Management Accounting Systems, Top Management Teams, and Sustainable Knowledge Acquisition: Effects on Performance

Abstract

1. Introduction

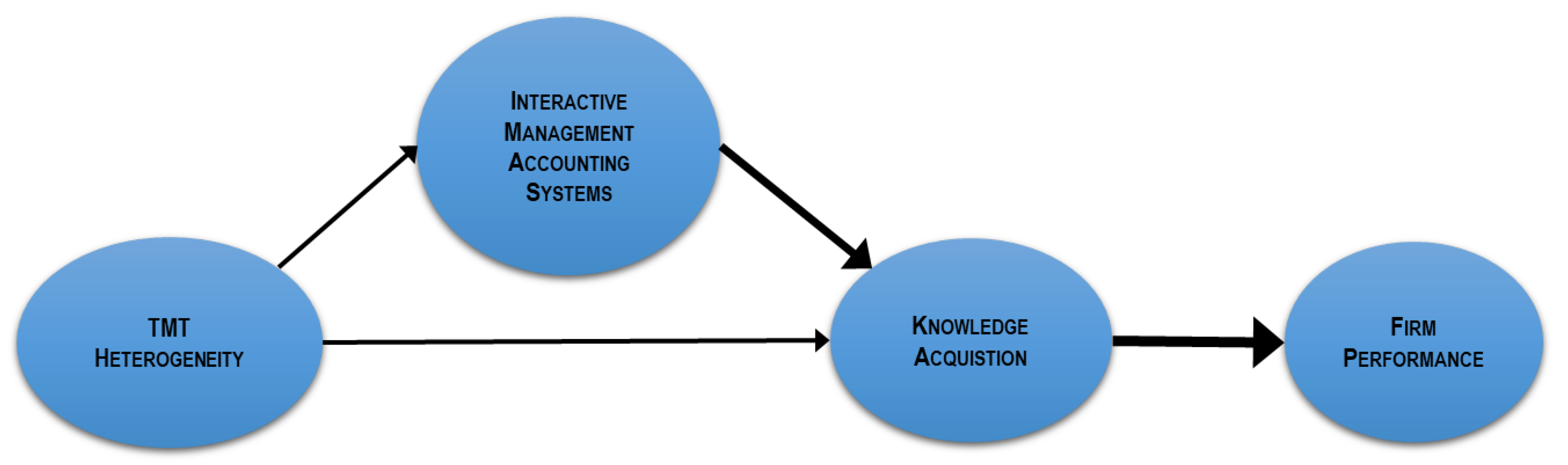

2. Theoretical Background and Hypothesis Development

3. Materials and Methods

4. Variable Measurement

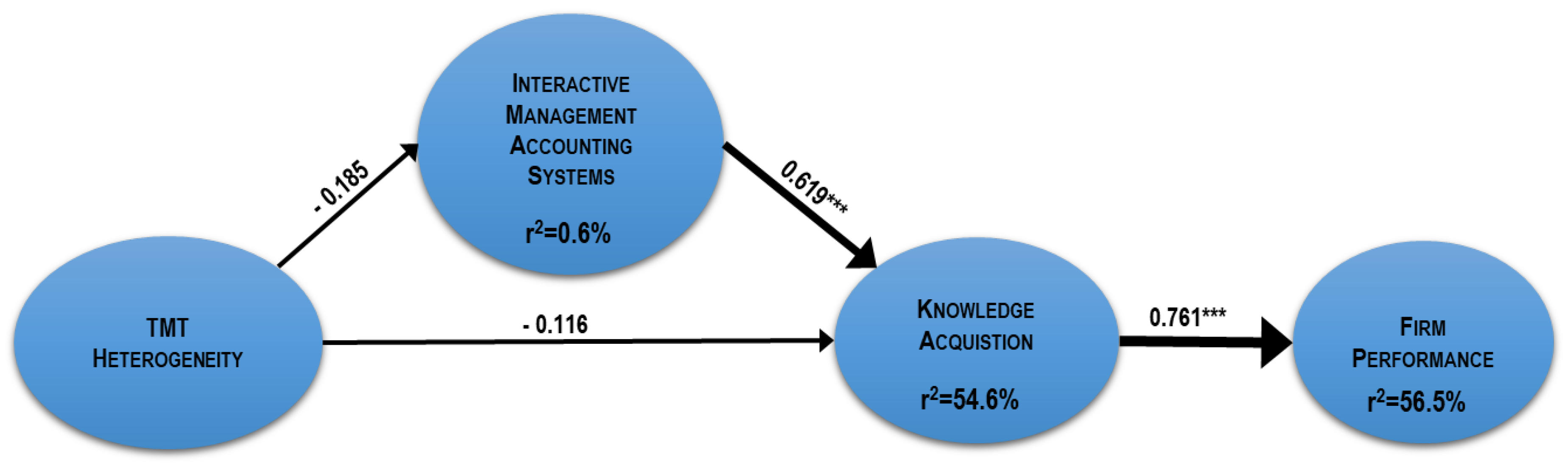

5. Analysis and Results

6. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Items | Knowledge Acquisition | ||

|---|---|---|---|

| External | Internal | ||

| 1 | My organization has processes for acquiring knowledge about our customers. | 0.654 | 0.329 |

| 2 | My organization has processes for generating new knowledge from existing knowledge. | 0.682 | 0.338 |

| 3 | My organization has processes for acquiring knowledge about our suppliers. | 0.210 | 0.574 |

| 4 | My organization uses feedback from projects to improve subsequent projects. | 0.545 | 0.475 |

| 5 | My organization has processes for distribution knowledge throughout the organization. | 0.603 | 0.564 |

| 6 | My organization has processes for exchanging knowledge with our business partners. | 0.406 | 0.788 |

| 7 | My organization has processes for interorganizational collaboration. | 0.190 | 0.783 |

| 8 | My organization has processes for acquiring knowledge about new products/services within our industry. | 0.880 | 0.242 |

| 9 | My organization has processes for acquiring knowledge about competitors within our industry. | 0.790 | 0.267 |

| 10 | My organization has processes for benchmarking performance. | 0.828 | 0.142 |

| 11 | My organization has teams devoted to identifying best practices. | 0.472 | 0.469 |

| 12 | My organization has processes for exchanging knowledge between individuals. | 0.195 | 0.804 |

Appendix B. Items for Each Research Variable

- Age

- University degree and title (years of education in medicine or general management/law)

- Years of experience as a clinician/doctor at public hospitals

- Years of experience as a clinician/doctor at other health care organizations

- Years of experience as a manager in current hospital

- Years of experience as a manager in other health care organizations

- Set and negotiate goals and targets

- Debate data assumptions and actions plans

- Challenge new ideas and ways of doing tasks

- Involvement in a permanent discussion with subordinates

- Learning tool

- Innovate new products/services.

- Identify new business opportunities

- Coordinate the development efforts of different units.

- Anticipate potential market opportunities for new products/services.

- Rapidly commercialize new innovations.

- Adapt quickly to unanticipated changes.

- Anticipate surprises and crises.

- Quickly adapt its goals and objectives to industry/market changes.

- Decrease market response times.

- React to new information about the industry or market.

- Be responsive to new market demands.

- Avoid overlapping development of corporate initiatives.

- Streamline its internal processes.

- Reduce redundancy of information and knowledge.

References

- Yang, J.; Yuan, M.; Yigitcanlar, T.; Newman, P.; Schultmann, F. Managing knowledge to promote sustainability in Australian transport infrastructure projects. Sustainability 2015, 7, 8132–8150. [Google Scholar] [CrossRef]

- Rašula, J.; Vukšić, V.B.; Štemberger, M.I. The impact of knowledge management on organizational performance. Econ. Bus. Rev. 2012, 14, 147–168. [Google Scholar]

- Nonaka, I.; Takeuchi, H. The Knowledge-Creating Company. How Japanese Companies Create the Dynamics of Innovation; Oxford University Press: New York, NY, USA, 1995. [Google Scholar]

- Lu, C.; Zhu, D.; Chang, Y. The moderating role of the interactive use of Management Accounting Systems (MCS) on the relation between knowledge management types and marketing project performance. Afr. J. Bus. Manag. 2001, 5, 687–698. [Google Scholar]

- El Sawy, O.A.; Malhotra, A.; Gosain, S.; Young, K. IT-enebled value innovation in the electronic economy: Insight from marshal industry. MIS Q. 2000, 23, 305–335. [Google Scholar] [CrossRef]

- Bousa, R.; Venkitachalam, K. Aligning strategies and processes in knowledge management: A framework. J. Knowl. Manag. 2013, 17, 331–346. [Google Scholar] [CrossRef]

- Pinho, I.; Rego, A.; Cunha, M.P. Improving knowledge management processes: A hybrid positive approach. J. Knowl. Manag. 2012, 16, 215–242. [Google Scholar] [CrossRef]

- Van Der Meer, R.; Sinnappan, S. The role of knowledge management in an organization’s sustainable development. In Proceedings of the Knowledge Management International Conference, Langkawi, Malaysia, 10–12 June 2008; University of Wollongong: Bega, Australia, 2008; pp. 1–6. [Google Scholar]

- Huang, L.-S.; Lai, C.-P. An investigation on critical success factors for knowledge management using structural equation modelling. Technol. Manag. 2012, 40, 24–30. [Google Scholar]

- Obeidat, B.Y.; Masa’deh, R.; Abdallah, A.B. The relationships among human resource management practices, organizational commitment, and knowledge management processes: A structural equation modeling approach. Int. J. Bus. Manag. 2014, 9, 9–26. [Google Scholar] [CrossRef]

- Ditillo, A. Designing management accounting systems to foster knowledge transfer in knowledge-intensive firms: A network-based approach. Eur. Account. Rev. 2012, 21, 425–450. [Google Scholar]

- Centobelli, P.; Cerchione, R.; Esposito, E. Knowledge management in startups: Systematic literature review and future research agenda. Sustainability 2017, 9, 361. [Google Scholar] [CrossRef]

- Ferreira, A.A.; Kuniyoshi, M.S. Critical factors in the implementation process of integrated management systems. J. Inf. Syst. Technol. Manag. 2015, 12, 145–164. [Google Scholar] [CrossRef]

- Azevedo, P.S.; Romão, M.; Rebelo, E. Success factors for using ERP (Enterprise Resource Planning) systems to improve competitiveness in the hospitality industry. Tour. Manag. Stud. 2014, 10, 165–168. [Google Scholar]

- Sureena, M.; Mahmood, A.K. The review of approaches to knowledge management system studies. J. Knowl. Manag. 2013, 17, 472–490. [Google Scholar]

- Green, G.; Liu, L.; Qi, B. Knowledge based management information systems for the effective business performance of SME’s. J. Int. Technol. Inf. Manag. 2009, 18, 201–222. [Google Scholar]

- Spender, J.C.; Grant, R.M. Knowledge and the firm: Overview. Strateg. Manag. J. 1996, 17, 5–9. [Google Scholar] [CrossRef]

- Shehata, G.M. Leveraging organizational performance via knowledge management systems platforms in emerging economies: Evidence from the Egyptian Information and Communication Technology (ICT) industry. J. Knowl. Manag. Syst. 2015, 45, 239–278. [Google Scholar] [CrossRef]

- Simons, T.; Peterson, R.S. Task conflict and relationship conflict in top management teams: The pivotal role of intra group trust. Adm. Sci. Q. 2000, 85, 102–111. [Google Scholar] [CrossRef] [PubMed]

- Moilanen, S. Knowledge translation in management accounting and control: A case study of a multinational firm in transitional economies. Eur. Account. Rev. 2007, 16, 757–789. [Google Scholar] [CrossRef]

- Hambrick, D.; Mason, P. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1986, 9, 193–206. [Google Scholar] [CrossRef]

- Certo, T.S.; Lester, R.H.; Dalton, C.M.; Dalton, D.R. Top management teams, strategy and financial performance: A meta-analytical examination. J. Manag. Stud. 2006, 43, 813–839. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Schuen, A. Dynamic capabilities in strategic management. Strateg. Manag. J. 1997, 18, 509–534. [Google Scholar] [CrossRef]

- Naranjo-Gil, D. The role of top management teams in hospitals facing strategic change: Effects on performance. Int. J. Healthc. Manag. 2015, 8, 34–41. [Google Scholar] [CrossRef]

- Naranjo-Gil, D.; Hartman, F. Management accounting systems, top management team heterogeneity and strategic change. Account. Organ. Soc. 2007, 32, 735–756. [Google Scholar] [CrossRef]

- Pein, R.; Maier, R. SimKnowledge—Analyzing impact of knowledge management measures on team organizations with multi agent-based simulation. Inf. Syst. Front. 2011, 13, 621–636. [Google Scholar] [CrossRef]

- Crossan, M.M.; Berdrow, I. Organizational learning and strategic renewal. Strateg. Manag. J. 2003, 24, 1087–1105. [Google Scholar] [CrossRef]

- Katila, R.; Ahuja, G. Something old, something new: A longitudinal study of search behavior and new product introduction. Acad. Manag. J. 2002, 45, 1183–1194. [Google Scholar]

- Tomé, E.; Figueiredo, P. Knowledge management and politics at the highest level: An exploratory analysis. Manag. Dyn. Knowl. Econ. 2015, 3, 193–212. [Google Scholar]

- Akbari, A.; Reza, M. The study of the effects of knowledge management on innovation and organizational performance: Case study in small and medium enterprises in Qom. Eur. Online J. Nat. Soc. Sci. 2015, 4, 677–686. [Google Scholar]

- Micic, R. Leadership role in certain phases of knowledge management processes. Ekonomika 2015, 61, 47–56. [Google Scholar] [CrossRef]

- Cooke, N.; Salas, E.; Cannon-Bowers, J.A.; Stout, R. Measuring team knowledge. Hum. Factors 2000, 42, 151–179. [Google Scholar] [CrossRef]

- Naranjo-Gil, D.; Hartmann, F. How top management teams use management accounting systems to implement strategy. J. Manag. Account. Res. 2006, 18, 21–53. [Google Scholar] [CrossRef]

- Malmi, T.; Brown, D.A. Management accounting systems as a package—Opportunities, challenges and research directions. Manag. Account. Res. 2008, 19, 287–300. [Google Scholar] [CrossRef]

- Sajeva, S. The analysis of key elements of socio-technical knowledge management system. Econ. Manag. 2010, 15, 765–774. [Google Scholar]

- Nonaka, I. A dynamic theory of organizational knowledge creation. Organ. Sci. 1994, 5, 14–37. [Google Scholar] [CrossRef]

- Girish, G.P.; Joseph, D.; Amar Rajú, G. Factors influencing adoption of knowledge management systems in India from a micro, small and medium enterprise’s perspective. Int. Rev. Manag. Market. 2015, 5, 135–140. [Google Scholar]

- Hung, S.; Tang, K. Expanding group support system capabilities from the knowledge management perspective. J. Int. Technol. Inf. Manag. 2006, 17, 21–42. [Google Scholar]

- Rao, Y.; Guo, K.; Chen, Y. Information systems maturity, knowledge sharing, and firm performance. Int. J. Account. Inf. Manag. 2015, 23, 106–127. [Google Scholar] [CrossRef]

- Deokar, V.A.; El-Gayar, F.O.; Samikar, S.; Wills, J.M. Communications of the association for information systems. Commun. AIS 2010, 20, 565–598. [Google Scholar]

- Frigotto, M.L.; Coller, G.; Collini, P. The strategy and management accounting systems relationship as emerging dynamic process. J. Manag. Gov. 2013, 17, 631–656. [Google Scholar] [CrossRef]

- Grant, R.M. Toward a knowledge-based theory of the firm. Strateg. Manag. J. 1996, 17, 109–122. [Google Scholar] [CrossRef]

- Rosca, V. A model for eliciting expert knowledge into sports-specific knowledge management systems. Rev. Int. Comp. Manag. 2014, 15, 57–68. [Google Scholar]

- Kruger, C.J.; Johnson, R.D. Information management as an enabler of knowledge management maturity: A South African perspective. Int. J. Inf. Manag. 2010, 30, 57–67. [Google Scholar] [CrossRef][Green Version]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard: Translating Strategy into Action; Harvard Business School Press: Boston, MA, USA, 2004. [Google Scholar]

- Năstase, M.; Predişcan, M.; Roiban, R.N. The role of employees in a process of change—A case study for the romanian organizations. Rev. Int. Comp. Manag. 2013, 14, 512–518. [Google Scholar]

- Herremans, I.M.; Isaac, R.G.; Kline, T.J.B.; Nazari, J.A. Intellectual capital and uncertainty of knowledge: Control by design of the management system. J. Bus. Eth. 2011, 98, 627–640. [Google Scholar] [CrossRef]

- Kasper, H.; Mühlbacher, J.; Müller, B. Intra-organizational knowledge sharing in MNCs depending on the degree of decentralization and communities of practice. J. Glob. Bus. Technol. 2008, 4, 59–67. [Google Scholar]

- Lane, P.J.; Koka, B.R.; Pathak, S. The reification of absorptive Capacity: A critical review and rejuvenation of the construct. Acad. Manag. Rev. 2006, 31, 833–863. [Google Scholar] [CrossRef]

- Yao–Sheng, L. The effect of human resource Management Accounting Systems on the relationship between knowledge management strategy and firm performance. Int. J. Manpow. 2011, 32, 494–511. [Google Scholar]

- Zahra, S.A.; George, G. Absorptive capacity: A review, reconceptualization, and extension. Acad. Manag. Rev. 2002, 27, 185–203. [Google Scholar] [CrossRef]

- Yuan, X.; Guo, Z.; Fang, E. An examination of how and when the top management team matters for firm innovativeness: The effects of TMT functional backgrounds. Innov. Manag. Policy Pract. 2014, 16, 323–342. [Google Scholar] [CrossRef]

- National Secretary of Planning and Development—SENPLADES. Official Registry No. 290. 12 May 2012. Presidency of the Republic. Available online: https://www.planificacion.gob.ec/wp-content/uploads/downloads/2013/12/Buen-Vivir-ingles-web-final-completo.pdf (accessed on 29 June 2018).

- Jácome, H.; King, K. Estudios Industriales de la Micro, Pequeña y Mediana Empresa. FLACSO-MIPRO 2012, 1, 45–80, 175–244. [Google Scholar]

- Barreneche García, A.; Bounfour, A. Knowledge asset similarity and business relational capital gains: Evidence from European manufacturing firms. Knowl. Manag. Res. Pract. 2014, 12, 246–260. [Google Scholar] [CrossRef]

- Singh, R.M.; Gupta, M. Knowledge management in teams: Empirical integration and development of a scale. J. Knowl. Manag. 2014, 18, 777–794. [Google Scholar] [CrossRef]

- Interval Revenue Service (Servicio de Rentas Internas del Ecuador–SRI). Special Taxpayer Database. 2017. Available online: http://www.sri.gob.ec/web/guest/catastros (accessed on 29 June 2018).

- Unique Registry of Taxpayers Law (Ley de Registro Único de Contribuyentes). Official Registry Supplement 398; National Congress of the Republic of Ecuador: Quito, EcuAdor, 2004. [Google Scholar]

- Naranjo–Gil, D. Salvando las dificultades del uso de la encuesta en la investigación contable de gestión: Una aplicación empírica. Rev. Esp. Financ. Contab. 2006, 35, 361–385. [Google Scholar] [CrossRef]

- Dillman, D.A. Mail and Internet Surveys; John Wiley and Sons Inc.: New York, NY, USA, 2000. [Google Scholar]

- Gold, A.H.; Malhotra, A.; Segars, A.H. Knowledge management: An organizational capabilities perspective. J. Manag. Inf. Syst. 2001, 18, 185–216. [Google Scholar] [CrossRef]

- Naranjo-Gil, D. The role of management control systems and top teams in implementing environmental sustainability policies. Sustainability 2016, 8, 359. [Google Scholar] [CrossRef]

- Naranjo-Gil, D. The use of the balanced scorecard and the budget in the strategic management of public hospitals. Gac. Sanit. 2010, 24, 220–224. [Google Scholar]

- Hulland, J. Use of Partial Least Squares (PLS) in strategic management research: A review of four recent studies. Strateg. Manag. J. 1999, 20, 195–204. [Google Scholar] [CrossRef]

- Chin, W.W. The Partial Least Squares Approach to Structural Equation Modeling; Marcoulides, G.A., Ed.; Modern Methods for Business Research: Mahwah, NJ, USA; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 1998; pp. 295–336. [Google Scholar]

| Construct Reliability and Validity | |||

|---|---|---|---|

| Cronbach’s Alpha | Composite Reliability | Average Variance Extracted (AVE) | |

| Firm Performance | 0.898 | 0.918 | 0.556 |

| Knowledge Acquisition | 0.874 | 0.902 | 0.539 |

| Interactive MAS Use | 0.882 | 0.909 | 0.627 |

| Discriminant Validity | |||

|---|---|---|---|

| Fornell–Larcker Criterion | |||

| Knowledge Acquisition | Firm Performance | Interactive MAS Use | |

| Knowledge Acquisition | 0.734 | ||

| Firm Performance | 0.752 | 0.746 | |

| Interactive MAS Use | 0.689 | 0.712 | 0.792 |

| F-Square | |||

|---|---|---|---|

| Firm Performance | Knowledge Acquisition | Interactive MAS Use | |

| TMT Heterogeneity | 0.158 | 0.063 | |

| Knowledge Acquisition | 1.299 | ||

| Interactive MAS Use | 0.801 | ||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ugalde Vásquez, A.F.; Naranjo-Gil, D. Management Accounting Systems, Top Management Teams, and Sustainable Knowledge Acquisition: Effects on Performance. Sustainability 2020, 12, 2132. https://doi.org/10.3390/su12052132

Ugalde Vásquez AF, Naranjo-Gil D. Management Accounting Systems, Top Management Teams, and Sustainable Knowledge Acquisition: Effects on Performance. Sustainability. 2020; 12(5):2132. https://doi.org/10.3390/su12052132

Chicago/Turabian StyleUgalde Vásquez, Andrés F., and David Naranjo-Gil. 2020. "Management Accounting Systems, Top Management Teams, and Sustainable Knowledge Acquisition: Effects on Performance" Sustainability 12, no. 5: 2132. https://doi.org/10.3390/su12052132

APA StyleUgalde Vásquez, A. F., & Naranjo-Gil, D. (2020). Management Accounting Systems, Top Management Teams, and Sustainable Knowledge Acquisition: Effects on Performance. Sustainability, 12(5), 2132. https://doi.org/10.3390/su12052132