4.2. Electrification Potential Given Typical Vehicle User Patterns

4.2.1. Potential for Electrification in the Near Term

The main barriers for the adoption of BE-HDVs in the near term stem from driving range limitations of battery-electric (pilot) vehicles, limited engine power, and, as a result, limitations to the possibility to drive with a trailer. To assess the extent of these barriers, we looked at use patterns and the composition of the Norwegian commercial vehicle fleet.

From an analysis of base data from Autosys and Statistics Norway’s survey of trucks, we found that the majority of Norway’s commercial vehicle fleet (ca. 75%) consists of trucks of up to five years old, of which most have engines ≥500 HP and are driven with a trailer. In light of limitations in terms of power and availability of alternatives to diesel, this suggests that near term electrification of this segment of trucks is unlikely.

For trucks with engines <500 HP, the trucks not using trailers in the reporting week (which are considered most suitable for electrification) constitute 16.6% of the total fleet, while those using trailers equate to another 7.5%. For the latter, trailer use often encompasses lighter city trailers, i.e., leaving some potential for electrification.

In terms of mileage, we found that newer trucks constitute an even larger share (85%) than in terms of vehicle number. Further, over 70% of mileage with newer trucks is carried out with engines ≥500 HP, mostly with a trailer attached. This is noteworthy since it is largely the segment for newer trucks where user requirements are set. These observations also confirm that based on current use patterns, electrification in the near term seems unlikely for a large part of the Norwegian commercial vehicle fleet.

Regarding segments where near-term electrification is most likely, and taking into account also variations in daily use, we found that trucks with engine power <500 HP and maximum daily mileages up to 200 km constitute only 3% (without trailer) and 1% (with trailer) of the total mileage driven with newer trucks. This indicates that with current technological limitations, the electrification potential in terms of vehicle-km that can be electrified is currently small. The potential might increase when access to charging infrastructure improves, supporting longer daily driving distances.

After our assessment of engine power and trailer use, we focused on differences between categories of trucks (with engines <500 HP, up to 5 years old, and without trailer (except for tractors for semitrailer). In this segment, trucks with closed chapel make up the largest share of mileage (ca. 50%), particularly for the driving of shorter daily distances. Tractor units with semitrailer constitute about a quarter of total mileage, but are mostly used on longer distances. Special trucks (e.g., refuse collection trucks and crane truck), in turn, stand for 20% of total mileage, in part, over shorter daily distances, while trucks with platform body and tank trucks make up only small shares of driving in this segment.

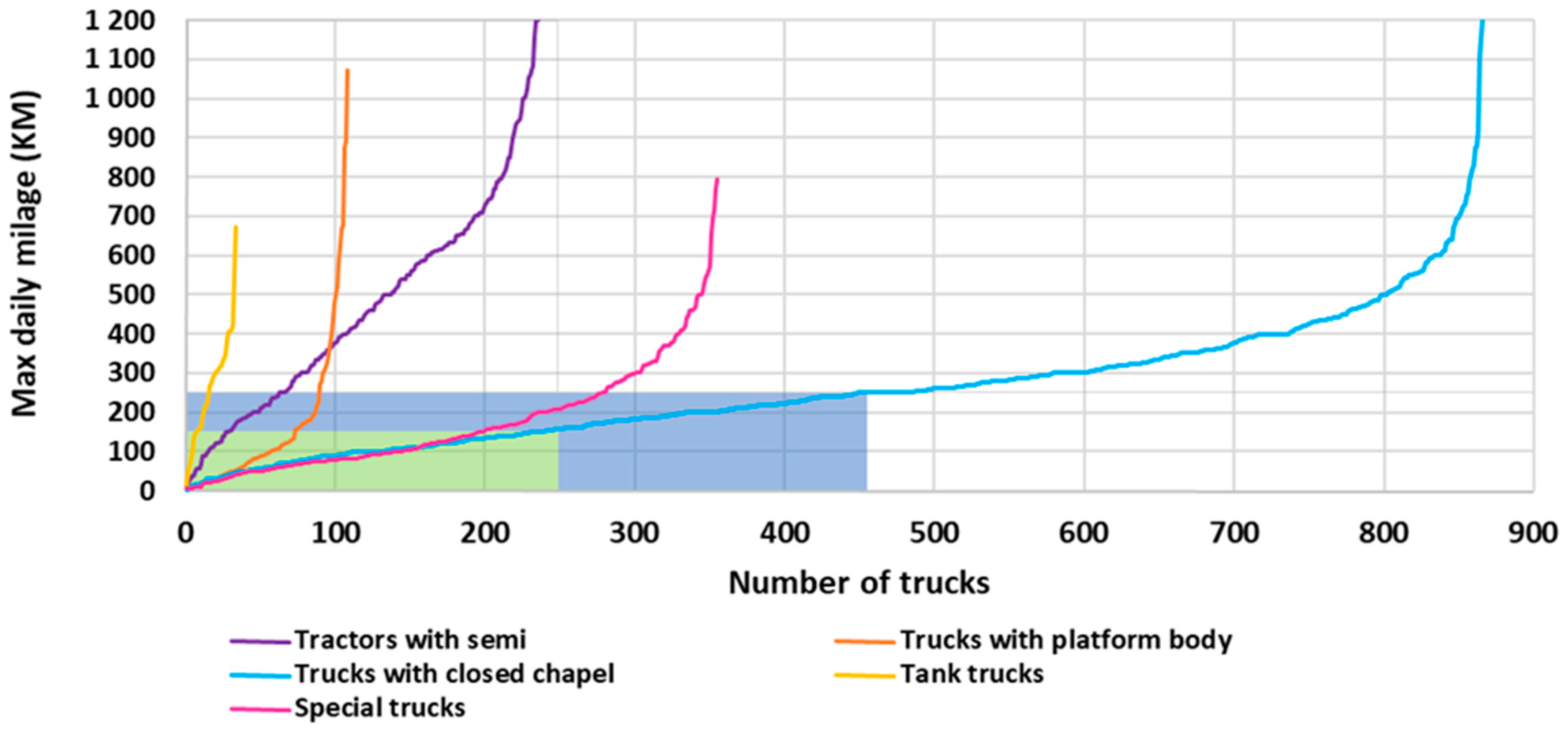

To investigate range limitations, we further looked at the maximum daily mileage for each truck, as reported in the reporting week for the survey of trucks.

Figure 2 shows an illustration of these maximum daily mileages in ascending order for different truck categories. Where daily mileages of a vehicle are below 150 km (the assumed all-electric driving range on a full battery without requiring daytime charging), vehicles are assumed to have potential for electrification (green-shaded area). For daily mileages between 150 and 250 km, we consider that a certain additional electrification potential exists, provided the availability of sufficient daytime charging opportunities or improved batteries (blue-shaded area).

Figure 2 shows that special trucks and trucks with closed chapel have most vehicles in the segment with potential for electrification, thereby constituting the main market for near-term electrification. This is confirmed by our case study, as early pilots with e-trucks were carried out with distribution and refuse collection trucks. For the other vehicle categories, maximum daily driving distances exceed what can currently be supported by battery-electric alternatives.

4.2.2. Potential for Electrification in a Longer Term

In a longer term, firms owning multiple trucks might have some flexibility to redistribute transport routes between vehicles, e.g., by assigning BE-trucks more to shorter-distance transport of volume goods. This flexibility is not easy to quantify because the transport industry is very fragmented and further consists of both hire-transporters (with many small firms) and own-transporters. Although we do not have data on the share of firms carrying out own transport, in our sample, own-transport constitutes 27% of trucks but only 18% of mileage. This suggests that on average, own-transport is carried out with smaller vehicles driving shorter mileages than hire-transport, implying that own-transport is more suitable for electrification. Own-transport vehicles are also more likely to be operated from only one terminal and can thus more easily be charged overnight. The fact that vehicles used for own-transport are, on average, older, however, works in the opposite direction.

Even with route redistribution and more abundant charging opportunities in the longer term, several challenges for the electrification of trucks remain, in particular relating to engine power, driving ranges, the trade-off between battery weight and payload, and limitations to the use of trailers.

Most driving is carried out by trucks having an engine power between 500 and 600 HP (53% of trips, 54% of vehicle-km and 66% of tonne-km), while driving with larger engines makes up relatively small shares. This suggests that if the majority of transport assignments are to be carried out with e-trucks in Norway, e-trucks with and engine power of up to 600 HP would be have to be available in the market.

With regard to driving ranges,

Table 3 illustrates the distribution of daily mileages for newer trucks, for different engine powers.

The table shows that more than a quarter of all driving with trucks in Norway is carried out by vehicles with daily mileages of up to 100 km, a fifth by vehicles with daily mileages between 100 and 200 km, and around 13% by vehicles with daily mileages between 200 and 300 km. Although a sizable share of driving is done with (much) higher daily mileages, this suggests that if batteries of e-trucks could support a vehicle range of 300 km (alongside engine powers up to 600 HP), this could give a potential for electrification for a large share of transport.

With regard to the weight of batteries, we looked at mileages driven with and without trailer for trucks ≤5 years old. Here, we found that for almost 79% of mileage with cargo, it is volume and not weight that fills up capacity and constitutes the capacity dimensioning factor. This suggests that the extra weight of batteries might not be as critical as is sometimes assumed. Furthermore, a proposal adopted by the European Parliament in April 2019 opens up for a two-tonne additional total vehicle weight allowance for zero-emission trucks [

37,

38]. This corresponds to the weight of about 200 kWh of batteries, and possibly more in the future, as the energy density of lithium-ion battery cells has been increasing by around 5–7%/year [

39].

Next, we looked at the distribution of total mileage without trailer attached (as it is the vehicle, not trailer, that is most crucial) by capacity utilization and vehicle’s maximum allowed total weight. Here, we found that, respectively, three quarters and a fifth of total mileage is driven by vehicles with maximum total weights between 10 and 20 tonnes and 20 and 30 tonnes. Driving with smaller vehicles only constitutes a fraction of total mileage. More importantly, for over 80% of total mileage driven with cargo, at least 20% of the vehicles’ weight capacity is unutilized. Particularly for vehicles with payloads over 10 tonnes, which constitute most of mileage with cargo, this indicates that there would often be sufficient ‘weight capacity’ to carry several tonnes of battery.

Finally, we looked at limitations on the use of trailers. Here, we found that 45% of trips are driven without trailer attached, particularly by trucks with engines between 200 to 600 HP, and of those, particularly with largest engines in this interval. In terms of mileage, rather than trips, the share of driving without trailer is only 28%. This indicates that trips without trailer are on average considerably shorter than trips where trailers are used.

There may be variations in how a vehicle is used over a year that may reduce the potentials described above. The datasets used only cover 1 week of trucking. A truck that is not fully utilizing the capacity during this week could potentially be doing it another week of the year. BE-trucks may thus reduce the flexibility of some operators to take on different transport assignments over the year.

4.3. Cost Competitiveness of Electric vs. ICE Operation

In

Section 3.3., we described the development of a model for comparing decomposed ownership costs of different propulsion technologies. For readability, results from our comparisons are presented in two tables.

Table 4 shows decomposed ownership costs for light distribution trucks based on the current early stage of technological maturity for BE- and FCHE-alternatives, while

Table 5 presents a similar decomposition for the scenarios with small-scale series production and mass production of electric vehicles, including a reduction hydrogen fuel prices. For conciseness, several smaller cost components were aggregated. Components that differ significantly between technologies or that might be used to create policy incentives, however, are presented separately. Wage costs are shown to illustrate their magnitude compared to other cost drivers.

Table 4 illustrates that in today’s early stage, ownership costs for light distribution vehicles with electric propulsion are considerably higher than for ICE-based propulsion systems. Compared to diesel vehicles (0.95 EUR/km), ownership costs for BE-vehicles (1.48 EUR/km) and FCHE-trucks (2.23 EUR/km) are, for example, 57% and 136% higher, respectively. Although not shown in further detail here, our calculations show that these figures are 55%/128% for heavy distribution trucks and 92%/161% for tractors for semitrailers. Compared to light distribution trucks, differences stem primarily from differences in investment cost premiums and fuel/energy consumption. It can further be seen that at 0.93 EUR/km, wage costs are of a similar order of magnitude as vehicle-ownership costs for light distribution vehicles with ICE. Our estimates on operational costs for both battery- and hydrogen-electric trucks fall within the ranges identified in a review of different studies by Plötz et al. [

9].

Table 5, in turn, shows that small-scale series production considerably reduces ownership costs for electric trucks. For FCHE light distribution trucks, per-km costs fall to 1.54 EUR (at current hydrogen prices), or 1.41 EUR if prices of hydrogen were to fall by half (driven by higher demand and larger-scale production). Even at these prices, however, ownership costs for FCHE vehicles remain considerably higher compared to ICE-trucks. For BE-trucks, in turn, ownership costs under small-scale series production, at 0.98 EUR/km, approach those of diesel trucks at typical mileages.

For the scenario with mass production, we found that ownership costs for battery-electric vehicles fall below those of ICE-vehicles. At this point, FCHE-trucks are still more expensive at annual mileages of 45,000 km, but may nevertheless have potential in specific use cases, e.g., within long-haul transport, where BE-operation yields more limitations.

When focusing on individual cost components, we see that capital costs, albeit decreasing with technological maturity stage, remain the main cost driver for electric trucks in the foreseeable future. Administration and insurance costs and general levies such as Norway’s annual weight fee, are only minor costs drivers. Even though the weight fee has an environmental component, this component plays such a small role that its effects are marginal at most. Costs for washing, consumables, and tyres, too, are only moderate cost drivers, and not expected to differ between technologies. Costs for general maintenance, in turn, are expected to be lower for electric vehicles than for ICE, but savings make up a minor share of TCO.

Looking at energy-related expenses, however, we found considerable differences. For diesel vehicles, in addition to fuel costs, operators pay a CO2-levy and road use levy (together equaling ~0.26 EUR/km), while energy costs for biodiesel and biogas vehicles are of a similar order. On top of this come road toll charges of around 0.14 EUR/km. Energy costs for BE-vehicles, in turn, are much lower, at under 0.05 EUR/km (or around 0.07 EUR/km with only fast charging). For FCHE-vehicles, energy costs at current prices are still relatively high, but could fall towards 0.13 EUR/km. These results show that savings on operation costs for electric vehicles increase with annual mileage, particularly due to lower energy costs per km, but also due to toll savings and to a lesser extent, savings on maintenance.

Just as distance-dependent costs decrease with increasing annual mileages, capital costs (derived from the investment base and premium cost) will also decrease with annual driving distances. To illustrate this,

Table 6 summarizes at what annual mileages BE- and FCHE-trucks may become cost-competitive with corresponding ICE-trucks. Results are presented for light distribution trucks, heavy distribution trucks, and tractors for semitrailer.

The table shows that in the current early market phase, e-trucks cannot compete with the costs of ICE-based vehicles, except for when mileages would be unrealistically high in light of limitations to the driving range set by current battery technology.

In the scenario assuming small-scale series production, our calculations show that BE-vehicles become cost competitive compared to diesel vehicles at mileages between 43,000 and 58,000 km. The reason for BE-light distribution trucks reaching cost-parity versus diesel at lower mileages than heavy distribution trucks is that the cost premium of investment is relatively high compared to savings on energy costs. Again, it is important to remember that estimates on cost premium and fuel consumption are uncertain, and that fuel consumption is affected by load weight and topography. Data on vehicle usage, e.g., from Statistics Norway’s Survey of Trucks, indicate that such annual mileages are not unusual for newer diesel-based trucks. Provided that limitations to range, payload etc., are reduced, e-trucks may thus become a feasible alternative.

Finally, in the scenario assuming mass production, we found that BE-vehicles become cost-competitive compared to diesel operation starting from annual mileages between 19,000 and 23,000 km, and at even lower mileages compared to biodiesel and biogas vehicles. These findings indicate that even when advantages such as toll exemptions would be reduced, BE-vehicles may prove cost-competitive alternatives.

For FCHE-trucks, in turn, we find that ownership costs are higher than for BE-trucks in all scenarios, because both cost premiums of investment and energy costs per km are expected to remain higher, even when hydrogen prices are reduced by half. Compared to ICE-based trucks, we find that FCHE-operation may become cost-competitive in a stage of mass production at annual mileages between 50,000 km (tractors) and 65,000 km (heavy distribution trucks). Such mileages are not uncommon in many use cases (particularly for tractors). Even though BE-operation might be cheaper, limitations might, therefore, make hydrogen the alternative of choice in cases with, e.g., intensive use, long-haul unsuitable for BE-trucks, or when cost premiums for FCHE trucks are reduced more than is assumed here.

4.4. Socio-Economic Costs of Phasing-in Zero-Emission Technologies

With regard to the socio-economic costs of phasing-in zero-emission technologies,

Section 3.4. describes components that constitute public and private costs and benefits.

Table 7 shows how these public and private costs and benefits sum to socio-economic costs, and what this implies for society’s costs per tonne reduction in CO

2-emissions. Figures are for light distribution trucks and compared to a diesel truck, assuming today’s early phase of technological maturity (and cost levels) for electric vehicles. To illustrate the role of mileage, figures are further presented both for typical annual mileages of 45,000 km and lower mileages of 20,000 km.

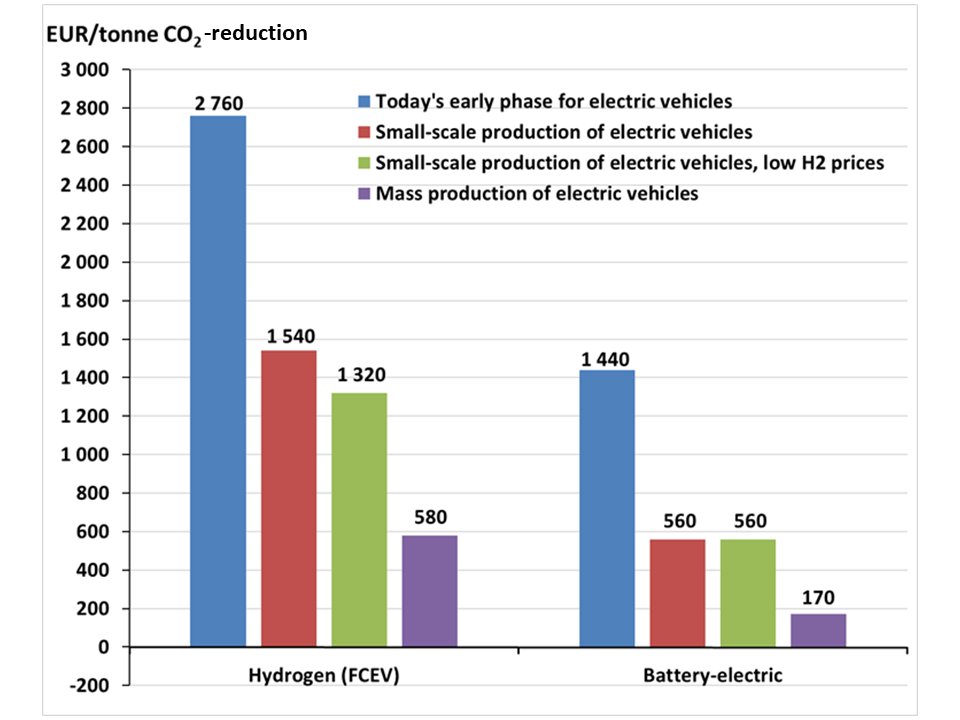

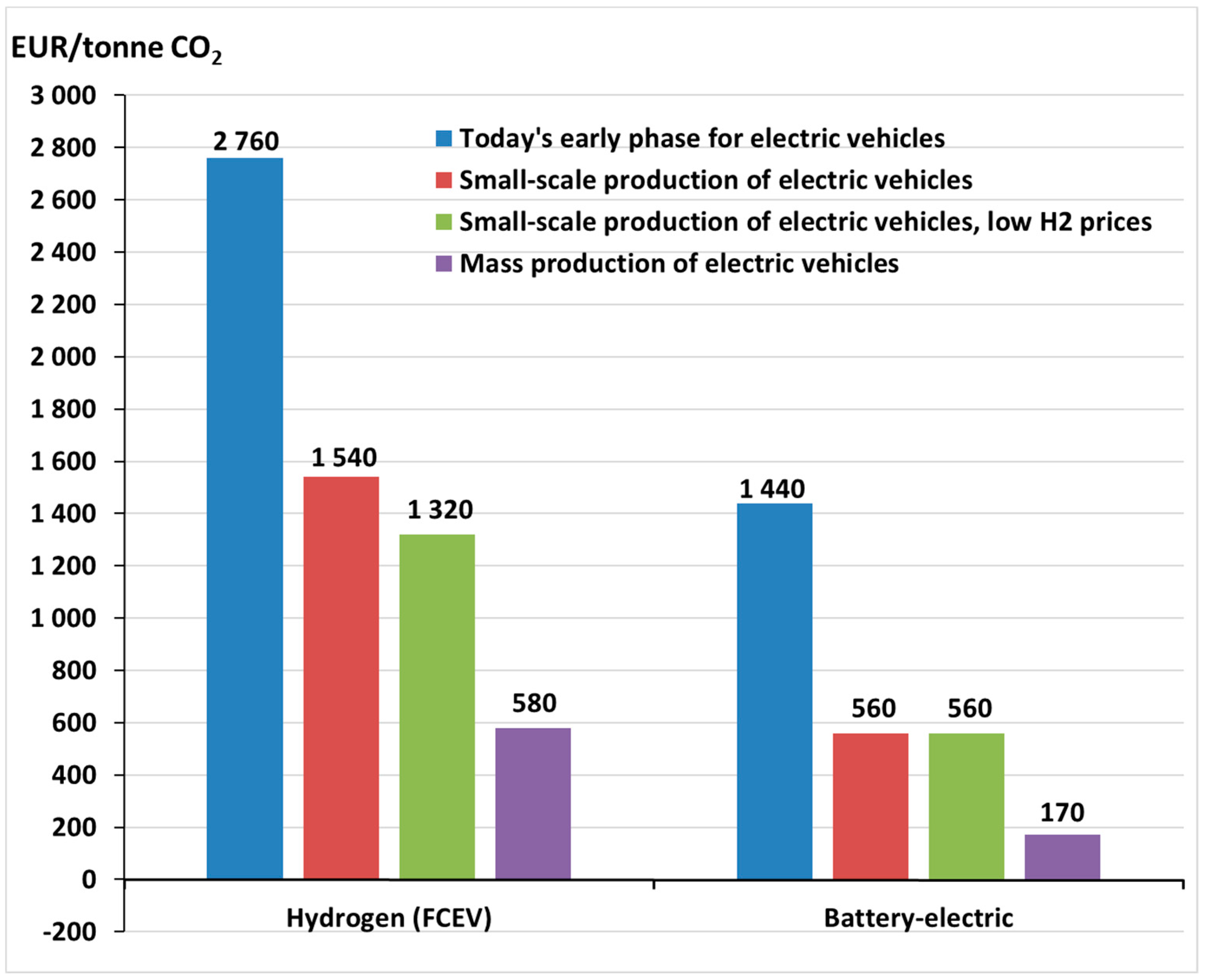

From the table, it can be seen that a transition to alternative propulsion technologies yields socio-economic costs of between EUR 43,000 and 353,000 per truck when assuming typical mileages. Consequently, the costs of reducing CO2-emissions by one tonne vary from EUR 340 for biogas to 2760 for FCHE trucks, while it is EUR 1440 for BE-trucks.

At low annual mileages, socio-economic costs from a transition to biogas and hydrogen are slightly lower, while for electric propulsion, they are somewhat higher. These differences are due to external damage costs from diesel operation being lower at lower mileages, but also savings on energy costs and maintenance from a transition to alternative propulsion being lower. Since reductions in CO2-emissions are much lower with less intensive vehicle use (while cost premiums of alternative propulsion trucks remain the same), the socio-economic costs per unit CO2 reduced are considerably higher at lower mileages.

Figure 3 illustrates how socio-economic costs per reduced tonne in CO

2-emissions go down in future scenarios with larger scales of production (i.e., lower investment cost premiums) and at typical mileages.

The figure clearly shows that socio-economic costs for reducing CO

2-emissions towards alternative technology trucks become lower when electric propulsion systems reach more mature stages. At the same time, it is assumed that the costs of FCHE-vehicles will remain higher than for BE-vehicles. This is due to both higher cost premiums of investments and lower savings on energy costs compared to conventional trucks. Moreover, Weken et al. [

26] concluded that although FCHE technology is considerably more expensive and less technologically mature than BE-trucks, it could prove a solution to the range and charging time challenges of BE-trucks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}