sustainable Balanced Scorecard Model for Chilean Wineries. In Proceedings of the 8th International Conference of Academy of Wine Business Research, Geisenheim, Germany, 28–30 June 2014. [Google Scholar]

- Epstein, M.; Wisner, P. Using a balanced scorecard to implement sustainability. Environ. Qual. Manag. 2001, 11, 1–10. [Google Scholar] [CrossRef]

- Epstein, M.; Wisner, P. Good Neighbors: Implementing Social and Environmental Strategies with the BSC; Balanced Scorecard Report; Article reprint number B0105C; Harvard Business School: Cambridge, MA, USA, 2001. [Google Scholar]

- Rohm, H.; Montgomery, D. Sustainability to Corporate Strategy Using the Balanced Scorecard; The Balanced Scorecard Institute: Cary, NC, USA, 2011. [Google Scholar]

- Campos, L.; Selig, P. SGADA—Sistema de gestão e avaliação do desempenho Ambiental: A aplicação de um modelo de SGA que utiliza o Balanced Scorecard. REAd-Rev. Eletrónica Adm. 2002, 8, 139–163. Available online: https://seer.ufrgs.br/read/article/view/42729/27084 (accessed on 4 March 2021).

- Möller, A.; Schaltegger, S. The Sustainability Balanced Scorecard as a Framework for Eco-Efficiency Analysis. J. Ind. Ecol. 2005, 9, 73–83. [Google Scholar] [CrossRef]

- Schaltegger, S.; Wagner, M. Integrative Management of Sustainability Performance, Measurement and Reporting. Int. J. Account. Audit. Perform. Eval. 2006, 3, 1–19. [Google Scholar] [CrossRef]

- Hristov, I.; Chirico, A.; Appolloni, A. Sustainability Value Creation, Survival and Growth of the Company: A Critical Perspective in the Sustainability Balanced Scorecard (SBSC). Sustainability 2019, 11, 2119. [Google Scholar] [CrossRef] [Green Version]

- Ferber Pineyrua, D.; Redondo, A.; Pascual, J.; Gento, Á. Knowledge Management and Sustainable Balanced Scorecard_ Practical Application to a Service SME. Sustainability 2021, 13, 7118. [Google Scholar] [CrossRef]

- Gimeno, J.; Moneva, J.; Lameda, I. La variable medioambiental en el Quadro de Mando Integral. In Proceedings of the I Conferência Luso-Espanhola em Gestão e Contabilidade Ambiental, Leiria, Portugal, 5–6 May 2005. [Google Scholar]

- Claver-Cortés, E.; López-Gamero, M.; Molina-Azorín, J.; Zaragoza-Sáez, P. Intellectual and environmental capital. J. Intellect. Cap. 2007, 8, 171–182. [Google Scholar] [CrossRef]

- Ferreira, A.; Otley, D. The design and use of performance management systems: An extended framework for analysis. Manag. Account. Res. 2009, 20, 263–282. [Google Scholar] [CrossRef]

- Lueg, R.; Radlach, R. Managing sustainable development with management control systems: A literature review. Eur. Manag. J. 2016, 34, 158–171. [Google Scholar] [CrossRef]

- Gupta, V.; Rose, L.; Jordão, R.V.D. Guest editorial—Healthy organizations: Insights from Latin American research. Manag. Res. 2019, 17, 118–126. [Google Scholar] [CrossRef]

- Curado, C.; Manica, J. Management control systems in Madeira Island largest firms: Evidence on the Balanced Scorecard usage. J. Bus. Econ. Manag. 2010, 11, 652–670. [Google Scholar] [CrossRef] [Green Version]

- Bieker, T. Sustainability management with the balanced scorecard. In Proceedings of the 5th International Summer Academy on Technology Studies, Deutschlandsberg, Austria; 2003. Available online: https://pdfs.semanticscholar.org/14e4/29573f02177da59e7150bf72a663ea2a2781.pdf (accessed on 3 March 2021).

- Creswell, J. Mixed-method research: Introduction and application. In Handbook of Educational Policy; Academic Press: San Diego, CA, USA, 1999; pp. 455–472. [Google Scholar]

- Creswell, J. Qualitative Inquiry and Research Design: Choosing among Five Approaches; Sage Publications, Inc.: Thousand Oaks, CA, USA, 2012. [Google Scholar]

- Smith, J. A Practical Guide to Research Methods, 2nd ed.; Sage: London, UK, 2008. [Google Scholar]

- Creswell, J.; Clark, V. Designing and Conducting Mixed Methods Research, 2nd ed.; Sage Publications, Inc.: Thousand Oaks, CA, USA, 2011. [Google Scholar]

- Lessard-Hébert, M.; Goyette, G.; Boutin, G. Investigação Qualitativa: Fundamentos e Práticas; Instituto Piaget: Lisbon, Portugal, 1990. [Google Scholar]

- Borowski, P. New Technologies and Innovative Solutions in the Development Strategies of Energy Enterprises. HighTech Innov. J. 2020, 1, 39–58. [Google Scholar] [CrossRef]

- Federação Internacional dos Vinhos e Bebidas Espirituosas (FIVS). Global Wine Producers Environmental Sustainability Principles. 2016. Available online: https://www.fivs.org/environmental-sustainability/ (accessed on 27 December 2020).

- Comissão Vitivinícola Regional Alentejana (CVRA). Relatório Anual 2020: Gestão e Contas; Comissão Vitivinícola Regional Alentejana: Évora, Portugal, 2021. [Google Scholar]

- Comissão Vitivinícola Regional Alentejana (CVRA). Vinhos do Alentejo: Facts & Figures; Comissão Vitivinícola Regional Alentejana: Évora, Portugal, 2019. [Google Scholar]

- Comissão Vitivinícola Regional Alentejana (CVRA). Relatório Anual 2019: Gestão e Contas; Comissão Vitivinícola Regional Alentejana: Évora, Portugal, 2020. [Google Scholar]

- Banco de Portugal (BdP). Análise Setorial das Sociedades não Financeiras em Portugal 2011–2016; Estudos da Central de Balanços, 26; Banco de Portugal: Lisbon, Portugal, 2016. [Google Scholar]

- Banco de Portugal (BdP). Análise das Empresas da Indústria das Bebidas; Estudos da Central de Balanços, 27; Banco de Portugal: Lisbon, Portugal, 2017. [Google Scholar]

- Comissão Vitivinícola Regional Alentejana (CVRA). Política Ambiental. 2019. Available online: https://www.vinhosdoalentejo.pt/media/Documentos/Politica_Ambiental.pdf (accessed on 5 January 2021).

- Demediuk, P. The applicability of the Balanced Scorecard in small wineries. In Proceedings of the 9th Asia-Pacific Decision Sciences Institute Conference, Seoul, Korea, 1–4 July 2004. [Google Scholar]

- Stevanovic, T.; Randelovic, M. Sustainability Balanced Scorecard and eco-efficiency analysis. Econ. Organ. 2012, 9, 257–270. [Google Scholar]

- Federação das Indústrias do Estado Geral de Goiás (FIEG). Mapa Estratégico da Indústria Goiana—Goiás 2020—Indústria Rumo ao Futuro; Federação das Indústrias do Estado Geral de Goiás: Goiânia, Brazil, 2010. [Google Scholar]

- Comissão Vitivinícola Regional Alentejana (CVRA). Plano de Acção para a Implementação da Estratégia para a Região dos Vinhos do Alentejo 2014–2020; Comissão Vitivinícola Regional Alentejana: Évora, Portugal, 2016. [Google Scholar]

- Jones, G. Sustainable vineyard developments worldwide. Internet J. Enol. Vitic. 2012, 7, 7. [Google Scholar]

- Barroso, J. Plano de Sustentabilidade dos Vinhos do Alentejo; Comissão Vitivinícola Regional Alentejana: Évora, Portugal, 2015. [Google Scholar]

- Ferreira, H.; Valentim, M.; Gaspar, L.; Óscar, G.; Barroso, J. A sustentabilidade na produção de vinhos do Alentejo, contributo da Adega de Borba. In Proceedings of the 10º Simpósio de Vitivinicultura do Alentejo, Évora, Portugal, 4–6 May 2016; ATEVA–Associação Técnica dos Viticultores do Alentejo: Évora, Portugal, 2016; Volume II, pp. 99–1047. [Google Scholar]

- Fialho, A.; Félix, E.; Jorge, F.; Del Mar Soto Moya, M. Communication of the Commitment to Sustainability and the UN SDGs in the Iberian Foundations. In Governance and Sustainability (Developments in Corporate Governance and Responsibility; Crowther, D., Seifi, S., Eds.; 15. Emerald Publishing Limited: Bingley, UK, 2020; pp. 91–111. [Google Scholar]

- United Nations (UN). Agenda 2030—Agenda Para o Desenvolvimento Sustentável; United Nations: New York, NY, USA, 2015. Available online: http://www.un.ric.org/pt/objetivos-de-desenvolvimento-sustentavel/ (accessed on 9 December 2020).

- Pomarici, E. Recent trends in the international wine marketing and arising research questions. Wine Econ. Policy 2016, 5, 1–3. [Google Scholar] [CrossRef]

| Strategic Areas to be Assessed | Absolute and Relative Frequency | Total | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| Aligning production methods with the preservation of natural resources and biodiversity [Q14.5] (ii) | 0 | 1 | 3 | 43 | 55 | 102 |

| 0 | 0.98% | 2.94% | 42.16% | 53.92% | ||

| Promoting the rational use of resources [Q14.6] (i) | 0 | 0 | 4 | 32 | 66 | 102 |

| 0 | 0 | 3.92% | 31.37% | 64.71% | ||

| Working on the sustainability certification process [Q14.31] (iii) | 0 | 1 | 11 | 37 | 53 | 102 |

| 0 | 0.98% | 10.78% | 36.27% | 51.97% | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gomes, M.J.; Sousa, A.; Novas, J.; Jordão, R.V.D. Environmental Sustainability in Viticulture as a Balanced Scorecard Perspective of the Wine Industry: Evidence for the Portuguese Region of Alentejo. Sustainability 2021, 13, 10144. https://doi.org/10.3390/su131810144

Gomes MJ, Sousa A, Novas J, Jordão RVD. Environmental Sustainability in Viticulture as a Balanced Scorecard Perspective of the Wine Industry: Evidence for the Portuguese Region of Alentejo. Sustainability. 2021; 13(18):10144. https://doi.org/10.3390/su131810144

Chicago/Turabian StyleGomes, Maria José, António Sousa, Jorge Novas, and Ricardo Vinícius Dias Jordão. 2021. "Environmental Sustainability in Viticulture as a Balanced Scorecard Perspective of the Wine Industry: Evidence for the Portuguese Region of Alentejo" Sustainability 13, no. 18: 10144. https://doi.org/10.3390/su131810144

APA StyleGomes, M. J., Sousa, A., Novas, J., & Jordão, R. V. D. (2021). Environmental Sustainability in Viticulture as a Balanced Scorecard Perspective of the Wine Industry: Evidence for the Portuguese Region of Alentejo. Sustainability, 13(18), 10144. https://doi.org/10.3390/su131810144