Abstract

During the past decades, environmental related taxes, energy, and carbon taxes has been recommended by environmental scientists as a policy tool to mitigate pollutant emissions in developed and developing economies. Among developed nations, Denmark, Finland, Sweden, the Netherlands, and Norway were the first regions to adopt a tax on carbon dioxide (CO2) emissions and research into the impacts of carbon tax on carbon emissions bring significant implications. The prime objective and goal of this work is to explore the role of carbon tax reforms for environmental quality in European economies. This is probably the first study to conduct a comparative study in European context for carbon-tax implementation and non-implementation policies. To this end, the present study reports new conclusions and implications regarding the effectiveness of environmental regulations and policies for climate change and sustainability. In the present study, the authors exhaustively explore the impacts of the carbon-tax on the mitigation of CO2 emissions. Using the propensity score matching method, the results of the estimation of the different matching methods allow us to observe a positive and significant impact of the adoption of the carbon-tax on stimulating the reduction of carbon emissions.

Keywords:

carbon-tax; CO2 emissions; environmental related taxes; environmental regulations; propensity score method JEL Classification:

Q55; Q58

1. Introduction

Climate change is an undeniable fact today. Its damage to the state of the environment and to humanity has been considered the most serious problem causing environment changes worldwide. The emissions of CO2 remain the main factor in greenhouse gases (GHG) and the increase in its mass comes mainly from the harmful use of polluting (non-renewable) energies. According to the latest assessment report of the Intergovernmental Panel on Climate Change [1], the annual growth of CO2 emissions (fossil fuels, cement production, etc.) over the period 2002–2011 was 54% above the 1990 level. Regarding the challenges of climate change, reducing the level of greenhouse gas, CO2 emissions, and seeking low-growth development of emissions has become predictable.

To mitigate the greenhouse gas and CO2 emissions, the international organization (United Nations (UN), European Union (EU), Intergovernmental Panel on Climate Change (IPCC), Organization for Economic Co-operation and Development (OECD) have recommended several policies and administrative reforms, energy transformation, environmental related taxes, carbon-tax, emission standards, and emission trading schemes. Among these methods, economists and international organizations strongly recommend the tax on carbon emissions, which is a gainful tool for achieving a given reduction target [2]. The tax on carbon emissions is imposed on polluting energies and related products such as coal, oil, and gas and is based on their share of CO2 emissions. Depending on the increase of emissions, taxation will increase too. This could be helpful to reduce the consumption of fossil fuel energies and CO2 emissions. The interaction between emissions tax and emissions of CO2 is bilateral [3]. On one side, they inspire energy saving as well as the investments in the progress of the energy effectiveness and support the exchange of the combustible crops and then there will be some development in the structures of energy consumption and production.

On the other side, they affect the investment and the behaviors of energy consumption by recycling the receipts of the taxes collected from emissions [4]. The determinants of carbon emissions are not uniform across developed, developing, and emerging economies, and their assessment on carbon emissions mitigation is limited. The governments and policymakers around the globe submitted their Intended Nationally Determined Contributions (INDCs), which are plans to mitigate the pollution level and greenhouse gas emissions and reformed the strategies to climate change issues in the Paris Agreement [5]. Similarly, the United Nations developed several sustainable development goals (SDGs) of developed and developing economies to reduce the pollution and environmental externalities. Few of these SDGs of developed economies address the cleaner and greener energy, affordable energy, reduction of fossil fuels, sustainable growth, and environmental regulations. After the 1991s, few of the European economies started to implement energy related taxes, environmental taxes, and carbon-taxes to reduce the pollutant flux. However, the issues of climate change are still persistent, and it needs more advanced and innovative reforms. The current research is an attempt to check the performance of environmental regulations for European economies (tax adopted and non-tax adopted) and fulfills the research gap by offering new solutions regarding the role of carbon-tax in developed countries.

Currently, only some countries are implementing a carbon emissions tax due to their damaging effects on the competitiveness of local productions and the externality of CO2 attenuation. These states (or areas) that must adopt taxation of carbon emissions include Denmark, Estonia, Finland, France, Ireland, Iceland, Latvia, Norway, Poland, Portugal, United Kingdom, Slovenia, Sweden, Switzerland, South Africa, Chile, United Kingdom, Colombia, Canada, Japan, and Mexico. A common feature of their operation relates to the insertion of exemption and relief taxes [6], particularly for industrial regions with a big share of energy use. This suggestion raises numerous questions: for example, does a carbon-tax lead to reduce CO2 emissions level? If so, how important is the impact of carbon taxation policy on environment? Against this backdrop, the key hypothesis of this study is whether the carbon tax reform implemented nations have less carbon emission as compared to non-tax implementation nations? In recent years, the gradually critical difficulties linked to security of energy, savings of energy, and the CO2 emissions mitigation have forced many countries like France, Japan, and China to register the tax on CO2 emissions on the agenda. The question of how to profit from the benefits and avert the weaknesses of taxes from CO2 emissions should be a matter of important worry for these nations. To provide an evidence of tax from emissions of CO2 to these countries, it is well important to deliberate the effects of attenuation real of the carbon-tax on the European Convention countries [7,8].

This article mainly offers two innovations in the existing literature. Firstly, this research reports a comparative analysis for European tax implemented and non-implemented economies. To this end, the study examined the relationship between energy intensity, carbon intensity, population, income, and carbon emissions for sample economies. Previously, the empirical studies have ignored the aspect of comparative analysis and role of energy intensity, carbon intensity, and population [7,9,10]. From a theoretical sense, population, energy, and carbon intensity presents overall resource utilization and energy efficiency. The environmental taxes, regulations, and administrative policies are helpful to promote cleaner energy sources by making the charge competition with inexpensive fuels. For example, imposing carbon-tax on inexpensive and less-expensive products (coal and oil) might promote the cost of electricity production as compared to renewable power generation sources. Similarly, the effective tax policies in the case of carbon trading sets a definite limit on overall greenhouse gas and emissions of CO2. Hence, the present study reports new highlights and solutions regarding the role of carbon-tax for emissions of CO2. Environmental (environmental taxes, energy taxes, and carbon taxes were initially implemented by few developed nations of Europe and OECD; with the passage of time, the environmental taxation policy has been adopted across developed, developing, and emerging countries [2]) and carbon-tax are regarded as policy instruments which have diverse effects on the economy, residents, and climate change. Theoretically, it is considered that the tax implementation is a policy for sustainable transformation, as the environmental policies would induce to transform the industrial and manufacturing processing’s [2,8,11].

Secondly, the current research reports new conclusions and solutions regarding the climate change in European developed economies. In doing so, the findings of this study can be regarded as a way forward to achieve few of the sustainable development goals (SDG–7: clean and affordable energy, SDG–8: sustainable economic growth, SDG–13: Climate Action) of developed economies. During the past decade, the developed economies have struggled to upgrade the energy strategies i.e., zero-nuclear by Japan, energy vehicles by Japan, shale gas by USA. Although these efforts might be significant for energy security, but under the pressure of rising population growth, energy, and carbon intensity, the energy usage of developed economies raised by 2.5%/year. Among the developed economies, only the OECD energy consumption is accounted for 60% of global energy demand, which mainly consists of non-renewables and fossil fuels [12,13]. The inquiry into the role of carbon-tax, population, energy, and carbon intensity is logical and consistent with the strand of existing research [10,14,15,16].

2. Literature Review

Regarding the current surveys related to the impact of the human activities on the environment, the carbon-tax is often regarded as a profitable tool to mitigate emissions rate. The effectiveness of the carbon-tax was studied by many authors and the results differ according to the impact and objectives. The study joins the Pigovian (Pigovian tax is implemented on those goods which creates negative externalities; the main aim of such taxes is to make the price of good equal to social marginal costs and create socially efficient resource allocation) tax theory, which deals with the environmental charges by adding the carbon-tax into total charges. The carbon-tax is a type of consumption tax which can depend on the CO2 emissions from energy consumption or fossil fuels. The carbon-tax mainly focuses on the carbon mitigation. Hence, the carbon-tax also promotes energy saving, development of cleaner and cheaper energy sources, and technological transformation, as compared to other energy or environmental taxes [11,15,17]. The present study endorses the findings of [2,8]. There is a dearth of literature regarding the role of carbon-tax and environmental taxes for energy and environmental issues. Few of the relevant studies are discussed here.

Agostini et al. [18] examined the reaction of implementing taxation on the emissions of CO2 produced by the processes of combustion into the countries of OECD-Europeans. A sectorial model of the consumption of power is built to inspect the saving energy and the substitution properties between fuels induced by the introduction of various taxes on carbon during the period of simulation 1989–1994. The empirical results documented that environmental related taxes are a useful policy tool in carbon mitigation. The energy saving or the process of substitution of the fuels which result from the introduction of the environmental taxation and stabilization from the emissions with the level from 1988 only with the sector from production of electricity, and reached only if the high tax rates are supposed (100 $/tons. C). The study revealed that the implementation of a tax of 100 $/tons can restrict and reduce the carbon emissions. The outcomes would endorse the summary of various synchronized environmental tools.

According to Agostini et al. [18] the environmental policy must be designed by taking account of the specific economic situation and the technological choices of each country alone. The environmental policies specifically coordinated to each country are to be recommended, where international coordination should relate to the environmental objectives rather than instruments. In a similar study, Baranzini et al. [4] evaluated the carbon-tax with regard to their competitiveness, the distribution, and the environmental impacts. The results showed that the carbon-tax can be an interesting option of the environmental policy and that their principal negative impacts can be compensated by the design of the tax and the use of the generated revenues from taxes. Among the sample countries of Europe, Norway followed very strict policies for climate change. The principal tool of the policy is a relatively high level of greenhouse gas emissions, and the country implemented carbon-tax in 1991 [19].

Bruvoll and Larsen [20] studied the effectiveness of carbon-tax in Norway and they noted a significant reduction of the emissions per unit of GDP (gross domestic product) because of the reduced radiant intensity, although the total emissions increased. In spite of the taxes and the considerable rises in price for certain types of fuel, the effect of the carbon-tax was modest. Although the partial effect of the variations of the radiant intensity and mix lower energetics was a reduction of the emissions of CO2 by 14%, the taxation of carbon contributed to the reduction by only 2%. The taxation of carbon was recommended for a long time because of their cost-effectiveness ratio to arrive to a reduction of the emissions given.

Zhang and Baranzini [21] mentioned in their article about the principal economic impacts of the taxes on carbon emissions. On the basis of examination of the empirical studies on the taxes carbon/existing energy, they concluded that the competing losses and the distributive effects generally significant and are not certainly less often perceived. Due to the convention’s billing targets, the future rate of the carbon tax may be higher than those already imposed. Thus, the economic effects can be more serious. In this context, it has been well proved that the way of using the generated income coming from taxes will be significant in determining the final economic effects of carbon-tax. However, being given the ultimate objective of Convention-tallies, the future environmental and carbon related taxes might increase than the existing tax rates and thus the economic impacts which result from it could be acuter. In such context, the literature argues that the generated tax revenues can be of fundamental importance to determine the future economic output and population welfare [2].

Lee et al. [22] analyzed the impacts of the combination of a tax on the carbon and the exchanges of emissions on the various sectors of industry. The results highlighted that the loss of GDP was caused by the dependent carbon-tax. A petrochemical industry during the period 2011–2020 may induce carbon 5.7% during nine years. However, the value of the losses of the GDP will drop by 4.7%, if the carbon-tax is implemented jointly with the exchanges of emissions. Moreover, among the sectors related to petrochemical industry, the sectors emitting more carbon must buy additional licenses of emissions to achieve the goals of environment and carbon emissions.

Callan et al. [23] studied the effects of tax policies on the carbon and the recycling of the incomes through the distribution of income in the Irish Republic. The results argued that a tax on the carbon of 20 €/tCO2 would cost the households less the poorest steps than 3 €/week and the richest households of more than 4 €/week. A tax on carbon is regressive, therefore, the revenues from taxes are used to increase the social security benefits and the tax credits. The households through the distribution of income can be better without exhausting the revenues from taxes carbon total.

Lu et al. [24] investigated the impact of the tax on carbon for the case of China. By building a model of recursive balance general dynamics, the authors have examined the damping effects of the complementary policies. The authors studied the role of taxes and the effects of damping of the complementary policies by building a model of recursive balance general dynamics. The simulation model findings mentioned that the carbon-tax is an effective political tool because it can reduce the pollution level by mitigating the carbon level. Further, the study argued that tax related policies will reduce the economic output of China. The present model designates new equilibrium for each sequential independent period of time after tax on carbon and the complementary policies are imposed. Thus, this kind of model could describe the long-term impacts of these policies. The results of the simulation show that the carbon-tax is an efficient average since it reduces the rate of carbon emissions with a small negative effect on economic growth. The drop in the indirect taxes will help reduce the negative impact of the carbon-tax on the production speed and competitiveness. In addition, giving households subsidies in the meantime helps to stimulate household consumption. Therefore, the complementary policies used jointly with the carbon-tax will assist on reducing the negative effects of the tax rate on the nation’s economy. The dynamic EGC analysis proves that the impact of the carbon-tax on GDP growth is relatively small, while the reduction in carbon emissions is relatively large. As the most effective market base mitigation instrument, the carbon-tax is strongly advisable by economists and universal governments. Several countries were the first to adopt the carbon-tax policy (e.g., Denmark, Finland, Sweden, the Netherlands, and Norway). In these countries, the examination on the placement effects of the carbon-tax will be of great practical importance and therefore they will set an example for countries that take the tax.

Similarly, Lin and Li [17] considered the actual effects of CO2 emissions mitigation in five northern European countries using the difference-in-difference (DID) method. The results from the empirical study indicate that, in Finland, the carbon-tax has a significant and negative impact on the growth of its CO2 emissions per capita. The effects of carbon-tax in Denmark, Sweden, and the Netherlands are recorded to be negative but not significant. The mitigation effects of the carbon-tax are weakened due to tax liberalization policies on certain radiant-intensive industries in these countries. In Norway, the fast growth of the energy-generating products involves a substantial increase in the CO2 emissions in the sectors of oil drilling and of the exploitation of natural gas; the carbon-tax did not carry out its effects of attenuation.

Studying the data of environmental related taxes, Morley [7] investigated how the tax policies induce pollution and energy consumption. The empirical results concluded that envirnomental related taxes are negatively associated with pollution level, while the tax policies may not effect the energy concusmption. Vera and Sauma [14] investigated the role of carbon-tax in mitigating emissions for the case of Chile. The empirical results claimed that imposed carbon-tax might reduce the emissions level by 1% with respect to the forcasted period 2014 to 2024. For the case of European countries, Borozan [25] claimed that the energy related taxes signficantly affect the electricty use more efficiently by affecting the energy prices directly and indirectly.

Sen and Vollebergh [26] estimated the effects of carbon-tax on energy consumption of OECD countries. The study concluded that one euro increase in energy taxes might reduce the carbon emissions from fossil fuels by 0.74% in OECD countries. For the case of European Union countries, Borozan [15] explored the role of energy taxes and income on residential energy demand. The empirical findings of panel quantile regressions revealed that energy taxes and income significantly boost the residential energy consumption in Europe. Studying the data of OECD economies, He et al. [12] explored the role of environmental related taxes for energy efficiency. Based on the panel logit and DEA (data envelopment analysis) models, the results suggested that the energy related taxes significantly enhance the energy efficiency of coal and natural gas energy sources consumption. In the same line, He et al. [19] concluded that the double dividends of energy taxes significantly reduce the carbon emissions in four Nordic and G7 countries.

In a comparative study, He et al. [27] investigated the effectiveness of environmental taxes in reducing pollution levels in China and OECD countries. Based on the findings of Auto-Regressive Distributed Lag Modelling Approach (ARDL) for annual data of Chinese provinces and OECD countries, the research concluded that environmental related taxes are an effective tool to curb the pollution levels.

More recently, Wang and Wei [11] investigated the threshold effects of technological progress and environmental regulations on carbon emissions of OECD and emerging economies. The authors used the annual data of 24 OECD and 8 emerging economies for the period of 1990 to 2015. The PSTR (panel smooth transition regression) model findings revealed that the strict regulations in emerging economies may harm the economic development. Further, the study mentioned that that OECD countries should improve environmental related technologies to improve energy efficiency for lower pollution levels.

In a more comprehensive study, Ulucak et al. [8] researched the non-linear effects of environmental taxation on carbon emissions for four BRICS (Brazil, Russia, India, China, South Africa) countries. The empirical results of the PSTR model argued that environmental taxes may not be effective to reduce the carbon emissions and pollution level. Similarly, the results highlighted negative effect of environmental related technologies on carbon emissions. In the same line, Shahzad et al. [28] reported that energy consumption for fossil fuels induces environmental extremities, while the role of energy taxes, carbon taxes, and environmental related taxes is still ambiguous for developed and emerging economies.

The rising energy demand of fossil fuels and non-renewable sources have triggered the greenhouse gas emissions and carbon emissions. The European countries initiated environmental regulations and tax policies, which can limit the industries to use coal, oil, and other non-renewable energy sources. Hence, the investigation into the role of carbon-tax for countries who implemented tax and non-tax implementation countries is of logical and sound mind. As a final remark, our study joins the strand of [2,6,8,11,12,19].

3. Data and Methodology

3.1. Data Sources and Modelling

The Kaya identity is a useful equation for quantifying the total emissions of the greenhouse gas carbon dioxide (CO2) from human sources. However, in the present study, the carbon emissions are used as a key dependent factor. The traditional model is based on readily available information and can be used to quantify the current carbon level and how the relevant factors need to change relative to each other over time to reach a target level of CO2 emissions in the future.

The identity has been used, and continues to be important, in the discussion of global climate policy decisions. The Kaya identity states the total emission level of CO2 as the product of four factors:

Regarding the selection of covariates, Kaya decomposed the factors related to CO2 emissions in population (POP), GDP per capita (), energy intensity (), and carbon intensity () with PE as primary energy. More recently, [6,12,15,19,24,26] also studied the role of energy taxes and environmental taxes for environmental issues in Europe, China, and OECD countries.

To investigate whether the adoption of carbon-tax policy in European countries promotes the reduction of CO2, we implement the nearest-neighbor matching (hereafter NNM) methodology initiated by Rubin [29] and developed by Rosenbaum and Rubin [30]. This estimator was derived by Abadie and Imbens [31]. This method is becoming increasingly popular and widely used in micro-econometrics as well as in different areas such as health, education, etc. [32,33,34]. The NNM approach has nevertheless been recently employed in macroeconomic studies.

Based on the work of Cameron and Trivedi [35] and Greene, [36] the primary regression equation of endogenous treatment-effects model is:

where is a vector of covariates that affect the outcome, and are coefficients to be estimated, and are error terms. is considered a dummy variable taking the value 1 if a country adopts a carbon-tax policy, and 0 if not.

The decision to obtain the treatment is made according to the rule:

3.2. Nearest-Neighbor Matching (NNM)

The matching estimators are based on the probable outcomes of the model, in which each individual has a well-defined outcome for each level of treatment. In the binary-treatment probable outcome model, is the potential outcome obtained by an individual if the treatment level is equal to 1 and is the potential outcome obtained by each individual if the treatment level is equal to 0.

Formally, the average treatment effect (ATE) is given as follows:

while the average treatment effect on the treated (ATET) is observed in Equation (4):

NNM uses an average of the individuals that are most identic, but get the other level of treatment, to predict the unobserved potential outcome. NNM uses the covariates to find the most similar individuals that get the other treatment level.

More formally, consider the vector of covariates and frequency weight for observation . The distance between and is parameterized by the vector norm

where S is a matrix which is defined symmetric and positive.

where presents an vector (full of ones), is defines the identity matrix of order P, and W is a square matrix of dimension n, defined diagonal and contains incidence weights.

The exact form of ATE and ATET estimator is:

3.3. Sample

Our panel database includes 28 EU economies over the period 1990–2017. Data come from several sources, including Eurostat, US Energy Information Administration [37], and World Bank Development Indicators [38].

- Treatment group

The carbon tax was first introduced in Finland in 1990. It applied to fuel, coal, and natural gas. In 1994, Finland divided the fuel tax into a mixed energy tax and a carbon tax. Its amount is 20 €/ton of CO2 in 2008. In 2004, Latvia introduced the carbon tax in their system of environmental taxes established since 1990. It mainly covers the use of fuels. Its amount is 30 €/ton of CO2. Denmark adopted a proposal to levy a carbon tax in 1991 and put it into practice in 1992. The tax covered natural gas, petroleum, and other mineral fuels, except biofuel. Its rate was 20.60 €/ton of CO2 for individuals, as well as for industry and services for heating, 3.50 €/ton of CO2 for energy-intensive industrial sectors [39,40,41,42,43].

Slovenia has applied a carbon tax since 1996 for CO2 emissions resulting from the combustion of fossil fuels. Its amount was 17 €/ton CO2 in 2015. In 1991, Sweden introduced a carbon tax of 24 €/ton of CO2, which covered all fuels. At the same time, the rate of the existing energy tax has been reduced. The amount of the tax reached 114 €/ton of CO2 in 2019.

In France, the carbon tax was introduced in 2014; it is a tax on fossil fuels, petroleum products, natural gas, and coal proportional to their CO2 emissions. From an initial amount of 7 €/ton of CO2, it rose in 2020 to 56 €/ton of CO2 in 2020. The United Kingdom introduced the carbon tax in 2001. It aimed to reduce annual CO2 emissions by 2.5 million tones before 2010. It affects all energy consumers, with the exception of residential and transportation. The amount of the tax is 18 €/t CO2. Ireland introduced a carbon tax in 2010 that covers virtually all fossil fuels for the residential and tertiary sectors, transport and agriculture. the general rate is 20 €/t CO2 in 2019.

- Control group

In this article, we have chosen the member countries of the European Union as the control group these countries have not adopted a carbon tax. The selected countries are Belgium, Portugal, Cyprus, Germany, Hungary, Greece, Malta, Romania, Spain, Bulgaria, Lithuania Czech, Estonia, Croatia, Netherlands, Slovakia, Luxembourg, Italy, Austria, and Poland. Table 1 enlists the treatment group and control group of countries.

Table 1.

List of the sample countries with dates of carbon-tax adoption.

4. Result and Analysis

4.1. Preliminary Results

The matching method is used to try to twin each country treated with one or more untreated countries whose observable characteristics are closest possible. The objective of pairing is to build a reference group comparable with the treated group has fi N to allow an estimate not skewed of the effect of the treatment on the treated individuals, by controlling the skew of selection [40,41,42].

4.1.1. Covariate Balance Summary Test

To have an idea of balance between the covariables, we have to study the differences with standardized differences and ratios in variance. A perfectly balanced covariable has a standardized difference = 0 and one ratio in variance = 1. Table 2 mentions the covariates balance summary for all studied variables including income, population, energy intensity, and carbon intensity.

Table 2.

Covariates balance summary test.

The result indicates that the covariables are balanced or took 5 countries for the treatment against 5 countries for control.

4.1.2. Kernel Density

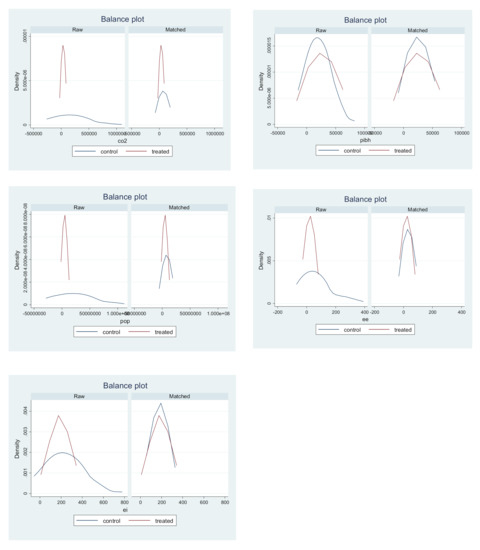

The kernel density is a non-parametric estimate method to check the density of probability for any random variable. It is based on a sample of a statistical population and makes it possible to estimate the density in any point of the support. Figure 1 reports the Kernel density for all studied variables for European economies.

Figure 1.

Kernel Density test.

The covariate is said to be balanced once its proper distribution does not vary between treatment levels. The kernel density gives density plots of a covariate over the processing levels of the raw data and the sample (weighted or paired). The kernel density is checked because it reports the density diagrams of a covariate on the processing levels for raw data for weighted and matched samples. It is important to mention here that if the matched sample of the covariate and density curves of the weighted sample are similar at different levels of treatment, the covariate is considered balanced in the weighted and matched samples. Similarly, the density graphs for the matched group sample are almost similar, suggesting that the estimated match would balance the covariates.

4.2. Analysis and Findings

The results of estimation of different methods allow observing a positive and significant influence of the adoption of the carbon-tax on the stimulation of the reduction of CO2 emissions.

The nearest neighbor methodology used for matching has shown a positive and significant impact of the carbon-tax with a reduction over the entire period ranging from 2.61% to 3.04% for the average effect of the treatment (ATE). i.e., the difference between the countries of treatment and the countries of control. The nearest neighbor methodology gave positive and significant results for the average effect of the treatment on the variable treated (ATET) over the entire period ranging from 2.29% to 2.55%. Table 3 enlists the estimations of ATE and ATET for the studied countries.

Table 3.

Results of estimation.

The outcomes from the estimation show that promoting of carbon-tax policies can significantly motivate the mitigation of CO2 emissions in the European Union. In particular, our empirical conclusions that policies relating to the carbon-tax have a positive impact on reducing CO2 are consistent with those obtained by Lin and Li [44] for the case of Denmark, Sweden, and the Netherlands. More recently, Borozan [25] and He et al. [19] also reported similar conclusions for the case of Europoen and G7 countries.

5. Discussion of Findings

Our analysis allowed us to determine the effectiveness of the carbon-tax; however, for this policy to be more effective, certain measures must be taken. The tax achieves its objective if and only if three conditions are met. All the polluters are effectively cost minimizers, but this condition is in particular not met in the case where the polluting agents are public enterprises, electricity production enterprises for example or local communities; all are well informed about their marginal cost abatement cost curves and there is no possibility of polluting emissions not taxed but for this condition to be respected, as in the case of standards, it is necessary to effectively control the volume of emissions [37,38,44,45,46]. However, it is important to examine certain cases which make the practice of taxation difficult. Defense activities and transferable externalities: one of the possibilities to defend oneself from the effects of an externality consists in transferring it (on the condition that it is rival) to other agents, which induces new inefficiencies [38,46,47,48].

Overall, the empirical results allow us to draw few arguments and implications. The empirical results argue that energy consumption, income, and population might be the main culprits for the rising level of pollution. The European-developed economies have witnessed high income growth, population growth, and energy intensity, which is mainly due to the rapid industrialization and economic activities in these economies. Notably, each of these require different policies and monitoring to control the pollutant emissions from the atmosphere. Notably, the rising level of population and income induce to use more resources in terms of natural resources, coal, oil, and other fossil fuels, while the abundant consumption of fossil fuels leads toward the pollution and environmental externalities [49,50,51]. At the same time, renewable energy consumption can be a useful tool to reduce the greenhouse gas emissions. Similarly, the control of urban income and relevant population control policies can also restrict energy consumption and climate change issues [50].

It is worthwhile to mention here that our study joins the conclusions of Borozan [15], Hashmi and Alam [10], and Shahzad [2]. The empirical findings allow us to draw few implications. Firstly, the government of developed economies should take necessary actions and regulations such as replacing the fossil fuels with renewable energy sources in overall energy mix and manufacturing treating. This is due to the reason that several European countries still dominate in the consumption of fossil fuels and non-renewables. While an objective to achieve the mentioned sustainable development goals, cleaner production and sustainability the energy transformation policies are very much required and in need of this era. To this end, the investments on renewables and cleaner energy sources should be promoted, so that the path towards the sustainable development can be achieved. Secondly, the government of European economies, especially the countries, e.g., Finland, Denmark, Slovenia, Sweden, France, and the United Kingdom must redesign the carbon-tax and environmental tax policies with more effective and required pressure to monitor and control the energy use and carbon emissions. In doing so, the developed countries in the European region can enforce regulations to install carbon treatment plants, greenhouse gas treatment plants, and afforestation policies. Similarly, the industrial firms should replace their polluting technologies with environmentally friendly machines. Such policies can restrict and reduce the energy demand; consequently, it can mitigate the greenhouse gas emissions from the atmosphere [38,44,45,46].

The carbon tax can modify the competitiveness of companies exposed to competition from countries that do not have one or apply lower rates. It reduces the competitiveness of companies emitting a lot of CO2. But conversely, if the tax proceeds are redistributed, the competitiveness of those emitting little CO2 can be improved.

Some countries have chosen not to apply the tax to relocatable activities or to apply it at reduced rates. Customs measures, such as “border adjustment taxes,” can also be put in place to protect domestic activities. However, international negotiations may be necessary as this area is highly regulated, notably by the World Trade Organization. In order not to harm the competitiveness of national industrial sectors, countries adopting the carbon tax have exempted energy-intensive or manufacturing industries from taxes. The main tax exemption policies in these countries are as follows:

Denmark has imposed a carbon tax on households and businesses. To ensure international competitiveness, all companies were reimbursed at 50% of the standard rate. Additional reimbursements have been granted depending on the energy intensity of each company [52]. Sweden reduced the tax burden on manufacturing industries in 1993. For some energy intensive industries, such as the iron and steel industry, the carbon tax burden is reduced to 1.7% of the value of production. This limit was then reduced to 1.2%. Finland, unlike other Scandinavian countries which distinguishes tax rates for private users from those for industrial users, does not allow industry tax exemptions or relief [6].

The present study argues that the implementation of relevant policies will be helpful to achieve the economic goals and sustainable development goals of European countries. In this case, the policy adopted must combine tax and compensation, because the existence of a possibility of transfer implies the creation of social gain or loss: a tax must be imposed on a victim who transfers externality but compensation must be paid to a victim who chooses to keep the externality when he has the possibility of transferring it because this creates a benefit for others; finally, the last receiver of the nuisance should not receive compensation if he did not have, in any case, possibilities of transferring it [8].

The problem of diffuse pollution is that another type of difficulty is introduced by the treatment of diffuse pollution, that is to say pollution caused by many sources of pollution, difficult or very expensive to identify or control, which pose to be both a problem of measuring emissions and above all a problem of moral hazard, when the consequences of the behavior of polluters on the overall level of pollution cannot be individualized. The ambient tax mechanisms proposed by Lin and Li [11], Wang and Wei [17], and Shahzad et al. 2020 [28], based on the incentive theory, consist of a combination of penalties and gratuities: each polluter pays a tax or receives a subsidy according to the overall performance. That is to say the deviation from a given level of ambient concentration of pollutants, and must pay, in the event of excessive overall pollution, a fixed penalty equal to the totality of the damage created by the excess [53]. This procedure makes it possible to achieve the environmental objective aimed at by combating stowaways, because it makes each polluter individually responsible for the total pollution and not only for his own. However, it has the disadvantage of being able to operate only if polluters actually feel that their behavior has consequences for the overall level of emissions [54,55,56]. Carbon pricing policies have an impact on the competitiveness of the European manufacturing sector, which recorded a respective decrease in production and total employment of 5% and 26% between 2001 and 2016. At the industry level, jobs destroyed in the affected companies are compensated by recruitments in other companies in the same industry during the same year [56,57,58].

On average, large energy-intensive companies reduce their carbon emissions more and redeploy more workers than energy-efficient small companies. The carbon-tax has reduced carbon emissions on average by around 5%. The net effect on employment is much weaker and even slightly positive at + 0.8% [58]. Several sectors are experiencing strong reductions in their carbon emissions, with little redeployment of employees. On the contrary, the automotive and plastics sectors are experiencing larger employee redeployments and smaller reductions in their carbon emissions. Other industries, such as metal products, combine a high reallocation of jobs with a huge reduction in emissions due to their large size.

If the carbon tax allows the European manufacturing sector to respect its carbon budget and does not negatively affect total employment, it nevertheless generates significant redeployments of employees in several branches of activity. Because these redeployments have redistributive impacts and generate costs for workers who are forced to change jobs, these results highlight the need to implement complementary labor market policies that minimize costs for concerned workers and facilitate adjustments in terms of employment between companies. In addition, as these transition costs are generally highly localized in regions specialized in energy-intensive industrial activities, they can also result in potentially significant regional effects and therefore in a high political cost [58].

6. Conclusions and Practical Implications

In order to elaborate the real influence of the carbon-tax in the mitigating of CO2 emissions rate, the authors try to estimate its effects in the countries of the European Union which have adopted this policy by using the method of more nearest neighbor matching. The paper focuses on the real mitigation properties during the carbon-tax implementation period and tries to give additional evidence to decision makers by evaluating the results. This study makes a comparative analysis for carbon-tax implementation and non-implementation European economies. The treatment group (tax implementation countries) includes Finland, Latvia, Denmark, Slovenia, Sweden, Ireland, France, and the United Kingdom, while the non-implementation groups consist of other European economies.

The mitigation influence of the carbon-tax changes from one country to another. On average, the coefficients for the countries adopting the carbon-tax are positive, but none of them exceeds the criterion of importance, showing the limited effects of the carbon-tax in these countries. The different influences of the carbon-tax in diverse states are essentially due to the different carbon-tax rates, the scope of the tax exemption, and the different use of carbon-tax revenues. The environmental externality requires a uniform tax proportion for many sectors which also explains why the carbon-tax in some countries (for example, Finland) works better than other countries, even if the tax rates nominal are generally lower.

Faced with the serious problem of climate change, the choice to reduce CO2 emissions and seek low-carbon development has become inevitable. It is suggested that adjusting the industrial structure, increasing investment in research and development, and rising energy prices are reasonable choices for reducing CO2 emissions. For states that involve collecting a carbon-tax, the execution of a flat-rate tax can effectively reduce emissions of CO2. However, when executing differential tax rates to avoid a loss of industrial competitiveness, it is required to embed the income from carbon-tax revenues on environmental measures or to increase carbon-tax rates in order to mitigate the effects of the taxation. The results of this study are in line with the sustainable development goals, cleaner production and achieving energy efficiency objectives.

The idea that revenues from an environmental tax could be used to stimulate economic activity or economic efficiency has been central to the “double dividend” literature in environmental economics. The name comes from the idea that imposing an environmental tax could produce two “dividends”: first, a reduction in polluting emissions, and second, an increase in GDP and economic efficiency through the use of environmental tax revenues.

We consider three general categories of uses of carbon tax revenues that could potentially stimulate economic activity: reductions in other taxes (such as payroll taxes or corporate or personal income taxes), reductions in government budget deficit, or funding of valuable public spending.

As final remarks, it can be said that the tax regulations for environment and technological innovation in European economies can be targeted to achieve high income, industrial growth, and low greenhouse gas emissions. Overall, the environmental issues in the developed countries are caused by the growth in income, population, energy intensity, and lack of technological innovation and environmental policies. With the passage of time, the world needs transformation, reforms, and technological shifting for sustainable development, cleaner production, and low pollution. In view of the above discussion, the existing policies and reforms in Europe need to be restructured for reducing the adverse environmental externalities caused by growth trajectory and ensuring sustainable development.

The environmental and carbon tax regulations are widely used and adopted as the most effective means of reducing emissions among other climate protection policies, which has been applied in developed nations. However, the impact of tax regulations on social welfare and economic growth remains unknown and can be the subject of a future study. Furthermore, the current study mainly focuses on the carbon emissions. The role of carbon tax for per capita income, energy demand, balance of trade, and industrial manufacturing can be a subject in future studies.

Author Contributions

A.G., Introduction, estimates, concept building, data; W.X., writing implications, editing, and revision improvements; M.B.J., literature review, methods, analysis, supervision; U.S., literature review, discussion, conclusion, and implications. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding and the article publication charges were funded by Umer Shahzad and Wanjun Xia with the support of Anhui University of Finance and Economics.

Conflicts of Interest

The authors declare no conflict of interest.

Ethics Approval and Consent to Participate

Not applicable.

Availability of Data and Materials

The datasets used during the current study are available from the corresponding or first author on reasonable request.

References

- IPCC Climate Change 2013 The Physical Science Basis; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2013; Volume 43, ISBN 9789291691388.

- Shahzad, U. Environmental taxes, energy consumption, and environmental quality: Theoretical survey with policy implications. Environ. Sci. Pollut. Res. 2020, 27, 24848–24862. [Google Scholar] [CrossRef]

- Barker, T.; Baylis, S.; Madsen, P. A UK carbon/energy tax. The macroeconomics effects. Energy Policy 1993, 21, 296–308. [Google Scholar] [CrossRef]

- Baranzini, A.; Goldemberg, J.; Speck, S. A future for carbon taxes. Ecol. Econ. 2000, 32, 395–412. [Google Scholar] [CrossRef]

- Farooq, M.U.; Shahzad, U.; Sarwar, S.; Zaijun, L. The impact of carbon emission and forest activities on health outcomes: Empirical evidence from China. Environ. Sci. Pollut. Res. 2019, 26, 12894–12906. [Google Scholar] [CrossRef] [PubMed]

- Ekins, P.; Speck, S. Competitiveness and Exemptions from Environmental Taxes in Europe. Environ. Resour. Econ. 1999, 13, 369–396. [Google Scholar] [CrossRef]

- Morley, B. Empirical evidence on the effectiveness of environmental taxes. Appl. Econ. Lett. 2012, 19, 1817–1820. [Google Scholar] [CrossRef]

- Ulucak, R.; Kassouri, Y. An assessment of the environmental sustainability corridor: Investigating the non-linear effects of environmental taxation on CO2 emissions. Sustain. Dev. 2020, 1, 1–9. [Google Scholar] [CrossRef]

- Cottrell, J.; Schlegelmilch, K.; Runkel, M.; Mahler, A. Environmental Tax Reform in Developing, Emerging and Transition Economies; German Development Institute: Bonn, Germany, 2016; ISBN 9783960210177. [Google Scholar]

- Hashmi, R.; Alam, K. Dynamic relationship among environmental regulation, innovation, CO2 emissions, population, and economic growth in OECD countries: A panel investigation. J. Clean. Prod. 2019, 231, 1100–1109. [Google Scholar] [CrossRef]

- Wang, H.; Wei, W. Coordinating technological progress and environmental regulation in CO2 mitigation: The optimal levels for OECD countries & emerging economies. Energy Econ. 2019, 87, 104510. [Google Scholar] [CrossRef]

- He, P.; Sun, Y.; Shen, H.; Jian, J.; Yu, Z. Does environmental tax affect energy efficiency? An empirical study of energy efficiency in OECD countries based on DEA and Logit model. Sustainability 2019, 11, 3792. [Google Scholar] [CrossRef]

- Bashir, M.A.; Sheng, B.; Dogan, B.; Sarwar, S.; Shahzad, U. Export product diversification and energy efficiency: Empirical evidence from OECD countries. Struct. Chang. Econ. Dyn. 2020, 55, 232–243. [Google Scholar] [CrossRef]

- Vera, S.; Sauma, E. Does a carbon tax make sense in countries with still a high potential for energy efficiency? Comparison between the reducing-emissions effects of carbon tax and energy efficiency measures in the Chilean case. Energy 2015, 88, 478–488. [Google Scholar] [CrossRef]

- Borozan, D. Unveiling the heterogeneous effect of energy taxes and income on residential energy consumption. Energy Policy 2019, 129, 13–22. [Google Scholar] [CrossRef]

- Mardones, C.; Cabello, M. Effectiveness of local air pollution and GHG taxes: The case of Chilean industrial sources. Energy Econ. 2019, 83, 491–500. [Google Scholar] [CrossRef]

- Lin, B.; Li, X. The effect of carbon tax on per capita CO2 emissions. Energy Policy 2011, 39, 5137–5146. [Google Scholar] [CrossRef]

- Agostini, P.; Botteon, M.; Carraro, C. A carbon tax to reduce CO2 emissions in Europe. Energy Econ. 1992, 14, 279–290. [Google Scholar] [CrossRef]

- He, P.; Chen, L.; Zou, X.; Li, S.; Shen, H.; Jian, J. Energy taxes, carbon dioxide emissions, energy consumption and economic consequences: A comparative study of Nordic and G7 countries. Sustainability 2019, 11, 6100. [Google Scholar] [CrossRef]

- Bruvoll, A.; Larsen, B.M. Greenhouse gas emissions in Norway: Do carbon taxes work? Energy Policy 2004, 32, 493–505. [Google Scholar] [CrossRef]

- Zhang, Z.X.; Baranzini, A. What do we know about carbon taxes? An inquiry into their impacts on competitiveness and distribution of income. Energy Policy 2004, 32, 507–518. [Google Scholar] [CrossRef]

- Lee, C.F.; Lin, S.J.; Lewis, C. Analysis of the impacts of combining carbon taxation and emission trading on different industry sectors. Energy Policy 2008, 36, 722–729. [Google Scholar] [CrossRef]

- Callan, T.; Lyons, S.; Scott, S.; Tol, R.S.J.; Verde, S. The distributional implications of a carbon tax in Ireland. Energy Policy 2009, 37, 407–412. [Google Scholar] [CrossRef]

- Lu, C.; Tong, Q.; Liu, X. The impacts of carbon tax and complementary policies on Chinese economy. Energy Policy 2010, 38, 7278–7285. [Google Scholar] [CrossRef]

- Borozan, D. Efficiency of energy taxes and the validity of the residential electricity environmental Kuznets curve in the European Union. Sustainability 2018, 10, 2464. [Google Scholar] [CrossRef]

- Sen, S.; Vollebergh, H. The effectiveness of taxing the carbon content of energy consumption. J. Environ. Econ. Manag. 2018, 92, 74–99. [Google Scholar] [CrossRef]

- He, P.; Ning, J.; Yu, Z.; Xiong, H.; Shen, H.; Jin, H. Can environmental tax policy really help to reduce pollutant emissions? An empirical study of a panel ARDL model based on OECD countries and China. Sustainability 2019, 11, 4384. [Google Scholar] [CrossRef]

- Shahzad, U.; Ferraz, D.; Doğan, B.; Aparecida, D. Export Product Diversification and CO2 Emissions: Contextual evidences from Developing and Developed Economies. J. Clean. Prod. 2020, 276, 124146. [Google Scholar] [CrossRef]

- Rubin, D. B Estimating causal effects of treatment in randomized and nonrandomized studies. J. Educ. Psychol. 1974, 66, 688–701. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Matched Sampl. Causal Eff. 1983, 70, 170–184. [Google Scholar] [CrossRef]

- Abadie, A.; Imbens, G.W. Bias-corrected matching estimators for average treatment effects. J. Bus. Econ. Stat. 2011, 29, 1–11. [Google Scholar] [CrossRef]

- Cameron, A.C.; Trivedi, P.K. Microeconometrics: Methods and Applications; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar] [CrossRef]

- Greene, W.H. Econometric Analysis, 6th ed.; Prentice-Hall: Upper Saddle River, NJ, USA, 2011; ISBN 0130661899. [Google Scholar]

- Administration, E.I. Energy Data. Available online: https://www.eia.gov/opendata/ (accessed on 10 July 2020).

- World Bank World Development Indicators. Available online: http://databank.worldbank.org/data/reports.aspx?source=world-development-indicators# (accessed on 10 July 2020).

- Schubert, K. Pour la taxe carbone. La politique économique face à la menace climatique. HAL 2009, 1–90. [Google Scholar] [CrossRef]

- Shrestha, R.M.; Marpaung, C.O.P. Supply- and demand-side effects of carbon tax in the Indonesian power sector: An integrated resource planning analysis. Energy Policy 1999, 27, 185–194. [Google Scholar] [CrossRef]

- Rapanos, V.T.; Polemis, M.L. Energy demand and environmental taxes: The case of Greece. Energy Policy 2005, 33, 1781–1788. [Google Scholar] [CrossRef]

- Liang, Q.M.; Wei, Y.M. Distributional impacts of taxing carbon in China: Results from the CEEPA model. Appl. Energy 2012, 92, 545–551. [Google Scholar] [CrossRef]

- Dehejia, R.H.; Wahba, S. Propensity score-matching methods for nonexperimental causal studies. Rev. Econ. Stat. 2002, 84, 151–161. [Google Scholar] [CrossRef]

- Imbens, G. Nonparametric estimation of average treatment effects under exogeneity: A review. Rev. Econ. Stat. 2004, 86, 4–29. [Google Scholar] [CrossRef]

- Caliendo, M.; Bonn, I. Some practical guidance for the implementation of propensity score matching. J. Econ. Surv. 2008, 22, 31–72. [Google Scholar] [CrossRef]

- Lin, B.; Zhu, J. Energy and carbon intensity in China during the urbanization and industrialization process: A panel VAR approach. J. Clean. Prod. 2017, 168, 780–790. [Google Scholar] [CrossRef]

- Babiker, M.H.; Metcalf, G.E.; Reilly, J. Tax distortions and global climate policy. J. Environ. Econ. Manag. 2003, 46, 269–287. [Google Scholar] [CrossRef]

- Floros, N.; Vlachou, A. Energy demand and energy-related CO2 emissions in Greek manufacturing: Assessing the impact of a carbon tax. Energy Econ. 2005, 27, 387–413. [Google Scholar] [CrossRef]

- Giblin, S.; McNabola, A. Modelling the impacts of a carbon emission-differentiated vehicle tax system on CO2 emissions intensity from new vehicle purchases in Ireland. Energy Policy 2009, 37, 1404–1411. [Google Scholar] [CrossRef]

- Boyd, R.; Krutilla, K.; Viscusi, W.K. Energy taxation as a policy instrument to reduce CO2 emissions: A net benefit analysis. J. Environ. Econ. Manag. 1995, 29, 1–24. [Google Scholar] [CrossRef]

- Dasgupta, S.; Roy, J. Understanding technological progress and input price as drivers of energy demand in manufacturing industries in India. Energy Policy 2015, 83, 1–13. [Google Scholar] [CrossRef]

- Sarwar, S.; Shahzad, U.; Chang, D.; Tang, B. Economic and non-economic sector reforms in carbon mitigation: Empirical evidence from Chinese provinces. Struct. Chang. Econ. Dyn. 2019, 49, 146–154. [Google Scholar] [CrossRef]

- Sarwar, S. Role of urban income, industrial carbon treatment plants and forests to control the carbon emission in China. Environ. Sci. Pollut. Res. 2019, 26, 16652–16661. [Google Scholar] [CrossRef] [PubMed]

- Wier, M.; Birr-Pedersen, K.; Jacobsen, H.K.; Klok, J. Are CO2 taxes regressive? Evidence from the Danish experience. Ecol. Econ. 2005, 52, 239–251. [Google Scholar] [CrossRef]

- Shahzad, U.; Doğan, B.; Sinha, A.; Fareed, Z. Does Export product diversification help to reduce energy demand: Exploring the contextual evidences from the newly industrialized countries. Energy 2020, 214, 118881. [Google Scholar] [CrossRef]

- Chen, J.; Xu, C.; Cui, L.; Huang, S.; Song, M. Driving factors of CO2 emissions and inequality characteristics in China: A combined decomposition approach. Energy Econ. 2019, 78, 589–597. [Google Scholar] [CrossRef]

- Cui, L.; Sun, Y.; Song, M.; Zhu, L. Co-financing in the green climate fund: Lessons from the global environment facility. Clim. Policy 2020, 20, 95–108. [Google Scholar] [CrossRef]

- Cui, L.; Li, R.; Song, M.; Zhu, L. Can China achieve its 2030 energy development targets by fulfilling carbon intensity reduction commitments? Energy Econ. 2019, 83, 61–73. [Google Scholar] [CrossRef]

- Cui, L.; Song, M.; Zhu, L. Economic evaluation of the trilateral FTA among China, Japan, and South Korea with big data analytics. Comput. Ind. Eng. 2019, 128, 1040–1051. [Google Scholar] [CrossRef]

- Cui, L.; Sun, Y.; Melnikiene, R.; Song, M.; Mo, J. Exploring the impacts of Sino–US trade disruptions with a multi-regional CGE model. Econ. Res. Istraz. 2019, 32, 4015–4032. [Google Scholar] [CrossRef]

- Dussaux, D. Par Les effets conjugués des prix de l’énergie et de la taxe carbone sur la performance économique et environnementale des entreprises françaises du secteur manufacturier. OECD Publ. 2020, 5, 1–84. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).