1. Introduction

Energy poverty remains one of Africa’s most significant barriers to socioeconomic progress. More than 600 million households lack access to essential energy services and population growth is expected to perpetuate existing shortages in the coming decades [

1]. Insufficient public funding of regional power infrastructure is a determinant for entrenched social inequalities. Inadequate electricity supply restricts the availability of lighting, industrial innovations and development of social institutions, which moderates the quality of education and pace of economic development. Several studies elucidate a cointegration between energy accessibility, consumption and per capita incomes [

2]. Frequent power outages and constraints on supply have been associated to the large dependency of costly captive diesel generators [

3]. High mortality rates throughout the continent have also been attributed to the persistent reliance on biofuels by households [

4].

The shortage of public investment in the power sector reflects macroeconomic and microeconomic challenges, including subdued capital market development, ineffective fiscal management, and the concentration of state ownership in the sector [

5]. Whilst public funding constitutes the primary source of financing for power projects in the region, investment in new capacity has been limited. Identifying the levels which encourage private sector participation in domestic markets is necessary to address the supply deficits (p. 228, [

6]).

A large body of literature highlights the importance of implementing power sector reforms in African economies [

7]. Regulatory changes have been particularly salient in the promotion of external investment to the generation segment of energy markets. However, have generally lacked social legitimacy [

8]. Although barriers to efficiency remain, the number of Independent Power Producer (IPP) projects and total investment have increased in countries pursuing reforms. Subsequently, mobilizing private sector participation is not only necessary to reduce the infrastructure investment gap but, given the right framework and incentives, can drive the development of renewable energy deemed critical for the sustainable development of African economies.

Extensive research predicating solutions for increasing the external sources of finance, frequently highlight a combination of non-financial and financial drivers. Whilst the uncompetitive risk-reward profiles of African renewable energy projects have contributed to the shortage of private investment, various non-financial criteria can explain the preferences of these investors [

9]. Moreover, this set of criteria also determine the range of possible projects from which a financial decision is made. Consequently, cognitive biases may preclude African energy projects from being considered during the early-stages of the assessment; during the perception and formulation of alternatives. The dissemination of information by a decision-maker is, for example, dependent on the interdependence of his/her a-priori beliefs, extent of institutional pressure, knowledge about the operating context and attitude towards radical innovation [

10]. Subsequently, focusing on financial drivers without acknowledging the behaviors and the expected responses of investors overlooks an important aspect of research.

The paper contributes to research in several ways. First, the identification of investment decision making criteria help to understand better the characteristics which motivate private investments in renewable energy projects. Second, the delineation of non-financial and financial drivers is important for designing policies aimed at mobilizing external sources of investment. Finally, the paper reinforces the relevance of Multi-Criteria Decision Making (MCDM) methodologies as a practical tool for understanding complex investment decisions. The paper fills a gap in the literature by introducing a fuzzy TOPSIS approach to identify the drivers of investment and to delineate the significance of financial and non-financial criteria on the evaluation of African renewable energy projects. We posit that although financial incentives and drivers are necessary to encourage greater participation, domestic policies need to have tangible effects on investor confidence. We specifically address the attitudes of the private sector to regulatory commitment and solutions based on local capacity building. A market-based mechanism to disintermediate governance issues and address institutional rigidities, which exacerbate regional energy challenges, are among the prescriptions in the paper.

The remainder of the paper is as follows:

Section 2 reviews private investment in African renewable energy projects.

Section 3 introduces the research approach of the paper and the MCDM methodology of the empirical analysis.

Section 4 describes the primary data used in the study.

Section 5 discusses the main findings, offers policy recommendations and concludes.

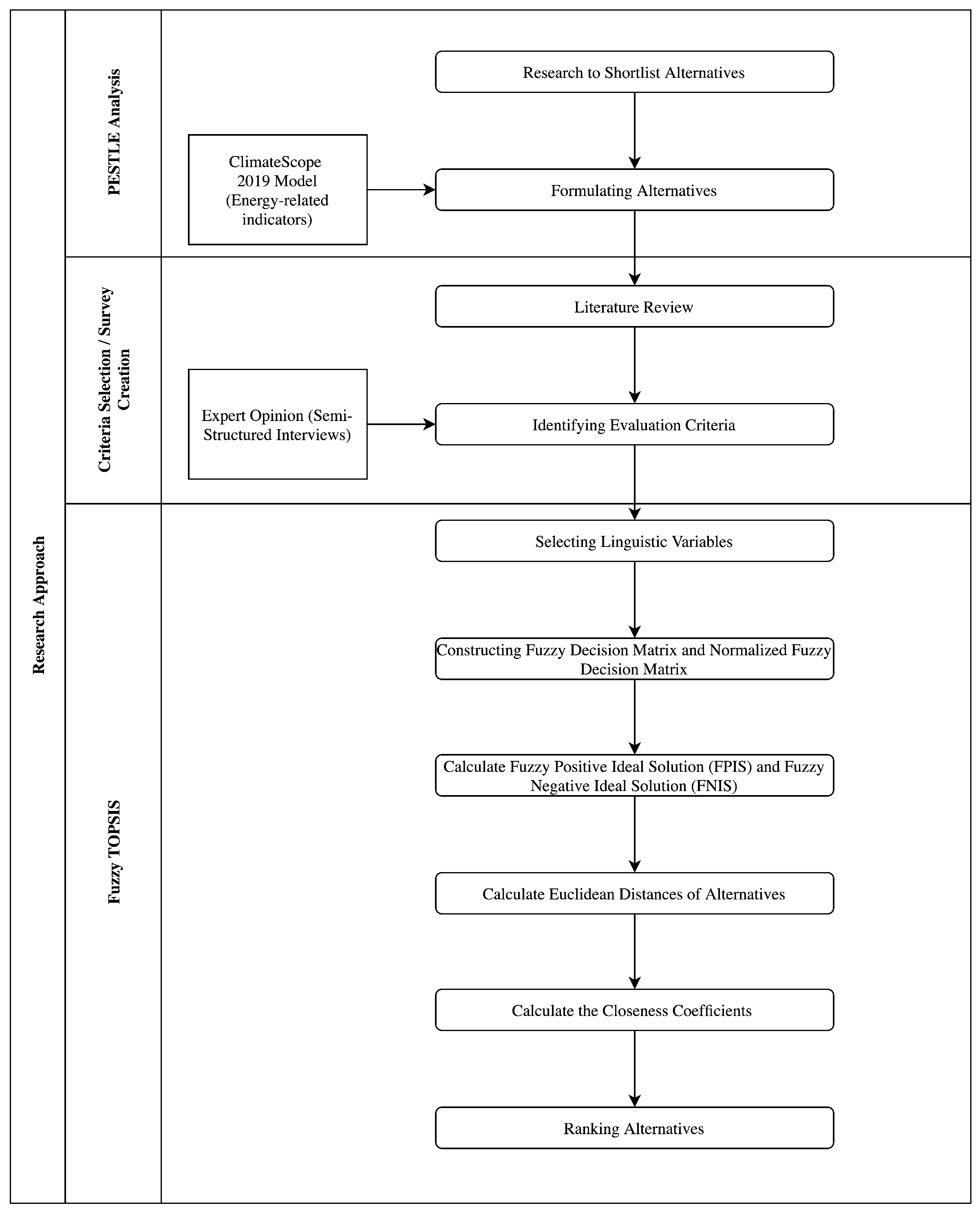

3. Methodology

First, we conduct a PESTLE analysis to select 5 African countries as alternatives for a hypothetical renewable energy (RE) project investment. In social sciences PESTLE and its variants, such as the STEEP method, can be used to delineate the impact of macro-environmental factors on the performance of an investment decision [

35,

36]. We examine sixteen macroeconomic and microeconomics indicators, including value chains by clean energy sector, demand dynamics and policy-clean energy to corroborate the relevance of South Africa, Kenya, Nigeria, Cameroon and Tunisia, as ideal alternatives in the study. These countries are identified as leaders in regional indexes examining favorable location-specific characteristics for clean energy investments [

37]. Second, the non-financial and financial drivers of investment decision-making are determined by the combined results of expert interviews and a theoretical analysis. We assign these drivers to evaluation criteria based on their economic, political, technical, environment or social aspects. Third, a fuzzy TOPSIS experiment is designed to obtain the order preferences of project attributes and preferred alternatives (countries) from a cohort of 49 investment professionals.

Figure 3 outlines the research approach of the paper, which comprises three distinct stages.

Fuzzy TOPSIS

MCDM methodologies are well-suited to the analysis of choice optimization problems in fields of finance, energy analysis and energy planning [

38]. The associated methods capture the varying degrees of influence of criteria (both financial and non-financial) and overcome the shortcomings of assessing investment decision-making based exclusively on financial valuation approaches. Incomplete information, increases the relevance of assessing behavioral factors to explain choice outcomes and diminishes forecasting accuracy (p. 405, [

9]). The process of identifying an optimal solution from a group of alternatives in a MCDM problem can be summarized in a matrix format [

39], as shown in Equation (

1).

where

D, denotes the alternatives (

,

,...,

) selected by a decision-maker based on an evaluation criteria’s (

,

,...,

) corresponding rating, denoted as

, Further, in group decision-making the rating is aggregated by weightings,

,

,...,

associated to each criterion. In other words,

, captures the significance of a criteria within a group of determinants that represent the preferences of multiple decision-makers. Conventionally, crisp numbers (

) are associated to the weightings and ratings of MCDM methodologies, however, are ineffective at interpreting the results derived from the inclusion of linguistic scales in experiments.

Terms such as “Very high importance” replace crisp number representations to overcome the known challenges of evaluating utility functions based on binary number aggregation. However, in order to do so, these functions are restated and interpreted in terms of a matter of degree [

40]. In the seminal work of [

41], triangular fuzzy set theory is used to improve the interpretation of linguistic Likert scales. By applying this logic to MCDM in a fuzzy TOPSIS approach, the ratings,

, can be represented by a membership function. Consequently, a criterion with a “Very high importance” rate, normally inputted into the experiment with a crisp number value of 1, can instead be transformed and represented as the triplet,

. The transformation of a crisp value utility function using the triangular set theory is shown in Equation (

2).

By constructing decision matrices and calculating the distance between the ratings (as triplet values), the fuzzy TOPSIS approach extrapolates both a least and most preferred solution for a given decision problem. Consequently, the distance between an alternative to these two outputs determines an overall order preference, which becomes indicative of a decision-makers optimal choice. Notable implementations of the approach include the works of [

39,

42], who introduce the following stages in their research design:

Linguistic variables are chosen, and the ratings assigned by participants to the evaluation criteria are subsequently aggregated to identify weightings. This step provides the and (criteria weight and rating, respectively) as output.

Crisp values and , for evaluating the alternatives, are assigned triangular fuzzy numbers before being used to construct both a decision matrix and normalised decision matrix, obtained through linear scale transformation.

Weightings, from step 1, are aggregated with the normalised decision matrix to obtain a fuzzy weighted normalized decision matrix.

The fuzzy positive-ideal solution (FPIS) and fuzzy negative-ideal solution (FNIS) are calculated by the Euclidean distance of an alternatives criteria to the optimal and least preferred triplet values, shown in Equations (5) and (6).

From step 4, the ideal positive (

) and ideal negative (

) distance measurements are calculated. The closeness coefficients provide the alternative ranking and an order of preference based on the proximity of an alternative to the ideal positive and negative solution.

The TOPSIS methodology relies extensively on input provided by experts. Specifically, participants with prior knowledge in African renewable energy markets and investment-related transactions provide insight to the pertinent evaluation criteria used in investment decision-making and rank the country alternatives. Semi-structured interviews constitute the primary data collection approach for identifying investment decision-making drivers.

Both [

43,

44] highlight that effective qualitative studies depend on conducting an optimal number of interviews to obtain a sufficient level of insight to trends and developments within the scope of research. In order to prevent the saturation of knowledge, arising from the collection of increasingly common responses, 14 in-depth interviews were conducted.

The second source of primary data, used to conduct stage 3 of the research methodology, was collected through an online survey based on the existing work of [

45]. Non-probability sampling, using online services to both identify and screen participants, was used to source the data. Most of the 49 participants reported that they had more than 5 years of experience in energy or investment-related industries and between 3 to 5 years of experience in working for private firms in the African energy sector. Few responses were collected from industry professionals working in either the non-profit or public sector.

4. Results

4.1. Evaluation Criteria

The evaluation criteria introduced in the fuzzy TOPSIS approach reflect the combined inputs of a theoretical analysis and qualitative analysis. Whilst extant literature highlights a heterogeneous application of criteria across studies, it is possible to deductively categorise the indicators observed within the corpus into five categories. Namely, economic, environmental, social, technical and political-related issues. Most studies attempted to solve a profit-based optimization problem, relying on cost-based factors and valuation metrics to explain determinants of choice. Economic criteria, therefore, describes the indicators used to assess a renewable energy project’s financial performance such as investment cost, cost of imports, NPV, project duration, IRR and taxes [

38,

46].

Additionally, the quality of local infrastructure, access to natural resources and environmental impact (measured by CO

2 and Nox), frequented as an environmental criteria [

47,

48]. Studies, which included these indicators, assessed the suitedness of a technology in a specific geography placing attention on the external environment rather than the performance-related consequences of technology deployment. Similarly, the technical criterion enables a comparative assessment of technology feasibility, however, these drivers are independent of location-specificity constraints. The authors in [

48], introduce module design and the technical capacity of PV technologies to rank alternative investments. Local labour quality, stakeholder acceptance and the availability of human resources predominated as indicators of social criteria [

49].

Finally, very few studies considered the relevance of political issues, however, those examining optimal site selection or determinants of international investment were more likely to do so. Political criteria commonly included risk and security issues, resulting in varying definitions. Specific indicators such as the promotion of private ownership, incentives, investment freedom and corruption emerged across only a select number of studies (see

Table 1).

Although, the results of the qualitative analysis reinforce the relevance of economic, environmental, social, technical and political aspects, notable differences are observed in

Table 1. First, few interviewees included environmental criteria in their responses. The limited number of references to natural resource abundance and environmental impact is, however, palpably explained by the macro-level context of study. Examining the evaluation criteria used in similar international MCDM studies, focused on country-level decision-making problems, supports the assertion.

Both [

50,

51], for example, either excluded environmental criteria from their studies or focused on measurements of infrastructure quality to analyse the decision-making determinants of optimal FDI location choices. Second, the political aspects of African renewable energy investments are emphasised in detail throughout the interviews, however, received less attention in the theoretical analysis. Political instability, energy policies, Power Purchase Agreement (PPA) quality, energy market characteristics, Feed-in-Tariffs (FITs), and approval and permits, identified as indicators to assess project feasibility. The emphasis on political factors arguably reflects the expectations of lower government effectiveness and increased uncertainty of project completion in many African countries. Consequently, the evaluation criteria chosen for the fuzzy TOPSIS approach incorporate aspects from each of the five categories, however, particular attention is placed on the political determinants of investments.

Similarly, economic factors are emphasised due to their recurrence during the interviews and in the literature review, conducted as part of the theoretical analysis. A summary of the evaluation criteria included in the fuzzy TOPSIS approach is shown in

Table 2.

4.1.1. Social Criteria

The social criterion, C1. Local Demand Characteristics utilizes indicators such as per capita income and national electrification rates to proxy the level of power consumption within a country. In low income economies the cost of energy services constitutes a significant proportion of total monthly household expenditures and, in turn, influences the demand for additional capacity to be connected to the local grid [

52].

4.1.2. Economic Criteria

Three criteria are introduced to test the pertinence of economic considerations on private investment: C2. Macroeconomic Uncertainty, C3. Retail Electricity Prices (USD) and C4. Unlevered Cost of Capital. Macroeconomic uncertainty, as defined by local currency volatility and inflation, increases a developers financing risks and is expected to influence the investment decision. Additionally, both the unlevered cost of capital and retail electricity prices, are introduced to proxy the financial attractiveness of an investment.

4.1.3. Environmental Criteria

The theoretical analysis and qualitative analysis highlights a relationship between the technical capacity and quality of local energy-related infrastructure, and investment performance. The C5. Infrastructure Quality criterion considers the quality of power lines, distribution grids and other energy-related assets as proxies for the complexity of connecting generation assets to local energy grids. Additionally, it is presumed that low infrastructure quality increase the likelihood for energy curtailment and other distribution losses. These indicators may simultaneously influence the financing risks that arise from revenue forecasting errors during planning.

4.1.4. Political Criteria

Political risk remains prevalent throughout the African continent and is expected to significantly influence the investment decision. Government Effectiveness is low relative to the rest of the world (see

Figure 1) and requires investors to consider the potential impact of political instability, corruption and fragmentation on the performance of a project. To capture these aspects in the fuzzy TOPSIS approach, we introduce C6. Power Purchase Quality, C7. Energy Policies and Tax Rates, and C8. Energy Market Characteristic as political criteria. On the one hand, PPAs encourage private sector participation through revenue-based incentives and provides the contractual arrangements needed to obtain additional security for investment such as guarantees. On the other hand, the efficacy of these arrangements to stimulate investment hinges on regulatory commitment and the likelihood of offtaker risk. Additionally, energy policies, taxes and the energy market characteristics can stimulate private sector participation in the energy sector. Ref. [

11], for example, conjecture that regulatory frameworks are necessary antecedents to encourage new investment in generation assets.

4.1.5. Technical Criteria

The C9. Access to Local Market Information criterion refers to the availability of information for an investment and is expected to influence decision-makers as a non-financial driver [

10]. Due to the high technical requirements of renewable energy projects, the availability of advisors, technical experts and consultants within a country moderates a private firm’s knowledge of the local operating context.

4.2. Criteria Weights

Results for the criteria weights were collected from 49 investment professionals with energy-related experience in Africa. The first stage of the survey required participants to rank evaluation criteria based on a Likert scale, ranging from “Very low importance” to “Very high importance” (

Table 3).

Based on the survey submissions, the fuzzy weights for each evaluation criteria were calculated. The ranking in

Table 4 indicates that PPA quality is considered the most important determinant for assessing projects alternatives, followed by macroeconomic uncertainty and local demand characteristics. Thirty-one respondents in the study rated the importance of the PPA as being of “Very high importance”, significantly higher than the 23 responses received for the macroeconomic uncertainty criteria.

Although the ranking of criteria appears consistent with the findings in the theoretical analysis and amongst the collected interview responses, several intriguing results emerged in the output. The order preference of the equity cost of capital, for example, was inferior to the local retail energy price. Further, local infrastructure quality ranked third last by order of weighting, significantly lower than presumed from both the theoretical analysis and expert interviews.

4.3. Fuzzy TOPSIS Results

Both the fuzzy decision matrix and fuzzy weighted normalized decision matrix are derived from the output of the preceding discussion. Having obtained the evaluation criteria weightings, the vector values are aggregated with the ratings assigned by participants for the evaluation criteria of each alternative. Subsequently, the favored solution represents the perceived attractiveness of criteria for a country and the overall importance assigned to an individual criterion based on the group weightings. Normalization occurs by calculating the Euclidean distance of each response to the FPIS and FNIS, as both the highest and lowest possible scores attainable from the list of criteria.

Table 5 summarizes the fuzzy Weighted Normalized Decision Matrix. Given the importance of the leading criteria, PPA quality, macroeconomic uncertainty and local demand characteristics, the alternatives with the highest triangular membership function are preferred as investment destinations. The output indicates that individuals prefer the local demand characteristics and PPA quality in South Africa, whereas issues related to macroeconomic uncertainty are less concerning to investors in Kenya. As highlighted in

Table 6, these results are also supported by the FPIS and FNIS outputs for each alternative. The preferred country for the renewable energy investment is expected to have the shortest distance from the FPIS (lowest value) and longest distance from the FNIS (highest value).

The closeness coefficients for each country are calculated as the final stage of the fuzzy TOPSIS analysis.

Figure 4 plots the combined results of these outputs. Consequently, South Africa is identified as the preferred investment destination for renewable energy projects based on the survey responses and the evaluation criteria introduced in the study. Kenya ranked second, followed by Tunisia, Nigeria and Cameroon, respectively.

In addition to the order preference of alternatives, differences between objective indicator values, their expected ratings and the actual response from participants are observable. South Africa, which has preferential local demand characteristics and a low unlevered cost of capital relative to the alternatives should, for example, rank as the preferred alternative in these categories. More specifically, the order preference of alternatives presumably follows a symmetrical ranking between the rating of the evaluation criteria and the presented indicators. Whilst the assertion upholds in this example, asymmetries are also identified in several areas.

First, variances in the expected results emerged whenever an evaluation criterion contained identical indicator values for several alternatives. The countries, Kenya, Nigeria and Tunisia had the same indicator values for PPA quality. Our fuzzy weighted normalized decision matrix, however, signifies a large variance in the fuzzy triangular numbers: (0.441,0.715,0.923), (0.250,0.468,0.689) and (0.376,0.635,0.846), respectively. Second, whilst the PPA quality rating in South Africa should be inferior relative to the other alternatives, the results failed to promulgate the relationship.

Instead, South Africa received the highest rating for this criterion as exemplified by the membership function, (0.502,0.777,0.973). The results are interesting for several reasons. Foremost, whilst Kenya, Nigeria and Tunisia offer standardized contracts in both local and foreign currency, South Africa provides similar contracts in local currency, only [

37]. When PPAs cannot be denominated in hard currencies such as EUR and USD, investors are susceptible to increased financing risk arising from foreign exchange liabilities. Additionally, although participants reported greater concern for macroeconomic uncertainty in South Africa than in Kenya and Tunisia, the results seem inconsistent. Subsequently, the findings suggest that additional drivers, excluded from the study, were also considered in responses. Whilst indicators capturing the likelihood of contract renegotiations and regulatory commitment were purposefully excluded from analysis (due to data limitations), it is palpable that such issues took precedence in responses.

5. Discussion and Conclusions

Several interesting findings related to the non-financial and financial determinants of investments in African renewable energy projects are highlighted in the paper. Foremost, the quality of regional PPAs significantly moderates a decision-maker’s choice of investment. Of the nine evaluation criteria introduced in the study, the policy-related issues embedded in contractual arrangements preside as the primary concern for investment decisions. Determinants such as macroeconomic uncertainty and local demand characteristics are also identified as pertinent variables in the study. The ratings assigned to the evaluation criteria highlight that valuation indicators such as the cost of capital are considered less significant during the early stages of the decision process.

Further, the rankings of the alternative country locations are mostly consistent with the assumed order preference derived from the indicator values of the nine evaluation criteria. Specifically, participants correctly identified the preferred solution (alternative) based on rational expectations. Countries with preferential conditions for leading criteria were also more likely to be given a higher rating by the decision makers. Inconsistencies emerged, however, whenever the values associated to an evaluation criteria were identical for two or more countries.

Finally, our findings are in line with the seminal work of [

10]. Although their econometric analysis of behavioral factors in energy investments was tested on 135 European investors, we find several similarities in the results of the fuzzy TOPSIS study. First, the expert interviews and order preferences corroborate the relevance of a priori beliefs, institutional pressure, attitude towards technological innovation and knowledge of the RE operational context as non-financial drivers. Second, an investor’s confidence in the effectiveness of existing policies and confidence in technology adequacy both influence the capital allocation decision for renewable energy projects. However, whilst the conceptual model suggests that the latter takes precedence over the former, our findings suggest otherwise. Beliefs about the effectiveness of policies predominates as a pertinent evaluation criterion used by investors to evaluate investments in African energy infrastructure. Country and regional heterogeneities, including issues related to the complexity of the business environment and macroeconomic environment are compelling arguments to explain the observed differences.

5.1. Confidence in Policies

Investor confidence in policies has been promulgated extensively throughout the paper as a cause for the perceived absence of investment opportunities throughout Africa. Solutions to the energy investment gap requires addressing regional realities, including comparatively low government effectiveness. Further, the high degree of bundled ownership in energy markets has resulted in skill and knowledge shortages for the development of effective renewable energy sectors, hindering the confidence instilled by investors when examining potential investment locations. Several remedies to the current challenges are conjectured.

First, due to the low energy sector privatization in many African countries, government preferences determine the competitiveness of different power infrastructure technologies. Subject to the co-movement of oil and renewable energy prices, and exacerbated by poor governance, it is not surprising to evidence changes in contracted PPAs over time. As such, aligning private sector objectives to domestic policies is pertinent to achieve cooperation with local stakeholders, and to mitigate political interference. Further, these factors also influence energy sector development: frequent changes to targets and policies slow technological progress. In order to address the adverse consequences of market imperfections on FDI inflows, governments are tasked with establishing markets for renewable energy. Stimulating the demand-side eliminates institutional rigidities from power infrastructure investments. In India, Renewable Energy Certificates (RECs), have been used to encourage the production of power from sustainable sources [

53]. These certificates (or credits) are traded via digital marketplaces, facilitating a competitive environment for trade. Consequently, the use of RECs augments the preferences for renewable energy investments and, partially, reduces the significance of issues related to an investors confidence in policy effectiveness.

Second, investment in local capacity building is encouraged to enhance the effectiveness of PPA contracts in bi-lateral and tender agreements. The development of local skills reduces regulatory dependence on external advisors to facilitate effective bidding rounds and, simultaneously, improves the business environment for new entrants. Ref. [

11] posit that skills shortages in the energy sector cause costly delays, administrative bottlenecks, incoherent frameworks and contracting issues. Improving confidence in policies is also considered tantamount to the enhancement of knowledge in energy sectors. In this regard, there is a compelling opportunity to contribute to renewable energy development in Africa. Companies and institutions which support regulators in the development of skills, tools and knowledge, can contribute to addressing the barriers for private sector participation.

Third, we posit that an interrelationship exists between investor confidence in policies and the financial risk exposure of developers during construction and operation stages. During pre-operation, the equity and debt capital allocated to a project must exceed all expected cash outflows. Simultaneously the availability of financial resources is contingent on the quality of the agreements conferred to the energy provider in a local jurisdiction. Consequently, enhancement of the perceived attractiveness of an investment destination, hereby referring to non-financial drivers of investment decisions, improves a generators ability to procure financing at lower cost. Or, improves the sources of capital available to the investor. Remedying the determinants of confidence in policy effectiveness not only improves the perception of alternatives by the decision maker but has spillover effects on the nexus of stakeholders included in the project. Lower costs of capital, resulting from the perceived reduction in uncertainty, for example, can encourage new private sector participants into African economies.

The Gordian knot which plagues Africa is unlikely to unravel without institutional change. In India, setting up integrated arrangements for promoting renewable energy sources proved effective in bypassing institutional rigidities [

53]. As such, the paper also addresses the need for investors to adopt valuation methodologies, which capture risk differences throughout project development stages (during planning, operation and construction). Risk-adjusted discount rates and assumptions in a DCF model are identified as a possible methods to capture the variability of financing risks throughout the different stages of project development. Additionally, the paper highlights the benefits of quantifying drivers and areas of uncertainty to understand better the issues impacting a decision-makers choice. Given the simplicity of designing and conducting a MCDM analysis, practitioners are encouraged to integrate the results of these methodologies into financial models and existing assessment procedures. By delineating the expected weightings and importance of financial inputs, methodologies such as the fuzzy TOPSIS prove useful in explicating the macroeconomic issues impacting the performance of a project.

5.2. Limitations and Areas of Further Research

Although the paper provides valuable results, highlighting several issues pertaining to Africa’s infrastructure investment gap, its macroeconomic scope of analysis imposes limitations on the research findings. First, different renewable technology attributes, including capacity and cost, are important considerations affecting investments in power infrastructure. Assessing the suitability of wind, solar and thermal projects is, therefore, achieved by relying on different evaluation criteria, excluded from the research approach. The omission of location-specific infrastructure issues makes it difficult to evaluate technology options in the optimal investment location. Assessing investor preferences for different technologies in African economies constitutes an important area of research as technology adequacy and innovation are expected to moderate a decision-makers choice.

Second, findings from the fuzzy TOPSIS analysis are generalized to elucidate the challenges of renewable energy projects in Africa. Both arguments in favour of and against the homogeneity of countries throughout the continent are considered. Arguably, however, the heterogeneity between countries, including those in the same regions, is difficult to overlook. Delineating the specific issues related to investor confidence in policies, in the form of PPA quality, is an important finding of the paper. Studies examining energy policy effectiveness, and PPA quality, in country-specific case studies would, however, contribute significantly to the present discussion.

Thirdly, because the paper utilises a private-sector perspective, profit maximization arguments are predominately used to address the research question. Given the added social cost of infrastructure projects, analysing the viewpoints of government and the decision-making determinants of the public sector would also be of value. Interestingly, ref. [

54], has alluded to the conflicting interests of regulators during periods of uncertainty. Countries identified as laggards of socio-economic development are often constrained by conflicting priorities, which likely exacerbate the poor policy effectiveness concerns of investors.

5.3. Conclusions

A growing body of research posits the necessity for private sector participation in African power sectors in order to encourage renewable energy development and to address perpetuating investment gaps. Presently, public funding in the region is not sufficient to provide basic energy services and to match the expected increase in demand correlated with population growth in the coming decades. Consequently, large African populations still rely on unsustainable captive hydrocarbon energy solutions for industrial application, and biofuels for household use. The lack of infrastructure remains a cause of Africa’s subdued socio-economic development.

Whilst external financing of power infrastructure has increased in recent years due to the progressive movement of power sector reform, private sector participation in African energy projects is still low relative to other low-to-middle income economies. Macroeconomic and microeconomic constraints explain the comparatively small number of privately funded power infrastructure. High levels of economic uncertainty, low government effectiveness and the concentration of state ownership in the sectors increase the complexity of developing these projects in African economies. Whilst uncertainty is coalesced in the risk-reward profiles of local energy projects, these factors also influence the non-financial drivers through which investors make choices. In particular, the dissemination of information by a decision-maker depends on the interpretation of country or project-specific criteria through personal beliefs, attitudes and knowledge of the local environment. Despite the evidence that non-financial drivers matter to explain investor behaviour in renewable energy projects, the relevance of these factors in an African context has received limited attention.

The paper addresses the knowledge gap by delineating the non-financial and financial determinants of private investment in African renewable energy. Understanding the links between these categories and their influence on investment decisions is necessary to predicate policy recommendations. We used nine broad evaluation criteria that capture financial and non-financial drivers of an investment. Our findings reveal that political criteria predominate as primary indicators for investors when examining country-level indicators of project feasibility. Issues related to government effectiveness, the presence of energy policies, PPA quality, energy market characteristics and approvals contribute to the challenge of renewable energy infrastructure development in Africa.

Experts rated the importance of 9 evaluation criteria and ranked the attractiveness of 5 African countries for a hypothetical renewable energy infrastructure investment. Of these criteria, PPA quality ranked highest by the degree of importance, followed by macroeconomic uncertainty and local demand characteristics, respectively. The cost of capital and the quality of local infrastructure ranked lower than expected. It is palpable that investors considered the certainty of infrastructure-related challenges in emerging economies less significant than the consequences of unexpected events and interference on project performance. Further, of the 5 African countries in the experiment, South Africa emerged as the preferred investment destination for renewable energy projects, followed by Kenya, Tunisia, Nigeria and Cameroon, respectively.

Our findings indicate that investor confidence in policy effectiveness moderates the investment decision more in Africa, relative to Western alternatives. We propose several solutions to address these differences and the interdependence between policy-related evaluation criteria such as PPA quality and the outcome of the MCDM experiment. First, we posit the importance of local capacity building through the provision of resources to acquire skills and knowledge in energy sector development, effective policy frameworks and contracts, as signalling effects for improvements to regulatory commitment. Enhancing the effectiveness of bi-lateral contract and tender rounds encourages the development of local renewable energy industries directly and influences the perceptions of external investors. Second, stimulating demand-side pressure can disintermediate areas of government tasked with encouraging renewable energy development. Trading these contracts on exchanges both increases the competitiveness of renewable energy technologies and mitigates institutional rigidities, which contribute to the perceived lack of policy confidence.

Enhancing the indicators through which criteria such as PPA quality and macroeconomic uncertainty are interpreted by private investors can significantly contribute to resolving Africa’s power infrastructure gap. In short, presenting projects in a manner that is palatable to international alternatives is just part of the solution. Ensuring regulatory commitment is critical to remedy the legacy of beliefs about uncertainty throughout the continent.

{kind=link}

{kind=link}

{kind=link}

{kind=link}