Cost-Driven Assessment of Technologies’ Potential to Reach Climate Neutrality in Energy-Intensive Industries

,

,  , and

, and

Abstract

1. Introduction

- The current subsector-overarching literature on industrial climate neutrality often lacks sector-specific information—we aim to provide a novel level of detail for subsectors’ processes while the ability to deduce an overarching picture for EIIs is preserved by grouping technologies into four climate neutrality pathways.

- Techno-economic analyses of technology options are mostly limited to studies that only investigate one specific subsector (e.g., iron and steel)—we aim to provide accompanying investment costs, fuel, and GHG certificate costs for technologies needed for climate neutrality in EIIs and compare them to conventional fossil-based routes.

2. Methodology

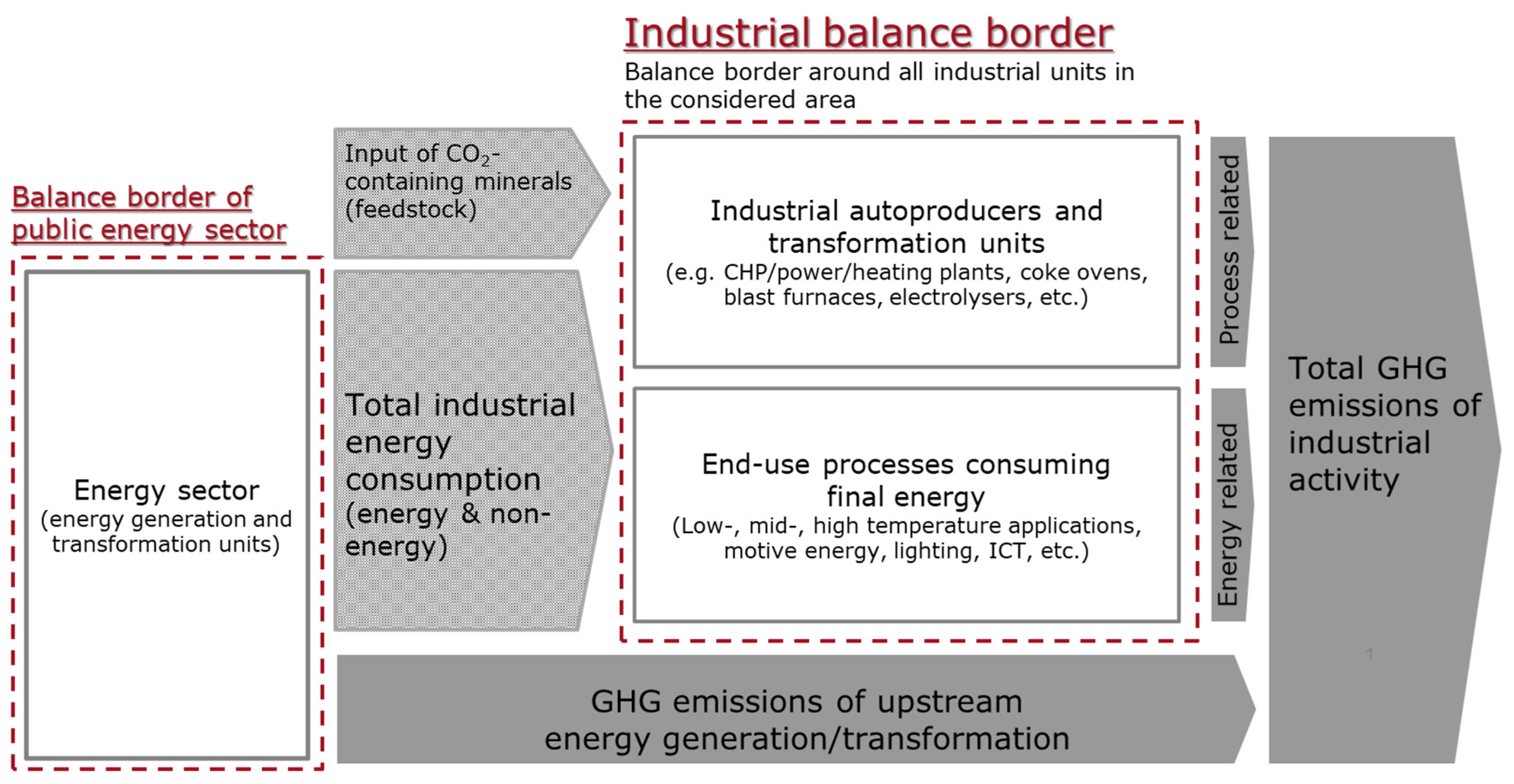

2.1. Clustering of Climate Neutrality Pathways; Potential and Balance Border Definitions

- Electrification;

- The use of CO2-neutral gases and biomass combustion;

- Circular economy measures;

- Carbon capture.

2.2. Modelling Approach

- Space heating;

- Stationary engines;

- Process heat < 200 °C;

- Process heat > 200 °C;

- Subsector-specific production processes (e.g., steelmaking or cement production).

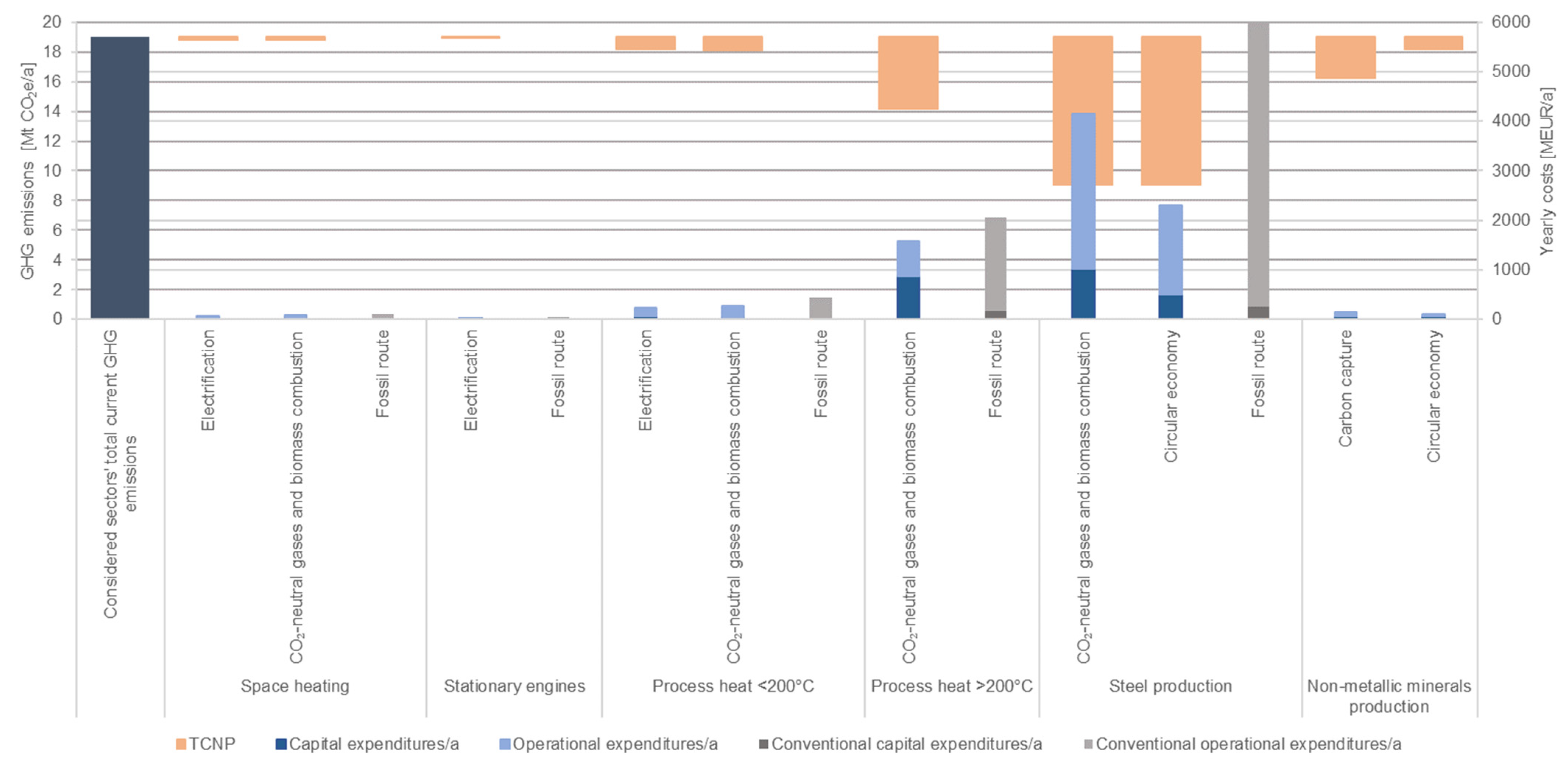

- The technical climate neutrality potential (TCNP) per pathway and EII subsector in kt CO2e/a as the core indicator identifying the technologies and applications with the greatest lever for attaining climate neutrality.

- The corresponding change in energy consumption by energy carrier in GWh/a to indicate the impact of technology options on the energy system. In addition, the energy consumption of the upstream production of required energy carriers (e.g., electricity for hydrogen electrolysis) is denoted individually.

- Corresponding capital expenditures in MEUR/a show the expectable investment costs that can be put against the regular investment costs of the reference fossil-based technology.

- Corresponding operational expenditures, including fuel and GHG certificate costs, as well as maintenance costs in MEUR/a, to visualise expenditures due to the operation of the technology.

- The resulting total annual expenditures in MEUR/a, taking into account depreciation rates, to show the total costs of technology adoption in the long term.

3. Case Study for Energy-Intensive Industries in Austria

3.1. Case Description

3.1.1. General Framework Conditions for 2040

3.1.2. Technology Framework

3.1.3. Electrification

3.1.4. Use of CO2-Neutral Gases and Combustion of Solid Biomass

3.1.5. Carbon Capture

3.1.6. Circular Economy

3.2. Iron and Steel

3.2.1. Energy-Related Emissions

3.2.2. Process-Related Emissions

3.3. Non-Metallic Minerals

3.3.1. Energy-Related Emissions

3.3.2. Process-Related Emissions

3.4. Pulp and Paper

Energy-Related Emissions

4. Discussion

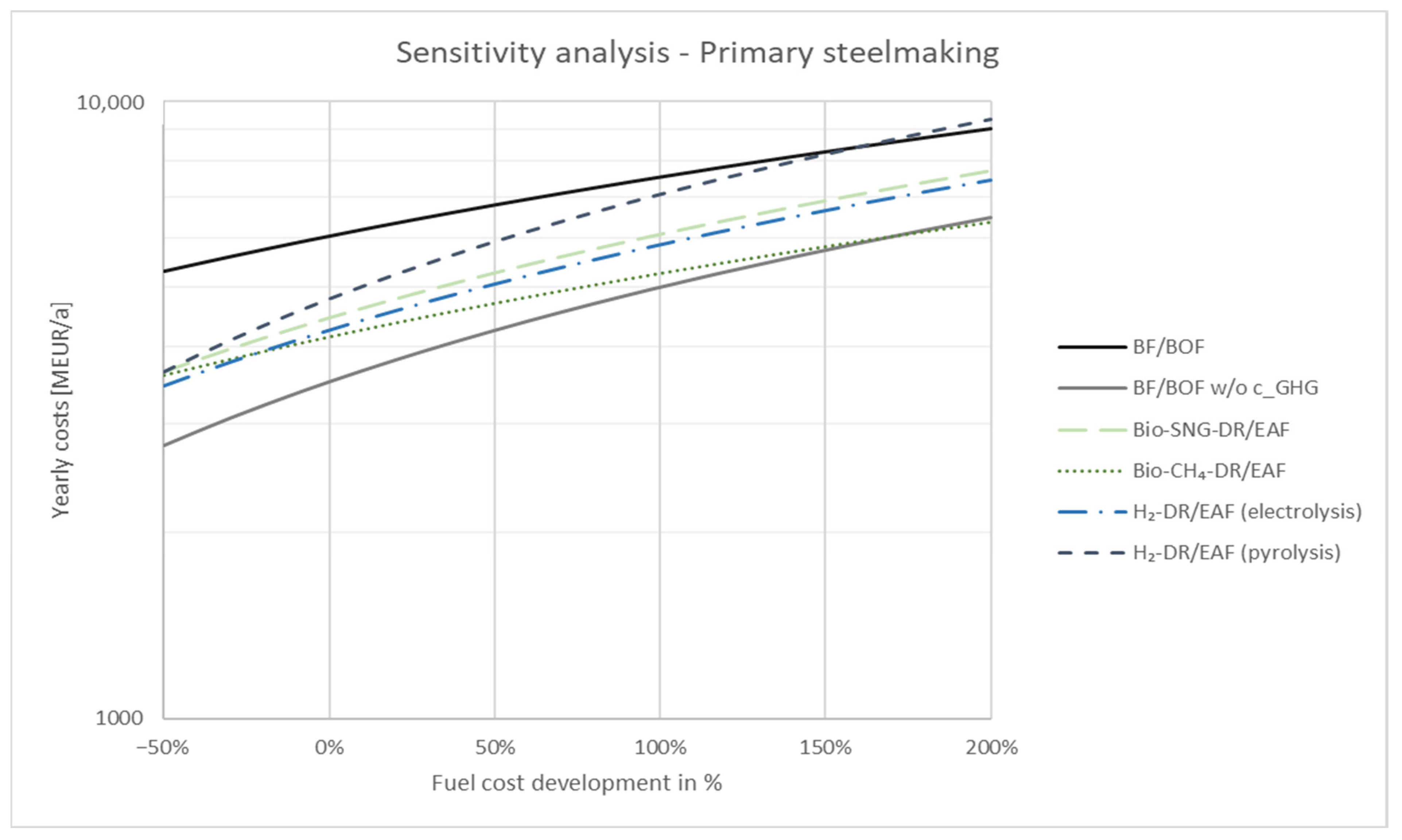

4.1. Sensitivity Analysis

4.2. Discussion of Case Study Results

5. Conclusions

- The use of CO2-neutral gases can provide significant GHG reductions over a wide variety of applications and features the most significant total technical climate neutrality potential. Due to energy-intensive production routes for H2, significantly more energy is needed than when considering current fossil-based industrial processes or the alternative bio-CH4 route.

- At lower temperature levels (up to 200 °C), electrification through heat pumps can positively impact absolute energy efficiency and provides a sustainable setup that is robust against volatile energy prices.

- The impact of intensified circular economy measures is most notable regarding energy and resource efficiency. In the case of steel production, only the already sustainable but energy-intensive EAF-based production route allows for additional recycling capacities. Similarly, in cement production, circular economy measures reduce the especially hard-to-abate geogenous emissions.

- Several technologies for the successful sequestration of CO2 exist. However, they differ significantly in energy intensity as well as investment requirements. For example, end-of-pipe solutions like the investigated amine scrubber feature easy application and comparatively low capital expenditures but show significant drawbacks regarding energy efficiency, operational expenditures, and price robustness. Oxyfuel carbon capture requires larger capital expenditures but provides significantly lower total costs of deployment annually—an already existing advantage that may well increase in consideration of expectable learning curves for this technology.

- Prices of GHG certificates are shown to constitute the most essential leveliser of the costs of fossil fuels when comparing conventional fossil-based annual costs for 2040 with those of alternative technologies. For necessary steering effects to take place across all investigated application cases, their prices should lie between 200 and 300 EUR/t CO2. This resulting span corresponds to price ranges identified in a study by the German climate neutrality research initiative ARIADNE, which investigated necessary CO2 certificate costs for reaching the 2030 GHG reduction goals of the “Fit for 55” policy programme [69].

- Our exemplary case study in Austria shows that alternative technologies in four main climate neutrality pathways can operate at total annual costs comparable to their conventional fossil-based equivalents. Their implementation timeline will be guided by the timeline of decisions for future replacement investments, which has to be an essential focal point for future studies.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| BF/BOF | Blast furnace/basic oxygen furnace |

| CAPEX | Capital expenditures |

| CH4 | Methane |

| CHP | Combined heat and power |

| CS | Crude steel |

| DR | Direct reduction |

| EAF | Electric arc furnace |

| EII | Energy-intensive industry |

| EU | European Union |

| GHG | Greenhouse gas |

| IEA | International energy agency |

| LCOE | Levelised cost of electricity |

| MRL | Market readiness level |

| OPEX | Operational expenditures |

| RTD | Research and technological development |

| SNG | Substitute natural gas |

| TCNP | Technical climate neutrality potential |

| TRL | Technology readiness level |

| UK | United Kingdom |

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Application | Full Load Hours | CAPEX in EUR2020 | cinst in %CAPEX | crel in %CAPEX | Reference for Costs | |

|---|---|---|---|---|---|---|

| Electrification | ||||||

| LT heat pumps (COP 3.0) | Space heating | 2200 | 400 EUR/kWth | 67 | 0.5 | [48]; own assumption for crel |

| HT heat pumps (COP 2.5) | Process heat < 200 °C | 4000 | 520 EUR/kWth | 100 | 2.0 | [48]; own assumption for crel |

| Electric engines | Stationary engines | 4000 | 100 EUR/kWel | 20 | 0.5 | [70]; own assumption for cinst and crel |

| Use of CO2-neutral gases and biomass combustion a | ||||||

| Gas furnace (CH4, H2) | Space heating, process heat </> 200 °C; subsector-specific processes | 4000 | 250 EUR/kWth | Included in CAPEX | 4.0 | [48,49] |

| Generation of bio-CH4 | 8000 | 2700 EUR/kWCH4 | 35 | 2.0 | Own assumptions based on [34,71] | |

| Generation of bio-SNG | 8000 | 2000 EUR/kWSNG | 35 | 2.0 | [34] | |

| Generation of H2 through electrolysis | 3500 | 515 EUR/kWel | 35 | 4.0 | [34,61] | |

| Generation of H2 through methane pyrolysis | 3500 | 475 EUR/kWH2 | 35 | 4.0 | [61]; own assumption for cinst and crel | |

| Solid biomass combustion | 8000 | 600 EUR/kWth | 35 | 2.0 | [59]; own assumption for cinst and crel | |

| CH4-DR/EAF b | Primary steelmaking | - | 400 EUR/tCS | Included in CAPEX | 71.0 c | [51,52,61] |

| H2-DR/EAF b | - | |||||

| Carbon capture | ||||||

| Oxyfuel combustion | Non-metallic mineral production | - | 220 EUR/tCO2 | 40 | 2.0 | [63]; own assumption for cinst and crel |

| Amine scrubbing | - | 131 EUR/tCO2 | 25 | 2.0 | ||

| Circular economy | ||||||

| Increased use of scrap metal in EAF d | Steel production | - | - | - | - | - |

| Recycling of concrete | Cement production | - | 1 EUR/tconcrete | - | - | [61,64] |

References

- European Environment Agency. Annual European Union Greenhouse Gas Inventory 1990–2019 and Inventory Report 2021; 2021. Available online: https://www.eea.europa.eu/publications/annual-european-union-greenhouse-gas-inventory-2021 (accessed on 16 December 2021).

- Eurostat. National Accounts Employment Data by Industry. 2021. Available online: https://ec.europa.eu/eurostat/web/products-datasets/-/nama_10_a64_e (accessed on 16 December 2021).

- Eurostat. Manufacturing Statistics—NACE Rev. 2. 2021. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Manufacturing_statistics_-_NACE_Rev._2#Sectoral_analysis (accessed on 16 December 2021).

- Eurostat. Manufacture of Chemicals and Chemical Products Statistics—NACE Rev. 2. 2015. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Archive:Manufacture_of_chemicals_and_chemical_products_statistics_-_NACE_Rev._2&direction=next&oldid=249526 (accessed on 16 December 2021).

- European Commission. The European Green Deal: Communication from the Commission to the European Parliament, the European Council, the Council, the European Economic and Social Committee and the Committee of the Regions Com (2019) 640 Final; European Commission: Brussels, Belgium, 2019.

- High-Level Group on Energy-Intensive Industries. Masterplan for a Competitive Transformation of EU Energy-Intensive Industries Enabling a Climate-Neutral Circular Economy by 2050; Publications Office of the European Union: Luxembourg, 2019. [Google Scholar]

- Fais, B.; Sabio, N.; Strachan, N. The critical role of the industrial sector in reaching long-term emission reduction, energy efficiency and renewable targets. Appl. Energy 2016, 162, 699–712. [Google Scholar] [CrossRef]

- Nurdiawati, A.; Urban, F. Towards Deep Decarbonisation of Energy-Intensive Industries: A Review of Current Status, Technologies and Policies. Energies 2021, 14, 2408. [Google Scholar] [CrossRef]

- Gerres, T.; Chaves Ávila, J.P.; Llamas, P.L.; San Román, T.G. A review of cross-sector decarbonisation potentials in the European energy intensive industry. J. Clean. Prod. 2019, 210, 585–601. [Google Scholar] [CrossRef]

- Teske, S.; Niklas, S.; Talwar, S. Decarbonisation Pathways for Industries. In Achieving the Paris Climate Agreement Goals; Teske, S., Ed.; Springer: Cham, Switzerland, 2022; pp. 81–129. ISBN 978-3-030-99176-0. [Google Scholar]

- EUROFER. Low Carbon Roadmap: Pathways to a CO2-Neutral European Steel Industry; EUROFER: Brussels, Belgium, 2019; Available online: https://www.eurofer.eu/assets/Uploads/EUROFER-Low-Carbon-Roadmap-Pathways-to-a-CO2-neutral-European-Steel-Industry.pdf (accessed on 2 February 2023).

- CEMBUREAU. Cementing the European Green Deal: Reaching Climate Neutrality along the Cement and Concrete Value Chain by 2050; CEMBUREAU: Brussels, Belgium, 2020; Available online: https://cembureau.eu/library/reports/2050-carbon-neutrality-roadmap/ (accessed on 2 February 2023).

- Harpprecht, C.; Naegler, T.; Steubing, B.; Tukker, A.; Simon, S. Decarbonization scenarios for the iron and steel industry in context of a sectoral carbon budget: Germany as a case study. J. Clean. Prod. 2022, 380, 134846. [Google Scholar] [CrossRef]

- Keys, A.; van Hout, M.; Daniels, B. Decarbonisation Options for the Dutch Steel Industry: Updated Version; The Hague, The Netherlands. 2021. Available online: https://www.pbl.nl/sites/default/files/downloads/pbl-2019-decarbonisation-options-for-the-dutch-steel-industry_3723.pdf (accessed on 2 February 2023).

- Negri, A.; Ligthart, T. Decarbonisation Options for the Dutch Polyolefins Industry; The Hague, The Netherlands. 2021. Available online: https://www.pbl.nl/sites/default/files/downloads/pbl-2021-decarbonisation-options-for-the-dutch-polyolefins-industry_4236.pdf (accessed on 2 February 2023).

- Griffin, P.W.; Hammond, G.P.; Norman, J.B. Industrial decarbonisation of the pulp and paper sector: A UK perspective. Appl. Therm. Eng. 2018, 134, 152–162. [Google Scholar] [CrossRef]

- McKinsey & Company. Net-Zero Europe, Decarbonization Pathways and Socioeconomic Implications; McKinsey & Company: Chicago, IL, USA, 2020. [Google Scholar]

- Agora Energiewende; Wuppertal Institut. Klimaneutrale Industrie: Schlüsseltechnologien und Politikoptionen für Stahl, Chemie und Zement, Berlin, Germany, 2019. Available online: https://www.agora-industrie.de/fileadmin/Projekte/2018/Dekarbonisierung_Industrie/164_A-EW_Klimaneutrale-Industrie_Studie_WEB.pdf (accessed on 25 November 2021).

- Rahnama Mobarakeh, M.; Kienberger, T. Climate neutrality strategies for energy-intensive industries: An Austrian case study. Clean. Eng. Technol. 2022, 10, 100545. [Google Scholar] [CrossRef]

- Lechtenböhmer, S.; Nilsson, L.J.; Åhman, M.; Schneider, C. Decarbonising the energy intensive basic materials industry through electrification—Implications for future EU electricity demand. Energy 2016, 115, 1623–1631. [Google Scholar] [CrossRef]

- Schneider, C.; Lechtenböhmer, S.; Bauer, T.; Nitz, P.; Hettesheimer, T.; Wietschel, M.; Meulenberg, W.; Gurtner, R. Low Carbon Industrie: Elektrifizierung und geschlossene Kohlenstoffkreisläufe. Innovationen für die Energiewende. 2018. Available online: https://publica.fraunhofer.de/entities/publication/ccc67d43-d049-45b0-a6ab-ecde8679e31e/details (accessed on 27 November 2021).

- Madeddu, S.; Ueckerdt, F.; Pehl, M.; Peterseim, J.; Lord, M.; Kumar, K.A.; Krüger, C.; Luderer, G. The CO2 reduction potential for the European industry via direct electrification of heat supply (power-to-heat). Environ. Res. Lett. 2020, 15, 124004. [Google Scholar] [CrossRef]

- Trattner, A.; Klell, M.; Radner, F. Sustainable hydrogen society—Vision, findings and development of a hydrogen economy using the example of Austria. Int. J. Hydrog. Energy 2022, 47, 2059–2079. [Google Scholar] [CrossRef]

- Szarka, N.; Lenz, V.; Thrän, D. The crucial role of biomass-based heat in a climate-friendly Germany–A scenario analysis. Energy 2019, 186, 115859. [Google Scholar] [CrossRef]

- IEA Bioenergy. IEA Bioenergy Report 2023: How Bioenergy Contributes to a Sustainable Future. 2023. Available online: https://www.ieabioenergyreview.org/wp-content/uploads/2022/12/IEA_BIOENERGY_REPORT.pdf (accessed on 15 February 2024).

- Rahnama Mobarakeh, M.; Santos Silva, M.; Kienberger, T. Pulp and Paper Industry: Decarbonisation Technology Assessment to Reach CO2 Neutral Emissions—An Austrian Case Study. Energies 2021, 14, 1161. [Google Scholar] [CrossRef]

- Agora Industry. Mobilising the Circular Economy for Energy-Intensive Materials. How Europe Can Accelerate Its Transition to Fossil-Free, Energy-Efficient and Independent Industrial Production, 2022. Available online: https://static.agora-energiewende.de/fileadmin/Projekte/2021/2021_02_EU_CEAP/A-EW_254_Mobilising-circular-economy_study_WEB.pdf (accessed on 21 July 2023).

- Mitigation Pathways Compatible with 1.5 °C in the Context of Sustainable Development. In Global Warming of 1.5 °C; IPCC, Ed.; Cambridge University Press: Cambridge, UK, 2022; pp. 93–174. ISBN 9781009157940. [Google Scholar]

- Li, J.; Tharakan, P.; Macdonald, D.; Liang, X. Technological, economic and financial prospects of carbon dioxide capture in the cement industry. Energy Policy 2013, 61, 1377–1387. [Google Scholar] [CrossRef]

- IPCC. Carbon Dioxide Capture and Storage. 2005. Available online: https://www.ipcc.ch/site/assets/uploads/2018/03/srccs_wholereport.pdf (accessed on 21 July 2023).

- Plaza, M.G.; Martínez, S.; Rubiera, F. CO2 Capture, Use, and Storage in the Cement Industry: State of the Art and Expectations. Energies 2020, 13, 5692. [Google Scholar] [CrossRef]

- Kaltschmitt, M.; Hartmann, H.; Hofbauer, H. Energie Aus Biomasse; Springer: Berlin, Heidelberg, 2016; ISBN 978-3-662-47437-2. [Google Scholar]

- Steubing, B.; Zah, R.; Waeger, P.; Ludwig, C. Bioenergy in Switzerland: Assessing the domestic sustainable biomass potential. Renew. Sustain. Energy Rev. 2010, 14, 2256–2265. [Google Scholar] [CrossRef]

- Rosenfeld, D.C.; Lindorfer, J.; Böhm, H.; Zauner, A.; Fazeni-Fraisl, K. Potentials and costs of various renewable gases: A case study for the Austrian energy system by 2050. Detritus 2021, 16, 106–120. [Google Scholar] [CrossRef]

- Global Reporting Standards. Consolidated Set of the GRI Standards. 2022. Available online: https://www.globalreporting.org/standards (accessed on 4 March 2023).

- Nagovnak, P.; Kienberger, T.; Baumann, M.; Binderbauer, P.; Vouk, T. Improving the methodology of national energy balances to adapt to the energy transition. Energy Strategy Rev. 2022, 44, 100994. [Google Scholar] [CrossRef]

- United Nations. International Recommendations for Energy Statistics (IRES); United Nations: New York, NY, USA, 2018. Available online: https://unstats.un.org/unsd/energystats/methodology/ires/ (accessed on 22 November 2022).

- Nagovnak, P.; Schützenhofer, C.; Rahnama Mobarakeh, M.; Cvetkovska, R.; Stortecky, S.; Hainoun, A.; Alton, V.; Kienberger, T. Assessment of technology-based options for climate neutrality in Austrian manufacturing industry. Heliyon 2024, 10, e25382. [Google Scholar] [CrossRef] [PubMed]

- Bundeskanzleramt Österreich. Aus Verantwortung für Österreich. Regierungsprogramm 2020–2024; Bundeskanzleramt Österreich: Wien, Austria, 2020. [Google Scholar]

- European Commission. 2022 Draft Trajectories for Parameters for Reporting on National GHG Projections in 2023; European Commission: Brussels, Belgium, 2022.

- European Commission. EU Reference Scenario 2020: Energy, Transport and GHG Emissions—Trends to 2050; European Commission: Brussels, Belgium, 2021.

- Sejkora, C.; Lindorfer, J.; Kühberger, L.; Kienberger, T. Interlinking the Renewable Electricity and Gas Sectors: A Techno-Economic Case Study for Austria. Energies 2021, 14, 6289. [Google Scholar] [CrossRef]

- Institut für Energetik und Umwelt; Institut für Technologie und Biosystemtechnik Bundesforschungsanstalt f. Landwirtschaft; Kuratorium für Technik und Bauwesen in der Landwirtschaft. Handreichung Biogasgewinnung und -Nutzung; Bundesministerium für Ernährung, Landwirtschaft und Verbraucherschutz: Berlin, Germany, 2006; ISBN 3-00-014333-5. [Google Scholar]

- Propellets Austria. Pelletpreise Österreich. Available online: https://www.propellets.at/aktuelle-pelletpreise (accessed on 8 August 2022).

- Sejkora, C.; Kühberger, L.; Radner, F.; Trattner, A.; Kienberger, T. Exergy as Criteria for Efficient Energy Systems—A Spatially Resolved Comparison of the Current Exergy Consumption, the Current Useful Exergy Demand and Renewable Exergy Potential. Energies 2020, 13, 843. [Google Scholar] [CrossRef]

- Statistics Austria. Energiebilanzen für Österreich: Gesamtenergiebilanz Österreich 1970 bis 2020. 2022. Available online: https://www.statistik.at/web_de/statistiken/energie_umwelt_innovation_mobilitaet/energie_und_umwelt/energie/energiebilanzen/index.html (accessed on 12 February 2024).

- Statistics Austria. Nutzenergieanalyse für Österreich. 2023. Available online: https://www.statistik.at/statistiken/energie-und-umwelt/energie/nutzenergieanalyse (accessed on 12 February 2024).

- The Danish Energy Agency. Technology Data Catalogue. Available online: https://ens.dk/en/our-services/projections-and-models/technology-data (accessed on 6 March 2023).

- Popovski, E.; Fleiter, T.; Santos, H.; Leal, V.; Fernandes, E.O. Technical and economic feasibility of sustainable heating and cooling supply options in southern European municipalities-A case study for Matosinhos, Portugal. Energy 2018, 153, 311–323. [Google Scholar] [CrossRef]

- Lisbona, P.; Gori, R.; Romeo, L.M.; Desideri, U. Techno-economic assessment of an industrial carbon capture hub sharing a cement rotary kiln as sorbent regenerator. Int. J. Greenh. Gas Control 2021, 112, 103524. [Google Scholar] [CrossRef]

- Fischedick, M.; Marzinkowski, J.; Winzer, P.; Weigel, M. Techno-economic evaluation of innovative steel production technologies. J. Clean. Prod. 2014, 84, 563–580. [Google Scholar] [CrossRef]

- Küster Simic, A.; Schönfeldt, J. H2-Transformation der Stahlindustrie und des Energieanlagenbaus; Hans Böckler Stiftung: Dusseldorf, Germany, 2022. [Google Scholar]

- Arpagaus, C.; Bless, F.; Uhlmann, M.; Schiffmann, J.; Bertsch, S.S. High temperature heat pumps: Market overview, state of the art, research status, refrigerants, and application potentials. Energy 2018, 152, 985–1010. [Google Scholar] [CrossRef]

- Jakobs, R.M.; Stadtländer, C. Final Report Annex 48: Industrial Heat Pumps, Second Phase; Borås, Sweden. 2021. Available online: https://heatpumpingtechnologies.org/publications/final-report-annex-48-industrial-heat-pumps-second-phase/ (accessed on 1 June 2022).

- Umweltbundesamt GmbH. Szenario Erneuerbare Energie 2030 und 2050–Zusammenfassung (REP-0576); Umweltbundesamt GmbH: Vienna, Austria, 2016. [Google Scholar]

- Jakobs, R.M.; Stadtländer, C. Industrial Heat Pumps, Second Phase. 2020. Available online: https://etkhpcorderapi.extweb.sp.se/api/file/2085 (accessed on 3 March 2023).

- International Energy Agency. Energy Technology Perspectives 2020. 2021. Available online: https://www.iea.org/reports/energy-technology-perspectives-2020 (accessed on 1 June 2022).

- European Commission. Stepping up Europe’s 2030 Climate Ambition: Investing in a Climate-Neutral Future for the Benefit of Our People; European Commission: Brussels, Belgium, 2020.

- QM Holzheizwerke. Planungshandbuch, 3rd ed.; komplett überarbeitete Auflage; CARMEN: Straubing, Germany, 2022; ISBN 978-3-937441-96-2. [Google Scholar]

- Navigant. Gas for Climate: The Optimal Role for Gas in a Net-Zero Emissions Energy System; Navigant: Utrecht, The Netherlands, 2019. [Google Scholar]

- Diendorfer, C.; Gahleitner, B.; Dachs, B.; Kienberger, T.; Nagovnak, P.; Böhm, H.; Moser, S.; Thenius, G.; Knaus, K. Klimaneutralität Österreichs bis 2040: Beitrag der österreichischen Industrie; Bundesministerium für Klimaschutz, Umwelt, Energie, Mobilität, Innovation und Technologie: Vienna, Austria, 2021. [Google Scholar]

- Korczak, K.; Kochański, M.; Skoczkowski, T. Mitigation options for decarbonization of the non-metallic minerals industry and their impacts on costs, energy consumption and GHG emissions in the EU—Systematic literature review. J. Clean. Prod. 2022, 358, 132006. [Google Scholar] [CrossRef]

- Anantharaman, R.; Berstad, D.; de Lena, E.; Fu, C.; Gardasdottir, S.; Jamali, A.; Perez-Calvo, J.-F.; Roman, M.; Roussanaly, S.; Ruppert, J.; et al. CEMCAP Comparative Techno-Economic Analysis of CO2 Capture in Cement Plants. 2018. Available online: https://ec.europa.eu/research/participants/documents/downloadPublic?documentIds=080166e5c0910e2e&appId=PPGMS (accessed on 5 March 2023).

- Nusselder, S.; Maqbool, A.S.; Deen, R.; Blake, G.; Bouwens, J.; Fauzi, R.T. Closed-loop Economy: Case of Concrete in The Netherlands. 2015. Available online: https://www.slimbreker.nl/downloads/IPG-concrete-final-report(1).pdf (accessed on 26 April 2022).

- Umweltbundesamt GmbH. Austria’s National Inventory Report 2020; Umweltbundesamt GmbH: Vienna, Austria, 2021. [Google Scholar]

- Anantharaman, R.; Berstad, D.; de Lena, E.; Fu, C.; Gardasdottir, S.; Jamali, A.; Perez-Calvo, J.-F.; Roman, M.; Roussanaly, S.; Ruppert, J.; et al. CEMCAP Publishable Summary Period 1. 2018. Available online: https://www.sintef.no/globalassets/sintef-energi/cemcap/pr_publishable_summary_1.pdf/ (accessed on 14 April 2023).

- Austropapier. Branchenbericht 2020. 2021. Available online: https://austropapier.at/website2020/wp-content/uploads/2021/08/bb20-ganzer-bericht-hires.pdf (accessed on 26 April 2022).

- Guminski, A.; Fiedler, C.; Kigle, S.; Pellinger, C.; Dossow, P.; Ganz, K.; Jetter, F.; Kern, T.; Limmer, T.; Murmann, A.; et al. eXtremOS Summary Report; Forschungsstelle für Energiewirtschaft: Munich, Germany, 2021. [Google Scholar]

- Pietzcker, R.; Feuerhahn, J.; Haywood, L.; Knopf, B.; Leukhardt, F.; Luderer, G.; Osorio, S.; Pahle, M.; Dias Bleasby Rodrigues, R.; Edenhofer, O. Notwendige CO2-Preise Zum Erreichen des Europäischen Klimaziels 2030; Potsdam-Institut für Klimafolgenforschung: Potsdam, Germany, 2021. [Google Scholar]

- Topmotors. Topmotors Merkblatt Nr. 10: Motorpreise. 2021. Available online: https://topmotors.ch/sites/default/files/2018-08/D_MB_10_Motorenpreise.pdf (accessed on 6 March 2023).

- Puchas, K.; ARGE Biogasnetzwerk, Österreich. BFIT: Beyond Feed-In-Tariff; ARGE Biogasnetzwerk Österreich: Güssing, Austria, 2017. [Google Scholar]

| Type of Emissions | Description |

|---|---|

| Energy-related emissions |

|

| Process-related emissions |

|

| Energy Carrier | Assumed Reference Prices in 2040 in EUR2020 | Reference |

|---|---|---|

| Oil | 58.7 EUR/MWh | [40] |

| Natural gas | 40.7 EUR/MWh | [40] |

| Coal | 12.0 EUR/MWh | [40] |

| Electricity | 101.6 EUR/MWh | [41] |

| Electricity (spot market) a | 35.0 EUR/MWh | [42] |

| Biomass for anaerobic fermentation | Ø32.0 EUR/MWh | [43] |

| Solid biomass (incl. for gasification) | 55.7 EUR/MWh | [44] |

| Subsector | Space Heating | <100 °C | 100–200 °C | 200–300 °C | 300–500 °C | >500 °C |

|---|---|---|---|---|---|---|

| Iron and steel | 0.1% | 0.6% | 0.9% | 0.1% | 0.7% | 97.6% |

| Non-metallic minerals | 0.1% | 1.4% | 1.2% | 0.0% | 0.8% | 96.5% |

| Pulp and paper | 0.6% | 18.6% | 45.5% | 1.9% | 33.3% | 0.0% |

| Full Load Hours | CAPEX in EUR2020 | cinst in %CAPEX | crel in %CAPEX | Reference For Costs | |

|---|---|---|---|---|---|

| Coal furnace | 4000 | 147 EUR/kWth | 50 | 1.5 | [48] |

| Oil furnace | 4000 | 30 EUR/kWth | 70 | 4.0 | [48] |

| Gas furnace | 4000 | 250 EUR/kWth | Included in CAPEX | 4.0 | [48,49] |

| Diesel engine | 4000 | 100 EUR/kWmech | 20 | 4.0 | Own assumptions |

| Gas engine | 4000 | 100 EUR/kWmech | 20 | 4.0 | Own assumptions |

| Rotary kiln (cement) | - | 190 EUR/tClinker | Included in CAPEX | 2.0 | [50]; own assumption for crel |

| BF/BOF (prim. steelmaking) | - | 442 EUR/tCrude steel | Included in CAPEX | 60.0 a | [51,52] |

| Energy Demand | Emissions | ACAPEX | COPEX | Total Costs | ||

|---|---|---|---|---|---|---|

| [GWh/a] | [kt CO2e/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Space heating | Coal furnace | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Oil furnace | 9.5 | 2.8 | 0.0 | 1.3 | 1.3 | |

| Gas furnace | 329.5 | 65.7 | 1.7 | 29.9 | 31.6 | |

| Stationary engines | Diesel engine | 6.1 | 1.8 | 0.0 | 0.8 | 0.8 |

| Gas engine | 87.9 | 17.5 | 0.2 | 8.0 | 8.2 | |

| Process heat < 200 °C | Coal furnace | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Oil furnace | 5.4 | 1.6 | 0.0 | 0.7 | 0.7 | |

| Gas furnace | 121.6 | 24.2 | 0.6 | 11.0 | 11.6 | |

| Process heat > 200 °C | Coal furnace | 1866.9 | 620.7 | 8.3 | 177.7 | 186.0 |

| Oil furnace | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | |

| Gas furnace | 5287.1 | 1054.5 | 26.5 | 479.9 | 506.4 | |

| Primary steelmaking | BF/BOF | 26,777.0 | 10,200.0 | 244.7 | 5808.3 | 6053.0 |

| Climate Neutrality Pathway | Source of Emission | Technology | Application |

|---|---|---|---|

| Electrification | Energy-related | Use of heat pumps | Space heating Process heat < 200 °C |

| Energy-related | Electric engines | Stationary engines | |

| Process-related (a) | Electric arc furnace | Primary steelmaking in combination with direct reduction | |

| Use of CO2-neutral gases and solid biomass combustion | Process-related | Direct reduction of iron ore with gases | Primary steelmaking in combination with EAF |

| Energy-related | Bio-CH4 | Space heating Process heat </> 200 °C | |

| Energy-related | H2 from electrolysis | Space heating Process heat </> 200 °C | |

| Energy-related | H2 from pyrolysis | Space heating Process heat </> 200 °C | |

| Energy-related | Solid biomass comb. | Space heating Process heat < 200 °C | |

| Carbon capture (b) | |||

| Circular economy | Process-related | Using EAF | Increased use of scrap metals |

| Technology | Application | TCNP | Energy Balance | ACAPEX | COPEX | Total Costs |

|---|---|---|---|---|---|---|

| [ktCO2e/a] | [GWh/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Electrification | ||||||

| LT heat pumps | Space heating | −63 | Fossil: −339 | |||

| Electr.: +100 | 7.3 | 11.6 | 18.9 | |||

| HT heat pumps | Process heat < 200 °C | −23 | Fossil: −127 | |||

| Electr.: +42 | 2.2 | 4.9 | 7.1 | |||

| Electric engines | Motive power | −17 | Fossil: −94 | |||

| Electr.: +44 | 0.1 | 5.1 | 5.2 | |||

| Use of CO2-neutral gases and solid biomass combustion | ||||||

| Bio-CH4 | Space heating | −69 | Fossil: −339 | |||

| Bio-CH4: +339 | 12.4 | 11.2 | 25.3 | |||

| Bio-CH4 | ||||||

| 1.7 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −26 | Fossil: −127 | ||||

| Bio-CH4: +128 | 4.7 | 4.2 | 9.5 | |||

| Bio-CH4 | ||||||

| 0.6 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1675 | Fossil: −7154 | ||||

| Bio-CH4: +7154 | 261.6 | 235.8 | 533.2 | |||

| Bio-CH4 | ||||||

| 35.9 | ||||||

| Furnace | ||||||

| Bio-SNG | Space heating | −69 | Fossil: −339 | |||

| Bio-SNG: +339 | 9.2 | 19.2 | 30.1 | |||

| Bio-SNG | ||||||

| 1.7 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −26 | Fossil: −127 | ||||

| Bio-SNG: +128 | 3.5 | 7.2 | 11.4 | |||

| Bio-SNG | ||||||

| 0.6 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1675 | Fossil: −7154 | ||||

| Bio-SNG: +7154 | 193.7 | 404.9 | 634.6 | |||

| Bio-SNG | ||||||

| 35.9 | ||||||

| Furnace | ||||||

| H2 from electrolysis | Space heating | −45 | Fossil: −339 | |||

| H2: +305 | 6.8 | 15.3 | 23.6 | |||

| Electr.: +427 | H2 | |||||

| 1.5 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −17 | Fossil: −127 | ||||

| H2: +114 | 2.6 | 5.7 | 8.8 | |||

| Electr.: +160 | H2 | |||||

| 0.6 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1170 | Fossil: −7154 | ||||

| H2: +6438 | 143.7 | 322.7 | 498.7 | |||

| Electr.: +9014 | H2 | |||||

| 32.3 | ||||||

| Furnace | ||||||

| H2 from methane pyrolysis | Space heating | −64 | Fossil: −339 | |||

| H2: +305 | 4.5 | 26.5 | 32.5 | |||

| CH4: +570 | H2 | |||||

| Electr.: +87 | 1.5 | |||||

| Furnace | ||||||

| Process heat < 200 °C | −24 | Fossil: −127 | ||||

| H2: +114 | 1.7 | 9.9 | 12.2 | |||

| CH4: +213 | H2 | |||||

| Electr.: +33 | 0.6 | |||||

| Furnace | ||||||

| Process heat > 200 °C | −1572 | Fossil: −7154 | ||||

| H2: +6438 | 94.6 | 559.3 | 686.3 | |||

| CH4: +12,040 | H2 | |||||

| Electr.:+1837 | 32.3 | |||||

| Furnace | ||||||

| Solid biomass | Space heating | −68 | Fossil:−339 | |||

| Biomass:+339 | 2.0 | 18.9 | 21.0 | |||

| Process heat < 200 °C | −25 | Fossil:−127 | ||||

| Biomass:+127 | 0.8 | 7.1 | 7.9 | |||

| Technology | Application | TCNP | Energy Balance | ACAPEX | COPEX | Total Costs |

|---|---|---|---|---|---|---|

| [ktCO2e] | [GWh/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Use of CO2-neutral gases and solid biomass combustion | ||||||

| Bio-CH4-DR/EAF | Primary steelmaking incl. EAF | −9977 | Fossil: −26,777 | |||

| Bio-CH4: +21,900 | 221.5 | 3127.7 | 4149.9 | |||

| Electr.: +3983 | DR-CS | |||||

| 800.7 | ||||||

| Bio-SNG | ||||||

| Bio-SNG-DR/EAF | Primary steelmaking incl. EAF | −9977 | Fossil: −26,777 | |||

| Bio-SNG: +21,900 | 221.5 | 3646.8 | 4461.3 | |||

| Electr.:+3983 | DR-CS | |||||

| 593.1 | ||||||

| Bio-CH4 | ||||||

| H2-DR/EAF (electrolysis) | Primary steelmaking incl. EAF | −8547 | Fossil: −26,777 | |||

| H2: +18,235 | 221.5 | 3623.4 | 4251.8 | |||

| Electr.: +25,530 | DR-CS | |||||

| Bio-CH4/SNG: +3726 | ||||||

| Electr.: +3985 | 406.9 | |||||

| Electrolysis | ||||||

| H2-DR/EAF (pyrolysis) | Primary steelmaking incl. EAF | −9686 | Fossil: −26,777 | |||

| H2: +18,235 | 221.5 | 4298.9 | 4788.5 | |||

| CH4: +34,100 | DR-CS | |||||

| Electr.: +5197 | ||||||

| Bio-CH4/SNG: +3726 | 268.1Pyrolysis | |||||

| Electr.: +3985 | ||||||

| Circular economy | ||||||

| EAF | 50% scrap metal input in steelmaking | −9977 | Fossil: −26,777 | |||

| Bio-CH4: +10,950 | 110.7 | 1794.1 | 2305.2 | |||

| Reducing need for Bio-CH4-DR | Electr.: +3983 | DR-CS | ||||

| 400.3 | ||||||

| Bio-CH4 | ||||||

| EAF | 50% scrap metal input in steelmaking | −9977 | Fossil: −26,777 | |||

| Bio-SNG: +10,950 | 110.7 | 2053.6 | 2460.9 | |||

| Reducing need for Bio-SNG-DR | Electr.: +3983 | DR-CS | ||||

| 296.5 | ||||||

| Bio-SNG | ||||||

| EAF | 50% scrap metal input in steelmaking | −9233 | Fossil: −26,777 | |||

| H2: +9118 | 110.7 | 2101.4 | 2415.7 | |||

| Reducing need for H2-DR (electrolysis) | Electr.: +12,765 | DR-CS | ||||

| Bio-CH4/SNG: +1863 | ||||||

| Electr.: +4499 | 203.5 | |||||

| Electrolysis | ||||||

| EAF | 50% scrap metal input in steelmaking | −9803 | Fossil: −26,777 | |||

| H2: +9118 | 110.7 | 2439.2 | 2684.0 | |||

| Reducing need for H2-DR (pyrolysis) | CH4: +17,050 | DR-CS | ||||

| Electr.: +2599 | ||||||

| Bio-CH4/SNG: +1863 | 134.0Pyrolysis | |||||

| Electr.: +4499 | ||||||

| Energy Demand | Emissions | ACAPEX | COPEX | Total Costs | ||

|---|---|---|---|---|---|---|

| [GWh/a] | [ktCO2e/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Space heating | Coal furnace | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Oil furnace | 26.9 | 7.9 | 0.0 | 3.6 | 3.6 | |

| Gas furnace | 319.1 | 63.6 | 1.6 | 29.0 | 30.6 | |

| Stationary engines | Diesel engine | 46.4 | 13.6 | 0.1 | 6.1 | 6.3 |

| Gas engine | 0.6 | 0.1 | 0.0 | 0.1 | 0.1 | |

| Process heat < 200 °C | Coal furnace | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Oil furnace | 0.7 | 0.2 | 0.0 | 0.1 | 0.1 | |

| Gas furnace | 208.3 | 41.54 | 1.0 | 18.9 | 20.0 | |

| Process heat > 200 °C | Rotary kiln | 3321.0 | 972.9 | 73.2 | 722.5 | 795.7 |

| Coal furnace | 215.7 | 71.7 | 1.0 | 20.5 | 21.5 | |

| Oil furnace | 94.5 | 27.7 | 0.1 | 12.5 | 12.6 | |

| Gas furnace | 3181.8 | 634.6 | 16.0 | 288.8 | 304.8 |

| Climate Neutrality Pathway | Source of Emission | Technology | Application |

|---|---|---|---|

| Electrification | Energy-related | Use of heat pumps | Space heating Process heat < 200 °C |

| Electric engines | Stationary engines | ||

| Use of CO2-neutral gases and biomass combustion | Energy-related | Bio-CH4 | Space heating Process heat </> 200 °C |

| H2 from electrolysis | Space heating Process heat </> 200 °C | ||

| H2 from pyrolysis | Space heating Process heat </> 200 °C | ||

| Solid biomass comb. | Space heating Process heat < 200 °C | ||

| Carbon capture | Process-related | Oxyfuel-combustion | Production |

| Amine scrubbing | |||

| Circular economy | Process-related | Concrete recycling |

| Technology | Application | TCNP | Energy Balance | ACAPEX | COPEX | Total Costs |

|---|---|---|---|---|---|---|

| [ktCO2e] | [GWh/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Electrification | ||||||

| LT heat pumps | Space heating | −66 | Fossil: −346 | |||

| Electr.: +102 | 7.5 | 11.8 | 19.3 | |||

| HT heat pumps | Process heat < 200 °C | −38 | Fossil: −209 | |||

| Electr.: +69 | 3.6 | 8.0 | 11.6 | |||

| Electric engines | Motive power | −13 | Fossil: −47 | |||

| Electr.: +22 | 0.1 | 2.5 | 2.6 | |||

| Use of CO2-neutral gases and solid biomass combustion | ||||||

| Bio-CH4 | Space heating | −72 | Fossil: −346 | |||

| Bio-CH4: +346 | 12.6 | 11.4 | 25.8 | |||

| Bio-CH4 | ||||||

| 1.7 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −42 | Fossil: −209 | ||||

| Bio-CH4: +209 | 7.6 | 6.9 | 15.6 | |||

| Bio-CH4 | ||||||

| 1.0 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1672 | Fossil: −6813 | ||||

| Bio-CH4: +6813 | 249.1 | 224.5 | 507.8 | |||

| Bio-CH4 | ||||||

| 34.2 | ||||||

| Furnace | ||||||

| Bio-SNG | Space heating | −72 | Fossil: −346 | |||

| Bio-SNG: +346 | 9.4 | 19.6 | 30.7 | |||

| Bio-SNG | ||||||

| 1.7 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −42 | Fossil: −209 | ||||

| Bio-SNG: +209 | 5.7 | 11.8 | 18.5 | |||

| Bio-SNG | ||||||

| 1.0 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1672 | Fossil: −6813 | ||||

| Bio-SNG: +6813 | 184.5 | 385.6 | 604.3 | |||

| Bio-SNG | ||||||

| 34.2 | ||||||

| Furnace | ||||||

| H2 from electrolysis | Space heating | −47 | Fossil: −346 | |||

| H2: +311 | 6.9 | 15.6 | 24.1 | |||

| Electr.: +436 | H2 | |||||

| 1.6 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −27 | Fossil: −209 | ||||

| H2: +188 | 4.2 | 9.4 | 14.5 | |||

| Electr.: +263 | H2 | |||||

| 0.9 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1192 | Fossil: −6813 | ||||

| H2: +6131 | 136.8 | 307.3 | 474.9 | |||

| Electr.: +8584 | H2 | |||||

| 30.7 | ||||||

| Furnace | ||||||

| H2 from pyrolysis | Space heating | −67 | Fossil: −346 | |||

| H2: +312 | 4.6 | 27.0 | 33.2 | |||

| CH4: +582 | H2 | |||||

| Electr.: +89 | 1.6 | |||||

| Furnace | ||||||

| Process heat < 200 °C | −39 | Fossil: −209 | ||||

| H2: +188 | 2.8 | 16.4 | 20.1 | |||

| CH4: +352 | H2 | |||||

| Electr.: +54 | 0.9 | |||||

| Furnace | ||||||

| Process heat > 200 °C | −1574 | Fossil: −6813 | ||||

| H2: +6131 | 90.1 | 532.6 | 653.5 | |||

| CH4: +11,466 | H2 | |||||

| Electr.: +1749 | 30.7 | |||||

| Furnace | ||||||

| Solid biomass | Space heating | −72 | Fossil: −346 | |||

| Biomass: +346 | 2.1 | 19.3 | 21.4 | |||

| Process heat < 200 °C | −42 | Fossil: −209 | ||||

| Biomass: +209 | 1.3 | 11.7 | 12.9 | |||

| Technology | Application | TCNP | Energy Balance | ACAPEX | COPEX | Total Costs |

|---|---|---|---|---|---|---|

| [ktCO2e] | [GWh/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Carbon Capture | ||||||

| Oxyfuel-combustion | Sector-spec. processes | −2771 | Electr.: +676 | 70.4 | 78.1 | 148.6 |

| Amine scrubbing | Sector-spec. processes | −2729 | Electr.: +1421 | 37.5 | 164.3 | 201.8 |

| Circular economy | ||||||

| Bio-CH4 | Recycling of concrete | −827 | Bio-CH4: +1466 | 56.4 | 46.9 | 110.7 |

| Bio-CH4 | ||||||

| 7.4 | ||||||

| Furnace | ||||||

| Bio-SNG | Recycling of concrete | −827 | Bio-SNG: +1466 | 42.5 | 81.7 | 131.5 |

| Bio-SNG | ||||||

| 7.4 | ||||||

| Furnace | ||||||

| H2 from electrolysis | Recycling of concrete | −712 | H2: +1466 | 35.5 | 71.8 | 114.7 |

| H2 | ||||||

| 7.4 | ||||||

| Electr.: +2052 | Furnace | |||||

| H2 from pyrolysis | Recycling of concrete | −804 | H2: +1466 | 24.4 | 126.1 | 157.8 |

| CH4: +2741 | H2 | |||||

| Electr.: +418 | 7.4 | |||||

| Furnace | ||||||

| Energy Demand | Emissions | ACAPEX | COPEX | Total Costs | ||

|---|---|---|---|---|---|---|

| [GWh/a] | [kt CO2e/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Space heating | Coal furnace | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Oil furnace | 18.8 | 5.5 | 0.0 | 2.5 | 2.5 | |

| Gas furnace | 393.2 | 78.4 | 2.0 | 35.7 | 37.7 | |

| Stationary engines | Diesel engine | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Gas engine | 363.0 | 72.4 | 0.9 | 32.9 | 33.8 | |

| Process heat < 200 °C | Coal furnace | 475.0 | 158.0 | 2.1 | 45.2 | 47.3 |

| Oil furnace | 22.4 | 6.6 | 0.0 | 3.0 | 3.0 | |

| Gas furnace | 3467.6 | 691.6 | 17.4 | 314.7 | 332.1 | |

| Process heat > 200 °C | Coal furnace | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Oil furnace | 3.9 | 1.1 | 0.0 | 0.5 | 0.5 | |

| Gas furnace | 7184.1 | 1432.8 | 36.0 | 652.1 | 688.1 |

| Climate Neutrality Pathway | Source of Emission | Technology | Application |

|---|---|---|---|

| Electrification | Energy-related | Use of heat pumps | Space heating Process heat < 200 °C |

| Energy-related | Electric engines | Stationary engines | |

| Use of CO2-neutral gases and solid biomass combustion | Energy-related | Bio-CH4 | Space heating Process heat </> 200 °C |

| Energy-related | H2 from electrolysis | Space heating Process heat </> 200 °C | |

| Energy-related | H2 from pyrolysis | Space heating Process heat </> 200 °C | |

| Energy-related | Solid biomass comb. | Space heating Process heat </> 200 °C | |

| Carbon capture | |||

| Circular economy |

| Technology | Application | TCNP | Energy Balance | ACAPEX | COPEX | Total Costs |

|---|---|---|---|---|---|---|

| [ktCO2e] | [GWh/a] | [MEUR/a] | [MEUR/a] | [MEUR/a] | ||

| Electrification | ||||||

| LT heat pumps | Space heating | −75 | Fossil: −412 | |||

| Electr.: +122 | 8.9 | 14.1 | 23.1 | |||

| HT heat pumps | Process heat < 200 °C | −789 | Fossil: −3965 | |||

| Electr.: +123 | 68.3 | 154.1 | 222.3 | |||

| Electric engines | Motive power | −62 | Fossil: −363 | |||

| Electr.: +171 | 0.0 | 19.8 | 19.8 | |||

| Use of CO2-neutral gases and solid biomass combustion | ||||||

| Bio-CH4 | Space heating | −82 | Fossil: −412 | |||

| Bio-CH4: +412 | 15.1 | 13.6 | 30.7 | |||

| Bio-CH4 | ||||||

| 2.1 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −863 | Fossil: −3965 | ||||

| Bio-CH4: +3965 | 145.0 | 130.7 | 295.5 | |||

| Bio-CH4 | ||||||

| 19.9 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1523 | Fossil: −7188 | ||||

| Bio-CH4: +7188 | 262.8 | 236.9 | 535.7 | |||

| Bio-CH4 | ||||||

| 36.0 | ||||||

| Furnace | ||||||

| Bio-SNG | Space heating | −82 | Fossil: −412 | |||

| Bio-SNG: +412 | 11.2 | 23.3 | 36.5 | |||

| Bio-SNG | ||||||

| 2.1 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −863 | Fossil: −3965 | ||||

| Bio-SNG: +3965 | 107.4 | 224.4 | 351.7 | |||

| Bio-SNG | ||||||

| 19.9 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1523 | Fossil: −7188 | ||||

| Bio-SNG: +7188 | 194.7 | 406.9 | 637.6 | |||

| Bio-SNG | ||||||

| 36.0 | ||||||

| Furnace | ||||||

| H2 from electrolysis | Space heating | −82 | Fossil: −412 | |||

| H2: +372 | 8.3 | 18.6 | 28.8 | |||

| Electr.: +520 | H2 | |||||

| 1.9 | ||||||

| Furnace | ||||||

| Process heat < 200 °C | −583 | Fossil: −3965 | ||||

| H2: +3569 | 79.6 | 178.8 | 276.4 | |||

| Electr.: +4996 | H2 | |||||

| 17.9 | ||||||

| Furnace | ||||||

| Process heat > 200 °C | −1005 | Fossil: −7188 | ||||

| H2: +7188 | 160.4 | 360.1 | 553.0 | |||

| Electr.: +10,063 | H2 | |||||

| 32.5 | ||||||

| Furnace | ||||||

| H2 from pyrolysis | Fossil: −412 | |||||

| Space heating | −73 | H2: +372 | 5.5 | 32.2 | 39.6 | |

| CH4: +694 | H2 | |||||

| Electr.: +106 | 1.9 | |||||

| Furnace | ||||||

| Fossil: −3965 | ||||||

| Process heat < 200 °C | −778 | H2: +3569 | 52.5 | 310.0 | 380.4 | |

| CH4: +6674 | H2 | |||||

| Electr.: +1018 | 17.9 | |||||

| Furnace | ||||||

| Fossil: −7188 | ||||||

| Process heat > 200 °C | −1377 | H2: +5170 | 95.4 | 623.9 | 751.9 | |

| CH4: +13,443 | H2 | |||||

| Electr.: +2051 | 32.5 | |||||

| Furnace | ||||||

| Solid biomass | Space heating | −82 | Fossil: −412 | |||

| Biomass: +412 | 2.5 | 23.0 | 25.5 | |||

| Process heat < 200 °C | −863 | Fossil: −3965 | ||||

| Biomass: +3965 | 23.9 | 221.3 | 245.2 | |||

| Process heat > 200 °C | −1523 | Fossil: −7188 | ||||

| Biomass: +7188 | 43.3 | 401.2 | 444.5 | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nagovnak, P.; Rahnama Mobarakeh, M.; Diendorfer, C.; Thenius, G.; Böhm, H.; Kienberger, T. Cost-Driven Assessment of Technologies’ Potential to Reach Climate Neutrality in Energy-Intensive Industries. Energies 2024, 17, 1058. https://doi.org/10.3390/en17051058

Nagovnak P, Rahnama Mobarakeh M, Diendorfer C, Thenius G, Böhm H, Kienberger T. Cost-Driven Assessment of Technologies’ Potential to Reach Climate Neutrality in Energy-Intensive Industries. Energies. 2024; 17(5):1058. https://doi.org/10.3390/en17051058

Chicago/Turabian StyleNagovnak, Peter, Maedeh Rahnama Mobarakeh, Christian Diendorfer, Gregor Thenius, Hans Böhm, and Thomas Kienberger. 2024. "Cost-Driven Assessment of Technologies’ Potential to Reach Climate Neutrality in Energy-Intensive Industries" Energies 17, no. 5: 1058. https://doi.org/10.3390/en17051058

APA StyleNagovnak, P., Rahnama Mobarakeh, M., Diendorfer, C., Thenius, G., Böhm, H., & Kienberger, T. (2024). Cost-Driven Assessment of Technologies’ Potential to Reach Climate Neutrality in Energy-Intensive Industries. Energies, 17(5), 1058. https://doi.org/10.3390/en17051058