Research on Risk Measurement of China’s Carbon Trading Market

Abstract

:1. Introduction

- (1)

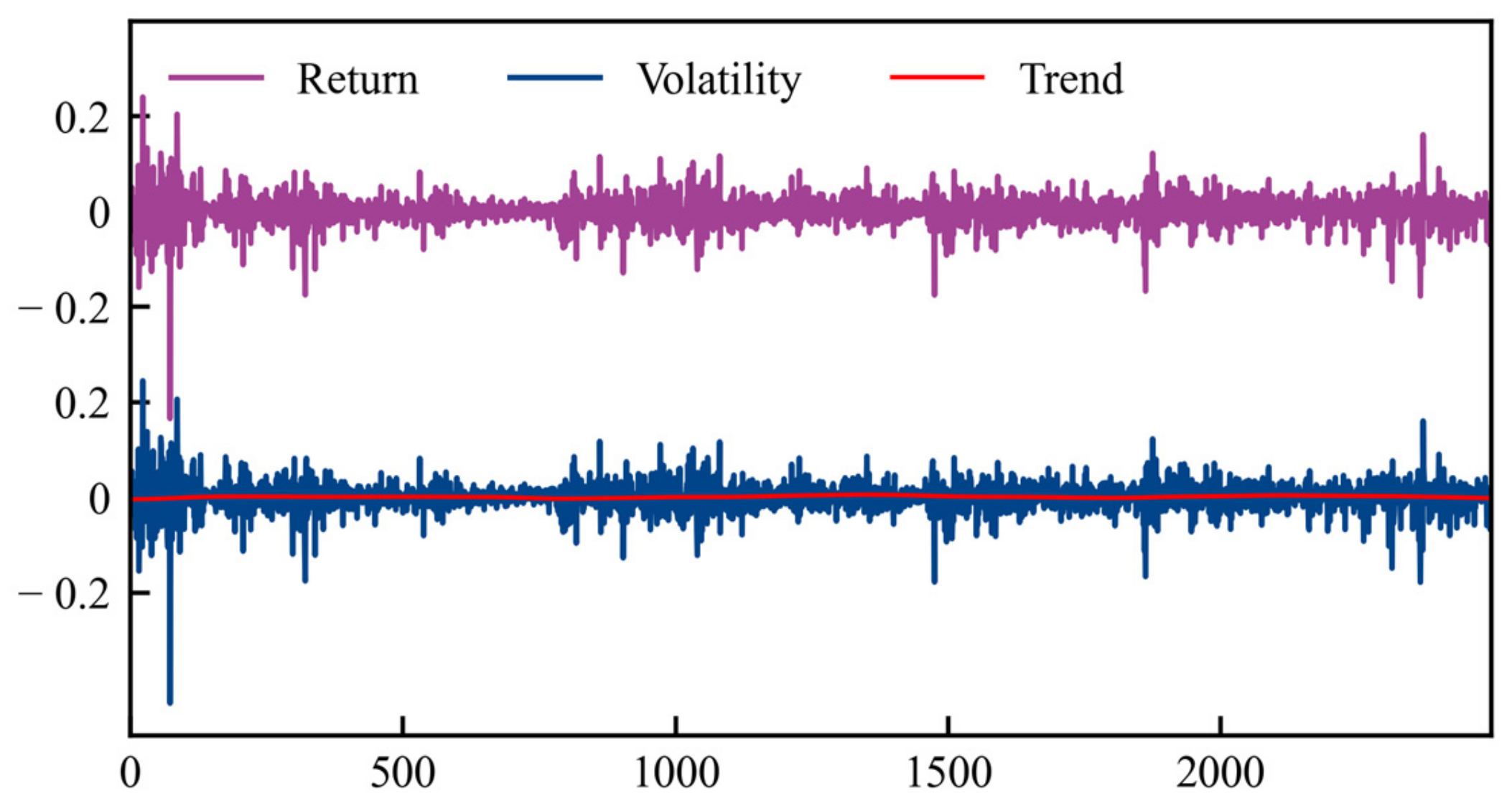

- This study employs the HP filter to decompose carbon price returns into trend and volatility components, with the volatility component being closely associated with the market risk. Analysis of the volatility component of carbon price returns without the trend component enhances the understanding of the changes and trends in carbon market risks, thus facilitating an accurate risk quantification. The HP filter effectively accomplishes filtering without data loss, mitigates interference from trend components, and enhances the precision of empirical results.

- (2)

- This study utilizes the EGARCH model, which overcomes the shortcomings of the GARCH model in capturing asymmetry in asset returns. Additionally, EVT is incorporated to effectively address the limitation of the EGARCH model in measuring extreme tail risks. EVT provides a comprehensive consideration of extreme situations, resulting in a precise risk measurement for the Chinese carbon market.

- (3)

- A comprehensive assessment and comparison of volatility and risks in eight carbon pilot markets in China and in the national carbon market are conducted. Furthermore, comparisons with a mature carbon market, namely EU-ETS, are performed. This research provides policy recommendations for the future healthy development of China’s carbon market.

2. Methodology

2.1. HP Filtering Method

2.2. EGARCH

2.3. EVT-VaR

- (1)

- EVT

- (2)

- POT model

- (3)

- Static VaR Model

- (4)

- Dynamic VaR (EGARCH-EVT-VaR)

2.4. Kupiec Failure Frequency Test

3. Data Preprocessing

3.1. Data Source

3.2. HP Filter Rejection Trend Processing

3.3. Stationarity and ARCH Effect Test

4. Empirical Analysis

4.1. Empirical Results on the Carbon Market in China

4.1.1. Parameter Estimation of the EGARCH Model

4.1.2. Static VaR Estimation Results

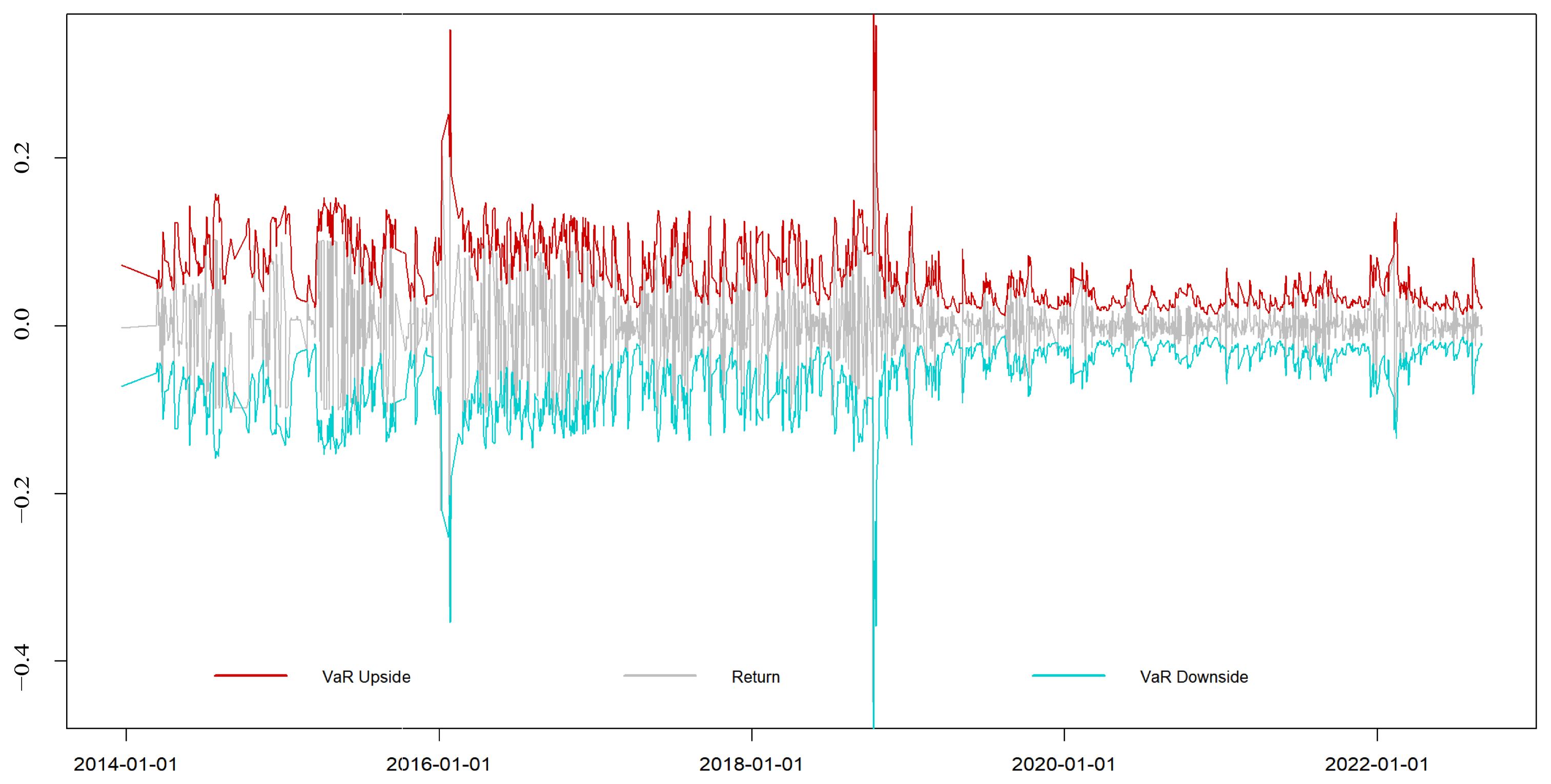

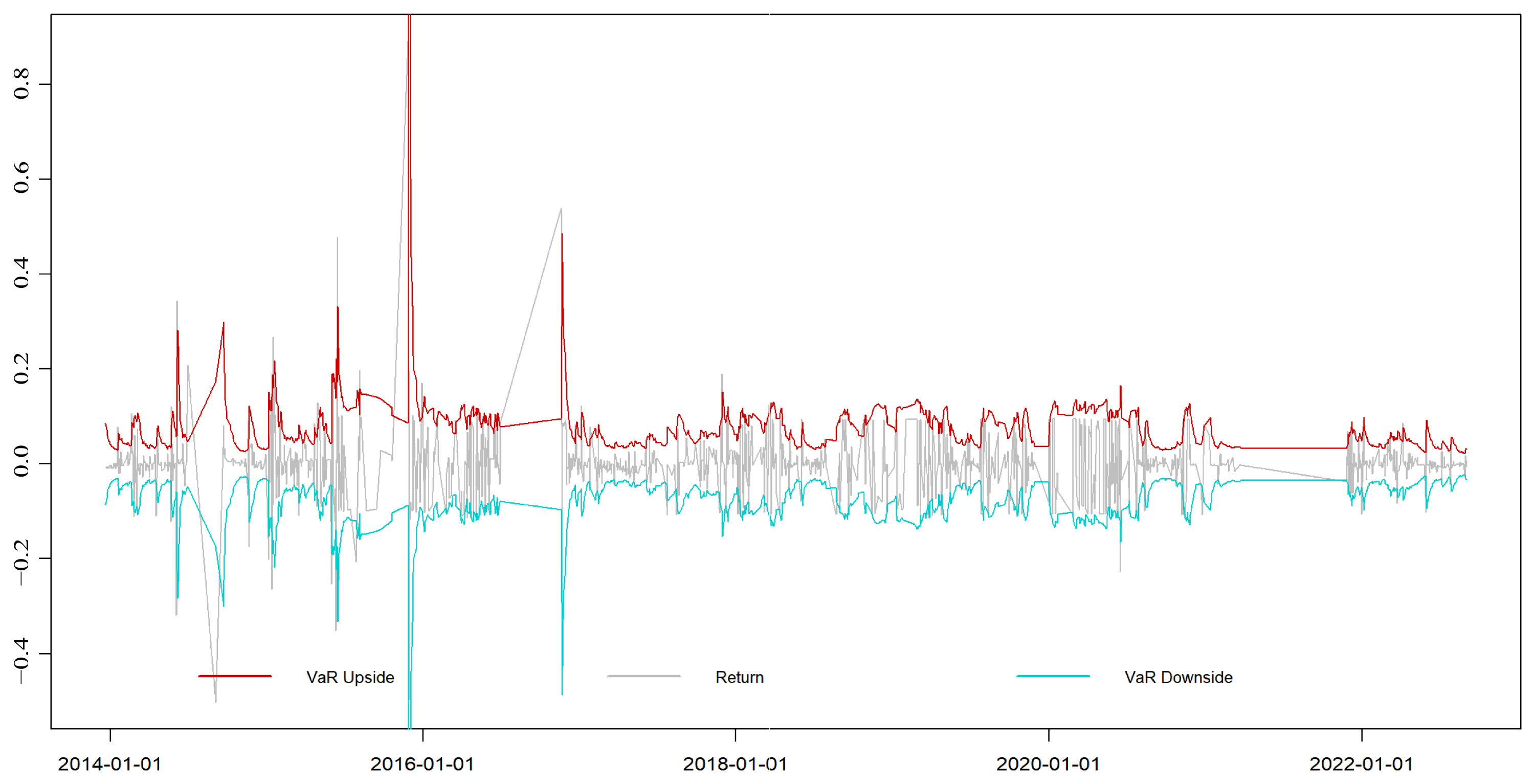

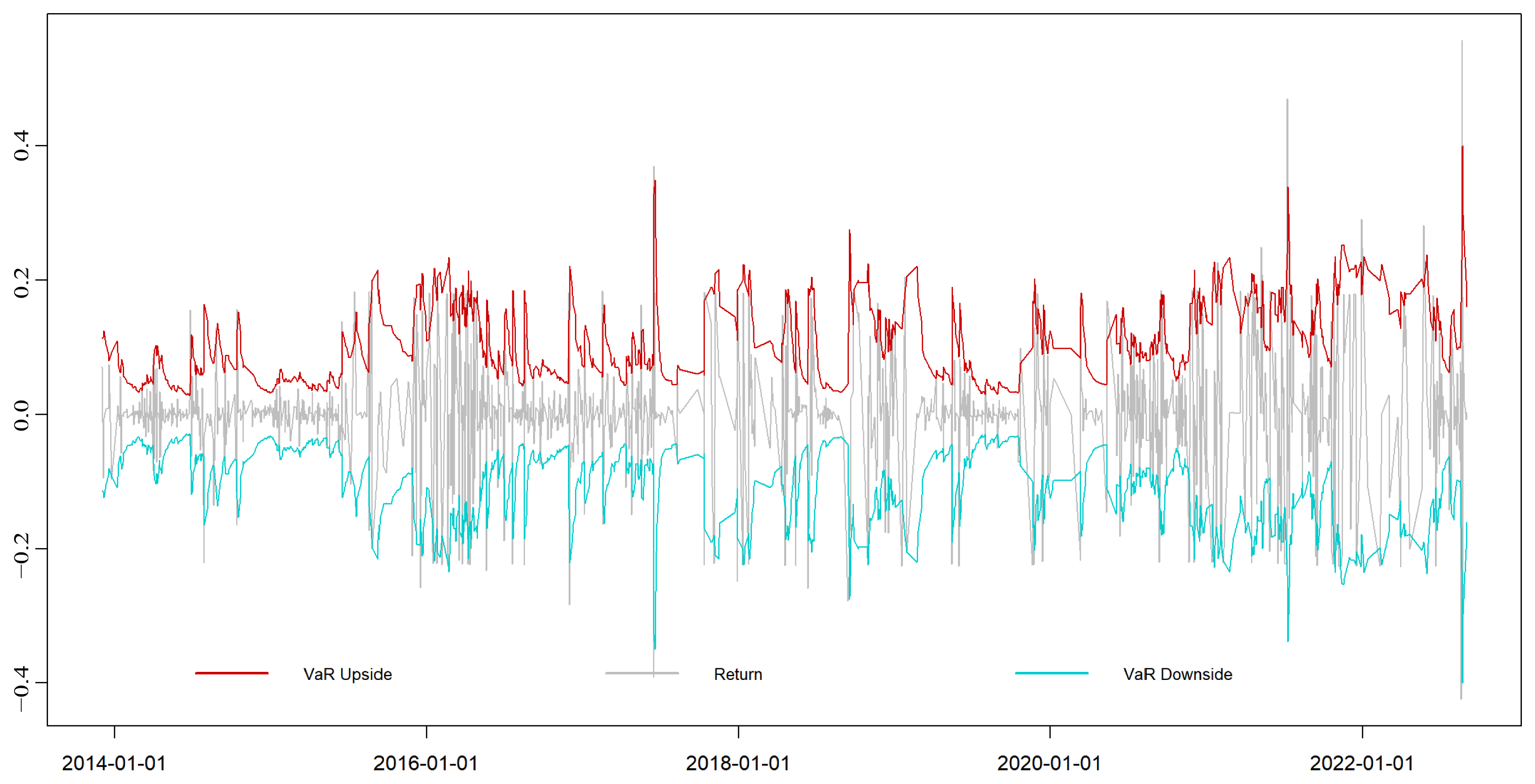

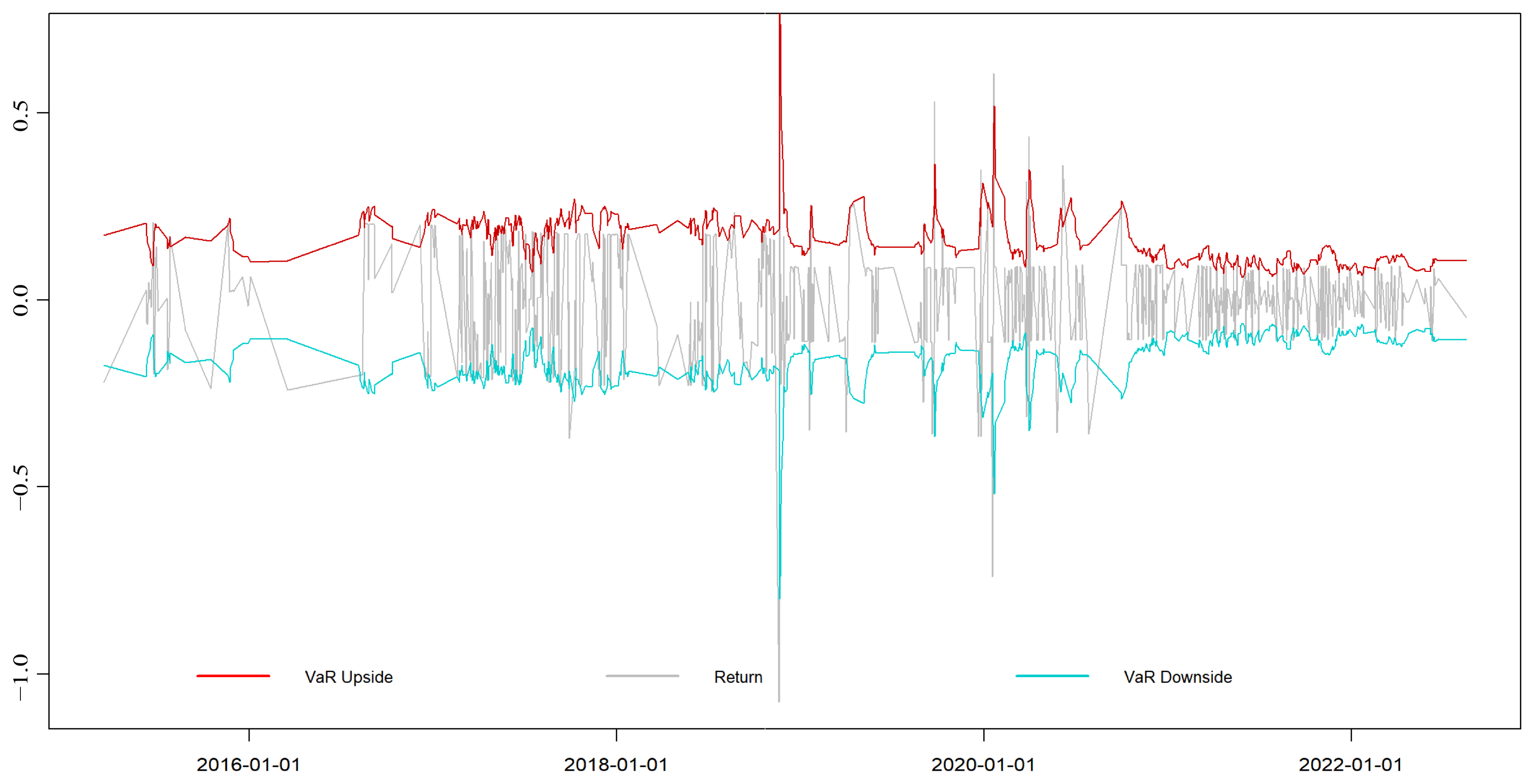

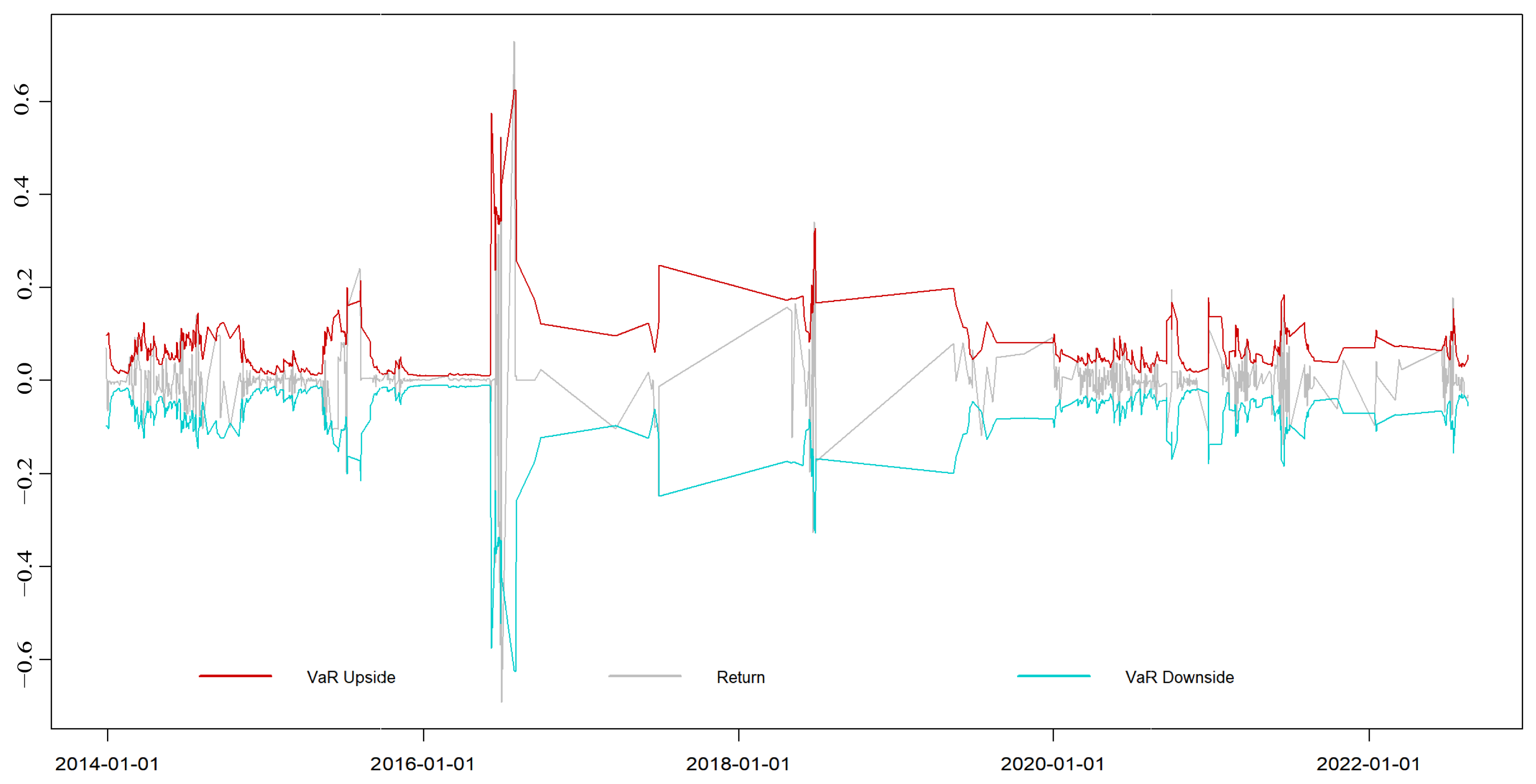

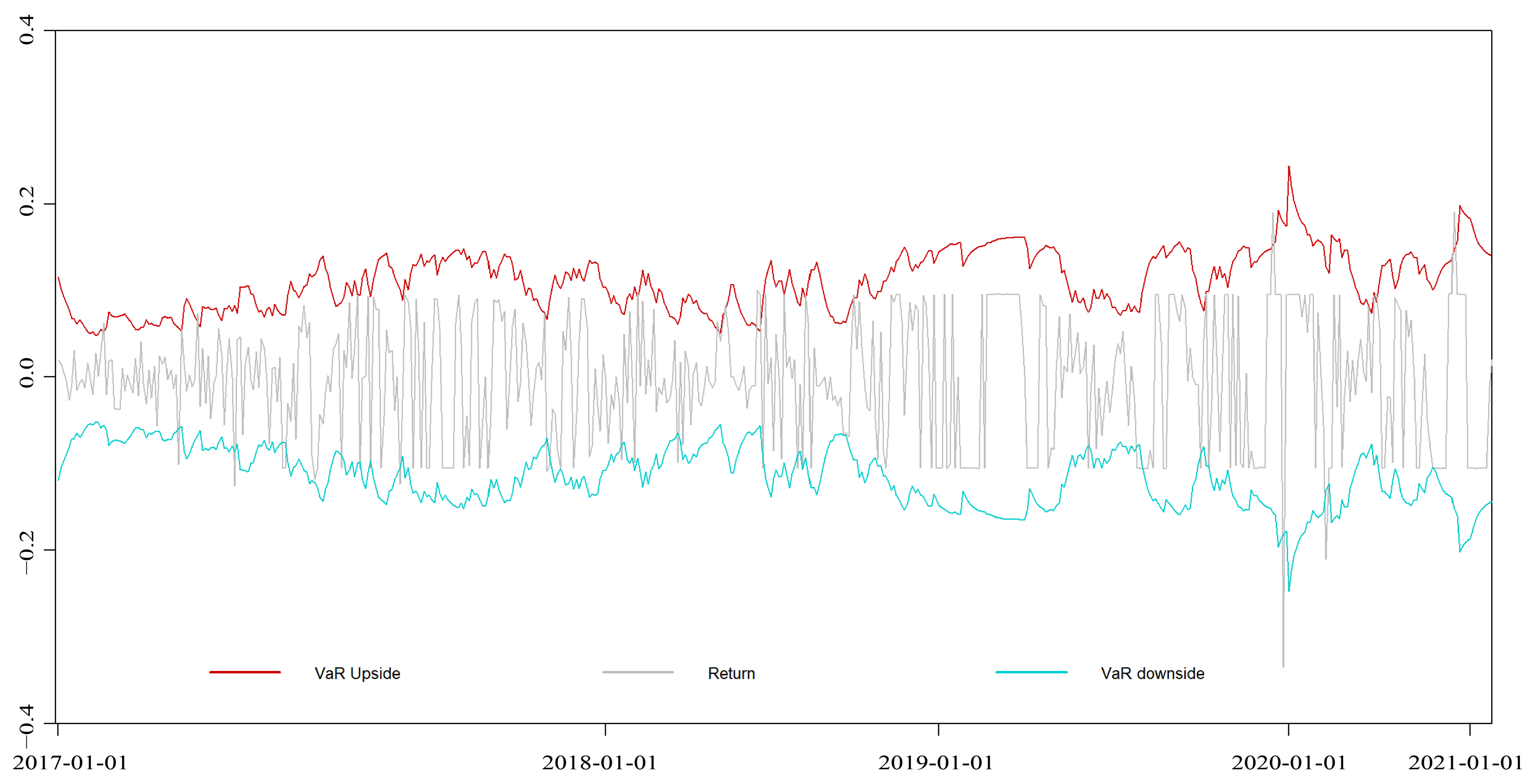

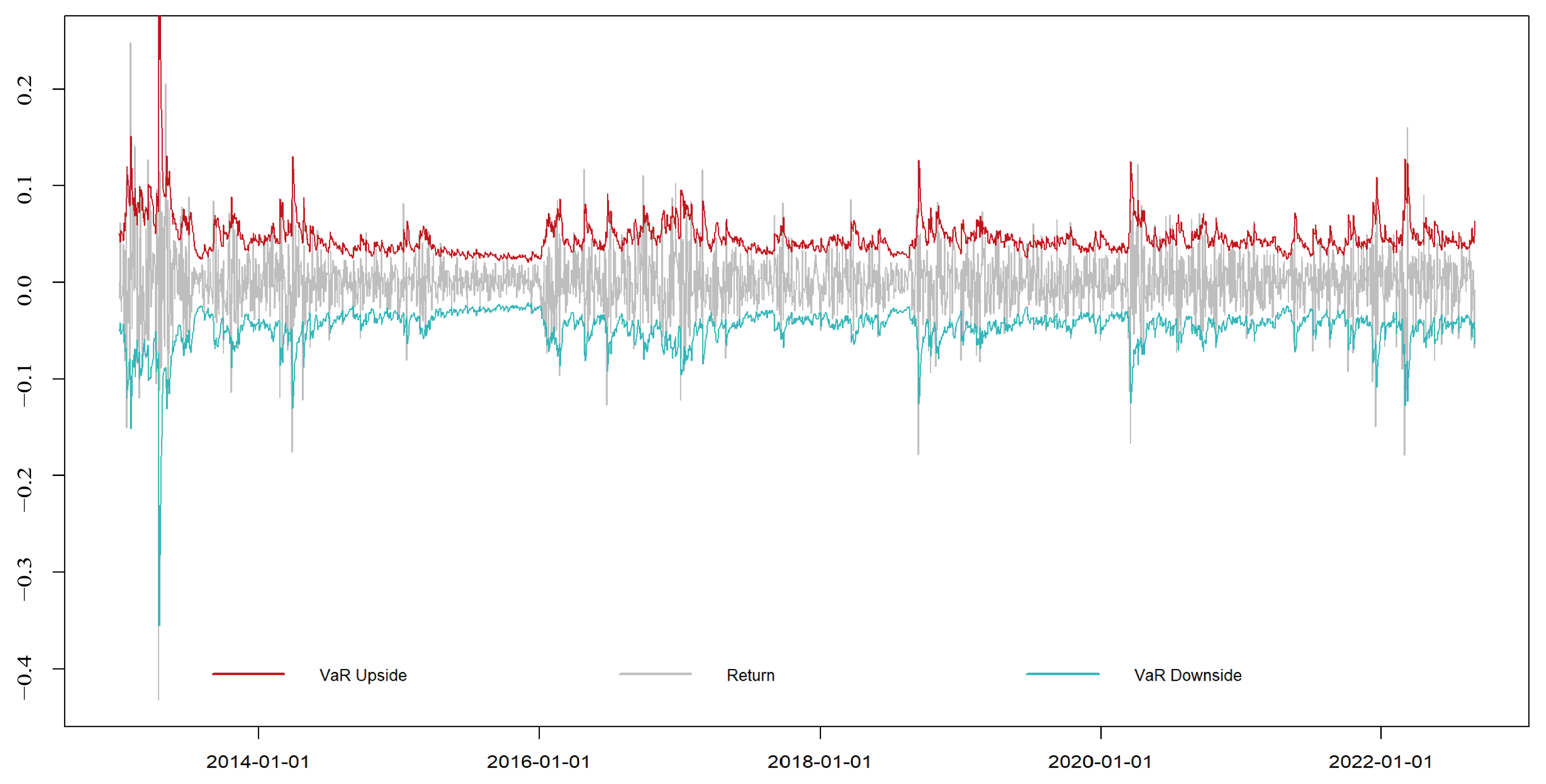

4.1.3. Dynamic VaR Estimation Results

- (1)

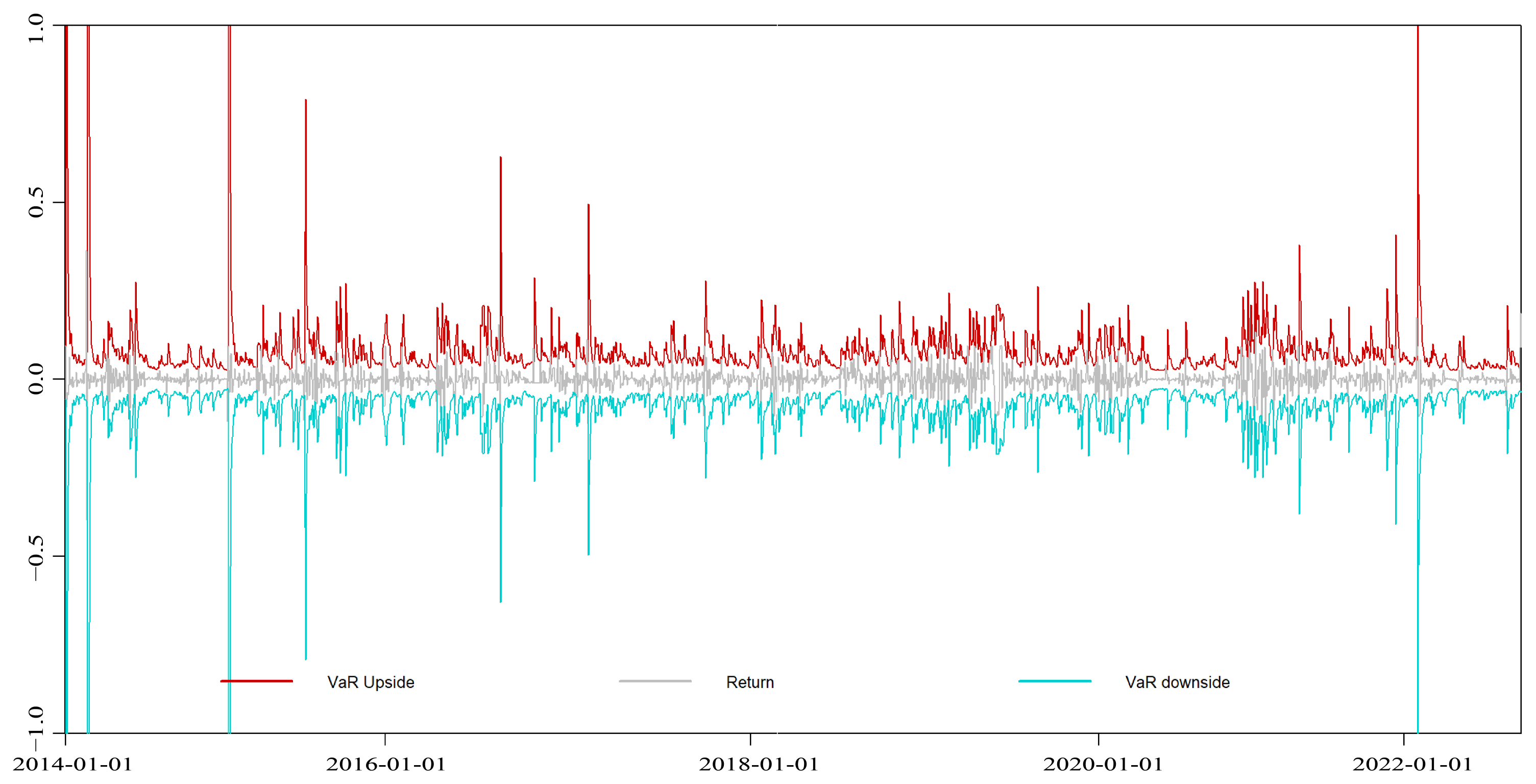

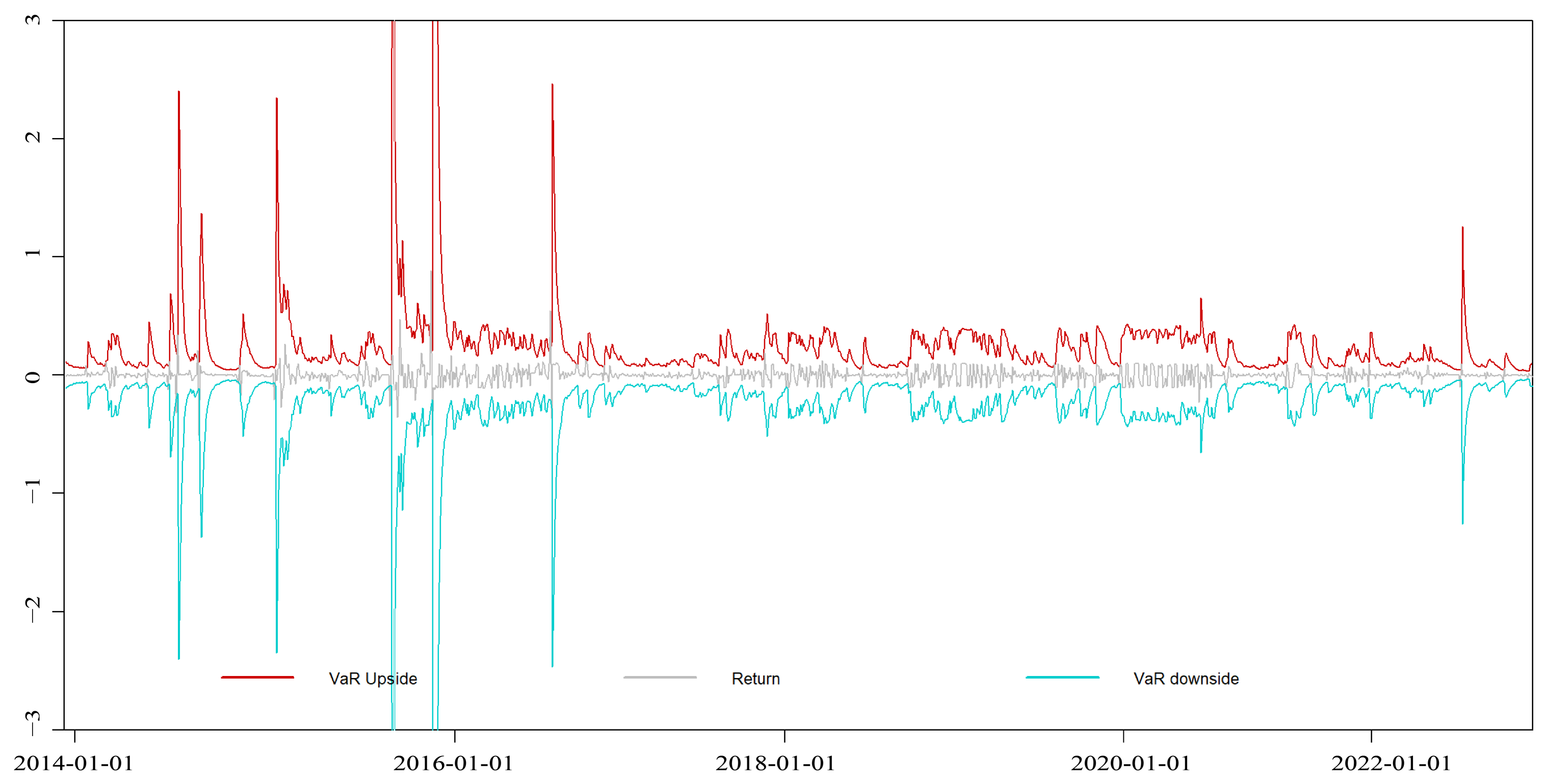

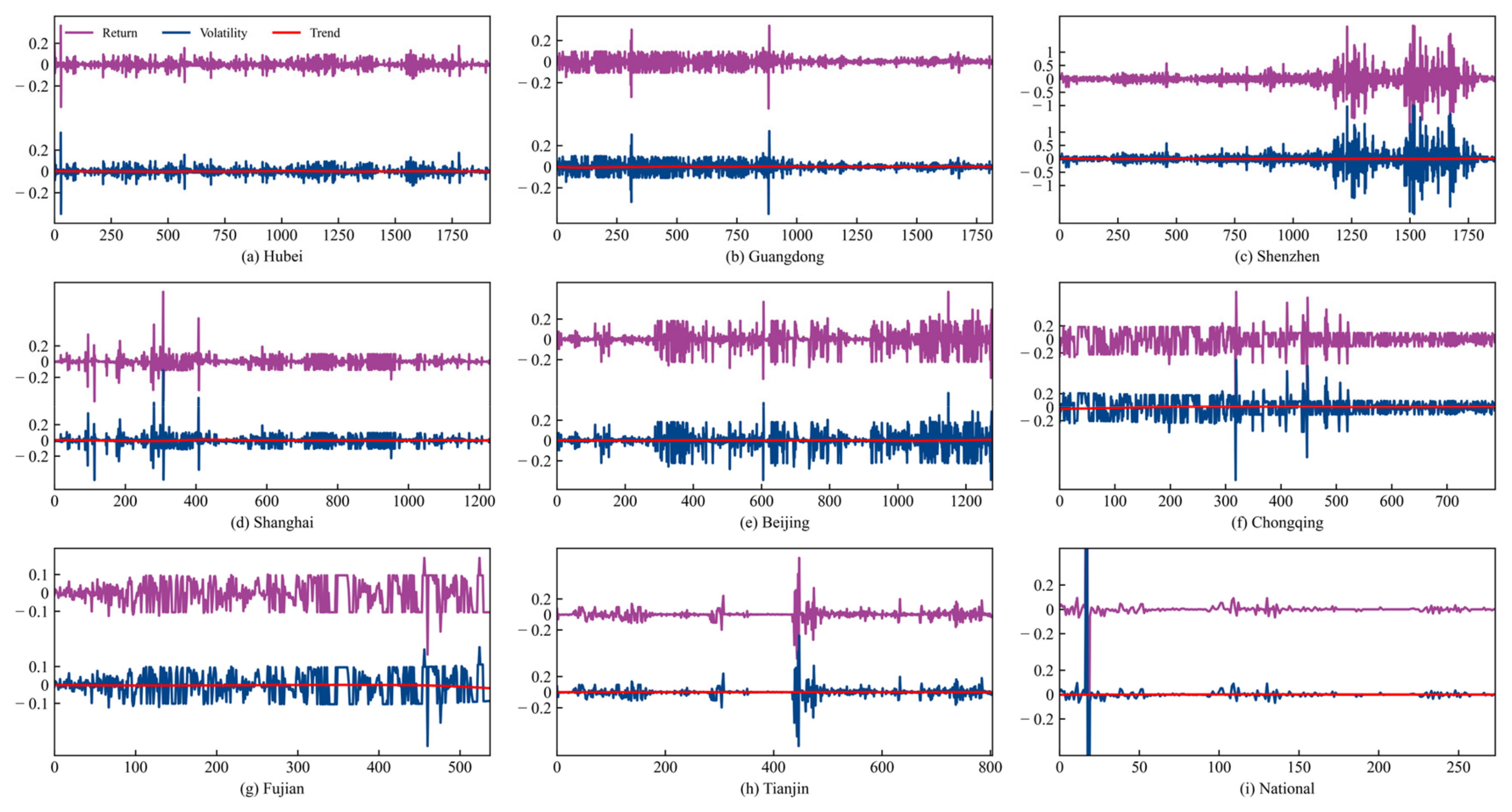

- Pilot carbon market development phase (2013–2016). The period from 2013 to 2016 marked the initial development phase of carbon markets in China. During this phase, the establishment of various pilot carbon markets elicited considerable attention, and policies related to carbon trading were gradually introduced. The risk profiles of carbon markets in Hubei, Guangdong, and Shenzhen remained stable during this stage primarily because of the effective risk management measures implemented in these regions. Although the risks in the Shanghai and Beijing markets remained stable and within a manageable range throughout this period, with no notable abnormal fluctuations, they exhibited higher levels of risk volatility compared with the risks in the Hubei, Guangdong, and Shenzhen carbon markets. By contrast, the carbon markets in Chongqing, Fujian, and Tianjin experienced overall substantial fluctuations and high market risks. VaR exhibited several abrupt changes, indicating unfavorable performance overall. In the case of the Fujian carbon market, which was at its nascent stage during this period, its available carbon price data were lacking, so its risk dynamics could not be examined. In summary, during the pilot carbon market development phase, variations in the geographical conditions and resource endowments of each carbon pilot market led to distinct characteristics in risk volatility, resulting in different evolution trends.

- (2)

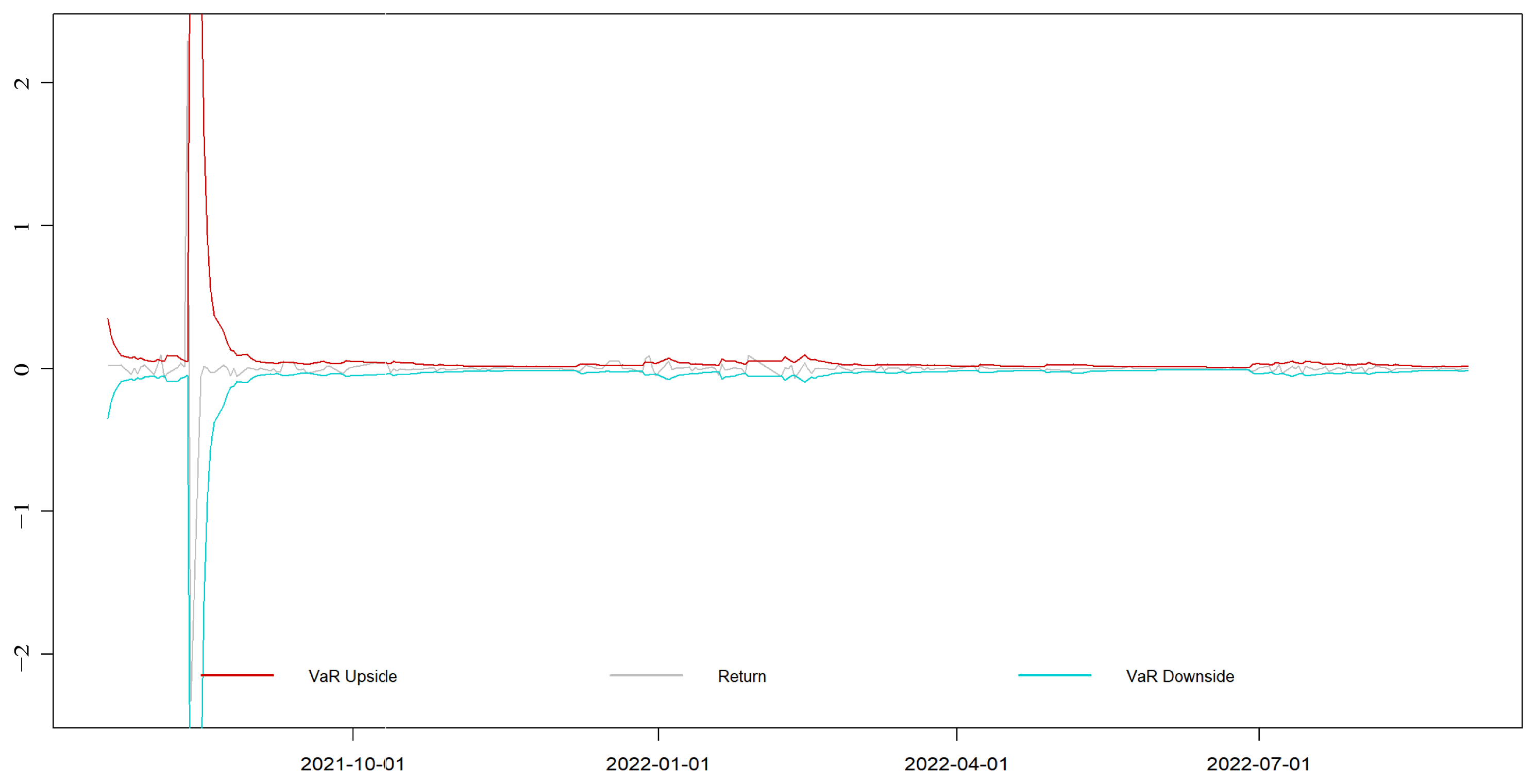

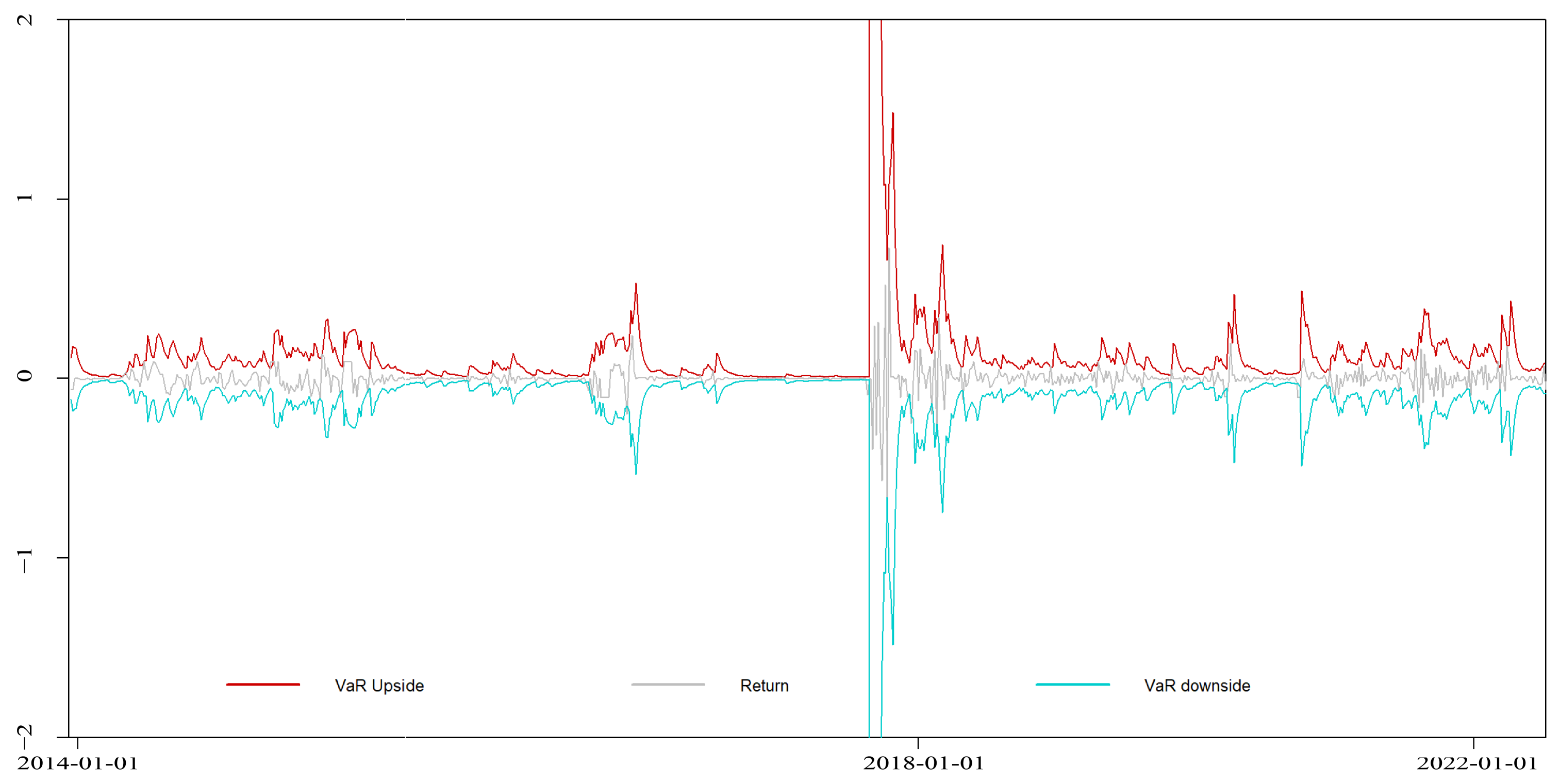

- National carbon market launch phase (2017–2020). China began the construction of a national carbon market at the end of 2017, and after nearly four years of pilot operation, it was officially launched in July 2021. During this phase, the risk profile of the Hubei carbon market continued to exhibit a stable development trend. VaR did not experience considerable fluctuations and remained stable. This stability can be attributed to Hubei’s industrial base and industrial structure, which ensure the vibrancy of carbon trading and price stability. The risk in the Guangdong carbon market, with the smallest carbon price fluctuations and the highest level of risk management, showed a gradual decline. The Shenzhen carbon market, which is currently the most remarkable carbon market in China, experienced intense volatility and abrupt changes in its dynamic VaR. The magnitude of risk variation was unprecedented, indicating the market’s sensitivity to policy changes. The establishment of the national carbon market considerably affected carbon trading in this region. The Shanghai carbon market did not exhibit substantial changes. Unlike risk volatility, dynamic VaR decreased and remained stable without considerable fluctuations. This finding suggests that the construction of the national carbon market has a positive effect on the Shanghai market. Although Beijing is not the primary carbon market in China, its unique location exposed it to the largest-ever market risk changes. The carbon markets in Chongqing, Fujian, and Tianjin, due to their limited trading volumes and low market activity, were minimally affected. From the perspective of risk changes in China’s pilot carbon markets, the establishment of the national carbon market had a direct effect on these pilot markets, and this influence is expected to persist for a long period. Therefore, facilitating the smooth transition of pilot carbon markets to the national carbon market is a challenge for China as it promotes long-term low-carbon economic development.

- (3)

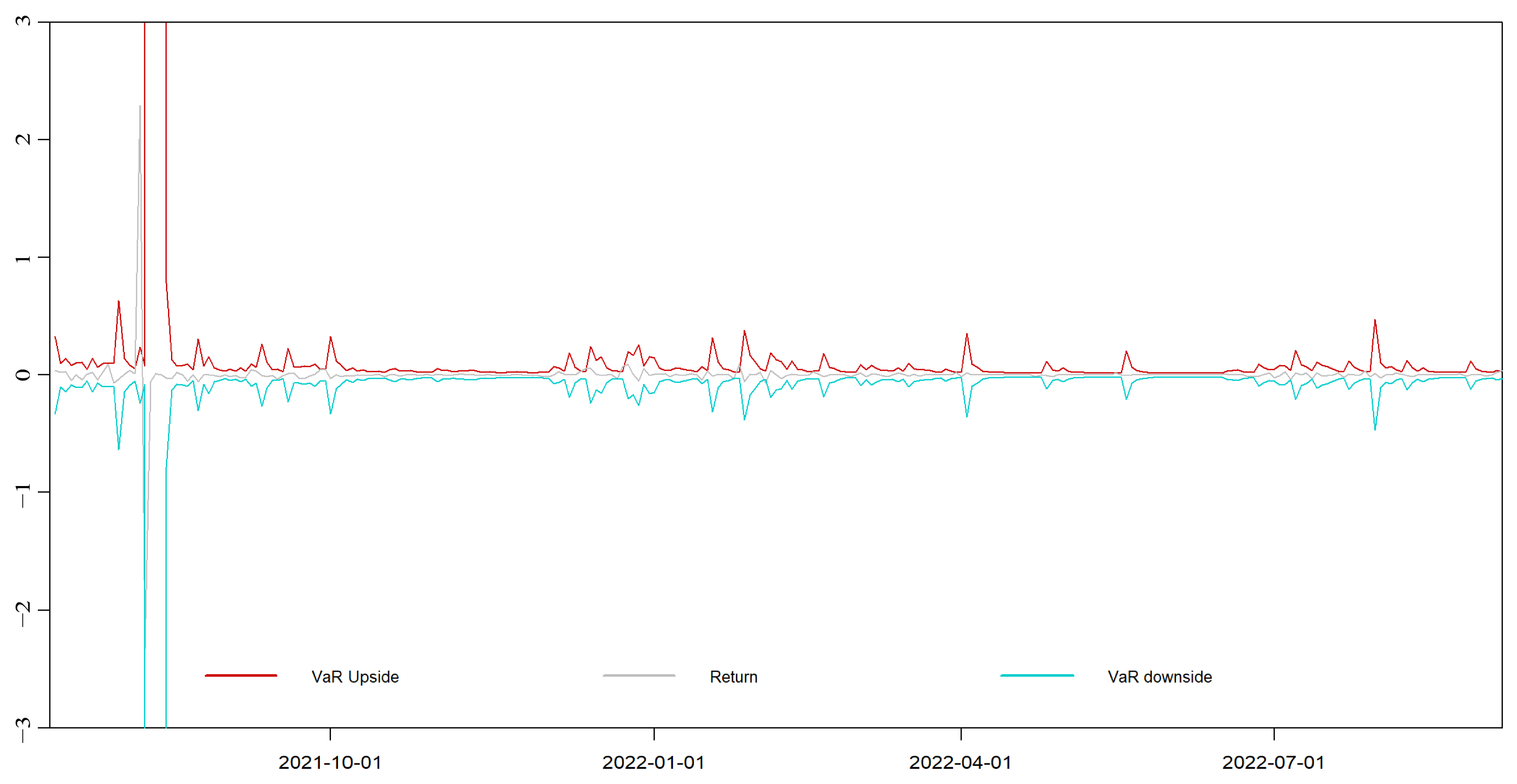

- National carbon market development phase (2021–present). During this phase, the carbon markets in the pilot regions of Hubei and Guangdong generally showed stable development trends. Their risk management levels were high, and the carbon markets operated well. By contrast, the Shenzhen carbon market had the highest degree of volatility and volatility intensity among all the pilot carbon markets, resulting in an overall higher risk. The Shanghai carbon market demonstrated stability. Its dynamic VaR gradually decreased, and volatility was gradually mitigated, with the market risk remaining within manageable limits. Beijing’s carbon market, due to its unique location and sensitivity to policy changes, experienced considerable risk fluctuations. Additionally, the economic environment underwent substantial changes due to the pandemic, which further affected the market. The combination of these factors led to a substantial increase in risk in the Beijing carbon market. The risk dynamics of Tianjin and Chongqing carbon markets improved slightly during this phase compared with the risk dynamics in the two previous phases; volatility was reduced, and no abrupt changes occurred. With regard to the Fujian carbon market, its risk dynamics after 13 January 2021, could not be analyzed due to the absence of carbon price data. The national carbon market experienced one notable fluctuation event at the beginning of trading, followed by an immediate reduction in volatility. Afterward, it maintained relatively minor fluctuations, demonstrating an overall stable trend.

4.1.4. Model Comparison

4.1.5. Results of the Kupiec Failure Frequency Test

4.2. Empirical Results of EU-ETS

5. Conclusions and Policy Implications

5.1. Conclusions

- (1)

- Analysis of the price volatility in the Chinese carbon markets showed that the data processed by HP filtering to remove the trend component retained the main volatility characteristics of the original data and improved the accuracy of the measurement results of the econometric models. When the EGARCH model was used to measure the asymmetry of volatility components, the results showed that for all the Chinese carbon markets, external shocks had an asymmetric effect, and a long-term memory effect, with a stronger reaction to positive shocks than to negative shocks, was observed. Carbon price returns exhibited a significant fat-tailed distribution. The carbon price returns of Hubei showed intense volatility, with one notable early volatility event, but overall, the market displayed a certain pattern. The carbon price returns of Guangdong showed a converging trend from large to small volatility components. The carbon markets in Chongqing and Fujian had the highest degree of volatility component variation because they had low trading volumes, discontinuous trading, and overall low activity, which led to multiple sharp declines. The national carbon market, established not long ago, had only one period with significant volatility in its early days, followed by a relatively stable period.

- (2)

- The EGARCH-EVT-VaR model was employed to quantitatively analyze the risks in various carbon markets in China. A comparison of its measurement results with those of the EGARCH-VaR model showed that the EGARCH-EVT dynamic VaR model, which is based on EVT, can better fit carbon market returns compared with standard dynamic VaR models. The EGARCH-EVT dynamic VaR model can effectively measure the risks in Chinese carbon markets. Consequently, using this model to assess the risks in Chinese carbon markets is effective. The empirical results showed that the risk profiles of different carbon markets in China varied considerably and had low correlations, and the overall risk fluctuations did not exhibit substantial commonality. Hubei and Guangdong carbon markets had the best risk control among all the carbon markets in China.

- (3)

- Compared with the EU-ETS carbon market, the Chinese carbon markets exhibited greater volatility and risk characteristics. According to the dynamic VaR results, the dynamic VaR values for EU-ETS were relatively stable, mostly ranging within ±0.2. By contrast, even in the stable Hubei and Guangdong carbon markets, the dynamic VaR values could fluctuate beyond ±0.2, and the most volatile Shenzhen carbon market experienced dramatic fluctuations in dynamic VaR values within the range of ±2. This result demonstrates regional disparities in the development of Chinese carbon markets.

5.2. Policy Implications

- (1)

- Strengthen the experience sharing of Hubei and Guangdong carbon markets: Hubei and Guangdong carbon markets are leading in terms of risk management. They can serve as a reference for other carbon markets. The government should continue to prioritize the development of these carbon markets, improve the trading mechanisms, enhance the transparency of information, establish efficient working mechanisms, ensure the scientific allocation of carbon quotas, and produce macroeconomic policies to boost participant confidence. Doing so will increase the enthusiasm of participants in carbon trading.

- (2)

- Establish a reasonable risk warning and prevention mechanism: According to the current empirical results, the risk levels of the various carbon markets in China are high. Upward and downward risks are not conducive to the healthy development of carbon markets. Upward risks may lead to speculative behavior by enterprises and may divert the market from its primary emission reduction objectives. Downward risks may result in economic losses for enterprises, and such losses may discourage participation in the carbon market.

- (3)

- Learn from mature carbon markets internationally: EU-ETS, after its development through Phases One, Two, and Three, has accumulated a wealth of experience in carbon market development and construction. Its carbon prices are currently stable and slowly rising, encouraging enterprises to reduce emissions. Therefore, China’s national carbon market and various pilot markets should summarize and learn from the favorable experiences, such as carbon quota allocation plans and stable market policies, derived from the development of EU-ETS.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix B

References

- IEA. CO2 Emissions in 2022; IEA: Paris, France, 2023. [Google Scholar]

- Li, X.; Hu, Z.; Cao, J. The Impact of Carbon Market Pilots on Air Pollution: Evidence from China. Environ. Sci. Pollut. Res. 2021, 28, 62274–62291. [Google Scholar] [CrossRef]

- Zhang, Y.-J.; Wei, Y.-M. An Overview of Current Research on EU ETS: Evidence from Its Operating Mechanism and Economic Effect. Appl. Energy 2010, 87, 1804–1814. [Google Scholar] [CrossRef]

- Liu, X.; Zhou, X.; Zhu, B.; Wang, P. Measuring the Efficiency of China’s Carbon Market: A Comparison between Efficient and Fractal Market Hypotheses. J. Clean. Prod. 2020, 271, 122885. [Google Scholar] [CrossRef]

- Liu, X.; Zhou, X.; Zhu, B.; He, K.; Wang, P. Measuring the Maturity of Carbon Market in China: An Entropy-Based TOPSIS Approach. J. Clean. Prod. 2019, 229, 94–103. [Google Scholar] [CrossRef]

- Zhang, S.; Ji, H.; Tian, M.; Wang, B. High-Dimensional Nonlinear Dependence and Risk Spillovers Analysis between China’s Carbon Market and Its Major Influence Factors. Ann. Oper. Res. 2022, 1–30. [Google Scholar] [CrossRef] [PubMed]

- Zhu, B.; Wang, P.; Chevallier, J.; Wei, Y. Carbon Price Analysis Using Empirical Mode Decomposition. Comput. Econ. 2015, 45, 195–206. [Google Scholar] [CrossRef]

- Lin, B.; Huang, C. Analysis of Emission Reduction Effects of Carbon Trading: Market Mechanism or Government Intervention? Sustain. Prod. Consum. 2022, 33, 28–37. [Google Scholar] [CrossRef]

- Zhang, J.; Xu, Y. Research on the Price Fluctuation and Risk Formation Mechanism of Carbon Emission Rights in China Based on a GARCH Model. Sustainability 2020, 12, 4249. [Google Scholar] [CrossRef]

- Yu, H.; Wang, H.; Liang, C.; Liu, Z.; Wang, S. Carbon Market Volatility Analysis Based on Structural Breaks: Evidence from EU-ETS and China. Front. Environ. Sci. 2022, 10, 973855. [Google Scholar] [CrossRef]

- Yang, X.; Zhang, C.; Yang, Y.; Wang, W.; Wagan, Z.A. A New Risk Measurement Method for China’s Carbon Market. Int. J. Financ. Econ. 2022, 27, 1280–1290. [Google Scholar] [CrossRef]

- Liu, J.; Jiang, T.; Ye, Z. Information Efficiency Research of China’s Carbon Markets. Financ. Res. Lett. 2021, 38, 101444. [Google Scholar] [CrossRef]

- Cong, R.; Lo, A.Y. Emission Trading and Carbon Market Performance in Shenzhen, China. Appl. Energy 2017, 193, 414–425. [Google Scholar] [CrossRef]

- Fu, Y.; Zheng, Z. Volatility Modeling and the Asymmetric Effect for China’s Carbon Trading Pilot Market. Phys. A Stat. Mech. Appl. 2020, 542, 123401. [Google Scholar] [CrossRef]

- Lyu, J.; Cao, M.; Wu, K.; Li, H. Price Volatility in the Carbon Market in China. J. Clean. Prod. 2020, 255, 120171. [Google Scholar] [CrossRef]

- Liu, J.; Huang, Y.; Chang, C.-P. Leverage Analysis of Carbon Market Price Fluctuation in China. J. Clean. Prod. 2020, 245, 118557. [Google Scholar] [CrossRef]

- Qin, Q.; Huang, Z.; Zhou, Z.; Chen, Y.; Zhao, W. Hodrick–Prescott Filter-Based Hybrid ARIMA–SLFNs Model with Residual Decomposition Scheme for Carbon Price Forecasting. Appl. Soft Comput. 2022, 119, 108560. [Google Scholar] [CrossRef]

- Utnik-Banaś, K.; Schwarz, T.; Szymanska, E.J.; Bartlewski, P.M.; Satoła, Ł. Scrutinizing Pork Price Volatility in the European Union over the Last Decade. Animals 2022, 12, 100. [Google Scholar] [CrossRef] [PubMed]

- Liu, N.-Y.; Wang, H.-J. Study on Price Fluctuation Characteristics of Xinjiang Jujube Based on HP Filtering Method. Xinjiang Agric. Sci. 2018, 55, 2320. [Google Scholar]

- Xiaoling, J.; Zhilu, S.; Xiande, L. Characteristics and Its Influencing Factors of Barley Price Fluctation in China. Zhongguo Nongye Ziyuan Yu Quhua 2018, 39, 23–30. [Google Scholar]

- Liu, F.; Shao, S.; Li, X.; Pan, N.; Qi, Y. Economic Policy Uncertainty, Jump Dynamics, and Oil Price Volatility. Energy Econ. 2023, 120, 106635. [Google Scholar] [CrossRef]

- Jiao, L.; Liao, Y.; Zhou, Q. Predicting Carbon Market Risk Using Information from Macroeconomic Fundamentals. Energy Econ. 2018, 73, 212–227. [Google Scholar] [CrossRef]

- Wang, L.; Tang, L.; Qiu, X.M.; Zhang, X.X.; Ma, R.H. The Risk Measurement of China’s Carbon Financial Market: Based on Garch and Var Model. Appl. Ecol. Environ. Res. 2019, 17, 9301–9315. [Google Scholar] [CrossRef]

- Chai, S.L.; Zhou, P. Measuring the Integrated Risk of Carbon Financial Market by a Non-Parametric Copula-CvaR Model. Chin. J. Manag. Sci. 2019, 27, 1–13. [Google Scholar]

- Zhu, B.; Ye, S.; He, K.; Chevallier, J.; Xie, R. Measuring the Risk of European Carbon Market: An Empirical Mode Decomposition-Based Value at Risk Approach. Ann. Oper. Res. 2019, 281, 373–395. [Google Scholar] [CrossRef]

- Zhu, B.; Zhou, X.; Liu, X.; Wang, H.; He, K.; Wang, P. Exploring the Risk Spillover Effects among China’s Pilot Carbon Markets: A Regular Vine Copula-CoES Approach. J. Clean. Prod. 2020, 242, 118455. [Google Scholar] [CrossRef]

- Sheng, C.; Zhang, D.; Wang, G.; Huang, Y. Research on Risk Mechanism of China’s Carbon Financial Market Development from the Perspective of Ecological Civilization. J. Comput. Appl. Math. 2021, 381, 112990. [Google Scholar] [CrossRef]

- Fang, S.; Cao, G. Modelling Extreme Risks for Carbon Emission Allowances—Evidence from European and Chinese Carbon Markets. J. Clean. Prod. 2021, 316, 128023. [Google Scholar] [CrossRef]

- Geng, W.; Zhao, X.; Zhou, X. Research on Extreme Risk Measurement in the International Carbon Emission Futures Market, Based on a Two-Component Beta-Skew-t-EGARCH-POT Model. Appl. Econ. 2022, 55, 4194–4203. [Google Scholar] [CrossRef]

- Liu, J.; Man, Y.; Dong, X. Tail Dependence and Risk Spillover Effects between China’s Carbon Market and Energy Markets. Int. Rev. Econ. Financ. 2023, 84, 553–567. [Google Scholar] [CrossRef]

- Madhusudan, K.; Samit, P. Downside Risk and Portfolio Optimization of Energy Stocks: A Study on the Extreme Value Theory and the Vine Copula Approach. Energy J. 2023, 44, 139–179. [Google Scholar] [CrossRef]

- Feng, Z.-H.; Wei, Y.-M.; Wang, K. Estimating Risk for the Carbon Market via Extreme Value Theory: An Empirical Analysis of the EU ETS. Appl. Energy 2012, 99, 97–108. [Google Scholar] [CrossRef]

- Jingjing, J.; Bin, Y.E.; Xiaoming, M.A. Value-at-Risk Estimation of Carbon Spot Markets Based on an Integrated GARCH-EVT-VaR Model. Acta Sci. Nat. Univ. Pekin. 2015, 51, 511. [Google Scholar]

- Wang, X.; Yan, L. Measuring the Integrated Risk of China’s Carbon Financial Market Based on the Copula Model. Environ. Sci. Pollut. Res. 2022, 29, 54108–54121. [Google Scholar] [CrossRef]

- Zhao, J.; Cui, L.; Liu, W.; Zhang, Q. Extreme Risk Spillover Effects of International Oil Prices on the Chinese Stock Market: A GARCH-EVT-Copula-CoVaR Approach. Resour. Policy 2023, 86, 104142. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econom. J. Econom. Soc. 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Hosking, J.R.; Wallis, J.R. Parameter and Quantile Estimation for the Generalized Pareto Distribution. Technometrics 1987, 29, 339–349. [Google Scholar] [CrossRef]

- Jorion, P. Value at Risk: The New Benchmark for Managing Financial Risk; The McGraw-Hill Companies, Inc.: New York, NY, USA, 2007. [Google Scholar]

- Kupiec, P.H. Techniques for Verifying the Accuracy of Risk Measurement Models. J. Deriv. 1995, 95, 73–84. [Google Scholar] [CrossRef]

- Xu, J.; Tan, X.; He, G.; Liu, Y. Disentangling the Drivers of Carbon Prices in China’s ETS Pilots—An EEMD Approach. Technol. Forecast. Soc. Chang. 2019, 139, 1–9. [Google Scholar] [CrossRef]

- Lamphiere, M.; Blackledge, J.; Kearney, D. Carbon Futures Trading and Short-Term Price Prediction: An Analysis Using the Fractal Market Hypothesis and Evolutionary Computing. Mathematics 2021, 9, 1005. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Carbon Trading Market | Sample Size | Mean | Standard Deviation | Skewness | Kurtosis | J-B Test |

|---|---|---|---|---|---|---|

| Hubei | 1917 | 0.0000 | 0.0336 | −0.1544 | 23.0059 | 31,976.54 (0.0000) |

| Guangdong | 1816 | 0.0000 | 0.0456 | −0.5078 | 12.9327 | 7543.151 (0.0000) |

| Shenzhen | 1865 | 0.0000 | 0.2777 | −0.0435 | 19.1561 | 20,284.05 (0.0000) |

| Shanghai | 1230 | 0.0000 | 0.0683 | 1.5487 | 37.6493 | 62,021.13 (0.0000) |

| Beijing | 1278 | 0.0000 | 0.0870 | −0.3684 | 5.8054 | 448.0050 (0.0000) |

| Chongqing | 787 | 0.0000 | 0.1398 | −0.6181 | 8.8495 | 1172.118 (0.0000) |

| Fujian | 537 | 0.0000 | 0.0717 | −0.2503 | 2.7632 | 6.8604 (0.0000) |

| Tianjin | 804 | 0.0003 | 0.0698 | −0.1752 | 42.0751 | 51,153.90 (0.0000) |

| China | 276 | 0.0000 | 0.1995 | −0.2399 | 133.6022 | 194,025.3 (0.0000) |

| Carbon Markets | Test Statistic | 1% | 5% | 10% | Probability | Conclusion |

|---|---|---|---|---|---|---|

| Hubei | −51.8254 | −3.9628 | −3.4122 | −3.1280 | 0.0000 | stable |

| Guangdong | −44.6094 | −3.9631 | −3.4123 | −3.1281 | 0.0000 | stable |

| Shenzhen | −28.9288 | −3.9629 | −3.4122 | −3.1280 | 0.0000 | stable |

| Shanghai | −20.7942 | −3.9656 | −3.4125 | −3.1288 | 0.0000 | stable |

| Beijing | −29.1092 | −3.9652 | −3.4133 | −3.1287 | 0.0000 | stable |

| Chongqing | −13.1804 | −3.9698 | −3.4156 | −3.1300 | 0.0000 | stable |

| Fujian | −17.4629 | −3.9753 | −3.4182 | −3.1316 | 0.0000 | stable |

| Tianjin | −37.7743 | −3.4383 | −2.8649 | −2.5686 | 0.0000 | stable |

| China | −12.3683 | −3.9927 | −3.4267 | −3.13659 | 0.0000 | stable |

| Carbon Markets | F-Statistic | Prob. F | Obs∗R-Squared | Prob. Chi-Square |

|---|---|---|---|---|

| Hubei | 531.0208 | 0.0000 | 416.1256 | 0.0000 |

| Guangdong | 103.5125 | 0.0000 | 98.0297 | 0.0000 |

| Shenzhen | 438.5068 | 0.0000 | 355.3029 | 0.0000 |

| Shanghai | 95.5243 | 0.0000 | 88.7691 | 0.0000 |

| Beijing | 375.3255 | 0.0000 | 290.5247 | 0.0000 |

| Chongqing | 115.7247 | 0.0000 | 101.0971 | 0.0000 |

| Fujian | 39.9024 | 0.0000 | 37.2671 | 0.0000 |

| Tianjin | 155.8933 | 0.0000 | 434.3331 | 0.0000 |

| China | 282.3283 | 0.0000 | 67.0057 | 0.0000 |

| Parameters | Hubei | Guangdong | Shenzhen | Shanghai | Beijing | Chongqing | Fujian | Tianjin | China |

|---|---|---|---|---|---|---|---|---|---|

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| (1.0000) | (1.0000) | (1.0000) | (1.0000) | (1.0000) | (1.0000) | (1.0000) | (1.0000) | (1.0000) | |

| −0.6540 | −0.6356 | −0.2676 | −0.4851 | −0.4515 | −0.3778 | −0.5570 | −0.5915 | −0.8010 | |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0317) | (0.0276) | (0.0000) | (0.0000) | |

| 0.0401 | 0.0575 | −0.0053 | 0.0400 | −0.0018 | 0.0081 | 0.0298 | −0.0679 | −0.2988 | |

| (0.0273) | (0.0256) | (0.8792) | (0.1258) | (0.9500) | (0.7920) | (0.4136) | (0.0900) | (0.0000) | |

| 0.8993 | 0.9010 | 0.9078 | 0.9000 | 0.9001 | 0.9116 | 0.8996 | 0.9000 | 0.9002 | |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| 0.3557 | 0.6467 | 0.6826 | 0.4729 | 0.4781 | 0.4734 | 0.3633 | 0.6589 | 0.4055 | |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| AIC | −4.2426 | −4.0468 | −0.8570 | −3.0355 | −2.5120 | −1.3515 | −2.5970 | −4.0620 | −5.1516 |

| BIC | −4.2281 | −4.0316 | −0.85702 | −3.0147 | −2.4919 | −1.3219 | −2.5571 | −4.0329 | −5.0861 |

| L-K | 4077.89 | 3683.52 | 804.17 | 1876.37 | 1614.00 | 537.50 | 702.30 | 1637.94 | 715.93 |

| Carbon Markets | |||

|---|---|---|---|

| Hubei | 0.6322 | 0.2577 | 1.5957 |

| Guangdong | 0.6962 | 0.1844 | 1.5228 |

| Shenzhen | 0.4648 | 0.3752 | 1.3453 |

| Shanghai | 0.3607 | 0.4619 | 1.0536 |

| Beijing | 0.3760 | 0.2595 | 1.0996 |

| Chongqing | 0.2062 | 0.3468 | 1.0201 |

| Fujian | 0.2956 | 0.0490 | 0.9753 |

| Tianjin | 0.6431 | −0.1889 | 0.8544 |

| China | 0.4567 | 0.6023 | 0.0294 |

| Carbon Markets | Averages | Max. | Min. | Standard Deviation | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

| Hubei | 0.0506 | 0.5744 | 0.0198 | 0.0261 | 7.9355 | 129.0302 |

| Guangdong | 0.0613 | 0.5183 | 0.0118 | 0.0403 | 2.2107 | 13.5942 |

| Shenzhen | 0.2851 | 3.7000 | 0.0445 | 0.2831 | 4.0066 | 25.7141 |

| Shanghai | 0.0786 | 1.9655 | 0.0222 | 0.0826 | 13.6247 | 266.6291 |

| Beijing | 0.1024 | 0.3997 | 0.0285 | 0.0579 | 1.0232 | 1.1268 |

| Chongqing | 0.1636 | 0.7989 | 0.0617 | 0.0672 | 2.6965 | 18.6657 |

| Fujian | 0.0916 | 0.2305 | 0.0414 | 0.0273 | 0.5495 | 0.5331 |

| Tianjin | 0.0618 | 0.6258 | 0.0098 | 0.0653 | 4.1686 | 25.3294 |

| China | 0.0608 | 2.9391 | 0.0074 | 0.2479 | 9.5951 | 98.1866 |

| Carbon Markets | Confidence Level | LR Test Statistic | p | Test Results |

|---|---|---|---|---|

| Hubei | 95% | 0.0109 | 0.9167 | accept |

| Guangdong | 0.0984 | 0.7538 | accept | |

| Shenzhen | 0.0177 | 0.8941 | accept | |

| Shanghai | 0.0072 | 0.9322 | accept | |

| Beijing | 0.0147 | 0.9032 | accept | |

| Chongqing | 0.1569 | 0.1570 | accept | |

| Fujian | 2.0102 | 0.1562 | accept | |

| Tianjin | 0.7390 | 0.3900 | accept | |

| China | 0.1070 | 0.7437 | accept |

| Carbon Markets | Averages | Standard Deviation | Skewness | Kurtosis | JB Test | ADF Test |

|---|---|---|---|---|---|---|

| EU-ETS | 0.0000 | 0.0325 | −0.9762 | 20.1146 | 30,859.17 | −38.0693 |

| (0.0000) | (0.0000) |

| Carbon Markets | F-Statistic | Prob. F | Obs∗R-Squared | Prob. Chi-Square |

|---|---|---|---|---|

| EU-ETS | 33.2769 | 0.0000 | 32.8647 | 0.0000 |

| Parameters | AIC | BIC | |||||

|---|---|---|---|---|---|---|---|

| EU-ETS | 0.000 (0.0000) | −0.6443 (0.0000) | −0.0290 (0.0000) | 0.9066 (0.0000) | 0.3544 (0.0000) | 4.2996 | −4.2879 |

| Carbon Markets | |||

|---|---|---|---|

| EU-ETS | 0.5733 | 0.0208 | 1.6838 |

| Carbon Markets | Averages | Max. | Min. | Standard Deviation | LR Value | p |

|---|---|---|---|---|---|---|

| EU-ETS | 0.0462 | 0.3555 | 0.0210 | 0.0183 | 0.0643 | 0.7999 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Duan, Y.; He, C.; Yao, L.; Wang, Y.; Tang, N.; Wang, Z. Research on Risk Measurement of China’s Carbon Trading Market. Energies 2023, 16, 7879. https://doi.org/10.3390/en16237879

Duan Y, He C, Yao L, Wang Y, Tang N, Wang Z. Research on Risk Measurement of China’s Carbon Trading Market. Energies. 2023; 16(23):7879. https://doi.org/10.3390/en16237879

Chicago/Turabian StyleDuan, Yanzhi, Chunlei He, Li Yao, Yue Wang, Nan Tang, and Zhong Wang. 2023. "Research on Risk Measurement of China’s Carbon Trading Market" Energies 16, no. 23: 7879. https://doi.org/10.3390/en16237879

APA StyleDuan, Y., He, C., Yao, L., Wang, Y., Tang, N., & Wang, Z. (2023). Research on Risk Measurement of China’s Carbon Trading Market. Energies, 16(23), 7879. https://doi.org/10.3390/en16237879