Response of Fresh Food Suppliers to Sustainable Supply Chain Management of Large European Retailers

,

,

Abstract

1. Introduction

2. Literature Review: Perishable Supply Chains

Conceptual Framework and Hypothesis

3. Methodology

3.1. Retailer Requirements

3.2. Supplier Response

- ▪

- R1 = Customer collaboration in local-regional and social economic development.

- ▪

- R2 = Production Scheduling with the customer in medium and long term.

- ▪

- R3 = Customer collaboration in actions related to environmental impact of production.

- ▪

- R4 = Implemented high rotation programs to promote quality (fresh produce sales, offers).

- ▪

- R5 = Degree of customer communication in relation to quality.

- ▪

- R6 = Achieving quality requirements of customer.

- ▪

- R7 = Use of intermodal transport as a sustainable transport mode.

- ▪

- R8 = Collaboration with customers to reduce transportation cost.

- ▪

- R9 = Coordinating transport with customer in order to improve processes.

- ▪

- R10 = Collaboration with customer to select logistics providers according to quality service.

- ▪

- R11 = Selection of transport (groupage) depending on quality product.

- ▪

- R12 = Degree of quality control during transport.

- ▪

- R13 = Collaboration with customer for quality at destination (logistics blocks).

- ▪

- R14 = Supply directly to store to reduce the environmental impact of routes.

- ▪

- R15 = Using warehouse destinations for route optimization.

3.2.1. Sample

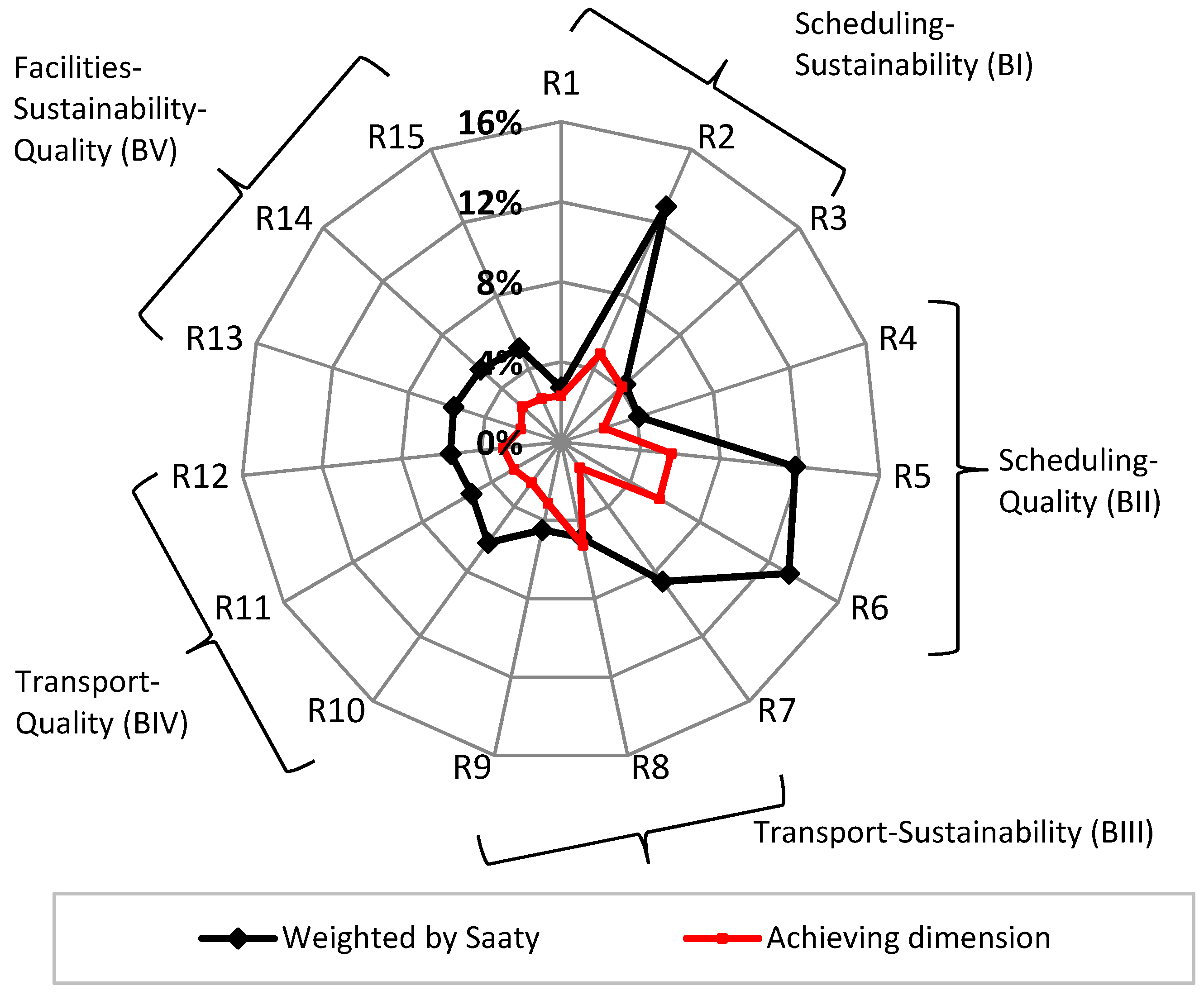

3.2.2. Weighting of the Importance of Supplier Responses

3.2.3. Relationship between Degree of Compliance, Size, and Performance

- ▪

- ▪

4. Results Analysis and Discussion

4.1. Analysis of Retailer Strategies and Operations

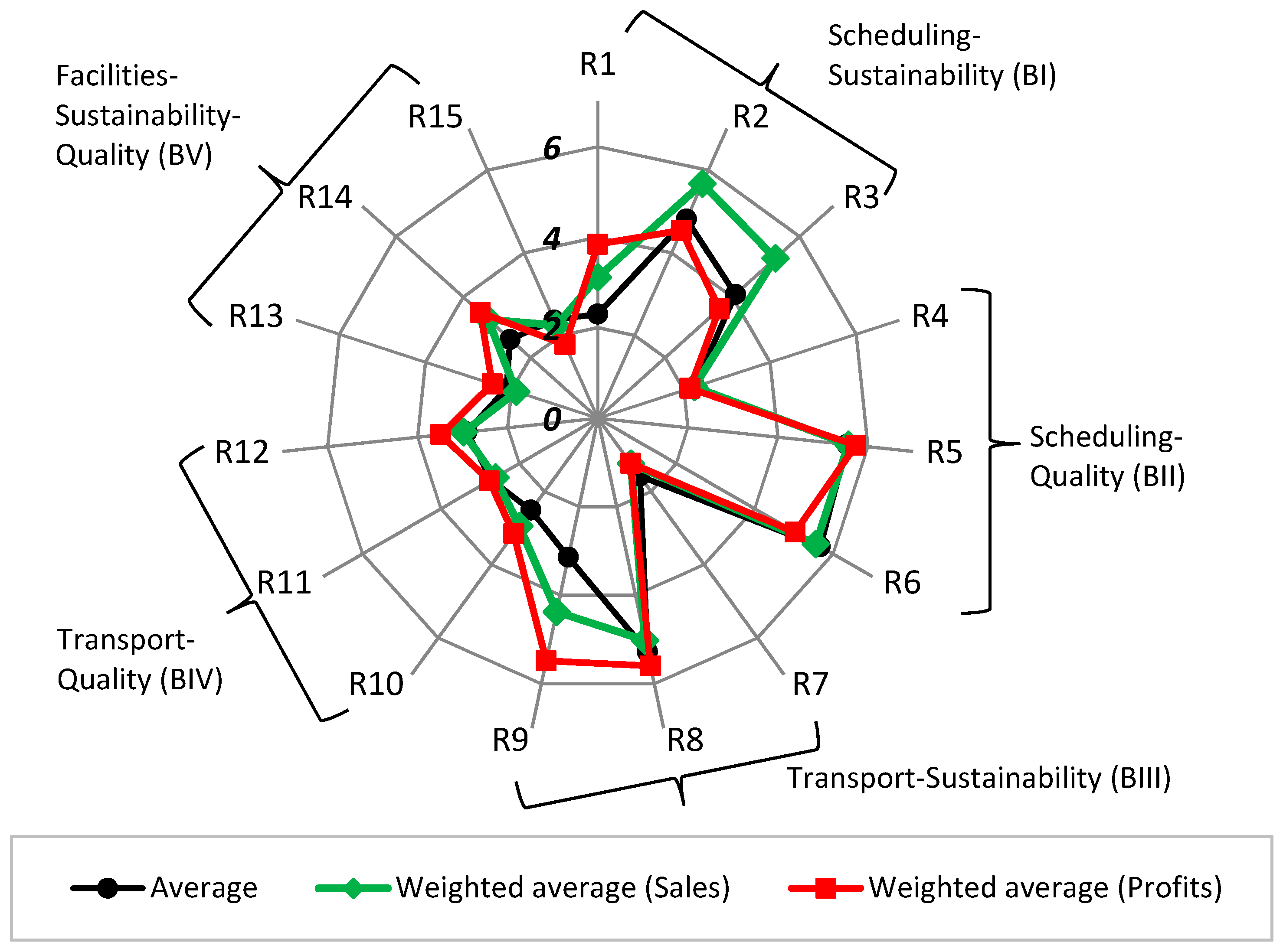

4.2. Responses of Horticultural Exporters

- ▪

- BI. Marketing enterprises respond well when scheduling their production according to what customers order (R2), as well as in terms of matters related to environmental and social impact (R3). They do not collaborate with the customer in local economic development (R1).

- ▪

- BII. As for quality issues, there is a close relationship with the customer (R5), accepting the latter’s requests (R6). It is necessary to increase production programs of high rotation to promote quality (R4).

- ▪

- BIII. There is no collaboration to implement inter-modality (R7), but there is to reduce costs of transport and other processes (R8, R9).

- ▪

- BIV. Results obtained are low regarding collaboration with the customer to improve transport quality.

- ▪

- BV. In addition, little has been done in terms of collaboration to optimize deliveries and intermediate facilities.

4.3. Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Survey

PART1

- ▪

- Turnover (euros): ________________

- ▪

- Profit Before Taxes (euros): ________________

- ▪

- Business Assets (euros): ________________

Production-Sustainability Programming

- 1.

- Do you collaborate with your client in the development of the local economy of your region?

1 2 3 4 5 6 7 - 2.

- Do you carry out a medium or long term sales program with your client?

1 2 3 4 5 6 7 - 3.

- Do you carry out actions aimed at controlling the social and environmental responsibility of your production?

1 2 3 4 5 6 7

Production-Quality-Health Programming

- 4.

- Do you have a sales program where the customer demands a continuous supply (high rotation) with the aim of promoting the freshness of the product at the point of sale?

1 2 3 4 5 6 7 - 5.

- Are the relationships with your supplier in terms of quality-healthiness continuous and close?

1 2 3 4 5 6 7 - 6.

- Do you always meet your customer’s quality certification requirements?

1 2 3 4 5 6 7

Transport-Sustainability

- 7.

- Do you use intermodality in freight transport?

1 2 3 4 5 6 7 - 8.

- Do you use collaboration strategies with your client so that the economic and environmental costs in the transport of goods are lower?

1 2 3 4 5 6 7 - 9.

- Does your client assume the cost of transport with the aim of optimizing routes?

1 2 3 4 5 6 7

Transport-Quality-Health

- 10.

- Do you coordinate with your client the hiring of logistic suppliers in order to assure the quality of the service?

1 2 3 4 5 6 7 - 11.

- Do you carry out any type of discrimination in the transport (groupage) depending on the product or destination of the production due to the demands of your client?

1 2 3 4 5 6 7 - 12.

- Do you have any type of system to control the quality of the product in the transport?

1 2 3 4 5 6 7

Installations-Sustainability/Quality-Sanitation

- 13.

- Do you collaborate with your client in maintaining the quality of the product in its logistics blocks?

1 2 3 4 5 6 7 - 14.

- Do you supply your customers at the final point of sale?

1 2 3 4 5 6 7 - 15.

- Do you use distribution warehouses in the main destinations to which you send your merchandise?

1 2 3 4 5 6 7

PART 2. WEIGHTING

| 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | |

| 1 | ||||||||||||||

| 2 | ||||||||||||||

| 3 | ||||||||||||||

| 4 | ||||||||||||||

| 5 | ||||||||||||||

| 6 | ||||||||||||||

| 7 | ||||||||||||||

| 8 | ||||||||||||||

| 9 | ||||||||||||||

| 10 | ||||||||||||||

| 11 | ||||||||||||||

| 12 | ||||||||||||||

| 13 | ||||||||||||||

| 14 |

- ▪

- 1 = The importance of the variables is equal.

- ▪

- 3 = The row variable is slightly more important than the column variable.

- ▪

- 5 = The row variable is more important than the column variable.

- ▪

- 7 = The row variable is much more important than the column variable.

- ▪

- 9 = The row variable is extremely more important than the column variable.

- ▪

- 1/3 = The variable column is slightly more important than the variable row.

- ▪

- 1/5 = The variable column is more important than the variable row.

- ▪

- 1/7 = The variable column is much more important than the variable row.

- ▪

- 1/9 = The variable column is extremely more important than the variable row.

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Mean | Dev. | PRO | ASS | R1 | R2 | R3 | R4 | R5 | R6 | R7 | R8 | R9 | R10 | R11 | R12 | R13 | R14 | R15 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SAL | 36.001 | 50.14 | 0.321 * | 0.690 ** | 0.490 ** | 0.630 ** | 0.520 ** | −0.010 | −0.218 | −0.112 | −0.357 ** | −0.167 | 0.641 ** | 0.365 ** | −0.075 | 0.059 | −0.225 | 0.422 ** | −0.097 |

| PRO | 344 | 1.487 | 0.226 | 0.098 | 0.326 * | −0.068 | −0.025 | 0.021 | 0.351 ** | 0.120 | 0.065 | 0.381 ** | 0.173 | 0.010 | 0.141 | 0.108 | 0.185 | 0.148 | |

| ASS | 15.792 | 23.604 | 0.402 ** | 0.630 ** | 0.495 ** | −0.019 | −0.259 * | −0.066 | −0.320 * | −0.169 | 0.587 ** | 0.326 * | −0.135 | 0.057 | −0.305 * | 0.399 ** | −0.008 | ||

| R1 | 2.302 | 1.225 | 0.386 ** | 0.136 | 0.647 ** | 0.099 | 0.149 | −0.099 | 0.092 | 0.237 | 0.074 | −0.191 | 0.164 | 0.040 | 0.481 ** | −0.078 | |||

| R2 | 5.233 | 2.114 | 0.263 * | 0.173 | 0.007 | 0.212 | −0.142 | −0.057 | 0.435 ** | 0.126 | 0.179 | −0.105 | −0.080 | 0.346 * | 0.003 | ||||

| R3 | 4.140 | 1.740 | −0.032 | −0.077 | −0.074 | −0.206 | −0.068 | 0.152 | 0.247 | −0.004 | −0.006 | −0.313 * | 0.269 * | 0.040 | |||||

| R4 | 2.256 | 1.071 | 0.238 | 0.139 | 0.147 | 0.194 | −0.084 | −0.368 ** | 0.001 | 0.001 | 0.204 | 0.144 | 0.161 | ||||||

| R5 | 6.512 | 1.437 | 0.454 ** | 0.361 ** | 0.187 | −0.351 * | −0.211 | 0.411 ** | 0.069 | 0.146 | 0.068 | 0.293 * | |||||||

| R6 | 6.395 | 1.545 | 0.047 | 0.125 | −0.222 | −0.047 | 0.303 * | 0.025 | −0.042 | 0.213 | 0.027 | ||||||||

| R7 | 1.581 | 0.698 | 0.210 | −0.353 * | −0.262 * | 0.193 | −0.059 | 0.331 * | −0.124 | 0.240 | |||||||||

| R8 | 5.279 | 1.141 | 0.049 | −0.027 | −0.033 | −0.040 | 0.074 | 0.142 | −0.142 | ||||||||||

| R9 | 3.186 | 1.607 | 0.485 ** | −0.025 | 0.164 | −0.120 | 0.250 | −0.155 | |||||||||||

| R10 | 2.512 | 0.883 | −0.176 | 0.390 ** | −0.242 | 0.325 * | 0.023 | ||||||||||||

| R11 | 2.721 | 1.054 | −0.375 ** | 0.321 * | −0.154 | 0.248 | |||||||||||||

| R12 | 2.907 | 0.971 | −0.085 | 0.203 | 0.090 | ||||||||||||||

| R13 | 2.116 | 0.731 | −0.001 | −0.029 | |||||||||||||||

| R14 | 2.605 | 1.137 | 0.007 | ||||||||||||||||

| R15 | 2.372 | 0.952 |

Appendix C

| R1 | R2 | R3 | R4 | R5 | R6 | R7 | R8 | R9 | R10 | R11 | R12 | R13 | R14 | R15 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| R1 | 1.00 | 0.21 | 0.23 | 0.28 | 0.52 | 0.50 | 0.44 | 0.44 | 0.84 | 0.23 | 0.66 | 1.47 | 0.39 | 0.39 | 0.39 |

| R2 | 6.21 | 1.00 | 1.80 | 1.80 | 3.80 | 1.00 | 1.00 | 3.40 | 1.40 | 2.20 | 3.40 | 3.40 | 5.00 | 3.00 | 3.00 |

| R3 | 5.85 | 0.60 | 1.00 | 1.40 | 0.97 | 0.52 | 0.44 | 0.57 | 0.60 | 0.55 | 0.60 | 0.87 | 0.46 | 0.60 | 0.60 |

| R4 | 3.40 | 0.60 | 0.87 | 1.00 | 0.41 | 0.36 | 0.25 | 0.84 | 1.00 | 1.00 | 1.00 | 0.73 | 1.00 | 1.00 | 1.00 |

| R5 | 3.40 | 0.50 | 2.08 | 3.81 | 1.00 | 1.67 | 1.27 | 2.20 | 3.80 | 2.87 | 3.80 | 2.60 | 3.80 | 4.60 | 2.60 |

| R6 | 5.04 | 1.00 | 3.40 | 4.20 | 1.14 | 1.00 | 1.67 | 4.20 | 3.40 | 4.60 | 2.60 | 2.60 | 3.40 | 4.60 | 3.80 |

| R7 | 2.60 | 1.00 | 2.62 | 4.61 | 1.27 | 1.14 | 1.00 | 2.60 | 3.00 | 2.60 | 1.00 | 1.00 | 1.00 | 1.00 | 1.80 |

| R8 | 2.62 | 0.31 | 2.60 | 1.80 | 0.60 | 0.25 | 0.47 | 1.00 | 0.28 | 0.28 | 1.64 | 2.60 | 1.00 | 1.00 | 1.00 |

| R9 | 1.00 | 0.73 | 2.22 | 1.00 | 0.39 | 0.31 | 0.47 | 3.42 | 1.00 | 1.11 | 1.00 | 0.87 | 0.41 | 0.44 | 0.41 |

| R10 | 4.21 | 0.60 | 3.40 | 1.00 | 0.85 | 0.25 | 0.60 | 3.42 | 1.68 | 1.00 | 1.80 | 1.00 | 1.40 | 1.00 | 1.00 |

| R11 | 2.52 | 0.31 | 2.22 | 1.00 | 0.25 | 0.47 | 1.00 | 0.73 | 1.00 | 0.73 | 1.00 | 1.80 | 2.20 | 1.40 | 1.40 |

| R12 | 0.70 | 0.41 | 1.00 | 2.22 | 0.47 | 0.47 | 1.00 | 0.57 | 1.81 | 1.00 | 0.87 | 1.00 | 2.60 | 2.20 | 1.80 |

| R13 | 4.61 | 0.20 | 2.62 | 1.00 | 0.39 | 0.41 | 1.00 | 1.00 | 3.82 | 0.87 | 0.73 | 0.47 | 1.00 | 1.40 | 1.80 |

| R14 | 4.61 | 0.41 | 2.22 | 1.00 | 0.36 | 0.39 | 1.00 | 1.00 | 3.42 | 1.00 | 1.00 | 0.47 | 0.87 | 1.00 | 1.80 |

| R15 | 4.61 | 0.41 | 2.22 | 1.00 | 0.47 | 0.39 | 0.73 | 1.00 | 3.82 | 1.00 | 1.00 | 0.60 | 0.73 | 0.73 | 1.00 |

References

- Seuring, S.; Mülle, M. From a literature review to a conceptual framework for sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Dües, C.M.; Tan, K.H.; Lim, M. Green as the new Lean: How to use Lean practices as a catalyst to greening your supply chain. J. Clean. Prod. 2013, 40, 93–100. [Google Scholar] [CrossRef]

- Marshall, D.; McCarthy, L.; Heavey, C.; McGrath, P. Environmental and social supply chain management sustainability practices: Construct development and measurement. Prod. Plan. Control 2015, 26, 673–690. [Google Scholar] [CrossRef]

- Sharma, V.K.; Chandna, P.; Bhardwaj, A. Green supply chain management related performance indicators in agro industry: A review. J. Clean. Prod. 2017, 141, 1194–1208. [Google Scholar] [CrossRef]

- Ciccullo, F.; Pero, M.; Caridi, M.; Gosling, J.; Purvis, L. Integrating the environmental and social sustainability pillars into the lean and agile supply chain management paradigms: A literature review and future research directions. J. Clean. Prod. 2018, 172, 2336–2350. [Google Scholar] [CrossRef]

- Fischer, C.; Hartmann, M.; Reynolds, N.; Leat, P.; Revoredo-Giha, C.; Henchion, M.; Albisu, L.M.; Gracia, A. Factors influencing contractual choice and sustainable relationships in European agri-food supply chains. Eur. Rev. Agric. Econ. 2010, 36, 541–569. [Google Scholar] [CrossRef]

- Pérez-Mesa, J.C.; Galdeano-Gómez, E. Collaborative firms managing perishable products in a complex supply network: An empirical analysis of performance. Supply Chain Manag. Int. J. 2015, 20, 128–138. [Google Scholar] [CrossRef]

- Camanzi, L.; Malorgio, G.; García-Azcárate, T. The role of producer organizations in supply concentration and marketing: A comparison between European countries in the fruit and vegetable sector. J. Food Prod. Mark. 2011, 17, 327–354. [Google Scholar] [CrossRef]

- Arzu, G.; Erman, T. Supply chain performance measurement: A literature review. Int. J. Prod. Res. 2010, 48, 5137–5155. [Google Scholar] [CrossRef]

- Dobson, P.; Waterson, M.; Davies, S. The patterns and implications of increasing concentration in European food retailing. J. Agric. Econ. 2003, 54, 111–125. [Google Scholar] [CrossRef]

- Galdeano-Gómez, E.; Pérez-Mesa, J.C.; Aznar-Sánchez, J. Internationalisation of SMEs and simultaneous strategies of cooperation and competition: An exploratory analysis. J. Bus. Econ. Manag. 2017, 17, 1114–1132. [Google Scholar] [CrossRef]

- Singh, U.S.; Mishra, U.S. Supply Chain Management through Vertical Coordination in Vegetable Industry. Int. J. Supply Chain Manag. 2014, 3, 148–154. [Google Scholar]

- Jiménez-Guerrero, J.F.; Pérez-Mesa, J.C.; De Burgos, J.; Piedra-Muñoz, L. Considering the consumer in the design of a supply chain of perishables. Int. Food Agribus. Manag. Rev. 2018, 21, 525–542. [Google Scholar] [CrossRef]

- Hingley, M. Power imbalance in UK agri-food supply channels: Learning to live with the supermarkets? J. Mark. Manag. 2005, 21, 63–88. [Google Scholar] [CrossRef]

- Flynn, B.B.; Huo, B.; Zhao, X. The impact of supply chain integration on performance: A contingency and configuration approach. J. Oper. Manag. 2010, 28, 58–71. [Google Scholar] [CrossRef]

- Brandenburger, A.M.; Nalebuff, B.J. Co-opetition; Doubleday: New York, NY, USA, 1996. [Google Scholar]

- Wassermann, S.; Faust, K. Social Network Analysis: Methods and Applications; Cambridge University Press: Cambridge, UK, 1994. [Google Scholar]

- Hernández-Rubio, J.; Pérez-Mesa, J.C.; Piedra-Muñoz, L.; Galdeano-Gómez, E. Determinants of food safety level in fruit and vegetable wholesalers’ supply chain: Evidences from Spain and France. Int. J. Environ. Res. Public Health 2018, 15, 2246. [Google Scholar] [CrossRef]

- De Pablo, J.; Lévy, J.P.; Pérez-Mesa, J.C. Notes About the Production and Supply-Demand of Fruit and Vegetables in the Countries of the European Union. J. Food Prod. Mark. 2007, 13, 95–112. [Google Scholar] [CrossRef]

- Fischer, C.; Hartman, M. Agri-Food Chain Relationships; CAB International: London, UK, 2010. [Google Scholar]

- Kumar, R.; Singh, R.K.; Shankar, R. Strategy development by Indian SMEs for improving coordination in supply chain an empirical study. Compet. Rev. 2014, 24, 414–432. [Google Scholar]

- Siddh, M.M.; Soni, G.; Jain, R.; Sharma, M.K.; Yadav, V. Agri-fresh food supply chain quality (AFSCQ): A literature review. Ind. Manag. Data Syst. 2017, 117, 2015–2044. [Google Scholar] [CrossRef]

- Matopoulos, A.; Vlachopoulou, M.; Manthou, V.; Manos, B. A conceptual framework for supply chain collaboration: Empirical evidence from the agri-food industry. Supply Chain Manag. Int. J. 2007, 12, 177–186. [Google Scholar] [CrossRef]

- Manzini, R.; Accorsi, R.; Ayyad, Z.; Bendini, A.; Bortolini, M.; Gamberi, M.; Valli, E.; Toschi, T.G. Sustainability and quality in the food supply chain. A case study of shipment of edible oils. Br. Food J. 2014, 116, 2069–2090. [Google Scholar] [CrossRef]

- Badole, C.M.; Jain, D.R.; Rathore, D.A.; Nepal, D.B. Research and Opportunities in Supply Chain Modeling: A Review. Int. J. Supply Chain Manag. 2013, 1, 63–85. [Google Scholar]

- Yu, M.; Nagurney, A. Competitive food supply chain networks with application to fresh produce. Eur. J. Oper. Res. 2012, 224, 273–282. [Google Scholar] [CrossRef]

- Blackburn, J.; Scudder, G. Supply Chain Strategies for Perishable Products: The Case of Fresh Produce. Prod. Oper. Manag. 2009, 18, 129–137. [Google Scholar] [CrossRef]

- Smith, D.; Sparks, L. Temperature controlled supply chains. In Food Supply Chain Management; Bourlakis, M.A., Weightman, P.W.H., Eds.; Blackwell Publishing: Oxford, UK, 2004; pp. 179–198. [Google Scholar]

- Gharehgozli, A.; Iakovou, E.; Chang, Y.; Swaney, R. Trends in global E-food supply chain and implications for transport: Literature review and research directions. Res. Transp. Bus. Manag. 2017, 25, 2–14. [Google Scholar] [CrossRef]

- Gosling, J.; Purvis, L.; Naim, M.M. Supply chain flexibility as a determinant of supplier selection. Int. J. Prod. Econ. 2010, 128, 11–21. [Google Scholar] [CrossRef]

- Pérez-Mesa, J.C.; Galdeano-Gómez, E.; Salinas, J. Logistics network and externalities for short sea transport: An analysis of horticultural exports from southeast Spain. Transp. Policy 2012, 24, 188–198. [Google Scholar] [CrossRef]

- Gold, S.; Kunz, N.; Reiner, G. Sustainable Global Agrifood Supply Chains. Exploring the Barriers. J. Ind. Ecol. 2016, 21, 249–260. [Google Scholar] [CrossRef]

- Iakovou, E.; Vlachos, D.; Achillas, C.; Anastasiadis, F. Design of sustainable supply chains for the agrifood sector: A holistic research framework. Agric. Eng. Int. CIGR J. 2014, 1–10. [Google Scholar]

- Saura, J.R.; Palos-Sanchez, P.R.; Correia, M.B. Digital Marketing Strategies Based on the E-Business Model: Literature Review and Future Directions. In Organizational Transformation and Managing Innovation in the Fourth Industrial Revolution; IGI Global: Hershey, PA, USA, 2019; pp. 86–103. [Google Scholar]

- Sini, P. Long and short supply chain coexistence in the agricultural food market on different scales: Oligopolies, local economies and the degree of liberalisation of the global market. Eur. Sci. J. 2014, 10, 1857–7881. [Google Scholar]

- Tregear, A. Progressing knowledge in alternative and local food networks: Critical reflections and a research agenda. J. Rural Stud. 2011, 27, 419–430. [Google Scholar] [CrossRef]

- Kneafsey, M.; Venn, L.; Schmutz, U.; Balázs, B.; Trenchard, L.; Eyden-Wood, T.; Bos, E.; Sutton, G.; Blackett, M. Short Food Supply Chains and Local Food Systems in the EU. A State of Play of their Socio-Economic Characteristics; Joint Research Centre Institute for Prospective Technological Studies; European Commission: Brussels, Belgium, 2013. [Google Scholar]

- Marsden, T.; Banks, J.; Bristow, G. Food Supply Chain Approaches: Exploring their Role in Rural Development. Sociol. Rural. 2000, 40, 424–438. [Google Scholar] [CrossRef]

- Siddh, M.M.; Soni, G.; Jain, R. Perishable food supply chain quality (PFSCQ): A structured review and implications for future research. J. Adv. Manag. Res. 2018, 12, 292–313. [Google Scholar] [CrossRef]

- Mellat-Parast, M. Supply chain quality management. Int. J. Qual. Reliab. Manag. 2013, 30, 511–529. [Google Scholar] [CrossRef]

- Borodin, V.; Bourtembourg, J.; Hnaien, F.; Labadie, N. Handling uncertainty in agricultural supply chain management: A state of the art. Eur. J. Oper. Res. 2016, 254, 348–359. [Google Scholar] [CrossRef]

- Tsolakis, N.K.; Keramydas, C.A.; Toka, A.K.; Aidonis, D.A.; Iakovou, E.T. Agrifood supply chain management: A comprehensive hierarchical decision-making framework and a critical taxonomy. Biosyst. Eng. 2014, 120, 47–64. [Google Scholar] [CrossRef]

- Ahumada, O.; Villalobos, J.R. Application of planning models in the agri-food supply chain: A review. Eur. J. Oper. Res. 2009, 195, 1–20. [Google Scholar] [CrossRef]

- Rong, A.; Akkerman, R.; Grunow, M. An optimization approach for managing fresh food quality throughout the supply chain. Int. J. Prod. Econ. 2011, 131, 421–429. [Google Scholar] [CrossRef]

- Boudahri, F.; Bennekrouf, M.; Sari, Z. Optimization and design of the transportation network of agri-foods supply chain: Application chicken meat. Int. J. Adv. Eng. Sci. Technol. 2011, 11, 213–220. [Google Scholar] [CrossRef]

- Hobbs, J.E.; Young, L. Vertical linkages in Agri-Food Supply Chains in Canada and the United States; Research and Analysis Directorate Strategic Policy Branch Agriculture and Agri-Food Canada: Ottawa, Canada, 2001. [Google Scholar]

- Higgins, A.; Antony, G.; Sandell, G.; Davies, I.; Prestwidge, D.; Andrew, B. A framework for integrating a complex harvesting and transport system for sugar production. Agric. Syst. 2004, 82, 99–115. [Google Scholar] [CrossRef]

- Widodo, K.H.; Nagasawa, H.; Morizawa, K.; Ota, M. A periodical flowering-harvesting model for delivering agricultural fresh products. Eur. J. Oper. Res. 2006, 170, 24–43. [Google Scholar] [CrossRef]

- Salin, V. Information technology in agri-food supply chains. Int. Food Agribus. Manag. Rev. 1998, 1, 326–334. [Google Scholar] [CrossRef]

- van der Vorst, J.G.A.J. Product traceability in food-supply chains. Accredit. Qual. Assur. 2006, 11, 33–37. [Google Scholar] [CrossRef]

- Siddh, M.M.; Soni, G.; Jain, R.; Sharma, M.K. Structural model of perishable food supply chain quality (PFSCQ) to improve sustainable organizational performance. Benchmarking Int. J. 2018, 25, 2272–2317. [Google Scholar] [CrossRef]

- Rajeev, A.; Pati, R.K.; Padhi, S.S.; Govindan, K. Evolution of sustainability in supply chain management: A literature review. J. Clean. Prod. 2017, 162, 299–314. [Google Scholar] [CrossRef]

- Epperson, J.E.; Estes, E.A. Fruit and vegetable supply-chain management, innovations, and competitiveness: Cooperative Regional Research Project S-222. J. Food Distrib. 1999, 30, 38–43. [Google Scholar]

- Hobbs, J.E.; Young, L. Closer vertical co-ordination in agrifood supply chains: A conceptual framework and some preliminary evidence. Supply Chain Manag. Int. J. 2000, 5, 131–142. [Google Scholar] [CrossRef]

- Lusiantoro, L.; Yates, N.; Mena, C.; Varga, L. A refined framework of information sharing in perishable product supply chains. Int. J. Phys. Distrib. Logist. Manag. 2018, 48, 254–283. [Google Scholar]

- Palos-Sanchez, P.; Martin-Velicia, F.; Saura, J.R. Complexity in the Acceptance of Sustainable Search Engines on the Internet: An Analysis of Unobserved Heterogeneity with FIMIX-PLS. Complexity 2018, 1–19. [Google Scholar] [CrossRef]

- Stalk, G.; Hout, T.M. Competing Against Time: How Time-Based Competition Is Reshaping Global Markets; Free Press: New York, NY, USA, 1990. [Google Scholar]

- Galdeano-Gómez, E.; Céspedes-Lorente, J.; Martínez-del-Río, J. Environmental performance and spillover effects on productivity: Evidence from horticultural firms. J. Environ. Manag. 2008, 88, 1552–1561. [Google Scholar] [CrossRef]

- Deloitte. Global Powers of Retailing 2016: Navigating the New Digital Divide. Available online: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Consumer-Business/gx-cb-global-powers-of-retailing-2016.pdf (accessed on 22 June 2017).

- Serrano, M.; Pérez-Mesa, J.C.; Sánchez-Fernández, R. Product-country image and crises in the Spanish horticultural sector: Classification and impact on the market. Econ. Agrar. Recur. Nat. 2018, 18, 111–133. [Google Scholar]

- Pérez-Mesa, J.C.; Serrano, M.; Sánchez-Fernández, R. Measuring the impact of crises in the horticultural sector: The case of Spain. Br. Food J. 2019, 121, 1050–1063. [Google Scholar] [CrossRef]

- Brennen, B.S. Qualitative Research Methods for Media Studies; Routledge: New York, NY, USA, 2012. [Google Scholar]

- Jensen, K.B. The social origins and uses of media and communication research. In A Handbook of Media and Communication Research: Qualitative and Quantitative Methodologies, 2nd ed.; Jensen, K.B., Ed.; Routledge: London, UK, 2012; pp. 273–293. [Google Scholar]

- Saaty, T.L. Decision making with the analytic hierarchy process. Int. J. Serv. Sci. 2008, 1, 83–98. [Google Scholar] [CrossRef]

- Saaty, T.L. Fundamentals of Decision Making and Priority Theory with the Analytic Hierarchy Process; RWS Publications: Pittsburg, CA, USA, 2000. [Google Scholar]

- Fichtner, J. On deriving priority vectors from matrices of pairwise comparisons. Socio-Econ. Plan. Sci. 1986, 20, 341–345. [Google Scholar] [CrossRef]

- Easley, R.; Valacich, J.; Venkataramanan, M. Capturing group preferences in a multicriteria decision. Eur. J. Oper. Res. 2000, 125, 73–83. [Google Scholar] [CrossRef]

- Forman, E.; Peniwati, K. Aggregating individual judgments and priorities with the Analytic Hierarchy Process. Eur. J. Oper. Res. 1998, 108, 165–169. [Google Scholar] [CrossRef]

- Chan, S.H.; Kensinger, J.W.; Keown, A.J.; Martin, J.D. Do strategic alliances create value? J. Financ. Econ. 1997, 46, 199–221. [Google Scholar] [CrossRef]

- Van Beers, C.; Van der Panne, G. Geography, knowledge spillovers and small firms’ exports: An empirical examination for The Netherlands. Small Bus. Econ. 2011, 37, 325–339. [Google Scholar] [CrossRef][Green Version]

- Petersen, K.; Handfield, R.; Ragatz, G. Supplier integration into new product development: Coordinating product, process, and supply chain design. J. Oper. Manag. 2005, 23, 371–388. [Google Scholar] [CrossRef]

- Calof, J.L. The Relationship between Firm Size and Export Behavior Revisited. J. Int. Bus. Stud. 1994, 25, 367–387. [Google Scholar] [CrossRef]

- Piedra-Muñoz, L.; Galdeano-Gómez, E.; Pérez-Mesa, J.C. Is Sustainability Compatible with Profitability? An Empirical Analysis on Family Farming Activity. Sustainability 2016, 8, 893. [Google Scholar] [CrossRef]

- Egea, F.; Torrente, R.; Aguilar, A. An efficient agro-industrial complex in Almería (Spain): Towards an integrated and sustainable bioeconomy model. New Biotechnol. 2017, 40, 103–112. [Google Scholar] [CrossRef] [PubMed]

- Giagnocavo, C.; Galdeano-Gómez, E.; Pérez-Mesa, J.C. Cooperative Longevity and Sustainable Development in a Family Farming System. Sustainability 2018, 10, 2198. [Google Scholar] [CrossRef]

| Variables | R1 | R2 | … | R15 |

|---|---|---|---|---|

| R1 | a1,1 = 1 | a1,2 = (1/a2,1) | … | a1,15 = (1/a15,1) |

| R2 | a2,1 | a22k = 1 | … | a2,15 |

| … | 1 | |||

| R15 | a15,1 | a15,2 | … | a 15,1 = 1 |

| Coordination–Collaboration–Communication | ||

|---|---|---|

| Sustainability | Quality–Food Safety | |

| Production scheduling | Development of local economies:

| Promote sales of fresh products:

|

| Transportation | Use of intermodal transportation:

| Quality control of logistics providers:

|

| Facilities | Creation of supplier–customer distribution hubs:

| Product control at logistics centers:

|

| Variables | Profits | Profits/Sales |

|---|---|---|

| Constant | 80.208 | −11.859 |

| Production Scheduling–Sustainability () | 4.276 | 2.336 |

| Production Scheduling–Quality () | ** 19.100 | * 3.985 |

| Transport-Sustainability () | 2.385 | 0.557 |

| Transport Quality () | 8.020 | 1.386 |

| Facilities–Sustainability–Quality () | 7.902 | 2.079 |

| Assets | * 8.081 | * 2.610 |

| F-stat | *** 4.662 | *** 3.978 |

| R2 Adjusted | 0.343 | 0.310 |

| Farrar–Glauber | 6.240 | 8.340 |

| White Test | 8.121 | 9.339 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pérez-Mesa, J.C.; Piedra-Muñoz, L.; García-Barranco, M.C.; Giagnocavo, C. Response of Fresh Food Suppliers to Sustainable Supply Chain Management of Large European Retailers. Sustainability 2019, 11, 3885. https://doi.org/10.3390/su11143885

Pérez-Mesa JC, Piedra-Muñoz L, García-Barranco MC, Giagnocavo C. Response of Fresh Food Suppliers to Sustainable Supply Chain Management of Large European Retailers. Sustainability. 2019; 11(14):3885. https://doi.org/10.3390/su11143885

Chicago/Turabian StylePérez-Mesa, Juan Carlos, Laura Piedra-Muñoz, Mª Carmen García-Barranco, and Cynthia Giagnocavo. 2019. "Response of Fresh Food Suppliers to Sustainable Supply Chain Management of Large European Retailers" Sustainability 11, no. 14: 3885. https://doi.org/10.3390/su11143885

APA StylePérez-Mesa, J. C., Piedra-Muñoz, L., García-Barranco, M. C., & Giagnocavo, C. (2019). Response of Fresh Food Suppliers to Sustainable Supply Chain Management of Large European Retailers. Sustainability, 11(14), 3885. https://doi.org/10.3390/su11143885