Clean Heat Standards: Foundations, Policy Mechanisms, and Recent Developments

,

,

Abstract

1. Introduction

2. Clean Energy Performance Standards

2.1. Fuel Economy and Zero-Emission Vehicle Standards

2.2. Energy Efficiency Obligations

2.3. Minimum Energy Efficiency Standards

2.4. Renewable Portfolio Standards

3. Design Features of Clean Heat Standards

3.1. Scope of the CHS

3.2. Definition of the Obligation

3.3. Obligated Parties

3.3.1. Energy Companies

3.3.2. Heating Appliance Manufacturers

3.3.3. Comparison

3.4. Eligible Actions

- In some US states, the inclusion of biofuels as a partial clean heat option has been hotly contested. Many policymakers see biofuels as a necessary transition option where a large fraction of the installed heating equipment could burn biofuels without requiring a furnace replacement. They propose “scoring” each offered biofuel by comparison to fossil fuels, with a lifecycle emissions factor calculated using models developed by the US EPA and the Argonne National Laboratory [48]. Biofuels could earn partial or full credit depending on their emission profile. Some environmental advocates, on the other hand, oppose giving clean heat credit to woody biomass and biofuels of any type.

- A similar controversy surrounds renewable natural gas. Gas utilities have proposed to capture fugitive methane from landfills, coalbeds, and/or agricultural operations and deliver it via pipelines to end-use customers to meet clean heat obligations. Since methane is a powerful greenhouse gas, they argue that capturing methane that would otherwise be vented and using that gas to displace fossil methane for heat will deliver substantial clean heat benefits. Some advocates oppose this option, fearing that it would undermine other policies to regulate fugitive methane emissions at their source.

- Jurisdictions also vary in the degree to which the CHS program encourages or supports inclusion of building weatherization as a clean heat resource. In Massachusetts, the Climate Plan proposed giving clean heat credits to weatherization in proportion to the emissions avoided, but the Draft Framework did not do so, on the ground that weatherization was supported in the state through other programs. Proposed CHS plans in Maryland and Vermont, on the other hand, would award clean heat credits to weatherization actions, particularly in low-income housing.

3.5. Flexibility Mechanisms

3.6. Compliance and Monitoring

3.7. Equity

4. Existing Clean Heat Standards

5. CHS in the Policy Mix

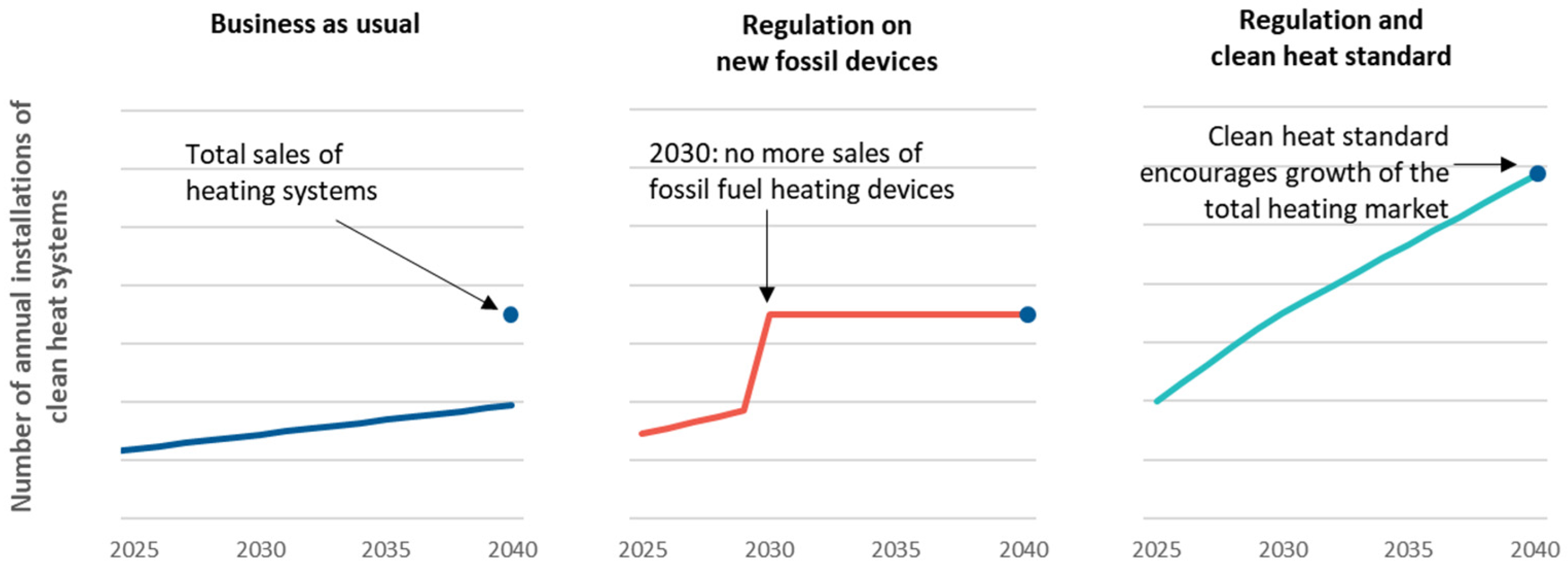

5.1. Interaction with Regulations on New Fossil Fuel Heating Systems

- Business as usual (BAU): The market for clean heat systems grows slowly with insufficient sales to replace the market for fossil heating systems entirely by 2040. Fossil heating systems are still sold to meet demand for heating devices in 2040.

- End date (effective 2030): A regulation halts fossil fuel boiler sales from 2030 onward. While the market transitions to clean heating systems, the total market size remains constant as manufacturers and installers shift to installing alternatives like heat pumps. Additionally, there could be an increase in fossil heating device sales before the end date, driven by consumer skepticism regarding clean heating technologies’ cost and performance.

- End date combined with CHS (effective 2025): Introducing a clean heat standard alongside the phaseout policy accelerates the transition. The clean heat standard ensures that the fossil fuel heating market is replaced by clean alternatives while also expanding the overall market size. By 2040, the total market doubles, facilitating the replacement of most fossil heating systems.

5.2. Complementary Policies and Financial Support Programmes

5.3. Heat Planning

5.4. Energy and Carbon Pricing

5.5. Potential Impact of CHS

6. Discussion

7. Conclusions and Policy Recommendations

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| CHS | clean heat standards |

| EU | European Union |

| EEOs | Energy Efficiency Obligations |

| GHG | greenhouse gases |

| UK | United Kingdom |

| US | United States of America |

References

- IEA. A Renewed Pathway to Net Zero Emissions; IEA: Paris, France, 2023. [Google Scholar]

- Filippidou, F.; Jimenez Navarro, J. Achieving the Cost-Effective Energy Transformation of Europe’s Buildings: Combinations of Insulation and Heating & Cooling Technologies Renovations: Methods and Data; JRC European Commission: Brussels, Belgium, 2019. [Google Scholar]

- Rosenow, J.; Hamels, S. Where to Meet on Heat? A Conceptual Framework for Optimising Demand Reduction and Decarbonised Heat Supply. Energy Res. Soc. Sci. 2023, 104, 103223. [Google Scholar] [CrossRef]

- IEA. The Future of Heat Pumps; IEA: Paris, France, 2022. [Google Scholar]

- Schlosser, F.; Jesper, M.; Vogelsang, J.; Walmsley, T.G.; Arpagaus, C.; Hesselbach, J. Large-Scale Heat Pumps: Applications, Performance, Economic Feasibility and Industrial Integration. Renew. Sustain. Energy Rev. 2020, 133, 110219. [Google Scholar] [CrossRef]

- Arpagaus, C.; Bless, F.; Uhlmann, M.; Schiffmann, J.; Bertsch, S.S. High Temperature Heat Pumps: Market Overview, State of the Art, Research Status, Refrigerants, and Application Potentials. Energy 2018, 152, 985–1010. [Google Scholar] [CrossRef]

- Gernaat, D.E.H.J.; de Boer, H.-S.; Dammeier, L.C.; van Vuuren, D.P. The Role of Residential Rooftop Photovoltaic in Long-Term Energy and Climate Scenarios. Appl. Energy 2020, 279, 115705. [Google Scholar] [CrossRef]

- Mills, B.F.; Schleich, J. Profits or Preferences? Assessing the Adoption of Residential Solar Thermal Technologies. Energy Policy 2009, 37, 4145–4154. [Google Scholar] [CrossRef]

- Munćan, V.; Mujan, I.; Macura, D.; Anđelković, A.S. The State of District Heating and Cooling in Europe—A Literature-Based Assessment. Energy 2024, 304, 132191. [Google Scholar] [CrossRef]

- Zhang, L.; Li, Y.; Zhang, H.; Xu, X.; Yang, Z.; Xu, W. A Review of the Potential of District Heating System in Northern China. Appl. Therm. Eng. 2021, 188, 116605. [Google Scholar] [CrossRef]

- Snape, J.R.; Boait, P.J.; Rylatt, R.M. Will Domestic Consumers Take up the Renewable Heat Incentive? An Analysis of the Barriers to Heat Pump Adoption Using Agent-Based Modelling. Energy Policy 2015, 85, 32–38. [Google Scholar] [CrossRef]

- Karytsas, S.; Choropanitis, I. Barriers against and Actions towards Renewable Energy Technologies Diffusion: A Principal Component Analysis for Residential Ground Source Heat Pump (GSHP) Systems. Renew. Sustain. Energy Rev. 2017, 78, 252–271. [Google Scholar] [CrossRef]

- Lowes, R.; Gibb, D.; Rosenow, J.; Thomas, S.; Malinowski, M.; Ross, A.; Graham, P. A Policy Toolkit for Global Mass Heat Pump Deployment; Regulatory Assistance Project: Brussels, Belgium, 2022. [Google Scholar]

- Melvin, J. The Split Incentives Energy Efficiency Problem: Evidence of Underinvestment by Landlords. Energy Policy 2018, 115, 342–352. [Google Scholar] [CrossRef]

- Knobloch, F.; Pollitt, H.; Chewpreecha, U.; Daioglou, V.; Mercure, J.-F. Simulating the Deep Decarbonisation of Residential Heating for Limiting Global Warming to 1.5 °C. Energy Effic. 2019, 12, 521–550. [Google Scholar] [CrossRef]

- Bataille, C.; Åhman, M.; Neuhoff, K.; Nilsson, L.J.; Fischedick, M.; Lechtenböhmer, S.; Solano-Rodriquez, B.; Denis-Ryan, A.; Stiebert, S.; Waisman, H.; et al. A Review of Technology and Policy Deep Decarbonization Pathway Options for Making Energy-Intensive Industry Production Consistent with the Paris Agreement. J. Clean. Prod. 2018, 187, 960–973. [Google Scholar] [CrossRef]

- Stavins, R.N. Chapter 9—Experience with Market-Based Environmental Policy Instruments. In Handbook of Environmental Economics; Mäler, K.-G., Vincent, J.R., Eds.; Elsevier: Amsterdam, The Netherlands, 2003; Volume 1, pp. 355–435. ISBN 1574-0099. [Google Scholar]

- Jaffe, A.B.; Newell, R.G.; Stavins, R.N. A Tale of Two Market Failures: Technology and Environmental Policy. Ecol. Econ. 2005, 54, 164–174. [Google Scholar] [CrossRef]

- Rosenow, J.; Cowart, R.; Thomas, S. Market-Based Instruments for Energy Efficiency: A Global Review. Energy Effic. 2019, 12, 1379–1398. [Google Scholar] [CrossRef]

- Santini, M.; Thomas, S.; Lowes, R.; Gibb, D.; Cowart, R.; Rosenow, J. Clean Heat Standards Handbook; Regulatory Assistance Project: Brussels, Belgium, 2024. [Google Scholar]

- Stebbins, G.; Neme, C. A Comparison of Clean Heat Standards: Current Progress and Key Elements; Prepared for the Environmental Defense Fund; Energy Futures Group, Inc.: Hinesburg, VT, USA, 2024. [Google Scholar]

- Agora Energiewende Boosting the Clean Heat Market. A Policy for Guiding the Transition of the EU Heating Industry; Agora Energiewende: Berlin, Germany, 2025. [Google Scholar]

- Cowart, R.; Neme, C. The Clean Heat Standard; Regulatory Assistance Project: Brussels, Belgium, 2021. [Google Scholar]

- Greene, D.L.; Greenwald, J.M.; Ciez, R. US Fuel Economy and Greenhouse Gas Standards: What Have They Achieved and What Have We Learned? Energy Policy 2020, 146, 111783. [Google Scholar] [CrossRef]

- Fritz, M.; Plötz, P.; Funke, S.A. The Impact of Ambitious Fuel Economy Standards on the Market Uptake of Electric Vehicles and Specific CO2 Emissions. Energy Policy 2019, 135, 111006. [Google Scholar] [CrossRef]

- Paltsev, S.; Henry Chen, Y.-H.; Karplus, V.; Kishimoto, P.; Reilly, J.; Löschel, A.; von Graevenitz, K.; Koesler, S. Reducing CO2 from Cars in the European Union. Transportation 2018, 45, 573–595. [Google Scholar] [CrossRef]

- Sykes, M.; Axsen, J. No Free Ride to Zero-Emissions: Simulating a Region’s Need to Implement Its Own Zero-Emissions Vehicle (ZEV) Mandate to Achieve 2050 GHG Targets. Energy Policy 2017, 110, 447–460. [Google Scholar] [CrossRef]

- Axsen, J.; Hardman, S.; Jenn, A. What Do We Know about Zero-Emission Vehicle Mandates? Environ. Sci. Technol. 2022, 56, 7553–7563. [Google Scholar] [CrossRef]

- Zhao, F.; Chen, K.; Hao, H.; Wang, S.; Liu, Z. Technology Development for Electric Vehicles under New Energy Vehicle Credit Regulation in China: Scenarios through 2030. Clean. Technol. Environ. Policy 2019, 21, 275–289. [Google Scholar] [CrossRef]

- Yang, Z.; Mock, P.; German, J.; Bandivadekar, A.; Lah, O. On a Pathway to De-Carbonization—A Comparison of New Passenger Car CO2 Emission Standards and Taxation Measures in the G20 Countries. Transp. Res. D Transp. Environ. 2018, 64, 53–69. [Google Scholar] [CrossRef]

- Rosenow, J.; Cowart, R.; Thomas, S.; Kreuzer, F. Market-Based Instruments for Energy Efficiency. Policy Choice and Design; IEA/OECD: Paris, France, 2017. [Google Scholar]

- Downs, A.; Cui, C. Energy Efficiency Resource Standards: A New Progress Report on State Experience; Report Number U1403; American Council for an Energy-Efficient Economy: Washington, DC, USA, 2014. [Google Scholar]

- Rosenow, J.; Bayer, E. Costs and Benefits of Energy Efficiency Obligations: A Review of European Programmes. Energy Policy 2017, 107, 53–62. [Google Scholar] [CrossRef]

- Wiel, S.; McMahon, J.E. Governments Should Implement Energy-Efficiency Standards and Labels—Cautiously. Energy Policy 2003, 31, 1403–1415. [Google Scholar] [CrossRef]

- Nadel, S. Appliance and Equipment Efficiency Standards. Annu. Rev. Energy Environ. 2002, 27, 159–192. [Google Scholar] [CrossRef]

- IEA. Achievements of Energy Efficiency Appliance and Equipment Standards and Labelling Programmes; International Energy Agency: Paris, France, 2021. [Google Scholar]

- Howarth, N.A.A.; Rosenow, J. Banning the Bulb: Institutional Evolution and the Phased Ban of Incandescent Lighting in Germany. Energy Policy 2014, 67, 737–746. [Google Scholar] [CrossRef]

- IEA. Energy Efficiency 2021; International Energy Agency: Paris, France, 2021. [Google Scholar]

- Rosenow, J.; Fawcett, T.; Eyre, N.; Oikonomou, V. Energy Efficiency and the Policy Mix. Build. Res. Inf. 2016, 44, 562–574. [Google Scholar] [CrossRef]

- Rosenow, J.; Kern, F.; Rogge, K. The Need for Comprehensive and Well Targeted Instrument Mixes to Stimulate Energy Transitions: The Case of Energy Efficiency Policy. Energy Res. Soc. Sci. 2017, 33, 95–104. [Google Scholar] [CrossRef]

- Upton, G.B.; Snyder, B.F. Funding Renewable Energy: An Analysis of Renewable Portfolio Standards. Energy Econ. 2017, 66, 205–216. [Google Scholar] [CrossRef]

- Dong, Y.; Shimada, K. Evolution from the Renewable Portfolio Standards to Feed-in Tariff for the Deployment of Renewable Energy in Japan. Renew. Energy 2017, 107, 590–596. [Google Scholar] [CrossRef]

- Buckman, G. The Effectiveness of Renewable Portfolio Standard Banding and Carve-Outs in Supporting High-Cost Types of Renewable Electricity. Energy Policy 2011, 39, 4105–4114. [Google Scholar] [CrossRef]

- Lee, Y.; Seo, I. Sustainability of a Policy Instrument: Rethinking the Renewable Portfolio Standard in South Korea. Sustainability 2019, 11, 3082. [Google Scholar] [CrossRef]

- Santini, M.; Cowart, R.; Thomas, S.; Gibb, D.; Lowes, R.; Rosenow, J. Clean Heat Standards: New Tools for the Fossil Heat Phaseout in Europe; Regulatory Assistance Project: Brussels, Belgium, 2023. [Google Scholar]

- Rosenow, J.; Thomas, S.; Gibb, D.; Baetens, R.; De Brouwer, A.; Cornillie, J. Clean Heating: Reforming Taxes and Levies on Heating Fuels in Europe. Energy Policy 2023, 173, 113367. [Google Scholar] [CrossRef]

- Rosenow, J.; Barnes, J.; Galvin, R.; O’Mara, S.; Lowes, R. Total Cost of Ownership of Heat Pumps and Policy Choice: The Case of Great Britain. iScience 2025, 28, 111784. [Google Scholar] [CrossRef]

- Argonne National Laboratory R&D GREET Lifecycle Assessment Model. Available online: https://www.anl.gov/topic/greet (accessed on 20 February 2025).

- Wiese, C.; Cowart, R.; Rosenow, J. The Strategic Use of Auctioning Revenues to Foster Energy Efficiency: Status Quo and Potential within the European Union Emissions Trading System. Energy Effic. 2020, 13, 1677–1688. [Google Scholar] [CrossRef]

- Colorado Senate. Senate Bill 21-264; Colorado General Assembly: Denver, CO, USA, 2021.

- Vermont Climate Council. Initial Vermont Climate Action Plan; Vermont Climate Council: Montpelier, VT, USA, 2021.

- Vermont General Assembly. S.5 (Act 18); Vermont General Assembly: Montpelier, VT, USA, 2023.

- State of Vermont Public Utility Commission. Report to the Vermont Legislature-Second Checkback Report on the Clean Heat Standard Under Act 18 of 2023, Section 6(i); Public Utility Commission: Montpelier, VT, USA, 2025.

- Executive Office of Energy and Environmental Affairs. Appendices to the Massachusetts Clean Energy and Climate Plan for 2025 and 2030. 2022. Available online: https://www.mass.gov/doc/appendices-to-the-clean-energy-and-climate-plan-for-2025-and-2030/download (accessed on 8 February 2025).

- Executive Office of Energy and Environmental Affairs. Massachusetts Clean Energy and Climate Plan for 2025 and 2030; Massachusetts Municipal Association: Boston, MA, USA, 2022.

- Massachusetts Commission on Clean Heat. Final Report; Massachusetts Municipal Association: Boston, MA, USA, 2022.

- Massachusetts Department of Environmental Protection Massachusetts Clean Heat Standard. Available online: https://www.mass.gov/info-details/massachusetts-clean-heat-standard (accessed on 8 February 2025).

- Massachusetts Department of Environmental Protection. MassDEP Clean Heat Standard (CHS). Draft Framework; Massachusetts Department of Environmental Protection: Boston, MA, USA, 2023.

- Maryland Climate Commission. Maryland Building Energy Transition Plan; Maryland Climate Commission: Baltimore, MD, USA, 2021.

- United States Maryland Department of the Environment. Maryland’s Climate Pollution Reduction Plan; United States Maryland Department of the Environment: Baltimore, MD, USA, 2023.

- United States Climate Alliance U.S. Climate Alliance Announces New Commitments to Decarbonize Buildings Across America, Quadruple Heat Pump Installations by 2030. Available online: https://usclimatealliance.org/press-releases/decarbonizing-americas-buildings-sep-2023/ (accessed on 20 February 2025).

- Department for Energy Security and Net Zero. Clean Heat Market Mechanism. Impact Asssessment; Department for Energy Security and Net Zero: London, UK, 2023.

- Légifrance Décret No 2022-640 Du 25 Avril 2022 Relatif Au Dispositif de Certificats de Production de Biogaz. 2022. Available online: https://www.legifrance.gouv.fr/jorf/id/JORFTEXT000045653118#:~:text=Entr%C3%A9e%20en%20vigueur%20%3A%20le%20texte,%C3%A0%20l'Etat%20de%20certificats (accessed on 8 February 2025).

- Légifrance Décret N° 2024-718 Du 6 Juillet 2024 Relatif à l’obligation de Restitution de Certificats de Production de Biogas. 2024. Available online: https://www.legifrance.gouv.fr/jorf/id/JORFTEXT000049891497 (accessed on 8 February 2025).

- Department of the Environment, Climate and Communications. Government Agrees to the Introduction of an Obligation on the Heat Sector by 2024. Available online: https://www.gov.ie/en/press-release/83757-government-agrees-to-the-introduction-of-an-obligation-on-the-heat-sector-by-2024 (accessed on 8 February 2025).

- Government of Ireland Consultation on the Introduction of a Renewable Heat Obligation. Available online: https://www.gov.ie/en/consultation/7bc5b-consultation-on-the-introduction-of-a-renewable-heat-obligation (accessed on 8 February 2025).

- Committee on Climate Change. 2024 Progress Report to Parliament; Committee on Climate Change: London, UK, 2024. [Google Scholar]

- Rogge, K.S.; Reichardt, K. Policy Mixes for Sustainability Transitions: An Extended Concept and Framework for Analysis. Res. Policy 2016, 45, 1620–1635. [Google Scholar] [CrossRef]

- Li, L.; Taeihagh, A. An In-Depth Analysis of the Evolution of the Policy Mix for the Sustainable Energy Transition in China from 1981 to 2020. Appl. Energy 2020, 263, 114611. [Google Scholar] [CrossRef]

- van den Bergh, J.; Castro, J.; Drews, S.; Exadaktylos, F.; Foramitti, J.; Klein, F.; Konc, T.; Savin, I. Designing an Effective Climate-Policy Mix: Accounting for Instrument Synergy. Clim. Policy 2021, 21, 745–764. [Google Scholar] [CrossRef]

- Braungardt, S.; Tezak, B.; Rosenow, J.; Bürger, V. Banning Boilers: An Analysis of Existing Regulations to Phase out Fossil Fuel Heating in the EU. Renew. Sustain. Energy Rev. 2023, 183, 113442. [Google Scholar] [CrossRef]

- IEA Germany’s 2nd Amendment to the Building Energy Act (GEG)—Phase-out of Fossil Fuels. Available online: https://www.iea.org/policies/18133-germanys-2nd-amendment-to-the-building-energy-act-geg-phase-out-of-fossil-fuels (accessed on 12 February 2025).

- Sunderland, L.; Gibb, D. Taking the Burn out of Heating for Low-Income Households; Regulatory Assistance Project: Brussels, Belgium, 2022. [Google Scholar]

- Chittum, A.; Østergaard, P.A. How Danish Communal Heat Planning Empowers Municipalities and Benefits Individual Consumers. Energy Policy 2014, 74, 465–474. [Google Scholar] [CrossRef]

- Rosenow, J.; Lowes, R.; Kemfert, C. The Elephant in the Room: How Do We Regulate Gas Transportation Infrastructure as Gas Demand Declines? One Earth 2024, 7, 1158–1161. [Google Scholar] [CrossRef]

- Lilliestam, J.; Patt, A.; Bersalli, G. The Effect of Carbon Pricing on Technological Change for Full Energy Decarbonization: A Review of Empirical Ex-Post Evidence. WIREs Clim. Chang. 2021, 12, e681. [Google Scholar] [CrossRef]

- Rosenow, J.; Platt, R.; Flanagan, B. Fuel Poverty and Energy Efficiency Obligations—A Critical Assessment of the Supplier Obligation in the UK. Energy Policy 2013, 62, 1194–1203. [Google Scholar] [CrossRef]

- Massachusetts Department of Environmental Protection. Massachusetts Clean Heat Standard Technical Session: Draft Framework Review; Massachusetts Department of Environmental Protection: Boston, MA, USA, 2023.

- Rosenow, J.; Gibb, D.; Nowak, T.; Lowes, R. Heating up the Global Heat Pump Market. Nat. Energy 2022, 7, 901–904. [Google Scholar] [CrossRef]

- Kranzl, L.; Hummel, M.; Müller, A.; Steinbach, J. Renewable Heating: Perspectives and the Impact of Policy Instruments. Energy Policy 2013, 59, 44–58. [Google Scholar] [CrossRef]

- Mills, E. Market Spoiling and Ineffectual Policy Have Impeded the Adoption of Heat Pump Water Heating for US Buildings and Industry. Energy Effic. 2022, 15, 23. [Google Scholar] [CrossRef]

- Sovacool, B.K.; Martiskainen, M. Hot Transformations: Governing Rapid and Deep Household Heating Transitions in China, Denmark, Finland and the United Kingdom. Energy Policy 2020, 139, 111330. [Google Scholar] [CrossRef]

- Rosenow, J.; Eyre, N. Reinventing Energy Efficiency for Net Zero. Energy Res. Soc. Sci. 2022, 90, 102602. [Google Scholar] [CrossRef]

- Kim, K.-H.; Jahan, S.A.; Kabir, E. A Review of Diseases Associated with Household Air Pollution Due to the Use of Biomass Fuels. J. Hazard. Mater. 2011, 192, 425–431. [Google Scholar] [CrossRef]

- Rosenow, J. A Meta-Review of 54 Studies on Hydrogen Heating. Cell Rep. Sustain. 2024, 1, 100010. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Type of Energy Company | Description |

|---|---|

| Pipeline gas distribution utilities | This includes both investor-owned and publicly operated utilities. The obligation could be placed on the regulated distribution company or, where gas supply is competitive, on the gas retail supplier. |

| Providers of delivered fossil fuels | Entities supplying distillate heating oil and propane could be regulated at the wholesale level—either at the point of importation into the obligating jurisdiction or, if a legal regime permits it, earlier in the wholesale chain. Alternatively, the obligation could be assigned to retailers of those fuels. Tracking methods used in existing tax and energy policies to identify fuels sold for heating could support the clean heat standard. |

| Solid and liquid bioenergy companies | These companies could be included if broader environmental objectives, such as reducing local air pollution, are prioritized. |

| Electricity retailers or distribution companies | Over time, as heating load moves from fossil companies to electricity providers, the electricity providers will increasingly have the revenue needed to provide incentives to building owners to support fuel switching. |

| Clean Heat Standard on Energy Companies | Clean Heat Standard on Heating Appliance Manufacturers | |

|---|---|---|

| Eligible actions | Possibility to include broad set of actions | Limited to heating appliance sales, where authorized |

| Role in heat decarbonization framework | Possibility to set trajectory for clean heat and to cover a broad range of sectors | Limited to setting a trajectory for new heating appliances |

| Market leverage | Can build on energy companies’ access to consumers | Can build on relationship between manufacturers and installers |

| Costs distributional impact | Costs reflected in energy bills, will disproportionately affect low-income households unless mitigated | Costs borne by consumers who purchase fossil fuel technologies Disproportionately affects low-income households |

| Biogas Certificate Scheme, France | Renewable Heat Obligation, Ireland | Clean Heat Targets, Colorado, US | Clean Heat Standard, Vermont, US | Clean Heat Standard, Massachusetts, US | Market-Based Mechanism for Low-Carbon Heat, UK | |

|---|---|---|---|---|---|---|

| Status | Implemented | Announced | Implemented | Pending | Under development | Pending |

| Obligated parties | Gas suppliers | Suppliers of heating fuels (including oil, liquefied petroleum gas, gas, coal, and peat) | Gas distribution utilities | Gas utility and fossil fuel heat providers | Retail sellers of natural gas, heating oil, propane, and electricity | Heating appliance manufacturers |

| Obligation | File green certificates, obtained by injecting biogas into a gas network or purchased from biogas producers | Achieve a heat obligation rate | File clean heat plans with Colorado’s Public Utilities Commission demonstrating GHG reductions by 2025 (4%) and 2030 (22%), compared to a 2015 baseline | Acquire and retire credits from actions that reduce GHG in the thermal sector, including low emission heating fuels, energy efficiency, weatherization, and electric or renewable heating systems | Acquire and retire credits from actions reducing GHG, with a ”full electrification” sub-target, including weatherization, energy efficiency, and energy-efficient new construction | Increased proportion of overall heating appliance sales must be low-carbon heat pumps |

| Unit of measurement | MWh | Ratio of renewable to non-renewable heat | GHG reductions | Lifecycle GHG reductions | Lifecycle GHG reductions | Ratio of heat pumps to fossil fuel appliances sales |

| Equity | No particular provision | No particular provision foreseen, but government notes that it will assess the impacts further | Prioritize investments ensuring benefits to disproportionately impacted and income-qualified customers | >16% of total reductions must come from low-income customers and >16% from moderate-income customers | 25% of the full electrification standard must be met by projects that serve customers who are eligible for low-income discount electricity rates | No particular provision foreseen; need strong consumer protection safeguards and standards |

| Jurisdiction | Carbon Savings as Reported | Time Period | Source of Data | Carbon Savings Per Year |

|---|---|---|---|---|

| UK | 2.1–5.1 million t CO2 (lifetime savings) | 2024–2025 | [62] | 0.14–0.34 million t CO2 (assuming 15-year lifetime of heating equipment) |

| Vermont | 2.1 million t CO2 (savings over 10 years) | 2026–2035 | [53] | 0.21 million t CO2 |

| Maryland | 0.8 million t CO2 (annual savings) | 2031 and 2045 | [60] | 0.8 million t CO2 |

| Massachusetts | 1 million t CO2 (annual savings) | 2026–2050 | [78] | 1 million t CO2 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rosenow, J.; Santini, M.; Cowart, R.; Thomas, S.; Gibb, D.; Lowes, R. Clean Heat Standards: Foundations, Policy Mechanisms, and Recent Developments. Energies 2025, 18, 2764. https://doi.org/10.3390/en18112764

Rosenow J, Santini M, Cowart R, Thomas S, Gibb D, Lowes R. Clean Heat Standards: Foundations, Policy Mechanisms, and Recent Developments. Energies. 2025; 18(11):2764. https://doi.org/10.3390/en18112764

Chicago/Turabian StyleRosenow, Jan, Marion Santini, Richard Cowart, Sam Thomas, Duncan Gibb, and Richard Lowes. 2025. "Clean Heat Standards: Foundations, Policy Mechanisms, and Recent Developments" Energies 18, no. 11: 2764. https://doi.org/10.3390/en18112764

APA StyleRosenow, J., Santini, M., Cowart, R., Thomas, S., Gibb, D., & Lowes, R. (2025). Clean Heat Standards: Foundations, Policy Mechanisms, and Recent Developments. Energies, 18(11), 2764. https://doi.org/10.3390/en18112764