Impacts of the Fossil Fuel Divestment Movement: Effects on Finance, Policy and Public Discourse

Abstract

1. Introduction

1.1. A Brief History of Divestment

1.2. Politics of Divestment

2. Methods and Framework

2.1. Literature and Interviews

2.2. Developing a Framework

2.2.1. Divestment as a Social Movement

2.2.2. Impacts of Social Movements

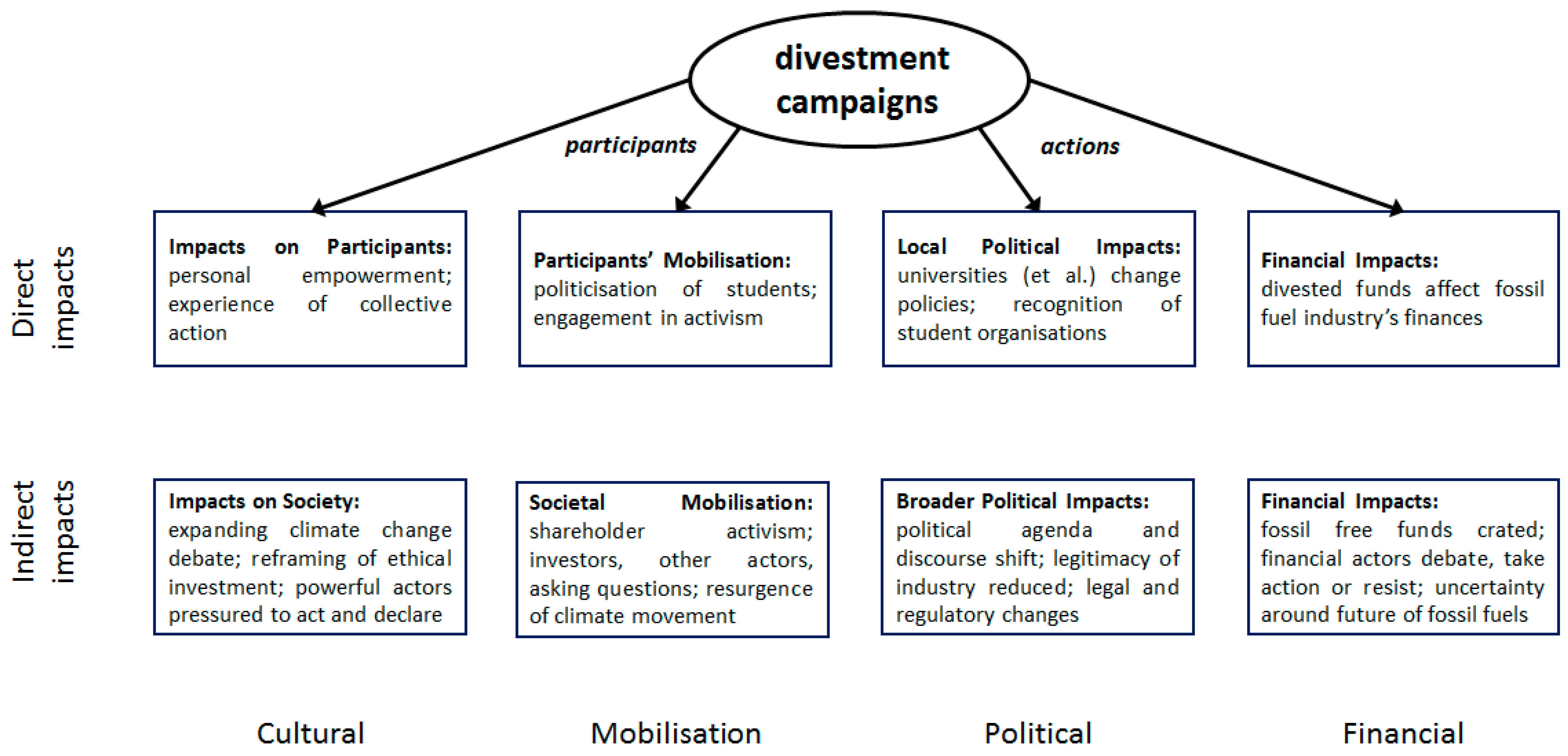

3. Direct Impacts of the Divestment Movement

3.1. Effects on Participants—Cultural and Mobilisation Impacts

The whole point is that a lot of people’s ability—or perception of their ability—to do anything about climate change is completely constrained by the perception that the problem is too big. It’s too abstract, it’s too global, it’s too long term. ... After talking about climate change for years and years and years, it’s nice to have something that you feel that you can actually [do]… A goal that you can attain in a reasonable timeframe.

I’ve seen people, after a year or a year and a half of organising for divestment, leave with a much deeper, more coherent radical politics ... than when they arrived and go on to continue organising with that in mind.

3.2. Direct Financial and Political Impacts

4. Indirect Impacts of the Divestment Movement

4.1. Changing the Discourse

4.1.1. Public Discourse Shift

4.1.2. Investors Raise Questions

We regularly host events where we bring together fund managers, asset owners and consultants to discuss the issues. In many cases, they would probably not be there were it not for the efforts of students and others to raise this up the agenda.

4.1.3. Finance Responds

have shown little willingness to engage with policy decision-makers with the publicity and assertiveness required. This calls into question whether these divestment critics are really looking for the best system change strategy or whether they are simply looking for reasons to justify their inaction.[30]

4.2. Legitimacy and Reputation

the initial aim is to move the money but also, it’s so much more about the social licence, legitimacy and power of those fossil fuel investment funds.(A1, student campaigner)

[to] reframe what we think of as an ethical investment and to include fossil fuels on the list of things that we can no longer invest in from an ethical standpoint and putting them on the same list as things like armaments and tobacco.(A2, former student activist)

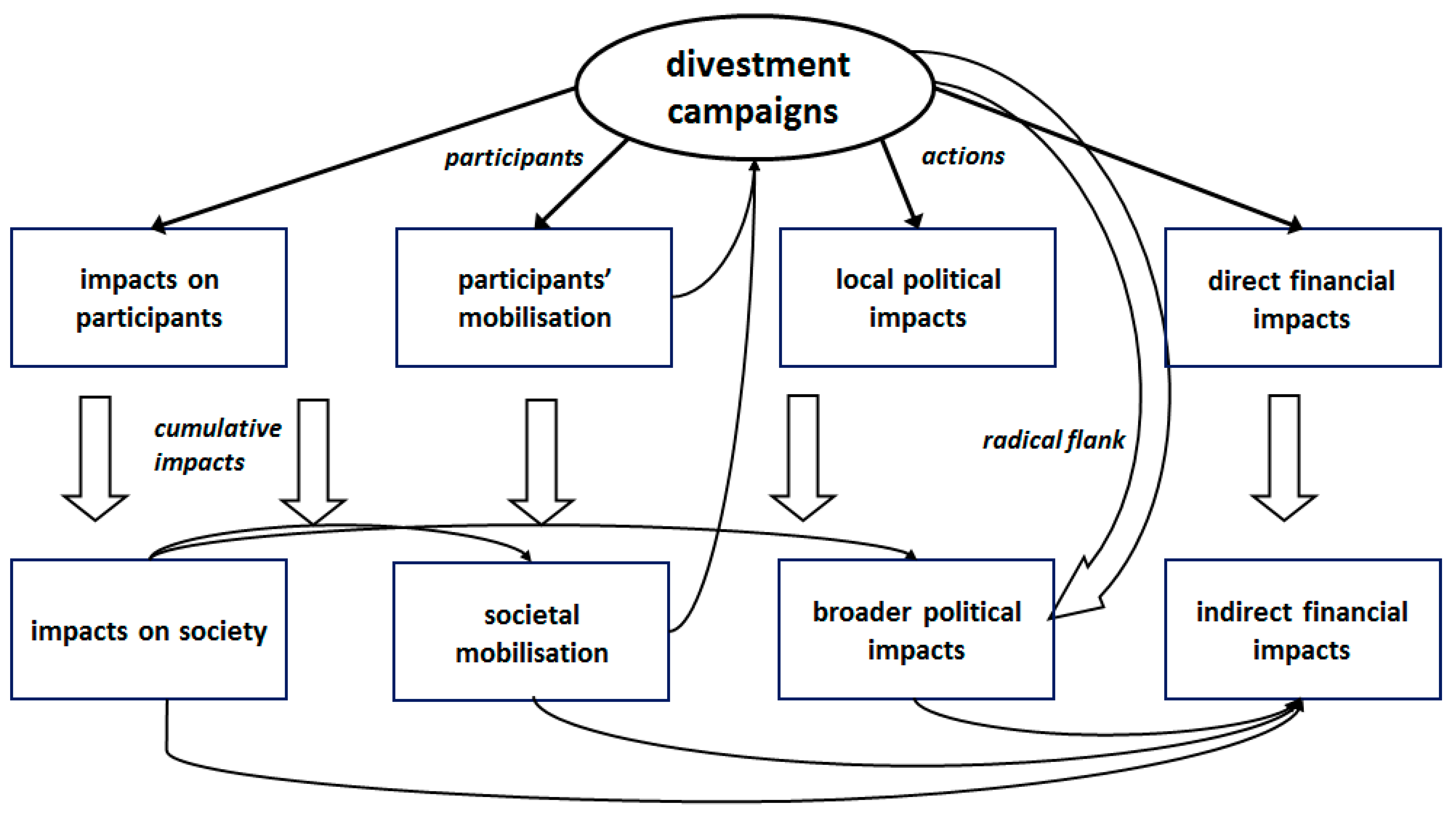

4.3. Radical Flank Effect

4.4. Fiduciary Duty

4.5. Reinvestment

It’s relatively straightforward for an investor to exclude fossil fuels. When it comes to solutions, it’s harder to identify what good looks like.(A3)

It’s not down to us, as people who are not expert in financial markets, to identify an alternative for them.(A6)

[S]ome UK universities have made reinvestment commitments as a result of divestment.(A7)

A number of major investors, including pension funds and insurance companies, are already starting to shift their investments. For example, over 400 investors with US$25 trillion in assets have joined the Investor Platform for Climate Actions, committed to increasing low-carbon and climate-resilient investments, including by working with policy-makers to ensure financing at scale.([46], p. 16)

4.6. Summary

5. Discussion and Conclusions

5.1. Direct and Indirect Impacts

5.2. Cultural, Mobilisation, Political and Financial Impacts

5.3. Impacts on Participants and Impacts of Action

Funding

Acknowledgments

Conflicts of Interest

References

- International Energy Agency (IEA). World Energy Outlook 2021; International Energy Agency: Vienna, Austria, 2012. [Google Scholar]

- Leaton, J. Unburnable Carbon—Are the World’s Financial Markets Carrying a Carbon Bubble? Carbon Tracker: London, UK, 2011. [Google Scholar]

- McGlade, C.; Ekins, P. The geographical distribution of fossil fuels unused when limiting global warming to 2°C. Nature 2015, 517, 187–190. [Google Scholar] [CrossRef] [PubMed]

- Erickson, P.; Lazarus, M.; Tempest, K. Carbon Lock-In from Fossil Fuel Supply Infrastructure; Stockholm Environment Institute: Seattle, WA, USA, 2015. [Google Scholar]

- Van Asselt, H. Governing the transition away from fossil fuels: The role of international institutions. Stock. Environ. Inst. Work. Pap. 2014, 7. [Google Scholar] [CrossRef]

- Ayling, J.; Gunningham, N. Non-state governance and climate policy: The fossil fuel divestment movement. Clim. Policy 2017, 17, 131–149. [Google Scholar] [CrossRef]

- Alexander, S.; Nicholson, K.; Wiseman, J. Fossil Free: The Development and Significance of the Fossil Fuel Divestment Movement; MSSI Issues Paper; Melbourne Sustainable Society Institute, The University of Melbourne: Melbourne, Australia, 2014; pp. 1–16. [Google Scholar]

- 350.org. Available online: https://350.org/ (accessed on 13 October 2017).

- Tollefson, J. Reality check for fossil-fuel divestment. Nature 2015, 521, 16–17. [Google Scholar] [CrossRef] [PubMed]

- Ansar, A.; Caldecott, B.; Tilbury, J. Stranded Assets and the Fossil Fuel Divestment Campaign: What Does Divestment Mean for the Valuation of Fossil Fuel Assets; Smith School of Enterprise and the Environment, University of Oxford: Oxford, UK, 2013. [Google Scholar]

- Dorsey, E.; Mott, R.N. Philanthropy Rises to the Fossil Divest-Invest Challenge. Available online: https://www.huffingtonpost.com/ellen-dorsey/philanthropy-rises-to-the_b_4690774.html (accessed on 18 July 2018).

- McKibben, B. Global Warming’s Terrifying New Math. Available online: https://www.rollingstone.com/politics/politics-news/global-warmings-terrifying-new-math-188550/ (accessed on 18 July 2018).

- Grady-Benson, J.; Sarathy, B. Fossil fuel divestment in US higher education: Student-led organising for climate justice. Local Environ. 2016, 21, 661–681. [Google Scholar] [CrossRef]

- Fossil Free Fossil Free: Divestment. Available online: http://gofossilfree.org/frequently-asked-questions/ (accessed on 16 April 2018).

- Ayling, J. A Contest for Legitimacy: The Divestment Movement and the Fossil Fuel Industry. Law Policy 2017, 39, 349–371. [Google Scholar] [CrossRef]

- Devinney, T. The Guardian’s Fossil Fuel Divestment Campaign Could Do More Harm Than Good. Available online: https://theconversation.com/the-guardians-fossil-fuel-divestment-campaign-could-do-more-harm-than-good-39000 (accessed on 14 November 2017).

- Healy, N.; Debski, J. Fossil fuel divestment: Implications for the future of sustainability discourse and action within higher education. Local Environ. 2017, 22, 699–724. [Google Scholar] [CrossRef]

- Ressler, L.; Schellentrager, M. A Complete Guide to Reinvestment. Available online: https://s3.amazonaws.com/s3.350.org/images/Reivestment_Guide.pdf (accessed on 22 July 2016).

- Power Shift Reinvestment in Climate Solutions. Available online: https://powershift.org/campaigns/divest/alternatives (accessed on 18 April 2018).

- United Nations Common Coding System (UNCCS). Safeguarding Future Retirement Funds—Time for Investors to Move out of High-Carbon Assets Says UN’s Top Climate Official; United Nations Common Coding System (UNCCS): New York, NY, USA, 2014. [Google Scholar]

- Weber, O.; Hunt, C. Want a Richer Pension? Divest of Fossil Fuels. Available online: https://theconversation.com/want-a-richer-pension-divest-of-fossil-fuels-93850 (accessed on 17 April 2018).

- DivestInvest.org. Available online: https://www.divestinvest.org/ (accessed on 13 October 2017).

- Dunn, H. Student Activism and the Climate Movement: An Exploration of Motivations, Successes and Challenges within the Fossil Fuel Divestment Campaign; University of Sussex: Brighton, UK, 2016. [Google Scholar]

- Snow, D.A.; Soule, S.A.; Kriesi, H. Mapping the terrain. In The Blackwell Companion to Social Movements; Snow, D.A., Soule, S.A., Kriesi, H., Eds.; Blackwell: Oxford, UK, 2004; pp. 3–16. ISBN 9780631226697. [Google Scholar]

- Rootes, C.; Nulman, E. The Impacts of Environmental Movements. In The Oxford Handbook of Social Movements; della Porta, D., Diani, M., Eds.; Oxford University Press: Oxford, UK, 2015; pp. 729–742. [Google Scholar]

- Staggenborg, S. Can Feminist Organizations Be Effective? In Feminist Organizations: Harvest of the New Women’s Movement; Ferree, M.M., Martin, P.Y., Eds.; Temple University Press: Philadelphia, PA, USA, 1995; pp. 339–355. ISBN 9781439901564. [Google Scholar]

- Giugni, M.G. Was It Worth the Effort? The Outcomes and Consequences of Social Movements. Annu. Rev. Sociol. 1998, 24, 371–393. [Google Scholar] [CrossRef]

- Marchetti, R. The Conditions for Civil Society Participation in International Decision Making. In The Oxford Handbook of Social Movements; della Porta, D., Diani, M., Eds.; Oxford University Press: Oxford, UK, 2015; pp. 753–766. [Google Scholar]

- Bernstein, M. Nothing Ventured, Nothing Gained? Conceptualizing Social Movement “Success” in the Lesbian and Gay Movement. Sociol. Perspect. 2003, 46, 353–379. [Google Scholar] [CrossRef]

- Thamotheram, R. The Fossil Fuel Divestment Debate: Is There a Consensus Way Forward? Available online: https://www.responsible-investor.com/home/article/rt_div/ (accessed on 14 November 2017).

- Solomon, C. We felt liberated. In Springtime: The New Student Rebellions; Solomon, C., Palmieri, T., Eds.; Verso: London, UK, 2011; pp. 11–16. ISBN 9781844678242. [Google Scholar]

- Piketty, T.; Jackson, T. Responsible Investors Must Divest from Fossils Fuels Now. The Guardian, 14 November 2015. [Google Scholar]

- Harrell, C.; Bosshard, P. Insuring Coal no More: An Insurance Scorecard on Coal and Climate Change. Available online: https://unfriendcoal.com/scorecard/ (accessed on 16 November 2017).

- Kemp, L. The Fossil Fuel Divestment Game Is Getting Bigger, Thanks to the Smaller Players. Available online: https://theconversation.com/the-fossil-fuel-divestment-game-is-getting-bigger-thanks-to-the-smaller-players-65109 (accessed on 19 December 2017).

- Schifeling, T.; Hoffman, A.J. Bill McKibben’s Influence on U.S. Climate Change Discourse: Shifting Field-Level Debates through Radical Flank Effects. Organ. Environ. 2017, 1–21. [Google Scholar] [CrossRef]

- Thamotheram, R. Part 3: Fossil Fuel Divestment: Is There a “Common Ground” Strategy? Available online: https://www.responsible-investor.com/home/article/rt_3/ (accessed on 14 November 2017).

- Goldenberg, S. Heirs to Rockefeller Oil Fortune Divest from Fossil Fuels over Climate Change. Available online: https://www.theguardian.com/environment/2014/sep/22/rockefeller-heirs-divest-fossil-fuels-climate-change (accessed on 18 July 2018).

- Leggett, J. Exxon, Dismissing Risk of Carbon Stranded Assets, Accused of Naivety. Available online: http://www.jeremyleggett.net/2014/04/exxon-dismisses-risk-of-stranded-assets-from-carbon/ (accessed on 16 November 2017).

- Linnenluecke, M.K.; Meath, C.; Rekker, S.; Sidhu, B.K.; Smith, T. Divestment from fossil fuel companies: Confluence between policy and strategic viewpoints. Aust. J. Manag. 2015, 40, 478–487. [Google Scholar] [CrossRef]

- Jotzo, F. Outrage at ANU Divestment Shows the Power of Its Idea. Available online: https://theconversation.com/outrage-at-anu-divestment-shows-the-power-of-its-idea-32736 (accessed on 13 October 2017).

- Bergman, N. Climate Camp and public discourse of climate change in the UK. Carbon Manag. 2014, 5, 339–348. [Google Scholar] [CrossRef]

- People & Planet People & Planet. Available online: https://peopleandplanet.org/ (accessed on 12 April 2018).

- ShareAction. The Law Commission’s Review of Fiduciary Duties: What It Means for Pension Funds; ShareAction: London, UK, 2014. [Google Scholar]

- Collinson, P. Boost for Fossil Fuel Divestment as UK Eases Pension Rules. Available online: https://www.theguardian.com/environment/2017/dec/18/boost-for-fossil-fuel-divestment-as-uk-eases-pension-rules (accessed on 18 December 2017).

- Thamotheram, R. Part 2: What Impact Could Divestment Have on Share Price and the Energy Sector? Available online: https://www.responsible-investor.com/home/article/rt_ff/P0/ (accessed on 14 November 2017).

- New Climate Economy. The Sustainable Infrastructure Imperative: Financing for Better Growth and Development; The Global Commission on the Economy and Climate: London, UK, 2016. [Google Scholar]

- Featherstone, D. Towards the relational construction of militant particularisms: Or why the geographies of past struggles matter for resistance to neoliberal globalisation. Antipode 2005, 37, 250–271. [Google Scholar] [CrossRef]

- Plows, A. Blackwood roads protest 2004: An emerging (re)cycle of UK eco-action? Environ. Polit. 2006, 15, 462–472. [Google Scholar] [CrossRef]

- Doherty, B.; Plows, A.; Wall, D. Environmental direct action in Manchester, Oxford and North Wales: A protest event analysis. Environ. Polit. 2007, 16, 805–825. [Google Scholar] [CrossRef]

- Rootes, C. The Transformation of Environmental Activism: An Introduction. In Environmental Protest in Western Europe; Rootes, C., Ed.; Oxford University Press: Oxford, UK, 2004; ISBN 9780191601064. [Google Scholar]

{kind=link}

{kind=link}

| Interviewee | Background or Profession |

|---|---|

| A1 | Student campaigner |

| A2 | Former divestment student activist |

| A3 | Project and research officer at a charitable trust |

| A4 | Former divestment student activist |

| A5 | Chair of a research and advocacy group |

| A6 | University academic involved in divestment |

| A7 | Campaigner at People & Planet |

| A8 | University finance director |

| B1 | Investment bank research analyst |

| B2 | Independent investment consultant |

| B3 | Senior economist in a fossil fuel corporation |

| B4 | Chief investment officer of a large pension scheme |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bergman, N. Impacts of the Fossil Fuel Divestment Movement: Effects on Finance, Policy and Public Discourse. Sustainability 2018, 10, 2529. https://doi.org/10.3390/su10072529

Bergman N. Impacts of the Fossil Fuel Divestment Movement: Effects on Finance, Policy and Public Discourse. Sustainability. 2018; 10(7):2529. https://doi.org/10.3390/su10072529

Chicago/Turabian StyleBergman, Noam. 2018. "Impacts of the Fossil Fuel Divestment Movement: Effects on Finance, Policy and Public Discourse" Sustainability 10, no. 7: 2529. https://doi.org/10.3390/su10072529

APA StyleBergman, N. (2018). Impacts of the Fossil Fuel Divestment Movement: Effects on Finance, Policy and Public Discourse. Sustainability, 10(7), 2529. https://doi.org/10.3390/su10072529