MetroScan: A Quick Scan Appraisal Capability to Identify Value Adding Sustainable Transport Initiatives

,

,  , ,

, ,

Abstract

1. Introduction

2. Methodology

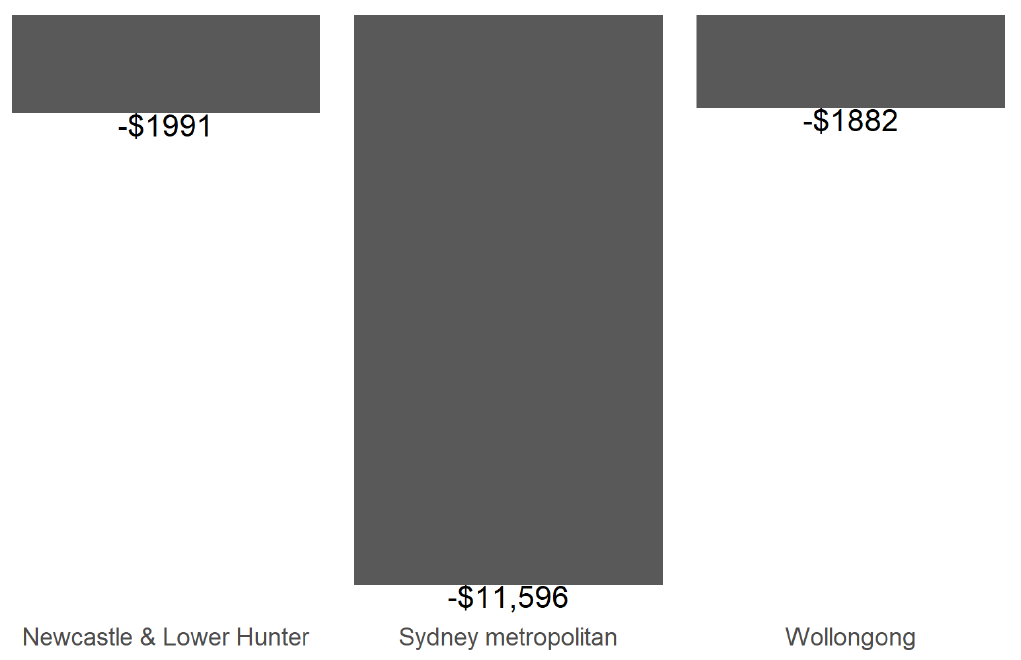

3. Case Study: A Reduction in Public Transport Fare Levels

3.1. The Cost–Benefit Perspective

3.2. Economic Impacts

3.3. Business Output (Sales)

3.4. Value Added or Gross Regional Product (GRP)

3.5. Jobs

4. Labour Income

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| General Outputs | |||

|---|---|---|---|

| Output | Description | Units | Comments |

| TCO2(kg) | Total annual carbon dioxide | Kilograms (kg) | Car (includes all passenger automobiles—sedan, wagons, utes, panel vans, 4WD), light commercial service vehicles, freight vehicles |

| NOx (kg) | Total annual nitrogen oxides | Kilograms (kg) | |

| CO (kg) | Total annual carbon monoxide | Kilograms (kg) | |

| NMVOC (kg) | Total annual volatile organic compounds | Kilograms (kg) | |

| N2O (kg) | Total annual nitrogen dioxide | Kilograms (kg) | |

| CH4 (kg) | Total annual chlorofluorocarbons | Kilograms (kg) | |

| TEUC.MC ($) | Total annual end-use money cost | Dollars ($) | All person trips, includes for car, LCV, and freight: op cost, regn charges, annualised vehicle cost, parking, toll, congestion charge; for PT = fares |

| TEUCPV.MC ($) | Total annual end-use money cost in present value terms | Dollars ($) | All person trips |

| TEUC.OC ($) | Total annual end-use operating costs | Dollars ($) | All person trips, car operating cost plus public transport fares |

| TEUCPV.OC ($) | Total annual end-use operating costs in present value terms | Dollars ($) | All person trips, car operating cost plus public transport fares |

| TEUC.TTC ($) | Total annual end-use travel time cost | Dollars ($) | All person trips; with travel time for ride-share for each person in car (converted to $). |

| TEUCPV.TTC ($) | Total end-use travel time cost in present value terms | Dollars ($) | All person trips; with travel time for ride-share for each person in car (converted to $). |

| TEUC.Time (min) | Total annual end-use travel time | Minutes (min) | All person trips; with travel time for ride-share for each person in car. |

| TEMUDTMC ($) | Total annual expected maximum utility from each model system for each of the model components defined—by the mode choice (CMC) links. | Dollars ($) | |

| TEMURLC ($) | Total annual expected maximum utility from each model system for each of the model components defined—by the linkage: residential location choice (RLC) links | Dollars ($) | |

| ACCDTMC(Utility units) | Accessibility indicators—by departure time and mode choice (DTMC) links. | Utility units | |

| ACCRLC(Utility units) | Accessibility indicators—by the linkage: residential location choice (RLC) links | Utility units | |

| TVKM(km) | Total annual passenger vehicle kilometres | Kilometres (km) | |

| TVKMTwAw(km) | Total annual passenger vehicle kilometres: to/from work and as part of work | Kilometres (km) | |

| TVKMOU(km) | Total annual passenger vehicle kilometres: other urban | Kilometres (km) | |

| TVKMNonU(km) | Total annual passenger vehicle kilometres: nonurban | Kilometres (km) | |

| AvOpCost(c/km) | Average operating cost of autos | C/km | |

| VehAnnCost($) | Annualised automobile capital cost | Dollars ($) | |

| VehOpCost($) | Total annual auto operating cost | Dollars ($) | |

| Tvehicles(number) | Total passenger vehicles | Number | Cars |

| Tenergy(litres) | Total energy consumed by passenger vehicles | Litres | Car (petrol and diesel) |

| TGovtVehReg($) | Total government revenue from auto ownership | Dollars ($) | Car |

| TGovtExcise($) | Total government revenue from fuel excise | Dollars ($) | Car (petrol and diesel) |

| TGovtCarbT($) | Total government revenue from carbon tax | Dollars ($) | Car (petrol and diesel) |

| TGovtSalesT($) | Total government revenue from sales tax (GST post 2000) | Dollars ($) | Car (petrol and diesel) |

| TTollRev($) | Total revenue from toll roads | Dollars ($) | Car |

| TPark($) | Total revenue from parking strategy | Dollars ($) | Tpark ($) Car |

| TRCong($) | Total revenue from congestion pricing | Dollars ($) | Car |

| TPT($) | Total revenue from public transport use | Dollars ($) | All PT (all modes, private and public). |

| TGVehPurCost($) | Total government revenue from vehicle purchase cost | Dollars ($) | Car |

| TVehMaxAgeValue($) | Total cost of vehicle maximum age buyout | Dollars ($) | Car |

| TGVehRebCost($) | Total government vehicle rebate cost | Dollars ($) | Car |

| THhld(number) | Total number of households | Number | |

| Tpop(number) | Total number of people resident in each city | Number | |

| TWrkrRes(number) | Total number of workers (p/t and f/t) in each residential location | Number | |

| TWrkrWork(number) | Total number of workers (p/t and f/t) in each workplace | Number | |

| TDA(proportion) | Modal share for car drive alone mode share | Proportion | All person trips |

| TRS(proportion) | Modal share for ride share | Proportion | All person trips |

| Ttrain(proportion) | Modal share for train travel | Proportion | All person trips |

| Tbus(proportion) | Modal share for bus travel | Proportion | All person trips |

| TLrl(proportion) | Modal share for light rail travel | Proportion | All person trips |

| Tbwy(proportion) | Modal share for busway use | Proportion | All person trips |

| TDA(PA)(number) | Total number of annual car drive alone trips | Number | All person trips |

| TRS(PA)(number) | Total number of annual car ride share trips | Number | All person trips |

| TTrain(PA)(number) | Total number of annual train trips | Number | All person trips |

| TBus(PA)(number) | Total number of annual bus trips | Number | All person trips |

| TLrl(PA)(number) | Total number of annual light rail trips | Number | All person trips |

| TBwy(PA)(number) | Total number of annual busway trips | Number | All person trips |

| Class01micro | Vehicle Class Proportion Class 1 | Proportion | Cars |

| Class02small | Vehicle Class Proportion Class 2 | Proportion | Cars |

| Class03med | Vehicle Class Proportion Class 3 | Proportion | Cars |

| Class04upmed1 | Vehicle Class Proportion Class 4 | Proportion | Cars |

| Class05upmed2 | Vehicle Class Proportion Class 5 | Proportion | Cars |

| Class06large | Vehicle Class Proportion Class 6 | Proportion | Cars |

| Class07lux | Vehicle Class Proportion Class 7 | Proportion | Cars |

| Class08lcom | Vehicle Class Proportion Class 8 | Proportion | Cars |

| Class094WD | Vehicle Class Proportion Class 9 | Proportion | Cars |

| Class10ltruck | Vehicle Class Proportion Class 10 | Proportion | Cars |

| Class11EVsm | Vehicle Class Proportion Class 11 | Proportion | Cars |

| Class12EVmed | Vehicle Class Proportion Class 12 | Proportion | Cars |

| Class13EVlge | Vehicle Class Proportion Class 13 | Proportion | Cars |

| Class14AFsm | Vehicle Class Proportion Class 14 | Proportion | Cars |

| Class15AFmed | Vehicle Class Proportion Class 15 | Proportion | Cars |

| Class16AFlge | Vehicle Class Proportion Class 16 | Proportion | Cars |

| RVKMPCar | Vehicle kilometres per vehicle | Vkm/Car | Cars |

| RVehiclePHhld | Vehicle per household | Veh/hld | Cars |

| RC02PVKM | CO2 per Vehicle kilometre | CO2/vkm | Cars |

| REnergyP100VKM | Energy per 100 Vehicle kilometres | Litres/100km | Cars |

| RVehPCapita | Vehicle per capita | Veh/capita | Cars |

| RGCPersT ($) | Generalised cost per person trip for car | $/car person trip | Cars, includes travel time (converted to $) and all money costs |

| RGCOPers ($) | Generalised cost per person trip for car | $/car person trip | Cars, includes travel time (converted to $) and only car op cost |

| RGCPubT ($) | Generalised cost per person trip for PT | $/PT person trip | All modes of public transport, fares plus travel time (converted to $) |

| RTEUGCPersT ($) | Total end use generalized cost per person trip | $/person trip | Sum of TEUC.OC plus TEUC.TC ($) |

| REMUDTMCPersT ($) | Departure time and mode choice consumer surplus per person trip | $/person trip | |

| REMURLCPersT ($) | Residential location (total) consumer surplus per person trip | $/person trip | |

| CmcAll (all trip matrices) | Number of all trips by mode | Number | |

| CmcCom (commuting to and from work trip matrices) | Number of commuting trips by mode | Number | |

| Crowding | Likelihood of getting a seat | Proportion | PT modes |

| Reliability | Likelihood of arriving on time/being late | Proportion | All modes |

| Reliability costs | $/person trip | All modes | |

| Value of personal time and reliability | $/person trip | All modes | |

| Safety cost | $ | All modes | |

| Additional consumer surplus | $ | All modes | |

| Additional Light Commercial Service Vehicle Outputs | |||

| Output | Description | Units | Comments |

| Number of trips | Number of trips by origin and destination | Number | By industry/occupation |

| Number of tours | Number of tours by origin and destination(s) | Number | By industry/occupation |

| Tour patterns | Types of tours by number of stops | Number | By industry/occupation |

| Trip time reliability | Reliability of trip times for service trips | Proportion | |

| Vehicle costs | $ | ||

| Labour costs | Labour costs associated with travel for service trips | $ | |

| Expected savings | Expected savings from improvements in travel time or reliability | $ | |

| Time lost due to congestion | Minutes lost due to congestion (relative to free flow) | Min | |

| Additional Freight Outputs | |||

| Output | Description | Units | Comments |

| Number of trips | Number of trips by origin and destination | Number | By vehicle and commodity class |

| Number of tours | Number of tours by origin and destination(s) | Number | By vehicle and commodity class |

| Total VKT | Total distance travelled | Km | By vehicle and commodity class |

| Tonnes | Total tonnes carried | Tonnes | By vehicle and commodity class |

| Tonne/km | Tonne/km | By vehicle and commodity class | |

| Tour patterns | Types of tours by number of stops | Number | By vehicle and commodity class |

| Trip time reliability | Reliability of trip times for freight trips | Proportion | By vehicle class |

| % Empty running | Proportion of VKT with empty vehicles | Proportion | By vehicle class |

| Vehicle costs | $ | ||

| Labour costs | Labour costs associated with travel | $ | |

| Parking costs | Parking costs including time | $ | |

| Expected savings | Expected savings from improvements in travel time or reliability | $ | |

| Freight value | Value of freight carried | $ | By vehicle and commodity class |

| Time lost due to congestion | Minutes lost due to congestion (relative to free-flow) | Min | By vehicle and commodity class |

| Economic impact and cost-benefit outputs | |||

| Output | Description | Units | Comments |

| Total employment (jobs) | Jobs | By industry or occupation | |

| Business productivity | $ | Total | |

| Social/environmental benefits | $ | Total | |

| Additional gross regional product | $ | Total | |

| GRP plus traveler non-$ benefits | $ | Total | |

| GRP plus total non-$ benefits | $ | Total | |

| Impact/Cost ratio | By impact measure | ||

| Total annual wages | $ | By industry or occupation | |

| Total annual value added | Gross value added (for metropolitan area) | $ | By industry or occupation |

| Total annual business output | Region equivalent to GDP (for metropolitan area) | $ | By industry or occupation |

| Value of imports | $ | ||

| Value of exports | $ | ||

| Value of internal flows | $ | ||

| Intermodal connectivity benefits | Benefits from access to multiple modes | $ | |

| Labour productivity benefits | $ | ||

| Business productivity benefits | Measures of agglomeration economies | $ | |

| Government revenue impacts | Changes in business sales, worker and business income, consumer spending, travel-related tolls and fees, and government revenues | $ | |

| Total benefits | Undiscounted nominal benefits | $ | |

| Total benefits (discounted) | Discounted real total benefits | $ | |

| Start-up costs | Project(s) start-up costs | $ | |

| Operating and maintenance costs | $ | ||

| Residual value | $ | ||

| Total costs | Undiscounted nominal costs | $ | |

| Total costs (discounted) | Discounted real total costs | $ | |

| Net benefits | $ | ||

| Cost benefit ratio | $ | ||

| Firm location outputs (Planned) | |||

| Output | Description | Units | Comments |

| Location of firms | Location of firms by industry/occupation | Firms | By industry, occupation |

| Firms by size | Number of firms by size | Firms | By industry and occupation |

| Location of business units | Location of business units (e.g., individual shop or office) | Business units | By industry and occupation |

| Location of jobs | Location of jobs | Jobs | By industry and occupation |

| Location of unfilled positions | Location of unfilled jobs (difference between jobs and employment) | Number | By industry and occupation |

| Productivity outputs | Productivity outputs by location | $ | By industry |

| Goods output | Goods outputs of firms by location | $ | By industry |

| Freight input (by value) | Materials/freight inputs for business use | $ | By industry |

| Freight input (by tonnes) | Materials/freight inputs for business use | Tonnes | By industry |

| Freight output (by value) | Freight outputs from business value-added | $ | By industry |

| Freight output (by tonnes) | Freight outputs from business value-added | Tonnes | By industry |

Appendix B. Benefit—Cost and Economic Impact Analyses

| Category | Source of Benefit and Cost | Explanation | Other Comments |

|---|---|---|---|

| Present Value of Benefit Stream | The dollar value of net welfare gain to transport system users (user benefits) and non-users (external benefits). It is possible that a transportation project may serve to reduce driver frustration about expected or unexpected delays, reduce air pollution levels, and enhance or otherwise affect the visual beauty of an area. All of these impacts are seen as having a value to society, which shows up in either willingness to pay studies (representing stated preferences) or in observed property value changes (reflecting revealed preferences). Such “societal” (or social) benefits can be counted in a benefit–cost analysis. However, not all types of benefits change the flow of income in the economy. | ||

| Travel Benefits | The traditionally used measure of user benefits, and are defined to include benefits accruing to drivers and passengers and vehicle costs as a result of improvements in travel times, travel expenses, and travel safety. Additional benefits, associated with switching modes of travel, origin–destination patterns, and “induced” generation of additional travel are also counted (through the concept of “consumer surplus”). | They also can include logistics benefits. These are the time and shipping cost savings to industries producing or consuming the commodities on board freight modes. Benefits arise because as shipping costs go down, businesses can increase productivity through inventory management, production scheduling, or distributional efficiencies. | |

| Value of Vehicle Operating Cost (VOC) | Fuel and oil consumption, tyre wear, maintenance, and depreciation, as well as fares and tolls (note—latter two costs are transfer payments if related to government) | Accounts for free flow ($/km) and congested conditions ($/km or $/hr depending on mode) | |

| Value of In-Vehicle Travel Time (IVTT) | Note—when we move from car to PT, we save the car time totally and incur a PT time, the difference reflecting the net INVT time benefit. | ||

| Value of Out-of-Vehicle Travel Time (OVTT) | This includes all ways of accessing or egressing a mode | Note that when we move from car to PT, we actually incur OVT losses | |

| Value of Improved Travel Time Reliability | This is linked to buffer time. TREDIS will compute the CHANGE in entered value of buffer time cost (difference between the project and base case) and then multiply that difference by the entered buffer time cost value. | ||

| Value of Safety Improvement | Based on average crash rates (per 100 million VKT) for all modes, and average costs incurred for each crash type ($/accident). | We allow for personal fatalities personal injuries and property damage. | |

| Environmental and Safety Benefits | |||

| Value of Emission Reduction for Mobile Source Pollutants | Accounts for free flow ($/km) and congested conditions ($/km or $/h depending on mode) | Local air pollution | |

| Value of Emission Reduction for Carbon Dioxide | Accounts for free flow ($/km) and congested conditions ($/km or $/h depending on mode) | Climate change, enhanced greenhouse gas emissions | |

| Wider Economic (Productivity) Benefits | Wider social benefits can also include “agglomeration” benefits, when a transport project facilitates greater accessibility and connectivity of productive factors in an economy. These “market access” effects are the result of knowledge spillovers, better matching of worker skills (and other inputs) to business needs, and sharing of commonly needed inputs to production. Increased worker productivity. Accessibility feeds agglomeration economies by means of input sharing, input matching, and knowledge spillovers. These mechanisms can create value in a region that is additional to user benefits. As such, productivity benefits are included in benefit/cost analysis. | ||

| Transfer Benefit Effects (net benefit adjustment) | Increase in public transport fares and car tolls collected from users (which are used to reduce net public investment cost) | ||

| Present Value of Cost Stream | |||

| Project Costs | |||

| Capital Investment Costs | |||

| Operation and Maintenance Costs | |||

| Cost Adjustments | |||

| Residual Value of Capital Costs | The residual value adjustment attempts to represent the value of the capital investment remaining after the analysis period. In CBA, the capital investment is spread over the built facility life. For example, if the project life is 40 years and analysis only goes for 20 years, then the nondepreciated value of the capital investment is credited as residual value. The user can choose the Useful Life in the inputs spreadsheet. Residual value applies only to capital investments that are associated with physical assets, i.e., construction categories “right-of-way”, “structures”, “terminals”, and “vehicles”. Residual value has the opposite sign of the project-minus-based capital investment costs. | In EIA, the capital investment is counted in the year in which it is actually spent. This residual credit is calculated based on linear depreciation of the construction cost, which is an excepted proxy for future benefits outside the project analysis period. | |

| Reduction in Effective Capital Cost Due to Value-Added Fees Collected by Government | This relates to fares and tolls (although we can decide how much of toll revenue accrues to Government or the private sector). The UK’s CBA guidance (WebTAG) is followed in Australia, which counts government toll collection as a reduction in the BCR denominator. (In the USA, practice counts it as an addition to the numerator offsetting user cost of tolls.) | You can see a matching value reflected under “Transfer Benefit Effects (net benefit adjustment)” “Change in Tax Revenues Collected By Government”. In the USA’s case, the two values would appear under the net benefit adjustment in the lines called “added fees.” | |

| Net Benefit (Benefits–Costs) | |||

| Transportation System Efficiency—Traveller Benefits Only | |||

| Traditional BCA—Traveller Benefits + Environmental Benefits | |||

| Full Societal BCA—All Benefit Categories | |||

| Benefit–Cost Ratio (Benefits/Costs) | |||

| Transportation System Efficiency—Traveller Benefits Only | |||

| Traditional BCA—Traveller Benefits + Environmental Benefits | |||

| Full Societal BCA—All Benefit Categories | |||

| Economic Impacts | Impacts on the flow of money in the economy, and are typically measured in terms of increased Jobs or Income. | It is possible that a transportation project will reduce business operating costs, which can increase profits (a component of value added). That may also improve competitiveness for locating a business in the affected area, resulting in further business sales and income growth there. Such impacts directly affect the flow of corporate income and lead directly to increases in worker income. As such, they represent an economic impact on the affected area. | |

| Productivity | The ratio of economic output/cost of inputs | The denominator is the total cost of all input factors, including labour, materials, utilities, transportation, and other services. Factors that affect the flow of income are productivity factors, whilst factors that have a social value (counted in CBA) do not directly affect income flows. Agglomeration and other productivity factors in the middle group are the core drivers of job and income growth in the economy. | |

| Market Access | Refers to the ability of transportation facilities and services to provide households and businesses with access to opportunities that they desire. Market access is often measured through the concept of “effective density”, which refers to the magnitude of surrounding market opportunities (e.g., workers to be utilised or customers to be served) from a specific location. An improvement in the performance of transportation facilities and services can enhance productivity in two ways: (1) By reducing time and/or expense costs incurred in the continuing operation of businesses. That effectively raises productivity by decreasing the denominator of the ratio. (2) By enlarging market access or connectivity, which grows the numerator while the denominator either remains constant or grows proportionally less than the numerator. This can occur as long as there are scale economies or other business operating efficiencies enabled by access to a larger market. | Transportation investments can potentially expand any of these forms of market access below: Businesses desire access to three basic kinds of markets: 1. Labour market: the workforce with required skills that a business can draw from to obtain its employees; 2. Input material market: the sources of specialised materials that a business can acquire (or specialised services that it can use) to produce its output; 3. Customer market: the buyers whose specific needs can be reasonably and competitively served by a business (this can include shoppers, tourists, or freight delivery recipients). For households, transportation can be viewed as providing worker access to employment and shopping opportunities that match to their skills and needs. | |

| Economic Geography (Competitiveness) | Labour and capital flows; export growth, import substitution; workforce and population migration. | Factors that cause shifts in the spatial pattern of economic growth. They are additional economic impacts that are a consequence of productivity changes. They count in EIA as they can affect the level of economic activity occurring in a defined study area, but in CBA they are considered spatial shifts which cancel out. | |

| Connectivity | This represents a form of “access” that is between two systems. | However, in practice it is useful to distinguish market access and connectivity. Whereas “market access” refers to a surrounding area or region comprising the market, connectivity commonly refers to characteristics of the link to terminals or interchanges. | |

| Output | The value of business production. For productivity analysis, it is measured as net value added. (For other analyses, it may be measured as gross business revenue.) | ||

| Value Added | A measure of business output (revenue from product sales) minus the cost of nonlabour inputs used to produce that product. | ||

| Gross Domestic Product | The amount of business value that is generated in a given nation, state, or region; this is almost the same as gross value added but it adds further adjustments for taxes paid (+) and subsidies received (-) by business units. | ||

| Gross Regional Product | GDP value for a state or region within a nation. | ||

References

- Hensher, D.A.; Wei, E.; Ho, L. Development of a Simplified and Practical Aggregate Spatial Freight Modal Demand Model System for Truck and Commodity Movements in Australia; Institute of Transport and Logistics Studies, The University of Sydney: Sydney, Australia, 2020. [Google Scholar]

- Hensher, D.A.; Ton, T. TRESIS: A transportation, land use and environmental strategy impact simulator for urban areas. Transportation 2002, 29, 439–457. [Google Scholar] [CrossRef]

- Hensher, D.A.; Stopher, P.R.; Bullock, P.; Ton, T. TRESIS (Transport and Environmental Strategy Impact Simulator): Application to a Case Study in NE Sydney. Transp. Res. Rec. 2004, 1898, 114–123. [Google Scholar] [CrossRef]

- Hensher, D.A.; Ho, C.; Ellison, R. Simultaneous location of firms and jobs in a transport and land use. J. Transp. Geogr. 2019, 75, 110–121. [Google Scholar]

- Hensher, D.A.; Ho, C.; Teye, C.; Liu, W.; Wei, E. Integrating business location choices into transport and land use planning tools. J. Transp. Econ. Policy 2020, 54, 1–31. [Google Scholar]

- Ho, C.; Hensher, D.A.; Ellison, R. Endogenous treatment of residential location choices in transport and land use models: Introducing the MetroScan framework. J. Transp. Geogr. 2017, 64, 120–131. [Google Scholar] [CrossRef]

- Ho, C.; Hensher, D.A.; Wang, S. Joint estimation of mode and time of day choice accounting for arrival time flexibility, travel time reliability and crowding on public transport. J. Transp. Geogr. 2020, 87, 102793. [Google Scholar]

- Ho, C.; Hensher, D.A. A workplace choice model accounting for spatial competition and agglomeration effects. J. Transp. Geogr. 2016, 51, 193–201. [Google Scholar] [CrossRef]

- Ellison, R.; Teye, C.; Hensher, D.A. Modelling Sydney’s light commercial service vehicles. Transp. Res. Part A 2017, 96, 79–89. [Google Scholar] [CrossRef]

- Ellison, R.; Hensher, D.A. The TRESIS approach to population synthesis and spatial micro simulation, contributed book chapter in Lovelace, R. In Spatial Microsimulation in R; Chapman & Hall/CRC The R Series; CRC Press: Boca Raton, FL, USA, 2016; Available online: https://www.crcpress.com/product/isbn/9781498711548 (accessed on 4 May 2020).

- Weisbrod, G. Models to predict the economic development impact of transportation projects: Historical experience and new applications. Ann. Reg. Sci. 2008, 42, 519–543. [Google Scholar] [CrossRef]

- Weisbrod, G.; Beckwith, J. Measuring economic development benefits for highway decision-making: The Wisconsin case. Transp. Res. Rec. 1991, 71, 1262. [Google Scholar]

- Weisbrod, G.; Simmonds, D. Defining economic impact and benefit metrics from multiple perspectives: Lessons to be learned from both sides of the Atlantic. Eur. Transp. Conf. Proc. 2011, 30, 2015. [Google Scholar]

- Weisbrod, G.; Lorenz, J. Getting up to speed with transportation economic tools. Plan. Mag. 2013, 79, 39–42. [Google Scholar]

- Beckmann, M.; McGuire, C.B.; Winsten, B.W. Studies in the Economics of Transportation; Yale University Press: New Haven, CT, USA, 1956. [Google Scholar]

- Bovy, P.; Jansen, G. Network aggregation effects upon equilibrium assignment outcomes: An empirical investigation. Transp. Sci. 1983, 17, 240–261. [Google Scholar] [CrossRef][Green Version]

- Donnelly, R.; Upton, W.; Knudson, B. Oregon’s transportation and land use model integration program. J. Transp. Land Use 2018, 11, 19–30. [Google Scholar] [CrossRef]

| Initiatives/Policies | Outputs |

|---|---|

| Spatial policies | Residential, employment location |

| Change in PT service frequency | Industry and occupation patterns |

| Introduction of new PT lines | Economic activity patterns |

| Expansion of roads, motorways | Mode and ToD travel patterns |

| Introduction of toll roads | Demographics and commuting |

| Change in parking policies | Freight shipment patterns |

| Change in residential densities | Environmental impacts |

| And many more | Tax revenue impacts |

| Nonspatial policies | Business outputs |

| Change in PT fare | Total jobs created |

| More flexible work practices | Total value added |

| Emission/congestion charges | Operating, maintenance costs |

| Introduction of greener vehicles | Net benefits |

| And many more | Cost-Benefit Ratio |

| Reduction/Savings in: | Car DA Business | Car RS Business | Car DA Personal | Car RS Personal | Car Totals |

|---|---|---|---|---|---|

| Gross Vehicle Trips | 1,492,736 | (599,599) | 79,949,592 | 8,274,158 | 89,116,887 |

| Gross VKT | 60,143,520 | (27,613,698) | 1,438,592,768 | 235,373,184 | 1,706,495,774 |

| Gross VHT | 1,287,220 | (685,509) | 32,766,562 | 4,804,496 | 38,172,769 |

| Gross Out of Vehicle Hours | 0 | 0 | 0 | 0 | 0 |

| Gross Buffer Time (hours) | 130,316 | (157,470) | 6,979,600 | 97,155 | 7,049,601 |

| Passenger Trips | 1,492,736 | (1,552,961) | 79,949,592 | 25,567,148 | 105,456,515 |

| Passenger Kilometres | 60,143,520 | (71,519,478) | 1,438,592,768 | 727,303,139 | 2,154,519,949 |

| Passenger Hours | 1,287,220 | (1,775,469) | 32,766,562 | 14,845,893 | 47,124,206 |

| Reduction/Savings in: | Bus Business | Train Business | Bus Personal | Train Personal | Transit Totals |

|---|---|---|---|---|---|

| Gross Vehicle Trips | 0 | 0 | 0 | 0 | 0 |

| Gross VKT | 0 | 0 | 0 | 0 | 0 |

| Gross VHT | 0 | 0 | 0 | 0 | 0 |

| Gross Out of Veh Hours | 19 | (1) | (11,803) | (16,850) | (28,635) |

| Gross Buffer Time (h) | 0 | 0 | 0 | 0 | 0 |

| Passenger Trips | 51,252 | (9337) | (45,694,004) | (66,208,241) | (111,860,330) |

| Passenger Kilometres | 1,870,589 | (73,597) | (689,842,433) | (1,842,711,278) | (2,530,756,719) |

| Passenger Hours | 54,777 | (2781) | (33,757,660) | (48,189,707) | (81,895,371) |

| Reduction/Savings in: | Car Totals | Transit Totals | Pass. Totals |

|---|---|---|---|

| Passenger Trips | 105,456,515 | (111,860,330) | (6,403,815) |

| Passenger Kilometres | 2,154,519,949 | (2,530,756,719) | (376,236,770) |

| Passenger Hours | 47,124,206 | (81,895,371) | (34,771,165) |

| Reduction/Savings in: | Truck Rigid Freight | Truck Articulated Freight | Truck Totals |

|---|---|---|---|

| Gross Vehicle Trips | (441,034) | (459,254) | (900,288) |

| Gross VKT | (60,961,856) | (93,152,704) | (154,114,560) |

| Gross VHT | (949,328) | (1,136,148) | (2,085,476) |

| Freight Tonne Trips | (2,593,283) | (10,769,518) | (13,362,801) |

| Freight Tonne Kilometres | (358,455,713) | (2,184,430,909) | (2,542,886,622) |

| Freight Tonne Hours | (5,582,049) | (26,642,671) | (32,224,720) |

| Reduction/Savings in: | Car DA Business | Car RS Business | Bus Business | Train Business | Car DA Personal | Car RS Personal | Bus Personal | Train Personal | Truck Rigid Freight | Truck Articulated Freight | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Passenger Cost (In Vehicle) | 73,989 | −102,054 | 3149 | −160 | 580,623 | 263,069 | −598,186 | −853,922 | 0 | 0 | −633,490 |

| Passenger Cost (Out of Vehicle) | 0 | 0 | 1 | 0 | 0 | 0 | −314 | −448 | 0 | 0 | −761 |

| Crew Cost | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | −32,132 | −37,805 | −69,937 |

| Freight Cost | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | −8317 | −35,701 | −44,018 |

| Reliability Cost | 7491 | −9,051 | 0 | 0 | 123,679 | 1722 | 0 | 0 | 0 | 0 | 123,839 |

| Fuel Cost w/Taxes | 8789 | −4167 | 0 | 1395 | 210,235 | 33,556 | 0 | 0 | −21,398 | −60,642 | 167,768 |

| Veh O&M Cost | 21,303 | −10,278 | 0 | 488 | 509,550 | 80,192 | 0 | 0 | −107,902 | −164,880 | 328,472 |

| Fee per Vehicle Trip | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Fee per Passenger Trip | 0 | 0 | 18,242 | 17 | 0 | 0 | −52,712 | −45,525 | 0 | 0 | −79,978 |

| Fee per Passenger Kilometer | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Fee per Vehicle Kilometer | −2116 | −267 | 0 | 0 | 4089 | 1046 | 0 | 0 | 0 | 0 | 2752 |

| Safety Cost | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Environmental Cost | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Induced Benefit | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 7% Discount Rate | 3% Discount Rate | |

|---|---|---|

| Present Value of Benefit Stream | −5319.91 | −9452.11 |

| Travel Benefits | −3696.50 | −6258.53 |

| Value of Consumer Surplus From Induced New Activity | 0 | 0 |

| Value of Improved Travel Time Reliability | 1674.07 | 2942.42 |

| Value of In-Vehicle Travel Time (IVTT) | −9720.74 | −17,026.87 |

| Value of Out-of-Vehicle Travel Time (OVTT) | −10.023 | −17.597 |

| Value of Safety Improvement | 0 | 0 |

| Value of Vehicle Operating Cost (VOC) | 4360.19 | 7843.52 |

| Environmental and Social Benefits | 0 | 0 |

| Logistics & Supply Chain Cost Savings | −945.294 | −1644.78 |

| Transfer Benefit Effects (net benefit adjustment) | −678.114 | −1548.80 |

| Revenue Collected by Government | −678.114 | −1548.80 |

| Present Value of Cost Stream | −678.114 | −1548.80 |

| Project Costs | 0 | 0 |

| Cost Adjustments | −678.114 | −1548.80 |

| Revenue Collected by Government | −678.114 | −1548.80 |

| Residual Value of Capital Spending | 0 | 0 |

| Net Benefit (Benefits—Costs) | −4641.80 | −7903.31 |

| Benefit Cost Ratio (Benefits/Costs) | 7.845 | 6.103 |

| Industry | Decrease | Industry | Increase |

|---|---|---|---|

| Automotive Repair & Maint. | −$383.6 | Ownership of Dwellings | $157.3 |

| Motor Vehicles & Parts; Equip. Mfg | −$372.6 | Accommodation | $27.7 |

| Prof., Sci, and Tech. Services | −$69.2 | Finance | $24.6 |

| Non-Res Property Operators & Real Estate | −$40.9 | Residential Care & Social Assist. | $23.7 |

| Wholesale Trade | −$33.7 | Health Care Services | $22.4 |

| ISP, Internet Pub., Websearch & Data | −$28.4 | Food & Beverage Services | $21.1 |

| Employment, Travel, and Other Admin. | −$24.0 | Primary & Secondary Education Services | $18.0 |

| Postal, Courier, & Delivery Service | −$19.7 | Personal Services | $8.7 |

| Rental and Hiring Services (ex. Real Estate) | −$18.0 | Higher Education Services | $7.8 |

| Aux. Finance & Insurance Services | −$17.2 | Other Services | $7.0 |

| Industry | Change in Output |

|---|---|

| Automotive Repair & Maint. | −$42.4 |

| Motor Vehicles & Parts; Equip. Mfg | −$40.8 |

| Prof., Sci and Tech. Services | −$9.4 |

| Other Agriculture | −$5.6 |

| Non-Res Property Operators & Real Estate | −$5.5 |

| Nonmetallic Mineral Mining | −$5.2 |

| Coal mining | −$4.7 |

| Cement Lime and Concrete Mfg | −$4.4 |

| Meat and Meat Product Mfg | −$4.3 |

| Employment, Travel, and Other Admin Services | −$4.2 |

| Industry | Change in Output |

|---|---|

| Automotive Repair & Maint. | −$41.1 |

| Motor Vehicles & Parts; Equip. Mfg | −$39.0 |

| Iron & Steel Mfg | −$20.2 |

| Prof., Sci, and Tech. Services | −$9.9 |

| Other Agriculture | −$8.8 |

| Nonmetallic Mineral Mining | −$5.5 |

| Wholesale Trade | −$5.0 |

| Non-Res Property Operators & Real Estate | −$4.5 |

| Construction Services | −$4.2 |

| Electricity Trans., Dist., and Market Operation | −$3.3 |

| Industry | Decrease | Increase | |

|---|---|---|---|

| Automotive Repair & Maint. | −1251 | Health Care Services | 143 |

| Motor Vehicles & Parts; Equip. Mfg | −699 | Residential Care and Social Assistance | 140 |

| Prof., Sci, and Tech. Services | −175 | Primary and Secondary Education | 136 |

| Retail Trade | −139 | Food and Beverage Services | 115 |

| Other Manufactured Products | −103 | Personal Services | 74 |

| Wholesale Trade | −68 | Other Services | 38 |

| Furniture Manufacturing | −60 | Accommodation | 32 |

| Employment, Travel & Other Admin. | −44 | Finance | 30 |

| Non-Res Property & Real Estate | −41 | Arts, Sports, Adult, and Other Education | 19 |

| Public Order & Safety | −37 | Higher Education Services | 19 |

| Industry | Change in Jobs |

|---|---|

| Automotive Repair & Maint. | −138 |

| Motor Vehicles & Parts; Equip. Mfg | −76 |

| Other Agriculture | −31 |

| Prof., Sci, and Tech. Services | −25 |

| Nonmetallic Mineral Mining | −24 |

| Other Manufactured Products | −20 |

| Food and Beverage Services | −16 |

| Retail Trade | −15 |

| Specialized Machinery and Equipment Mfg | −8 |

| Construction Services | −8 |

| Industry | Change in Jobs |

|---|---|

| Automotive Repair & Maint. | −134 |

| Motor Vehicles & Parts; Equip. Mfg | −73 |

| Other Agriculture | −55 |

| Nonmetallic Mineral Mining | −26 |

| Prof., Scientific, & Tech. Services | −25 |

| Iron and Steel Mfg | −19 |

| Retail Trade | −14 |

| Construction Services | −14 |

| Wholesale Trade | −10 |

| Specialized Machinery and Equipment Mfg | −7 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hensher, D.A.; Quoc Ho, C.; Liu, W.; Wei, E.; Ellison, R.; Schroeckenthaler, K.; Cutler, D.; Weisbrod, G. MetroScan: A Quick Scan Appraisal Capability to Identify Value Adding Sustainable Transport Initiatives. Sustainability 2020, 12, 7861. https://doi.org/10.3390/su12197861

Hensher DA, Quoc Ho C, Liu W, Wei E, Ellison R, Schroeckenthaler K, Cutler D, Weisbrod G. MetroScan: A Quick Scan Appraisal Capability to Identify Value Adding Sustainable Transport Initiatives. Sustainability. 2020; 12(19):7861. https://doi.org/10.3390/su12197861

Chicago/Turabian StyleHensher, David A., Chinh Quoc Ho, Wen Liu, Edward Wei, Richard Ellison, Kyle Schroeckenthaler, Derek Cutler, and Glen Weisbrod. 2020. "MetroScan: A Quick Scan Appraisal Capability to Identify Value Adding Sustainable Transport Initiatives" Sustainability 12, no. 19: 7861. https://doi.org/10.3390/su12197861

APA StyleHensher, D. A., Quoc Ho, C., Liu, W., Wei, E., Ellison, R., Schroeckenthaler, K., Cutler, D., & Weisbrod, G. (2020). MetroScan: A Quick Scan Appraisal Capability to Identify Value Adding Sustainable Transport Initiatives. Sustainability, 12(19), 7861. https://doi.org/10.3390/su12197861