Business Ethics as a Sustainability Challenge: Higher Education Implications

Abstract

1. Introduction

- In ethics-unfriendly environments, do ethics/CSR courses increase business students’ ethical awareness, in terms of their perceived importance of (i) general aspects of ethics and (ii) objectives of accounting education?

- In ethics-unfriendly environments, do gender and age of business students moderate the impact of ethics/CSR courses on business students’ ethical awareness, in terms of their perceived importance of (i) general aspects of ethics and (ii) objectives of accounting education?

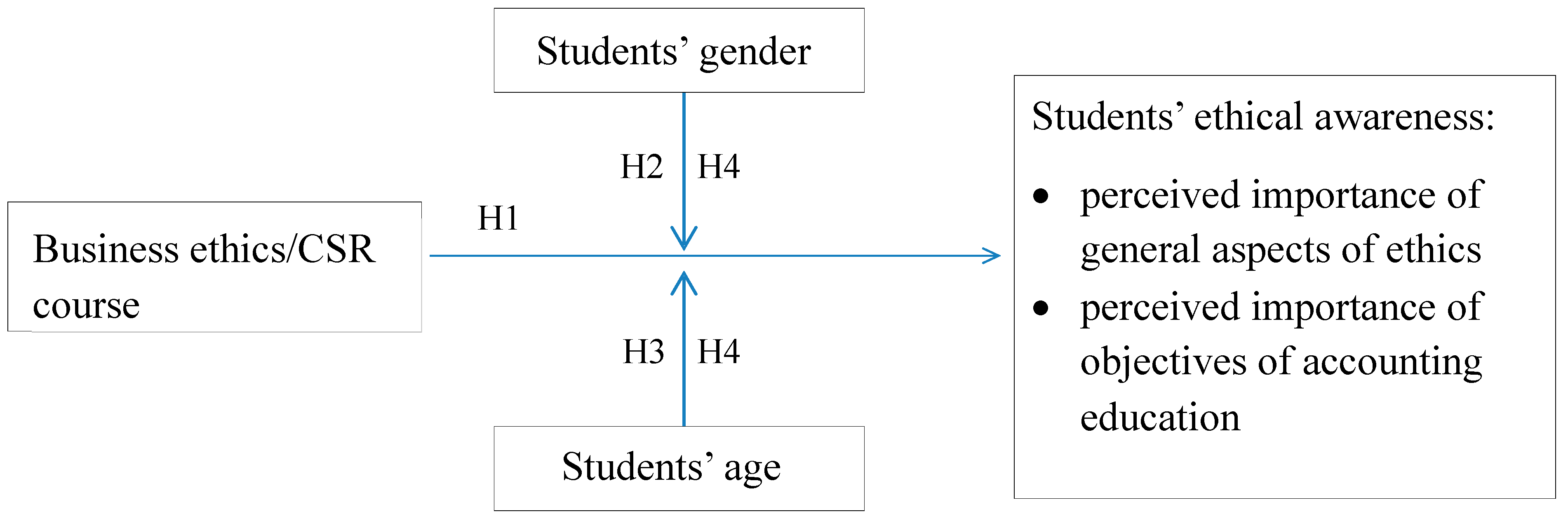

2. Literature Review and Hypotheses

2.1. Business Ethics and CSR Courses, Business Ethics Education Effectiveness, and Business Students’ Ethical Awareness

2.2. The Moderating Effect of Business Students’ Gender and Age on the Effectiveness of Business Ethics Education

3. Methodology

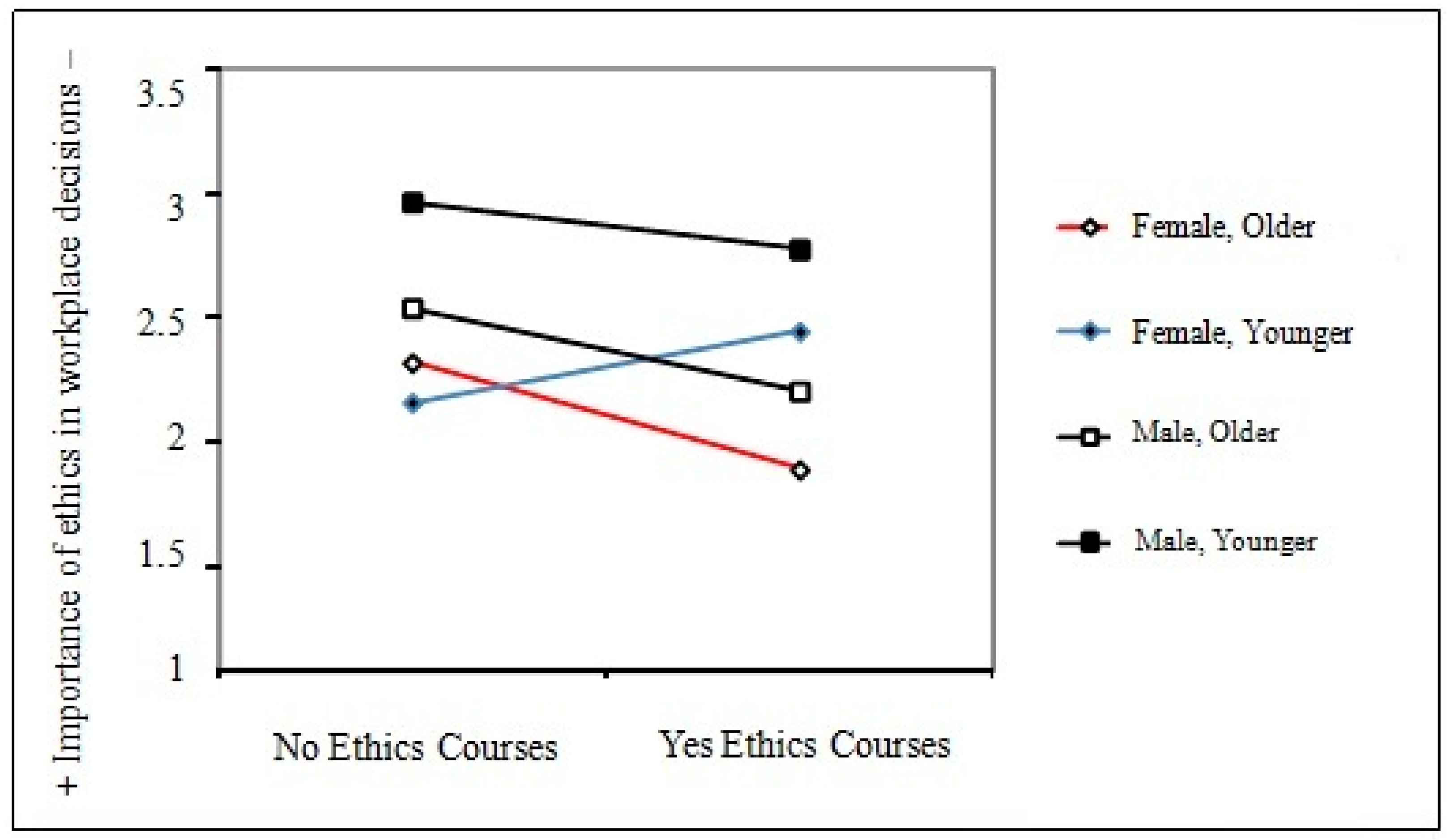

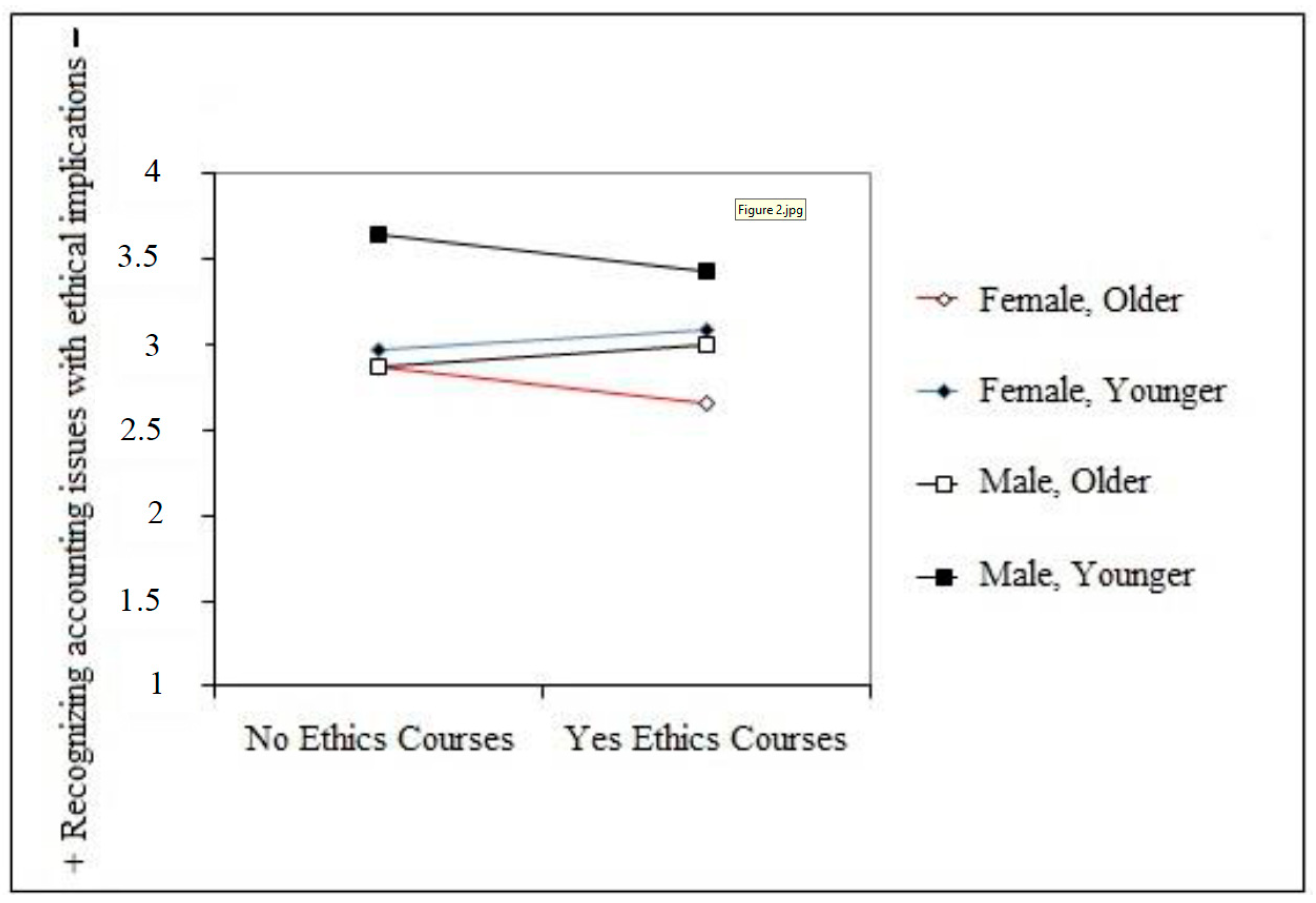

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

References

- Pauw, J.B.-D.; Gericke, N.; Olsson, D.; Berglund, T. The Effectiveness of Education for Sustainable Development. Sustainability 2015, 7, 15693–15717. [Google Scholar] [CrossRef]

- Setó-Pamies, D.; Papaoikonomou, E. A Multi-level Perspective for the Integration of Ethics, Corporate Social Responsibility and Sustainability (ECSRS) in Management Education. J. Bus. Ethics 2015. [Google Scholar] [CrossRef]

- Bergman, M.M.; Bergman, Z.; Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 2017, 9, 753. [Google Scholar] [CrossRef]

- Burford, G.; Hoover, E.; Velasco, I.; Janoušková, S.; Jimenez, A.; Piggot, G.; Podger, D.; Harder, M.K. Bringing the ‘missing pillar’ into Sustainable Development Goals: Towards intersubjective values-based indicators. Sustainability 2013, 5, 3035–3059. [Google Scholar] [CrossRef]

- Burford, G.; Hoover, E.; Stapleton, L.; Harder, M.K. An Unexpected Means of Embedding Ethics in Organizations: Preliminary Findings from Values-Based Evaluations. Sustainability 2016, 8, 612. [Google Scholar] [CrossRef]

- Bampton, R.; Cowton, C.J. The teaching of ethics in management accounting: Progress and prospects. Bus. Ethics Eur. Rev. 2002, 11, 52–61. [Google Scholar] [CrossRef]

- Biedenweg, K.; Monroe, M.C.; Oxarart, A. The importance of teaching ethics of sustainability. Int. J. Sust. Higher Educ. 2013, 14, 6–14. [Google Scholar] [CrossRef]

- Harris, H. Promoting ethical reflection in the teaching of business ethics. Bus. Ethics Eur. Rev. 2008, 17, 379–390. [Google Scholar] [CrossRef]

- Larrán Jorge, M.; Andrades Peña, F.J. Determinants of corporate social responsibility and business ethics education in Spanish universities. Bus. Ethics Eur. Rev. 2014, 23, 139–153. [Google Scholar] [CrossRef]

- Loeb, S.E. Teaching students accounting ethics: Some crucial issues. Issues Account. Educ. 1988, 3, 316–329. [Google Scholar]

- Maclagan, P. Conflicting obligations, moral dilemmas and the development of judgement through business ethics education. Bus. Ethics Eur. Rev. 2012, 21, 183–197. [Google Scholar] [CrossRef]

- Maclagan, P.; Campbell, T. Focusing on individuals’ ethical judgement in corporate social responsibility curricula. Bus. Ethics Eur. Rev. 2011, 20, 392–404. [Google Scholar] [CrossRef]

- Marnburg, E. Educational impacts on academic business practitioner’s moral reasoning and behaviour: Effects of short courses in ethics or philosophy. Bus. Ethics Eur. Rev. 2003, 12, 403–413. [Google Scholar] [CrossRef]

- Tormo-Carbó, G.; Seguí-Mas, E.; Oltra, V. Accounting ethics in unfriendly environments: The educational challenge. J. Bus. Ethics 2014. [Google Scholar] [CrossRef]

- Bampton, R.; Cowton, C.J. Taking stock of accounting ethics scholarship: A review of the journal literature. J. Bus. Ethics 2013, 114, 549–563. [Google Scholar] [CrossRef]

- Lee, B.K.; Sohn, S.Y. A Credit Scoring Model for SMEs Based on Accounting Ethics. Sustainability 2017, 9, 15–88. [Google Scholar] [CrossRef]

- Ceulemans, K.; Lozano, R.; Alonso-Almeida, M.M. Sustainability reporting in higher education: Interconnecting the Reporting Process and Organisational Change Management for Sustainability. Sustainability 2015, 7, 8881–8903. [Google Scholar] [CrossRef]

- Sammalisto, K.; Sundström, A.; von Haartman, R.; Holm, T.; Yao, Z. Learning about Sustainability—What Influences Students’ Self-Perceived Sustainability Actions after Undergraduate Education? Sustainability 2016, 8, 510. [Google Scholar] [CrossRef]

- Boni, A.; Lozano, J.F. The generic competences: An opportunity for ethical learning in the European convergence in higher education. High. Educ. 2007, 54, 819–831. [Google Scholar] [CrossRef]

- Sánchez, R.G.; Bolívar, M.P.R.; Hernández, A.M.L. Are Australian Universities Making Good Use of ICT for CSR Reporting? Sustainability 2015, 7, 14895–14916. [Google Scholar] [CrossRef]

- Uysal, O.O. Business ethics research with an accounting focus: A bibliometric analysis from 1988 to 2007. J. Bus. Ethics 2010, 93, 137–160. [Google Scholar] [CrossRef]

- CRUE. La Universidad Española en Cifras 2015/2016. Available online: http://www.crue.org/Documentos%20compartidos/Publicaciones/Universidad%20Espa%C3%B1ola%20en%20cifras/UEC_Digital_WEB.pdf (accessed on 18 May 2018).

- Randstad. Ingeniería Industrial, ADE e Informática son las Carreras con Mejores Perspectivas Laborales en España. 2014. Available online: http://www.randstad.es/nosotros/sala-prensa/randstad-17-09-2014 (accessed on 5 May 2015).

- Setó-Pamies, D.; Domingo-Vernis, M.; Rabassa-Figueras, N. Corporate social responsibility in management education: Current status in Spanish universities. J. Health Organ. Manag. 2011, 17, 604–620. [Google Scholar] [CrossRef]

- Garavan, T.N.; McGuire, D. Human resource development and society: Human resource development’s role in embedding corporate social responsibility, sustainability, and ethics in organizations. Adv. Dev. Hum. Resour. 2010, 12, 487–507. [Google Scholar] [CrossRef]

- Donaldson, T.; Dunfee, T.W. Towards a unified conception of business ethics: Integrative social contracts theory. Acad. Manag. Rev. 1994, 19, 252–284. [Google Scholar] [CrossRef]

- BBC. Rato and Other Bankia Officials Face Fraud Probe. BBC News. 4 July 2012. Available online: http://www.bbc.co.uk/news/business-18705836 (accessed on 24 April 2015).

- Kassam, A. Spanish authorities arrest 51 top figures in anti-corruption sweep. The Guardian. 27 October 2014. Available online: http://www.theguardian.com/world/2014/oct/27/spanish-authorities-arrest-51-anti-corruption-sweep (accessed on 5 May 2015).

- Gallego-Alvarez, I. Analysis of social information as a measure of the ethical behaviour of Spanish firms. Manag. Decis. 2008, 46, 580–599. [Google Scholar] [CrossRef]

- Dellaportas, S.; Cooper, B.J.; Leung, P. Measuring moral judgement and the implications of cooperative education and rule-based learning. Account. Financ. 2006, 46, 53–70. [Google Scholar] [CrossRef]

- Graham, A. The teaching of ethics in undergraduate accounting programmes: The students’ perspective. Account. Educ. 2012, 21, 599–613. [Google Scholar] [CrossRef]

- Waples, E.P.; Antes, A.L.; Murphy, S.T.; Connelly, S.; Mumford, M.D. A meta-analytic investigation of business ethics instruction. J. Bus. Ethics 2009, 87, 133–151. [Google Scholar] [CrossRef]

- Watts, L.L.; Mulhearn, T.J.; Medeiros, K.E.; Steele, L.M.; Connelly, S.; Mumford, M.D. Modeling the instructional effectiveness of responsible conduct of research education: A meta-analytic path-analysis. Ethics Behav. 2017, 27, 632–650. [Google Scholar] [CrossRef]

- Loeb, S.E. Active learning: An advantageous yet challenging approach to accounting ethics instruction. J. Bus. Ethics 2015, 127, 221–230. [Google Scholar] [CrossRef]

- Adkins, N.; Radtke, R.R. Students’ and faculty members’ perceptions of the importance of business ethics and accounting ethics education: Is there an expectations gap? J. Bus. Ethics 2004, 51, 279–300. [Google Scholar] [CrossRef]

- Bampton, R.; Maclagan, P. Why teach ethics to accounting students? A response to the sceptics. Bus. Ethics Eur. Rev. 2005, 14, 290–300. [Google Scholar] [CrossRef]

- Ferguson, J.; Collison, D.; Power, D.; Stevenson, L. Accounting education, socialisation and the ethics of business. Bus. Ethics Eur. Rev. 2011, 20, 12–29. [Google Scholar] [CrossRef]

- Neureuther, B.D.; Swicegood, P.; Williams, P. The efficacy of business ethics courses when coupled with a personal belief system. J. Coll. Teach. Learn. 2011, 1, 17–22. [Google Scholar] [CrossRef]

- Low, M.; Davey, H.; Hooper, K. Accounting scandals, ethical dilemmas and educational challenges. Crit. Perspect. Accoun. 2008, 19, 222–254. [Google Scholar] [CrossRef]

- Dearman, D.; Beard, J. Ethical Issues in Accounting and Economics Experimental Research: Inducing Strategic Misrepresentation. Ethics Behav. 2009, 19, 51–59. [Google Scholar] [CrossRef]

- O’Fallon, M.J.; Butterfield, K.D. A review of the empirical ethical decision-making literature: 1996–2003. J. Bus. Ethics 2005, 59, 375–423. [Google Scholar] [CrossRef]

- Ritter, B.A. Can business ethics be trained? A study of the ethical decision-making process in business students. J. Bus. Ethics 2006, 68, 153–164. [Google Scholar] [CrossRef]

- Nguyen, N.T.; Basuray, M.T.; Smith, W.P.; Kopka, D.; McCulloh, D. Moral issues and gender differences in ethical judgement using Reidenbach and Robin’s (1990) multidimensional ethics scale: Implications in teaching of business ethics. J. Bus. Ethics 2008, 77, 417–430. [Google Scholar] [CrossRef]

- Eagly, A.H. Sex Differences in Social Behaviour: A Social-Role Interpretation; Erlbaum: Hillsdale, NJ, USA, 1987. [Google Scholar]

- Eagly, A.H.; Steffen, V.J. Gender stereotypes stem from the distribution of women and men into social roles. J. Pers. Soc. Psychol. 1984, 46, 735–754. [Google Scholar] [CrossRef]

- Pan, Y.; Sparks, J.R. Predictors, consequence, and measurement of ethical judgments: Review and meta-analysis. J. Bus. Res. 2012, 65, 84–91. [Google Scholar] [CrossRef]

- Tenbrunsel, A.E.; Smith-Crowe, K. Ethical decision making: Where we’ve been and where we’re going. Acad. Manag. Ann. 2008, 2, 545–607. [Google Scholar] [CrossRef]

- Craft, J.L. A review of the empirical ethical decision-making literature: 2004–2011. J. Bus. Ethics 2013, 117, 221–259. [Google Scholar] [CrossRef]

- McCabe, A.C.; Ingram, R.; Dato-on, M.C. The business of ethics and gender. J. Bus. Ethics 2006, 64, 101–116. [Google Scholar] [CrossRef]

- Eweje, G.; Brunton, M. Ethical perceptions of business students in a New Zealand university: Do gender, age and work experience matter? Bus. Ethics Eur. Rev. 2010, 19, 95–111. [Google Scholar] [CrossRef]

- Stedham, Y.; Yamamura, J.H.; Beekun, R.I. Gender differences in business ethics: Justice and relativist perspectives. Bus. Ethics Eur. Rev. 2007, 16, 163–174. [Google Scholar] [CrossRef]

- Luthar, H.K.; Karri, R. Exposure to ethics education and the perception of linkage between organizational ethical behaviour and business outcomes. J. Bus. Ethics 2005, 61, 353–368. [Google Scholar] [CrossRef]

- Kohlberg, L. Stage and sequence: The cognitive- developmental approach to socialization. In Handbook of Socialization Theory and Research; Goslin, D.A., Ed.; Rand McNally: Chicago, UI, USA, 1969; pp. 347–480. [Google Scholar]

- Ede, F.O.; Panigrahi, B.; Stuart, J.; Calcich, S. Ethics in small minority businesses. J. Bus. Ethics 2000, 26, 133–146. [Google Scholar] [CrossRef]

- Kish-Gephart, J.J.; Harrison, D.A.; Treviño, L.K. Bad apples, bad cases, and bad barrels: Meta-analytic evidence about sources of unethical decisions at work. J. Appl. Psychol. 2010, 95, 1. [Google Scholar] [CrossRef] [PubMed]

- Peterson, D.; Rhoads, A.; Vaught, B.C. Ethical beliefs of business professionals: A study of gender, age and external factors. J. Bus. Ethics 2001, 31, 225–232. [Google Scholar] [CrossRef]

- Callahan, D. Goals in the teaching of ethics. In Ethics Teaching in Higher Education; Callahan, D., Bok, S., Eds.; Plenum Press: New York, NY, USA, 1980; pp. 61–80. [Google Scholar]

- Geary, W.; Sims, R. Can Ethics be Learned? Account. Educ. 1994, 3, 3–18. [Google Scholar] [CrossRef]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach; Guilford Press: New York, NY, USA, 2008. [Google Scholar]

- Cohen, J.; Cohen, P.; West, S.G.; Aiken, L.S. Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences; Routledge: Mahwah, NJ, USA, 2013. [Google Scholar]

- Hsiao, C.H. Impact of ethical and affective variables on cheating: Comparison of undergraduate students with and without jobs. High. Educ. 2015, 69, 55–77. [Google Scholar] [CrossRef]

- Herington, C.; Weaven, S. Improving consistency for DIT results using cluster analysis. J. Bus. Ethics 2008, 80, 499–514. [Google Scholar] [CrossRef]

- Kolb, D.A.; Boyatzis, R.E.; Mainemelis, C. Experiential learning theory: Previous research and new directions. In Perspectives on Thinking, Learning, and Cognitive Styles; Routledge: Abingdon, UK, 2001; pp. 227–247. [Google Scholar]

- Kolb, A.Y.; Kolb, D.A. Learning styles and learning spaces: Enhancing experiential learning in higher education. Acad. Manag. Learn. Educ. 2005, 4, 193–212. [Google Scholar] [CrossRef]

- Lawter, L.; Rua, T.; Guo, C. The interaction between learning styles, ethics education, and ethical climate. J. Manag. Dev. 2014, 33, 580–593. [Google Scholar] [CrossRef]

- Passarelli, A.M.; Kolb, D.A. The Learning Way: Learning from Experience as the Path to Lifelong. In The Oxford Handbook of Lifelong Learning; Oxford University Press: Oxford, UK, 2011; p. 70. [Google Scholar]

- Bandura, A. Social Learning Theory; Prentice-Hall: Englewood Cliffs, NJ, USA, 1977. [Google Scholar]

- Lie, L.Y.; Angelique, L.; Cheong, E. How do male and female students approach learning at NUS. CDTL Brief 2004, 7, 1–3. [Google Scholar]

- Baxter Magolda, M.B. Learning and gender: Complexity and possibility. High. Educ. 1998, 35, 351–355. [Google Scholar] [CrossRef]

- Prabhakar, V.; Swapna, B. Influence of learning styles. Int. J. Learn. 2009, 16, 169–184. [Google Scholar]

- Watts, L.L.; Medeiros, K.E.; Mulhearn, T.J.; Steele, L.M.; Connelly, S.; Mumford, M.D. Are ethics training programs improving? A meta-analytic review of past and present ethics instruction in the sciences. Ethics Behav. 2017, 27, 351–384. [Google Scholar] [CrossRef]

- Roxas, M.L.; Stoneback, J.Y. The Importance of gender Across Cultures in Ethical Decision-making. J. Bus. Ethics 2004, 50, 149–165. [Google Scholar] [CrossRef]

- Decety, J.; Michalska, K.J.; Kinzler, K.D. The developmental neuroscience of moral sensitivity. Emot. Rev. 2011, 3, 305–307. [Google Scholar] [CrossRef]

- Medeiros, K.E.; Watts, L.L.; Mulhearn, T.J.; Steele, L.M.; Mumford, M.D.; Connelly, S. What is working, what is not, and what we need to know: A meta-analytic review of business ethics instruction. J. Acad. Ethics 2017, 15, 245–275. [Google Scholar] [CrossRef]

- Chung, J.; Monroe, G. Exploring social desirability bias. J. Bus. Ethics 2003, 44, 291–302. [Google Scholar] [CrossRef]

- Carrigan, M.; Atalla, A. The myth of the ethical consumer—Do ethics matter in purchase behaviour? J. Consum. Mark. 2001, 18, 560–578. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; Organ, D.W. Self-reports in organizational research: Problems and prospects. J. Manag. 1986, 12, 531–544. [Google Scholar] [CrossRef]

- Haggard, P.; Eimer, M. On the relation between brain potentials and the awareness of voluntary movements. Exp. Brain. Res. 1999, 126, 128–133. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

| n = 551 | |

|---|---|

| Sex | |

| Female | 339 |

| Male | 209 |

| No response | 3 |

| Nationality | |

| Spanish | 479 |

| Other | 72 |

| Ethics/CSR courses taken | |

| Yes | 166 |

| No | 399 |

| Not sure | 36 |

| Variables | Mean | SD | GAE1 | GAE2 | GAE3 | GAE4 | OAE1 | OAE2 | OAE3 | OAE4 | OAE5 | OAE6 | OAE7 | E.C. | G. | A. |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GAE1. Ethics in business community | 2.57 | 1.40 | ||||||||||||||

| GAE2. Ethics in business courses | 2.50 | 1.30 | 0.762 ** | |||||||||||||

| GAE3. Ethics in pers. decisions | 2.08 | 1.21 | 0.513 ** | 0.535 ** | ||||||||||||

| GAE4. Ethics in workplace decis. | 2.37 | 1.27 | 0.517 ** | 0.580 ** | 0.683 ** | |||||||||||

| OAE1. Relating AE to moral issues | 3.33 | 1.44 | 0.295 ** | 0.357 ** | 0.257 ** | 0.307 ** | ||||||||||

| OAE2. Recognizing ethical implications of accounting issues | 3.05 | 1.33 | 0.333 ** | 0.422 ** | 0.309 ** | 0.360 ** | 0.660 ** | |||||||||

| OAE3. Developing “a sense of moral obligation” | 2.59 | 1.31 | 0.371 ** | 0.443 ** | 0.440 ** | 0.470 ** | 0.503 ** | 0.556 ** | ||||||||

| OAE4. Developing conflict-tackling abilities | 2.52 | 1.30 | 0.401 ** | 0.468 ** | 0.439 ** | 0.436 ** | 0.431 ** | 0.505 ** | 0.631 ** | |||||||

| OAE5. Learning to deal with uncertainties | 2.52 | 1.23 | 0.346 ** | 0.413 ** | 0.422 ** | 0.364 ** | 0.329 ** | 0.392 ** | 0.507 ** | 0.609 ** | ||||||

| OAE6. Fostering change in ethical behaviour | 2.99 | 1.28 | 0.383 ** | 0.469 ** | 0.367 ** | 0.450 ** | 0.476 ** | 0.480 ** | 0.538 ** | 0.572 ** | 0.471 ** | |||||

| OAE7. Understanding ethical aspects | 3.37 | 1.40 | 0.320 ** | 0.367 ** | 0.285 ** | 0.327 ** | 0.471 ** | 0.438 ** | 0.441 ** | 0.440 ** | 0.353 ** | 0.584 ** | ||||

| Ethics Courses | −0.57 | 0.823 | −0.062 | −0.093 * | −0.058 | −0.124 ** | −0.084 * | −0.053 | −0.045 | −0.071 | 0.002 | −0.127 ** | −0.002 | |||

| Gender | 0.24 | 0.972 | −0.162 ** | −0.160 ** | −0.155 ** | −0.203 ** | −0.089 * | −0.147 ** | −0.139 ** | −0.172 ** | −0.142 ** | −0.237 ** | −0.157 ** | 0.035 | ||

| Age | 21.23 | 3.58 | −0.065 | −0.106 * | −0.090 * | −0.138 ** | −0.156 ** | −0.165 ** | −0.113 * | −0.097 * | −0.056 | −0.199 ** | −0.104 * | 0.165 ** | −0.095 * |

| Step1 | Step2 | Step 3 | Step 4 | |||

|---|---|---|---|---|---|---|

| Independent/Moderating Variables | Ethics/CSR Course | Gender | Age | Course * Gender | Course * Age | Course * Gender * Age * |

| Dep. variable (items of GAE) | ||||||

| GAE1. Ethics in business community (n = 464) | ||||||

| B | −0.095 | −0.220 ** | −0.029 | −0.046 | –0.004 | –0.004 |

| SBE | 0.075 | 0.064 | 0.018 | 0.078 | 0.027 | 0.018 |

| R2 | 0.003 | 0.029 | 0.03 | 0.03 | ||

| F | 1.593 | 5.032 ** | 3.079 ** | 2.571 * | ||

| GAE2. Ethics in business courses (n = 463) | ||||||

| B | −0.150 * | −0.206 ** | −0.040 * | −0.034 | –0.037 | –0.013 |

| SBE | 0.070 | 0.059 | 0.016 | 0.072 | 0.025 | 0.016 |

| R2 | 0.009 | 0.041 | 0.045 | 0.046 | ||

| F | 4.578 * | 7.022 ** | 4.661 ** | 3.981 ** | ||

| GAE3. Ethics in personal decisions (n = 464) | ||||||

| B | −0.084 | −0.169 ** | −0.034 * | 0.047 | 0.006 | –0.014 |

| SBE | 0.065 | 0.055 | 0.015 | 0.067 | 0.023 | 0.015 |

| R2 | 0.003 | 0.035 | 0.036 | 0.037 | ||

| F | 1.682 | 5.982 ** | 3.681 ** | 3.211 ** | ||

| GAE4. Ethics in workplace decisions (n = 452) | ||||||

| B | −0.175 * | −0.242 ** | −0.049 ** | 0.056 | –0.036 | –0.033 * |

| SBE | 0.069 | 0.057 | 0.016 | 0.071 | 0.025 | 0.016 |

| R2 | 0.013 | 0.062 | 0.068 | 0.076 | ||

| F | 6.441 * | 10.695 ** | 7.026 ** | 6.624 ** | ||

| Step1 | Step2 | Step 3 | Step 4 | |||

|---|---|---|---|---|---|---|

| Independent/Moderating Variables | Ethics/CSR Course | Gender | Age | Course * Gender | Course * Age | Course * Gender * Age * |

| Dep. variable (items of OAE) | ||||||

| OAE1. Relating accounting education to moral issues (n = 462) | ||||||

| B | −0.161 * | −0.147 * | −0.061 ** | −0.064 | 0.007 | –0.025 |

| SBE | 0.076 | 0.065 | 0.018 | 0.078 | 0.027 | 0.018 |

| R2 | 0.009 | 0.039 | 0.041 | 0.044 | ||

| F | 4.482 * | 6.777 ** | 4.216 ** | 3.839 ** | ||

| OAE2. Recognizing ethical implications in accounting issues (n = 463) | ||||||

| B | −0.059 | −0.187 ** | −0.065 ** | −0.011 | 0.006 | –0.035 * |

| SBE | 0.070 | 0.059 | 0.016 | 0.072 | 0.025 | 0.016 |

| R2 | 0.001 | 0.046 | 0.047 | 0.055 | ||

| F | 0.713 | 8.083 ** | 4.848 ** | 4.827 ** | ||

| OAE3. Developing a “sense of moral obligation” (n = 464) | ||||||

| B | −0.070 | −0.172 ** | −0.045 ** | −0.007 | –0.005 | –0.025 |

| SBE | 0.070 | 0.060 | 0.016 | 0.073 | 0.025 | 0.016 |

| R2 | 0.002 | 0.030 | 0.030 | 0.034 | ||

| F | 0.993 | 5.102 ** | 3.058 ** | 2.947 ** | ||

| OAE4. Developing conflict-tackling abilities (n = 463) | ||||||

| B | −0.105 | −0.225 ** | −0.038 | 0.043 | –0.006 | –0.027 |

| SBE | 0.070 | 0.059 | 0.016 | 0.072 | 0.025 | 0.016 |

| R2 | 0.005 | 0.040 | 0.041 | 0.046 | ||

| F | 2.268 | 6.907 ** | 4.224 ** | 4.003 ** | ||

| OAE5. Learning to deal with uncertainties (n = 462) | ||||||

| B | 0.007 | −0.170 ** | −0.025 | −0.121 | –0.035 | –0.007 |

| SBE | 0.067 | 0.057 | 0.016 | 0.070 | 0.024 | 0.016 |

| R2 | 0.000 | 0.021 | 0.030 | 0.030 | ||

| F | 0.010 | 3.511 * | 3.045 * | 2.568 * | ||

| OAE6. Fostering change in ethical behaviour (n = 463) | ||||||

| B | −0.187 ** | −0.302 ** | −0.074 ** | −0.016 | –0.006 | –0.030 |

| SBE | 0.068 | 0.056 | 0.015 | 0.068 | 0.023 | 0.015 |

| R2 | 0.015 | 0.100 | 0.101 | 0.107 | ||

| F | 7.569 ** | 18.554 ** | 11.113 ** | 9.948 ** | ||

| OAE7. Understanding ethical aspects of accounting ethics (n = 463) | ||||||

| B | 0.022 | −0.221 ** | −0.048 ** | −0.010 | –0.011 | –0.013 |

| SBE | 0.074 | 0.063 | 0.017 | 0.076 | 0.026 | 0.017 |

| R2 | 0.000 | 0.036 | 0.036 | 0.037 | ||

| F | 0.087 | 6.161 ** | 3.718 ** | 3.190 ** | ||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tormo-Carbó, G.; Seguí-Mas, E.; Oltra, V. Business Ethics as a Sustainability Challenge: Higher Education Implications. Sustainability 2018, 10, 2717. https://doi.org/10.3390/su10082717

Tormo-Carbó G, Seguí-Mas E, Oltra V. Business Ethics as a Sustainability Challenge: Higher Education Implications. Sustainability. 2018; 10(8):2717. https://doi.org/10.3390/su10082717

Chicago/Turabian StyleTormo-Carbó, Guillermina, Elies Seguí-Mas, and Víctor Oltra. 2018. "Business Ethics as a Sustainability Challenge: Higher Education Implications" Sustainability 10, no. 8: 2717. https://doi.org/10.3390/su10082717

APA StyleTormo-Carbó, G., Seguí-Mas, E., & Oltra, V. (2018). Business Ethics as a Sustainability Challenge: Higher Education Implications. Sustainability, 10(8), 2717. https://doi.org/10.3390/su10082717