1. Introduction

With the development of global economy, environmental pollution is becoming more and more serious [

1,

2,

3,

4,

5,

6]. Especially, the greenhouse effect caused by carbon dioxide (CO

2) has become one of the most concerned environmental problems in the world. This greenhouse effect has become an extremely serious threat to human survival and socio-economic sustainable development. Globally supplied energy is still growing to support the global economy, but the world is also facing the challenge of reducing greenhouse gas emissions. According to the International Energy Agency (IEA), global energy consumption increased by 2.3% year-on-year in 2018 due to strong global economic growth, almost double the average growth rate since 2010. Global natural gas consumption was 3.86 trillion cubic meters, up 5.3% year-on-year, 2.3 times the average growth rate of the past five years. Energy efficiency improvements are weak, and energy-related CO

2 emissions are hitting new highs. The sum of energy demand growth in China, the United States and India accounts for about 70% of the global total. It is predicted that by 2030, the world’s energy demand will increase by about 60% compared with 2000, and the growth of energy demand in developing countries will make it account for the majority of the increase in CO

2 emissions. According to analysis, developing countries will account for about 85% of the increase in CO

2 emissions from 2000 to 2030 [

7]. Promoting greenhouse gas emission reduction is still an important task for human beings to cope with climate warming and promote sustainable use of resources. Whether it is the International Climate Convention negotiations; initiated in 1990, or the Kyoto Protocol (2005), the Bali Roadmap (2007), the Copenhagen Accord (2009) and Paris Agreement (2015), are committed to inhibit global warming through global cooperation.

To achieve sustainable development, we must consider the relationship between economic activities and environmental quality. There is substantial research on the relationship between economic growth, energy consumption, and carbon dioxide emissions. There are three research directions: the first part focuses on the relationship between economic growth and energy consumption; the second part focuses on the relationship between economic growth and carbon dioxide emissions; the third part puts the three variables under the same framework to study its dynamic causality. However, although many scholars have conducted a lot of research in the past 30 years, the relationship between the three has not been consistently concluded. The existing literature reveals that empirical studies differ substantially, for example, some studies investigate single countries [

8,

9,

10] and others examine multiple countries [

11,

12,

13,

14]. With the introduction of additional variables, the relationship between the three has undergone new changes, such as urbanization [

15], trade openness [

16], foreign direct investment [

17], industrialization [

18]. In this regard, it is believed that additional variables can help explain the complexity surrounding the relationship between economic activity and the environment [

19]. In recent years, financial development variables have attracted great attention from scholars. More and more scholars have begun to study financial development into the framework of economic growth, energy consumption and carbon dioxide emissions.

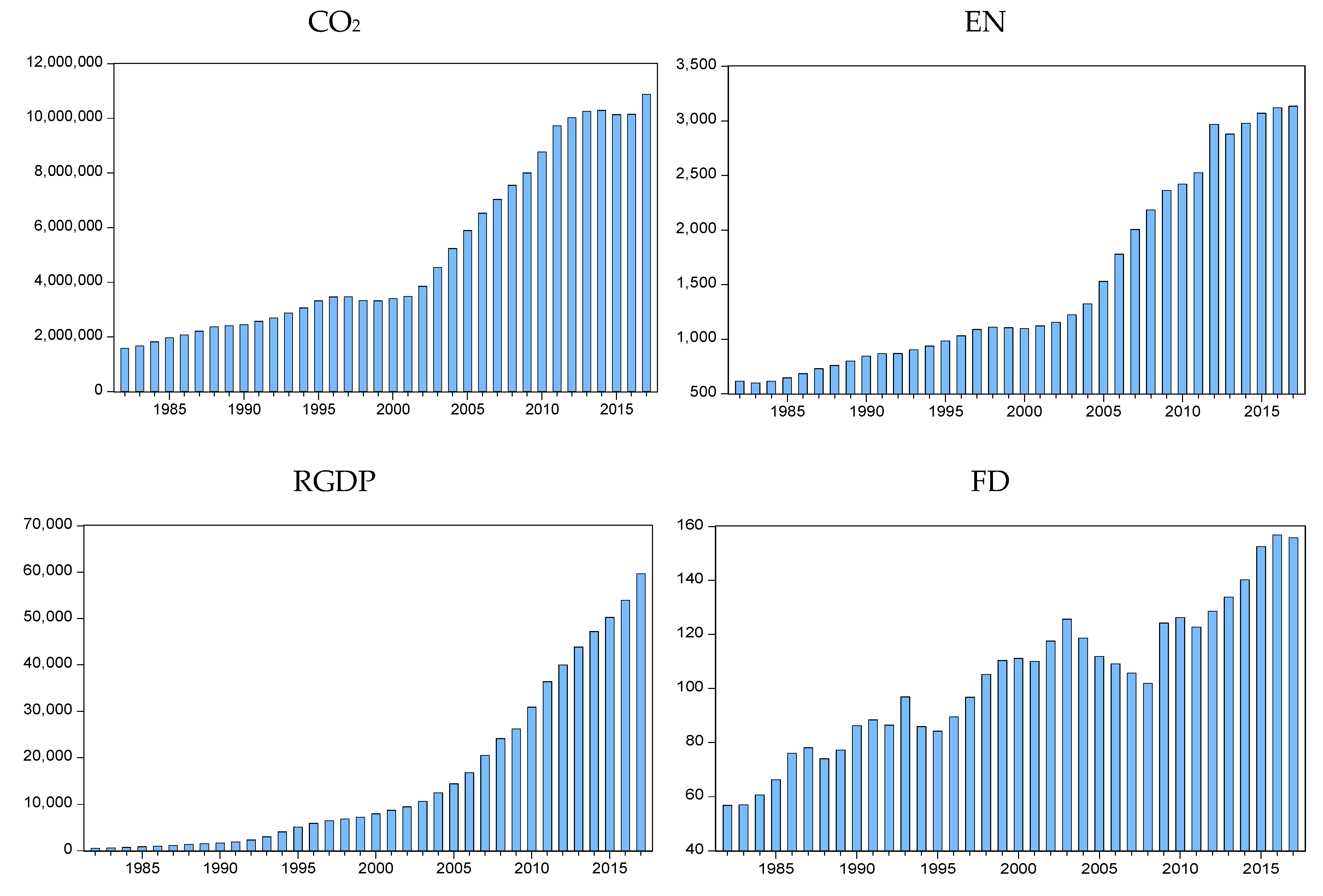

The choice of China is also motivated by the fact that China has been the second largest energy consumer and one of the fastest growing economies in the world. China is currently in the middle and late stages of industrialization, and has taken energy-saving and carbon-reduction measures to achieve a low-carbon economy. According to the China Statistical Yearbook 2018, from 2005 to 2017, the carbon dioxide intensity of GDP has dropped by 45%, and the annual average rate of decline has reached 4.9%. However, the Paris Agreement the proposed National Independent Contribution (NDC) targets, which is by 2030, the carbon dioxide intensity per unit of GDP will fall by 60% to 65% compared to 2005, and the proportion of non-fossil energy in primary energy consumption will increase to around 20%. Furthermore, China has experienced a significant rise in energy consumption and carbon emissions in recent decades. According to the World Energy China Outlook (2013–2014) forecast, the total energy demand in China will account for 24% of the world’s total energy demand in 2035, and the increase in energy demand will be as much as 38.5%. By then, the energy position of China will become more prominent in the world’s energy supply and demand pattern. Along with the rapid growth of the social economy, energy consumption continues to increase, and environmental pollutant emissions are further expanded, which has led to a severe test of carbon dioxide and sustainable economic development. At the same time, China’s financial development has grown rapidly in the past four decades, and its scale has expanded very rapidly. It has become an important world financial power. Therefore, we choose China as the research object to study the interaction between energy consumption, financial development, carbon dioxide emissions and economic growth, which has important policy significance for China to reduce carbon dioxide emissions.

The rest of this article is organized as follows.

Section 2 briefly reviews the literature.

Section 3 explains the data and methods.

Section 4 discusses the empirical results.

Section 5 summarizes the paper and discusses the policy implications.

2. Literature Review

The first strand of existing literature coops with a wide range of mixed result studies about energy consumption and economic growth. The Kraft and Kraft [

20] investigated the causal relationship between these two variables in 1978. Through a study for the United States, covering the period between 1947 and 1974, they found that there is a one-way causal relationship between GNP and energy consumption. However, Akarca and Long [

21] used data from 1947 to 1972 to conclude that there is no causal relationship between GNP and energy consumption. This also indicates that the choice of sample interval may affect the empirical results. Eden and Been [

22] conclude that there is also no causal relationship between the two in USA from 1947 to 1979. Masih [

23] studied the relationship between energy consumption and economic growth in six Asian countries based on Johansen cointegration test and VECM Granger test. The study found that only India, Pakistan and Indonesia have a long-term co-integration relationship between energy consumption and economic growth. Hye and Riaz [

24] studied the causal relationship between energy consumption and economic growth in Pakistan from 1971 to 2007 by autoregressive distributed lag (ARDL) and Granger causality test. The study found that a two-ways causal relationship between energy use and economic growth in the Short term, while the long-run causality result shows that a one-way causal relationship exist runs from economic growth to energy use. Odhiambo [

25] examined the relationship between energy consumption and economic growth in Tanzania, which shows the existence of one-way causality that runs from energy use to growth of the economy. Lin [

26] used the Johansen–Juselius (JJ) cointegration test and VECM Granger causality test to prove that there is a long-term equilibrium relationship between China’s power consumption and economic growth. In recent years, some scholars have compared the relationship among regions. For example, Li [

27] found that China’s energy consumption has a significant positive effect on economic growth and the eastern region of China has the most effective effect. Ahmed et al. [

28] investigated the relationship between per capita electricity consumption and per capita real income, and the relationship between per capita energy consumption and economic growth in Pakistan, and found that there is a two-way causal relationship between them.

The second strand of existing literature on this topic provides empirical evidence on the relationship between economic growth and CO

2 emissions. Existing research on the relationship between carbon emissions and economic growth mainly includes linear relationships [

29,

30], N-curve relationships [

31], and inverted U-shaped Curve relationships [

32]. Although most scholars support Inverted U-curve relationship relationship [

33,

34,

35], namely the environmental Kuznets curve (EKC), the findings of Robalino-López et al. [

36] and Baek [

37] showed that the inverted U-shaped curve does not hold, while Moomaw and Unruh [

38], Martinez Zarzoso, and Bengochea-Morancho [

39] found that there is an N-type relationship between economic growth and CO

2 emissions. The income per capita corresponding to the inflection point of the EKC curve varies widely, ranging from

$13,260 to

$80,000.Han and Lu [

40] studied the Environmental Kuznets curve in different countries and the findings also vary greatly, showing the relationship of inverted U and linear. Some scholars [

41,

42] found that carbon dioxide emissions per capita increased monotonously with real income per capita, and there was no inflection point. However, Lantz and Feng [

43] found that there was no significant relationship between per capita GDP and carbon dioxide emissions. There is no consensus on the relationship between carbon emissions and economic development [

44]. Lin and Jiang [

45] used the traditional environmental Kuznets model to simulate and predict the Kuznets curve of carbon dioxide in China on the basis of carbon dioxide emission prediction, and found that the results were quite different. The differences in the above literature conclusions are mainly due to the significant differences between the study region and the choice of empirical methods [

46]. Henisz [

47] pointed out that it is more reasonable to discuss the relationship between them from the perspective of causality compared with the EKC hypothesis. Since then, more and more scholars have chosen to use the causality test to explore the feedback mechanism of the interaction between economic growth and carbon dioxide emissions.

The third strand investigated the relationship between energy consumption, CO

2 emission and economic growth, beginning with Ang [

48] who introduced the first study where he examined the connection among variables in France for 1960–2000 by co-integration analysis and error correction model (ECM).The outcome reveals that economic growth and carbon dioxide emissions have a U-shaped relationship in the long run, and that economic growth contributes to an increase in energy consumption, while the increase in energy consumption lead to an increase in carbon dioxide emissions. Soytas et al. [

49] used co-integration methodology and VECM in Turkey and results indicate that a unidirectional causality exists from energy to GDP and energy consumption has a positive effect on economic growth. Tao and Song [

50] measured the dynamic relationship between carbon dioxide emission, energy consumption, gross national income per capita and trade openness in China using the sample data of 1971–2008 in China. The results show that there is a long-term equilibrium relationship among them, and the long-term and short-term Granger causality exists at the same time. Arouri et al. [

51] investigated the relationship between economic growth, energy consumption and carbon dioxide emissions in 12 countries of the Middle East and North Africa within the framework of panel unit root test and co-integration. The result is that there is a two-way causality between energy consumption and carbon dioxide in the long run. Govindaraju and Tang [

52] applied the Granger causality approach in China and India, the result reveals the long-run relationship among the variables in China but no Indian. Cowan [

53] studied the relationship between electricity consumption, economic growth and carbon dioxide emissions in BRICS from 1990 to 2010 under the framework of panel causality analysis. Osigwe and Arawomo [

54] used the Granger causality approach to study the link between energy consumption, oil prices and economic growth in Nigeria. A two-way causal relationship between energy consumption and economic growth has been established. Asongu et al. [

55] investigated the causal relationship between carbon dioxide emissions, energy consumption and GDP and there was a strong causal relationship between these variables.

In recent years, with the deepening of financial development, more and more scholars are paying attention to the relationship between financial development and economic growth [

56,

57]. In the modern economy, finance is the blood and accelerator of the economy, which affects the basic characteristics of energy consumption from many paths, and thus affects energy conservation and emission reduction. On the one hand, financial development will increase energy consumption. As the scale of financial development continues to expand and the efficiency of financial development continues to increase, consumers and businesses can obtain loans at a lower cost and in a more convenient way. For example, Sadorsky [

58] studied the impact of financial development on energy consumption in 22 new economies from 1990 to 2006 based on the generalized method of moments(GMM). The empirical results show that when financial development is measured by stock market indicators, there is a significant positive relationship between financial development and energy consumption. Sadorsky [

59] applied the same method to study nine economies along the east-central border of Europe, and found that when using bank indicators to measure financial development, the relationship between financial development and energy consumption was significantly positive. On the other hand, financial development will reduce energy consumption. Financial development encourages enterprises to introduce high-tech and equipment for energy conservation and environmental protection, and provide financial support for the development of knowledge-intensive and technology-intensive high-tech industries. Therefore, financial development can reduce energy consumption. For example, Tamazian and Chousa et al. [

60] found that financial development and economic growth could have an impact on the environmental quality, which would contribute to the reduction of carbon dioxide emissions and play a positive role in the improvement of environmental quality. Tamazian and Rao [

61] studied the relationship between financial development and environmental pollution in 24 transition countries based on the generalized method of moments (GMM) to control endogeneity. They believe that foreign investment found to measure financial development helps reduce carbon dioxide emissions per capita. Moreover, in addition to incorporating financial development into economic growth, energy consumption and carbon dioxide research, researchers have also added variables such as foreign direct investment (FDI), trade openness, and urbanization. For example, Farhani and Ozturk [

62] empirically examine the link relationship between CO

2 emissions, economic growth, energy consumption, financial development, trade openness, and urbanization in Tunisia for 1971–2012 by ARDL-ECM method. Moreover, they find that financial development has a positive and significant impact on environmental pollution. The monotonic positive relationship is also found between GDP and CO

2 emissions.

5. Conclusions and Policy Recommendation

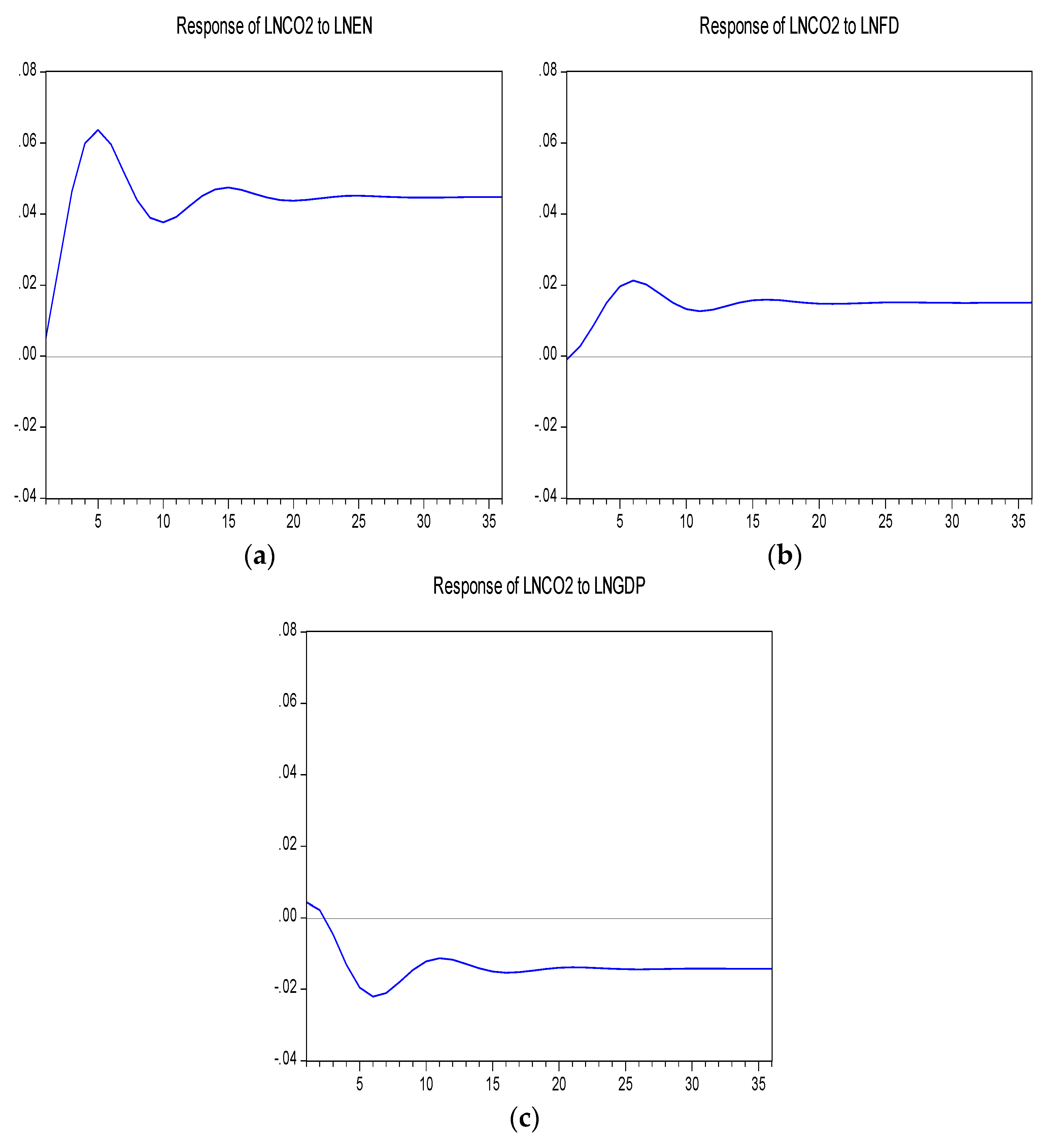

This paper investigates the effects of energy consumption, economic growth and financial development on CO2 emissions in China over the period of 1982–2017. The empirical results show that there is a long-term cointegration relationship between the four variables. According to the Granger causality test, in the short run, carbon dioxide emissions have a positive effect on energy consumption, economic growth and financial development; economic growth and financial development are Granger reasons for energy consumption. In the impulse response test results, it can be seen that there is a positive two-way causal relationship between CO2 emissions and energy consumption; financial development will promote carbon dioxide emissions in the short term, while the increase of CO2 emissions will inhibit financial development. Economic growth can inhibit CO2 emissions in the long run, and carbon dioxide emissions are more stimulating in the short term. From the results of variance decomposition, it can be seen that the variance contribution of CO2 emission prediction error is mainly from energy consumption and economic growth.

These results have some policy implications for China. First, we should steadily promote financial innovation, low-carbon finance, and green credit business. It is necessary to improve the development level of the stock market, strengthen the supervision and guidance of the capital market system, improve the information disclosure and other related systems in the capital market, and actively play the role of the stock market in promoting green energy conservation. Second, Energy consumption in China is exacerbating carbon dioxide emissions when energy consumption structure is still dominated by high-carbon energy such as coal. Therefore, the government should optimize energy structure, increase the efficiency of energy utilization and realize energy sustainable development in China. There must be a clear and specific strategy for encouraging renewable energy, such as providing adequate policy support in technological innovation. China has promoted the consumption revolution, strengthened energy technology innovation and energy system reform, and strived to build a clean, low-carbon, safe and efficient energy system, and accelerated the process of low-carbonization of energy. From 2005 to 2017, the proportion of non-fossil energy in primary energy consumption was increased to 13.8%, the proportion of natural gas was increased to 7.0%, the corresponding proportion of coal was dropped to 60.4%. Third, in view of the characteristics of China’s energy consumption, carbon emissions, financial development and economic growth, market-based measures can be adopted to improve environmental governance. Ren et al. [

75] found that carbon trading policy is helpful to improve energy structure and reduce CO

2 emissions by investigating China’s 30 provincial-level administrative regions in 2008–2015 panel data. Therefore, the government should continue to promote the construction of China’s carbon market, improve the participation of enterprises through reasonable pricing and quota allocation, and at the same time cooperate with other environmental protection policies to jointly promote sustainable development.

{kind=link}

{kind=link}