The Cost Benefit Analysis for the Concept of a Smart City: How to Measure the Efficiency of Smart Solutions?

Abstract

1. Introduction

2. Cost–Benefit Analysis

- Is specification/the basis of the intention stated in socio-economic, institutional and political contexts? Is there any social demand for the stated solution?

- Are there any alternative possibilities or are they analyzed (including zero option)?

- Are the groups of subjects and economic sectors identified?

- Speaking of direct and indirect, implicit and explicit costs and benefits, are they defined? Which indirect costs are expressed in monetary units? What are the financial sources? Are the non-market impacts taken into consideration? Moreover, are taxes and donations also taken into consideration?

- Do they work with interest rates? If so, which interest rate is it? Are time dynamics of the project and length of the project with its impact taken into consideration? Which method was chosen to assess the intentions?

- Were sensitivity analysis and risk assessment done?

- What decision was made as far as the intention’s acceptability and funding are concerned or what option was chosen?

3. Analysis of Realized Smart Activities and Smart Solutions

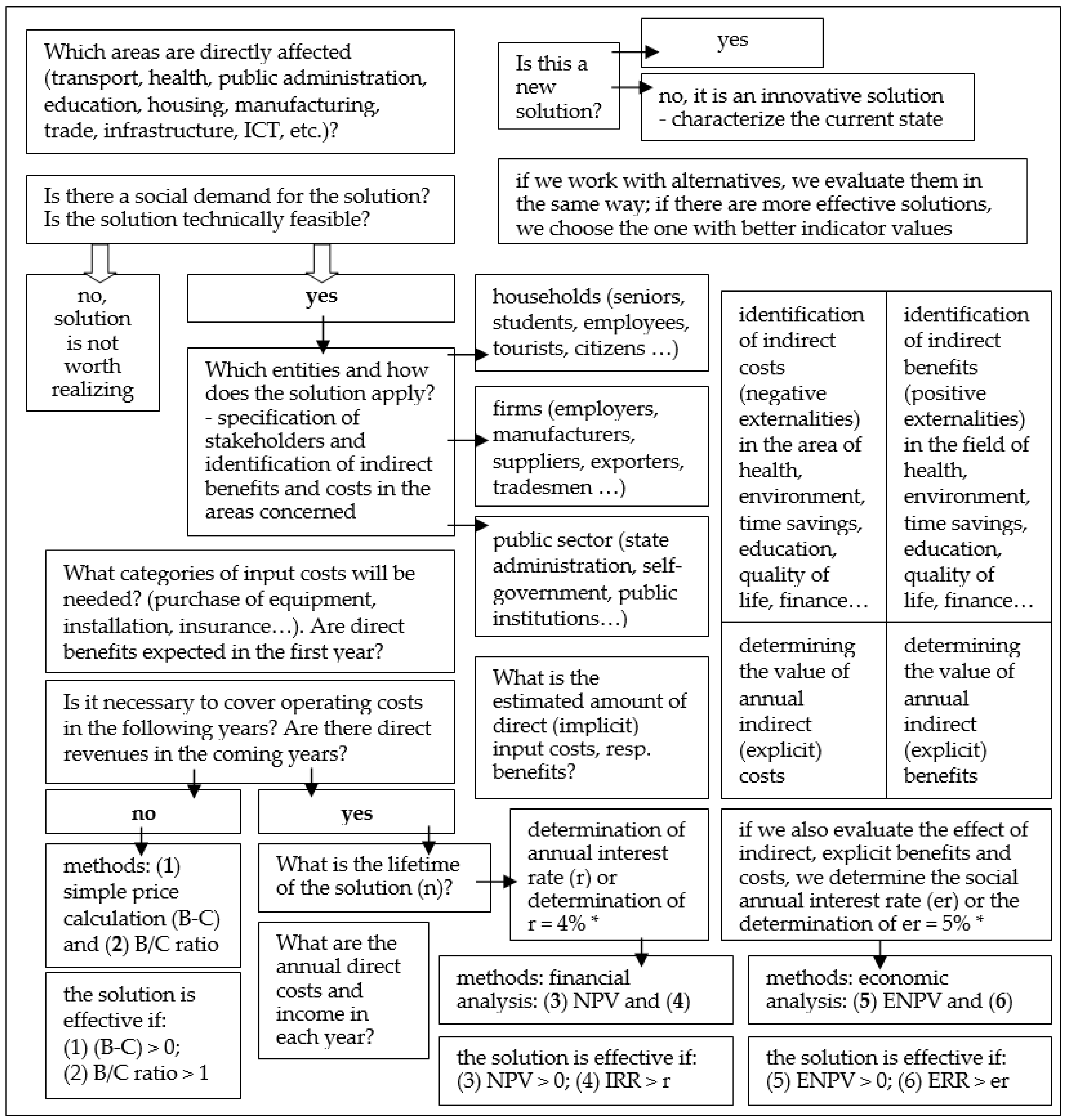

4. The Primary Analytical Framework for CBA in the Context of Smart City

- What does the proposed smart solution concern? Provided that it is an innovative solution, what is the current state (starting point), or will there be any alternative solutions? What is the contribution of the solution to the society (what is the added value?) or to the individual subjects (why are we doing it?)

- Did the subjects mention the necessity of the solution? How is (was) it detected?

- What input (direct) costs are expected and what is their amount (investment costs, service purchases, tangible property and material, intangible property, etc.)?

- Will it be necessary to finance the solutions in the following years, too? If yes, what will be the estimated direct operating costs in the individual years (energy, repairs, maintenance, personal expenses, service purchases, reinvestment expenses, etc.)?

- Are any direct benefits in the course of the solution expected? If yes, which and what amount and in which years? What is the number of users that the benefits will concern?

- What indirect social, utility and other benefits and costs and at what amount can we expect (positive and negative externalities) with the solutions will concern the households, firms and the public sector as well?

5. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Source | Smart Solution | Sector | Broader Presentation in a Social Context | Link to Demand Analysis | Alternatives | Descripted Subjects | Category of Costs | Direct Costs (Benefits) in CBA—Measured Parameters | Indirect Costs and Benefits (Measured) | Other Specific | Methods | Interest Rate | Sensitivity and/or Risk Analysis | Concrete Solution |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| [29] | car vs. bicycle, Copenhagen | private-mobility | short | yes | yes (1 alt) | people | private and social |

| Benefits: Health, Prolonged life, Perceived safety Costs: Discomfort, Branding /tourism, Air pollution, Climate change, Noise, Road deterioration, Congestion | for each year | simple price calculation (static); comparison | no | no | general solution: the bike is 6x better than a car |

| [30] | car vs. bicycle, Calgery | private-mobility | yes | general | yes (1 alt) | people | private and social |

| Benefits: Health, Prolonged life Costs: Collisions/Accidents,

| for each year | simple price calculation (static); comparison | no | no | general solution: the bike is 10x better than a car |

| [31] | Transportation system, Newark | PP–mobility | no | general | no | no | undivided |

| Benefits: Reduced travel time, Less fuel and energy consumption, Safety, Reduced gas emission

| --- | NPV; Benefit-Cost ratio | n = 30; r = 2.7% | no | the project is not be profitable within 30 years |

| [32] | E-car sharing, Prague | private–mobility | short | yes (questionnaire) | yes (2 alt) | 5 categories | undivided | Investment cost:

| Benefits included in EA:

| analysed for two periods | NPV and IRR ENPV, ERR, B/C ratio | r=4%; er=5% | yes | FA—ineffective EA-effective |

| [33] | Smart mobility-Ostrava | public-mobility | no | general | yes (zero var.) | citizens | undivided | Costs: investment costs; reinvestment costs; operating costs; incremental operating costs; Benefits: revenues from fares | Benefits: change in air pollution; climate change; noise pollution; passenger time savings | supplemented by socioeconomic effects | ENPV, ERR, B/C | n = 30; er = 5% | yes | this project is social and cost- effective |

| [34] | Public transport-Czechia | public-mobility | no | general | yes (4 alt) | citizens, passenger | by carrier, public sector and third parties | Subsidies to carriers, cost of purchasing alternative fuel vehicles, fuel costs, maintenance costs, construction infrastructure for pumping PH | Economical quantification of savings pollutant emissions, fuel cost savings, subsidies for the purchase of alternative fuel vehicles | analysis of the current situation | simple price calculation (static) | no | no | one alternative is cost-effective |

| [35] | Smart grids, Évora | PP-energy | no | no | no | no | undivided | Investment cost:

| main indirect benefits category: economic, reliability, environmental and security (in total 23 indicators) | externalities, social & enviro. impact | NPV; Benefit-Cost ratio | n = 19; r? | yes | --- |

| [36] | Smart electricity grids | PP-energy | yes | general | no | people | undivided | --- | Only Benefits: (1) economic benefits: optimized generator operation, reduced ancillary service cost, reduced distribution operation …; (2) reliability benefits: reduced restoration cost, reduced momentary outages…; (3) environmental benefits: reduced CO2, SOx, NOx emissions, reduced landscape use; (4) energy security benefits (reduced wide-scale blackouts) | environ-mental, energy, economic, societal impacts | simple price calculation (static) | no | no | smart electricity grids are socially desirable |

| [37] | Energy system, Great Britain | public-energy | yes | general | yes (2 alt) | domestic and non-domestic sector | undivided | Costs: (1) In Premises Costs: Installation of Meters…; (2) DCC Related Costs: External Service Provider Costs…; (3) Suppliers’ and Other Participants’ System Costs…; (4) Other Costs: Organisational Costs…; (5) Projected Future Costs | Benefits: (1) Consumer Benefits: Time and Energy Savings; (2) Supplier Benefits: Reduced Theft and Losses, Customer Calls…; (3) Demand Shifting Benefits; (4) Network Benefits: Better Informed Investment Decisions…; (5) Carbon and Air Quality Benefits | --- | NPV; Benefit-Cost ratio | n = 22; r = 3.5% | yes | use Smart meter is more efficient than advanced and traditional system |

| [38] | Electricity system | public-energy | no | general | no | no | undivided | Advanced PV inverters, Advanced wind turbines | Benefits: Reduced ancillary service cost, equipment failures, distribution operations cost, electricity losses & costs, sustained outages, major outages, restoration cost, momentary outages, sags & swells, emissions, wide-scale blackouts. Deferred distribution investments. | describe benefitciary (utility, customers, society, owners) | NPV; Benefit-Cost ratio | n = 15; r = 8%; π = 3% | yes, but shortly | this project is cost-effective |

| [39] | Smart grids-Turin | public-energy | no | general | yes (4 alt) | people | social | Standard cost and benefits | Benefits: energy performance and environmental impacts, energy savings and running benefits, real estate market value, green jobs creation | --- | ERR | discount social rate | no | a general ERR conclusion |

| [40] | Smart biofuel-Norway | PP-energy | short | general | no | people | undivided | Fixed costs (acquiring land, establishing the infrastructure & equipment cost), operation & maintenance costs: fuel and electricity or equipment, work force & maintenance of the equipment | no indirect costs and benefits are considered | --- | simple price calculation (static) and comparison | n = 10 | no | payback period of the propose plant is four years |

| [41] | Metering roll-out | PP-energy | no | general | yes (3 alt) | relevant actors | undivided | Fixed costs: financing, investments, transmitssion network fees & losses. Variable costs: market price of energy changing over time and electricity demand from the consumers; demand fluctuations | Benefits: energy saving, reduced risk of demand fluctuation and peak-consumption, | it depends on each of the actors | --- | --- | --- | the profit of the three scenarios differ in time |

| [42] | Distribution grids, Czechia | PP-energy | no | general | no | households | undivided | Costs: investment costs (Advanced Metering Management devices development, installation and introduction into operation and maintenance costs) | 9 categories of benefits: for example: Benefits of increased price of energy; B. of electromobility utilization; B. of cross-border monitoring; B. of mutual concurrence between various energy commodities | --- | NPV | n = 20; r = 8% | no | this project is not cost-effective |

| [43] | Gas Smart Metering Rollout, Ireland | PP-energy | no | general | no | individuals (residential and small businesses) | undivided | Costs: investment cost and incremental costs Benefits: energy saving | Networks Related Costs (Meter Capital Costs, Smart Communication Module Failures, Smart Metering IT Systems Costs, Electricity Smart Metering Interface) and Benefits (Reading, Siteworks Savings, Meter Exchanges, Prepayment—Meter Exchanges and Operations, Fuel Gas Savings, Revenue Protection—Theft of Gas, System Reinforcement) | --- | NPV | n = 4; r = 4% | yes | the project would be profitable |

| [44] | Smart agriculture | PP–agriculture | short | general | yes (3 alt) | households | undivided | Cost and benefits of CBA practices were collected from the household surveys (initial investment etc.) | --- | --- | NPV; IRR; payback period | n = 3-15; r = 9,10,12% | no | all are profitable, how depends on of locations |

| [45] | Smart agriculture—Southern Africa | private–agriculture | short | general | yes (9 al) | households | undivided | Analysed data: (1) gain yield, biomass, labour, inputs used & cost; (2) resource constraints & market access; (3) households characteristics; (4) social capital & information; (5) agroclimatic characteristics | --- | choice of growing technologies | NPV; IRR | no | yes | depends on area and alternative |

| [46] | Smart agriculture—Guatemala | public–agriculture | short | general | yes (8 alt) | people | undivided | Costs: installation costs and maintenance costs (materials, labour) | External effects: biodiversity, carbon sequestration and soil and water contamination Social effects: employment | external and social effects | IRR; ENPV, payback period | er = 12% | no | the results have information function |

| [47] | Close-to-nature adaptation | PP–environment | short | general | yes (4 alt) | people | financial, non-financial | Costs: (investment, operating and administrative costs) | Indirect valuable benefits: energy saving, reducing water volume in sewage treatment plants, flood risk, improving water quality, noise reduction, soil & CO2 erosion air quality improvement etc. | valuable and in-valuable effects | B/C | --- | sensitivity analysis | all alternatives are social and cost-effective |

| [48] | Forestry in city, Lisbon | public–environment | short | general | no | people | undivided | Costs: management planting, removals, control of pests and diseases, watering, administration costs: inspections, other costs | Benefits: Energy saving, Atmospheric carbon dioxide reductions, Air quality benefits, Stormwater runoff reductions, Property value benefits | for each year | NPV; Benefit-Cost ratio | no | no | general solution: the trees in the street are desirable |

| [49] | Cluster; Moravian-Silesian region | PP-business (other) | no | demand directly by the subject | no | stakeholders | undivided | standard fixed costs and operation costs | Benefits: increasing the number of orders & hence the sales of firms in the cluster; increasing the number of employees in both professional and manual professions; increase the number of joint projects involving a cluster member; number of cluster services used | --- | simple price calculation | --- | yes | is not clearly defined |

| [50] | Swimming areal—Ústí nad Labem | public–sport (other) | yes | general (city demand) | yes (3 alt) | especially residents | undivided | Fixed costs: investment costs and operation costs (for electricity, material, wages, overheads, maintenance and repairs, etc.) | Direct income: from swimming pool and swimming pool operation, sauna operation, fitness centre operation etc. Indirect cost: savings associated with job creation and a positive impact on the health and morbidity of the population | --- | NPV; ENPV; IRR; ERR | n = 15; er = 5% | yes | the project is effective if the subsidy is included in income |

| [51] | Smart grids technologies, Sweden | other | short—social welfare | general | Effects: (1) most common: Costs of energy production, Technical energy losses in transmission & distributional grids, Operational costs for transmission and distributional grids, Emissions of CO2, NOX & SO2. (2) common: not specified whether positive or negative, Security of supply (value of lost load, fewer disruptions), Power Quality, Congestion costs, Costs for reserve capacity, Restoration costs, Management costs, Monitoring costs (if not included in grid operational costs), Customer service costs, Costs of theft/fraud, Security. (3) little common: Electro technology industry development, Quality of service. | effects not specified if positive or negative | --- | --- | --- | --- | ||||

| [52] | Drinking water, Sweden | public-water management (other) | yes | general | yes (5 alt) | yes (33 categories of stakeholders) | undivided | All category together: (1) Water utility costs & benefits (Investments, Operational & maintenance costs, Other costs and benefits) (2) Water supply reliability effects (Lost value added in economic sectors, Losses for residential consumers), (3) Water-related health effects (Costs for health care, Lost production, Discomfort & loss of life), (4) Effects on ecosystem services (Drinking water, Irrigation, Hydropower, Industrial water use, Recreational activities, Flood & erosion risk reduction, Other water services, Retention of contaminants), (5) Effects on agriculture, forestry & industry due to water protection restrictions | --- | NPV | n1 = 30; n2 =70; r1 =1.4%; r2 = 3.5% | no | theoretical comparison of results | |

| [53] | Freetime Park—České Budějovice | public–sports (other) | yes | general (city demand) | yes (zero variant) | tourists, local citizens, other visitors | undivided | the cost of acquiring tangible fixed assets and current assets | socio-economic effects: (1) benefits for the city and other municipalities (corporate income tax payments; investment support; economic development of these municipalities); (2) benefits for the state & public institutions (payroll tax for new workers, social & health insurance, reduction of unemployment benefit payments, value added tax); (3) benefits for businesses in the region (increase in net profit) | financial and economic analysis; valuable and invaluable effects | NPV; IRR; profitability index IRR/I; payback period | r = 5% | risk analysis | this project is social and cost-effective |

References

- Borsekova, K.; Koróny, S.; Vaňová, A.; Vitálišová, K. Functionality between the size and indicators of smart cities: A research challenge with policy implications. Cities 2018, 78, 17–26. [Google Scholar] [CrossRef]

- Vybrané Kapitoly z Veřejné Správy a Regionální Rozvoje; Professional Publishing: Praha, Czech Republic, 2018.

- Turečková, K.; Nevima, J. SMART approach in regional development. In Proceedings of the 16th International Scientific Conference Economic Policy in the European Union Member Countries, Karviná, Czech Republic, 12–14 September 2018. [Google Scholar]

- Caragliu, A.; Del Bo, C.; Nijkamp, P. Smart cities in Europe. J. Urban Technol. 2011, 18, 65–82. [Google Scholar] [CrossRef]

- Dominici, G. Why does systems thinking matter? Bus. Syst. Rev. 2012, 1, 1–2. [Google Scholar]

- Turečková, K.; Nevima, J. SMART CITY concept in the Czech. Republic. In Proceedings of the 29th EBES Conference, Lisbon, Portugal, 10–12 October 2019; pp. 1039–1048. [Google Scholar]

- Borseková, K.; Vaňová, A.; Vitálišová, K. Smart Specialization for Smart Spatial Development: Innovative Strategies for Building Competitive Advantages in Tourism in Slovakia. Socio-Econ. Plan. Sci. 2017, 58, 39–50. [Google Scholar] [CrossRef]

- Slavík, J. Smart City v Praxi: Jak Pomocí Moderních Technologií Vytvářet Město Příjemné k Životu a Přátelské k Podnikání; Profi Press: Praha, Czech Republic, 2017. [Google Scholar]

- Sieber, P. Finanční A Socioekonomické Hodnocení Projektů (Metodická Příručka). Available online: https://www.ropstrednicechy.cz/ (accessed on 13 December 2019).

- Schindlerová, V.; Šajdlerová, I. Influence tool wear in materiál flow. Adv. Sci. Technol. Res. J. 2017, 11, 161–165. [Google Scholar] [CrossRef]

- Ochrana, F. Hodnocení Veřejných Zakázek a Veřejných Projektů, 2nd ed.; ASPI publishing: Praha, Czech Republic, 2001. [Google Scholar]

- European Union. European Commisssion, Guide to Cost-Benefit Analysis of Investment Projects; European Union: Luxembourg, 2015. [Google Scholar] [CrossRef]

- Organisation for Economic Co-operation and Development. Cost–benefit analysis and the environment: Recents developments. In Executive Summary; OECD: Paris, France, 2006. [Google Scholar]

- Marešová, P. Měření ve Znalostním Management—Aplikace Metody Cost Benefit Analysis; Gaudeaumus: Hradec Králové, Czech Republic, 2012. [Google Scholar]

- Samuelson, P.A.; Nordhaus, W.D. Ekonomie; NS Svoboda: Praha, Czech Republic, 2007. [Google Scholar]

- Suster, G.A.; Sirb, N.M.; Iancu, T.; Manescu, C. Externalities role in compiling cost–benefit analysis of projects financed from structural funds. In Proceedings of the 13th International Multidisciplinary Scientific Geoconference, Albena, Bulgaria, 16–22 June 2013; pp. 155–160. [Google Scholar]

- Boardman, A.E. Cost-Benefit Analysis: Concepts and Practice, 3rd ed.; Pearson Prentice Hall: Upper Saddle River, NJ, USA, 2006. [Google Scholar]

- Sieber, P. Metodická Příručka, Analýza Nákladů a Přínosů; Ministerstvo Pro Místní Rozvoj: Praha, Czech Republic, 2004. [Google Scholar]

- Romančíková, E. Effectiveness of the environmental investments. Ekonomický Časopis 2004, 52, 1262–1274. [Google Scholar]

- Hueting, R. The use of the discount rate in a cost–benefit analysis for different uses of a humid tropical forest area. Ecol. Econ. 1991, 3, 43–57. [Google Scholar] [CrossRef]

- Szekeres, S. Discounting in cost–benefit analysis. Soc. Econ. 2011, 33, 361–385. [Google Scholar] [CrossRef]

- Pakšiová, R. The Critical analysis of profit for its allocation decision-making. Sci. Ann. Econ. Bus. 2017, 64, 41–56. [Google Scholar] [CrossRef]

- Fuguitt, D.; Shanton, J. Cost-Benefit Analysis for Public Sector Decision Makers; Quorum Books: Westport, CT, USA, 1999. [Google Scholar]

- Horváth, P.; Pütter, J.M.; Haldma, T.; Lääts, K.; Dimante, D.; Dagilienė, L.; Kochalski, C.; Ratajczak, P.; Wagner, J.; Petera, P.; et al. Sustainability Reporting in Central and Eastern European Companies: Results of an International and Empirical Study; Springer: Cham, Switzerland, 2017. [Google Scholar]

- Nas, T.F. Cost-Benefit Analysis. Theory and Application, 2nd ed.; Lexington Books: Lanham, MD, USA, 2016. [Google Scholar]

- Kunreuther, H.; Cyr, C.; Grossi, P.; Tao, W. Using Cost-Benefit Analysis to Evaluate Mitigation for Lifeline Systems; National Science Foundation: Buffalo, NY, USA, 2001. [Google Scholar]

- Lee, J.; Kang, S.; Kim, C. Software architecture evaluation methods based on cost benefit analysis and quantitative decision making. Empir. Softw. Eng. 2009, 14, 453–475. [Google Scholar] [CrossRef]

- Mishan, E.J.; Quah, E. Cost-Benefit Analysis; Routledge: London, UK, 2007. [Google Scholar]

- Gössling, S.; Choi, A. Transport transitions in Copenhagen Comparing the cost of cars and bicycles. Ecol. Econ. 2015, 113, 106–113. [Google Scholar] [CrossRef]

- Dekker, K. The Dollars and Cents of Driving and Cycling: Calculating the Full Costs of Transportation in Calgary, Canada; Department of Earth Sciences, Uppsala University: Uppsala, Sweden, 2016. [Google Scholar]

- Xiong, X. Cost-Benefit Analysis of Smart Cities Technologies and Applications. Available online: http://udspace.udel.edu/bitstream/handle/19716/23818/Xiong_udel_0060M_13359.pdf?sequence=1&isAllowed=y/ (accessed on 19 December 2019).

- Studie Proveditelnosti E-car Sharing v Hlavním Městě Praha. Available online: https://www.smartprague.eu/projekty#mobilita-budoucnosti (accessed on 19 December 2019).

- Guidelines for Conducting A Cost-Benefit Analysis of Smart Grid Projects. Available online: https://ec.europa.eu/jrc/en/publication/reference-reports/guidelines-conducting-cost-benefit-analysis-smart-grid-projects (accessed on 19 December 2019).

- Cost-Benefit Analysis (CBA) for a National Gas. Smart Metering Rollout in Ireland. Available online: https://www.cru.ie/wp-content/uploads/2011/07/cer11180c.pdf (accessed on 19 December 2019).

- Social Costs and Benefits of Smart Grid Technologies. Available online: http://swedishsmartgrid.se/globalassets/publikationer/social_costs_and_benefits_of_smart_grid_technologies.pdf (accessed on 21 December 2019).

- Sjöstrand, K.; Lindhe, A.; Söderqvist, T.; Rosén, L. Cost-Benefit Analysis for Supporting Intermunicipal Decisions on Drinking Water Supply. J. Water 2019, 145, 04019060. [Google Scholar] [CrossRef]

- Soares, A.L.; Rego, F.C.; McPherson, E.G.; Simpson, J.R.; Peper, P.J.; Xiao, Q. Benefits and costs of street trees in Lisbon, Portugal. Urban For. Urban Green. 2011, 10, 69–78. [Google Scholar] [CrossRef]

- Masera, M.; Bompard, E.F.; Profumo, F.; Hadjsaid, N. Smart (Electricity) Grids form Smart Cities: Assessing roles and societal impacts. Proc. IEEE 2018, 106, 613–625. [Google Scholar] [CrossRef]

- Smart Metter Roll-out Cost-Benefit Analysis. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/831716/smart-meter-roll-out-cost-benefit-analysis-2019.pdf (accessed on 21 December 2019).

- Smart Grid and Renewables A Cost-Benefit Analysis Guide for Developing Countries. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2015/IRENA_PST_Smart_Grids_CBA_Guide_2015.pdf (accessed on 21 December 2019).

- Ekologizace Veřejné Dopravy-Ostrava Poruba. Available online: http://novatramvajporuba.cz/wp-content/uploads/2017/03/Zprava_Poruba_faze_II_2014-07-30_verze_2014-08-18.pdf (accessed on 22 December 2019).

- Podpora Veřejné Hromadné Dopravy ve Středočeském Kraji s Cílem Její Postupné Ekologizace Přechodem na Alternativní Druh Paliva, Resp. Pohonu. Available online: http://m.mesto-podebrady.cz/assets/File.ashx?id_org=12349&id_dokumenty=2181 (accessed on 22 December 2019).

- Mutenje, M.J.; Farnworth, C.R.; Stirling, C.; Thierfelder, C.; Mupangwa, W.; Nyagumbo, I. A cost–benefit analysis of climate-smart agriculture options in Southern Africa: Balancing gender and technology. Ecol. Econ. 2019, 163, 126–137. [Google Scholar] [CrossRef]

- Becchio, C.; Corgnati, S.; Dell’Anna, F.; Bottero, M. Cost Benefit Analysis and Smart Grids Projects. In Proceedings of the Sustainable Built Environment Conference—Towards Post-Carbon Cities, Turin, Italy, 18–19 February 2016. [Google Scholar]

- Smart Production of Biofuel for Small Communities. Available online: https://www.researchgate.net/profile/Albara_Mustafa/publication/312037541_Smart_production_of_biofuel_for_small_communities/links/5b07b48e4585157f8712f4cf/Smart-production-of-biofuel-for-small-communities.pdf (accessed on 27 December 2019).

- Sain, G.; Loboguerrero, A.M.; Corner-Dolloff, C.; Lizarazo, M.; Nowak, A.; Martínez-Barón, D.; Andrieu, N. Costs and benefits of climate-smart agriculture: The case of the Dry Corridor in Guatemala. Agric. Syst. 2017, 151, 163–173. [Google Scholar] [CrossRef]

- Adamec, M.; Pavlatka, P.; Stary, O. Costs and Benefits of Smart Grids and Accumulation in Czech. Distribution System. Available online: https://reader.elsevier.com/reader/sd/pii/S1876610211018376?token=FBF76E27263450B2484BE1BA8B26ED605F502493085F39AEC6601AEE8929C4840B67919FF2043886BC5D5FBCD4B4CF48 (accessed on 28 December 2019).

- Lan, L.; Sain, G.; Czaplicki, S.; Guerten, N.; Shikuku, K.M.; Grosjean, G.; Läderach, P. Farm-level and community aggregate economic impacts of adopting climate smart agricultural practices in three mega environments. PLoS ONE 2018, 13, e0207700. [Google Scholar] [CrossRef] [PubMed]

- Plavecký Areál Klíše. Available online: https://www.usti-nad-labem.cz/files/usti-nad-labem/zadosti106/import/f1538253-a3ce-4f98-a602-6186dd961de2.pdf (accessed on 29 December 2019).

- Ekonomická Analýza Přírodě Blízkých Adaptačních Opatření ve Městě. Available online: http://www.ieep.cz/wp-content/uploads/2017/09/Ekonomick%C3%A1-anal%C3%BDza-p%C5%99%C3%ADrod%C4%9B-bl%C3%ADzk%C3%BDch-adapta%C4%8Dn%C3%ADch-opat%C5%99en%C3%AD-ve-m%C4%9Bst%C4%9B-2017.pdf (accessed on 29 December 2019).

- Zefektivnění Činnosti Klastrů v Oblasti Spolupráce a Jeho Řízení. Available online: http://www.btklastr.cz/files/2017/04/Studie-proveditelnosti-BTK_b%C5%99ezen_2017.pdf (accessed on 29 December 2019).

- Finanční A Ekonomické Hodnocení Projektu Freetime Park Stromovka. Available online: https://www.c-budejovice.cz/sites/default/files/import/cz/rozvoj-mesta/nastenka-iprm/obecne-informace-k-iprm/formulare/Documents/FEHP_FTP%20Stromovka.pdf (accessed on 28 December 2019).

- Dehdarian, A. Scenario-based system dynamics modeling for the cost recovery of new energy technology deployment: The case of smart metering roll-out. J. Clean. Prod. 2018, 178, 791–803. [Google Scholar] [CrossRef]

- Melecky, L.; Stanickova, M. Cost Efficiency of EU Funded Projects: Case of Selected SMEs in the Moravian-Silesian Region. In Proceedings of the 12th International Conference on Strategic Management and its Support by Information Systems (SMSIS), Ostrava, Czech Republic, 25–26 May 2017. [Google Scholar]

- Johansson, P.O.; Kriström, B. Cost-Benefit Analysis for Project Appraisal; Cambridge Unviersity Press: Cambridge, UK, 2016. [Google Scholar]

- Pearce, D.; Atkinson, G.; Mourato, S. Cost-Benefit Analysis and the Environment, Recent Developments; OECD Publishing: Paris, France, 2006. [Google Scholar]

- Freeman, A.M.; Herriges, J.A.; Kling, C.L. The Measurement of Environmental and Resource Values: Theory and Methods; RFF Press: Washington, DC, USA, 2014. [Google Scholar]

- Markanday, A.; Galarraga, I.; Markandya, A. A critical review of cost–benefit analysis for climate change adaptation in cities. Clim. Chang. Econ. 2019, 10, 1–31. [Google Scholar] [CrossRef]

- Ward, W.A. Cost-Benefit Analysis Theory versus Practice at the World Bank 1960 to 2015. J. Benefit Cost Anal. 2019, 10, 124–144. [Google Scholar] [CrossRef]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Turečková, K.; Nevima, J. The Cost Benefit Analysis for the Concept of a Smart City: How to Measure the Efficiency of Smart Solutions? Sustainability 2020, 12, 2663. https://doi.org/10.3390/su12072663

Turečková K, Nevima J. The Cost Benefit Analysis for the Concept of a Smart City: How to Measure the Efficiency of Smart Solutions? Sustainability. 2020; 12(7):2663. https://doi.org/10.3390/su12072663

Chicago/Turabian StyleTurečková, Kamila, and Jan Nevima. 2020. "The Cost Benefit Analysis for the Concept of a Smart City: How to Measure the Efficiency of Smart Solutions?" Sustainability 12, no. 7: 2663. https://doi.org/10.3390/su12072663

APA StyleTurečková, K., & Nevima, J. (2020). The Cost Benefit Analysis for the Concept of a Smart City: How to Measure the Efficiency of Smart Solutions? Sustainability, 12(7), 2663. https://doi.org/10.3390/su12072663