3.1. Green Finance and Regional Green Energy Technological Innovation

The dual carbon goals clearly indicate that carbon reduction will be the dominant strategy for the construction of an ecological civilization in China in the foreseeable future. High-tech and clean production technologies are crucial to achieving this strategic objective. By advancing the research, application, and dissemination of green technologies, it is possible to reduce greenhouse gas emissions, enhance resource efficiency, and foster sustainable economic development. However, such technological innovations require substantial funding. Hence, developing green finance is considered an effective way to facilitate regional green energy technological innovation, which will consequently promote carbon reduction [

32,

33]. Green energy technologies can be financially supported by green finance while reducing the financing costs associated with innovation activities. By introducing financial tools like green bonds and green loans, enterprises engaged in technological innovation can access funds for the research, production, and promotion of environmentally friendly, low-carbon technologies [

34]. Furthermore, green finance assumes a supervisory role and forces businesses to participate in green innovation, acting as an essential tool to drive the transformation of development models toward sustainability. When providing financial support, financial institutions evaluate and disclose the environmental management practices of enterprises engaged in green technological innovation and encourage them to focus more on environmental responsibility and sustainable operations [

35].

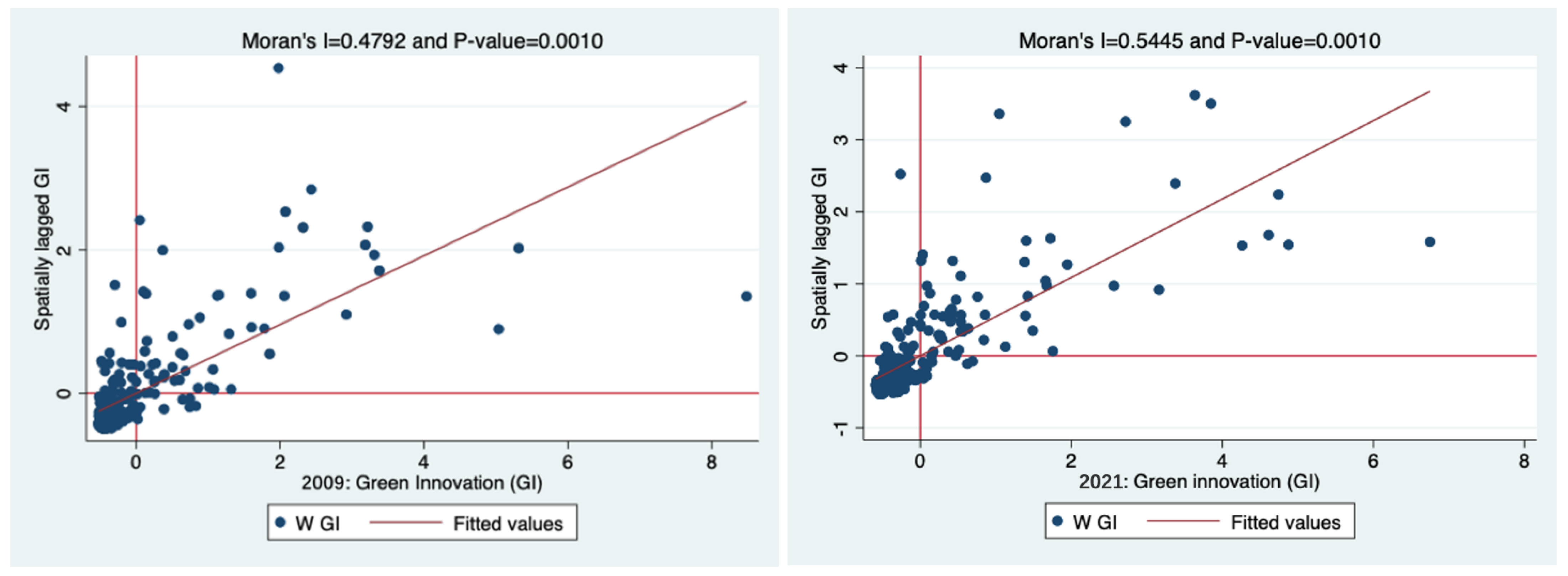

From a regional perspective, there are significant disparities in resource endowment and development levels among different regions in China. However, close economic ties and frequent flows of production factors exist among regions. The mutual influence and coordinated development among regions cannot be ignored. Therefore, further exploration is necessary to understand the spatial spillover effects of green finance on regional green energy technological innovation.

The development of green finance can stimulate local green energy technological innovation and industrial structure upgrades within a region [

36]. Extending financial services and industrial networks can increase investments in neighboring regions, facilitate knowledge and information spillovers, and promote specialized divisions of labor, thus affecting the technological innovation level and industrial structure of surrounding areas [

37]. From the perspective of green technological innovation, support from green finance attracts more investment and funds into the local green technology sector [

38]. These funds can be utilized to develop new technologies, improve existing ones, and expand the scale of green projects. The diffusion of capital, knowledge, and technology within the local area will contribute to promoting technological innovation in other regions [

39]. Concerning the industrial structure, green finance drives local enterprises toward green and sustainable development, which optimizes and upgrades the local industrial structure. This, in turn, attracts more enterprises and institutions from neighboring regions to the green technology sector, forming a virtuous cycle of industrial agglomeration [

40]. Additionally, successful innovation in green energy technology by certain entities supported by green finance can have a demonstration effect, prompting interest and emulation by enterprises and institutions in other regions, thus propelling the innovation and application of green energy technology and fostering green technological development within their respective regions [

41]. Therefore, green finance emerges as a critical driver of the coordinated development of regional green energy technological innovation. Technological innovation enterprises or projects supported by green finance not only drive their own and the entire region’s development but also generate a positive spillover effect on other regions. Based on the above analysis, we put forward the following hypotheses:

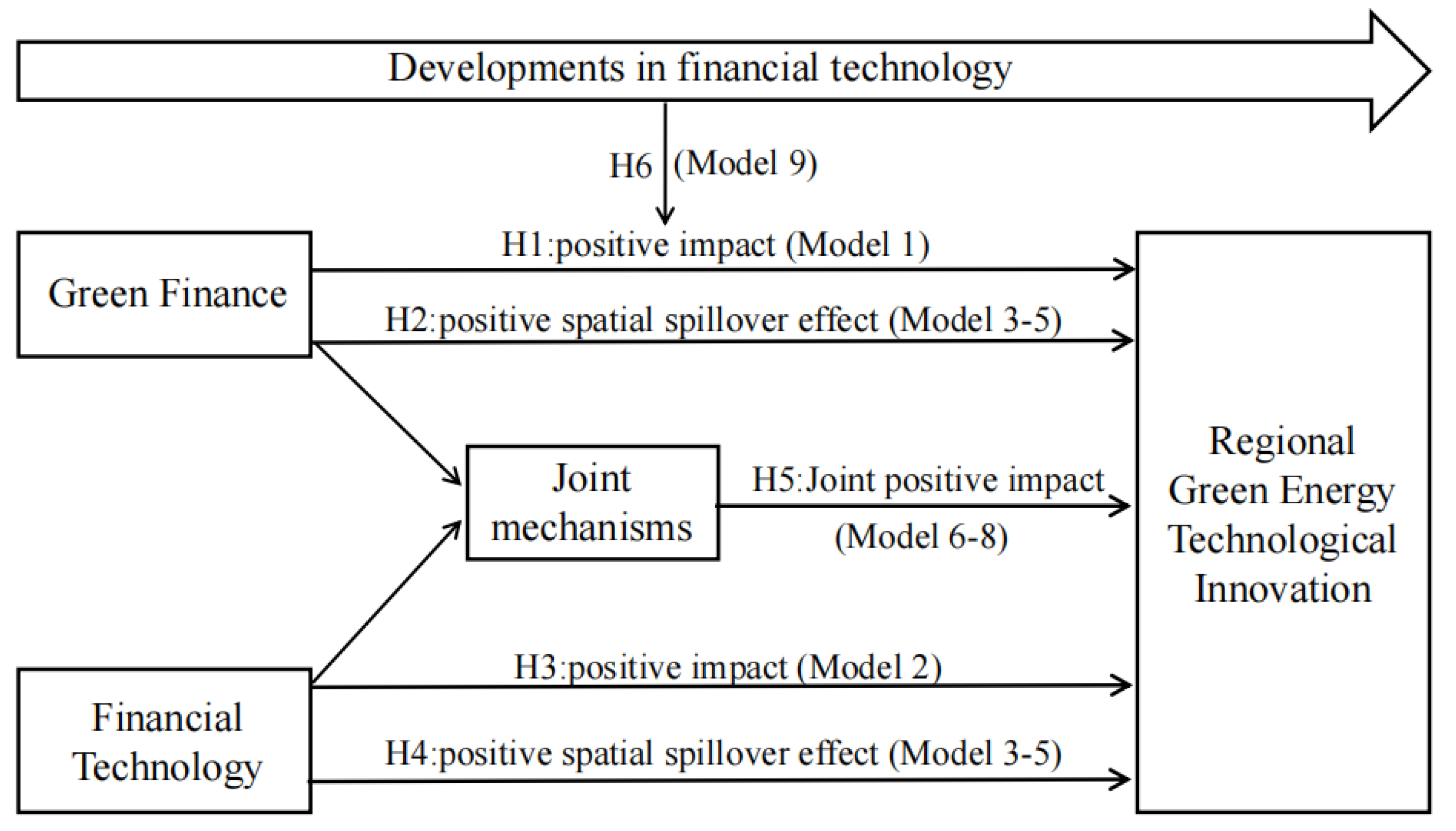

Hypothesis 1 (H1). Green finance has a significantly positive impact on regional green energy technological innovation.

Hypothesis 2 (H2). Green finance exhibits a significantly positive spatial spillover effect on regional green energy technological innovation.

3.2. Financial Technology and Regional Green Energy Technological Innovation

In 2011, the term “financial technology” was officially introduced to describe how technology-driven enterprises utilize cutting-edge technological advancements to strengthen the financial industry. Essentially, financial technology represents a shift toward technology-driven service provision, with the underlying goals revolving around optimization and transformation within the financial sector. Its dual objectives are to enhance efficiency and reduce costs, especially for enterprise users (B2B) [

42]. The development of financial technology has propelled information exchange, capital flow, and knowledge dissemination. On the one hand, the “technological dividends” generated by the advancement of financial technology can be widely applied to the research and development of low-carbon and energy-saving technologies, thereby enhancing the green effects of innovation. On the other hand, financial technology can infuse sufficient elements into the development of eco-friendly industries and the construction of an ecological civilization, driving industrial upgrading and transformation.

Green innovation is characterized by high starting points, significant investments, long cycles, and high risk. The pricing of green products sometimes dissuades certain customers [

43]. Research indicates that even after implementing green innovation, companies may not experience significantly improved financial performance; in some cases, there may even be a decline [

44]. Organizations transitioning toward green practices require financial or other resource support to achieve breakthrough green innovation. Moreover, outside of company boundaries, bank credits involve high management and supervisory costs both during and after the loan period. Serious “market failures” have occurred in green innovation concerning investment and transformation. Given China’s current economic transformation amidst an economic downturn, many emerging knowledge-intensive enterprises face internal financial constraints, necessitating the acquisition of essential funds through external financing to speed up the development and transformation of green innovation and research outcomes.

In this context, financial technology can potentially overcome the financial constraints faced by enterprises and mitigate the negative impact of “dual externality” on green innovation. “Dual externality” refers to the impact of innovation during its initial stages continuing to affect subsequent developments [

45]. It includes negative components that, to some extent, diminish enterprises’ enthusiasm for choosing green innovation. On the one hand, green innovation has a knowledge spillover effect. In this scenario, the lack of market protection for intellectual property rights might result in some companies imitating another company’s green technology, thereby weakening the incentive for the company to continue innovating [

46]. On the other hand, there is the issue of trade-offs in pollutant emissions. Businesses may be hesitant to spend large amounts of money on green innovation if the cost of innovation is higher than the cost of emissions. This leads to companies evading regulations and choosing direct emission of pollutants as a way to control costs and maintain profitability [

47].

Financial technology can be a driver when integrated with green innovation scenarios. Gomber et al. [

48] emphasize that financial technology can create new products and services through big data, thereby reducing the cost of banks acquiring customers. On the other hand, from a risk management perspective, financial technology can operate in the credit market, reducing information asymmetry, lowering screening and monitoring costs, and restraining borrowing enterprises [

49]. At the same time, by leveraging its characteristics, financial technology can assist lending institutions in establishing credit assessment models, further reducing risk assessment costs [

50]. This advanced optimization process can alleviate credit constraints for relevant enterprises, improving the distribution of green credit efficiency. Additionally, it can enhance the post-lending supervision capability, thereby improving the efficiency of enterprise green investments.

Furthermore, there is a strong correlation between regional financial technology development and the driving force of financial technology behind green innovation. The number of green patents by firms increases with the degree of regional financial technology development. While optimizing modern financial systems, financial technology simultaneously offers favorable funding and financial support for enterprises’ green transformation.

In today’s sustainable development-oriented environment, finance acts as a driver of business innovation, and the field of green innovation is a constituent part of extensive innovative endeavors propelled by advancements in financial technology.

The promotion of green innovation by financial technology is primarily concentrated in regions with higher environmental regulatory standards, considerably more financial institutions, high-polluting industries, and enterprises facing stricter financing constraints. Elucidating the relationships between financial technology, green finance, and regional green technological innovation during the period of comprehensive economic and social green transformation has significant practical importance with regard to deepening financial institutions’ business operations, facilitating industrial green transformation and upgrading, and realizing China’s dual-carbon strategic goals.

This study proposes the following theoretical mechanisms based on the above analysis:

Hypothesis 3 (H3). Financial technology has a significantly positive impact on regional green energy technological innovation.

Hypothesis 4 (H4). Financial technology exhibits a significantly positive spatial spillover effect on regional green energy technological innovation.

3.3. Green Finance, Financial Technology, and Regional Green Energy Technological Innovation

In recent years, China’s green finance has made great strides, laying the groundwork for a green finance system primarily centered around green credit. However, this development has also encountered some issues, such as inefficiencies in green financial service delivery, the emergence of “greenwashing”, and challenges related to information asymmetry. These situations have cast doubt on the quality of green finance development [

15,

51]. Against the backdrop of a new technological revolution and industrial transformation, financial technology, represented by emerging technologies such as artificial intelligence, big data, cloud computing, and blockchain, is rapidly permeating the field of green finance. This integration not only empowers the development of green finance from various perspectives but also effectively addresses the various issues encountered in the process of developing green finance [

52].

Financial technology can comprehensively collect enterprise information from multiple channels, effectively alleviating the information asymmetry prevalent in the field of green finance. This significantly reduces the difficulty of pre-review and the monitoring cost of green finance and enhances accuracy in identifying green entities and innovative green technology projects for financial institutions [

53]. On the one hand, big data technology can capture and integrate various standardized and non-standardized data in real-time, consolidating the data into credit or green behavior information. On the other hand, blockchain technology, with its “unforgeable”, “traceable”, and “immutable” properties, can monitor the real-time flow of green funds [

54]. At the same time, financial technology also uses digital technologies to provide relatively accurate forecasts of returns on various products. It can also precisely identify potential green finance demands of customers and enterprises across different scenarios, strongly propelling the innovation of green finance products and improving the efficiency of green financial services [

55]. Moreover, through information processing technology, financial technology assists regulatory authorities in collecting transactional information related to green finance, enhancing the comprehensive management capability of this emerging industry. This support is crucial in preventing capital idleness and addressing issues related to greenwashing [

56]. Green finance supports green projects and provides financial assistance to enterprises engaged in technological innovation, promoting the innovative development of green technology. Additionally, the extension of financial services and industrial networks plays a pivotal role in increasing investments, disseminating knowledge and information, and fostering a specialized division of labor in surrounding regions concerning green technological innovation.

Based on the above analysis, this paper posits the following hypothesis:

Hypothesis 5 (H5). Green finance and financial technology have a significant joint positive impact on regional energy green technology innovation.

3.4. Green Finance and Regional Green Energy Innovation across Different Stages of Financial Technology Development

The promotion of regional green energy technological innovation by green finance cannot be detached from the empowerment provided by financial technology. Financial technology serves as a crucial tool for green finance to stimulate and incentivize elements crucial for technological development and innovation. It guides capital flows toward green and emerging technology industries, supports green innovation activities, and facilitates the greenization of financial fund circulation [

48,

57,

58].

First, financial technology helps financial institutions alleviate issues such as idling capital and greenwashing caused by information asymmetry and incompleteness. In the absence of adequate financial technology (lacking relevant big data platforms and tools), investors struggle to obtain comprehensive information, making it challenging to appropriately assess the benefits and threats of regional technical advancement projects related to green energy. This limitation constrains the role of green finance in driving green energy technological innovation [

59]. Additionally, financial technology based on digital technologies like big data, blockchain, and artificial intelligence incorporates economic development cycles, risk preferences, and personalized demands into the design of green financial products. It innovates financial service solutions to better meet enterprise clients’ needs at different research and development stages. However, when financial technology is underdeveloped, the capital flow tends to be restricted within traditional financial systems, making it challenging to channel funds specifically into green energy technological innovation areas. The lack of specialized green financial products and services makes it challenging for investors and fund providers to easily find opportunities for investing in green energy technological innovation [

60]. Moreover, the development of financial technology dramatically simplifies and optimizes the transaction processes of green finance, reducing transaction costs while maintaining low operational risks. In contrast, underdeveloped financial technology results in complex and cumbersome transaction processes within green finance, indirectly limiting its role in driving green energy technological innovation [

60].

Green finance thus can only successfully drive regional green energy technological innovation at a high degree of financial technology development. The following hypothesis is posited based on the above analysis:

Hypothesis 6 (H6). When financial technology is underdeveloped, green finance cannot significantly drive regional green energy technological innovation. However, as the development level of financial technology increases, the positive impact of green finance on regional green energy technological innovation is continually strengthened.

{kind=link}

{kind=link}

{kind=link}