An Exploration of Content and Drivers of Online Sustainability Disclosure: A Study of Italian Organisations

Abstract

1. Introduction

2. Materials and Methods

2.1. Measurement Framework

2.2. Sampling Procedure and Data Collection

2.3. Data Analysis

2.3.1. Development of New Metrics to Assess Sustainability Aspects Disclosed Online

2.3.2. Correlation Coefficients and Differences between Industry Groups

2.3.2.1. Contingent Variables

2.3.3. Cluster Analysis

3. Results

3.1. Type of Environmental and Social Information Disclosed by Organisations Online

3.2. Association between Organisation Characteristics (Industry Group, Organisational Size, Environmental and Social Certifications and Business Model) and Environmental and Social Information Disclosed Online

3.2.1. Correlation Coefficients and Differences between Industry Groups

3.2.2. Cluster Analysis

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Thematic Area/Indices | Indicator | |

|---|---|---|

| Environmental certification (EC) | Existence of: | |

| EC1 c | ISO 14001 | |

| EC2 c | EMAS | |

| EC3 c | ISO 50001 | |

| EC4 c | Ecolabels (e.g., FSC, Energy star, MSC, EU ecolabel) | |

| EC5 c | GOLDPOWER | |

| EC6 c | LEED | |

| Social certification (SC) | Existence of: | |

| SC1 c | SA 8000 | |

| SC2 c | ISO 26000 | |

| SC3 c | OHSAS 18001 | |

| SC4 c | IFS | |

| SC5 c | ISO 22005 | |

| SC6 c | ISO 22000 | |

| Business model (BM) | Development of products or technologies for: | |

| BM1 c | Renewable energy | |

| BM2 c | Water treatment, purification or to improve efficiency on water use | |

| BM3 c | Report or communication of initiatives to produce or promote organic food and other products | |

| BM4 c | Relation with nuclear energy industry (e.g., construction of reactors, production of nuclear energy) | |

| Energy (EE) | Existence of: | |

| EE1 | Eolic generator | |

| EE2 | Wind or water mill | |

| EE3 | Co-generation plant | |

| EE4 | Photovoltaic panels | |

| EE5 | Energy-saving lamps | |

| EE6 | Building envelope thermal insulation | |

| EE7 | Green roof | |

| EE8 | Actions planned for the next 5 years | |

| Corporate Social Responsibility (CSR) | CSR1 * | Statement or policy of equal opportunities |

| CSR2 * | Ethical code | |

| CSR3 * | Development of training policies/training for employees (beyond mandatory regulation) | |

| CSR4 * | Risk analysis policy for employees’ protection in the working environment | |

| CSR5 | Sustainability/environmental report | |

| CSR6 | Day-care service/flexible working hours | |

| CSR7 | Environmental impact assessment studies | |

| CSR8 | External audit for CSR/Health and Safety/sustainability report | |

| CSR9 | Appropriate internal communication tools (e.g., whistle-blower, ombudsman, suggestion box, hotline, newsletter, intranet) to ensure better environmental management | |

| CSR10 | Partnership or initiatives with specialized NGOs/industry organisations/governmental or supra-governmental organisations focused on improving environmental issues | |

| CSR11 | Actions planned for the next 5 years | |

| Emissions (EM) | Monitor of environmental impacts caused by: | |

| EI1 * | Air emissions | |

| EI2 * | Land emissions and spills | |

| EI3 * | Water emissions | |

| EI4 * | Identification of specific objectives to reduce emissions | |

| EI5 | Information disclosed about initiatives for environment restoration | |

| EI6 | Quantitative information provided to support the information disclosed | |

| Supply chain (SP) | SP1 * | Environmental and social criteria to select suppliers |

| SP2 * | Policy to reduce environmental impacts of the supply chain | |

| SP3 * | Description of the origin of the resources used and the origin of production (product transparency and “Made in Italy”) | |

| SP4 * | Communication policies to inform consumers about the sustainability of the products | |

| SP5 | Initiatives to reduce the environmental impact of transportation used for staff | |

| SP6 | Initiatives to reduce the environmental impact of the transportation of products | |

| SP7 | Initiatives to return used/old products | |

| Waste Management (WM) & Circular economy (CE) | WM1 * | Separated waste collection |

| WM2 * | Separated waste collection description | |

| WM3 | Reference to regulation | |

| CE1 * | Use of recycled materials in the manufacturing of the products | |

| CE2 * | Flawed product recycling | |

| CE3 | Waste as energy/heat source | |

| CE4 | Biodegradable packaging material | |

| CE5 | Packaging recovery and reuse | |

| WM3/CE6 | Actions planned for the next 5 years | |

| WM4/CE7 | Quantitative information provided to support the information disclosed | |

| Water (WA) | WA1 * | Treatment/purification/capture plant of wastewater |

| WA2 * | Treatment/purification/capture plant of rainwater | |

| WA3 * | Amount of re-used water | |

| WA4 | Actions planned for the next 5 years | |

| WA5 | Quantitative information provided to support the information disclosed | |

| Product innovation (PD) | PD1 * | Description of initiatives in place to reduce the energy footprint of products during the use phase |

| Environmental product innovation policy/initiative on: | ||

| PD2 * | Eco-design | |

| PD3 * | Life-cycle assessment | |

| PD4 | Dematerialisation | |

| PD5 PD6 | Description of new product techniques to minimize environmental impact (all emissions) during the production process Development of goods and services that improve energy efficiency of buildings | |

Appendix B

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Organisationa Characteristics | 1 | Revenue | 1 | |||||||||||

| 2 | N. employees | 0.2982 | 1 | |||||||||||

| Contingent Variables | 3 | Environmental certifications | 0.1765 | 0.2787 | 1 | |||||||||

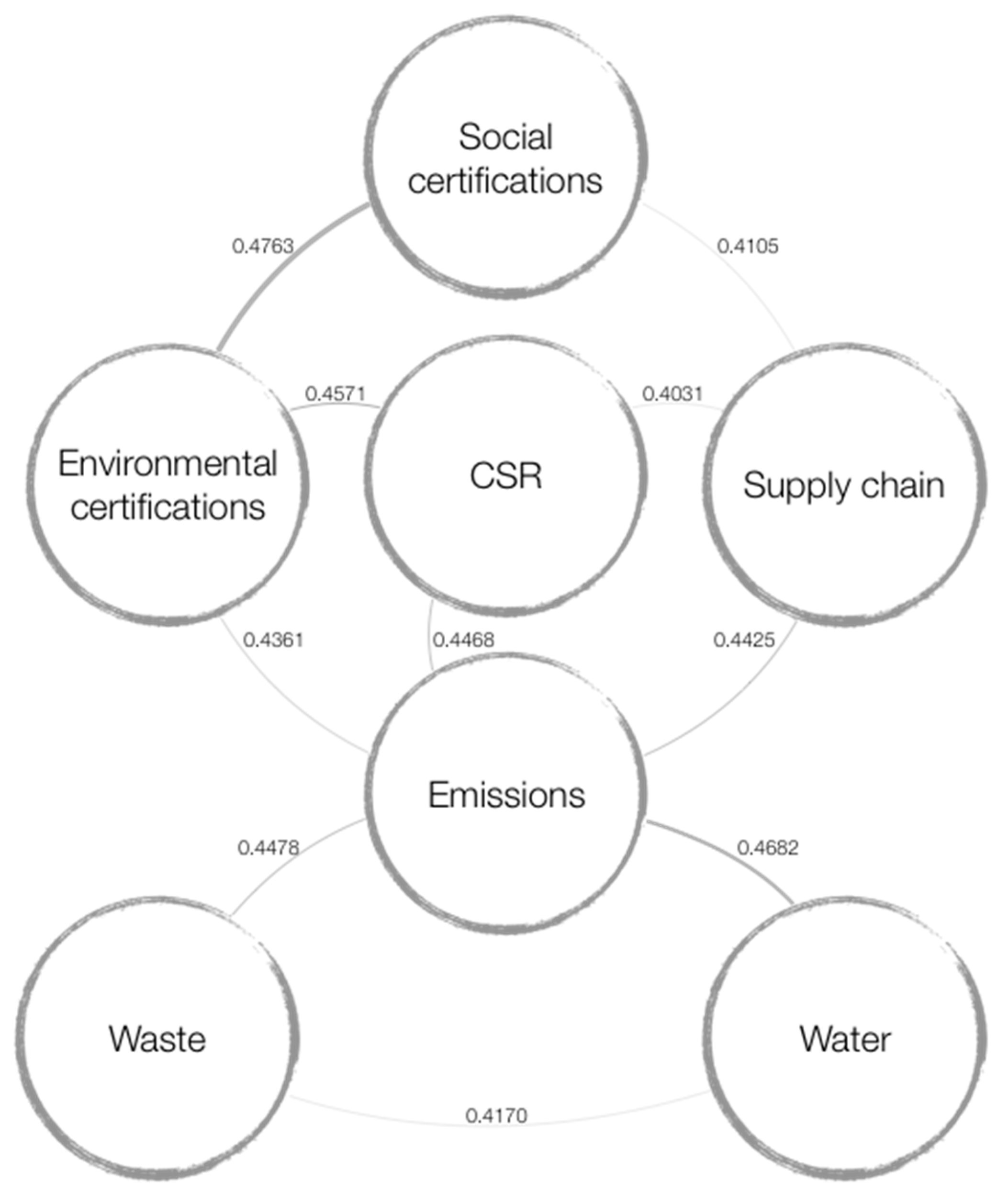

| 4 | Social certifications | 0.2321 | 0.1743 | 0.4763 | 1 | |||||||||

| 5 | Business model | 0.1195 | 0.0842 | 0.1555 | 0.2327 | 1 | ||||||||

| Thematic Areas | 6 | CSR | 0.2220 | 0.3180 | 0.4571 | 0.3790 | 0.1673 | 1 | ||||||

| 7 | Emissions | 0.2084 | 0.2136 | 0.4361 | 0.2917 | 0.1860 | 0.4468 | 1 | ||||||

| 8 | Supply chain | 0.2218 | 0.1549 | 0.3493 | 0.4105 | 0.2791 | 0.4031 | 0.4425 | 1 | |||||

| 9 | Waste Management | 0.0965 | 0.1422 | 0.3180 | 0.2090 | 0.0972 | 0.3095 | 0.4478 | 0.3359 | 1 | ||||

| 10 | Circular economy | 0.1251 | 0.1317 | 0.2623 | 0.1197 | 0.0627 | 0.2393 | 0.3947 | 0.2855 | 0.3234 | 1 | |||

| 11 | Water | 0.1807 | 0.1339 | 0.3300 | 0.2213 | 0.1671 | 0.2784 | 0.4682 | 0.3475 | 0.4170 | 0.3455 | 1 | ||

| 12 | Product innovation | 0.1709 | 0.1844 | 0.2997 | 0.2085 | 0.2287 | 0.2579 | 0.3746 | 0.3433 | 0.2000 | 0.2862 | 0.2800 | 1 |

References

- Siew, R.Y.J. A review of corporate sustainability reporting tools (SRTs). J. Environ. Manag. 2015, 164, 180–195. [Google Scholar] [CrossRef] [PubMed]

- Domingues, A.R.; Lozano, R.; Ceulemans, K.; Ramos, T.B. Sustainability reporting in public sector organisations: Exploring the relation between the reporting process and organisational change management for sustainability. J. Environ. Manag. 2017, 192, 292–301. [Google Scholar] [CrossRef] [PubMed]

- Farneti, F.; Guthrie, J. Sustainability reporting by Australian public sector organisations: Why they report. Acc. Forum 2009, 33, 89–98. [Google Scholar] [CrossRef]

- Directive 2014/95/EU of the European Parliament and of the Council Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups; EU: Brussels, Belgium, 2014.

- Haddock-Fraser, J. The Role of the News Media in Influencing Corporate Environmental Sustainable Development: An Alternative Methodology to Assess Stakeholder Engagement. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 327–342. [Google Scholar] [CrossRef]

- Lodhia, S.; Stone, G. Integrated Reporting in an Internet and Social Media Communication Environment: Conceptual Insights. Aust. Acc. Rev. 2017, 27, 17–33. [Google Scholar] [CrossRef]

- Isenmann, R.; Bey, C.; Welter, M. Online reporting for sustainability issues. Bus. Strategy Environ. 2007, 16, 487–501. [Google Scholar] [CrossRef]

- de Lancer Julnes, P. Performance Measurement Beyond Instrumental Use. In Performance Information in the Public Sector How It Is Used; Van Dooren, W., Van de Walle, S., Eds.; Palgrave Macmillan: Basingstoke, UK, 2011. [Google Scholar]

- Isenmann, R.; Ki-Cheol, K. Interactive Sustainability Reporting: Developing Clear Target Group Tailoring and Stimulating Stakeholder Dialogue. In Sustainability Accounting and Reporting; Schaltegger, S., Bennett, M., Burritt, R., Eds.; Springer: Berlin/Heidelberg, Germany, 2006; pp. 533–537. [Google Scholar]

- Manetti, G.; Bellucci, M.; Bagnoli, L. Stakeholder Engagement and Public Information Through Social Media: A Study of Canadian and American Public Transportation Agencies. Am. Rev. Public Adm. 2016, 47, 991–1009. [Google Scholar] [CrossRef]

- Deegan, C. Organisational Legitimacy as a Motive for Sustainability Reporting. In Sustainability Accounting and Accountability; Unerman, J., Bebbington, J., O’Dwyer, B., Eds.; Routledge (Taylor & Francis Group): London, UK, 2007; pp. 127–149. [Google Scholar]

- Cormier, D.; Magnan, M. The Economic Relevance of Environmental Disclosure and its Impact on Corporate Legitimacy: An Empirical Investigation. Bus. Strategy Environ. 2013, 24, 431–450. [Google Scholar] [CrossRef]

- Bebbington, J.; Higgins, C.; Frame, B. Initiating sustainable development reporting: Evidence from New Zealand. Acc. Audit. Account. J. 2009, 22, 588–625. [Google Scholar] [CrossRef]

- Herzig, C.; Schaltegger, S. Corporate sustainability reporting: An overview. In Sustainability Accounting and Reporting; Schaltegger, S., Bennett, M., Burritt, R., Eds.; Springer: Berlin/Heidelberg, Germany, 2006; pp. 301–324. [Google Scholar]

- Amran, A.; Ooi, S.K. Sustainability reporting: Meeting stakeholder demands. Strateg. Dir. 2014, 30, 38–41. [Google Scholar] [CrossRef]

- Lozano, R.; Nummert, B.; Ceulemans, K. Elucidating the relationship between Sustainability Reporting and Organisational Change Management for Sustainability. J. Clean. Prod. 2016, 125, 168–188. [Google Scholar] [CrossRef]

- Ceulemans, K.; Lozano, R.; Alonso-Almeida, M. Sustainability Reporting in Higher Education: Interconnecting the Reporting Process and Organisational Change Management for Sustainability. Sustainability 2015, 7, 8881–8903. [Google Scholar] [CrossRef]

- Mura, M.; Longo, M.; Micheli, P.; Bolzani, D. The Evolution of Sustainability Measurement Research. Int. J. Manag. Rev. 2018, 20, 661–695. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational Legitimacy: Social Values and Organizational Behavior. Pac. Sociol. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- da Silva Monteiro, S.M.; Aibar-Guzmán, B. Determinants of environmental disclosure in the annual reports of large companies operating in Portugal. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 185–204. [Google Scholar] [CrossRef]

- Castelo Branco, M.; Lima Rodrigues, L. Communication of corporate social responsibility by Portuguese banks. Corp. Commun. Int. J. 2006, 11, 232–248. [Google Scholar] [CrossRef]

- Tagesson, T.; Blank, V.; Broberg, P.; Collin, S.-O. What explains the extent and content of social and environmental disclosures on corporate websites: A study of social and environmental reporting in Swedish listed corporations. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 352–364. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M.; Van Velthoven, B. Environmental disclosure quality in large German companies: Economic incentives, public pressures or institutional conditions? Eur. Acc. Rev. 2005, 14, 3–39. [Google Scholar] [CrossRef]

- Gallego-Alvarez, I.; Ortas, E.; Vicente-Villardón, J.L.; Álvarez Etxeberria, I. Institutional Constraints, Stakeholder Pressure and Corporate Environmental Reporting Policies. Bus. Strategy Environ. 2017, 26, 807–825. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hörisch, J.; Freeman, R.E. Business Cases for Sustainability: A Stakeholder Theory Perspective. Org. Environ. 2017, 1–22. [Google Scholar] [CrossRef]

- Lüdeke-Freund, F.; Carroux, S.; Joyce, A.; Massa, L.; Breuer, H. The sustainable business model pattern taxonomy—45 patterns to support sustainability-oriented business model innovation. Sustain. Prod. Consum. 2018, 15, 145–162. [Google Scholar] [CrossRef]

- Bocken, N.M.P.; Short, S.W.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Allee, V. Reconfiguring the value network. J. Bus. Strategy 2000, 21, 36–39. [Google Scholar] [CrossRef]

- Rosati, F.; Faria, L.G.D. Business contribution to the Sustainable Development Agenda: Organizational factors related to early adoption of SDG reporting. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 588–597. [Google Scholar] [CrossRef]

- Del Mar Alonso-Almeida, M.; Llach, J.; Marimon, F. A Closer Look at the “Global Reporting Initiative” Sustainability Reporting as a Tool to Implement Environmental and Social Policies: A Worldwide Sector Analysis. Corp. Soc. Responsib. Environ. Manag. 2013, 21, 318–335. [Google Scholar] [CrossRef]

- De Villiers, C.; van Staden, C.J. Where firms choose to disclose voluntary environmental information. J. Acc. Public Policy 2011, 30, 504–525. [Google Scholar] [CrossRef]

- Tang, S.; Demeritt, D. Climate Change and Mandatory Carbon Reporting: Impacts on Business Process and Performance. Bus. Strategy Environ. 2018, 27, 437–455. [Google Scholar] [CrossRef]

- Hörisch, J.; Freeman, R.E.; Schaltegger, S. Applying Stakeholder Theory in Sustainability Management. Org. Environ. 2014, 27, 328–346. [Google Scholar] [CrossRef]

- Elkington, J. Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development. Calif. Manag. Rev. 1994, 36, 90–101. [Google Scholar] [CrossRef]

- De Villiers, C. Stakeholder Requirements for Sustainability Reporting. In Sustainability Accounting and Accountability; De Villiers, C., Maroun, W., Eds.; Routledge, Taylor & Francis Group: London, UK, 2018. [Google Scholar]

- Hahn, R.; Kühnen, M. Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized Organizations: Formal Structure as Myth and Ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef]

- Herremans, I.M.; Herschovis, M.S.; Bertels, S. Leaders and Laggards: The Influence of Competing Logics on Corporate Environmental Action. J. Bus. Ethics 2009, 89, 449–472. [Google Scholar] [CrossRef]

- Roca, L.C.; Searcy, C. An analysis of indicators disclosed in corporate sustainability reports. J. Clean. Prod. 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones Sustainability Index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Daddi, T.; Todaro, N.M.; De Giacomo, M.R.; Frey, M. A Systematic Review of the Use of Organization and Management Theories in Climate Change Studies. Bus. Strategy Environ. 2018, 27, 456–474. [Google Scholar] [CrossRef]

- van Dijk, B. Aida: Italian Company Information and Business Intelligence. Available online: https://www.bvdinfo.com/en-apac/our-products/company-information/national-products/aida (accessed on 26 February 2018).

- OECD. OECD Regions and Cities at a Glance 2018; OECD Publishing: Paris, France, 2018. [Google Scholar]

- Eurostat. Gross Domestic Product (GDP) at Current Market Prices by NUTS II Regions. Available online: http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=nama_10r_2gdp&lang=en (accessed on 16 November 2018).

- Regione Emilia-Romagna, Servizio Statistica e Informazione Geografica. Le Specializzazioni Produttive Regionali Attraverso I Censimenti Industria e Servizi 2001 e 2011 (Regional Production Census Industry and Services 2001 and 2011). Available online: http://statistica.regione.emilia-romagna.it/allegati/pubbl/2014/le-specializzazioni-produttive-regionali-attraverso-i-censimenti-industria-e-servizi-2001-e-2011 (accessed on 16 November 2018).

- Baines, T.S.; Lightfoot, H.W.; Evans, S.; Neely, A.; Greenough, R.; Peppard, J.; Roy, R.; Shehab, E.; Braganza, A.; Tiwari, A.; et al. State-of-the-art in product-service systems. Proc. Inst. Mech. Eng. Part B J. Eng. Manuf. 2007, 221, 1543–1552. [Google Scholar] [CrossRef]

- Kowalkowski, C.; Gebaue, C.; Oliva, R. Service growth in product firms: Past, present, and future. Ind. Mark. Manag. 2017, 60, 82–88. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Pearson: London, UK, 2004. [Google Scholar]

- Gangi, F.; Meles, A.; Monferrà, S.; Mustilli, M. Does corporate social responsibility help the survivorship of SMEs and large firms? Glob. Finance J. 2018, in press. [Google Scholar] [CrossRef]

- Guimarães-Costa, N.; e Cunha, M.P. The atrium effect of website openness on the communication of corporate social responsibility. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 43–51. [Google Scholar] [CrossRef]

- Kraft, M.E.; Stephan, M.; Abel, T.D. Coming Clean: Information Disclosure and Environmental Performance; The MIT Press: Cambridge, MA, USA, 2011. [Google Scholar]

- Semenova, N.; Hassel, L.G.; Nilsson, H. The value relevance of environmental and social performance: Evidence from Swedish SIX 300 companies. Liiketal. Aikak. 2010, 3, 265–292. [Google Scholar]

- Darnall, N.; Henriques, I.; Sadorsky, P. Adopting Proactive Environmental Strategy: The Influence of Stakeholders and Firm Size. J. Manag. Stud. 2010, 47, 1072–1094. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R. Business Cases and Corporate Engagement with Sustainability: Differentiating Ethical Motivations. J. Bus. Ethics 2015, 147, 241–259. [Google Scholar] [CrossRef]

- Manetti, G.; Bellucci, M. The use of social media for engaging stakeholders in sustainability reporting. Acc. Audit. Account. J. 2016, 29, 985–1011. [Google Scholar] [CrossRef]

- Ramos, T.B.; Martins, I.P.; Martinho, A.P.; Douglas, C.H.; Painho, M.; Caeiro, S. An open participatory conceptual framework to support State of the Environment and Sustainability Reports. J. Clean. Prod. 2014, 64, 158–172. [Google Scholar] [CrossRef]

| Industry Group | Total Number (Percentage) | Geographical Distribution (Percentage) |

|---|---|---|

| #1. Food industry | 365 (18%) | Emilia-Romagna (33%) Lombardy (34%) Piedmont (14%) Veneto (19%) |

| #2. Textile industry | 25 (1%) | Tuscany (100%) |

| #3. Manufacturing of leather and similar products | 85(4%) | Tuscany (47%) Veneto (53%) |

| #4. Manufacturing of paper and products derived from paper | 20 (1%) | Tuscany (100%) |

| #5. Manufacturing of chemical products | 155 (8%) | Lombardy (100%) |

| #6. Manufacturing of rubber and plastic materials | 40 (2%) | Piedmont (100%) |

| #7. Manufacturing of other products to produce non-metallic minerals | 40 (2%) | Emilia-Romagna (100%) |

| #8. Metallurgy | 180 (9%) | Lombardy (81%) Tuscany (19%) |

| #9. Manufacturing of metal products (excluding machinery and equipment) | 329 (16%) | Emilia-Romagna (15%) Lombardy (47%) Piedmont (15%) Veneto (23%) |

| #10. Manufacturing of electrical equipment and equipment for domestic non-electrical use | 30 (1%) | Veneto (100%) |

| #11. Manufacturing of machinery and other equipment | 509 (25%) | Emilia-Romagna (24%) Lombardy (35%) Piedmont (14%) Tuscany (12%) Veneto (16%) |

| #12. Manufacturing of vehicles, trailers and semi-trailers | 230 (11%) | Emilia-Romagna (17%) Piedmont (83%) |

| Factor Loadings | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Thematic Areas/Indices | Indicator | CSR | EM | SP | WM | CE | WA | PD | |

| Corporate Social Responsibility (CSR) | CSR1 | Statement or policy of equal opportunities | 0.91 | ||||||

| CSR2 | Ethical code | 0.95 | |||||||

| CSR3 | Development of training policies / training for employees (beyond mandatory regulation) | 0.50 | |||||||

| CSR4 | Risk analysis policy for employees’ protection in the working environment | 0.70 | |||||||

| Emissions (EM) | Monitor of environmental impacts caused by: | ||||||||

| EI1 | Air emissions | 0.45 | |||||||

| EI2 | Land emissions and spills | 0.97 | |||||||

| EI3 | Water emissions | 0.95 | |||||||

| EI4 | Identification of specific objectives to reduce emissions | 0.29 | |||||||

| Supply chain (SP) | SP1 | Environmental and social criteria to select suppliers | 0.54 | ||||||

| SP2 | Policy to reduce environmental impacts of the supply chain | 0.77 | |||||||

| SP3 | Description of the origin of the resources used and the origin of production (product transparency and “Made in Italy”) | 0.64 | |||||||

| SP4 | Communication policies to inform consumers about the sustainability of the products | 0.70 | |||||||

| Waste Management (WM) | WM1 | Separated waste collection | 0.92 | ||||||

| WM2 | Separated waste collection description | 0.68 | |||||||

| Circular economy (CE) | CE1 | Use of recycled materials in the manufacturing of the products | 0.89 | ||||||

| CE2 | Flawed product recycling | 0.60 | |||||||

| Water (WA) | WA1 | Treatment/purification/capture plant of wastewater | 0.56 | ||||||

| WA2 | Treatment/purification/capture plant of rainwater | 0.39 | |||||||

| WA3 | Amount of re-used water | 0.84 | |||||||

| Product innovation (PD) | PD1 | Description of initiatives in place to reduce the energy footprint of products during the use phase | 0.61 | ||||||

| Environmental product innovation policy/initiative on: | |||||||||

| PD2 | Eco-design | 0.61 | |||||||

| PD3 | Life-cycle assessment | 0.39 | |||||||

| Thematic Areas/Indices | Indicator | |

|---|---|---|

| Environmental certification (EC) | Existence of: | |

| EC1 | ISO 14001 | |

| EC2 | EMAS | |

| EC3 | ISO 50001 | |

| EC4 | Ecolabels (e.g., FSC, Energy star, MSC, EU ecolabel) | |

| EC5 | GOLDPOWER | |

| EC6 | LEED | |

| Social certification (SC) | Existence of: | |

| SC1 | SA 8000 | |

| SC2 | ISO 26000 | |

| SC3 | OHSAS 18001 | |

| SC4 | IFS | |

| SC5 | ISO 22005 | |

| SC6 | ISO 22000 | |

| Business model (BM) | Development of products or technologies for: | |

| BM1 | Renewable energy | |

| BM2 | Water treatment, purification or to improve efficiency on water use | |

| BM3 | Report or communication of initiatives to produce or promote organic food and other products | |

| BM4 | Relation with nuclear energy industry (e.g., construction of reactors, production of nuclear energy) | |

| Thematic Area | χ2 (11) |

|---|---|

| CSR | 46.446 |

| EM | 85.411 |

| SP | 369.846 |

| WM | 79.213 |

| WA | 204.853 |

| CE | 203.568 |

| PD | 112.209 |

| Cluster | CSR | EM | SP | WM | CE | WA | PD | Number of Organisations |

|---|---|---|---|---|---|---|---|---|

| A | 2.143 (0.76) | 2.328 (1.00) | 1.617 (1.00) | 0.684 (1.00) | 0.511 (1.00) | 0.563 (1.00) | 0.423 (1.00) | 144 |

| B | 1.698 (0.60) | 0.143 (0.06) | 0.188 (0.12) | 0.054 (0.08) | 0.087 (0.17) | 0.026 (0.05) | 0.055 (0.13) | 231 |

| C | 2.831 (1.00) | 0.239 (0.10) | 1.049 (0.65) | 0.207 (0.30) | 0.164 (0.32) | 0.107 (0.19) | 0.170 (0.40) | 241 |

| D | 0.186 (0.07) | 0.133 (0.06) | 1.081 (0.67) | 0.108 (0.16) | 0.132 (0.26) | 0.093 (0.17) | 0.106 (0.25) | 383 |

| E | 0.043 (0.02) | 0.032 (0.01) | 0.007 (0.00) | 0.017 (0.02) | 0.030 (0.06) | 0.007 (0.01) | 0.023 (0.05) | 1009 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mura, M.; Longo, M.; Domingues, A.R.; Zanni, S. An Exploration of Content and Drivers of Online Sustainability Disclosure: A Study of Italian Organisations. Sustainability 2019, 11, 3422. https://doi.org/10.3390/su11123422

Mura M, Longo M, Domingues AR, Zanni S. An Exploration of Content and Drivers of Online Sustainability Disclosure: A Study of Italian Organisations. Sustainability. 2019; 11(12):3422. https://doi.org/10.3390/su11123422

Chicago/Turabian StyleMura, Matteo, Mariolina Longo, Ana Rita Domingues, and Sara Zanni. 2019. "An Exploration of Content and Drivers of Online Sustainability Disclosure: A Study of Italian Organisations" Sustainability 11, no. 12: 3422. https://doi.org/10.3390/su11123422

APA StyleMura, M., Longo, M., Domingues, A. R., & Zanni, S. (2019). An Exploration of Content and Drivers of Online Sustainability Disclosure: A Study of Italian Organisations. Sustainability, 11(12), 3422. https://doi.org/10.3390/su11123422