Integrated Management Approach Towards Sustainability: An Egyptian Business Case Study

Abstract

:1. Introduction

2. Literature Review

2.1. Sustainability Accounting

2.2. Sustainability Management Control

2.3. Sustainability Reporting

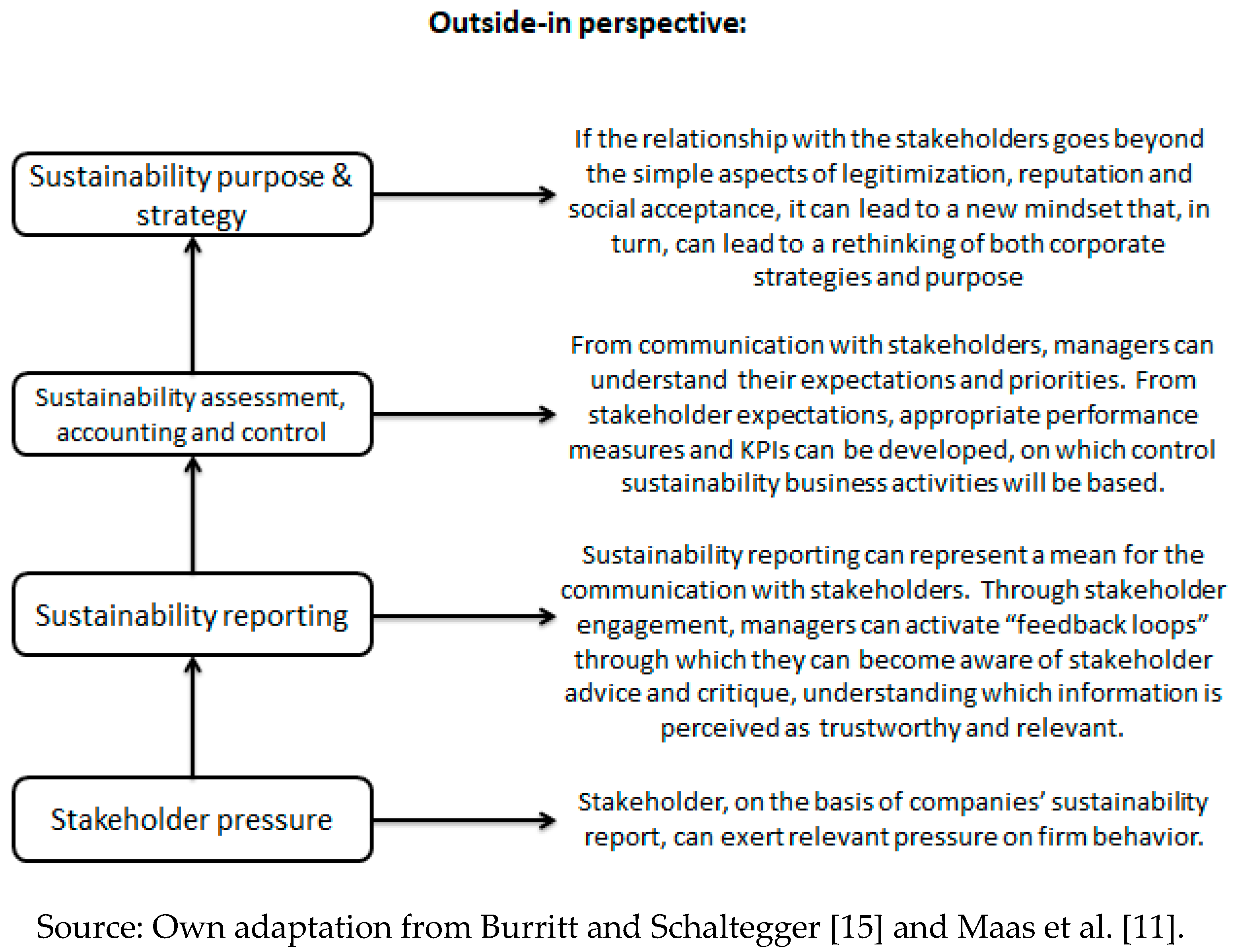

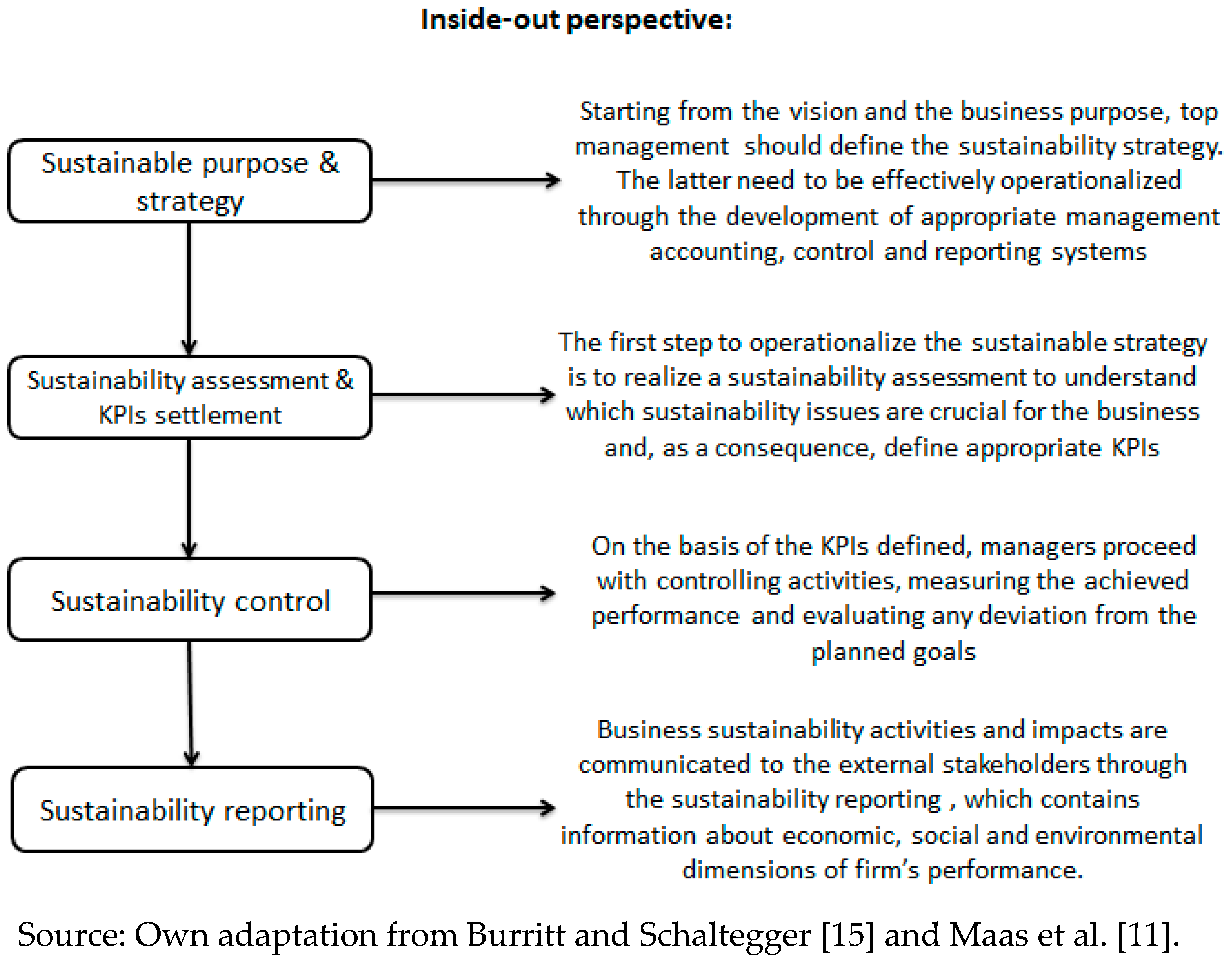

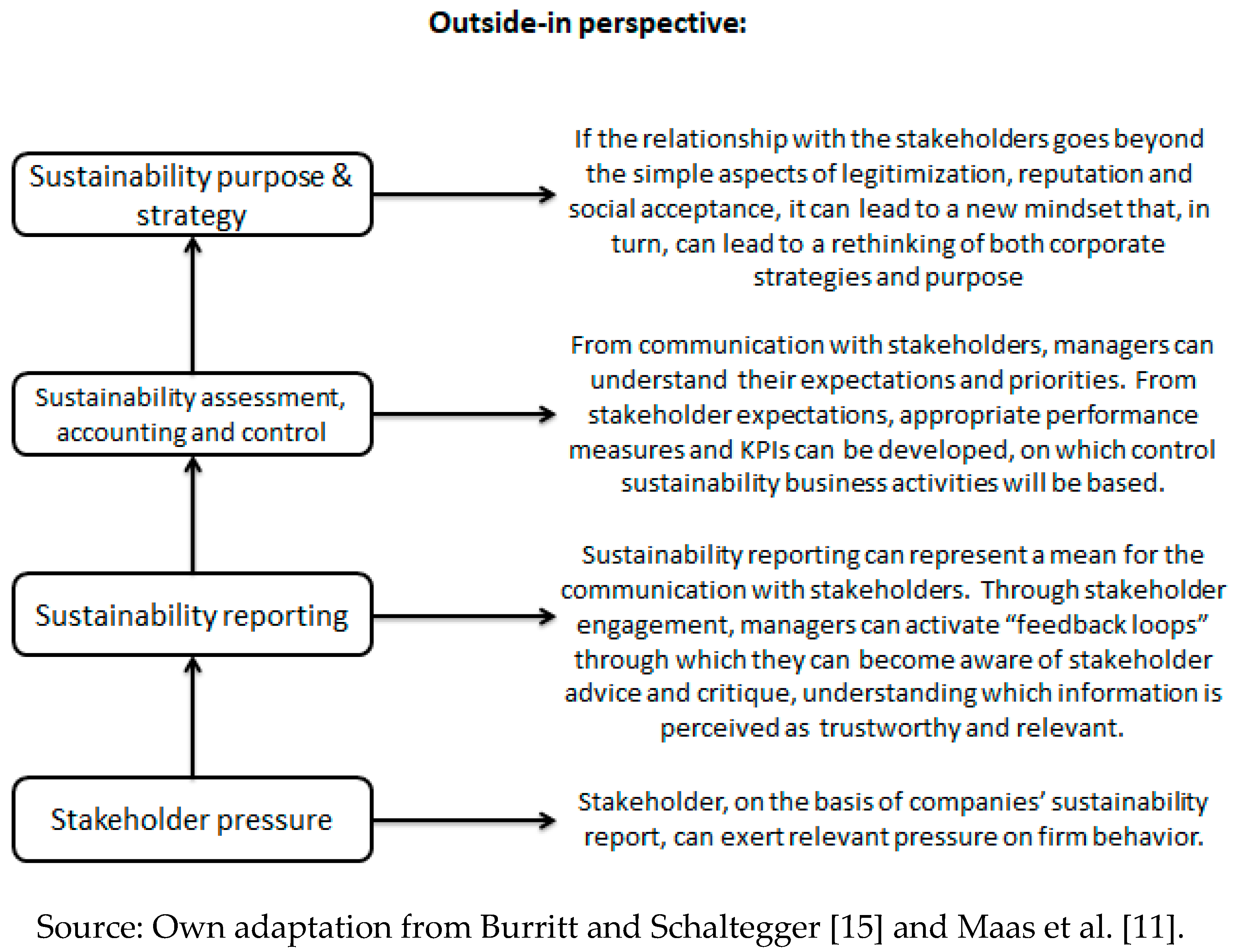

3. Theoretical Background: Moving Towards an Integrated Approach

- To provide empirical evidence to the theoretical framework proposed by Maas et al. [11].

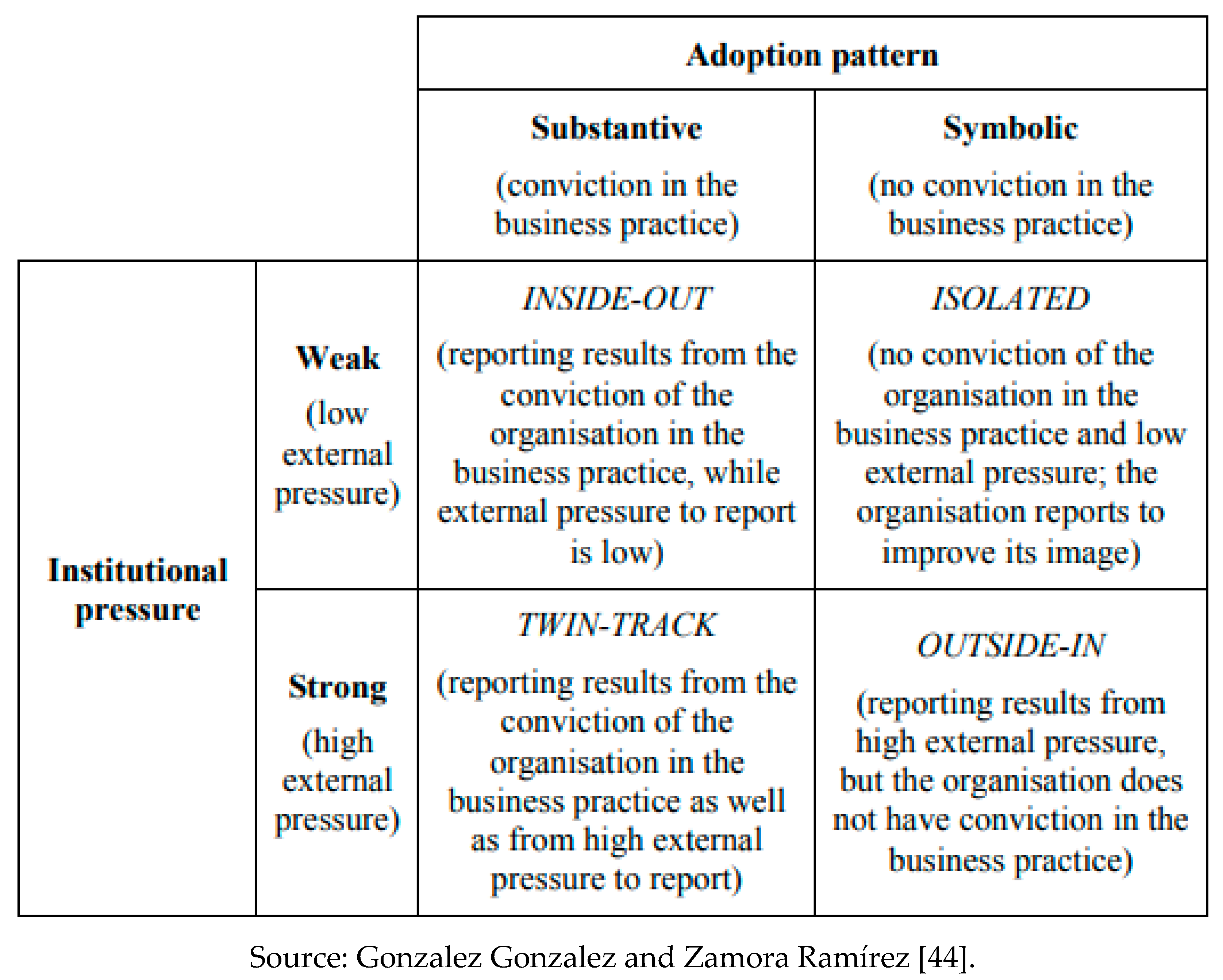

- To understand which sustainability path mainly occurs within this integration process (outside-in, inside-out or twin track).

- To shed light on the design and alignment modalities of all the managerial tools and practices involved in the corporate sustainability management.

4. Methodology

4.1. Selection of Case

4.2.Data Collection and Analysis

5. Case Study

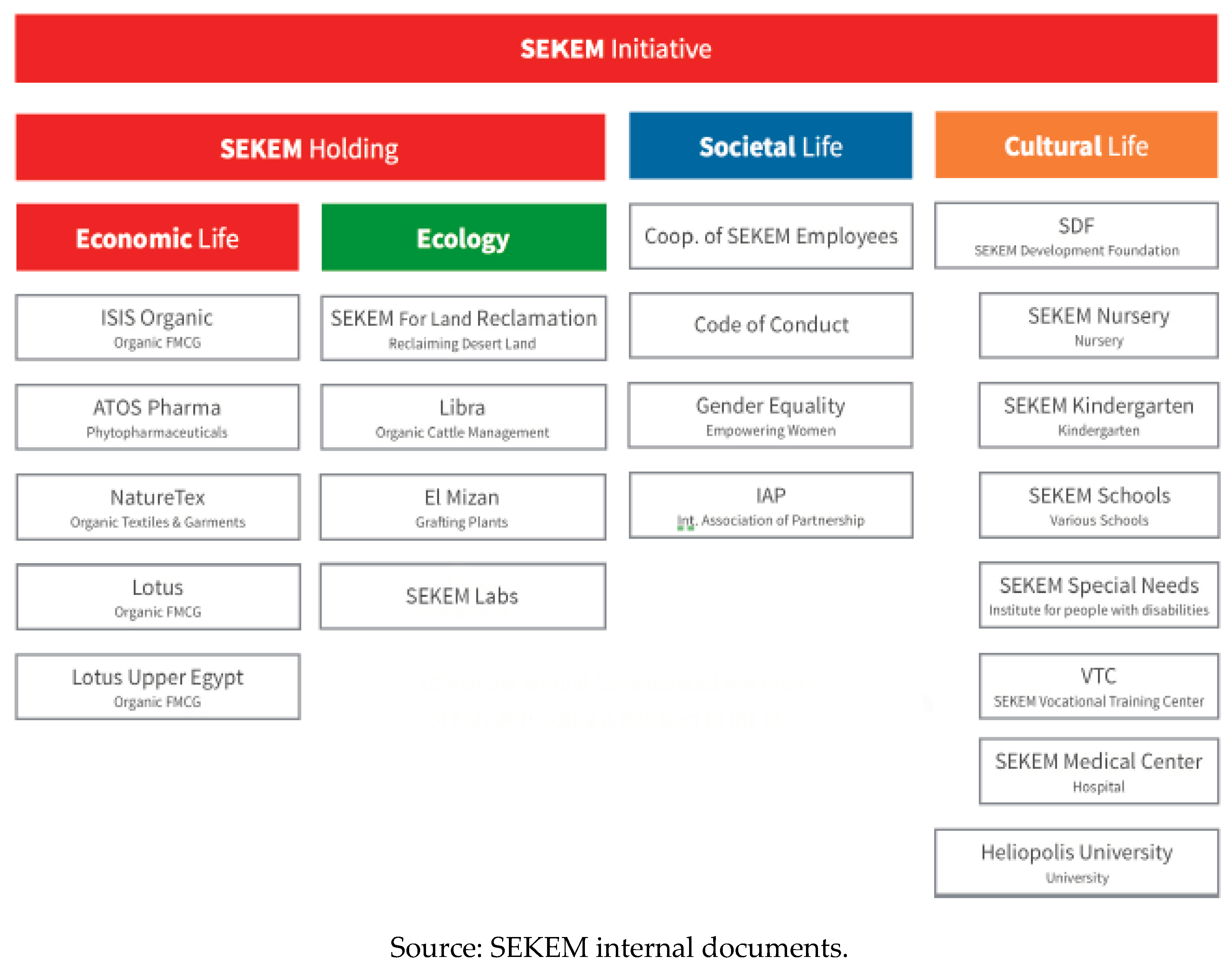

5.1. Business Background

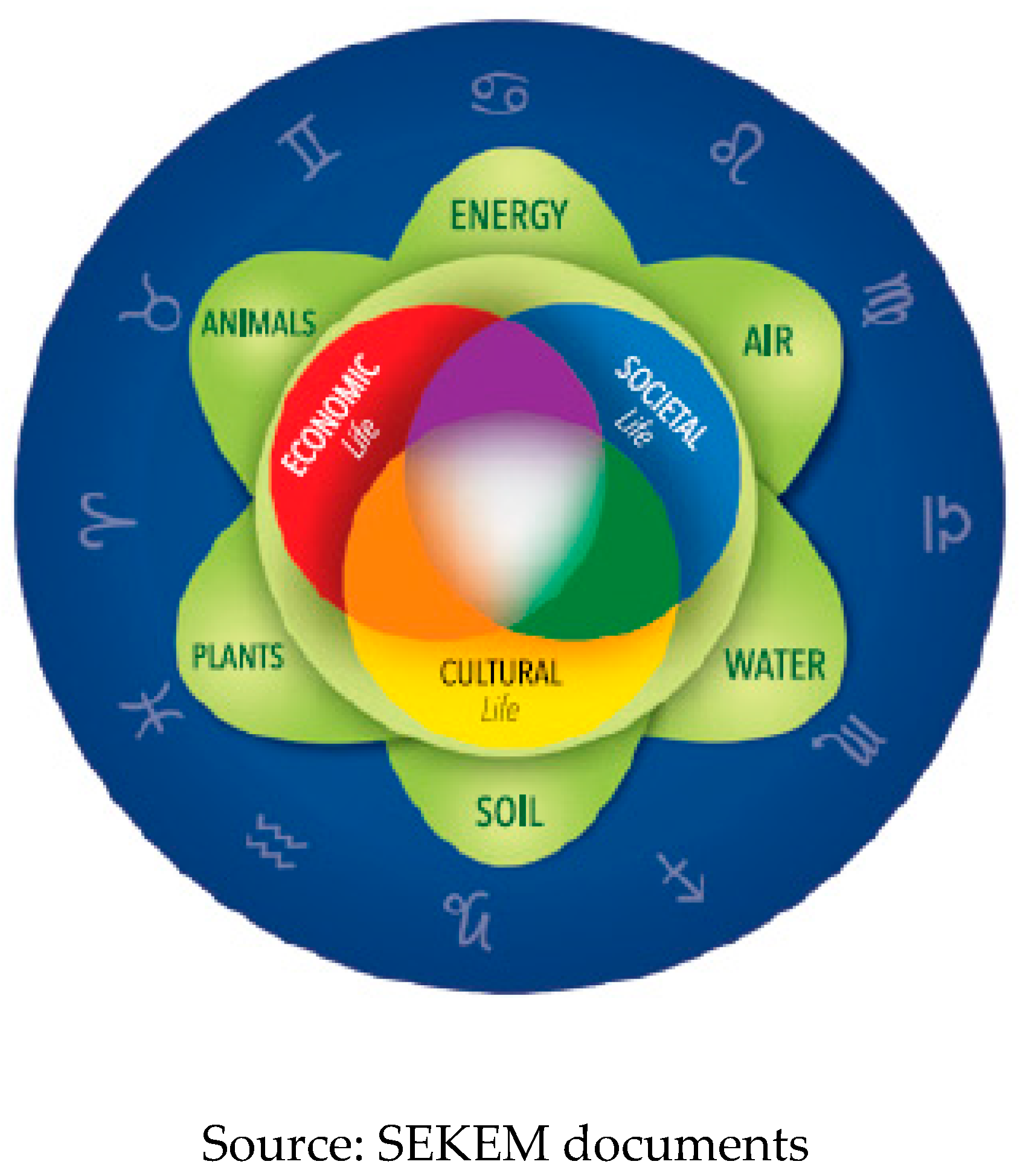

5.2. The SEKEM Purpose and Strategy

“The strong vision of the founder of sustainable development has become part of the company’s DNA and represents the philosophy without which SEKEM could not exist.”(SEKEM scholar affiliated)

“Sustainable development towards a future where every human being can unfold his individual potential; where mankind lives together in social forms reflecting human dignity; and where all economic activity is conducted in accordance with ecological and ethical principles.”

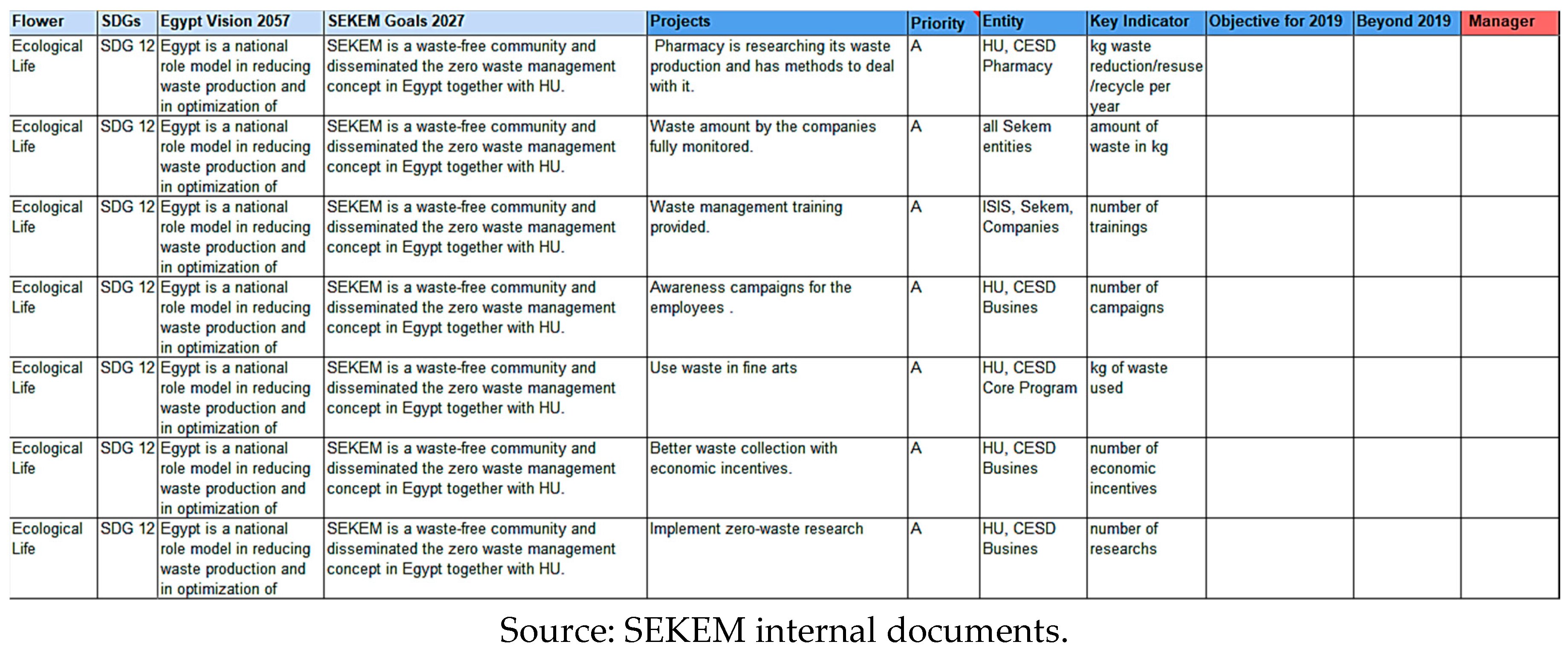

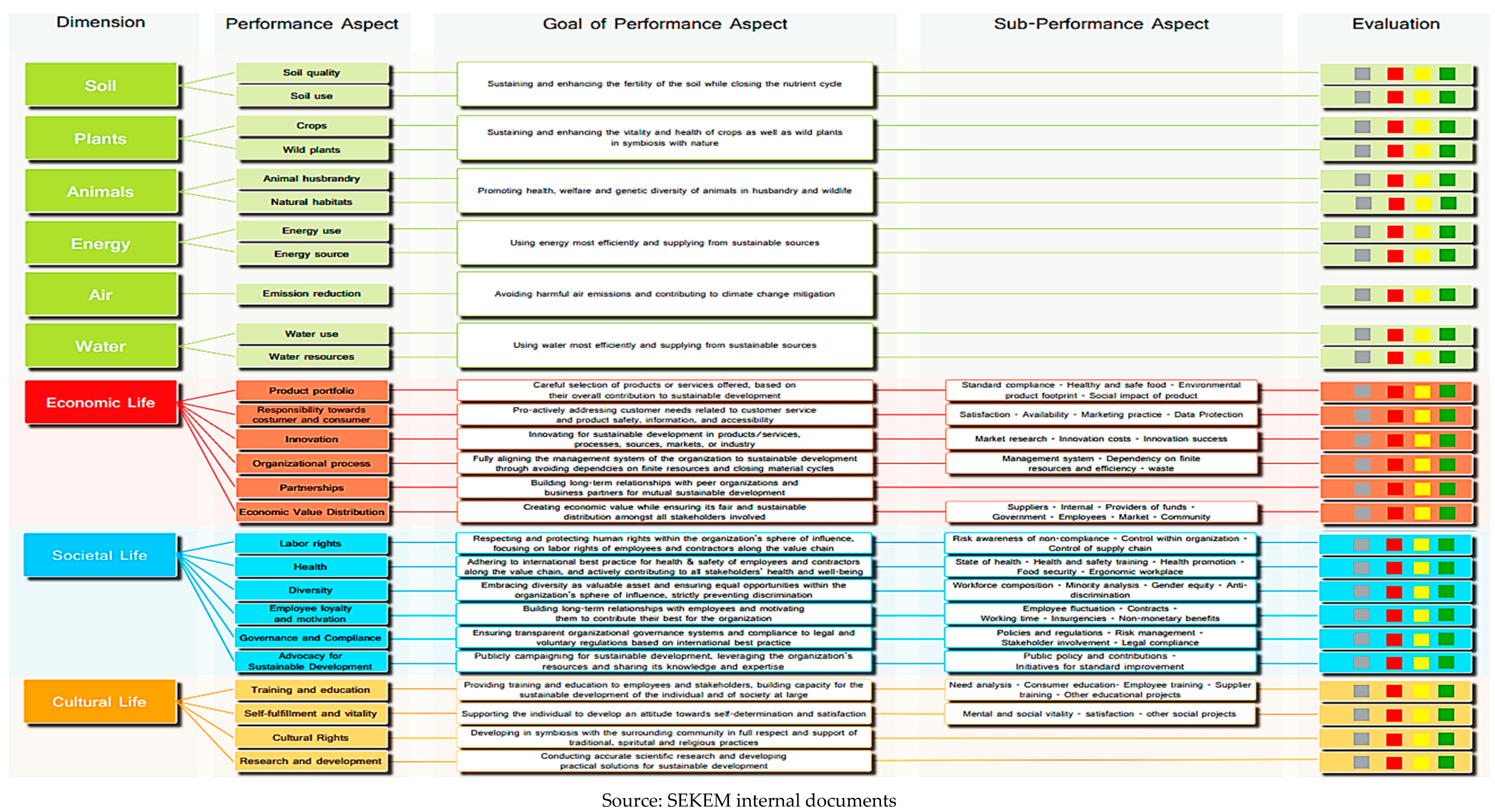

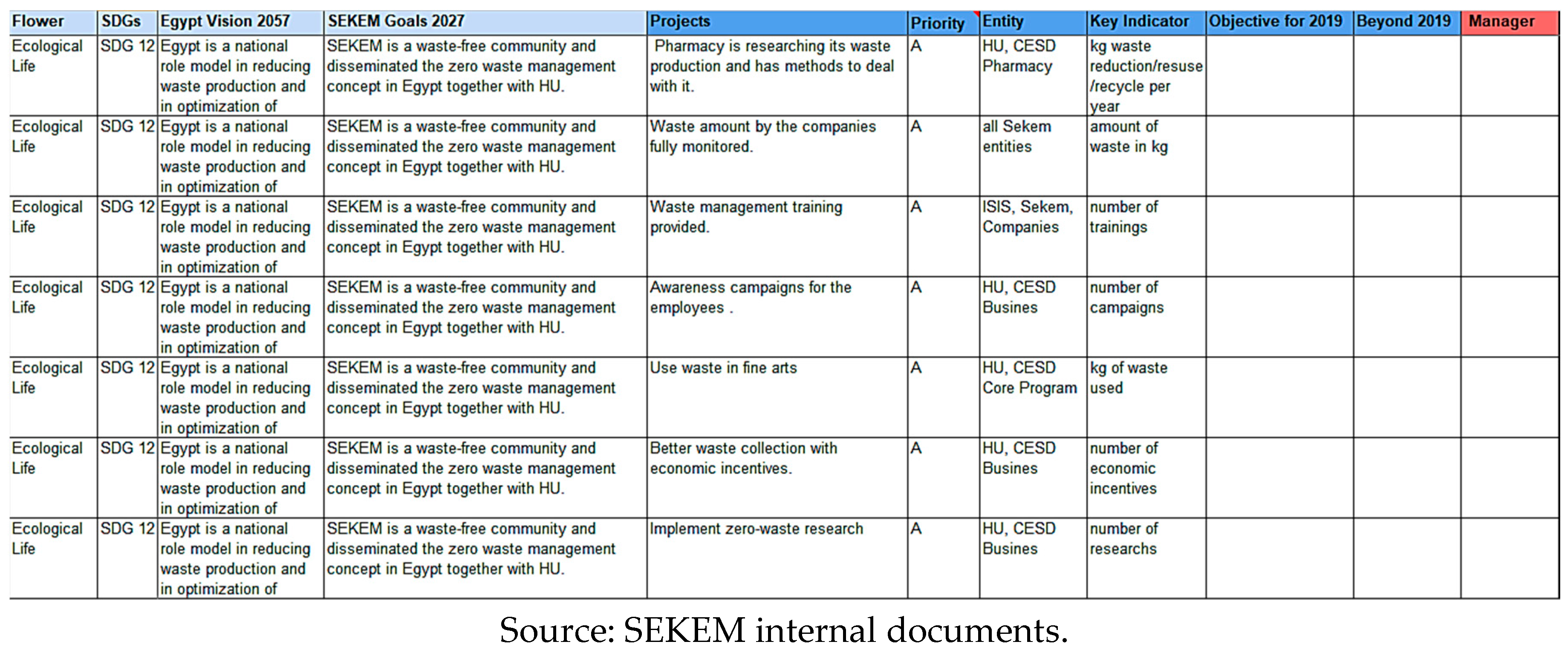

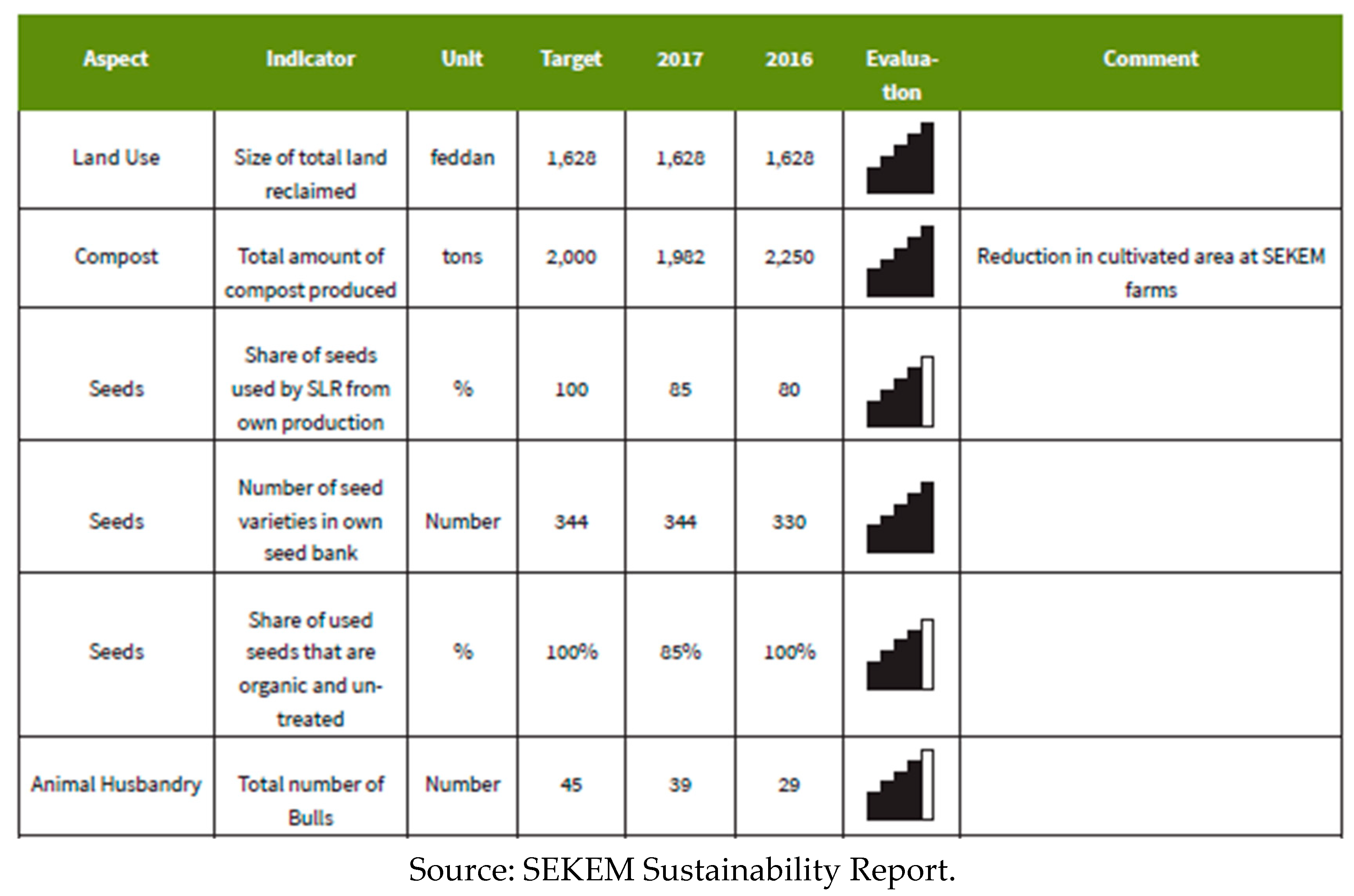

5.3. SEKEM Sustainability Accounting: From Strategy to KPI Settlement

5.4. SEKEM Sustainable Management Control: From Accounting to Balance Scorecard (BSC)

5.5. SEKEM Sustainability Reporting: From BSC to Sustainability Report

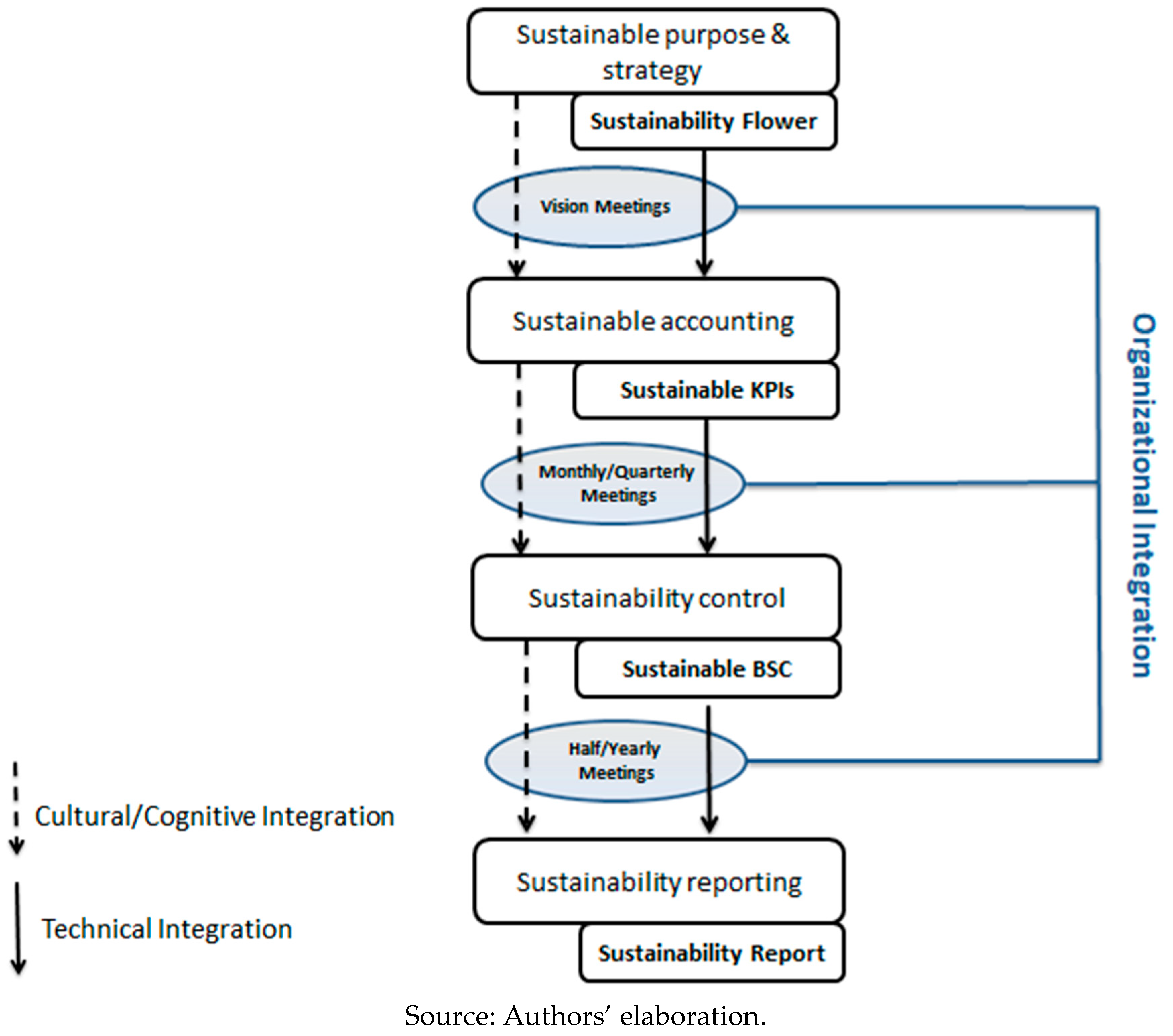

5.6. SEKEM Management Integration Path: Why and How

“we [referred to SD holding department] work with the management of each company level, as well as with the holding top management...We share the holistic reporting and management system information within management meetings, in order to discuss and improve measures and to relate them back to our long-term vision...This is our means for an effective integration and for building a shared vision...we continuously learn and continuously try to adapt the flower (and the related indicators and metrics) to the new aspects that come into play.”

“The spread of SEKEM purpose to the different employees and middle-management level, occur by regular vision meetings... Helmy Abouleish, the CEO and the cofounder of SEKEM, periodically meets different employees’ groups in order to discuss, on a philosophical but also practical level, what the SEKEM philosophy means... we [referred to SEKEM holding managers] support people in understanding what does SEKEM vision goals mean to them, what is their role, what do we expect from them, by couching, by training and by ongoing discussion in which the focus is not only on financial-economic aspects and data, but also on cultural, society, and ecological data and dimensions... Dialogue is the most important integration means!”

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Pillars | Issues | KPIs | Targets | 2017 | 2016 | SDGs |

|---|---|---|---|---|---|---|

| Economic | Economic Value Creation | Total Net Revenue (million EGP) | 470,934 | 476,449 | 380,932 | 1,8 |

| Economic Value Creation | Gross Profit (million EGP) | 235,488 | 237,857 | 199,356 | 1,8 | |

| Economic Value Creation | EBITDA (million EGP) | 130,082 | 131,962 | 100,495 | 1,8 | |

| Economic Value Creation | Net Profit before Tax (million EGP) | 6729 | 16,297 | 641 | 1,8 | |

| Economic Value Creation | Export Sales (%) | 0.37 | 0.34 | 0.30 | 1,8 | |

| Economic Value Creation | Local Sales (%) | 0.63 | 0.66 | 0.70 | 1,8 | |

| Economic Value Distribution | Ratio of highest to lowest annual full-time salary | 1:35 | 1:28 | 1:31 | 1,8 | |

| Economic Value Distribution | Total amount of Internal Investments (million EGP) | 10.0 | 9.70 | 10.0 | 1,8 | |

| Economic Value Distribution | Majority Shareholder Share (%) | 62.80 | 62.80 | 62.80 | 8 | |

| Economic Value Distribution | Share of Net Profit Invested into Community Development (%) | 0.10 | 0.10 | 0.10 | 8,11 | |

| Product Portfolio | Share of sales value of organic products (%) | 0.82 | 0.65 | 0.73 | 2,3,8,13 | |

| Product Portfolio | Share of sales value of products that have a Demeter certificate (%) | 0.60 | 0.61 | 0.53 | 2,3,8,13 | |

| Product Portfolio | Share of sales revenues of products with known product carbon footprint (%) | 1.00 | 0.84 | 0.80 | 8,12,13 | |

| Innovation | Share of total sales invested into company research and development (%) | 0.75 | 0.65 | 0.60 | 8,9 | |

| Innovation | Share of sales revenues from new products and services (%) | 0.20 | 0.11 | 0.20 | 8,9 | |

| Operations | Total weight of waste (tons) | 531 | 493 | 793 | 12,13 | |

| Operations | Total weight of organic waste (tons) | 427 | 404 | 493 | 12,13 | |

| Operations | Share of organic waste (%) | 0.80 | 0.82 | 0.69 | 12,13 | |

| Operations | Total weight of waste per sales (kg/EGP 1000) | 1.10 | 1.00 | 1.50 | 12,13 | |

| Operations | Share of organic waste recycled (%) | 1 | 1 | 1 | 12,13 | |

| Operations | Share of non-organic waste recycled (%) | 0.64 | 0.74 | 0.42 | 12,13 | |

| Operations | Share of recycled packaging material input (%) | 0.01 | 0.03 | 0.01 | 12,13 | |

| Environmental | Land Use | Size of total land reclaimed (feddan) | 1628 | 1628 | 1628 | 12,15 |

| Compost | Total amount of compost produced (tons) | 2000 | 1982 | 2250 | 12,13,15 | |

| Seeds | Share of seeds used by SLR from own production (%) | 100 | 85 | 80 | 12,15 | |

| Seeds | Number of seed varieties in own seed bank | 344 | 344 | 330 | 15 | |

| Seeds | Share of used seeds that are organic and untreated (%) | 1 | 0.85 | 1 | 12,13,15 | |

| Animal Husbandry | Share of animals that are kept according to Demeter standards (%) | 1.00 | 0.75 | 0.75 | 15 | |

| Energy | Total amount of gasoline consumption (lt) | 825,080 | 764,079 | 730,739 | 12,13 | |

| Energy | Total amount of gasoline consumption for equipment (lt) | 472,129 | 423,841 | 426,229 | 12,13 | |

| Energy | Total amount of gasoline consumption for power generation (lt) | 352,951 | 340,238 | 304,510 | 7,12,13 | |

| Energy | Total electricity consumption from grid (MWh) | 3822 | 2915 | 3506 | 7,12,13 | |

| Energy | Total electricity consumption from renewable sources (MWh) | 200 | 129 | 120 | 7,12,13 | |

| Energy | Total electricity consumption (grid, diesel and renewables) | 4750 | 3811 | 4436 | 7,12,13 | |

| Energy | Relative amount of electricity consumption per tousand EGP Sales (MWh) | 10.00 | 8 | 12 | 7,12,13 | |

| Emissions | Total amount of emissions (t Co2e) | 5448 | 4633 | 5008 | 13 | |

| Emissions | Relative amount of emissions per thousand EGP Sales(kg Co2e/1000 EGP) | 12.00 | 10 | 13 | 13 | |

| Water | Total amount of water usage for company and personal use (m3) | 47,438 | 46,143 | 89,717 | 6,12 | |

| Water | Total amount of water usage for agricultural use | 3,209,612 | 3,186,521 | 2,405,438 | 6,12 | |

| Water | Total amount of water usage for agricultural use from fossile water source (m3) | 1,081,063 | 1,115,586 | 1,304,339 | 6,12 | |

| Water | Share of water usage for agricultural use from fossile water source (%) | 0.34 | 0.35 | 0.54 | 6,12 | |

| Water | Relative amount of water usage for company and personal use (lt 1000/ EGP) | 101 | 97 | 236 | 6,12 | |

| Water | Share of waste water recycled and reused for tree irrigation (%) | 100 | 100 | 100 | 6,12 | |

| Water | Amount of significant spills in liters or other impact on water (lt) | 0.00 | 0 | 0 | 6,12 | |

| Social | Workforce Composition | Number of Senior Managers | 14 | 11 | 11 | 1,8,10 |

| Workforce Composition | Number of Middle Managers | 116 | 95 | 124 | 1,8,10 | |

| Workforce Composition | Number of Specialists | 485 | 402 | 475 | 1,8,10 | |

| Workforce Composition | Number of Labourers | 683 | 587 | 574 | 1,8,10 | |

| Workforce Composition | Number of Daily Workers | 180 | 168 | 160 | 1,8,10 | |

| Workforce Composition | Total Number of employees | 1508 | 1290 | 1344 | 1,8,10 | |

| Workforce Composition | Share of young employees (below the age of 36) (%) | 0.65 | 0.63 | 0.64 | 1,8,10 | |

| Workforce Diversity | Share of females in total work- force (excl. Daily Workers) (%) | 0.26 | 0.25 | 0.22 | 1,5,8,10 | |

| Workforce Diversity | Share of females in senior and middle manager positions (%) | 0.15 | 0.13 | 0.14 | 1,5,8,10 | |

| Workforce Diversity | Share of employees with disabilities (%) | 0.05 | 0.02 | 0.02 | 1,5,8,10 | |

| Loyalty and Motivation | Employee turnover (%) | 0.07 | 0.0748 | 0.072 | 1,8,10 | |

| Loyalty and Motivation | Total number of part time workers | 37.00 | 38 | 62 | 1,8,10 | |

| Loyalty and Motivation | Share of workforce that works part time (%) | 0.05 | 0.03 | 0.05 | 1,8,10 | |

| Loyalty and Motivation | Estimated share of non-monetary benefits of overall salaries (%) | 0.10 | 0.1 | 0.09 | 1,8,10 | |

| Advocacy for Sustainable Development | Number of events concerning SD where SEKEM representatives played an active role | n.a. | 36 | 26 | 1,8,10,17 | |

| Advocacy for Sustainable Development | Number of awards related to sustainable development received | 0.00 | 0 | 0 | 1,8,10,17 | |

| Advocacy for Sustainable Development | Number of articles in renowned publications on SEKEM and sustainable development per year | 250 | 307 | 288 | 4,11 | |

| Advocacy for Sustainable Development | Number of active membership in organizations relevant for sustainable development | 13 | 13 | 13 | 17 | |

| Health and Safety | Number of employee visits at the Medical Center | 6000 | 6855 | 5663 | 3,8,10 | |

| Health and Safety | Number of other visits at the Medical Center | n/a | 38,557 | 38,542 | 3,8,10 | |

| Health and Safety | Total Number of Medical Center visits | n/a | 45,412 | 44,205 | 3,8,10 | |

| Health and Safety | Share of employees with private health insurance (%) | 0.25 | 0.2519 | 0.26 | 3,8,10 | |

| Health and Safety | Total number of working days lost due to sick leave etc. | 2000 | 1720 | 2320 | 3,8,10 | |

| Health and Safety | Absentee rate (%) | 1.40 | 1.9 | 1.8 | 3,8,10 | |

| Health and Safety | Total number of work related injuries | 0.00 | 4 | 5 | 3,8,10 | |

| Health and Safety | Number of fatal injuries | 0.00 | 0 | 0 | 3,8,10 | |

| Cultural | Training and Capacity Building | Total Vocational training hours provided | 2.35 | 3.03 | 4.57 | 4,8,9 |

| Training and Capacity Building | Total Soft Skills training hours provided | 881 | 589 | 2.89 | 4,8,9 | |

| Training and Capacity Building | Total Quality Management Systems training hours provided | 8.25 | 8.25 | 1.36 | 4,8,9 | |

| Training and Capacity Building | Total Cultural/Arts training hours provided | 8.62 | 8.68 | 6.80 | 4,8,9,11 | |

| Training and Capacity Building | Total Equal Opportunity training hours provided | 1.00 | 1.28 | 80 | 4,5,8,9,11 | |

| Education | Number of students in SEKEM School | 300 | 297 | 303 | 1,4,5,8,11 | |

| Education | Number of children in SEKEM Kindergarten | 50 | 50 | 47 | 1,4,5,8,11 | |

| Education | Number of students in Vocational Training Center | n/a | 191 | 203 | 1,4,5,8,11 | |

| Education | Number of students in SEKEM Special Education | 35 | 37 | 34 | 1,4,5,8,11 | |

| Education | Number of babies in SEKEM Nursery | 38 | 27 | 38 | 1,4,5,8,11 | |

| Education | Number of students in Heliopolis University | 1.24 | 1.29 | 1.08 | 4,5,8,11 | |

| Education | Total number of SEKEM School graduates since 1998 | n/a | 254 | 229 | 4,5,8,11 | |

| Education | Total number of VTC graduates since 2000 | n/a | 975 | 898 | 4,5,8,11 | |

| Education | Students Graduated from SEKEMs Vocational Training Center | 120 | 77 | 64 | 1,4,5,8,11 | |

| Education | Value share of student scholarships at HU from total tuition fees (%) | 20 | 14 | 14 | 1,4,5,8,11 | |

| Education | Total number of Community School children since 1987 | n/a | 1.50 | 1.49 | 1,4,5,8,11 | |

| Education | Number of students in professional training for eurythmy | 10.0 | 8 | 8 | 1,4,5,8,11 | |

| Research and Development | Total number of funded research projects running in the reporting period | 20.0 | 20 | 19 | 1,4,5,8,11 |

References

- UN. Transforming our world: The Agenda 2030 for Sustainable Development. 2015. Available online: http://www.un.org/ga/search/view_doc.asp?symbol=A/RES/70/1&Lang=E (accessed on 15 June 2018).

- Porter, M.E.; Kramer, M.R. The link between competitive advantage and corporate social responsibility. Harvard Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Jasch, C.; Stasiškienė, Ž. From Environmental Management Accounting to Sustainability Management Accounting. Environ. Res. Eng. Manag. 2005, 34, 77–88. [Google Scholar]

- Adams, D. The power of corporate purpose. In The Reputable Firm: How Digitalization of Communication Is Revolutionizing Reputation Management; Aula, P., Heinonen, J., Eds.; Springer: Cham, Switzerland, 2015; ISBN 9783319220086. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984; ISBN 978-0-521-15174-0. [Google Scholar]

- Donaldson, T.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Schaltegger, S.; Wagner, M. Managing sustainability performance measurement and reporting in an integrated manner. Sustainability accounting as the link between the sustainability balanced scorecard and sustainability reporting. In Sustainability Accounting and Reporting; Schaltegger, S., Bennett, M., Burritt, R., Eds.; Springer: Dordrecht, The Netherlands, 2006; pp. 681–697. [Google Scholar]

- Falle, S.; Rauter, R.; Engert, S.; Baumgartner, R.J. Sustainability management with the sustainability balanced scorecard in SMEs: Findings from an Austrian case study. Sustainability 2016, 8, 545. [Google Scholar] [CrossRef]

- Gond, J.P.; Grubnic, S.; Herzig, C.; Moon, J. Configuring management control systems: Theorizing the integration of strategy and sustainability. Manag. Account Res. 2012, 23, 205–223. [Google Scholar] [CrossRef]

- Battaglia, M.; Passetti, E.; Bianchi, L.; Frey, M. Managing for integration: A longitudinal analysis of management control for sustainability. J. Clean. Prod. 2016, 136, 213–225. [Google Scholar] [CrossRef]

- Maas, K.; Schaltegger, S.; Crutzen, N. Integrating corporate sustainability assessment, management accounting, control, and reporting. J. Clean. Prod. 2016, 136, 237–248. [Google Scholar] [CrossRef]

- Adams, C.A.; Frost, G.R. Integrating sustainability reporting into management practices. Account. Forum 2008, 32, 288–302. [Google Scholar] [CrossRef]

- Riccaboni, A.; Leone, E.L. Implementing strategies through management control systems: The case of sustainability. Int. J. Prod. Perform. Manag. 2010, 59, 130–144. [Google Scholar] [CrossRef]

- Giovannoni, E.; Maraghini, M.P. The challenges of integrated performance measurement systems: Integrating mechanisms for integrated measures. Account. Audit. Accoun. 2013, 26, 978–1008. [Google Scholar] [CrossRef]

- Burritt, R.L.; Schaltegger, S. Sustainability accounting and reporting: Fad or trend? Account. Audit. Accoun. 2010, 23, 829–846. [Google Scholar] [CrossRef]

- De Villiers, C.; Rouse, P.; Kerr, J. A new conceptual model of influences driving sustainability based on case evidence of the integration of corporate sustainability management control and reporting. J. Clean. Prod. 2016, 136, 78–85. [Google Scholar] [CrossRef]

- Seelos, C.; Mair, J. Social entrepreneurship: Creating new business models to serve the poor. Bus. Horizons 2005, 48, 241–246. [Google Scholar] [CrossRef]

- Mair, J.; Marti, I. Social entrepreneurship research: A source of explanation, prediction, and delight. J. World Bus. 2006, 41, 36–44. [Google Scholar] [CrossRef]

- Rimac, T.; Mair, J.; Battilana, J. Social entrepreneurs, socialization processes, and social change: The case of SEKEM. In Using a Positive Lens to Explore Social Change and Organizations: Building a Theoretical and Research Foundation; Golden-Biddle, K., Dutton, J., Eds.; Routledge: New York, NY, USA, 2012; pp. 71–89. ISBN 978-0-415-87885-2. [Google Scholar]

- Littlewood, D.; Holt, D. How social enterprises can contribute to the Sustainable Development Goals (SDGs)–A conceptual framework. In Entrepreneurship and the Sustainable Development Goals; Apostolopoulos, N., Al-Dajani, H., Holt, D., Jones, P., Newbery, R., Eds.; Emerald Publishing Limited: Bingley, UK, 2018; pp. 33–46. ISBN 978-1-78756-376-6. [Google Scholar]

- Haanaes, K.; Michael, D.; Jurgens, J.; Rangan, S. Making sustainability profitable. Harvard Bus. Rev. 2013, 91, 110–115. [Google Scholar]

- Horngren, C.T.; Sundem, G.L.; Schatzberg, J.O.; Burgstahler, D. Introduction to Management Accounting, 16th ed.; Pearson: New York, NY, USA, 2013; ISBN 978-0133058819. [Google Scholar]

- Gray, R.; Bebbington, J. Environmental accounting, managerialism and sustainability: Is the planet safe in the hands of business and accounting? In Advances in Environmental Accounting & Management; Emerald Group Publishing Limited: Bingley, UK, 2000; Volume 1, pp. 1–44. ISBN 978-0-76230-334-2. [Google Scholar]

- Gwilliam, D.; Jackson, R.H.G. Fair value in financial reporting: Problems and pitfalls in practice: A case study analysis of the use of fair valuation at Enron. Account. Forum 2008, 32, 240–259. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R.L. Sustainability accounting for companies: Catchphrase or decision support for business leaders? J. World Bus. 2010, 45, 375–384. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The sustainability balanced scorecard—Linking sustainability management to business strategy. Bus. Strateg. Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Bebbington, J.; Unerman, J.; O’Dwyer, B. Introduction to sustainability accounting and accountability. In Sustainability Accounting and Accountability, 2nd ed.; Bebbington, J., Unerman, J., O’Dwyer, B., Eds.; Routledge: Abingdon, UK, 2014; ISBN 978-0415695572. [Google Scholar]

- Merchant, K.A.; Riccaboni, A. Il Controllo di Gestione; McGraw-Hill: Milano, Italy, 2001; ISBN 978-8-83-867385-6. [Google Scholar]

- Berry, A.J.; Broadbent, J.; Otley, D.T. (Eds.) Management Control: Theories, Issues and Practices; Macmillan International Higher Education: London, UK, 2016; ISBN 979-0-333-57243-6. [Google Scholar]

- Otley, D. The contingency theory of management accounting and control: 1980–2014. Manag. Account. Res. 2016, 31, 45–62. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Mastering the management system. Harvard Bus. Rev. 2008, 86, 62. [Google Scholar]

- Schaltegger, S. Sustainability management control. In Environmental Management Accounting and Supply Chain Management; Springer: Dordrecht, The Netherlands, 2011; pp. 337–352. ISBN 978-94-007-1389-5. [Google Scholar]

- Schaltegger, S.; Burritt, R. Contemporary Environmental Accounting; Greenleaf: Sheffield, UK, 2000. [Google Scholar]

- Henri, J.-F.; Journault, M. Eco-control: The influence of management control systems on environmental and economic performance. Account. Org. Soc. 2010, 35, 63–80. [Google Scholar] [CrossRef]

- Simons, R. Levers of Control, How Managers Use Innovative Control Systems to Drive Strategic Renewal; Harvard Business School Press: Boston, MA, USA, 1995. [Google Scholar]

- Arvidsson, S. Disclosure of non-financial information in the annual report: A management-team perspective. J. Intellect. Cap. 2011, 12, 277–300. [Google Scholar] [CrossRef]

- Schaltegger, S.; Bennett, M.; Burritt, R. (Eds.) Sustainability Accounting And reporting; Springer Science & Business Media: Dordrecht, The Netherlands, 2006; Volume 21, ISBN 978-1-4020-4974-3. [Google Scholar]

- Dumay, J.; Dai, T. Integrated thinking as a cultural control? Meditari Account. Res. 2017, 25, 574–604. [Google Scholar] [CrossRef]

- Manes-Rossi, F.; Tiron-Tudor, A.; Nicolò, G.; Zanellato, G. Ensuring More Sustainable Reporting in Europe Using Non-Financial Disclosure—De Facto and De Jure Evidence. Sustainability 2018, 10, 1162. [Google Scholar] [CrossRef]

- Loh, L.; Thomas, T.; Wang, Y. Sustainability reporting and firm value: Evidence from Singapore-Listed companies. Sustainability 2017, 9, 2112. [Google Scholar] [CrossRef]

- Kolk, A. Sustainability, accountability and corporate governance: Exploring multinationals’ reporting practices. Bus. Strateg. Environ. 2008, 17, 1–15. [Google Scholar] [CrossRef]

- Lozano, R.; Nummert, B.; Ceulemans, K. Elucidating the relationship between sustainability reporting and organisational change management for sustainability. J. Clean. Prod. 2016, 125, 168–188. [Google Scholar] [CrossRef]

- GRI. About sustainability reporting. Available online: https://www.globalreporting.org/information/sustainability-reporting/Pages/default.aspx (accessed on 3 September 2018).

- Gonzalez Gonzalez, J.M.; Zamora Ramírez, C. Organisational communication on climate change: The influence of the institutional context and the adoption pattern. Int. J. Clim. Chang. Str. 2016, 8, 286–316. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research and Applications: Design and Methods; Sage publicatIons: Thousand Oaks, CA, USA, 2017; ISBN 9781506336169. [Google Scholar]

- Eisenhardt, M.K. Building theories from case study research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Siggelkow, N. Persuasion with case studies. Acad. Manag. J. 2007, 50, 20–24. [Google Scholar] [CrossRef]

- Burns, J.; Scapens, R.W. Conceptualising management accounting change: An institutional framework. Manag. Account. Res. 2000, 11, 3–25. [Google Scholar] [CrossRef]

- Scapens, R.W. Researching management accounting practice: The role of case study methods. Br. Account. Rev. 1990, 22, 259–281. [Google Scholar] [CrossRef]

| Frequency of Meeting | Actors | Content of Meeting | Type of Documents Shared |

|---|---|---|---|

| Weekly meetings |

| Discussion, on a philosophical but also practical level, what the purpose of SEKEM means, with the aim to collect some ideas and translate the purpose into concrete solutions and projects (vision meetings) |

|

| Monthly meetings |

| Presentation and discussion of consolidated sustainability data with all companies’ groups |

|

| Quarterly meetings |

| Discussion and validation of data about sustainable performance of SEKEM group |

|

| Half year base meetings |

| Discussion and assessment of financial and nonfinancial business performance |

|

| Annual meetings |

| Discussion and approval of Sustainability Report |

|

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vitale, G.; Cupertino, S.; Rinaldi, L.; Riccaboni, A. Integrated Management Approach Towards Sustainability: An Egyptian Business Case Study. Sustainability 2019, 11, 1244. https://doi.org/10.3390/su11051244

Vitale G, Cupertino S, Rinaldi L, Riccaboni A. Integrated Management Approach Towards Sustainability: An Egyptian Business Case Study. Sustainability. 2019; 11(5):1244. https://doi.org/10.3390/su11051244

Chicago/Turabian StyleVitale, Gianluca, Sebastiano Cupertino, Loredana Rinaldi, and Angelo Riccaboni. 2019. "Integrated Management Approach Towards Sustainability: An Egyptian Business Case Study" Sustainability 11, no. 5: 1244. https://doi.org/10.3390/su11051244

APA StyleVitale, G., Cupertino, S., Rinaldi, L., & Riccaboni, A. (2019). Integrated Management Approach Towards Sustainability: An Egyptian Business Case Study. Sustainability, 11(5), 1244. https://doi.org/10.3390/su11051244