Strategic Bidding to Increase the Market Value of Variable Renewable Generators in New Electricity Market Designs

Abstract

1. Introduction

2. Overview of European Electricity Market Designs

2.1. Market Design Reforms

2.2. Portuguese Electricity Markets

3. New Market Designs and Strategic Bidding

3.1. New Market Designs

3.2. Probabilistic Quantile-Based Forecasts and Price Arbitrage

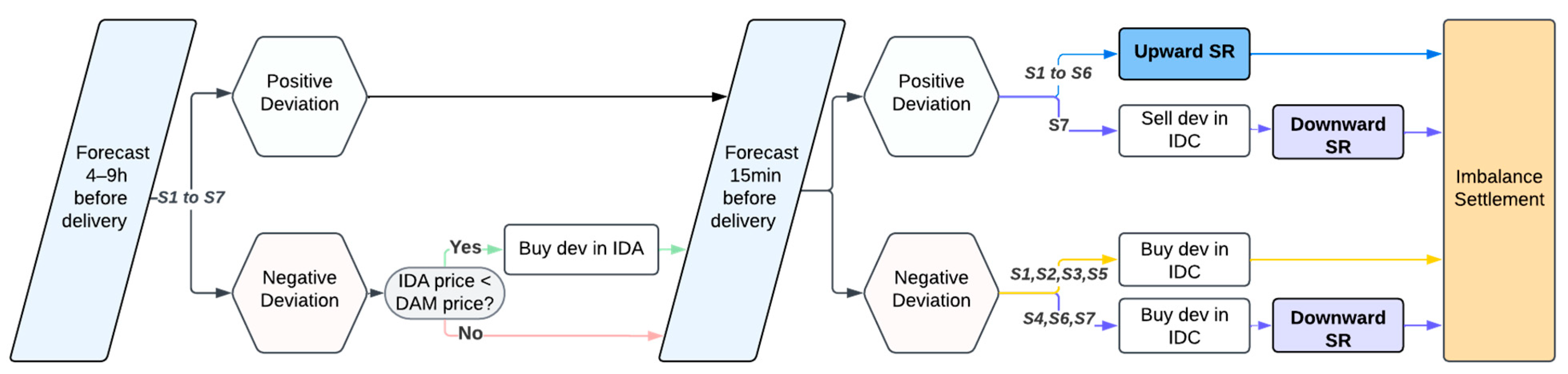

3.3. Strategic Bidding

- , are revenues from the DAM and IS, respectively;

- are revenues from the auction-based and continuous intraday markets, respectively;

- are the reserves revenue from capacity and energy markets.

- is the forecasted value 15 min before delivery and is the vRES position at the time of the IDC, which can be higher than the bid in DAM if the producer sold energy in the IDA, or lower if the producer was a buyer in the IDA. The average remuneration, (EUR/MWh), for the study period is calculated by dividing the total revenue across all hours by the total observed production, , for the same period (total number of periods).

4. Case Study

4.1. Scenarios

- Past: Asymmetrical bids, where upward doubles downward capacity.

- Actual: Existing legislation force constraints on the procurement of secondary capacity considering symmetrical bids for upward and downward capacity.

- New 1: This proposed market design separates the procurement of upward and downward balancing capacity in the secondary market, aligning with the new EIME legislation and European Balancing Guidelines. The secondary capacity market features a gate closure 15 min before delivery, in parallel with IDC.

- New 2: Similar to New1, but players can only bid in one balancing direction.

4.2. Results

4.2.1. Ideal Case

4.2.2. Operational Case

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| aFRR | Automatic-activated frequency restoration reserve |

| BM | Balancing market |

| BRP | Balance responsible party |

| CCGT | Combined cycle gas turbine |

| CET | Central European Time |

| CfD | Contracts for difference |

| DAM | Day-ahead market |

| EU | European Union |

| EUPHEMIA | EU Pan-European Hybrid Electricity Market |

| FCR | Frequency containment reserve |

| FiTs | Feed-in tariffs |

| GFS | Global forecast system |

| IDA | Auction-based IDM |

| IDC | Continuous IDM |

| IDM | Intraday market |

| IS | Imbalance settlement |

| KNN | K-nearest neighbor |

| LCOE | Levelized costs of energy |

| mFRR | Manually activated frequency restoration reserve |

| MIBEL | Iberian market of electricity |

| NWP | Numerical weather prediction |

| PPA | Power purchase agreement |

| PV | Photovoltaic |

| RR | Replacement reserve |

| SR | Secondary reserve |

| TSO | Transmission system operator |

| vRES | Variable renewable energy source |

| WPP | Wind power producer |

| Indices | |

| Quantile number | |

| K | Number of quantiles |

| Hours | |

| T | Total number of hours |

| Parameters | |

| DAM price | |

| Deterministic forecast 15 min before delivery in hour t | |

| Observed energy | |

| Probabilistic forecast quantiles | |

| Maximum price | |

| Variables | |

| Deviation | |

| Programmed dispatch 15 min before real-time operation | |

| Average remuneration | |

| Hourly total revenue | |

| Revenue from capacity reserve markets | |

| DAM revenue | |

| Revenue from energy reserve markets | |

| IDA revenue | |

| IDC revenue | |

| IS revenue |

References

- Hunt, S.; Shuttleworth, G. Competition and Choice in Electricity; Wiley: Chichester, UK, 1996. [Google Scholar]

- Shahidehpour, M.; Yamin, H.; Li, Z. Market Operations in Electric Power Systems; Wiley: Chichester, UK, 2002. [Google Scholar]

- Kirschen, D.; Strbac, G. Fundamentals of Power System Economics; Wiley: Chichester, UK, 2018. [Google Scholar]

- Nordström, H.; Söder, L.; Flynn, D.; Matevosyan, J.; Kiviluoma, J.; Holttinen, H.; Vrana, T.K.; van der Welle, A.; Morales-España, G.; Pudjianto, D.; et al. Strategies for Continuous Balancing in Future Power Systems with High Wind and Solar Shares. Energies 2023, 16, 5249. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Couto, A.; Estanqueiro, A. Participation of wind power producers in day-ahead and balancing markets: An overview and a simulation-based study. Wiley Interdiscip. Rev. Energy Environ. 2019, 8, e343. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Couto, A.; Santana, J.; Estanqueiro, A. Effects of Regulating the European Internal Market on the integration of Variable Renewable Energy. WIREs Energy Environ. 2019, 8, e346. [Google Scholar] [CrossRef]

- Grubb, M.; Newbery, D. UK Electricity Market Reform and the Energy Transition: Emerging Lessons. Energy J. 2018, 39, 1–26. [Google Scholar] [CrossRef]

- Strbac, G.; Papadaskalopoulos, D.; Chrysanthopoulos, N.; Estanqueiro, A.; Algarvio, H.; Lopes, F.; de Vries, L.; Morales-Espana, G.; Sijm, J.; Hernandez-Serna, R.; et al. Decarbonization of Electricity Systems in Europe: Market Design Challenges. IEEE Power Energy Mag. 2021, 19, 53–63. [Google Scholar] [CrossRef]

- European Parliament. Internal Energy Market. Available online: https://www.europarl.europa.eu/factsheets/en/sheet/45/internal-energy-market (accessed on 26 March 2025).

- Maris, G.; Flouros, F. The Green Deal, National Energy and Climate Plans in Europe: Member States’ Compliance and Strategies. Adm. Sci. 2021, 11, 75. [Google Scholar] [CrossRef]

- Su, Y.; Teh, J.; Liu, W. Hierarchical and distributed energy management framework for AC/DC hybrid distribution systems with massive dispatchable resources. Electr. Power Syst. Res. 2023, 225, 109856. [Google Scholar] [CrossRef]

- Bohland, M.; Schwenen, S. Renewable support and strategic pricing in electricity markets. Int. J. Ind. Organ. 2022, 80, 102792. [Google Scholar] [CrossRef]

- Brigatto, A.; Fanzeres, B. A soft robust methodology to devise hedging strategies in renewable energy trading based on electricity options. Electr. Power Syst. Res. 2022, 207, 107852. [Google Scholar] [CrossRef]

- Prema, V.; Bhaskar, M.S.; Almakhles, D.; Gowtham, N.; Rao, K.U. Critical Review of Data, Models and Performance Metrics for Wind and Solar Power Forecast. IEEE Access 2022, 10, 667–688. [Google Scholar] [CrossRef]

- Miettinen, J.; Holttinen, H. Impacts of wind power forecast errors on the real-time balancing need: A Nordic case study. IET Renew. Power Gener. 2019, 13, 227–233. [Google Scholar] [CrossRef]

- Martín-Martínez, S.; Lorenzo-Bonache, A.; Honrubia-Escribano, A.; Cañas-Carretón, M.; Gómez-Lázaro, E. Contribution of wind energy to balancing markets: The case of Spain. WIREs Energy Environ. 2018, 7, e300. [Google Scholar] [CrossRef]

- Frade, P.; Pereira, J.; Santana, J.; Catalão, J. Wind balancing costs in a power system with high wind penetration–Evidence from Portugal. Energy Policy 2019, 132, 702–713. [Google Scholar] [CrossRef]

- Ramirez, F.J.; Honrubia-Escribano, A.; Gomez-Lazaro, E.; Pham, A.T. Combining feed-in tariffs and net-metering schemes tobalance development in adoption of photovoltaic energy: Comparative economic assessment and policy implications for European countries. Energy Policy 2017, 102, 440–452. [Google Scholar] [CrossRef]

- Prol, J.; Steininger, K.; Zilberman, D. The cannibalization effect of wind and solar in the California wholesale electricity market. Energy Econ. 2020, 85, 104552. [Google Scholar] [CrossRef]

- Hinderks, W.J.; Wagner, A. Factor models in the German electricity market: Stylized facts, seasonality, and calibration. Energy Econ. 2020, 85, 104351. [Google Scholar] [CrossRef]

- Anatolitis, V.; Azanbayev, A.; Fleck, A.K. How to design efficient renewable energy auctions? Empirical insights from Europe. Energy Policy 2022, 166, 112982. [Google Scholar] [CrossRef]

- Algarvio, H. Risk-Sharing Contracts and risk management of bilateral contracting in electricity markets. Int. J. Electr. Power Energy Syst. 2023, 144, 108579. [Google Scholar] [CrossRef]

- Schlecht, I.; Maurer, C.; Hirth, L. Financial contracts for differences: The problems with conventional CfDs in electricity markets and how forward contracts can help solve them. Energy Policy 2024, 186, 113981. [Google Scholar] [CrossRef]

- Grubb, M.; Drummond, P.; Maximov, S. Separating electricity from gas prices through Green Power Pools: Design options and evolution. Inst. New Econ. Think. Work. Pap. Ser. 2022, 193, 1–34. [Google Scholar]

- Nash, J. Equilibrium points in n-person games. Proc. Natl. Acad. Sci. USA 1950, 36, 48–49. [Google Scholar] [CrossRef] [PubMed]

- Algarvio, H.; Lopes, F.; Santana, J. Strategic Operation of Hydroelectric Power Plants in Energy Markets: A Model and a Study on the Hydro-Wind Balance. Fluids 2020, 5, 209. [Google Scholar] [CrossRef]

- Rathod, A.A.; Subramanian, B. Scrutiny of Hybrid Renewable Energy System for Control, Power Management, Optimization and Sizing: Challenges and Future Possibilities. Sustainability 2022, 14, 16814. [Google Scholar] [CrossRef]

- Lei, X.; Yu, H.; Zhong, J.; Jia, Y.; Shao, Z.; Jian, L. Exploring electric vehicle’s potential as capacity reservation through V2G operation to compensate load deviation in distribution systems. J. Clean. Prod. 2024, 451, 141997. [Google Scholar] [CrossRef]

- Johanndeiter, S.; Bertsch, V. Bidding zero? An analysis of solar power plants’ price bids in the electricity day-ahead market. Appl. Energy 2024, 371, 123672. [Google Scholar] [CrossRef]

- Fabra, N.; Imelda. Market Power and Price Exposure: Learning from Changes in Renewable Energy Regulation. Am. Econ. J. Econ. Policy 2023, 15, 323–358. [Google Scholar] [CrossRef]

- Sousa, V.; Algarvio, H. Strategic Bidding to Increase the Market Value of Variable Renewable Generators in Electricity Markets. Energies 2025, 18, 1586. [Google Scholar] [CrossRef]

- Skytte, K.; Bobo, L. Increasing the value of wind: From passive to active actors in multiple power markets. WIREs Energy Environ. 2019, 8, e328. [Google Scholar] [CrossRef]

- Algarvio, H.; Lopes, F.; Couto, A.; Estanqueiro, A.; Santana, J. Variable Renewable Energy and Market Design: New Products and a Real-World Study. Energies 2019, 12, 4576. [Google Scholar] [CrossRef]

- Hamon, C.; Persson, M. Wind Power Participation in Frequency Regulation: A Profitability Assessment for Sweden. Available online: https://ri.diva-portal.org/smash/get/diva2:1751691/FULLTEXT01.pdf (accessed on 26 February 2025).

- Kraft, E.; Russo, M.; Keles, D.; Bertsch, V. Stochastic optimization of trading strategies in sequential electricity markets. Eur. J. Oper. Res. 2023, 308, 400–421. [Google Scholar] [CrossRef]

- Sleisz, A.; Sores, P.; Raisz, D. Algorithmic properties of the all-European day-ahead electricity market. In Proceedings of the 11th International Conference on the European Energy Market (EEM-14), Krakow, Poland, 28–30 May 2014; pp. 1–6. [Google Scholar]

- Bindu, S.; Chaves Ávila, J.P.; Olmos, L. Factors Affecting Market Participant Decision Making in the Spanish Intraday Electricity Market: Auctions vs. Continuous Trading. Energies 2023, 16, 5106. [Google Scholar] [CrossRef]

- Roumkos, C.; Biskas, P.N.; Marneris, I.G. Integration of European Electricity Balancing Markets. Energies 2022, 15, 2240. [Google Scholar] [CrossRef]

- ENTSO-E. ENTSO-E Network Code on Electricity Balancing. August 2024. Available online: https://eepublicdownloads.entsoe.eu/clean-documents/Network%20codes%20documents/NC%20EB/140806_NCEB_Resubmission_to_ACER_v.03.PDF (accessed on 26 February 2025).

- Matsumoto, T.; Bunn, D.; Yamada, Y. Mitigation of the inefficiency in imbalance settlement designs using day-ahead prices. IEEE Trans. Power Syst. 2022, 37, 3333–3345. [Google Scholar] [CrossRef]

- Dudău, R.; Simionel, T. The politics of the third energy package. Pet. Ind. Rev. 2011, 2011, 70–73. [Google Scholar]

- Nouicer, A.; Kehoe, A.; Nysten, J.; Fouquet, D.; Hancher, L.; Meeus, L. The EU Clean Energy Package, 2020 ed.; Retrieved from Cadmus, European University Institute Research Repository; Florence School of Regulation, Energy: Firenze, Italy, 2020; Available online: https://hdl.handle.net/1814/68899 (accessed on 26 March 2025).

- Erbach, G.; Jensen, L. Fit for 55 package. In BRIEFING Towards Climate Neutrality; EPRS, European Parliament: Brussels, Belgium, 2024. [Google Scholar]

- Frade, P.; Osório, G.; Santana, J.; Catalão, J. Cooperation Regional coordination in ancillary services: An innovative study for secondary control in the Iberian electrical system. Int. J. Electr. Power Energy Syst. 2019, 109, 513–525. [Google Scholar] [CrossRef]

- Frade, P.; Shafie-khah, M.; Santana, J.; Catalão, J. Cooperation in ancillary services: Portuguese strategic perspective on replacement reserves. Energy Strategy Rev. 2019, 23, 142–151. [Google Scholar] [CrossRef]

- Rada, A.G. Spanish hospitals show resilience amid crippling nationwide power outage. BMJ 2025, 389, r867. [Google Scholar] [CrossRef]

- Zhao, X.; Thakurta, P.; Flynn, D. Grid-forming requirements based on stability assessment for 100% converter-based Irish power system. IET Renew. Power Gener. 2022, 16, 447–458. [Google Scholar] [CrossRef]

- Calero, I.; Canizares, C.; Bhattacharya, K.; Baldick, R. Duck-curve mitigation in power grids with high penetration of PV generation. In Proceedings of the 2022 IEEE Power Energy Society General Meeting (PESGM), Seattle, WA, USA, 17–21 July 2022. [Google Scholar]

- Algarvio, H.; Couto, A.; Estanqueiro, A. RES. Trade: An Open-Access Simulator to Assess the Impact of Different Designs on Balancing Electricity Markets. Energies 2024, 17, 6212. [Google Scholar] [CrossRef]

- Kruse, J.; Schäfer, B.; Witthaut, D. Secondary control activation analysed and predicted with explainable AI. Electr. Power Syst. Res. 2022, 212, 108489. [Google Scholar] [CrossRef]

- Lage, M.; Castro, R. A Practical Review of the Public Policies Used to Promote the Implementation of PV Technology in Smart Grids: The Case of Portugal. Energies 2022, 15, 3567. [Google Scholar] [CrossRef]

- Peña, J.I.; Rodríguez, R.; Mayoral, S. Cannibalization, depredation, and market remuneration of power plants. Energy Policy 2022, 167, 113086. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, J.; Wang, X. Review on probabilistic forecasting of wind power generation. Renew. Sustain. Energy Rev. 2014, 32, 255–270. [Google Scholar] [CrossRef]

- Wang, Y.; Xu, H.; Zou, R.; Zhang, F.; Hu, Q. Dynamic non-constraint ensemble model for probabilistic wind power and wind speed forecasting. Renew. Sustain. Energy Rev. 2024, 204, 114781. [Google Scholar] [CrossRef]

- Dhaka, P.; Sreejeth, M.; Tripathi, M. A survey of artificial intelligence applications in wind energy forecasting. Arch. Comput. Methods Eng. 2024, 31, 4853–4878. [Google Scholar] [CrossRef]

{kind=link}

| Features | Past | Actual | New 1 | New 2 |

|---|---|---|---|---|

| Date | By September 2024 | Since September 2024 | - | - |

| Direction | Both | Both | Both | One |

| Gate closure | Day-ahead | Day-ahead | 15-min ahead | 15-min ahead |

| Payment | Single marginal | Single marginal | Double marginal | Double marginal |

| Period | 24 h | 24 h | 1 h | 1 h |

| Procurement | Asymmetrical | Symmetrical | Separated | Separated |

| size | Asymmetrical | Symmetrical | Dynamic | Dynamic |

| Strategy | Market Design | Deviation in IDC | |

|---|---|---|---|

| Positive | Negative | ||

| S1 | Past | Bid excess to upward SR | No participation in SR |

| S2 | Actual | Same as S1 | Same as S1 |

| S3 | Actual | Like S2 but not restricted to available capacity | Same as S1 |

| S4 | New 1 | Bid to upward and downward SR | Buy deficit in IDC and bid new position to downward SR |

| S5 | New 2 | Same as S1 | Same as S1 |

| S6 | New 2 | Same as S1 | Same as S4 |

| S7 | New 2 | Sell excess and bid to downward SR | Same as S4 |

| Variables | Market Design | |||

|---|---|---|---|---|

| Past | Actual | New 1 | New 2 | |

| Remuneration (EUR/MWh) | 85.77 | 104.76 | 106.75 | 80.07 |

| DAM trades (MWh) | 61.13 | 56.70 | 63.82 | 62.26 |

| IDA trades (MWh) | 9.40 | 8.03 | 7.45 | 15.40 |

| IDC trades (MWh) | 5.91 | 5.02 | 5.01 | 11.68 |

| Allocated Capacity (MW) | 147.23 | 216.56 | 176.55 | 119.10 |

| Activated Reserve (MWh) | 24.10 | 18.75 | 21.36 | 12.07 |

| Imbalances (MWh) | 20.69 | 26.81 | 24.82 | 18.27 |

| Curtailment (MWh) | 3.62 | 3.27 | 2.85 | 1.89 |

| Variables | Strategy | ||||||

|---|---|---|---|---|---|---|---|

| S1 | S2 | S3 | S4 | S5 | S6 | S7 | |

| Ideal (EUR/MWh) | 85.77 | 104.76 | 104.76 | 106.75 | 80.07 | 80.07 | 80.07 |

| Remuneration (EUR/MWh) | 42.65 | 43.94 | 47.94 | 63.01 | 40.71 | 49.97 | 62.29 |

| Difference to ideal (%) | −50% | −58% | −54% | −41% | −49% | −38% | −22% |

| DAM traded energy (MWh) | 98.73 | 100.77 | 100.77 | 99.57 | 99.38 | 99.38 | 99.38 |

| IDA traded energy (MWh) | 22.39 | 23.33 | 23.33 | 22.78 | 22.68 | 22.68 | 22.68 |

| IDC traded energy (MWh) | 16.59 | 18.47 | 18.47 | 15.77 | 15.80 | 15.80 | 28.08 |

| Allocated capacity (MW) | 17.05 | 19.70 | 50.15 | 70.32 | 12.28 | 38.34 | 67.98 |

| Activated reserve (MWh) | 6.43 | 5.68 | 6.18 | 8.59 | 6.40 | 7.87 | 4.43 |

| Imbalances (MWh) | 2.84 | 2.54 | 9.11 | 3.44 | 2.83 | 3.21 | 2.77 |

| Curtailment (MWh) | 3.94 | 3.13 | 3.16 | 5.95 | 4.33 | 5.33 | 3.32 |

| Total Revenue (M EUR) | Strategy | ||||||

|---|---|---|---|---|---|---|---|

| S1 | S2 | S3 | S4 | S5 | S6 | S7 | |

| DAM | 64.22 | 65.47 | 65.47 | 64.74 | 64.62 | 64.62 | 64.62 |

| IDA | −13.66 | −14.15 | −14.15 | −13.86 | −13.82 | −13.82 | −13.82 |

| IDC | −10.30 | −10.32 | −10.32 | −10.76 | −10.71 | −10.71 | −4.75 |

| Upward capacity | 6.10 | 5.23 | 12.62 | 6.66 | 6.68 | 6.68 | 0.00 |

| Downward capacity | 3.05 | 5.23 | 12.62 | 28.77 | 0.00 | 12.29 | 34.17 |

| Balancing energy | 4.32 | 3.99 | 4.08 | 3.65 | 4.55 | 3.88 | −1.62 |

| Positive imbalances cost | 0.65 | 0.55 | 0.56 | 0.86 | 0.62 | 0.77 | 0.64 |

| Negative imbalances cost | −0.90 | −0.91 | −10.76 | −1.03 | −0.89 | −1.05 | −1.15 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Algarvio, H.; Sousa, V. Strategic Bidding to Increase the Market Value of Variable Renewable Generators in New Electricity Market Designs. Energies 2025, 18, 2848. https://doi.org/10.3390/en18112848

Algarvio H, Sousa V. Strategic Bidding to Increase the Market Value of Variable Renewable Generators in New Electricity Market Designs. Energies. 2025; 18(11):2848. https://doi.org/10.3390/en18112848

Chicago/Turabian StyleAlgarvio, Hugo, and Vivian Sousa. 2025. "Strategic Bidding to Increase the Market Value of Variable Renewable Generators in New Electricity Market Designs" Energies 18, no. 11: 2848. https://doi.org/10.3390/en18112848

APA StyleAlgarvio, H., & Sousa, V. (2025). Strategic Bidding to Increase the Market Value of Variable Renewable Generators in New Electricity Market Designs. Energies, 18(11), 2848. https://doi.org/10.3390/en18112848