Evolutionary Trends in Carbon Market Risk Research

Abstract

1. Introduction

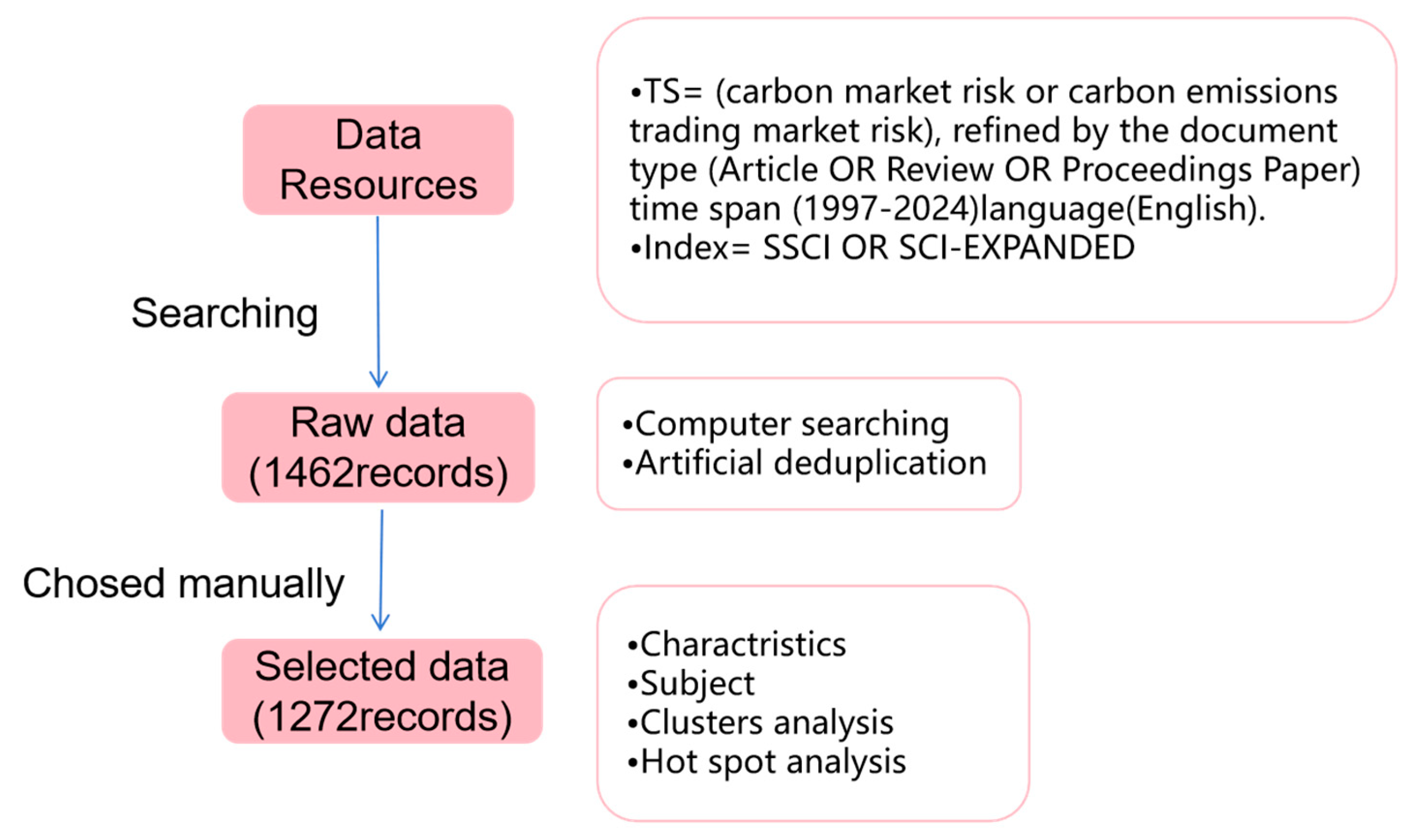

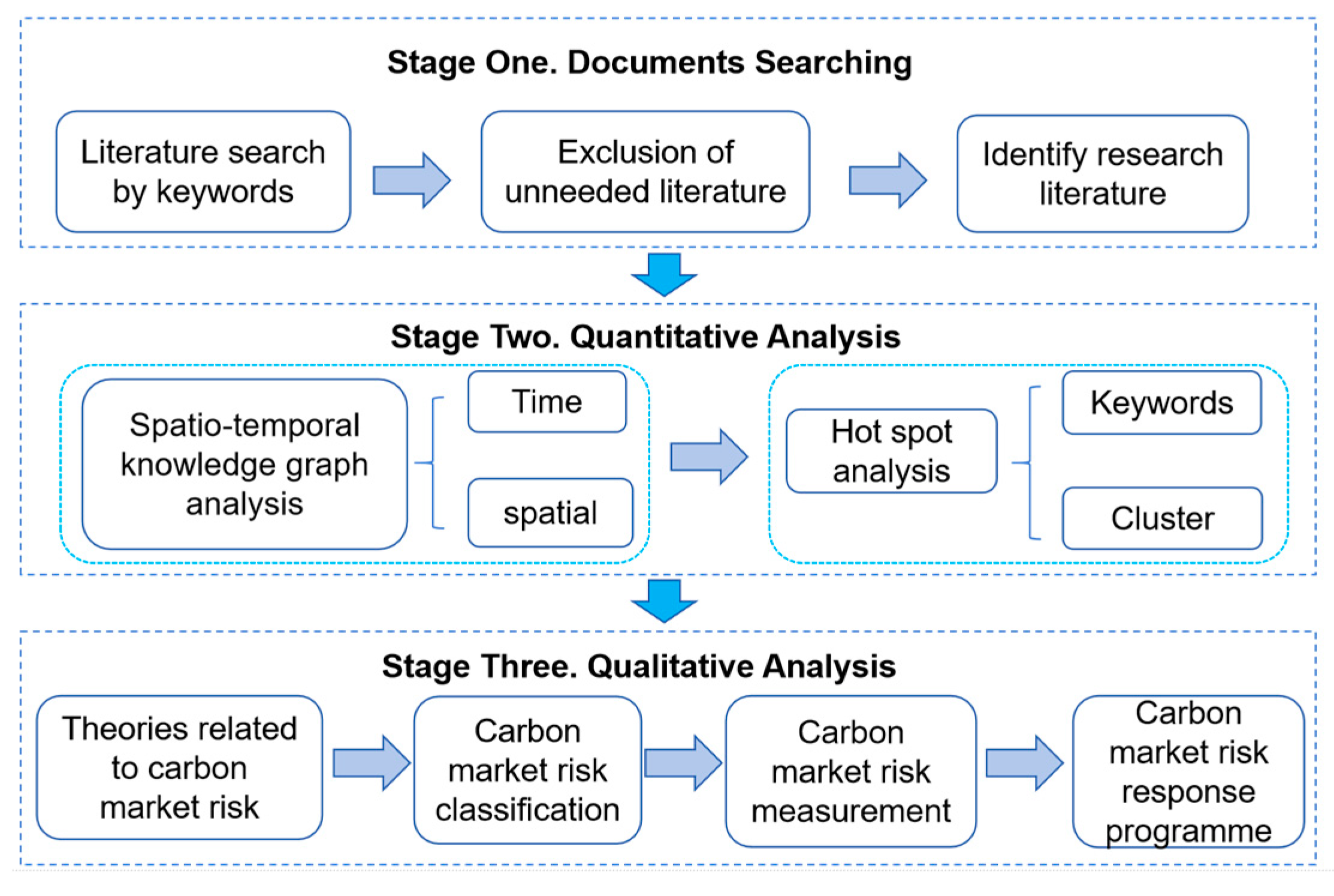

2. Materials and Methods

3. Results and Analyses

3.1. Spatiotemporal Knowledge Mapping and Research Trend Analysis

3.1.1. Time Distribution

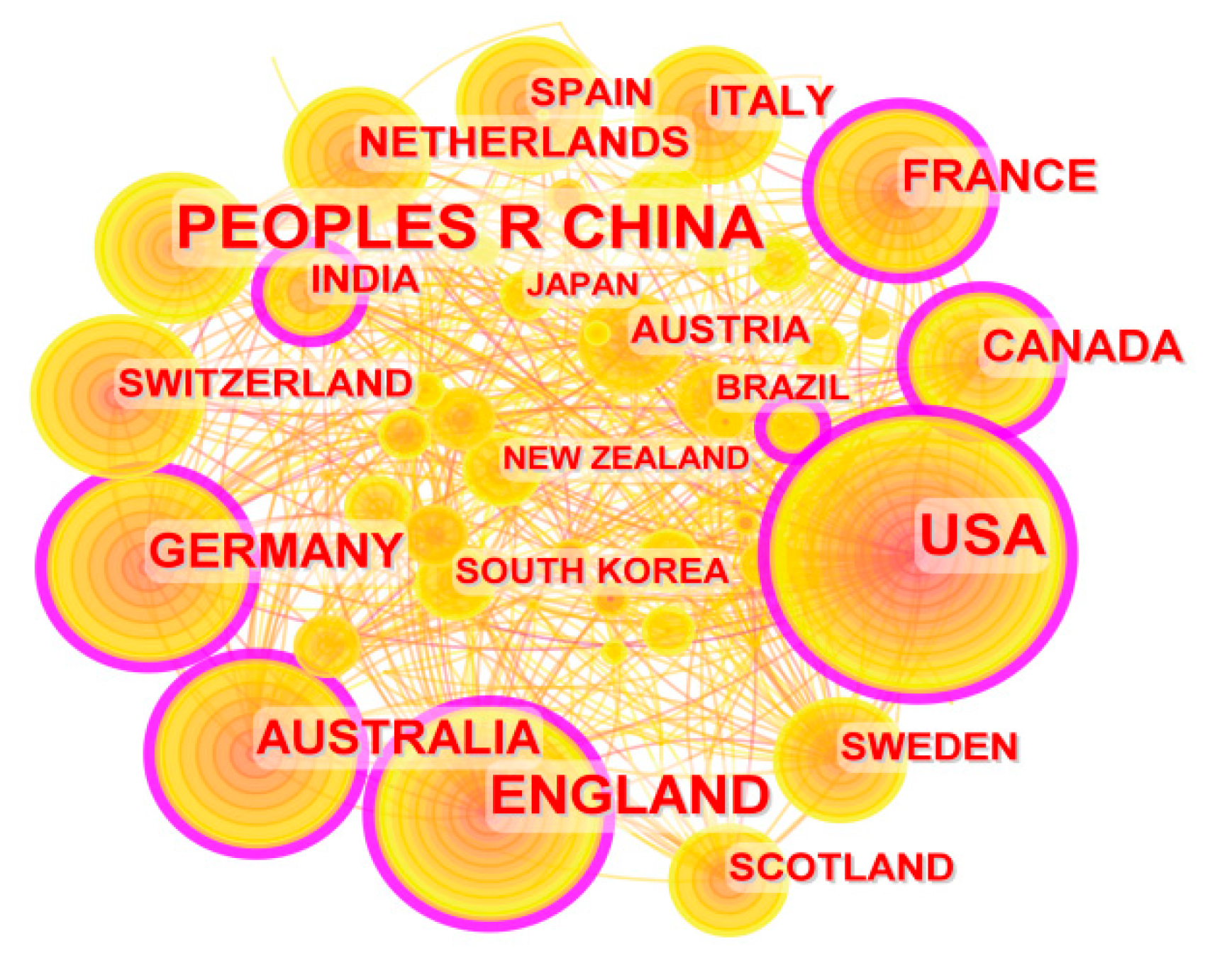

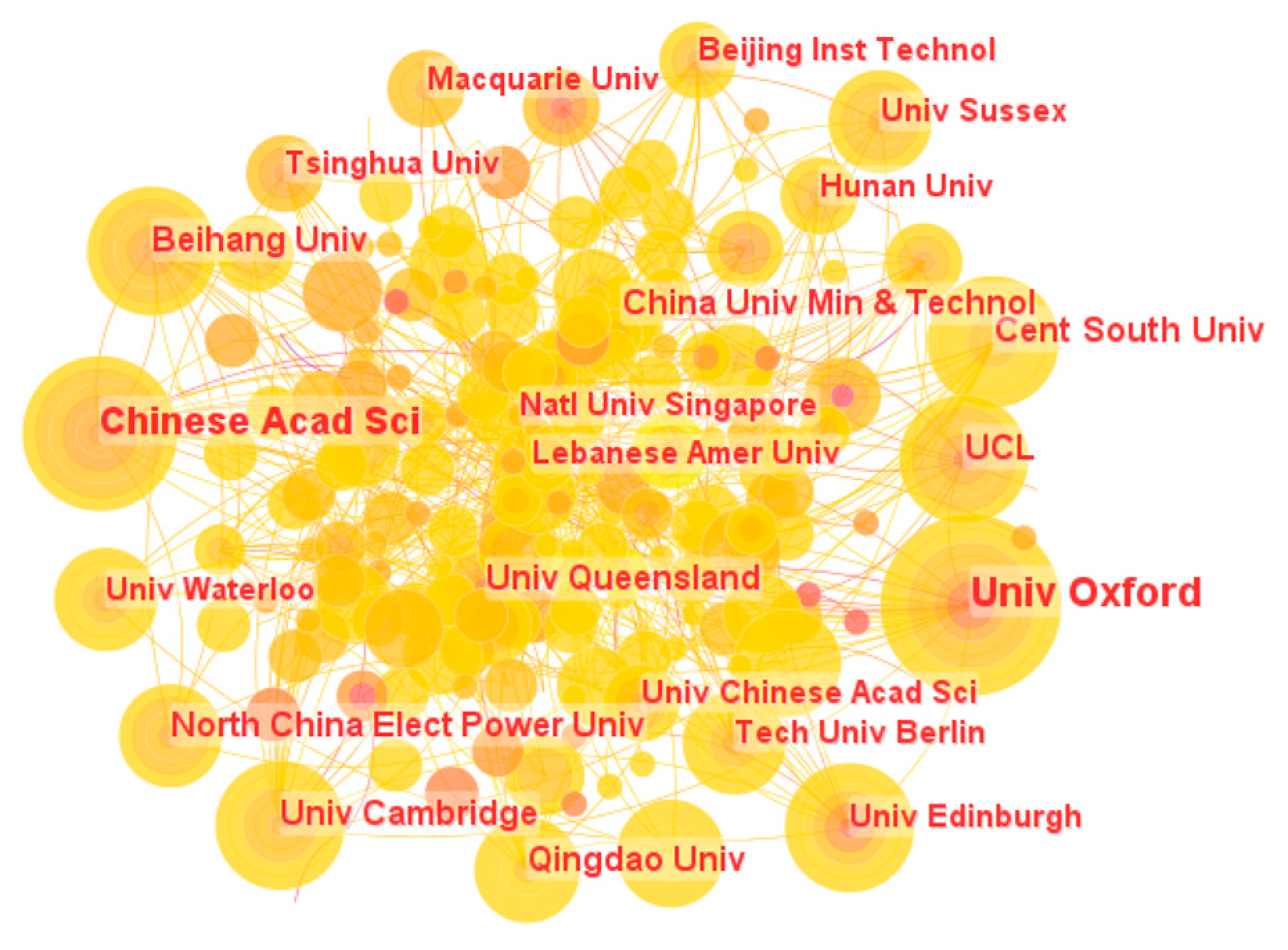

3.1.2. Spatial Distribution

3.2. Content Knowledge Mapping and Research Trend Analysis

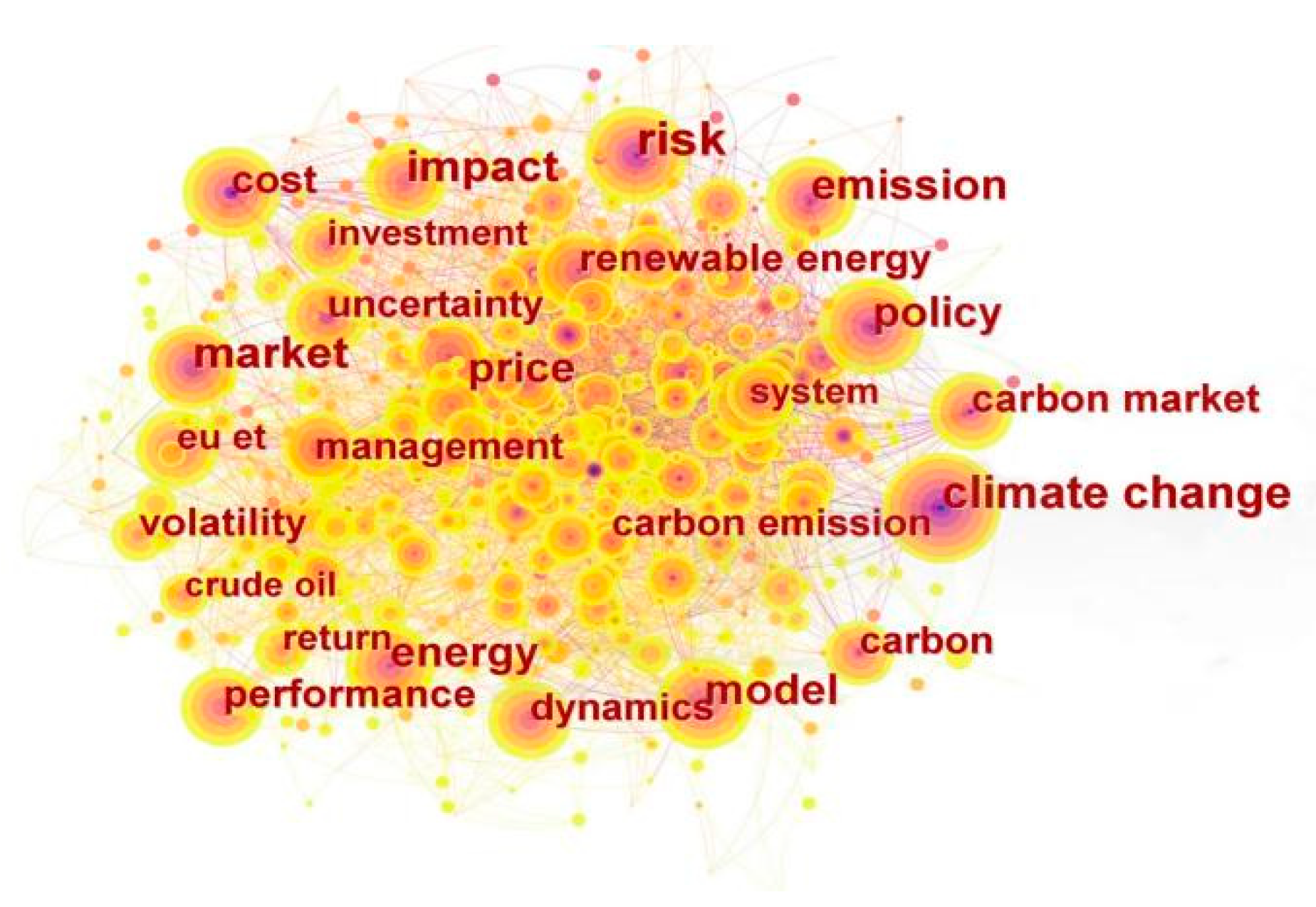

3.2.1. Keyword Co-Occurrence Analysis

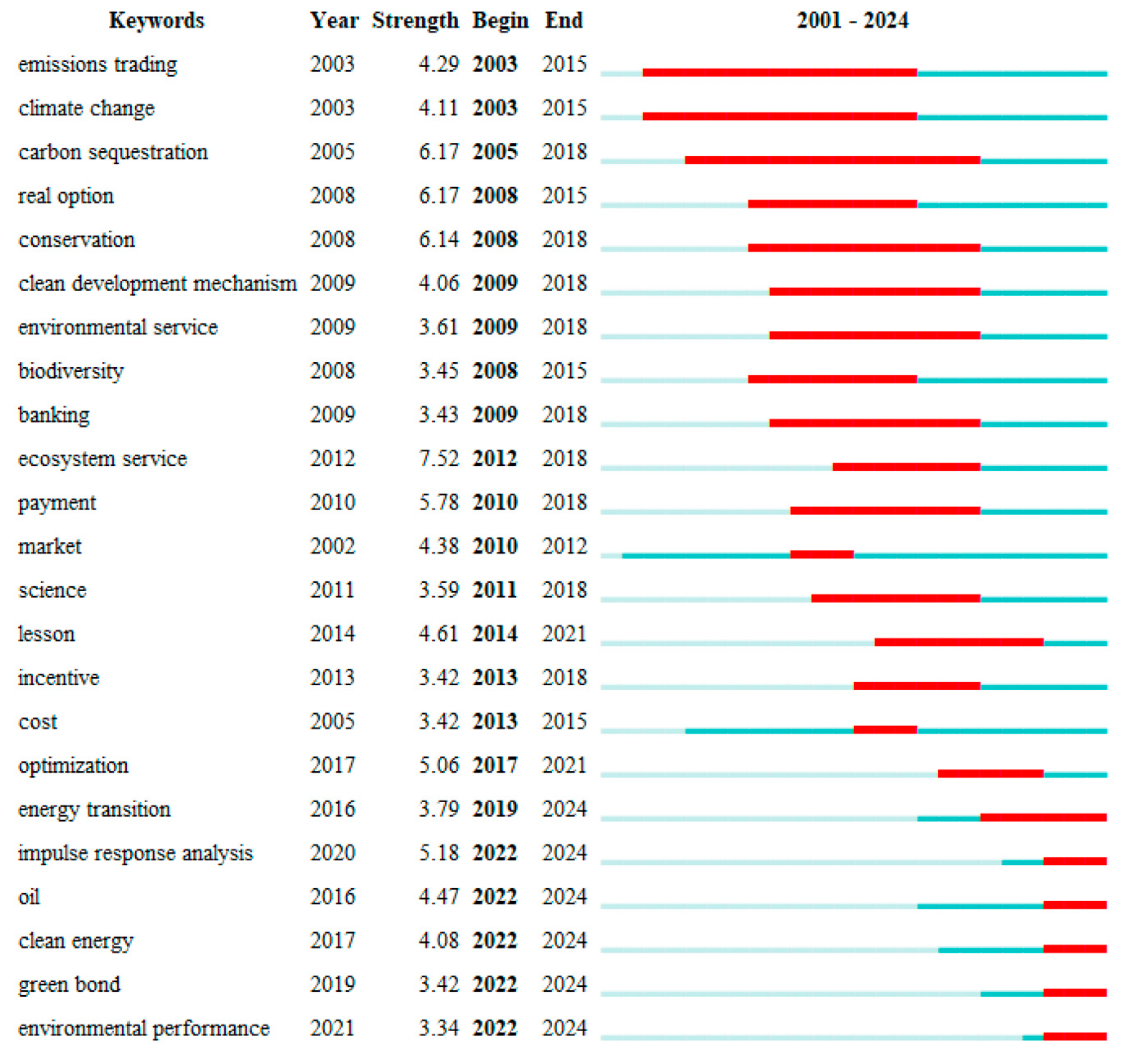

3.2.2. Keyword Highlighting Analysis

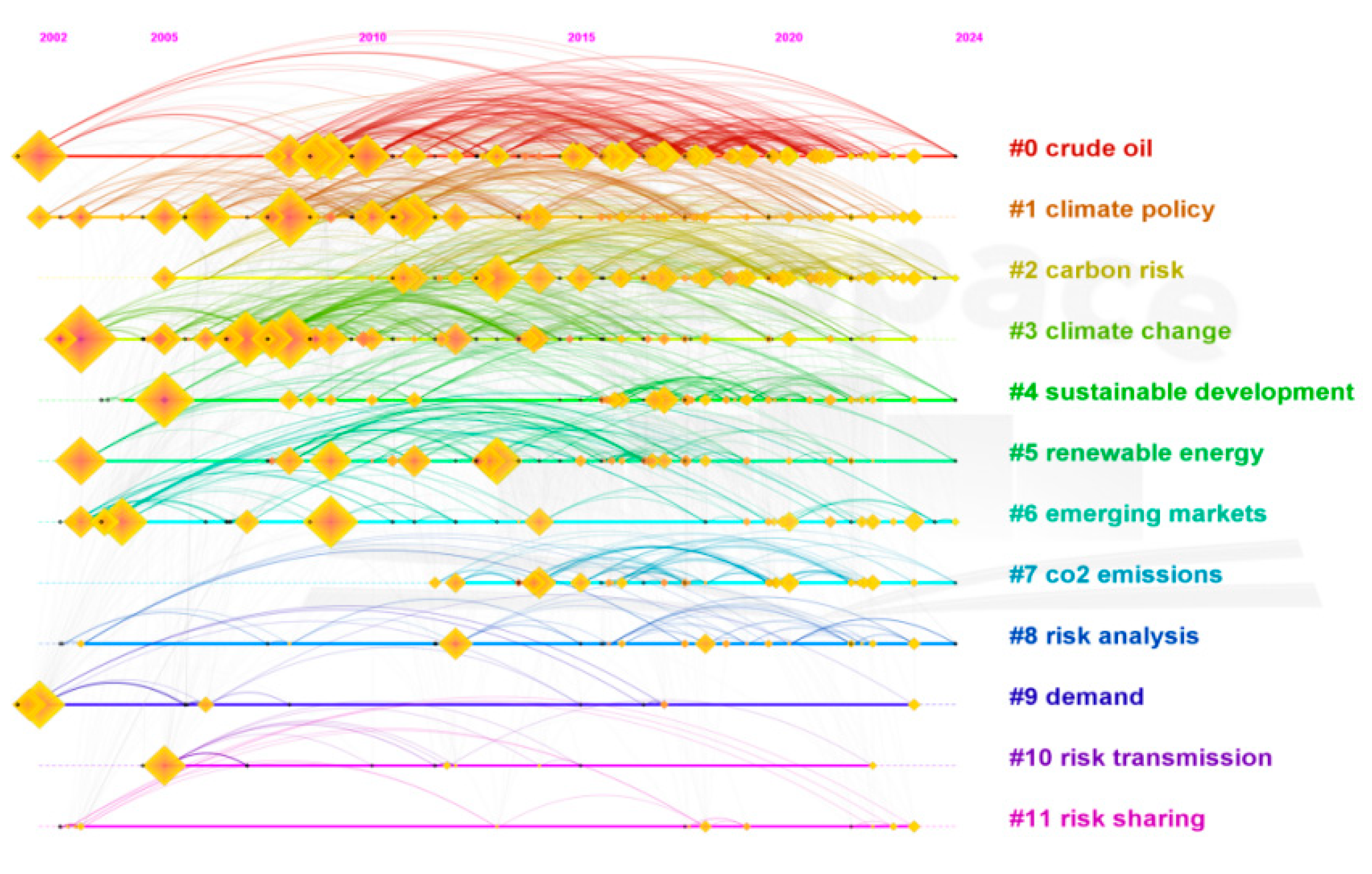

3.3. Cluster Mapping of Research Hotspots

3.4. Analysis of Research Trends under the Distribution of Subject Headings

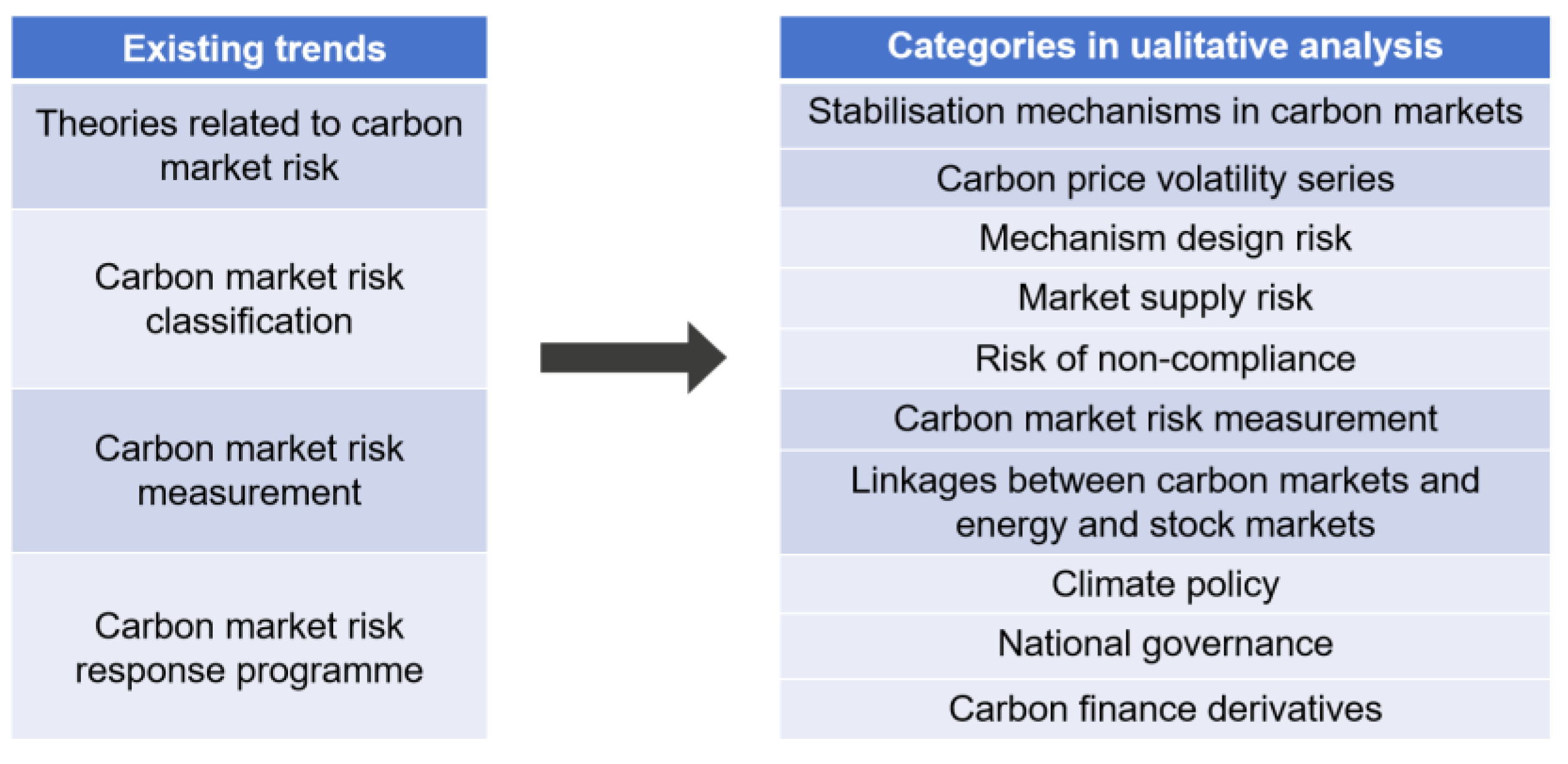

3.4.1. Theories Related to Carbon Market Risk

3.4.2. Carbon Market Risk Classification

3.4.3. Carbon Market Risk Measurement

3.4.4. Carbon Market Risk Response Program

3.5. Review of the State of the Art

4. Conclusions and Future Research Directions

4.1. Conclusions

4.1.1. Quantitative Analysis of Conclusions

4.1.2. Qualitative Analysis of Conclusions

4.2. Future Research Directions

4.2.1. International Cooperation

4.2.2. Promotion of Disciplinary Integration

4.2.3. Improving Risk Management in the Carbon Market

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Nomenclature

| c | Level of confidence in the value of a sample of carbon financial products at risk |

| G11(s) | The reward value for the first occurrence state of the first experiment |

| G12(s) | The reward value for the second occurrence state of the first experiment |

| G21(s) | The reward value for the first occurrence state of the second experiment |

| Peak value | |

| Fu(y) | Value exceeding the critical value |

| R | Value of sample carbon financial products at risk at confidence level c |

| s | The value of a state |

| t | Time |

| u | Critical value |

| x | Sequence of returns on financial products |

| Shape parameters of the carbon price yield distribution | |

| Scale parameters of the carbon price yield distribution | |

| ΔValue | The amount of change in the value of the carbon financial product in this medium over the holding period t |

| UNCED | United Nations Conference on Environment and Development |

| IET | International emission trading |

| JI | Joint implementation |

| CDM | Clean development mechanism |

| CCS | Carbon capture and storage |

| CCUS | Carbon capture utilization and storage |

| DAC | Direct air capture |

| EUA | EU allowance |

| CER | Certified emission reduction |

| AAU | Assigned amount units |

| ETS | Carbon emissions trading system |

| BMM | Block maxima model |

| POT | Peak over threshold |

| CER | Certification emission reduction |

| sCER | Secondary certification emission reduction |

| BS Model | Black–Scholes model |

References

- Global Stocktake. Available online: https://unfccc.int/zh/topics/global-stocktake (accessed on 30 November 2023).

- Geng, W.; Zhao, X.; Zhou, X. Research on extreme risk measurement in the international carbon emission futures market, based on a two-component Beta-Skew-t-EGARCH-POT model. Appl. Econ. 2023, 55, 4194–4203. [Google Scholar] [CrossRef]

- Feng, Z.H.; Wei, Y.M.; Wang, K. Estimating risk for the carbon market via extreme value theory: An empirical analysis of the EU ETS. Appl. Energy 2012, 99, 97–108. [Google Scholar] [CrossRef]

- Zhang, C.; Yang, Y.; Yun, P. Risk measurement of international carbon market based on multiple risk factors heterogeneous dependence. Finance Res. Lett. 2020, 32, 101083. [Google Scholar] [CrossRef]

- Zhang, Y.J.; Sun, Y.F. The dynamic volatility spillover between European carbon trading market and fossil energy market. J. Clean. Prod. 2016, 112, 2654–2663. [Google Scholar] [CrossRef]

- Reboredo, J.C.; Rivera-Castro, M.A.; Ugolini, A. Wavelet-based test of co-movement and causality between oil and renewable energy stock prices. Energy Econ. 2017, 61, 241–252. [Google Scholar] [CrossRef]

- Lin, B.; Chen, Y. Dynamic linkages and spillover effects between CET market, coal market and stock market of new energy companies: A case of Beijing CET market in China. Energy 2019, 172, 1198–1210. [Google Scholar] [CrossRef]

- Ilhan, E.; Sautner, Z.; Vilkov, G. Carbon Tail Risk. Rev. Finance Stud. 2021, 34, 1540–1571. [Google Scholar] [CrossRef]

- Shiffrin, R.M.; Börner, K. Mapping knowledge domains. Proc. Natl. Acad. Sci. USA 2004, 101, 5183–5185. [Google Scholar] [CrossRef]

- Rickels, W.; Görlich, D.; Peterson, S. Explaining European emission allowance price dynamics: Evidence from phase II. Ger. Econ. Rev. 2015, 16, 181–202. [Google Scholar] [CrossRef]

- Cong, R.; Lo, A.Y. Emission trading and carbon market performance in Shenzhen, China. Appl. Energy 2017, 193, 414–425. [Google Scholar] [CrossRef]

- Zeng, S.; Jia, J.; Su, B.; Jiang, C.; Zeng, G. The volatility spillover effect of the European Union (EU) carbon financial market. J. Clean. Prod. 2021, 282, 124394. [Google Scholar] [CrossRef]

- Marimoutou, V.; Soury, M. Energy markets and CO2 emissions: Analysis by stochastic copula autoregressive model. Energy 2015, 88, 417–429. [Google Scholar] [CrossRef]

- Zhao, Y.; Xu, W. Measurement of risk spillover effect based on EV-Copula method. Humanit. Soc. Sci. Commun. 2023, 10, 765. [Google Scholar] [CrossRef]

- Feng, Z.H.; Zou, L.L.; Wei, Y.M. Carbon price volatility: Evidence from EU ETS. Appl. Energy 2011, 88, 590–598. [Google Scholar] [CrossRef]

- Dai, P.-F.; Xiong, X.; Huynh, T.L.D.; Wang, J. The impact of economic policy uncertainties on the. volatility of European carbon market. J. Commod. Mark. 2022, 26, 100208. [Google Scholar] [CrossRef]

- Deeney, P.; Cummins, M.; Dowling, M.; Smeaton, A.F. Influences from the European Parliament on EU emissions prices. Energy Policy 2016, 88, 561–572. [Google Scholar] [CrossRef]

- Costanza, R.; d’Arge, R.; De Groot, R.; Farber, S.; Grasso, M.; Hannon, B.; Limburg, K.; Naeem, S.; O’neill, R.V.; Paruelo, J.; et al. The value of the world’s ecosystem services and natural capital. Nature 1997, 387, 253–260. [Google Scholar] [CrossRef]

- Costanza, R. Ecosystem services: Multiple classification systems are needed. Biol. Conserv. 2008, 141, 350–352. [Google Scholar] [CrossRef]

- Summers, D.M.; Regan, C.M.; Settre, C.; Connor, J.D.; O’connor, P.; Abbott, H.; Frizenschaf, J.; van der Linden, L.; Lowe, A.; Hogendoorn, K.; et al. Current carbon prices do not stack up to much land use change, despite bundled ecosystem service co-benefits. Glob. Chang. Biol. 2021, 27, 2744–2762. [Google Scholar] [CrossRef]

- Dominioni, G. Pricing carbon effectively: A pathway for higher climate change ambition. Clim. Policy 2022, 22, 897–905. [Google Scholar] [CrossRef]

- Eslahi, M.; Mazza, P. Can weather variables and electricity demand predict carbon emissions allowances prices? Evidence from the first three phases of the EU ETS. Ecol. Econ. 2023, 214, 107985. [Google Scholar] [CrossRef]

- Adediran, I.A.; Swaray, R. Carbon trading amidst global uncertainty: The role of policy and geopolitical uncertainty. Econ. Model. 2023, 123, 106279. [Google Scholar] [CrossRef]

- Settre, C.M.; Connor, J.D.; Wheeler, S.A. Emerging water and carbon market opportunities for environmental water and climate regulation ecosystem service provision. J. Hydrol. 2019, 578, 124077. [Google Scholar] [CrossRef]

- Kreuter, U.P.; Harris, H.G.; Matlock, M.D.; Lacey, R.E. Change in ecosystem service values in the San Antonio area, Texas. Ecol. Econ. 2001, 39, 333–346. [Google Scholar] [CrossRef]

- Levasseur, A.; Lesage, P.; Margni, M.; Brandão, M.; Samson, R. Assessing temporary carbon sequestration and storage projects through land use, land-use change and forestry: Comparison of dynamic life cycle assessment with ton-year approaches. Clim. Chang. 2012, 115, 759–776. [Google Scholar] [CrossRef]

- Guo, J.; Gong, P. The potential and cost of increasing forest carbon sequestration in Sweden. J. For. Econ. 2017, 29, 78–86. [Google Scholar] [CrossRef]

- Mo, J.; Cui, L.; Duan, H. Quantifying the implied risk for newly-built coal plant to become stranded asset by carbon pricing. Energy Econ. 2021, 99, 105286. [Google Scholar] [CrossRef]

- Tee, J.; Scarpa, R.; Marsh, D.; Guthrie, G. Forest valuation under the New Zealand emissions trading scheme: A real options binomial tree with stochastic carbon and timber prices. Land Econ. 2014, 90, 44–60. [Google Scholar] [CrossRef]

- Yemshanov, D.; McCarney, G.R.; Hauer, G.; Luckert, M.M.; Unterschultz, J.; McKenney, D.W. A real options-net present value approach to assessing land use change: A case study of afforestation in Canada. For. Policy Econ. 2015, 50, 327–336. [Google Scholar] [CrossRef]

- Elias, R.; Wahab, M.; Fang, L. Retrofitting carbon capture and storage to natural gas-fired power plants: A real-options approach. J. Clean. Prod. 2018, 192, 722–734. [Google Scholar] [CrossRef]

- Li, L.; Duan, M.; Guo, X.; Wang, Y. The stimulation and coordination mechanisms of the carbon emission trading market of public buildings in China. Front. Energy Res. 2021, 9, 715504. [Google Scholar] [CrossRef]

- Liu, X.; Wojewodzki, M.; Cai, Y.; Sharma, S. The dynamic relationships between carbon prices and policy uncertainties. Technol. Forecast. Soc. Chang. 2023, 188, 122325. [Google Scholar] [CrossRef]

- Byun, S.J.; Cho, H. Forecasting carbon futures volatility using GARCH models with energy volatilities. Energy Econ. 2013, 40, 207–221. [Google Scholar] [CrossRef]

- Rakpho, P.; Yamaka, W. The forecasting power of economic policy uncertainty for energy demand and supply. Energy Rep. 2021, 7, 338–343. [Google Scholar] [CrossRef]

- Wang, Y.; Guo, Z. The dynamic spillover between carbon and energy markets: New evidence. Energy 2018, 149, 24–33. [Google Scholar] [CrossRef]

- Vellachami, S.; Hasanov, A.S.; Brooks, R. Risk transmission from the energy markets to the carbon market: Evidence from the recursive window approach. Int. Rev. Financ. Anal. (IRFA) 2023, 89, 102715. [Google Scholar] [CrossRef]

- Duan, K.; Liu, Y.; Yan, C.; Huang, Y. Differences in carbon risk spillovers with green versus traditional assets: Evidence from a full distributional analysis. Energy Econ. 2023, 127, 107049. [Google Scholar] [CrossRef]

- Tian, Y.; Akimov, A.; Roca, E.; Wong, V. Does the carbon market help or hurt the stock price of electricity companies? Further evidence from the European context. J. Clean. Prod. 2016, 112, 1619–1626. [Google Scholar] [CrossRef]

- Soliman, A.M.; Nasir, M.A. Association between the energy and emission prices: An analysis of EU emission trading system. Resour. Policy 2019, 61, 369–374. [Google Scholar] [CrossRef]

- Shobe, W.; Holt, C.; Huetteman, T. Elements of emission market design: An experimental analysis of California’s market for greenhouse gas allowances. J. Econ. Behav. Organ. 2014, 107, 402–420. [Google Scholar] [CrossRef]

- Holt, C.A.; Shobe, W.M. Price and quantity collars for stabilizing emission allowance prices: Laboratory experiments on the EUETS market stability reserve. J. Environ. Econ. Manag. 2016, 76, 32. [Google Scholar] [CrossRef]

- Perkis, D.F.; Cason, T.; Tyner, W. An experimental investigation of hard and soft price ceilings in emissions permit markets. Environ. Resour. Econ. 2016, 63, 703–718. [Google Scholar] [CrossRef]

- Mensi, W.; Hammoudeh, S.; Shahzad, S.J.H.; Shahbaz, M. Modeling systemic risk and dependence structure between oil and stock markets using a variational mode decomposition-based copula method. J. Bank. Finance 2017, 75, 258–279. [Google Scholar] [CrossRef]

- Chai, S.; Zhou, P. The Minimum-CVaR strategy with semi-parametric estimation in carbon market hedging problems. Energy Econ. 2018, 76, 64–75. [Google Scholar] [CrossRef]

- Balcilar, M.; Demirer, R.; Hammoudeh, S.; Nguyend, D.K. Risk spillovers across the energy and carbon markets and hedging strategies for carbon risk. Energy Econ. 2016, 54, 159–172. [Google Scholar] [CrossRef]

- Chevallier, J. Evaluating the carbon-macroeconomy relationship: Evidence from threshold vector error-correction and Markov-switching VAR models. Econ. Model. 2011, 28, 2634–2656. [Google Scholar] [CrossRef]

- Dou, Y.; Li, Y.; Dong, K.; Ren, X. Dynamic linkages between economic policy uncertainty and the carbon futures market: Does COVID-19 pandemic matter? Resour. Policy 2022, 75, 102455. [Google Scholar] [CrossRef]

- Przybojewska, I.; Pyka, M. EU carbon emission allowances as environmental and financial instruments–Is it possible to kill two birds with one stone? J. Energy Nat. Resour. Law 2024, 42, 1–26. [Google Scholar] [CrossRef]

- Yuan, X.; Bi, G.; Li, H.; Zhang, B. Stackelberg equilibrium strategies and coordination of a low-carbon supply chain with a risk-averse retailer. Int. Trans. Oper. Res. 2022, 29, 3681–3711. [Google Scholar] [CrossRef]

- Wu, Q.; Chiu, C.H. The impacts of carbon insurance on supply chain and environment considering technology risk under cap-and-trade mechanism. Transp. Res. Part E Logist. Transp. Rev. 2023, 180, 103334. [Google Scholar] [CrossRef]

- Gouda, S.K.; Saranga, H. Sustainable supply chains for supply chain sustainability: Impact of sustainability efforts on supply chain risk. Int. J. Prod. Res. 2018, 56, 5820–5835. [Google Scholar] [CrossRef]

- Zhao, L.; Wen, F. Risk-return relationship and structural breaks: Evidence from China carbon market. Int. Rev. Econ. Finance 2022, 77, 481–492. [Google Scholar] [CrossRef]

- Wang, T.; Zhang, X.; Ma, Y.; Wang, Y. Risk contagion and decision-making evolution of carbon market enterprises: Comparisons with China, the United States, and the European Union. Environ. Impact Assess. Rev. 2023, 99, 107036. [Google Scholar] [CrossRef]

- Lang, Q.; Ma, F.; Mirza, N.; Umar, M. The interaction of climate risk and bank liquidity: An emerging market perspective for transitions to low carbon energy. Technol. Forecast. Soc. Chang. 2023, 191, 122480. [Google Scholar] [CrossRef]

- Song, Y.; Liu, T.; Ye, B.; Zhu, Y.; Li, Y.; Song, X. Improving the liquidity of China’s carbon market: Insight from the effect of carbon price transmission under the policy release. J. Clean. Prod. 2019, 239, 118049. [Google Scholar] [CrossRef]

- Zhang, J.; Han, W. Carbon emission trading and equity markets in China: How liquidity is impacting carbon returns? Econ. Res.-Ekon. Istraz. 2022, 35, 6466–6478. [Google Scholar] [CrossRef]

- Pearse, R.; Böhm, S. Ten reasons why carbon markets will not bring about radical emissions reduction. Carbon Manag. 2014, 5, 325–337. [Google Scholar] [CrossRef]

- Wang, X.; Zhang, X.B.; Zhu, L. Imperfect market, emissions trading scheme, and technology adoption: A case study of an energy-intensive sector. Energy Econ. 2019, 81, 142–158. [Google Scholar] [CrossRef]

- Kim, H.S.; Koo, W.W. Factors affecting the carbon allowance market in the US. Energy Policy 2010, 38, 1879–1884. [Google Scholar] [CrossRef]

- Adekoya, O.B. Predicting carbon allowance prices with energy prices: A new approach. J. Clean. Prod. 2021, 282, 124519. [Google Scholar] [CrossRef]

- Di Febo, E.; Ortolano, A.; Foglia, M.; Leone, M.; Angelini, E. From Bitcoin to carbon allowances: An asymmetric extreme risk spillover. J. Environ. Manag. 2021, 298, 113384. [Google Scholar] [CrossRef]

- Fang, S.; Cao, G. Modelling extreme risks for carbon emission allowances—Evidence from European and Chinese carbon markets. J. Clean. Prod. 2021, 316, 128023. [Google Scholar] [CrossRef]

- Wei, Y.; Wang, Y.; Vigne, S.A.; Ma, Z. Alarming contagion effects: The dangerous ripple effect of extreme price spillovers across crude oil, carbon emission allowance, and agriculture futures markets. J. Int. Financ. Mark. Inst. Money 2023, 88, 101821. [Google Scholar] [CrossRef]

- Ha, L.T.; Bouteska, A.; Sharif, T.; Abedin, M.Z. Dynamic interlinkages between carbon risk and volatility of green and renewable energy: A TVP-VAR analysis. Res. Int. Bus. Finance 2024, 69, 102278. [Google Scholar] [CrossRef]

- Li, H.; Li, Q.; Huang, X.; Guo, L. Do green bonds and economic policy uncertainty matter for carbon price? New insights from a TVP-VAR framework. Int. Rev. Financ. Anal. 2023, 86, 102502. [Google Scholar] [CrossRef]

- Ren, X.; Xiao, Y.; He, F.; Gozgor, G. The contagion of extreme risks between fossil and green energy markets: Evidence from China. Quant. Finance 2024, 24, 627–642. [Google Scholar] [CrossRef]

- Li, P.; Zhang, H.; Yuan, Y.; Hao, A. Time-varying impacts of carbon price drivers in the EU ETS: A TVP-VAR analysis. Front. Environ. Sci. 2021, 9, 651791. [Google Scholar] [CrossRef]

- Patton, A.J.; Ziegel, J.F.; Chen, R. Dynamic semiparametric models for expected shortfall (and value-at-risk). J. Econ. 2019, 211, 388–413. [Google Scholar] [CrossRef]

- Zaroni, H.; Maciel, L.B.; Carvalho, D.B.; Pamplona, E.D.O. Monte Carlo Simulation approach for economic risk analysis of an emergency energy generation system. Energy 2019, 172, 498–508. [Google Scholar] [CrossRef]

- Zhang, C.; Ma, T.; Shi, C.; Chiu, Y.H. Carbon emission from the electric power industry in Jiangsu province, China: Historical evolution and future prediction. Energy Environ. 2023, 34, 1910–1936. [Google Scholar] [CrossRef]

- Batten, J.A.; Kinateder, H.; Szilagyi, P.G.; Wagner, N.F. Hedging stocks with oil. Energy Econ. 2021, 93, 104422. [Google Scholar] [CrossRef]

- Hsiao, Y.J.; Tsai, W.C. Financial literacy and participation in the derivatives markets. J. Bank. Finance 2018, 88, 15–29. [Google Scholar] [CrossRef]

- Wang, Y.; Wang, J. Pricing of American Carbon Emission Derivatives and Numerical Method under the Mixed Fractional Brownian Motion. Discret. Dyn. Nat. Soc. 2021, 2021, 6612284. [Google Scholar] [CrossRef]

- Demiralay, S.; Gencer, H.G.; Bayraci, S. Carbon credit futures as an emerging asset: Hedging, diversification and downside risks. Energy Econ. 2022, 113, 106196. [Google Scholar] [CrossRef]

- Gong, X.; Li, M.; Guan, K.; Sun, C. Climate change attention and carbon futures return prediction. J. Futur. Mark. 2023, 43, 1261–1288. [Google Scholar] [CrossRef]

- Liu, Z.; Huang, S. Carbon option price forecasting based on modified fractional Brownian motion optimized by GARCH model in carbon emission trading. N. Am. J. Econ. Finance 2021, 55, 101307. [Google Scholar] [CrossRef]

- Viteva, S.; Veld-Merkoulova, Y.V.; Campbell, K. The forecasting accuracy of implied volatility from ECX carbon options. Energy Econ. 2014, 45, 475–484. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Annual Number of Publications | Cumulative Number of Articles Issued |

|---|---|---|

| 2024 | 28 | 1274 |

| 2023 | 186 | 1246 |

| 2022 | 189 | 1060 |

| 2021 | 160 | 871 |

| 2020 | 139 | 711 |

| 2019 | 102 | 572 |

| 2018 | 92 | 470 |

| 2017 | 76 | 378 |

| 2016 | 54 | 302 |

| 2015 | 37 | 248 |

| 2014 | 38 | 211 |

| 2013 | 35 | 173 |

| 2012 | 33 | 138 |

| 2011 | 30 | 105 |

| 2010 | 14 | 75 |

| 2009 | 17 | 61 |

| 2008 | 14 | 44 |

| 2007 | 7 | 30 |

| 2006 | 6 | 23 |

| 2005 | 5 | 17 |

| 2004 | 2 | 12 |

| 2003 | 6 | 10 |

| 2002 | 4 | 4 |

| No | Journal | Topic | Frequency |

|---|---|---|---|

| 1 | Energy Economics | Energy development, energy commodities, environment and climate | 98 |

| 2 | Sustainability | Climate change, urban planning, renewable energy | 80 |

| 3 | Energy Policy | Energy and environmental regulations, the security of the energy supply | 72 |

| 4 | Journal of Cleaner Production | Cleaner production, environment, and sustainability research | 50 |

| 5 | Climate Policy | Policy and governance, adaptation and mitigation, policy design and development, and program delivery | 47 |

| 6 | Applied Economics | Energy conversion and conservation, the optimal use of energy resources | 27 |

| 7 | Renewable and Sustainable Energy Reviews | Renewable and sustainable energy applications, policies, and environmental impacts | 22 |

| 8 | Finance Research Letters | Emerging markets, energy finance, and energy markets | 21 |

| 9 | Resources Policy | Mineral and fossil fuel extraction, production, and use | 21 |

| 10 | Ecology Economic | Valuation of natural resources, sustainable agriculture and development, ecologically integrated technology | 18 |

| No | Keyword | Word Frequency | Year of First Occurrence | Keyword | Centrality | Year of First Occurrence |

|---|---|---|---|---|---|---|

| 1 | risk | 219 | 2008 | carbon market | 0.08 | 2006 |

| 2 | climate change | 185 | 2003 | carbon | 0.08 | 2005 |

| 3 | impact | 158 | 2009 | dynamics | 0.07 | 2002 |

| 4 | market | 154 | 2002 | emission | 0.05 | 2007 |

| 5 | price | 125 | 2004 | investment | 0.05 | 2009 |

| 6 | emission | 121 | 2007 | economics | 0.05 | 2003 |

| 7 | policy | 118 | 2006 | climate | 0.05 | 2007 |

| 8 | energy | 114 | 2009 | adoption | 0.05 | 2010 |

| 9 | model | 112 | 2010 | energy efficiency | 0.05 | 2003 |

| 10 | renewable energy | 87 | 2003 | governance | 0.04 | 2008 |

| 11 | carbon market | 87 | 2006 | climate policy | 0.04 | 2010 |

| 12 | volatility | 85 | 2016 | technology | 0.04 | 2011 |

| 13 | performance | 85 | 2013 | CO2 emission | 0.04 | 2015 |

| 14 | cost | 82 | 2005 | carbon sequestration | 0.04 | 2005 |

| 15 | carbon | 73 | 2005 | energy market | 0.04 | 2004 |

| No. | Size of Cluster | Co-Occurring Keywords Ranked 1–5 in Each Cluster | S | Average Year of Citation |

|---|---|---|---|---|

| #0 | 168 | crude oil; spillover; carbon market; carbon price; EU ETS | 0.714 | 2017 |

| #1 | 142 | climate policy; real options; emissions trading; carbon capture and storage; clean development mechanism | 0.653 | 2013 |

| #2 | 135 | carbon risk; carbon disclosure; cost of debt; carbon emissions; CDP | 0.581 | 2018 |

| #3 | 132 | climate change; ecosystem services; biodiversity; forest management | 0.747 | 2012 |

| #4 | 81 | sustainable development; natural gas; portfolio theory; optimal taxation; quantile connectedness | 0.752 | 2017 |

| #5 | 73 | renewable energy; climate change; electricity system; carbon market; investment | 0.788 | 2015 |

| #6 | 72 | emerging markets; financial performance; geopolitical risk; COVID-19 pandemic; exponentially weighted moving average | 0.808 | 2013 |

| #7 | 58 | CO2 emissions; demand uncertainty; financial development; carbon leakage; economic growth | 0.769 | 2018 |

| #8 | 36 | risk analysis; carbon pricing; nanomaterials; global climate change; energy policy | 0.915 | 2016 |

| #9 | 27 | demand; scenario; dynamics; carbon reduction technology risk; thematic synthesis | 0.961 | 2007 |

| #10 | 22 | risk transmission; spectral analysis; Econ Model; dredged material; integrated model | 0.961 | 2009 |

| #11 | 19 | risk sharing; GHG emissions; market-based measures; CGE modelling; unit root test | 0.943 | 2010 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, X.; Ning, X.; Wu, C.; Zhang, Y. Evolutionary Trends in Carbon Market Risk Research. Energies 2024, 17, 4655. https://doi.org/10.3390/en17184655

Liu X, Ning X, Wu C, Zhang Y. Evolutionary Trends in Carbon Market Risk Research. Energies. 2024; 17(18):4655. https://doi.org/10.3390/en17184655

Chicago/Turabian StyleLiu, Xinchen, Xuanwei Ning, Chengliang Wu, and Yang Zhang. 2024. "Evolutionary Trends in Carbon Market Risk Research" Energies 17, no. 18: 4655. https://doi.org/10.3390/en17184655

APA StyleLiu, X., Ning, X., Wu, C., & Zhang, Y. (2024). Evolutionary Trends in Carbon Market Risk Research. Energies, 17(18), 4655. https://doi.org/10.3390/en17184655