Sustainability and Business Outcomes in the Context of SMEs: Comparing Family Firms vs. Non-Family Firms

Abstract

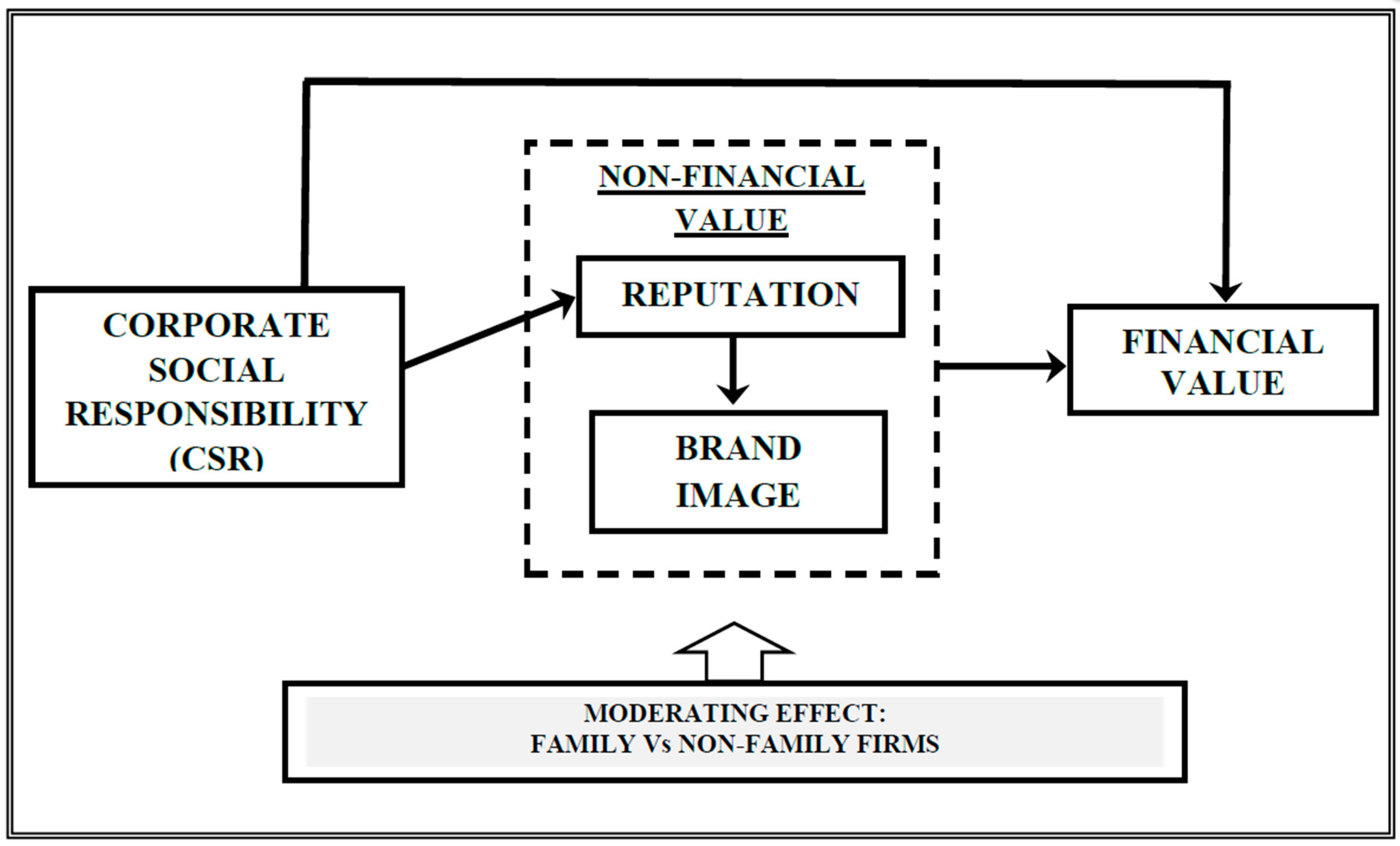

1. Introduction

2. Theoretical Background and Hypotheses Development

2.1. CSR and SMEs

2.2. The Context of Family Firms: The Stewardship Theory and the Socioemotional Wealth Theory

2.3. CSR Precedes Corporate Reputation and Brand Image

2.4. Antecedents of Financial Value

3. Materials and Methods

- (a)

- Property: The majority of the votes are owned by the person or persons of the family that founded the company, are owned by the person who has or has acquired the company’s capital stock, or are the property of their wives, parents, son(s), or direct heirs of the child(ren).

- (b)

- Control: The majority of the votes can be direct or indirect.

- (c)

- Governance: There is at least one representative of the family or relative participates in the management or governance of the company.

- (d)

- Vote: The person who founded or acquired the company (its social capital) or their family members or descendants own 25% of the voting rights.

4. Findings and Results

5. Discussion

- Implement sustainability and CSR activities to reinforce their reputation and brand image. These approaches must be linked to the core of the firm and related to the firms’ activity.

- Dedicate resources to better communicate with their stakeholders, not necessarily in terms of amount of money, but in identifying the adequate and most efficient channels to interact with them.

- Select adequate managers and establish suitable control mechanisms. In this sense, human resources management is also of interest.

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Measurement Scales

| Scales Go from 1 = “Totally Disagree” to 7 = “Totally Agree” | |||

| VARIABLE/ITEMS | Cross Loadings (Total Sample) | Cross Loadings (Family Firms) | Cross Loadings (Non-Family Firms) |

| CORPORATE SOCIAL RESPONSIBILITY | |||

| Adapted from: Hur (2014); Wagner et al. (2009); Du et al. (2007) | (CR = 0.905; AVE = 0.762) | (CR = 0.906; AVE = 0.763) | (CR = 0.944; AVE = 0.809) |

| CSR1.-I think my company is socially responsible. | 0.873 | 0.822 | 0.898 |

| CSR2.-My company is committed to increasing well-being in the society. | 0.937 | 0.949 | 0.980 |

| CSR3.-We are respectful with the environment. | 0.921 | 0.907 | 0.900 |

| CSR4.-Our human resources procedures go above and beyond the legal requirements. | 0.860 | 0.845 | 0.902 |

| CORPORATE REPUTATION | |||

| Adapted from: Martínez and Rodríguez-Del Bosque (2016); Hur et al. (2014); Lai et al. (2010) | (CR = 0.973; AVE = 0.900) | (CR = 0.970; AVE = 0.890) | (CR = 0.976; AVE = 0.911) |

| CR1.-I think my company has a good reputation. | 0.940 | 0.946 | 0.934 |

| CR2.-I think my company is well-known. | 0.939 | 0.937 | 0.946 |

| CR3.-I think my company is admired. | 0.964 | 0.962 | 0.972 |

| CR4.-I think my company is prestigious. (*) | --- | --- | --- |

| CR5.-In general, I think my company has a good reputation. | 0.942 | 0.930 | 0.967 |

| BRAND IMAGE | |||

| Adapted from: Hur (2014); Hsu (2012); Yoo and Donth (2001) | (CR = 0.877; AVE = 0.641) | (CR = 0.853; AVE = 0.593) | (CR = 0.932; AVE = 0.775) |

| B1.-My company’s logo is easily recognized in my environment. | 0.769 | 0.739 | 0.872 |

| B2.-My environment is aware of the values our brand transmits. | 0.752 | 0.708 | 0.848 |

| B3.-My brand stands out among its competitors. | 0.782 | 0.795 | 0.832 |

| B4.-My brand is recalled easily by consumers. | 0.797 | 0.763 | 0.836 |

| B5.-Society can trust in my brand. | 0.784 | 0.779 | 0.825 |

| FINANCIAL VALUE | |||

| Adapted from: Torugsa et al. (2012); Lai et al. (2010) | (CR = 0.814; AVE = 0.899) | (CR = 0.860; AVE = 0.755) | (CR = 0.815; AVE = 0.598) |

| FV1.-We have increased sales, in comparison to our competitors. | 0.892 | 0.830 | 0.722 |

| FV2.-We have increased market share, in comparison to our competitors. | 0.918 | 0.907 | 0.794 |

| FV3.-We get a good return on our investment, in comparison to our competitors. | 0.876 | 0.860 | 0.725 |

| CR: Composite Reliability; AVE: Average Variance Extracted * Following recommendations made during the pre-test, this item was omitted as it was considered very similar to items previously included in the scale. | |||

Appendix B. Descriptive Statistics (Mean, st. d.) for the Subsamples

| Mean (st. d.) | Family Firms | Non-Family Firms |

| CSR | 4.44 (1.25) | 3.91 (1.33) |

| REPUTATION | 4.90 (1.45) | 4.58 (1.44) |

| BRAND IMAGE | 4.97 (1.07) | 4.80 (1.05) |

| FINANCIAL VALUE | 5.17 (1.16) | 4.98 (1.28) |

Appendix C. Discriminant Validity

| Variables | CSR | Reputation | Brand Image | Financial Value | |

| FAMILY FIRMS | CSR | 0.873 | |||

| REPUTATION | 0.655 | 0.943 | |||

| BRAND IMAGE | 0.552 | 0.704 | 0.770 | ||

| FINANCIAL VALUE | 0.665 | 0.668 | 0.491 | 0.869 | |

| Data appearing on the main diagonal are the square roots of the AVE (Average Variance Extracted) of the variables. The rest of the data represents the correlations between constructs. All correlations are significant p < 0.01 [66]. | |||||

| Variables | CSR | Reputation | Brand Image | Financial Value | |

| NON-FAMILY FIRMS | CSR | 0.899 | |||

| REPUTATION | 0.530 | 0.954 | |||

| BRAND IMAGE | 0.605 | 0.715 | 0.880 | ||

| FINANCIAL VALUE | 0.664 | 0.578 | 0.660 | 0.773 | |

| Data appearing on the main diagonal are the square roots of the AVE (Average Variance Extracted) of the variables. The rest of the data represents the correlations between constructs. All correlations are significant p < 0.01 [66]. | |||||

References

- Suh, C.; Lee, I. An empirical study on the manufacturing firm’s strategic choice for sustainability in SMEs. Sustainability 2018, 10, 572. [Google Scholar] [CrossRef]

- Schmidt, F.; Zanini, R.; Korzenowski, A.; Schmidt, R.; Benchimol, K. Evaluation of sustainability practices in small and medium-sized manufacturing enterprises in Southern Brazil. Sustainability 2018, 10, 2460. [Google Scholar] [CrossRef]

- Baumgartner, R. Managing corporate sustainability and CSR: A conceptual framework combining values, strategies and instruments contributing to sustainable development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Aragón, C.; Narvaiza, L.; Altuna, M. Why and how does social responsibility differ among SMEs? A social capital systemic approach. J. Bus. Ethics 2016, 138, 365–384. [Google Scholar] [CrossRef]

- Baumann-Pauly, D.; Wickert, C.; Spence, L.; Scherer, A. Organizing corporate social responsibility in small and large firms: Size matters. J. Bus. Ethics 2013, 115, 693–705. [Google Scholar] [CrossRef]

- Russo, A.; Tencati, A. Formal vs. informal CSR strategies: Evidence from Italian micro, small, medium-sized, and large firms. J. Bus. Ethics 2009, 85, 339–353. [Google Scholar] [CrossRef]

- Aguado, E.; Holl, A. Differences of corporate environmental responsibility in small and medium enterprises: Spain and Norway. Sustainability 2018, 10, 1877. [Google Scholar] [CrossRef]

- Oudah, M.; Jabeen, F.; Dixon, C. Determinants linked to family business sustainability in the UAE: An AHP approach. Sustainability 2018, 10, 246. [Google Scholar] [CrossRef]

- Sharma, P.; Chrisman, J.; Gersick, K. 25 years of Family Business Review: Reflections on the past and perspectives for the future. Fam. Bus. Rev. 2012, 25, 5–15. [Google Scholar] [CrossRef]

- Zahra, A.; Sharma, P. Family business research: A strategic reflection. Fam. Bus. Rev. 2004, 15, 331–346. [Google Scholar] [CrossRef]

- Boesso, G.; Favotto, F.; Michelon, G. Stakeholder prioritization, strategic corporate social responsibility and company performance: Further evidence. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 424–440. [Google Scholar] [CrossRef]

- Anser, M.; Zhang, Z.; Kanwal, L. Moderating effect of innovation on corporate social responsibility and firm performance in realm of sustainable development. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1–24. [Google Scholar] [CrossRef]

- Junquera, B.; Barba-Sánchez, V. Environmental proactivity and firms’ performance: Mediation effect of competitive advantages in Spanish wineries. Sustainability 2018, 10, 2155. [Google Scholar] [CrossRef]

- Reverte, C.; Gómez-Melero, E.; Cegarra-Navarro, J. The influence of corporate social responsibility practices on organizational performance: Evidence from eco-responsible Spanish firms. J. Clean. Prod. 2016, 112, 2870–2884. [Google Scholar] [CrossRef]

- Garriga, E.; Melé, D. Corporate social responsibility theories: Mapping the territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Putnam, R. Bowling Alone; Simon & Schuster: New York, NY, USA, 2000. [Google Scholar]

- Ostrom, E. Governing the Commons; Cambridge University Press: Cambridge, MA, USA, 1991. [Google Scholar]

- Perrini, F. SMEs and CSR theory: Evidence and implications from an Italian perspective. J. Bus. Ethics 2006, 67, 305–316. [Google Scholar] [CrossRef]

- Ellerup, A.; Thomsen, C. CSR communication in small and medium-sized enterprises: A study of the attitudes and beliefs of middle managers. Corp. Commun. Int. J. 2009, 14, 176–189. [Google Scholar] [CrossRef]

- Torres, A.; Bijmolt, T.; Tribó, J.; Verhoef, P. Generating global brand equity through corporate social responsibility to key stakeholders. Int. J. Res. Mark. 2012, 29, 13–24. [Google Scholar] [CrossRef]

- Spence, L.; Schmidepeter, R. SMEs, social capital and the common good. J. Bus. Ethics 2003, 45, 93–108. [Google Scholar] [CrossRef]

- Brown, T.; Dacin, P. The company and the product: Corporate associations and consumer product responses. J. Mark. 1997, 61, 68–84. [Google Scholar] [CrossRef]

- Orlitzky, M.; Siegel, D.; Waldman, D. Strategic corporate social responsibility and environmental sustainability. Bus. Soc. 2011, 50, 6–27. [Google Scholar] [CrossRef]

- Papagiannakis, G.; Lioukas, S. Values attitudes and perceptions of managers as predictors of corporate environmental responsiveness. J. Environ. Manag. 2012, 100, 41–51. [Google Scholar] [CrossRef] [PubMed]

- Kallmuenzer, A.; Nikolakis, W.; Peters, M.; Zanon, J. Trade-offs between dimensions of sustainability: Exploratory evidence from family firms in rural tourism regions. J. Sustain. Tour. 2017, 26, 1–18. [Google Scholar] [CrossRef]

- Van Gils, A.; Dibrell, C.; Neubaum, D.; Craig, J. Social issues in the family enterprise. Fam. Bus. Rev. 2014, 27, 193–205. [Google Scholar] [CrossRef]

- Cui, V.; Ding, S.; Liu, M.; Wu, Z. Revisiting the effect of family involvement on corporate social responsibility: A behavioural agency perspective. J. Bus. Ethics 2017, 152, 291–309. [Google Scholar] [CrossRef]

- Block, J.; Wagner, M. The effect of family ownership on different dimensions of corporate social responsibility: Evidence from large US firms. Bus. Strategy Environ. 2013, 23, 475–792. [Google Scholar] [CrossRef]

- Déniz, M.; Cabrera, M. Corporate social responsibility and family business in Spain. J. Bus. Ethics 2005, 56, 27–41. [Google Scholar] [CrossRef]

- Aoi, M.; Asaba, S.; Kubota, K.; Takehara, H. Family firms, firm characteristics, and corporate social performance: A study of public firms in Japan. J. Fam. Bus. Manag. 2015, 5, 192–217. [Google Scholar] [CrossRef]

- Laguir, I.; Laguir, L.; Elbaz, J. Are family small- and medium-sized enterprises more socially responsible than nonfamily small- and medium-sized enterprises? Corp. Soc. Responsib. Environ. Manag. 2016, 23, 386–398. [Google Scholar] [CrossRef]

- Binza, C.; Hair, J., Jr.; Pieper, T.; Baldau, A. Exploring the effect of distinct family firm reputation on consumers’ preferences. J. Fam. Bus. Strategy 2013, 4, 3–11. [Google Scholar] [CrossRef]

- Benavides-Velasco, C.; Quintana-García, C.; Guzmán-Parra, V. Trends in family business research. Small Bus. Econ. 2013, 40, 41–57. [Google Scholar] [CrossRef]

- Zientara, P. Socioemotional Wealth and Corporate Social Responsibility: A critical analysis. J. Bus. Ethics 2017, 144, 185–199. [Google Scholar] [CrossRef]

- Niehm, L.; Swinney, J.; Miller, N. Community social responsibility and its consequences for family business performance. J. Small Bus. Manag. 2008, 46, 331–350. [Google Scholar] [CrossRef]

- Fitzgerald, M.; Haynes, G.; Schrank, H.; Danes, S. Socially responsible processes of small family business owners: Exploratory evidence from the National Family Business Survey. J. Small Bus. Manag. 2010, 48, 524–551. [Google Scholar] [CrossRef]

- Marques, P.; Presas, P.; Simon, A. The heterogeneity of family firms in CSR engagement. Fam. Bus. Rev. 2014, 27, 206–227. [Google Scholar] [CrossRef]

- Yusof, M.; Nor, L.; Hoopes, J. Virtuous CSR: An Islamic family business in Malaysia. J. Fam. Bus. Manag. 2014, 4, 133–148. [Google Scholar] [CrossRef]

- Berrone, P.; Cruz, C.; Gomez-Mejia, L. Socioemotional wealth in family firms: Theoretical dimensions, assessment approaches, and agenda for future research. Fam. Bus. Rev. 2012, 25, 258–279. [Google Scholar] [CrossRef]

- Labelle, R.; Hafsi, T.; Francoeur, C.; Ben Amar, W. Family firms’ corporate social performance: A calculated quest for socioemotional wealth. J. Bus. Ethics 2015, 148, 511–525. [Google Scholar] [CrossRef]

- Van de Ven, B.; Jeurissen, R. Competing responsibly. Bus. Ethics Q. 2005, 15, 299–317. [Google Scholar] [CrossRef]

- Agyemang, O.; Ansong, A. Corporate social responsibility and firm performance of Ghanaian SMEs: Mediating role of access to capital and firm reputation. J. Glob. Respir. 2017, 8, 47–62. [Google Scholar] [CrossRef]

- Galbreath, J. The impact of board structure on corporate social responsibility: A temporal view. Bus. Strategy Environ. 2017, 26, 358–370. [Google Scholar] [CrossRef]

- Castelo, M.; Lima, L. Corporate social responsibility and resource-based perspectives. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar]

- Stanaland, A.; Lewin, M.; Murphy, P. Consumer perceptions of the antecedents and consequences of corporate social responsibility. J. Bus. Ethics 2011, 102, 47–55. [Google Scholar] [CrossRef]

- Hur, W.; Kim, H.; Woo, J. How CSR leads to corporate brand equity: Mediating mechanisms of corporate brand credibility and reputation. J. Bus. Ethics 2014, 125, 75–86. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Du, S.; Bhattacharya, C.; Sen, S. Reaping relational rewards from corporate social responsibility: The role of competitive positioning. Int. J. Res. Mark. 2007, 24, 224–241. [Google Scholar] [CrossRef]

- Brislin, R. Cross-Cultural Research Methods; Castle Rock: Garrison, NY, USA, 1973. [Google Scholar]

- Wagner, T.; Lutz, R.; Weitz, B. Corporate hypocrisy: Overcoming the threat of inconsistent corporate social responsibility perceptions. J. Mark. 2009, 73, 77–91. [Google Scholar] [CrossRef]

- Martínez, P.; Rodríguez del Bosque, I. Corporate image and reputation as drivers of customer loyalty. Corp. Reput. Rev. 2016, 19, 166–178. [Google Scholar]

- Lai, C.; Chiu, C.; Yang, C.; Pai, D. The effects of corporate social responsibility on brand performance: The mediating effect of industrial brand equity and corporate reputation. J. Bus. Ethics 2010, 95, 457–469. [Google Scholar] [CrossRef]

- Hsu, K. The advertising effects of corporate social responsibility on corporate reputation and brand equity: Evidence from the life insurance industry in Taiwan. J. Bus. Ethics 2012, 109, 189–201. [Google Scholar] [CrossRef]

- Yoo, B.; Donthu, N. Developing and validating a multi-dimensional consumer based brand equity scale. J. Bus. Res. 2001, 52, 1–14. [Google Scholar] [CrossRef]

- Homburg, C.; Krohmer, H.; Workman, J. Strategic Consensus and Performance: The Role of Strategy Type and Market-Related Dynamism. Strateg. Manag. J. 1999, 20, 356–357. [Google Scholar] [CrossRef]

- Torugsa, N.; O’Donohue, W.; Hecker, R. Capabilities, proactive CSR and financial performance in SMEs: Empirical evidence from an Australian manufacturing industry sector. J. Bus. Ethics 2012, 109, 483–500. [Google Scholar] [CrossRef]

- Instituto de Empresa Familiar. La Empresa Familiar en España. 2015. Available online: http://www.iefamiliar.com/ (accessed on 1 November 2018).

- Ringle, C.; Wende, S.; Will, A. SmartPLS 2.0.M3; SmartPLS: Hamburg, Germany, 2005. [Google Scholar]

- Gefen, D.; Rigdon, E.; Straub, D. An update and extension to SEM guidelines for administrative and social science research. MIS Q. 2011, 35, 3–14. [Google Scholar] [CrossRef]

- Reinartz, W.; Haenlein, M.; Henseler, J. An empirical comparison of the efficacy of covariance-based and variance-based SEM. Int. J. Res. Mark. 2009, 26, 332–344. [Google Scholar] [CrossRef]

- Roldán, J.; Sánchez-Franco, M. Variance-based structural equation modeling: Guidelines for using partial least squares in information systems research. In Research Methodologies, Innovations and Philosophies in Software Systems Engineering and Information Systems; Mora, M., Gelman, O., Steenkamp, A., Eds.; IGI Global: Hershey, PA, USA, 2012. [Google Scholar]

- Henseler, J. Bridging design and behavioral research with variance-based structural equation modeling. J. Advert. 2017, 46, 178–192. [Google Scholar] [CrossRef]

- Felipe, C.; Roldán, J.; Leal-Rodríguez, A. Impact of Organizational Culture Values on Organizational Agility. Sustainability 2017, 9, 2354. [Google Scholar] [CrossRef]

- Carmines, E.; Zeller, R. Reliability and Validity Assessment. In Sage University Paper Series on Quantitative Applications in the Social Sciences 07-017; Sage: Beverly Hills, CA, USA, 1979. [Google Scholar]

- Fornell, C.; Larcker, D. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Barclay, D.; Higgins, C.; Thompson, R. The partial least square approach to causal modelling: Personal computer adoption and use as illustration. Technol. Stud. 1995, 2, 284–324. [Google Scholar]

- Podsakoff, P.; Mackenzie, S.; Lee, J. Common method biases in behavioural research: A critical review of literature and recommendation remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Podsakoff, P.; Organ, D. Self-reports in organizational research: Problems and prospects. J. Manag. 1986, 12, 531–544. [Google Scholar] [CrossRef]

- Hair, J., Jr.; Hult, G.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Henseler, J.; Hubona, G.; Ray, P. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Henseler, J.; Chin, W. A comparison of approaches for the analysis of interaction effects between latent variables using partial least squares path modelling. Struct. Equ. Model. 2010, 17, 82–109. [Google Scholar] [CrossRef]

- Hair, J., Jr.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Hair, J., Jr.; Sarstedt, M.; Ringle, C.; Gudergan, S. Advances Issues in Partial Least Squares Structural Equation Modeling; Sage Publications: Thousand Oaks, CA, USA, 2018. [Google Scholar]

- Hair, J.; Anderson, R.; Tatham, R.; Black, W. Multivariate Data Analysis with Readings; Prentice-Hall: Upper Saddle River, NJ, USA, 1998. [Google Scholar]

- Steenkamp, J.; Baumgartner, H. Assessing measurement invariance in cross-national consumer research. J. Consum. Res. 1998, 25, 78–90. [Google Scholar] [CrossRef]

- Moliner-Velázquez, B.; Fuentes-Blasco, M.; Servera, D.; Gil-Saura, I. From retail innovation and image to loyalty: Moderating effects of product type. Serv. Bus. 2018, 1–26. [Google Scholar] [CrossRef]

- Tenenhaus, M.; Esposito, V.; Chatelin, Y.; Lauro, C. PLS path modelling. Comput. Stat. Data Anal. 2005, 48, 159–205. [Google Scholar] [CrossRef]

- Hu, L.; Bentler, P. Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification. Psychol. Methods 1998, 3, 424–453. [Google Scholar] [CrossRef]

- Williams, L.; Vandenberg, R.; Edwards, R. Structural equation modeling in management research: A guide for improved analysis. Acad. Manag. Ann. 2009, 3, 543–604. [Google Scholar] [CrossRef]

- Chin, W.; Frye, T. PLS-Graph, Version 3.00 Build 1017; University of Houston: Houston, TX, USA, 2003. [Google Scholar]

- Keil, M.; Tan, B.; Wei, K. A cross-cultural study on escalation of commitment behavior in software projects. MIS Q. 2000, 24, 299–325. [Google Scholar] [CrossRef]

- González-Benito, J.; González-Benito, O. Environmental proactivity and business performance: An empirical analysis. Omega 2006, 33, 1–15. [Google Scholar] [CrossRef]

- Sen, S.; Cowley, J. The relevance of Stakeholder Theory and Social Capital Theory in the context of CSR in SMEs: An Australian perspective. J. Bus. Ethics 2013, 118, 413–427. [Google Scholar] [CrossRef]

{kind=link}

| IMPACT ON ENDOGENOUS VARIABLES | Family Firms (n = 140) | Non-Family Firms (m = 69) |

|---|---|---|

| Path Coefficients (β) t-Value (Bootstrap) | Path Coefficients (β) t-Value (Bootstrap) | |

| H1: CSR → Corporate Reputation | 0.655 *** (14,565) | 0.530 *** (5057) |

| H2: Corporate Reputation → Brand Image | 0.855 *** (25,891) | 0.715 *** (15,050) |

| H3: CSR → Financial Value | 0.418 *** (3930) | 0.403 *** (4855) |

| H4: Corporate Reputation → Financial Value | 0.434 *** (4391) | 0.035 (n.s.) |

| H5: Brand Image → Financial Value | n.s. | n.s. |

| IMPACT ON THE ENDOGENOUS VARIABLE | FAMILY (β) (n = 140) | NON-FAMILY (β) (m = 69) | SE | SP | t-Test | |

|---|---|---|---|---|---|---|

| FAMILY | NON-FAMILY | |||||

| H1: CSR → Corporate Reputation | 0.655 | 0.530 | 0.045 | 0.105 | 0.070 | 12.057 *** |

| H2: Corporate Reputation → Brand Image | 0.855 | 0.715 | 0.033 | 0.048 | 0.043 | 21.994 *** |

| H3: CSR → Financial Value | 0.418 | 0.403 | 0.106 | 0.083 | 0.091 | 1.116 n.s. |

| H4: Corporate Reputation → Financial Value | 0.434 | n.s. | 0.099 | 0.269 | 0.174 | 15.584 *** |

| H5: Brand Image → Financial Value | n.s. | n.s. | --- | --- | --- | --- |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

López-Pérez, M.E.; Melero-Polo, I.; Vázquez-Carrasco, R.; Cambra-Fierro, J. Sustainability and Business Outcomes in the Context of SMEs: Comparing Family Firms vs. Non-Family Firms. Sustainability 2018, 10, 4080. https://doi.org/10.3390/su10114080

López-Pérez ME, Melero-Polo I, Vázquez-Carrasco R, Cambra-Fierro J. Sustainability and Business Outcomes in the Context of SMEs: Comparing Family Firms vs. Non-Family Firms. Sustainability. 2018; 10(11):4080. https://doi.org/10.3390/su10114080

Chicago/Turabian StyleLópez-Pérez, María Eugenia, Iguácel Melero-Polo, Rosario Vázquez-Carrasco, and Jesús Cambra-Fierro. 2018. "Sustainability and Business Outcomes in the Context of SMEs: Comparing Family Firms vs. Non-Family Firms" Sustainability 10, no. 11: 4080. https://doi.org/10.3390/su10114080

APA StyleLópez-Pérez, M. E., Melero-Polo, I., Vázquez-Carrasco, R., & Cambra-Fierro, J. (2018). Sustainability and Business Outcomes in the Context of SMEs: Comparing Family Firms vs. Non-Family Firms. Sustainability, 10(11), 4080. https://doi.org/10.3390/su10114080