Integrating System and Operator Perspectives for the Evaluation of Power-to-Gas Plants in the Future German Energy System

, , , ,

, , , ,

Abstract

:1. Introduction

1.1. Background

1.2. State of Research

1.3. Contribution of This Paper

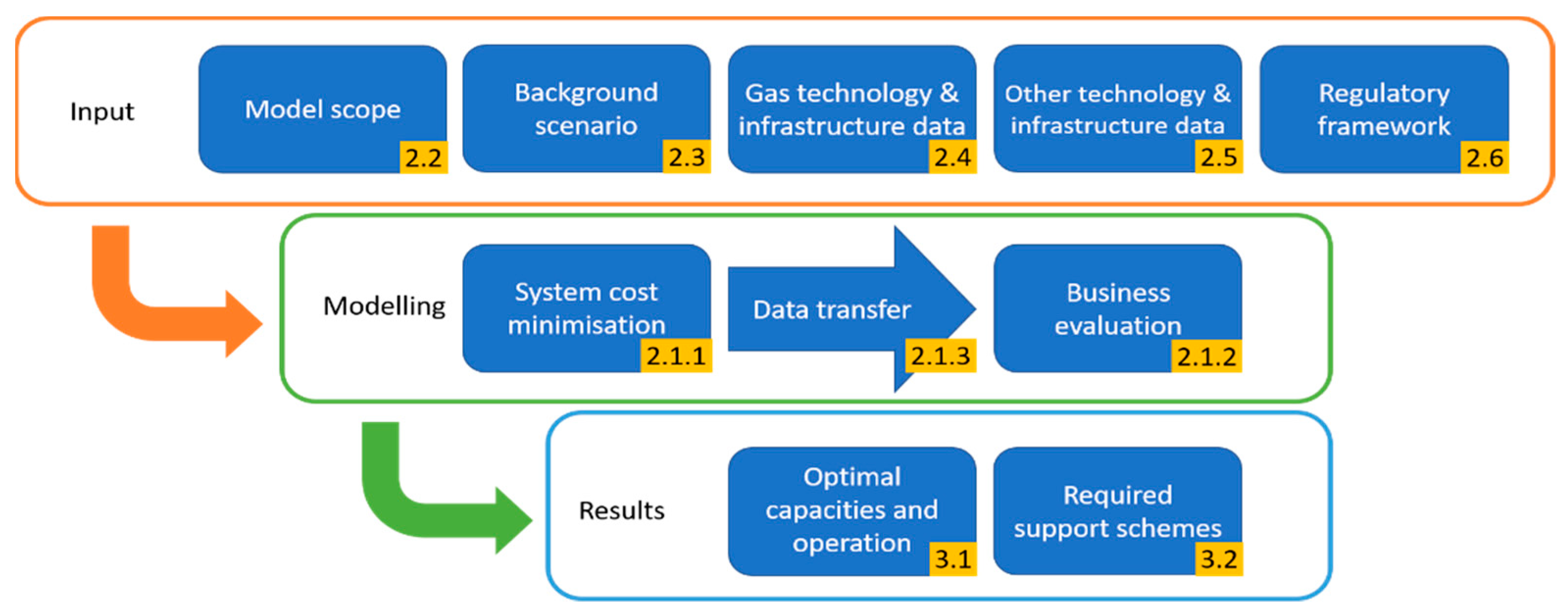

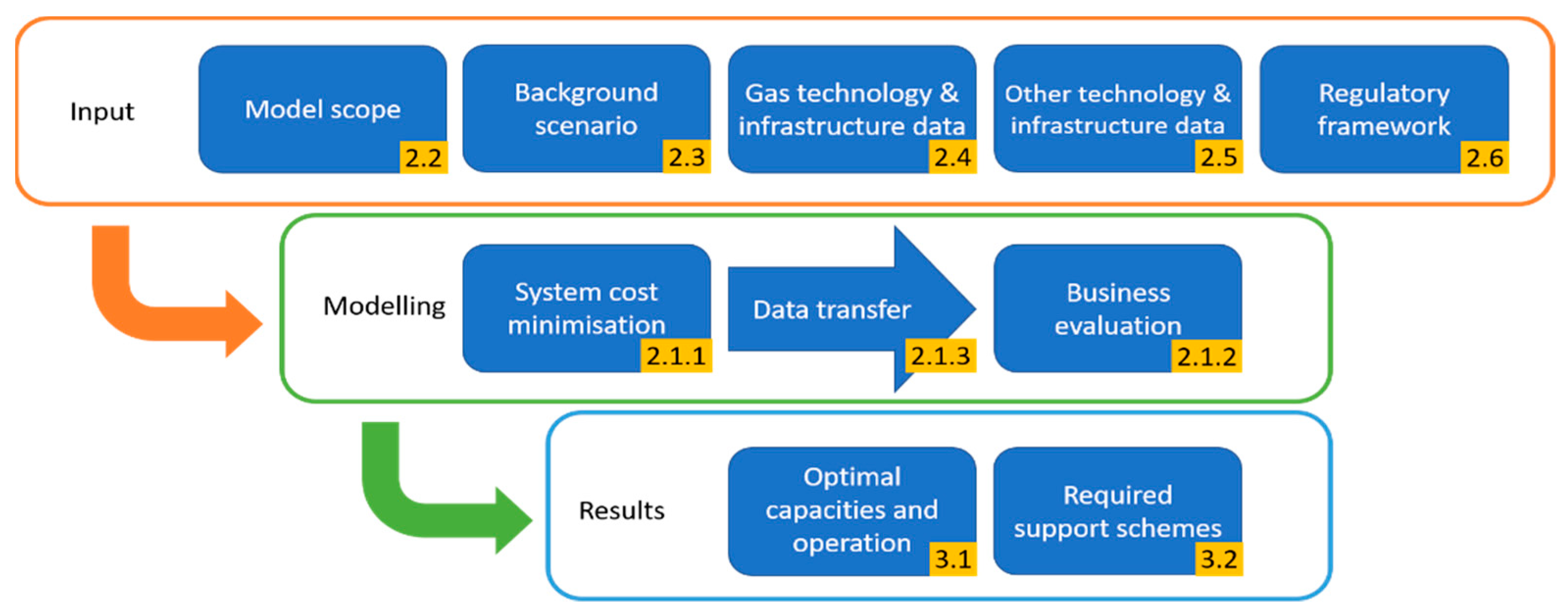

2. Materials and Methods

2.1. Modelling Approach

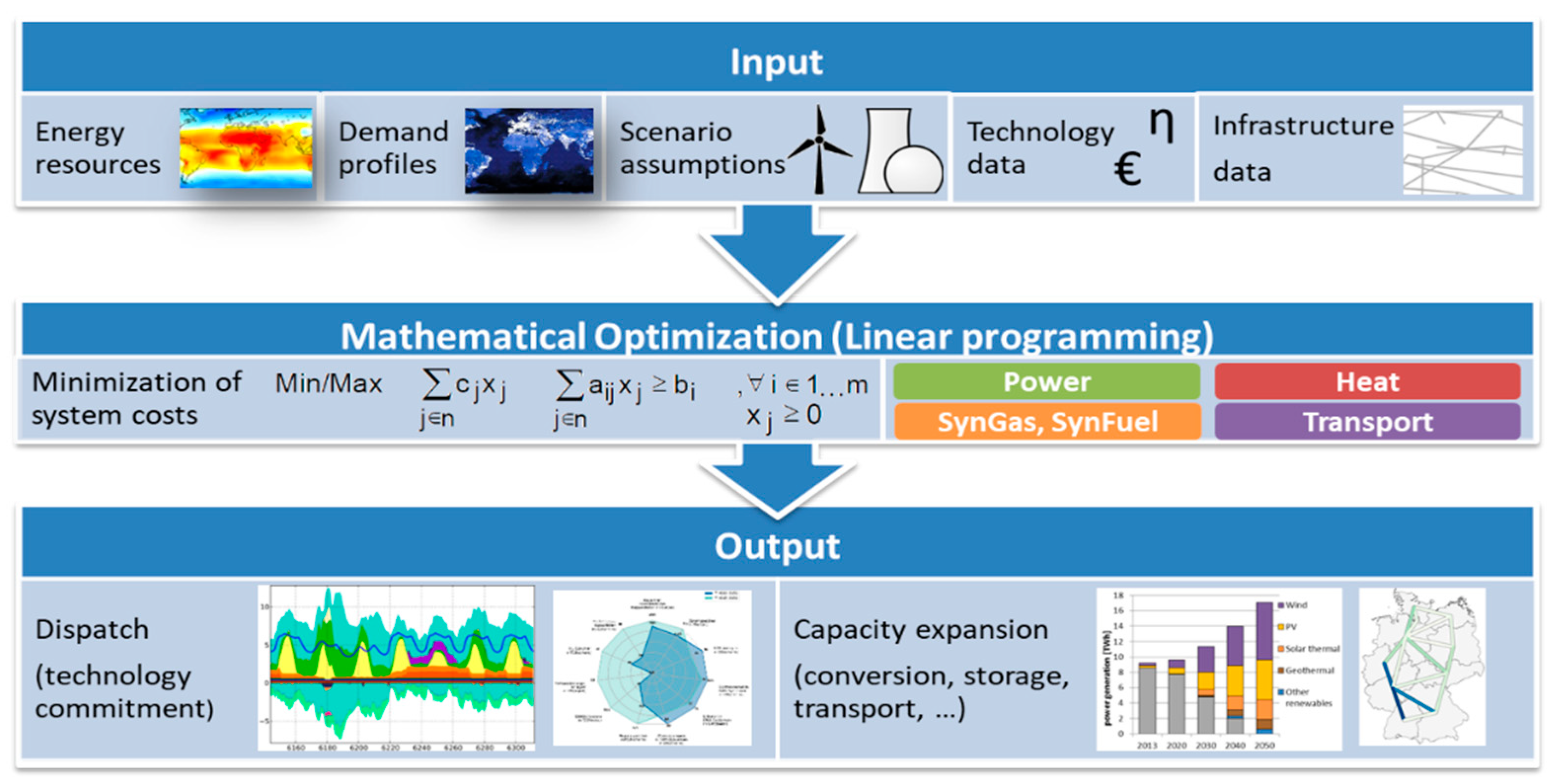

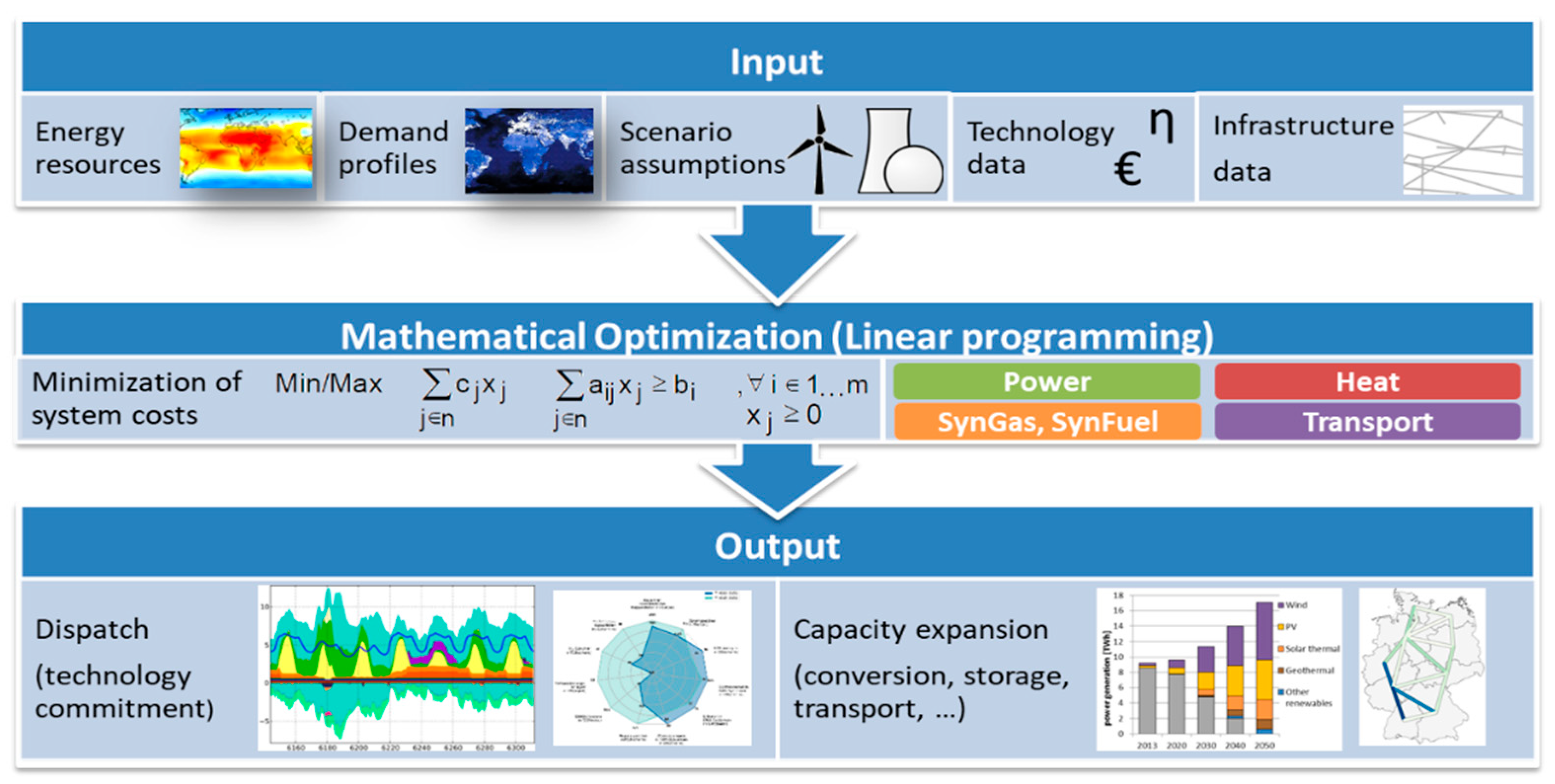

2.1.1. REMix

2.1.2. MuGriFlex

2.1.3. Model Coupling

- Plant sizes (expressed as rated thermal output relative to peak requirement of the local energy system) for combined heat and power (CHP) plants, gas- and electric boilers, heat pumps (HP), thermal energy storage, etc.

- Operation of plants: full load hours per year

- Hourly time-series of power generation costs: These are assumed to be the electricity cost of the power plant running at the margin. To receive electricity prices, the surcharges, to be paid by the respective use case, are added.

- Time-series of produced synthetic gas to establish the gas production costs, taking into account the electricity cost at the given time

2.2. Set-Up of the Case Study

2.3. Main Assumptions about the Energy Future

2.3.1. General Assumptions

2.3.2. Energy Demand Scenario for Germany and Europe

2.4. Fundamentals and Modelling Assumptions for the Natural Gas and Hydrogen Sector

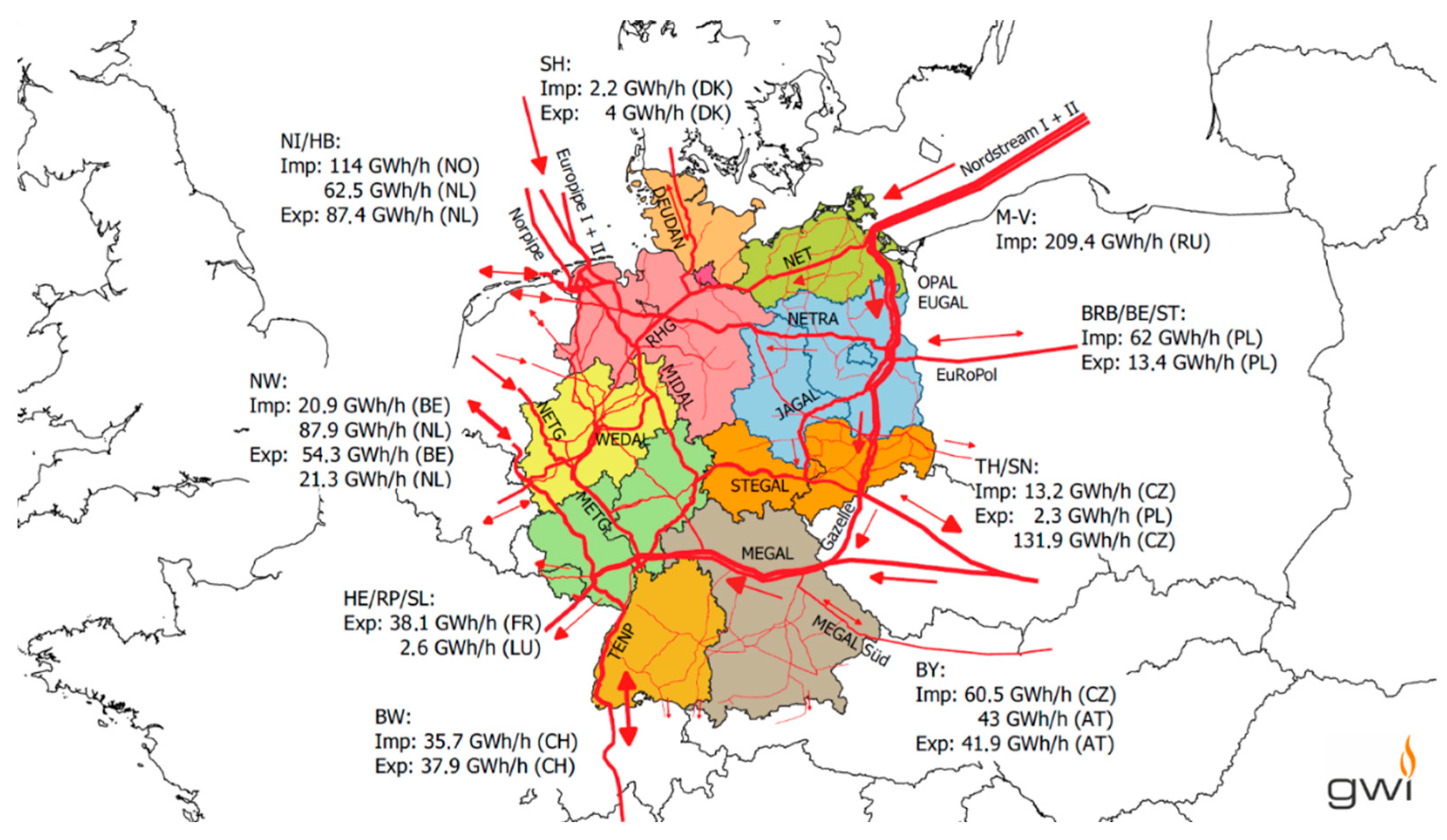

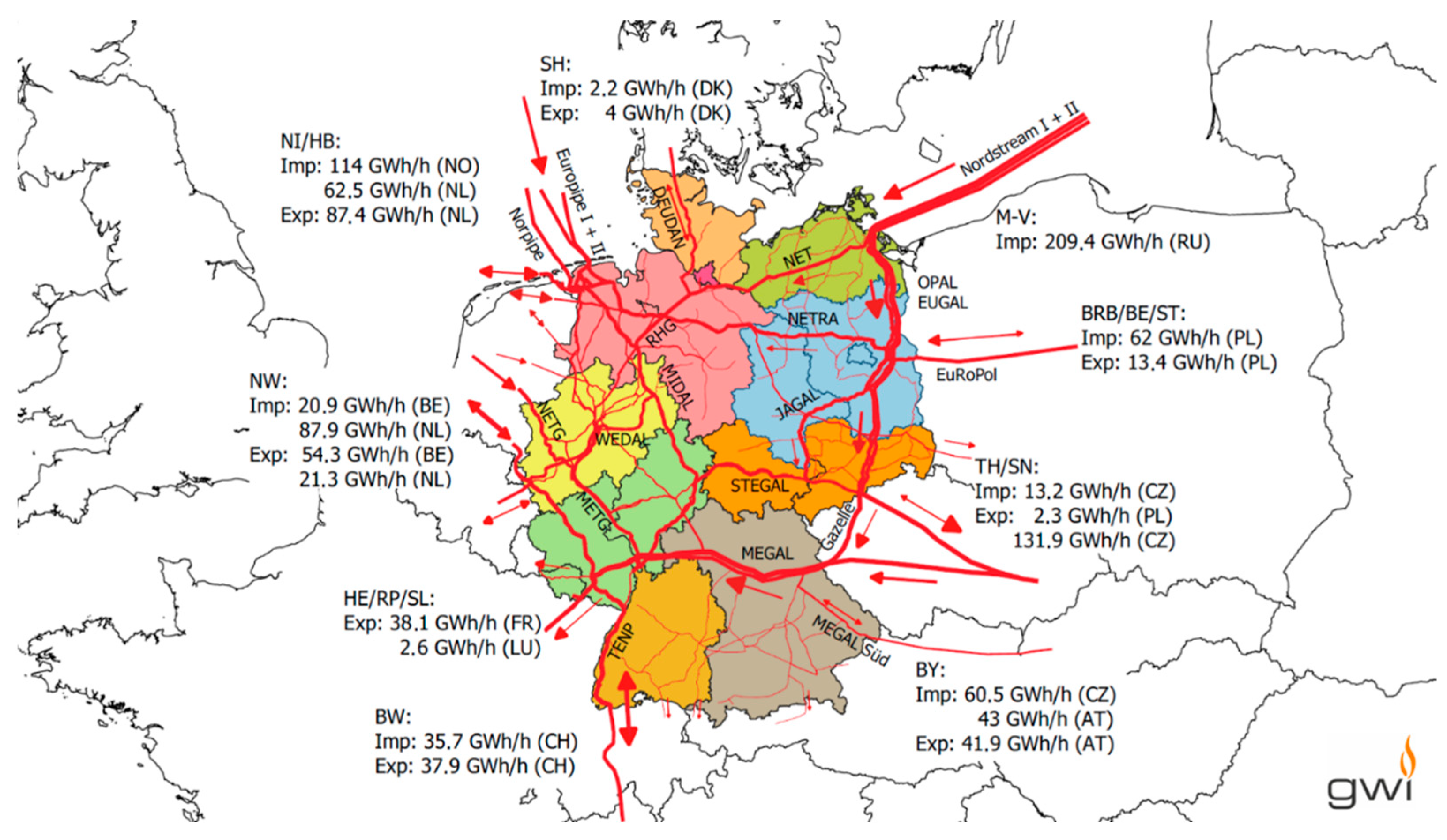

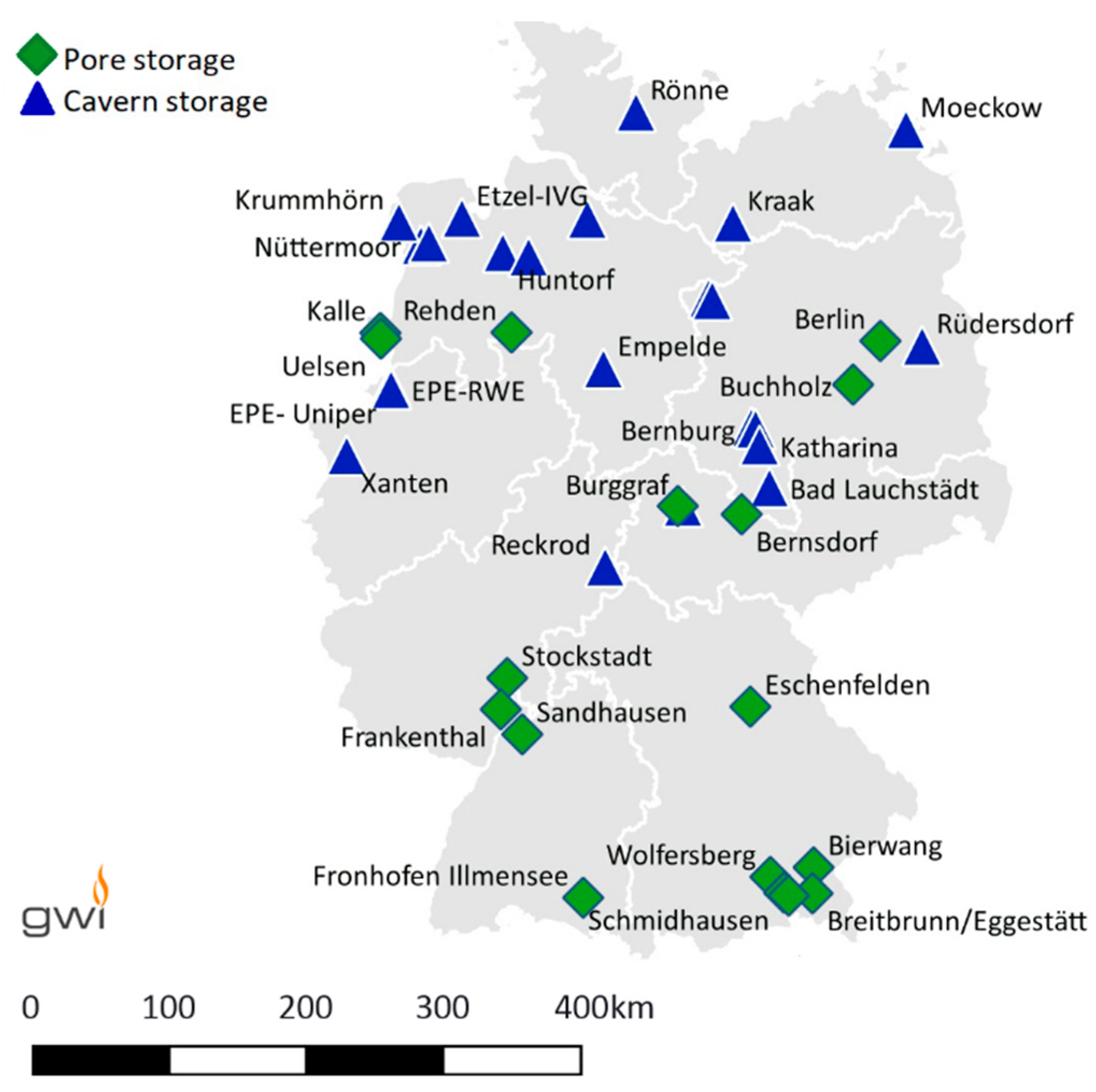

2.4.1. Natural Gas Transportation Grids and Hydrogen Transport Option

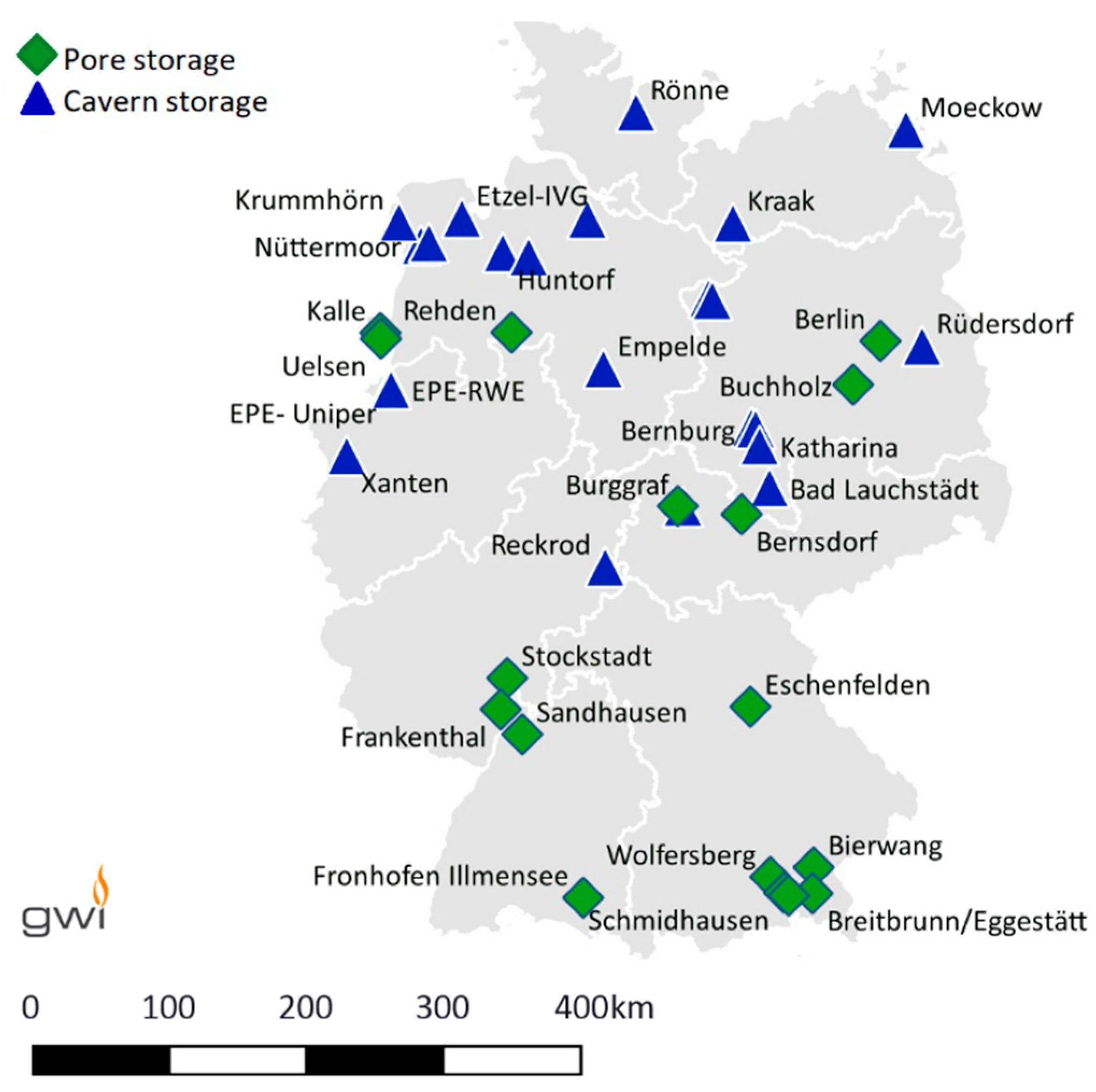

2.4.2. Natural Gas Storage and Hydrogen Storage Option

2.4.3. Renewable Gas Production: Electrolysis and Methanation

2.4.4. Injection of Hydrogen and Biomethane into the Existing Natural Gas Grids

2.4.5. Gas Compression

2.4.6. Pre-Heating of Natural Gas for Decompression

2.5. Further Model Input Assumptions

2.6. Legal and Regulatory Framework in Germany

3. Results

3.1. Results of the Energy System Optimisation

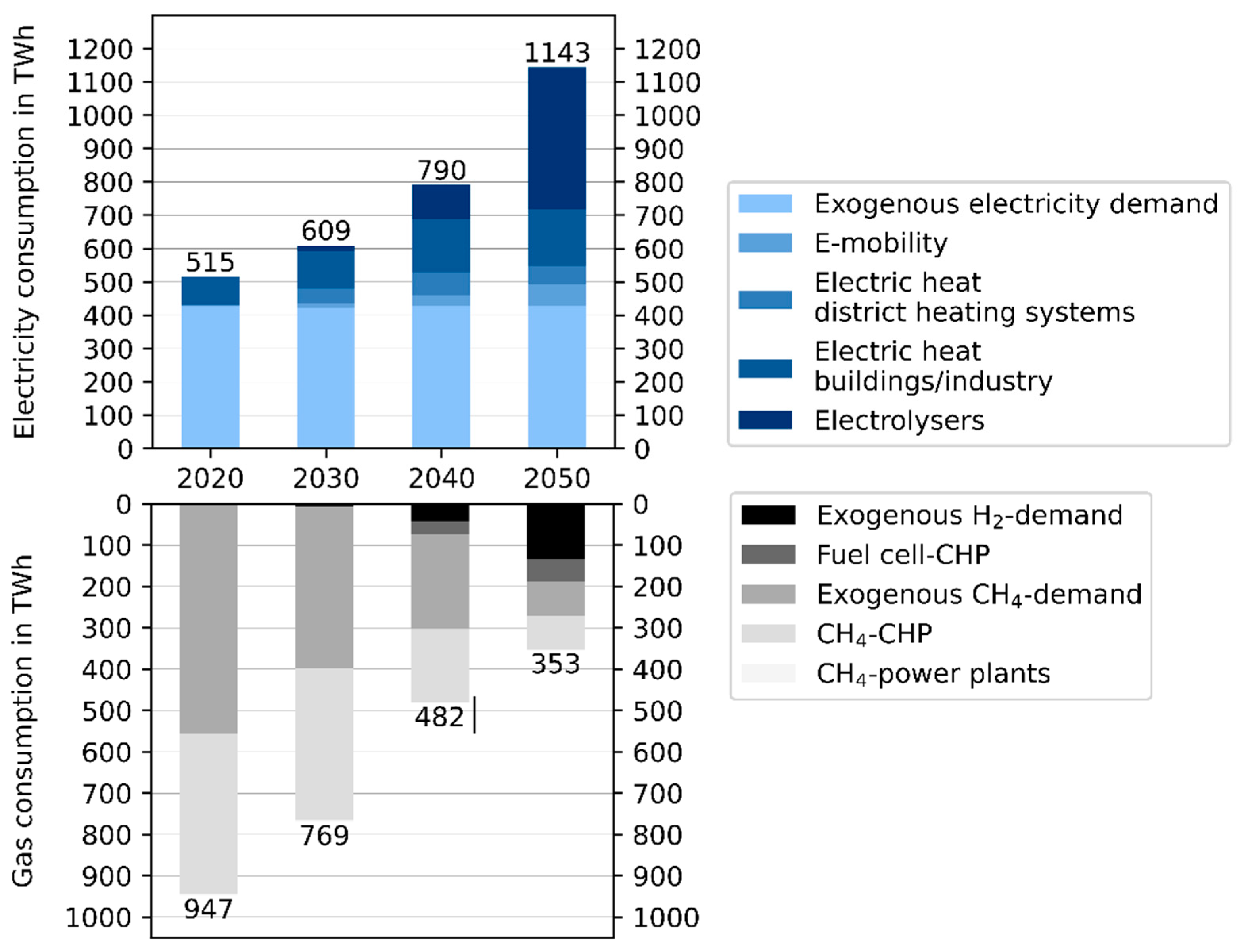

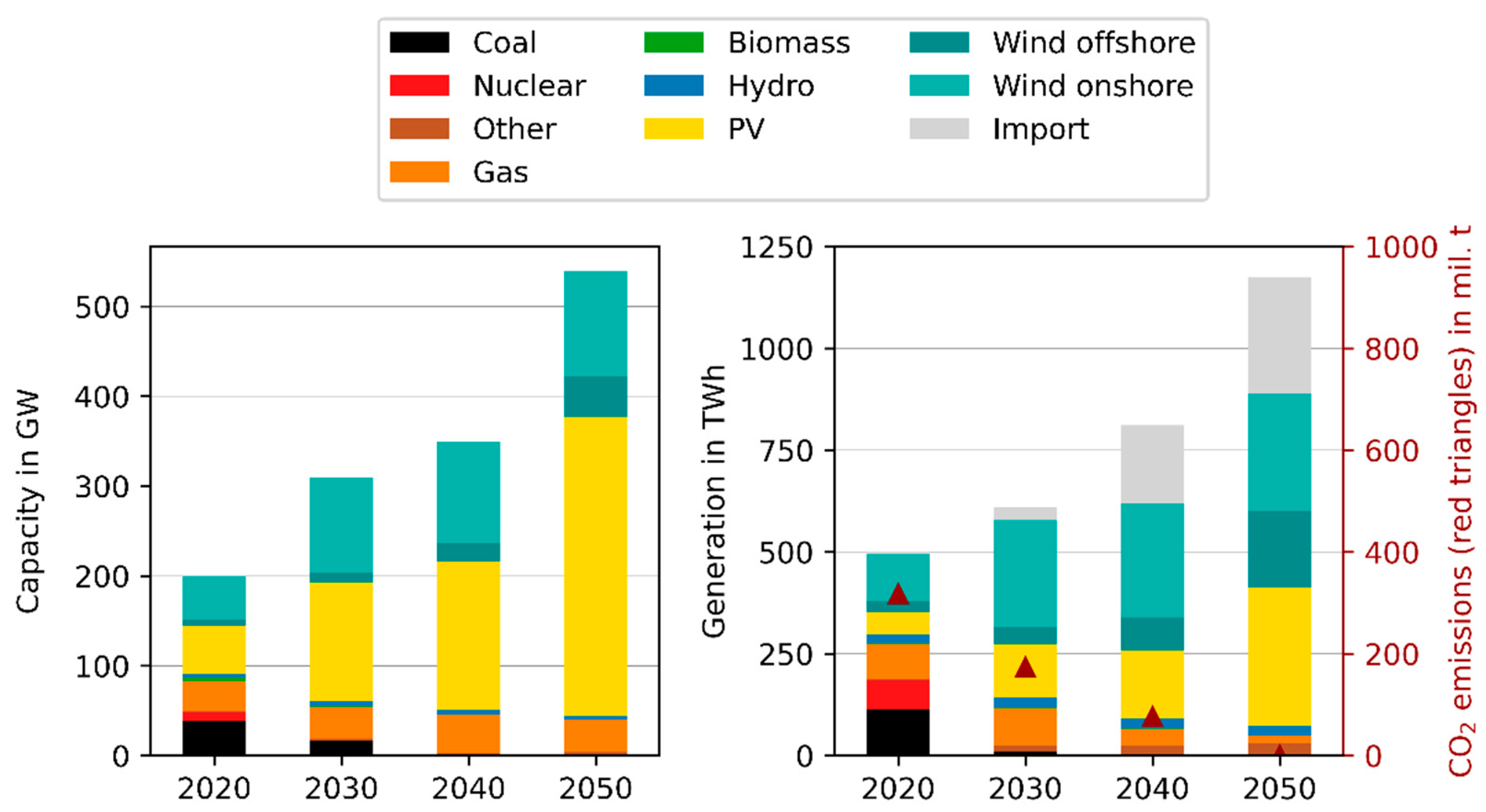

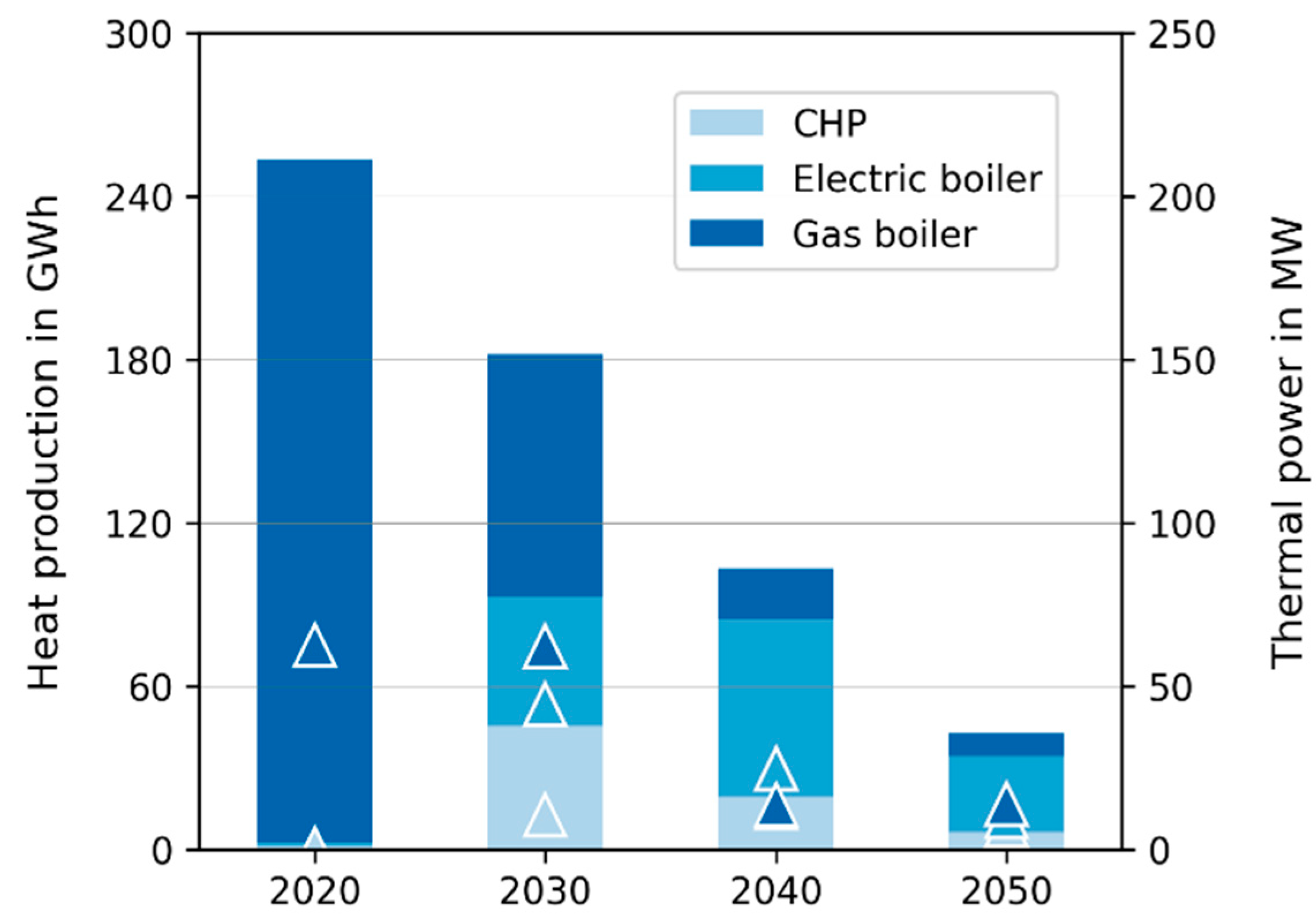

3.1.1. Development of Energy Demand

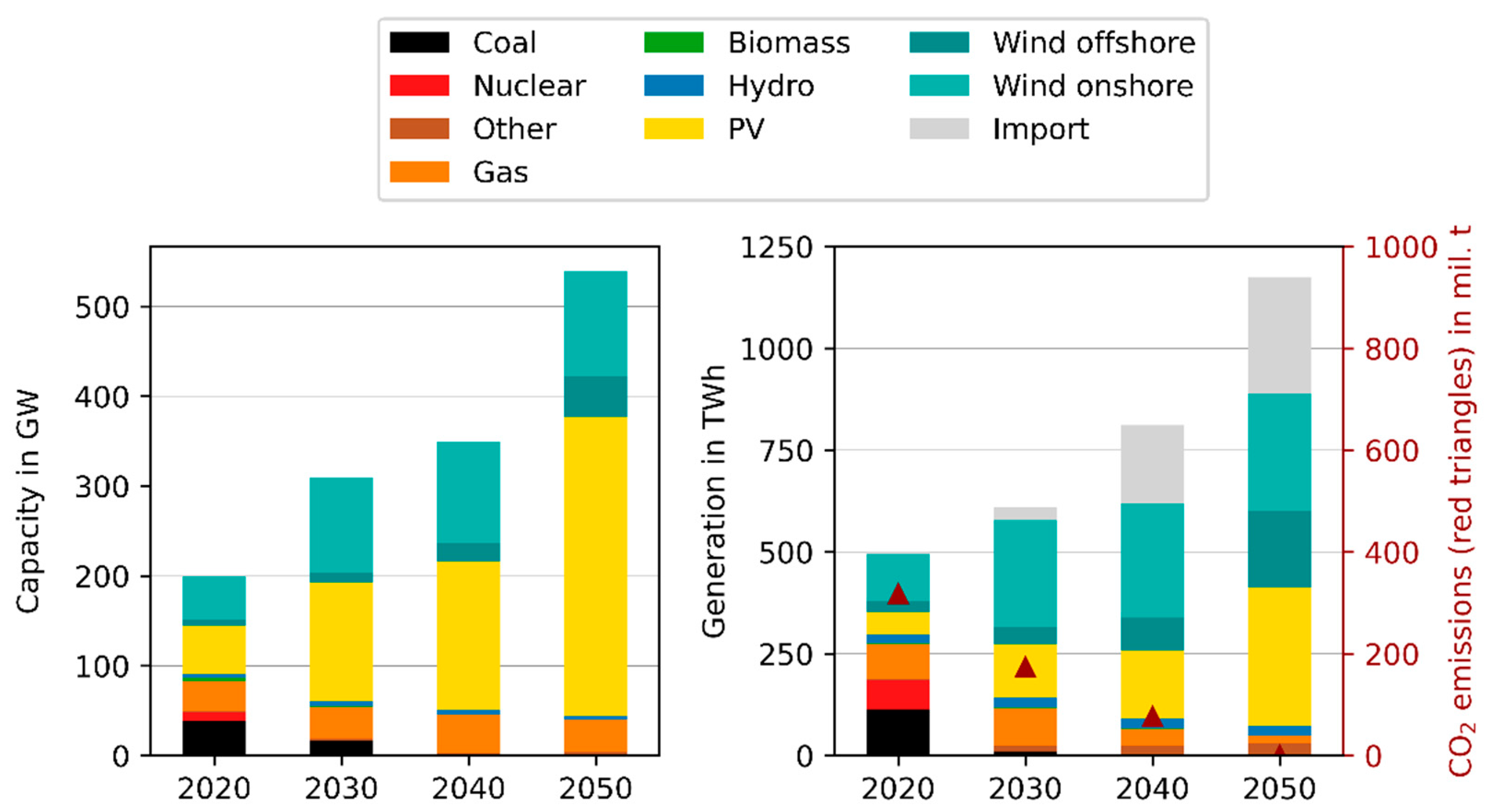

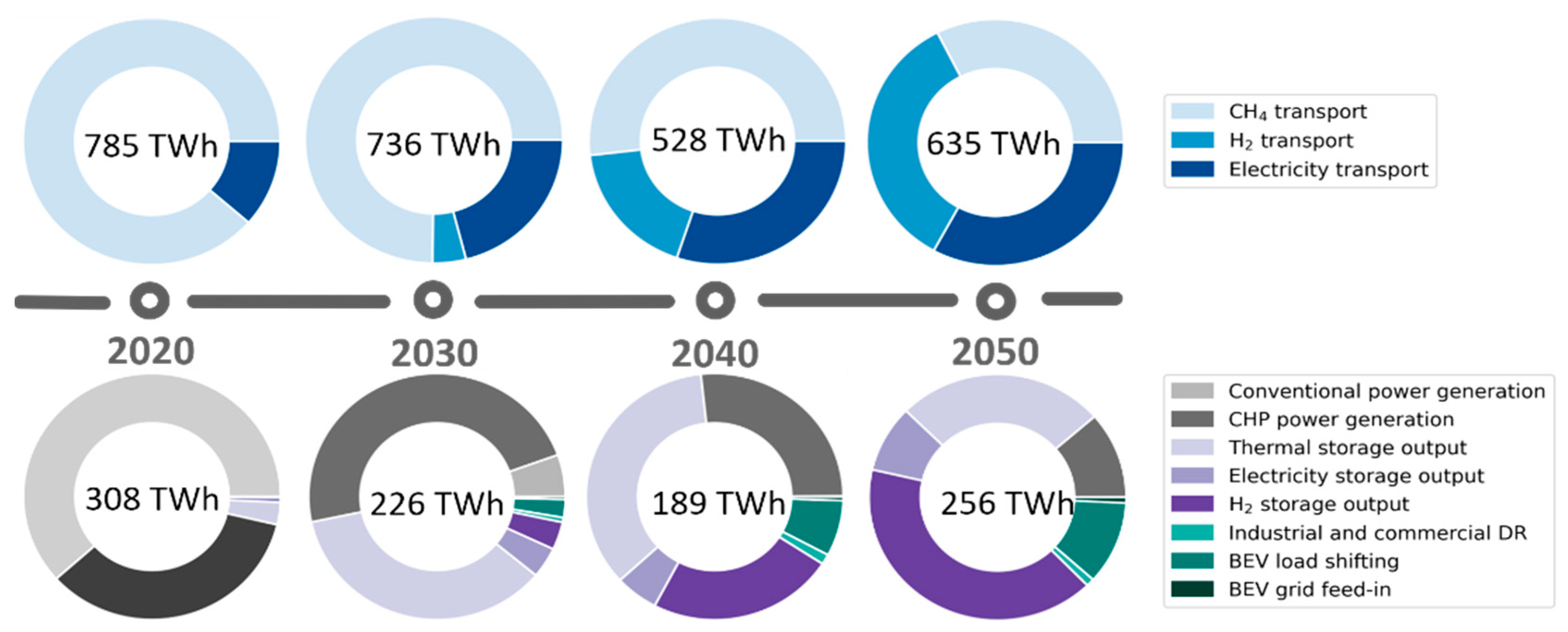

3.1.2. Development of Power Supply and Flexibility Provision

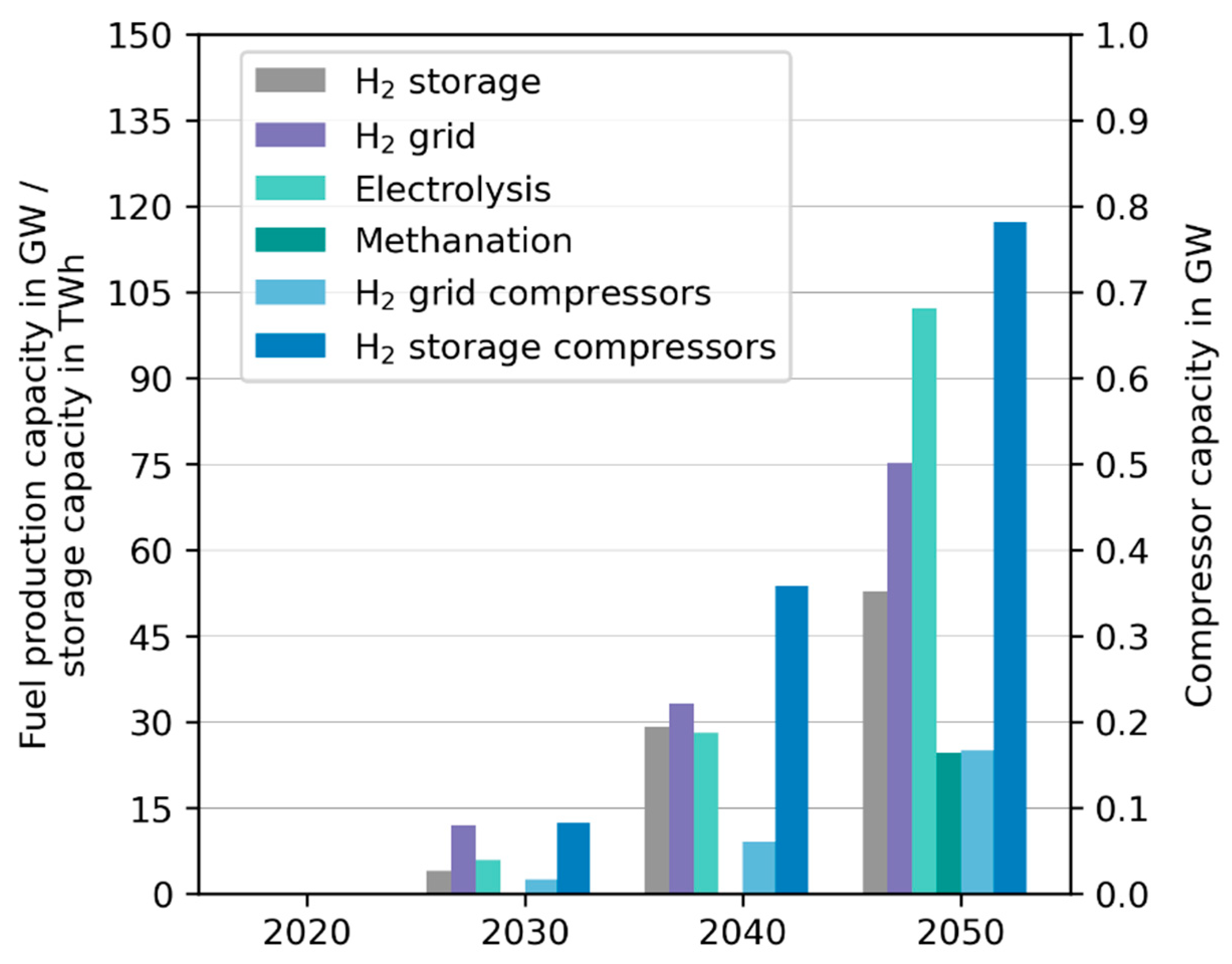

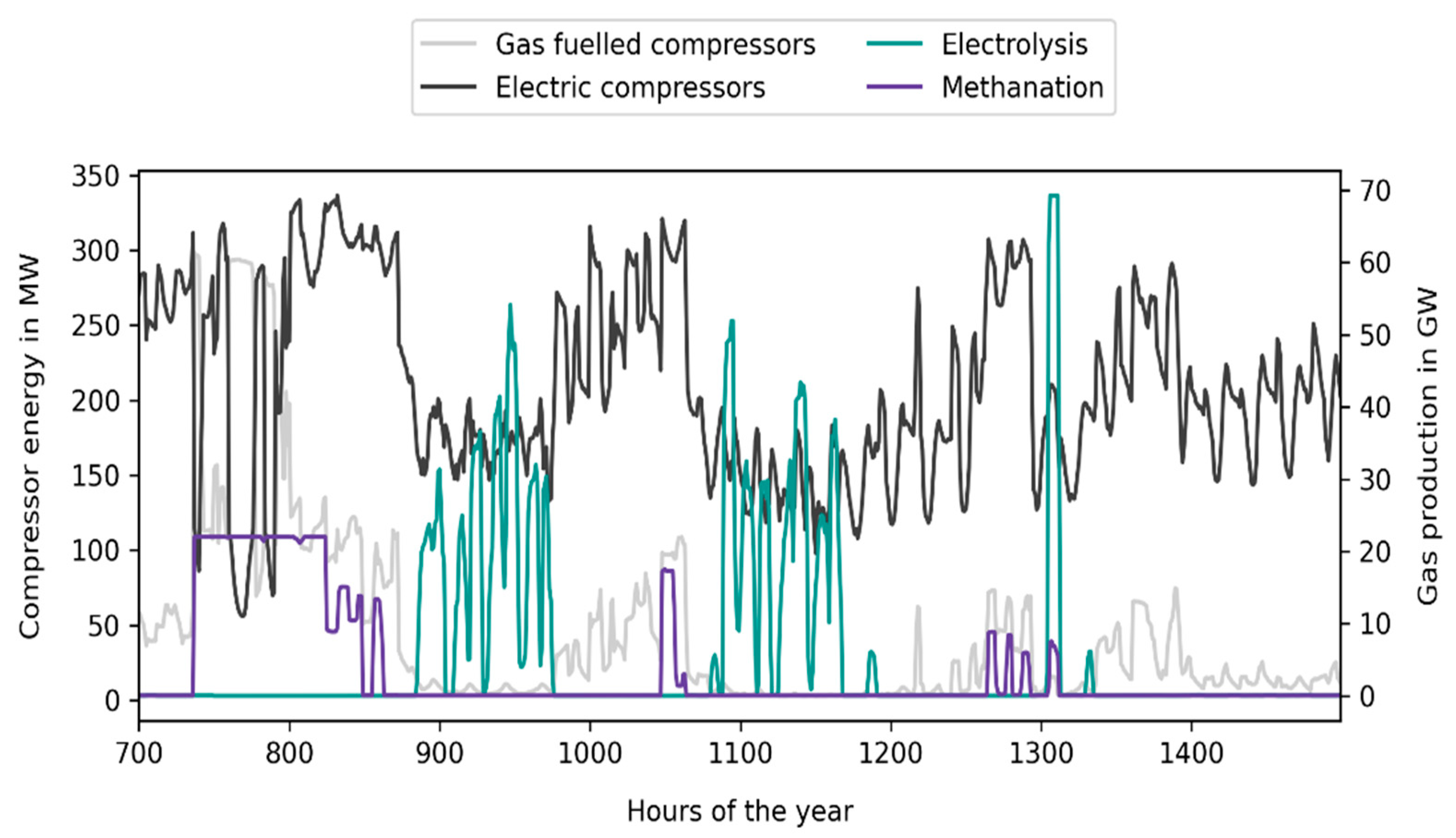

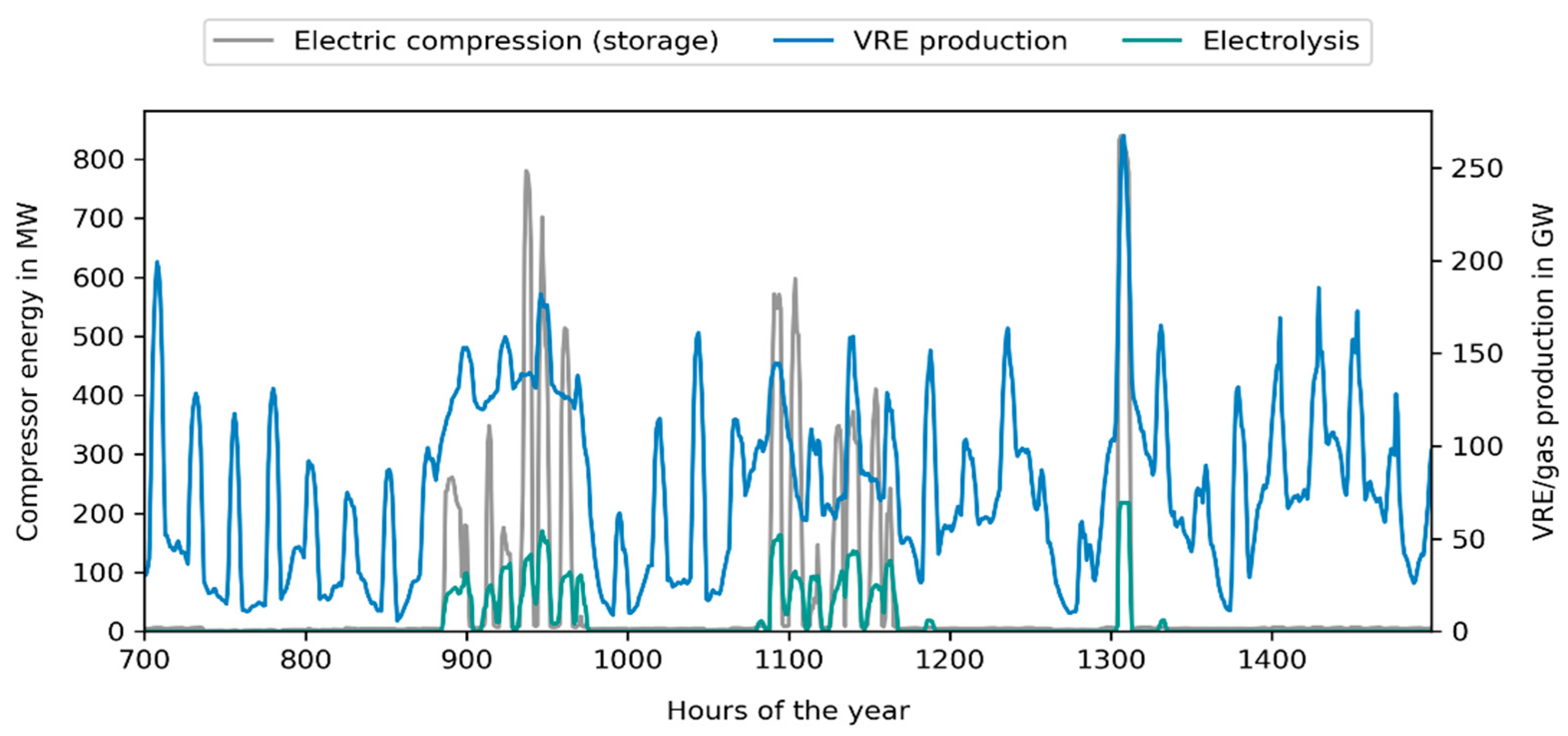

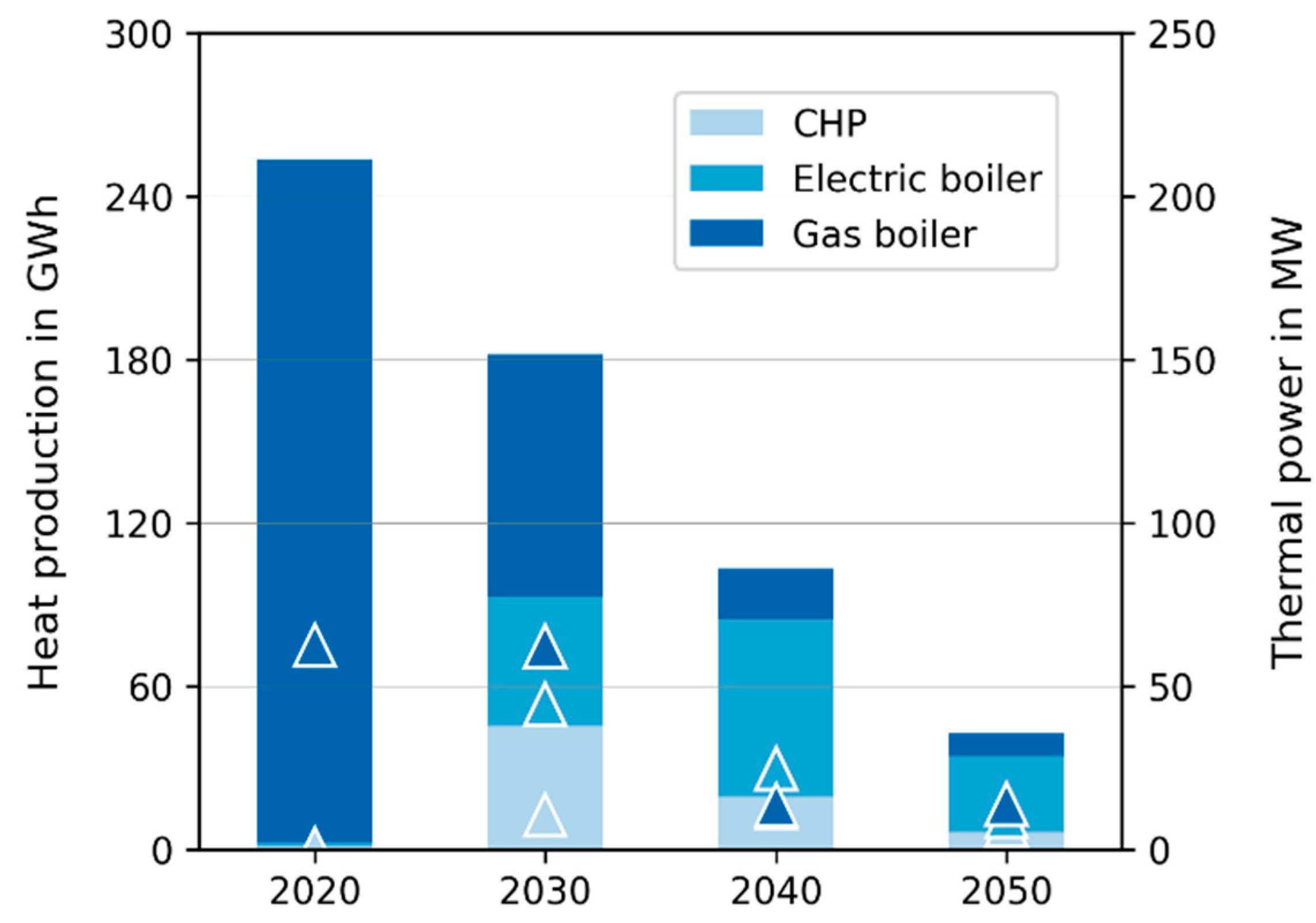

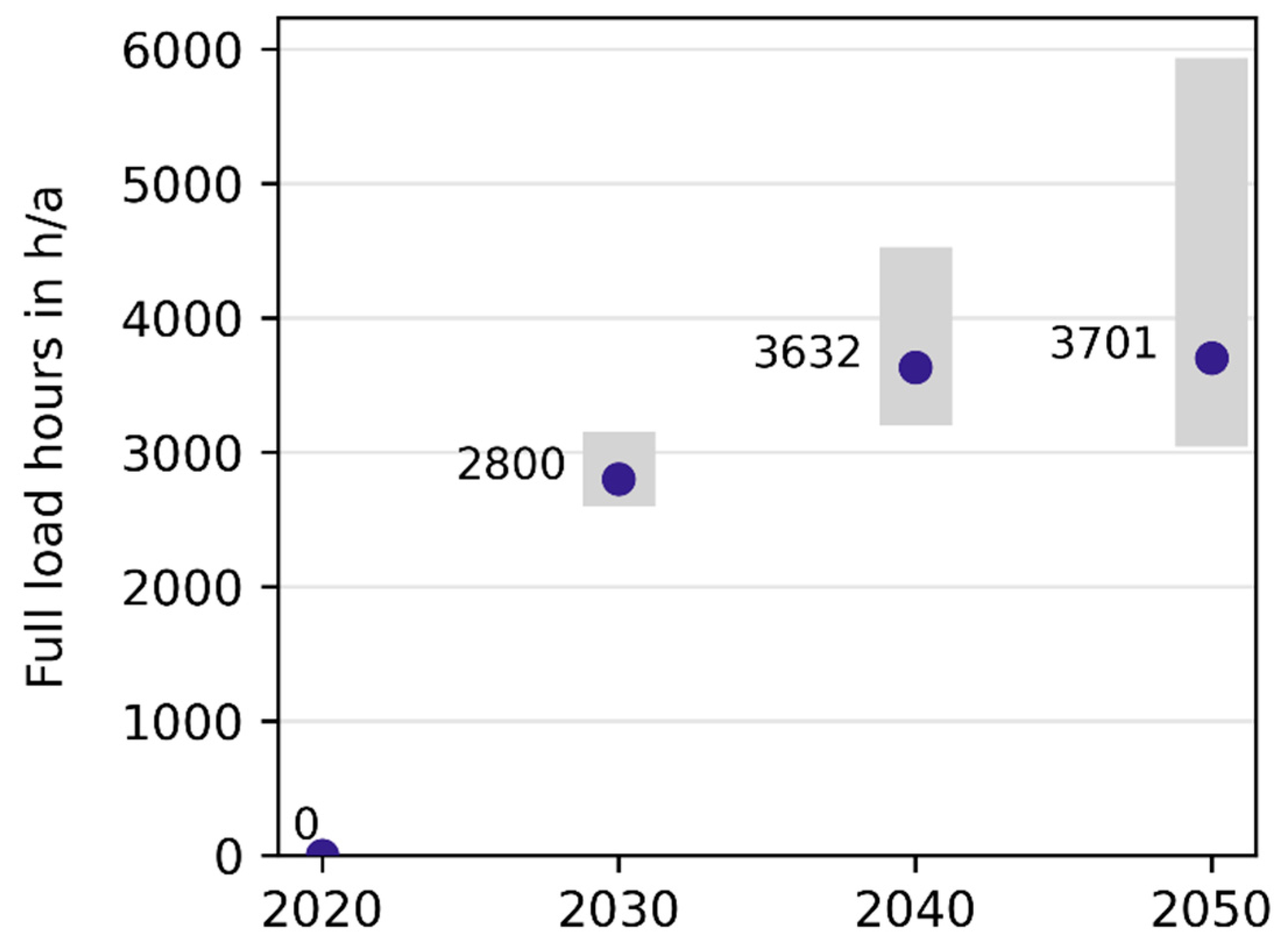

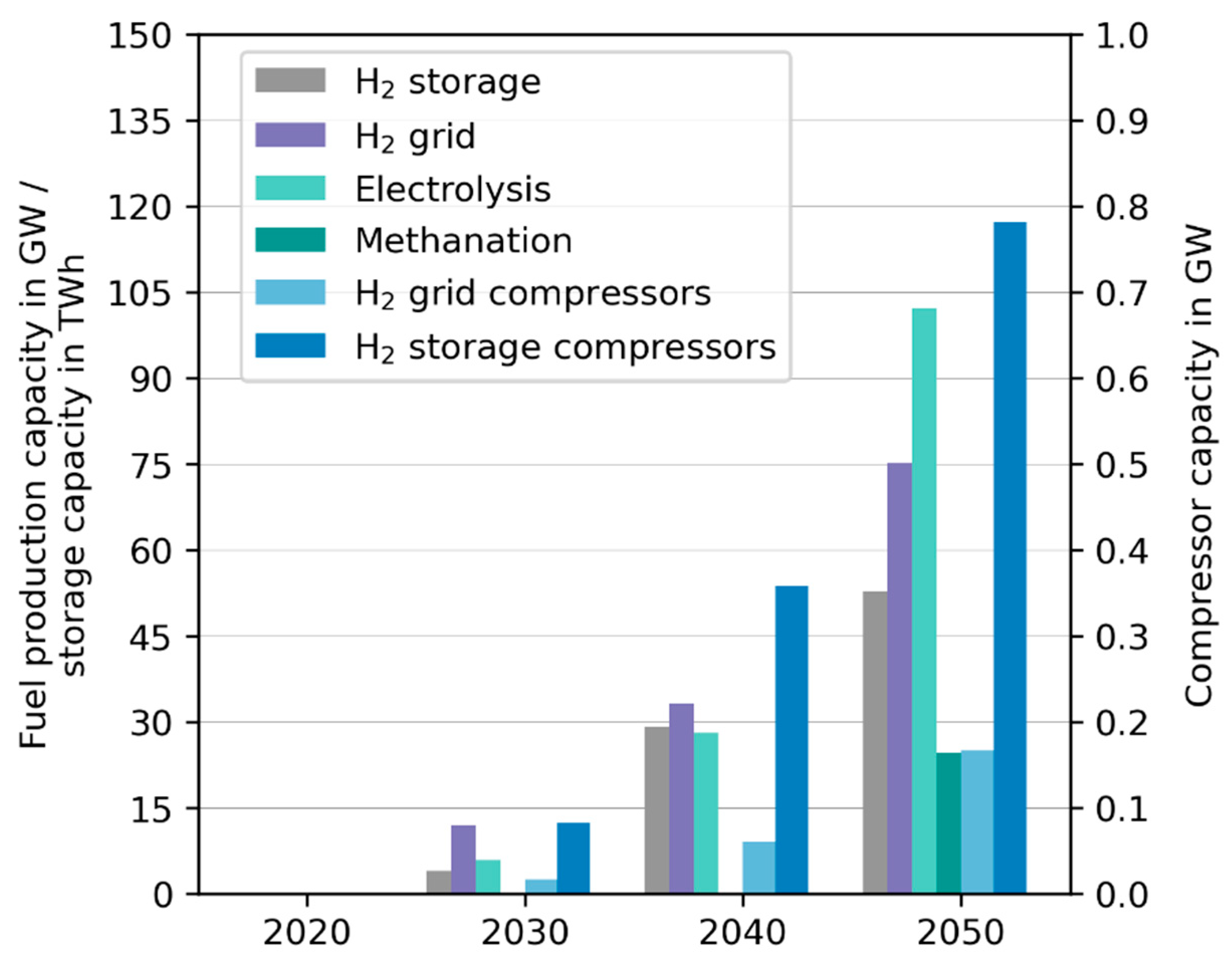

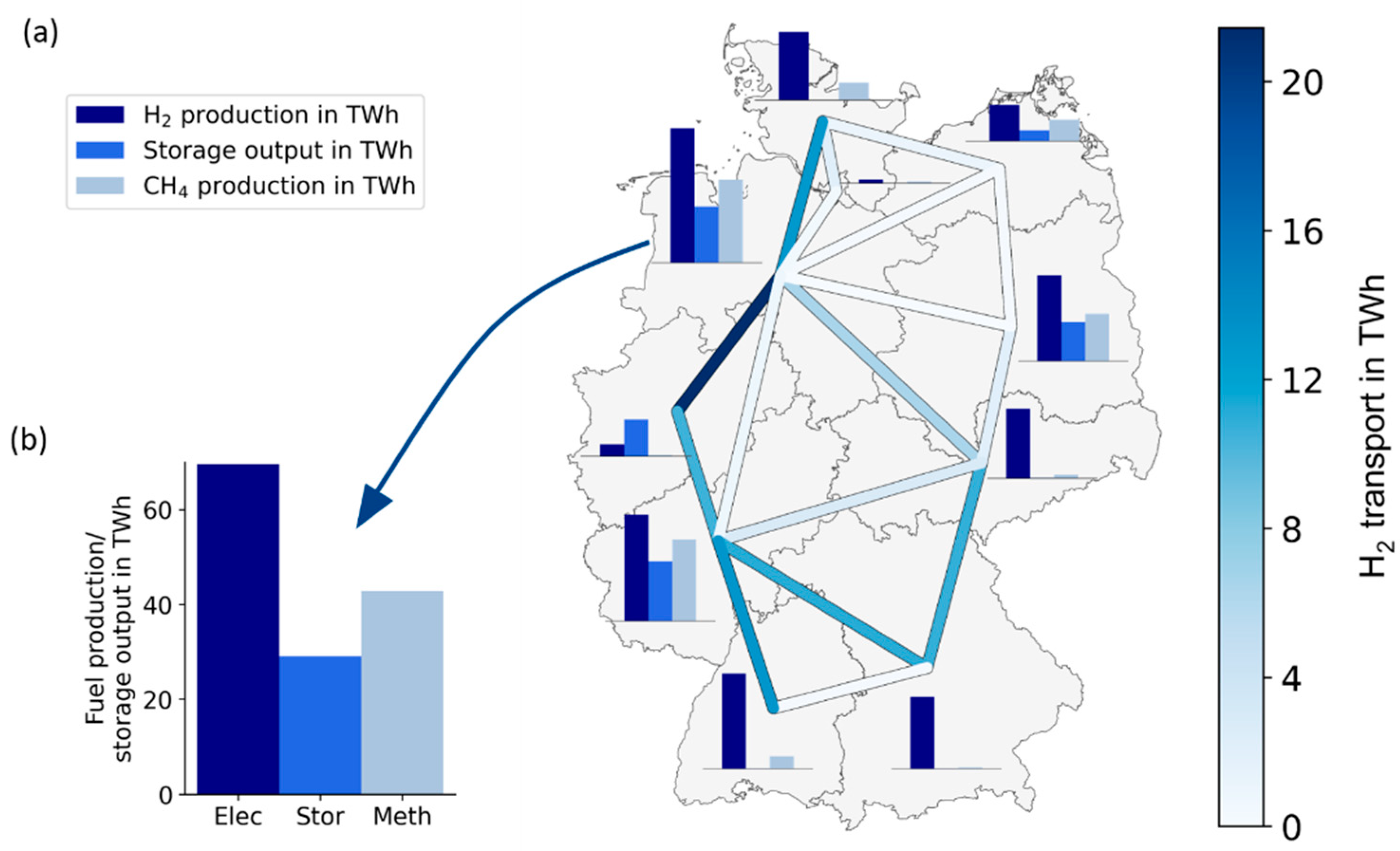

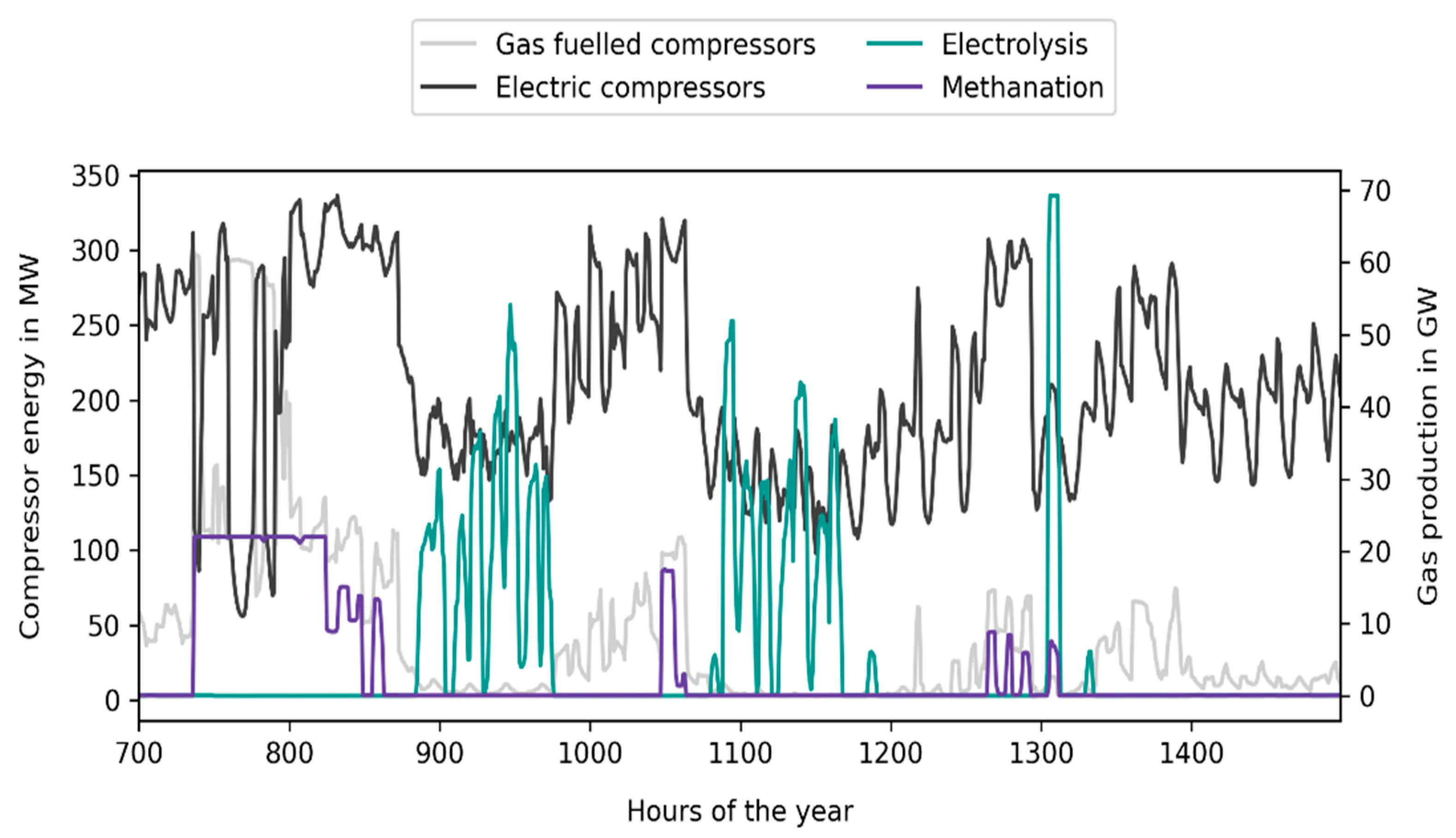

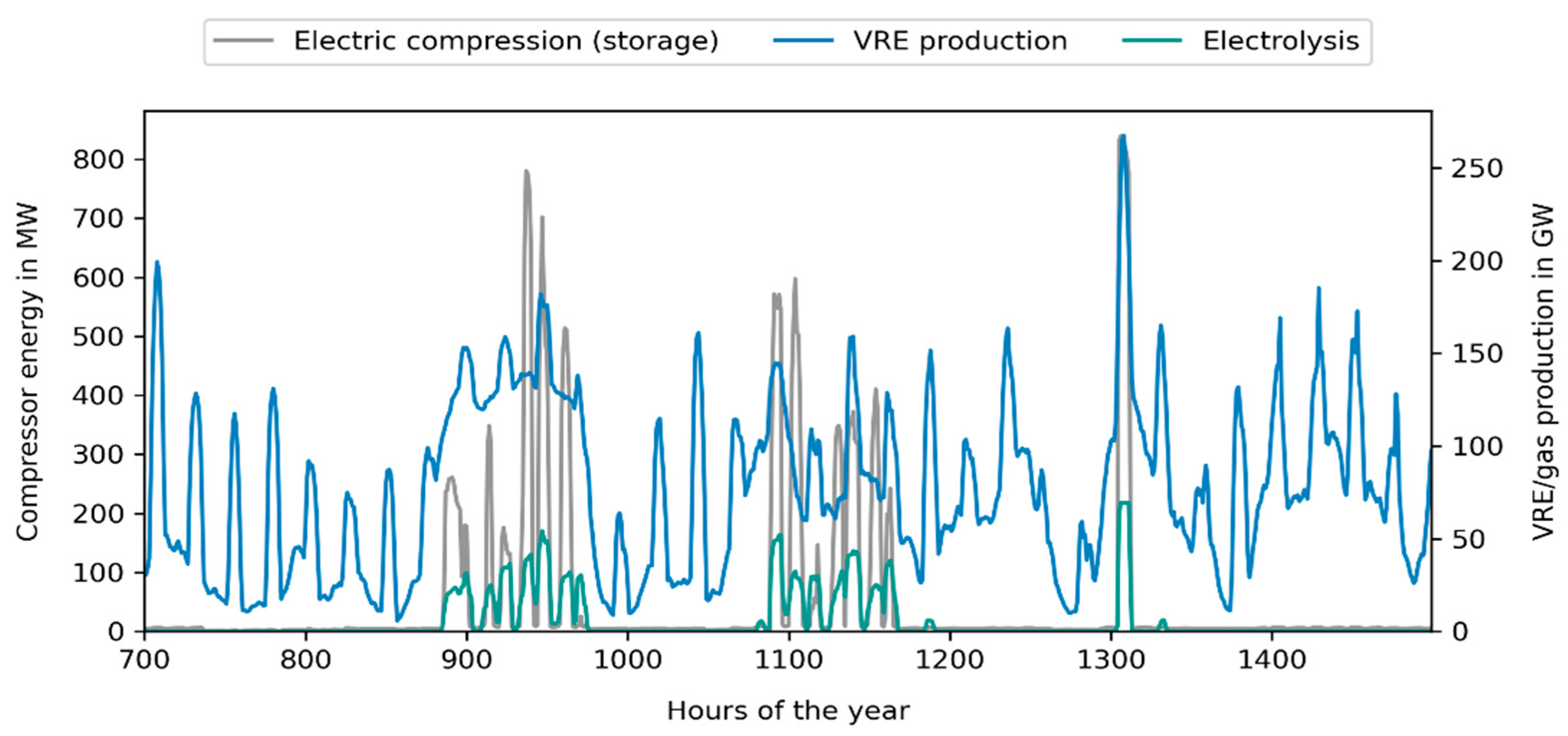

3.1.3. Deployment and Operation of Gas Infrastructures in Germany

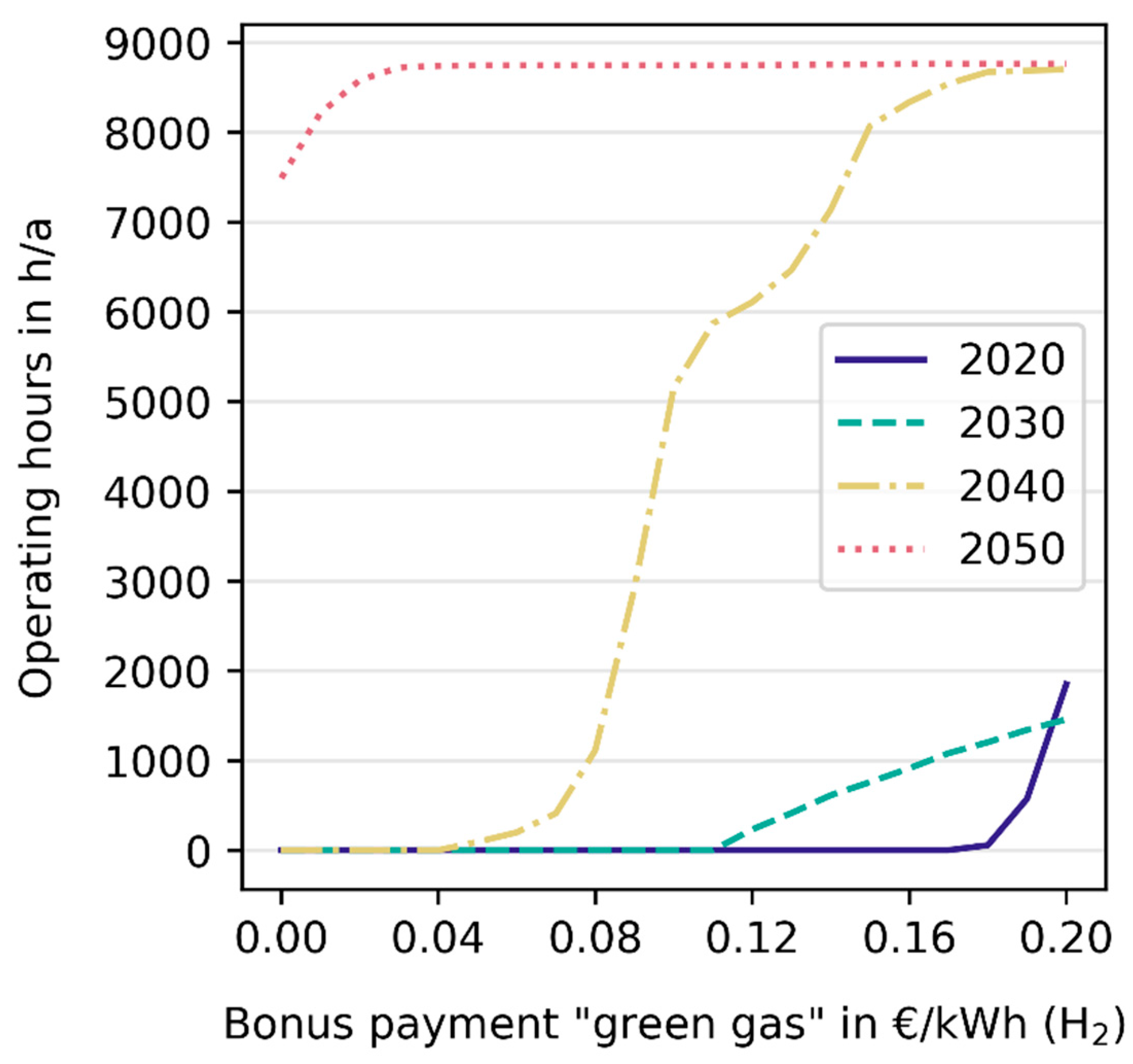

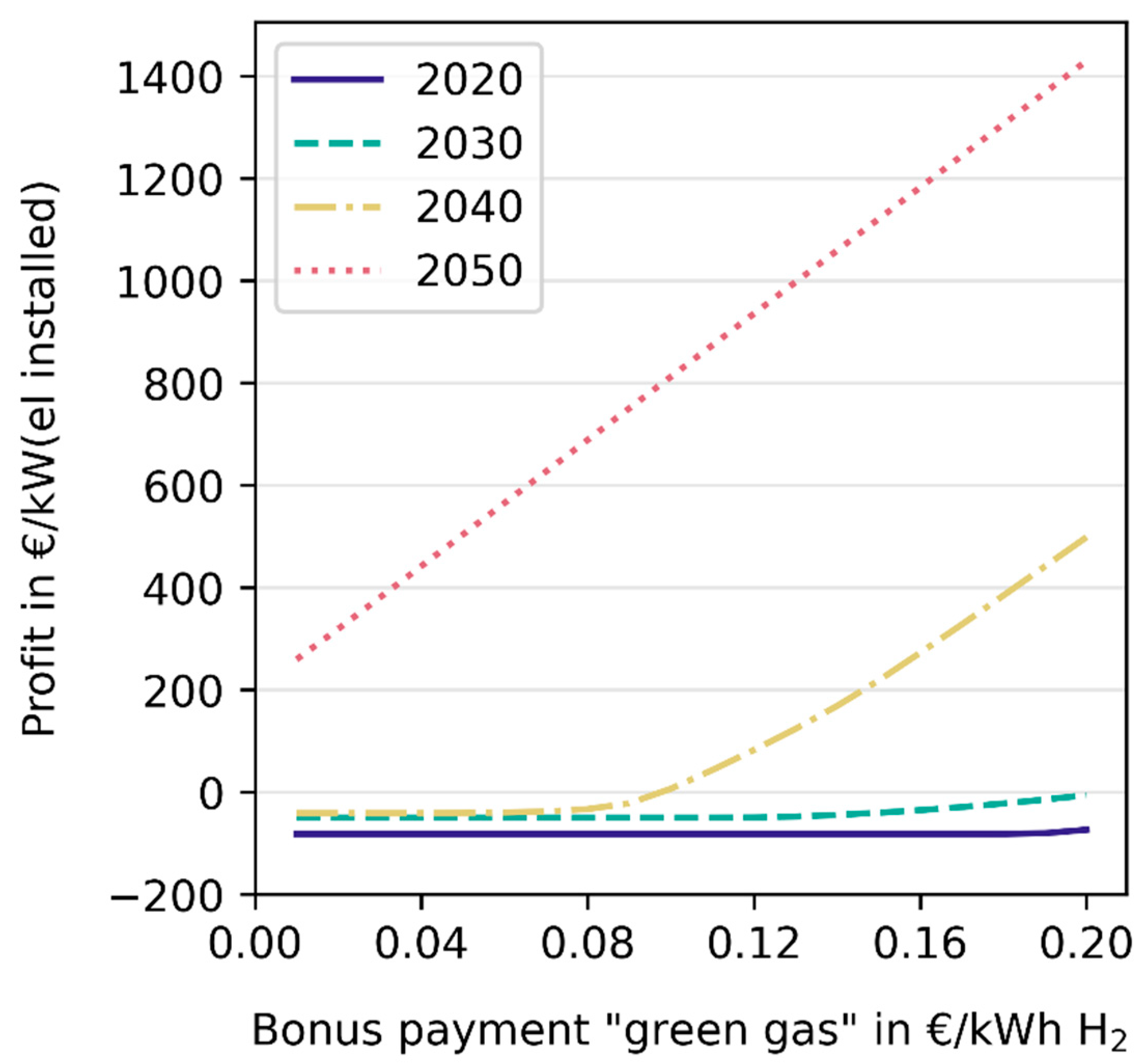

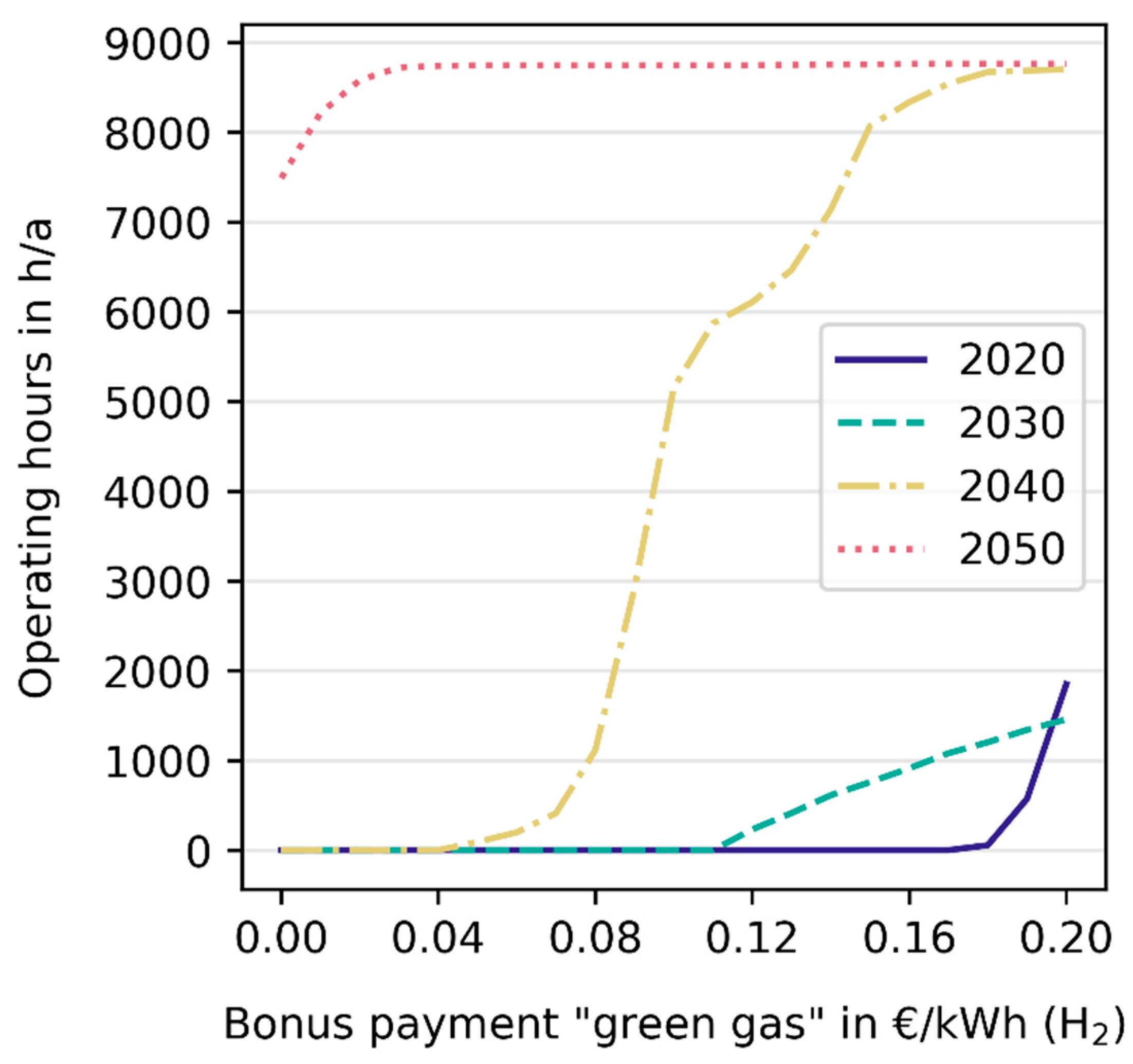

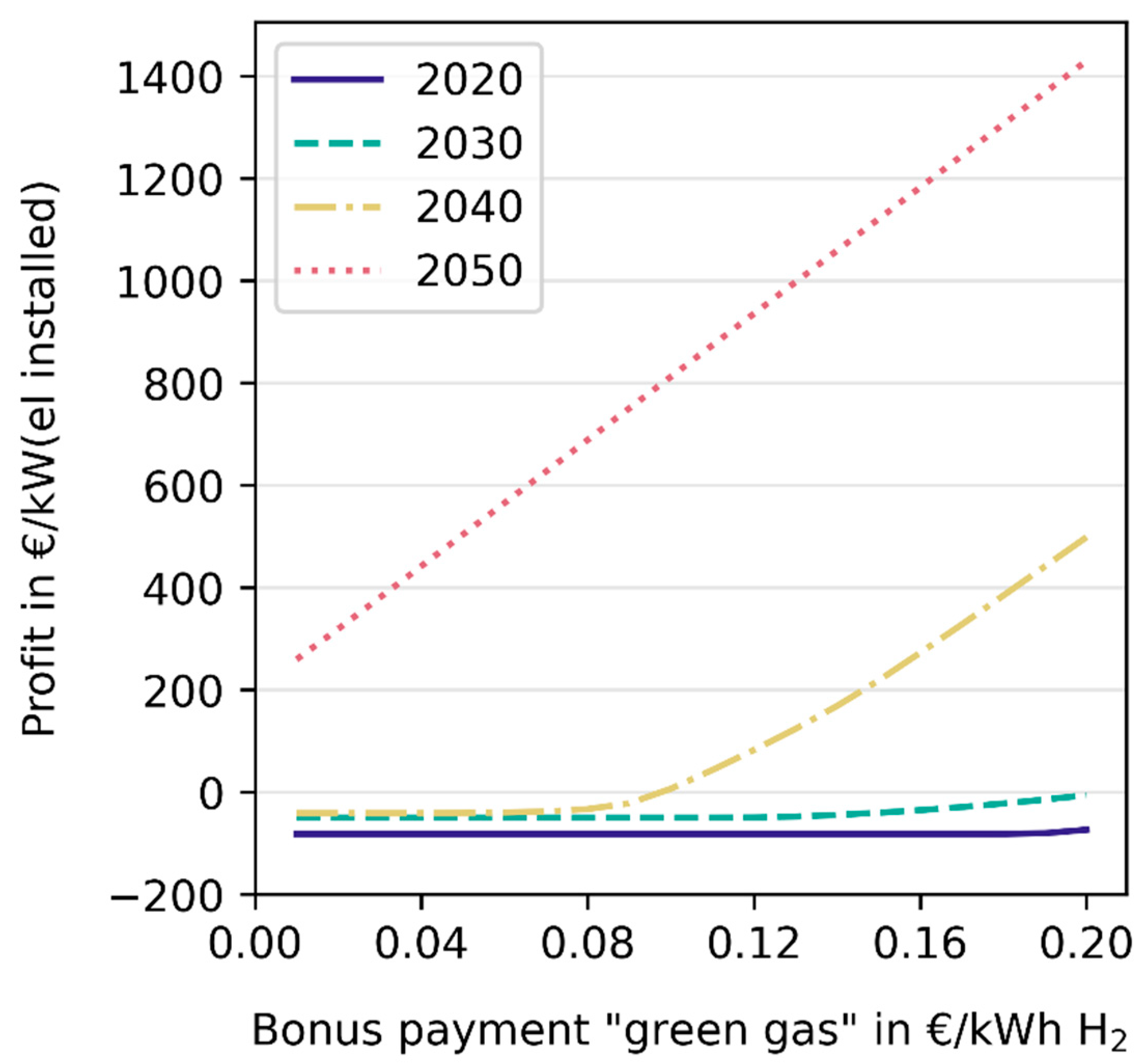

3.2. Business Perspective of Power-to-Gas-Plants

4. Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Heide, D.; Von Bremen, L.; Greiner, M.; Hoffmann, C.; Speckmann, M.; Bofinger, S. Heide Seasonal Optimal Mix of Wind and Solar Power in a Future, Highly Renewable Europe. Renew. Energy 2010, 35, 2483–2489. [Google Scholar] [CrossRef]

- Heide, D.; Greiner, M.; von Bremen, L.; Hoffmann, C. Reduced Storage and Balancing Needs in a Fully Renewable European Power System with Excess Wind and Solar Power Generation. Renew. Energy 2011, 36, 2515–2523. [Google Scholar] [CrossRef] [Green Version]

- Gils, H.C.; Simon, S. Carbon Neutral Archipelago-100% Renewable Energy Supply for the Canary Islands. Appl. Energy 2017, 188, 342–355. [Google Scholar] [CrossRef] [Green Version]

- Brown, T.; Schlachtberger, D.; Kies, A.; Schramm, S.; Greiner, M. Synergies of Sector Coupling and Transmission Reinforcement in a Cost-Optimised, Highly Renewable European Energy System. Energy 2018, 160, 720–739. [Google Scholar] [CrossRef] [Green Version]

- Hauser, P.; Heinrichs, H.U.; Gillessen, B.; Müller, T. Implications of Diversification Strategies in the European Natural Gas Market for the German Energy System. Energy 2018, 151, 442–454. [Google Scholar] [CrossRef]

- Kabirian, A.; Hemmati, M.R. A Strategic Planning Model for Natural Gas Transmission Networks. Energy Policy 2007, 35, 5656–5670. [Google Scholar] [CrossRef]

- Wulf, C.; Linßen, J.; Zapp, P. Review of Power-to-Gas Projects in Europe. Energy Procedia 2018, 155, 367–378. [Google Scholar] [CrossRef]

- Farrokhifar, M.; Nie, Y.; Pozo, D. Energy Systems Planning: A Survey on Models for Integrated Power and Natural Gas Networks Coordination. Appl. Energy 2020, 262, 114567. [Google Scholar] [CrossRef]

- Breyer, C.; Tsupari, E.; Tikka, V.; Vainikka, P. Power-to-Gas as an Emerging Profitable Business Through Creating an Integrated Value Chain. Energy Procedia 2015, 73, 182–189. [Google Scholar] [CrossRef] [Green Version]

- Caglayan, D.; Heinrichs, H.U.; Robinius, M.; Stolten, D. Robust Design of a Future 100% Renewable European Energy Supply System with Hydrogen Infrastructure. Int. J. Hydrog. Energy 2021, 46, 29376–29390. [Google Scholar] [CrossRef]

- Torralba-Díaz, L.; Schimeczek, C.; Reeg, M.; Savvidis, G.; Deissenroth-Uhrig, M.; Guthoff, F.; Fleischer, B.; Hufendiek, K. Identification of the Efficiency Gap by Coupling a Fundamental Electricity Market Model and an Agent-Based Simulation Model. Energies 2020, 13, 3920. [Google Scholar] [CrossRef]

- van Leeuwen, C.; Mulder, M. Power-to-Gas in Electricity Markets Dominated by Renewables. Appl. Energy 2018, 232, 258–272. [Google Scholar] [CrossRef]

- Li, X.; Mulder, M. Value of Power-to-Gas as a Flexibility Option in Integrated Electricity and Hydrogen Markets. Appl. Energy 2021, 304, 117863. [Google Scholar] [CrossRef]

- Gils, H.C.; Gardian, H.; Pregger, T.; Schaffert, J.; Tali, E.; Fette, M.; Brandstätt, C. REMix Model Input Data for the THG95/GHG95 Scenario Analysed within the MuSeKo Project. Available online: https://zenodo.org/record/5705414 (accessed on 16 November 2021).

- Gils, H.C.; Scholz, Y.; Pregger, T.; de Tena, D.L.; Heide, D. Integrated Modelling of Variable Renewable Energy-Based Power Supply in Europe. Energy 2017, 123, 173–188. [Google Scholar] [CrossRef] [Green Version]

- Luca de Tena, D.; Pregger, T. Impact of Electric Vehicles on a Future Renewable Energy-Based Power System in Europe with a Focus on Germany. Int. J. Energy Res. 2018, 42, 2670–2685. [Google Scholar] [CrossRef]

- Gils, H.C. Balancing of Intermittent Renewable Power Generation by Demand Response and Thermal Energy Storage. Ph.D. Thesis, Uniersität Stuttgart, Stuttgart, Germany, 2015. [Google Scholar]

- Michalski, J.; Bünger, U.; Crotogino, F.; Donadei, S.; Schneider, G.-S.; Pregger, T.; Cao, K.-K.; Heide, D. Hydrogen Generation by Electrolysis and Storage in Salt Caverns: Potentials, Economics and Systems Aspects with Regard to the German Energy Transition. Int. J. Hydrog. Energy 2017, 42, 13427–13443. [Google Scholar] [CrossRef]

- Gils, H.C.; Gardian, H.; Schmugge, J. Interaction of Hydrogen Infrastructures with Other Sector Coupling Options towards a Zero-Emission Energy System in Germany. Renew. Energy 2021, 180, 140–156. [Google Scholar] [CrossRef]

- Brandstätt, C.; Fette, M. Feasibility of Balancing Renewable Electricity through Heat and Gas Based “Storage Chains”. In Proceedings of the International Renewable Energy Storage Conference (IRES), Düsseldorf, Germany, 9–11 March 2015. [Google Scholar]

- Brandstätt, C.; Fette, M.; Meyer, S. Multi-Grid-Storage Flexibilität für die Stromversorgung aus Gas- und Wärmenetzen. Final Report. 2015. Available online: https://www.ifam.fraunhofer.de/de/Institutsprofil/Standorte/Bremen/Formgebung_Funktionswerkstoffe/Energiesystemanalyse/Projektdetails/MuGriSto.html (accessed on 5 July 2021).

- Brandstätt, C.; Fette, M.; Gils, H.C.; Gardian, H.; Pregger, T.; Schaffert, J.; Brücken, N.; Tali, E. Final Report: Multi-Sektor-Kopplung (MuSeKo)—Modellbasierte Analyse der Integration Erneuerbarer Stromerzeugung Durch Die Kopplung der Stromversorgung Mit Dem Wärme, Gas- und Verkehrssektor; BMWi; Grant Agreement No, 03ET4038; Fraunhofer-Institut für Fertigungstechnik und Angewandte Materialforschung (IFAM): Bremen, Germany; Deutsches Zentrum für Luft- und Raumfahrt (DLR): Stuttgart, Germany; Gas- und Wärme-Institut Essen e.V. (GWI): Essen, Germany, 2020. [Google Scholar] [CrossRef]

- Pfluger, B.; Tersteegen, B.; Franke, B.; Bernath, C.; Boßmann, T.; Deac, G.; Elsland, R.; Fleiter, T.; Kühn, A.; Ragwitz, M.; et al. Langfristszenarien Fur Die Transformation Des Energiesystems in Deutschland—Modul 1: Hintergrund, Szenarioarchitektur Und Übergeordnete Rahmenparameter; Fraunhofer ISI, Consentec GmbH, ifeu, Bundesministerium für Wirtschaft und Energie: Berlin, Germany, 2017; p. 45. [Google Scholar]

- Project E-Highway2050—Modular Development Plan of the Pan-European Transmission System 2050. Available online: https://docs.entsoe.eu/baltic-conf/bites/www.e-highway2050.eu/results/ (accessed on 17 December 2021).

- Bundesministerium für Wirtschaft und Technologie (BMWi). Bundesministerium für Umwelt, Naturschutz und Reaktorsicherheit Energiekonzept Für Eine Umweltschonende, Zuverlässige Und Bezahlbare Energieversorgung; BMWi: Berlin, Germany, 2010; p. 34.

- International Energy Agency (IEA); European Network of Transmission System Operators for Gas (ENTSO-G). Netherlands Ministry of Economic Affairs and Climate Policy L-Gas Market Conversion Review—Winter Report 2021 Task Force Monitoring L-Gas Market Conversion 2021. Available online: https://groenevinger.files.wordpress.com/2021/02/bijlage-2-winter-report.pdf (accessed on 17 December 2021).

- FNB Gas—Die Fernleitungsnetzbetreiber. German Gas Network Development Plan (Netzentwicklungsplan Gas) 2016–2026; FNB Gas: Berlin, Germany, 2017; Available online: https://www.bundesnetzagentur.de/DE/Sachgebiete/ElektrizitaetundGas/Unternehmen_Institutionen/NetzentwicklungSmartGrid/Gas/fruehereNEP/NEP_Gas2016/NEP_Gas2016_node.html (accessed on 31 January 2022).

- European Network of Transmission System Operators for Gas (entsog): The European Natural Gas Network 2017. Available online: https://www.entsog.eu/sites/default/files/2018-09/ENTSOG_CAP_2017_A0_1189x841_FULL_064.pdf (accessed on 3 January 2019).

- Caglayan, D.; Weber, N.; Heinrichs, H.; Linssen, J.; Robinius, M.; Kukla, P.; Stolten, D. Technical Potential of Salt Caverns for Hydrogen Storage in Europe. Int. J. Hydrog. Energy 2020, 45, 6793–6805. [Google Scholar] [CrossRef]

- Stolzenburg, K.; Hamelmann, R.; Wietschel, M.; Genoese, F.; Michaelis, J.; Lehmann, J.; Miege, A.; Krause, S.; Sponholz, C.; Donadei, S.; et al. Integration von Wind-Wasserstoff-Systemen in Das Energiesystem—Abschlussbericht (Final Report); PLANET: Essen, Germany; fh lübeck Projekt-GmbH: Lübeck, Germany; Fraunhofer ISI: Karlsruhe, Germany; IFEU: Heidelberg, Germany; KBB: Bannewitz, Germany, 2014. [Google Scholar]

- Zivar, D.; Kumar, S.; Foroozesh, J. Underground Hydrogen Storage: A Comprehensive Review. Int. J. Hydrog. Energy 2021, 46, 23436–23462. [Google Scholar] [CrossRef]

- Thema, M.; Bauer, F.; Sterner, M. Power-to-Gas: Electrolysis and Methanation Status Review. Renew. Sustain. Energy Rev. 2019, 112, 775–787. [Google Scholar] [CrossRef]

- Gorre, J.; Ruoss, F.; Karjunen, H.; Schaffert, J.; Tynjälä, T. Cost Benefits of Optimizing Hydrogen Storage and Methanation Capacities for Power-to-Gas Plants in Dynamic Operation. Appl. Energy 2020, 257, 113967. [Google Scholar] [CrossRef]

- Commission of the European Union, Joint Research Centre, Institute for Energy and Transport. The JRC-EU-TIMES Model: Bioenergy Potentials for EU and Neighbouring Countries; European Union: Luxembourg, 2015. [Google Scholar] [CrossRef]

- Scholz, Y. Renewable Energy Based Electricity Supply at Low Costs: Development of the REMix Model and Application for Europe. Ph.D. Thesis, University of Stuttgart, Stuttgart, Germany, 2012. [Google Scholar] [CrossRef]

- Monitoring Report 2020; Bundesnetzagentur für Elektrizität, Gas, Telekommunikation, Post und Eisenbahnen: Bonn, Germany; Bundeskartellamt: Bonn, Germany, 2021; p. 503.

- StromStG 1999: Stromsteuergesetz Vom 24. März 1999 (BGBl. I S. 378; 2000 I S. 147), Das Zuletzt Durch Artikel 207 Der Verordnung Vom 19. Juni 2020 (BGBl. I S. 1328) Geändert Worden Ist. 1999. Available online: http://www.gesetze-im-internet.de/stromstg/ (accessed on 1 February 2022).

- KWKG 2005: Kraft-Wärme-Kopplungsgesetz Vom 21. Dezember 2015 (BGBl. I S. 2498), Das Zuletzt Durch Artikel 7 Des Gesetzes Vom 8. August 2020 (BGBl. I S. 1818) Geändert Worden Ist. 2015. Available online: http://www.gesetze-im-internet.de/kwkg_2016/ (accessed on 1 February 2022).

- Husarek, D.; Schmugge, J.; Niessen, S. Hydrogen Supply Chain Scenarios for the Decarbonisation of a German Multi-Modal Energy System. Int. J. Hydrog. Energy 2021, 46, 38008–38025. [Google Scholar] [CrossRef]

- Cerniauskas, S.; Jose Chavez Junco, A.; Grube, T.; Robinius, M.; Stolten, D. Options of Natural Gas Pipeline Reassignment for Hydrogen: Cost Assessment for a Germany Case Study. Int. J. Hydrog. Energy 2020, 45, 12095–12107. [Google Scholar] [CrossRef] [Green Version]

- Van Leeuwen, R.P. Towards 100% Renewable Energy Supply for Urban Areas and the Role of Smart Control. Ph.D. Thesis, University of Twente, Enschede, The Netherlands, 2017. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Fuel | 2020 | 2030 | 2040 | 2050 |

|---|---|---|---|---|

| Natural gas | 38.4 | 41.0 | 43.2 | 42.1 |

| Hard coal | 15.1 | 16.2 | 17.3 | 20.5 |

| Lignite | 4.1 | 4.1 | 4.1 | 4.1 |

| Uranium | 3.2 | 3.2 | 3.2 | 3.2 |

| Oil | 58.3 | 60.5 | 65.9 | 71.3 |

| Biogas | 28.1 | 28.1 | 28.1 | 28.1 |

| Solid biomass | 26.9 | 26.9 | 26.9 | 26.9 |

| Scenario | 2020 | 2030 | 2040 | 2050 |

|---|---|---|---|---|

| Emission cost in €/t CO2 | 32 | 94 | 154 | 216 |

| Country | 2020 Conv. | 2050 Conv. | 2050 BEV | 2050 H2 | 2050 HP | 2050 E-H |

|---|---|---|---|---|---|---|

| Germany | 428 | 344 | 145 | 423 | 70 | 159 |

| Austria | 72 | 47 | 12 | 10 | 4 | 3 |

| Belgium | 91 | 67 | 16 | 15 | 9 | 5 |

| Czech Republic | 67 | 41 | 10 | 10 | 4 | 4 |

| Denmark (East) | 14 | 8 | 3 | 3 | 1 | 0.6 |

| Denmark (West) | 23 | 13 | 5 | 5 | 2 | 1 |

| France | 486 | 380 | 99 | 90 | 36 | 6 |

| Italy | 325 | 284 | 84 | 77 | 17 | 12 |

| Luxembourg | 7 | 4 | 1 | 0.5 | 0.3 | 0.2 |

| Netherlands | 115 | 93 | 19 | 17 | 11 | 7 |

| Norway | 131 | 84 | 8 | 7 | 2 | 0.6 |

| Poland | 161 | 79 | 34 | 29 | 9 | 7 |

| Sweden | 146 | 91 | 16 | 15 | 6 | 5 |

| Switzerland | 64 | 49 | 10 | 10 | 4 | 2 |

| Total | 2129 | 1582 | 463 | 709 | 174 | 212 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schaffert, J.; Gils, H.C.; Fette, M.; Gardian, H.; Brandstätt, C.; Pregger, T.; Brücken, N.; Tali, E.; Fiebrandt, M.; Albus, R.; et al. Integrating System and Operator Perspectives for the Evaluation of Power-to-Gas Plants in the Future German Energy System. Energies 2022, 15, 1174. https://doi.org/10.3390/en15031174

Schaffert J, Gils HC, Fette M, Gardian H, Brandstätt C, Pregger T, Brücken N, Tali E, Fiebrandt M, Albus R, et al. Integrating System and Operator Perspectives for the Evaluation of Power-to-Gas Plants in the Future German Energy System. Energies. 2022; 15(3):1174. https://doi.org/10.3390/en15031174

Chicago/Turabian StyleSchaffert, Johannes, Hans Christian Gils, Max Fette, Hedda Gardian, Christine Brandstätt, Thomas Pregger, Nils Brücken, Eren Tali, Marc Fiebrandt, Rolf Albus, and et al. 2022. "Integrating System and Operator Perspectives for the Evaluation of Power-to-Gas Plants in the Future German Energy System" Energies 15, no. 3: 1174. https://doi.org/10.3390/en15031174

APA StyleSchaffert, J., Gils, H. C., Fette, M., Gardian, H., Brandstätt, C., Pregger, T., Brücken, N., Tali, E., Fiebrandt, M., Albus, R., & Burmeister, F. (2022). Integrating System and Operator Perspectives for the Evaluation of Power-to-Gas Plants in the Future German Energy System. Energies, 15(3), 1174. https://doi.org/10.3390/en15031174