Has the EU Emissions Trading System Worked Properly? †

Abstract

1. Introduction

2. Literature Review

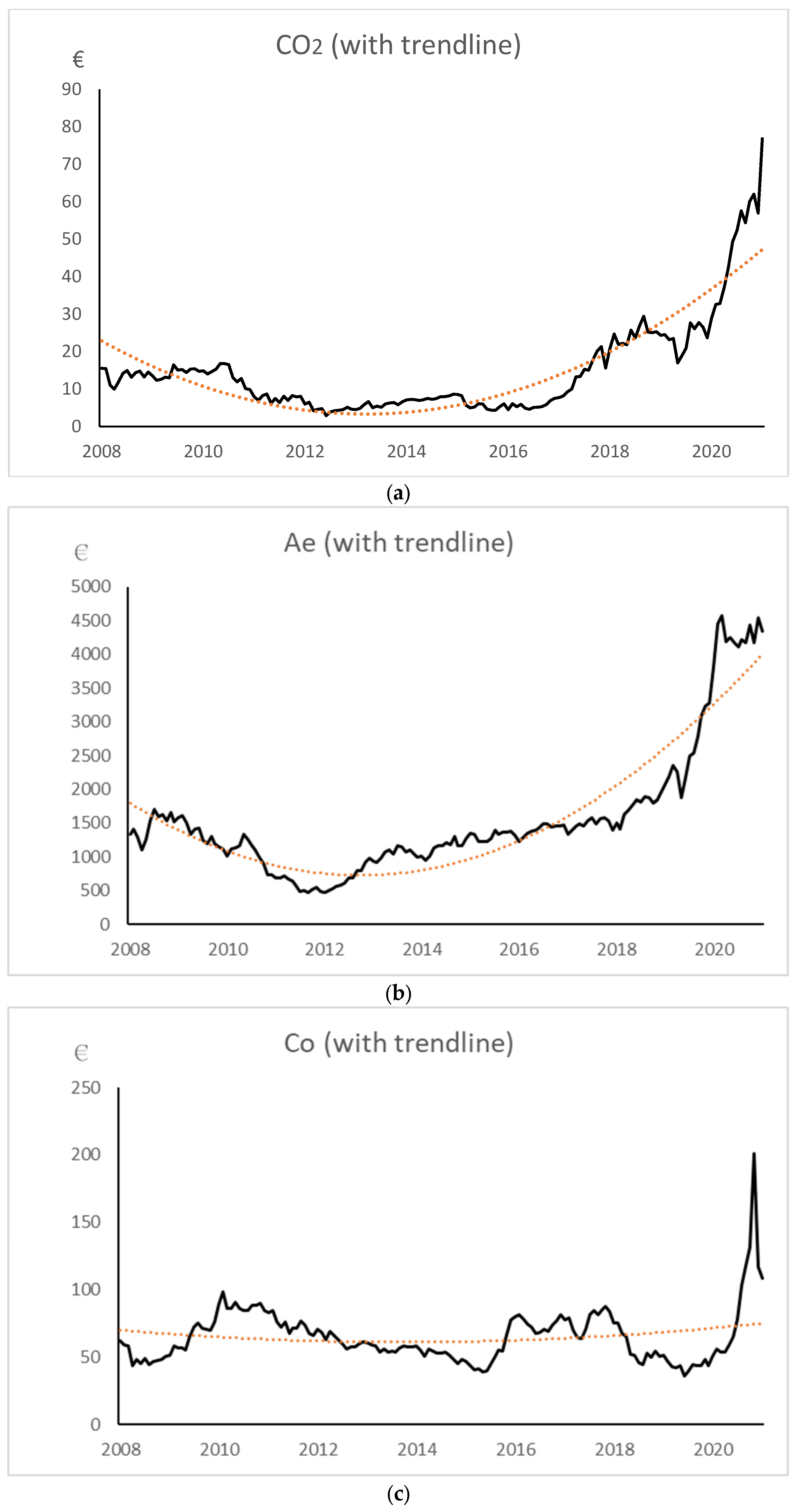

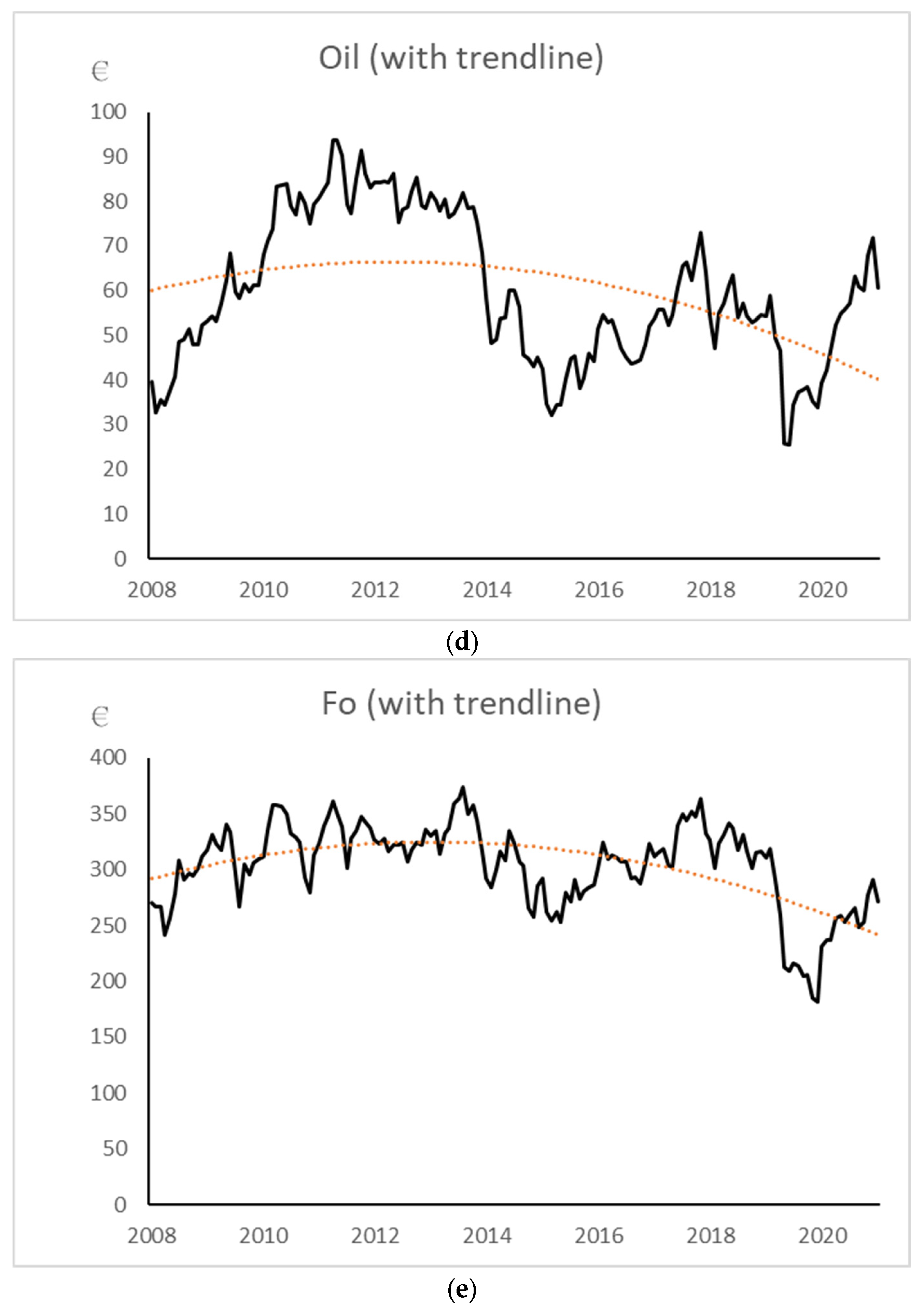

3. Data Description

4. Method

4.1. Assessing the Direction Principle

4.2. Assessing the Linking and Leadership Principles

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- European Commission. 2021. Available online: https://ec.europa.eu/clima/policies/ets_en (accessed on 20 December 2023).

- Eskander, S.; Fankhauser, S. Reduction in greenhouse gas emissions from national climate legislation. Nat. Clim. Chang. 2020, 10, 750–756. [Google Scholar] [CrossRef]

- Koch, N.; Naumann, L.; Pretis, F.; Ritter, N.; Schwarz, M. Attributing agnostically detected large reduction in road CO2 emissions to policy mixes. Nat. Energy 2022, 7, 844–856. [Google Scholar] [CrossRef]

- Brouwers, R.; Schoubben, F.; Van Hulle, C.; Van Uytbergen, S. The initial impact of EU ETS verification events on stock prices. Energy Policy 2016, 94, 138–149. [Google Scholar] [CrossRef]

- Wang, M.; Zhou, P. Does emission permit allocation affect CO2 cost pass-through? A theoretical analysis. Energy Econ. 2017, 66, 140–146. [Google Scholar] [CrossRef]

- Nava, C.; Meleo, L.; Cassetta, E.; Morelli, G. The impact of the EU ETS on the aviation sector: Competitive effects of abatement efforts by airlines. Transp. Res. Part A Policy Pract. 2018, 113, 20–34. [Google Scholar] [CrossRef]

- Best, R.; Burke, P.; Jotzo, F. Carbon pricing efficacy: Cross-country Evidence. Environ. Resour. Econ. 2020, 77, 67–94. [Google Scholar] [CrossRef]

- Vollebergh, H.; Brink, C. What can we learn from EU ETS? ifo DICE Rep. 2020, 18, 23–29. [Google Scholar] [CrossRef]

- Gu, G.; Zheng, H.; Tong, L.; Dai, Y. Does carbon financial market as an environmental policy tool promote regional energy conversation and emission reduction? Evidence from China. Energy Policy 2022, 163, 112826. [Google Scholar] [CrossRef]

- McCollum, D.; Zhou, W.; Bertram, C.; de Boer, H.; Bosetti, V.; Busch, S.; Despres, J.; Drouet, L.; Emmerling, J.; Fay, M.; et al. Energy investment needs fulfilling the Paris Agreement and achieving the sustainable development goals. Nat. Energy 2018, 3, 589–599. [Google Scholar] [CrossRef]

- Paris Agreement. Decision1/CP.17; UNFCCC: New York, NY, USA, 2015. [Google Scholar]

- Rinscheid, A.; Wüstenhagen, R. Germany’s decision to phase out coal by 2038 lags behind citizen’ timing preferences. Nat. Energy 2019, 4, 856–863. [Google Scholar] [CrossRef]

- Creti, A.; Jouvet, P.-A.; Mignon, V. Carbon price drivers: Phase I versus Phase II equilibrium? Energy Econ. 2012, 43, 327–334. [Google Scholar] [CrossRef]

- Charles, A.; Darne, O.; Fouilloux, J. Market efficiency in the European carbon markets. Energy Policy 2013, 60, 785–792. [Google Scholar] [CrossRef]

- Koch, N.; Fuss, S.; Grosjean, G.; Edenhofer, O. Causes of the EU ETS price drop: Recession, CDM, renewable policies or bit of everything? New evidence. Energy Policy 2014, 73, 676–685. [Google Scholar] [CrossRef]

- Tian, Y.; Akimov, A.; Roca, E.; Wong, V. Does the carbon market help or hurt the stock price of electricity companies? Further evidence from the European context. J. Clean. Prod. 2016, 112, 1619–1626. [Google Scholar] [CrossRef]

- Da Silva, P.P.; Moreno, B.; Figueiredo, N.C. Firm specific impacts of CO2 prices on the stock market value of the Spanish power industry. Energy Policy 2016, 94, 492–501. [Google Scholar] [CrossRef]

- Jimenez-Rodriguez, R. What happens to the relationship between EU allowances prices and stock market indices in Europe? Energy Econ. 2019, 81, 13–24. [Google Scholar] [CrossRef]

- Ortas, E.; Alvarez, I. The efficacy of the European Union Emissions Trading Scheme: Depicting the co-movement of carbon assets and energy commodities through wavelet decomposition. J. Clean. Prod. 2016, 116, 40–49. [Google Scholar] [CrossRef]

- Soliman, A.; Nasir, M. Association between the energy and emission prices: An analysis of EU emission trading system. Resour. Policy 2019, 61, 369–374. [Google Scholar] [CrossRef]

- Garcia, A.; Garcia-Alvarez, M.; Moreno, B. The impact of EU allowance prices on the stock market indices of the European power industries: Evidence from the ongoing EU ETS Phase III. Organ. Environ. 2020, 34, 1–20. [Google Scholar] [CrossRef]

- Jin, W.; Shi, X.; Zhang, L. Energy transition without dirty capital stranding. Energy Econ. 2021, 102, 105508. [Google Scholar] [CrossRef]

- He, X.; Mishra, S.; Aman, A.; Shahbaz, M.; Razzaq, A.; Sharif, A. The linkage between clean energy stocks and the fluctuations in oil price and financial stress in the US and Europe? Evidence from QARDL approach. Resour. Policy 2021, 72, 102021. [Google Scholar] [CrossRef]

- Hanif, W.; Hernandez, J.; Mensi, W.; Kang, S.; Uddin, G.; Yoon, S.-M. Nonlinear dependence and connectedness between clean/renewable energy sector equity and European emission allowance prices. Energy Econ. 2021, 101, 105409. [Google Scholar] [CrossRef]

- Chang, C.-L.; Ilomäki, J.; Laurila, H.; McAleer, M. Causality between CO2 emissions and stock markets. Energies 2020, 13, 2893. [Google Scholar] [CrossRef]

- Kirikkaleli, D.; Adebayo, T. Do renewable energy consumption and financial development matter for environmental sustainability? New global evidence. Sustain. Dev. 2021, 29, 583–594. [Google Scholar] [CrossRef]

- Daskalakis, G.; Markellos, R. Are the European carbon markets efficient? Rev. Futures Mark. 2008, 17, 103–128. [Google Scholar]

- Montagnoli, A.; de Vries, F. Carbon trading thickness and market efficiency. Energy Econ. 2010, 32, 1331–1336. [Google Scholar] [CrossRef]

- Alexeeva-Talebi, V. Cost pass-through of the EU emissions allowances: Examining the European petroleum markets. Energy Econ. 2011, 33, S75–S83. [Google Scholar] [CrossRef]

- Medina, V.; Pardo, A.; Pascual, R. The timeline of trading frictions in the European carbon market. Energy Econ. 2014, 42, 378–394. [Google Scholar] [CrossRef]

- Oestreich, M.; Tsiakas, I. Carbon emissions and stocks returns: Evidence from the EU emissions trading scheme. J. Bank. Financ. 2015, 58, 294–308. [Google Scholar] [CrossRef]

- Chang, C.-L.; Ilomäki, J.; Laurila, H.; McAleer, M. Moving average market timing in European energy markets: Production versus emissions. Energies 2018, 11, 3281. [Google Scholar] [CrossRef]

- Friedman, M. Essays in Positive Economics; University of Chicago Press: Chicago, IL, USA, 1953. [Google Scholar]

- Samuelson, P. Proof that properly anticipated prices fluctuate randomly. Ind. Manag. Rev. 1965, 6, 4–12. [Google Scholar]

- Dickey, D.; Fuller, W. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 1981, 49, 1057–1072. [Google Scholar] [CrossRef]

- Phillips, P.; Perron, P. Testing for a unit root in time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Mai, T.-K.; Foley, M.; McAleer, M.; Chang, C.-L. Impact of COVID-19 on returns-volatility spillovers in national and regional carbon markets in China. Renew. Sustain. Energy Rev. 2022, 169, 112861. [Google Scholar] [CrossRef]

- Dai, X.; Xiao, L.; Wang, Q.; Dhesi, G. Multiscale interplay of higher-order moments between the carbon and energy markets during Phase III of the EU ETS. Energy Policy 2021, 156, 112428. [Google Scholar] [CrossRef]

- Chang, C.-L.; McAleer, M.; Wang, Y. Testing co-volatility spillovers for natural gas spot, futures and ETS spot using dynamic conditional covariances. Energy 2018, 151, 984–997. [Google Scholar] [CrossRef]

- Engle, R.; Granger, C. Co-integration and error correction: Representation, estimation, and testing. Econometrica 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Granger, C. Investigating causal relations by econometric models and cross-spectral methods. Econometrica 1969, 37, 424–438. [Google Scholar] [CrossRef]

- Granger, C. Testing for causality: A personal viewpoint. J. Econ. Dyn. Control 1980, 2, 329–352. [Google Scholar] [CrossRef]

- Johansen, S. Statistical analysis of cointegration vectors. J. Econ. Dyn. Control 1988, 12, 231–254. [Google Scholar] [CrossRef]

- Sims, C. Macroeconomics and reality. Econometrica 1980, 48, 1–48. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Definition | Currency | Source |

|---|---|---|---|

| Carbon dioxide emission allowance futures (CO2) | ICE-ECX EUA EUA Futures of CO2 Emission Allowances | EURO | ICE Futures Limite Europe |

| Renewable energy index (Ae) | Ardour Global Alternative Energy Price Index Europe | EURO | Alerian S-Network Global Europe |

| Coal ARA futures (Co) | ICE COAL ARA One month coal futures price delivered to Amsterdam, Rotterdam, or Antwerp | EURO per ton | ICE Futures Europe |

| Brent oil futures (Oil) | ICE Futures Europe Brent Crude Oil Futures | EURO per barrel | ICE Futures Europe |

| Fossil energy index (Fo) | STOXX Europe 600 Oil & Gas stocks price index, EURO | EURO | STOXX Ltd., Qontigo Europe |

| Monthly Data | |||||

|---|---|---|---|---|---|

| CO2 | Ae | Co | Oil | Fo | |

| Mean | 14.827 | 1562.067 | 65.324 | 59.845 | 303.420 |

| SD | 12.945 | 955.629 | 20.130 | 16.577 | 38.406 |

| Max | 76.810 | 4571.960 | 200.966 | 93.805 | 374.266 |

| Min | 2.870 | 478.210 | 35.881 | 25.499 | 181.139 |

| Skewness | 2.257 | 1.864 | 2.447 | 0.166 | −0.882 |

| Kurtosis | 8.734 | 5.921 | 15.369 | 2.011 | 3.619 |

| J-B | 8.793 ** | 4.0001 ** | 5.924 ** | 94.144 * | 4.857 ** |

| Obs. | 157 | 157 | 157 | 157 | 157 |

| Monthly Returns | |||||

| Returns | CO2 | Ae | Co | Oil | Fo |

| Mean | 1.025 | 0.755 | 0.352 | 0.269 | 0.003 |

| SD | 14.537 | 7.367 | 9.806 | 9.512 | 5.819 |

| Max | 31.478 | 19.531 | 42.176 | 30.249 | 24.262 |

| Min | −50.173 | −21.090 | −53.808 | −59.397 | −19.516 |

| Skewness | −0.771 | −0.185 | −0.553 | −1.683 | 0.107 |

| Kurtosis | 4.125 | 3.034 | 10.207 | 12.212 | 4.750 |

| J-B | 23.663 * | 0.901 | 345.618 * | 625.244 * | 20.200 * |

| Obs. | 157 | 157 | 157 | 157 | 157 |

| Price | Returns | ||

|---|---|---|---|

| Variable | Specification | Augmented Dickey–Fuller | Augmented Dickey–Fuller |

| CO2 | Constant | 4.782 | −14.674 * |

| Constant and time trend | 3.046 | −15.172 * | |

| Ae | Constant | −1.699 | −11.200 * |

| Constant and time trend | −0.178 | −11.524 * | |

| Co | Constant | −2.907 | −12.409 * |

| Constant and time trend | −2.935 | −12.406 * | |

| Oil | Constant | −2.534 | −10.493 * |

| Constant and time trend | −3.059 | −10.488 * | |

| Fo | Constant | −2.753 | −11.722 * |

| Constant and time trend | −3.216 | −11.704 * | |

| Variable | Specification | Phillips–Perron | Phillips–Perron |

| CO2 | Constant | 5.201 | −14.630 * |

| Constant and time trend | 3.497 | −15.174 * | |

| Ae | Constant | 1.544 | −11.243 * |

| Constant and time trend | −0.212 | −11.519 * | |

| Co | Constant | −2.940 | −12.452 * |

| Constant and time trend | −2.902 | −12.447 * | |

| Oil | Constant | −2.048 | −10.347 * |

| Constant and time trend | −2.382 | −10.349 * | |

| Fo | Constant | −2.853 | −11.732 * |

| Constant and time trend | −3.334 | −11.719 * |

| Lag | LogL | LR | FPE | AIC | SC | HQ |

|---|---|---|---|---|---|---|

| 0 | −17.239 | NA | 9.35 × 107 | 0.307 | 0.4094 | 0.348 |

| 1 | 832.736 | 1629.607 | 1.07 × 1011 | −11.072 | −10.456 * | −10.822 * |

| 2 | 858.263 | 47.1800 | 1.06 × 1011 * | −11.079 * | −9.9504 | −10.621 |

| 3 | 878.104 | 35.304 | 1.14 × 1011 | −11.008 | −9.366 | −10.341 |

| 4 | 892.486 | 24.599 | 1.33 × 1011 | −10.862 | −8.7063 | −9.986 |

| 5 | 909.776 | 28.379 | 1.50 × 1011 | −10.756 | −8.087 | −9.671 |

| 6 | 923.886 | 22.186 | 1.76 × 1011 | −10.605 | −7.4233 | −9.312 |

| 7 | 939.486 | 23.454 | 2.05 × 1011 | −10.476 | −6.7804 | −8.974 |

| 8 | 960.181 | 29.686 | 2.23 × 1011 | −10.416 | −6.2078 | −8.706 |

| 9 | 990.282 | 41.104 * | 2.15 × 1011 | −10.487 | −5.7649 | −8.568 |

| 10 | 1004.683 | 18.671 | 2.60 × 1011 | −10.340 | −5.1055 | −8.213 |

| 11 | 1021.102 | 20.155 | 3.09 × 1011 | −10.222 | −4.4739 | −7.886 |

| 12 | 1036.377 | 17.699 | 3.78 × 1011 | −10.088 | −3.8266 | −7.544 |

| Hypothesized | |||

|---|---|---|---|

| No. of CE(s) | Eigenvalue | Trace Test | Prob. |

| None ** | 79.696 | 0.006 | |

| At most 1 | 0.192 | 46.673 | 0.063 |

| At most 2 | 0.154 | 20.683 | 0.388 |

| At most 3 | 0.078 | 8.107 | 0.461 |

| At most 4 | 0.050 | 0.227 | 0.634 |

| Null | ||

|---|---|---|

| α = 0 | Test Statistic | Prob. |

| CO2 | 1.228 | 0.268 |

| Ae * | 5.585 | 0.018 |

| Co | 0.248 | 0.618 |

| Oil * | 5.100 | 0.024 |

| Fo * | 5.965 | 0.015 |

| CO2 and Co | 2.171 | 0.338 |

| ΔAet | ΔOilt | ΔFot | ΔCO2t | ΔCot | |

|---|---|---|---|---|---|

Long run | −0.015 ** (0.0045) | −0.0236 ** (0.0067) | −0.0131 ** (0.0042) | 0.0078 (0.0096) | 0.0009 (0.0045) |

| Short run | |||||

| ΔCO2t−1 | −0.223 ** (0.083) | 0.112 * (0.054 | |||

| ΔCO2t−2 | 0.042 (0.096 | 0.060 (0.046) | |||

| ΔAet−1 | 0.0304 (0.175) | 0.002 (0.148) | |||

| ΔAet−2 | −0.333 (0.203) | −0.121 (0.099) | |||

| ΔCot−1 | −0.157 (0.106) | −0.046 (0.114) | |||

| ΔCot−2 | −0.071 (0.135) | 0.158 (0.122) | |||

| ΔOilt−1 | 0.164 (0.201) | 0.254 ** (0.087) | |||

| ΔOilt−2 | 0.022 (0.153) | 0.017 (0.134) | |||

| ΔFot−1 | −0.242 (0.320) | −0.119 (0.229 | |||

| ΔFot−2 | −0.333 (0.203) | −0.121 (0.098) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chang, C.-L.; Ilomäki, J.; Laurila, H. Has the EU Emissions Trading System Worked Properly? Energies 2024, 17, 3651. https://doi.org/10.3390/en17153651

Chang C-L, Ilomäki J, Laurila H. Has the EU Emissions Trading System Worked Properly? Energies. 2024; 17(15):3651. https://doi.org/10.3390/en17153651

Chicago/Turabian StyleChang, Chia-Lin, Jukka Ilomäki, and Hannu Laurila. 2024. "Has the EU Emissions Trading System Worked Properly?" Energies 17, no. 15: 3651. https://doi.org/10.3390/en17153651

APA StyleChang, C.-L., Ilomäki, J., & Laurila, H. (2024). Has the EU Emissions Trading System Worked Properly? Energies, 17(15), 3651. https://doi.org/10.3390/en17153651