1. Introduction

The “2015 Paris Climate Conference (COP21)” put finance at the heart of the zero-emission scenario on environmental deprivation. Accordingly, global leaders have intended to scale up the “so-called green finance initiatives” to invest in low-carbon infrastructure and innovations [

1]. For instance: the “burgeoning market for green bonds” (which finances projects that are less energy intensive and are friendly to the environment). The other initiatives entail the creation of a new development bank and forming a “green-credit department” at ICBC-China, the world’s biggest bank. These initiatives revealed the critical role of the development of the banking sector in the fight against ecological deprivation. However, to date, no empirical study that studied the link between banking sector development and ecological footprint in a panel context.

On the other hand, some scholars have narrowed it down by studying the consequences of FD (financial development) on the environment [

2,

3,

4,

5,

6,

7]. At this point, we beg to ask the question, are well-developed banking sectors harmful or beneficial to environmental sustainability? It is reasonable to believe that a flourishing banking industry will result in more investment and production of fossil fuels (non-renewable energy sources) in an unregulated sector, thus increasing environmental deprivation. Furthermore, the development of banking can also trigger ecological disasters since the financial market promotes economic expansion, enabling households to buy homes, cars, and appliances. These activities pressure the environment through the non-renewable energy demand and consumption channel [

8].

Furthermore, the banking sector promotes industrialization by financing new factories and plants, which can trigger more water toxins and ecological deprivation [

9]. However, banking development may promote a quality environment: a well-functioning financial market may promote and finance intensive investments in R&D and eco-friendly ventures [

10,

11]. Vis-à-vis, banks may increase lending to high-polluting sectors; this transition may incentivize corporations to shift to green innovations.

Furthermore, the environmental social and governance (ESG) classification and incentives may induce firms to embrace less energy-intensive ventures, thus improving air quality. Therefore, a better understanding of the link between the banking sector and the environment is critical because “global transition to a low-carbon economy will need to be funded by the private financial sector if international climate goals are to be met on time” [

12]. Therefore, the intuition on the effects of banks on the environment is of utmost importance to assist authorities in gauging the ability of banking sector shocks to reduce pollution. Based on these two conflicting channels via which the banking sector may augment or decline ecological deprivation, as discussed above, the authors are motivated to investigate the potential effect of the banking sector on ecological footprint.

On the other hand, OECD economies have doubled their effect to accelerate renewable energy to abate unprecedented ecological degradation. In this sense, the OECD embraced the “technology push proposal Mission Innovation”, “announced in November 2015 at the United Nations Framework Convention on Climate Change’s 21st session of the Conference of the Parties”. The initiative aims to acutely augment public and private global renewable energy technology to tackle global warming, ensure relatively cheaper clean energy to consumers, and produce an avenue for commercial clean energy. This initiative has induced OECD nations to double their respective clean energy R&D (research and development) investments over the next five years [

13].

Based on the arguments above, the authors are motivated to examine the link between baking development, renewable energy, and ecological footprint in OECD economies. Thus, the paper makes the following contributions: first, it is the first article to examine the effect of the banking sector on the ecological footprint in OECD countries. The OECD members are chosen based on the following: The OECD members are one of the main drivers of global warming, contributing about 35% of worldwide CO

2 emissions [

14]. Furthermore, they account for over 18% and 65% of the worldwide population and GDP, respectively [

15]. Although the OECD has signed the 2015 Paris agreement, they are still heavily dependent on fossil fuels accounting for 80% of their total energy use.

Moreover, OECD nations recorded per capita emissions of 8.9 tons in 2018, whereas the rest of the globe has 4.3 tons [

16]. Thus, pollution cannot be curbed without the OECD countries. Second, few articles concentrated on the effect of the banking sector on CO

2 emissions [

17] but focused on country-specific. However, to bridge this gap, we use footprint ecological as a broader proxy of the environment, which incorporates diverse scopes of indicators affecting the environment entailing “built-up land, forest land, carbon footprint, grazing land, cropland, and ocean” unlike CO

2 emissions which measure only air pollution. Thirdly, the present work used panel Methods of Moments Quantile Analysis from 1990 to 2018. Finally, examining this relationship in the OECD nations provides new and substantial proof to help authorities benchmark and develop appropriate initiatives to combat ecological deprivation.

The residual of this paper is as follows: Following the data and models in part three, the second portion introduces an exhaustive literature study. Then, following the conclusion and policy implications in the final part, the empirical data and discussion are provided in

Section 4.

3. Empirical Methodology

The current study deals with the empirical effects of banking development, renewable energy consumption, and economic growth, quadratic term of economic growth on the ecological footprint in 27 OECD countries from 1990 to 2018. The data were obtained from world bank development indicators and the global footprint network. We use ecological footprint as a more comprehensive proxy of ecological sustainability, which incorporates diverse scopes of indicators affecting the environment, such as “built-up land, forest land, carbon footprint, grazing land, cropland, and ocean”. Thus, a decline in ecological footprint will signify a reduction in ecological sustainability. All the variables were transformed into their natural logarithmic form as formulated below:

In Equations (1) and (2), where

.

denotes log of ecological footprint,

is the log of banking development,

is economic growth,

is the log of the squared term of economic growth and

is the log of renewable energy utilization. The description of the variables and the sample OECD countries are shown in

Table 1 and

Table 2 below:

3.1. Parameter Estimation Using AMG and CCEMG Approach

The study used the augmented mean group (AMG) assessment proposed by [

55,

56] and the common correlated effects mean group (CCEMG) method as suggested by [

57] to assess the long run among the tested variables. The AMG tackles two main concerns of panel analysis (CD and heterogeneity) [

58]. Moreover, the AMG also provides specified cross-sectional estimation parameters. The CCEMG also possesses similar merits and provides robust results for non-stationary series [

59]. The manner they handle CD is the key difference between these two estimators. The AMG has annual dummy variables whilst the CCEMG has unobserved common factors that are proxied by averages (cross-sectional average) to tackle CD. Equation (2) is the CCE (Common Correlated Effects), and Equations (3) and (4) denote the CCEMG is estimated by taking the average of individual CCE results.

where

.

where

, and

is the error-term of stage (i) and stage (ii).

stands for cross-sectional group-specific AMG estimations.

3.2. Distributional Heterogeneity Analysis Using MMQR Approach

Due to limitations in the mentioned testing models, the MMQR (Method of Moments-Quantile-Regression) propounded by [

60] is applied to evaluate the heterogeneous and distributional impacts across each quintile in the tested model. This approach helps uncover the covariance impacts under conditional heterogeneity as a primary determinant the energy consumption. In addition, the MMQR approach allows the individual effects to influence the whole distribution.

The location-scale variant of various quantiles estimates

τ|

X is formulated as below:

The probability and parameters

are to be measured. The

signifies discrete, and the fixed effect is captured by

is K-vector examined components of

X, which are differentiable transformations formulated based on cross-sections and across time

is identically and separately disposed of across fixed

) and time (

).

represents distributed fixed cross-sections and via time (

t), and it is orthogonal to

it is also standardized to accomplish the moment conditions. This is formulated and presented as follows:

Symbolizes vectors of the regressors that augmented

In,

In,

InEG2.

TX symbolizes the quantile allocation of the

.

represents the coefficient of scalar, which is significant for the

. Unlike the statistical “fixed least-squares” outcomes. The discrete impact indicates no intercept shift. The

is represented by

which is formulated in the following equation.

To assess the causal linkage among the focused variables, the present research utilized Dumitrescu and Hurlin causality test [

61]. In this test, the non-homogeneous causality hypothesis

is compared by two options: The first categorizes the interlink among two variables that have significant causal interlink, while the second is estimated by two examined variables with no important causal linkage.

5. Discussion of Findings

This paper aims to assess the consequences of banking and economic expansion and renewable energy consumption on the ecological footprint of 27 OECD countries spanning data from 1990 to 2018. The findings of the “CCEMG and AMG” tests illustrated that REC negatively and significantly affects EF. The findings demonstrated that growth in REC led to a decline in the ecological footprint in OECD. The finding coincides with [

17], who investigated the relationship in South Africa.

However, banking development positively and significantly affects the ecological footprint in OECD economies, revealing that an increase in banking development raises the level of ecological deprivation in OECD economies. According to [

67], banks produce more than 700 times of carbon emissions from their loan portfolios than their offices. Moreover, banks provide loans for businesses that may invest in the production of fossil fuel-related activities (non-renewable energy sources) and new factories and plants, especially in an unregulated sector, thus increasing environmental deprivation. Similarly, the development of banking can also trigger ecological disasters via financing household purchases such as cars and other hazardous appliances. These activities pressure the environment through the non-renewable energy demand and consumption channel [

8].

In addition, the analysis showed that economic growth has a detrimental effect on ecological quality. This evidence is in line with the study of [

47], who established a positive association between economic expansion and ecological deprivation in the case of OECD nations. This finding can be attributed to the fact that most OECD countries are fossil fuel-dependent nations and an increase in economic expansion augments energy utilization, which in turn triggers high ecological pollution and deprivation. Similarly, most OECD countries lack the resources to embrace green technologies; as such, their existing technologies are obsolete in abating ecological deprivation. However, the quadratic term of economic growth was found to enhance ecological sustainability, thus validating the EKC hypothesis. This suggests that in the initial phases of economic expansion (scale effect), pollutions increase due to high energy demand, leading to declining ecological quality. Eventually, economic growth reaches a turning point in the second phase called the composition effect, in which production processes are transformed from the agricultural and industrial sectors to the service sector. This transformation promotes ecological sustainability due energy efficient technologies. This finding affirmed the study of [

48], who established a U-shaped relationship in the case of 17 European OECD nations, and [

49], who also affirmed the validity of a U-shaped link between income and the environment in 24 OECD countries.

The findings of the MMQR also demonstrated that REC improves ecological quality in OECD economies. It revealed that the effect of REC increased from 0.471 in the first quantile to 0.714 in the ninth quantile. For all quantiles (1 to 9), the findings clearly show an upsurge in ecological footprint because REC is an important factor in improving the environmental quality in OECD economies. This result can be explained by the fact that an increase in investment in green energy sources leads to a decrease in the consumption of fossil fuel sources, which eventually promotes environmental quality by decreasing the negative influence of fossil fuel pollution on the environment. Moreover, oil prices are considered one of the main triggers of economic expansion and energy use at the detriment of ecological quality [

67]. Thus, the unprecedented rising oil prices and declining cost of wind and solar energy might result in switching to cheaper and cleaner energy substitutes, thereby triggering a potential reduction in ecological risk.

On the other hand, banking sector development positively affected the level of environmental pollution in these economies in all the quantiles. The outcomes demonstrated that increased banking development is detrimental to the environment. Likewise, economic expansion positively influences increasing environmental pollution in OECD economies. The findings indicated an upsurge in ecological footprint is triggered by an increase in economic growth from 1.3245 in the first quantile to 1.089 in the ninth quantile. Finally, as suggested by [

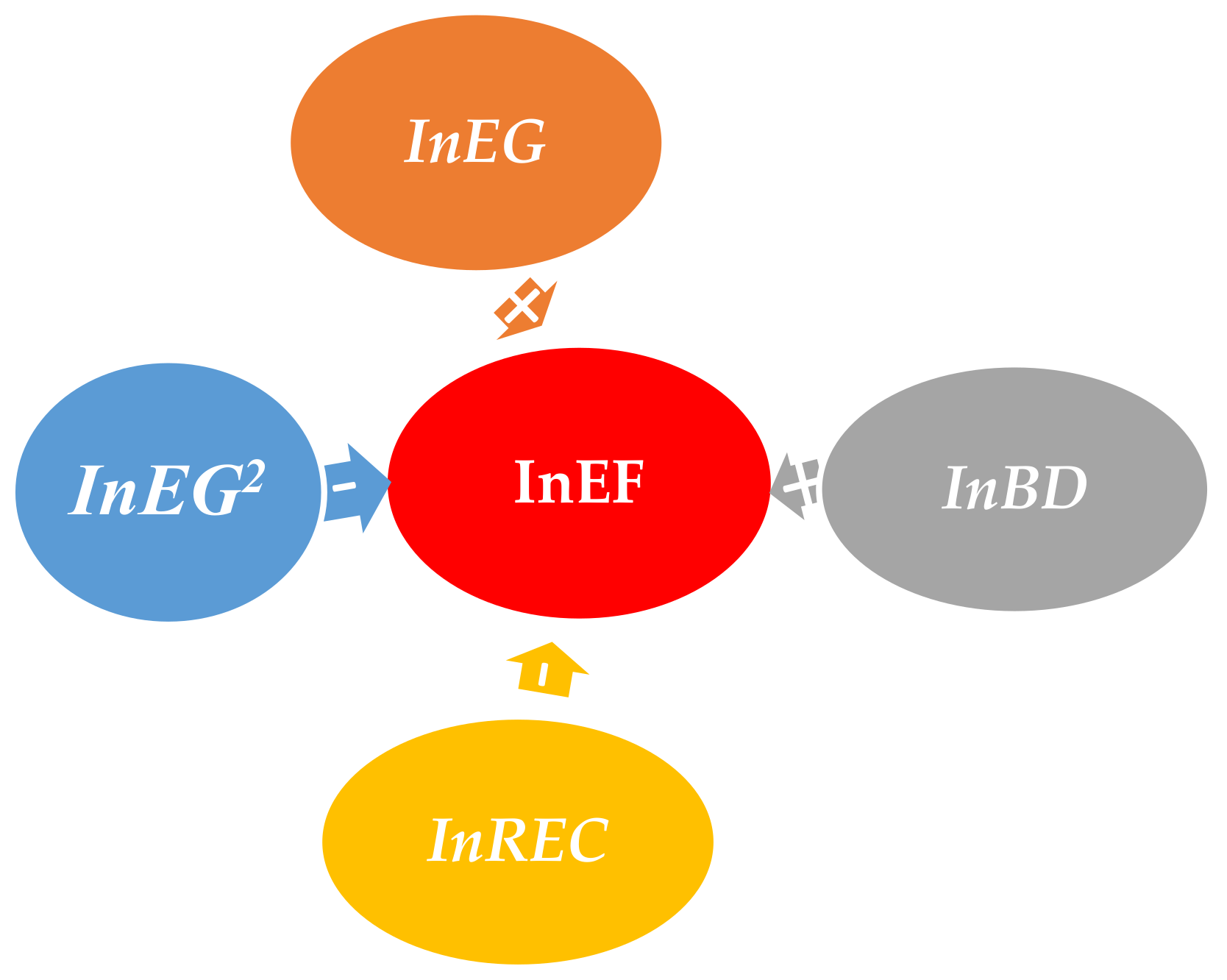

61], the heterogeneous causality testing approach is unitized to assess the causality between the focused variables. The outcome of this is a unidirectional causality moving from InEG, InEG

2, InREC, and InBD, to InEF. However, the study suggests that the banking sector has an influential role in promoting environmental quality by monitoring those corporations which accept funds from the banking sector to ensure ecologically friendly investments. The corporations that fail to abide by ecological standards and cause ecological pollution must be fined based on “environmental corporate social responsibility” and by increasing the interest rate allocated on such loans. Furthermore, the policymaker in OECD must promote the clean energy sector to promote energy efficiency and ecological sustainability.

6. Conclusions & Policy Implications

The OECD economies rely heavily on fossil fuels as their major power source, which has increased their environmental pollution over the past decades. On the other hand, the banking development in these economies has improved significantly over the last decades. The “2015 Paris Climate Conference (COP21)” put finance at the heart of the zero-emission scenario on environmental deprivation. Global leaders have intended to scale up the “so-called green finance initiatives” to invest in low-carbon infrastructure and innovations [

1]. Are well-developed banking sectors harmful or beneficial to environmental quality? In this context, the paper investigated the effect of banking sector development and renewable energy on ecological footprint from 1990 to 2018 using moment quantile regression and the cointegration panel regressions (CCEMG and AMG). Through advanced quintile panel techniques, the empirical findings showed that a 1% surge in banking expansion is projected to augment EF across all quantiles (first to ninth).

Similarly, the findings showed % increase in economic growth is projected to increase ecological footprint across all quantiles (first to ninth). These results confirmed that banking development and economic growth dampen ecological sustainability in the OECD nations. In contrast, the empirical findings showed that a 1% surge in REC is projected to decline ecological deprivation across all quantiles (first to ninth). These results affirmed the positive influence of renewable energy on ecological sustainability in the OECD nations.

Having noted the banking sector in these countries was found to exhibit a detrimental effect on the environment, it is important to note that the banking sector has great potential in facilitating the pathway to low carbon emission. Banking development may promote a quality environment by financing intensive investments in R&D and eco-friendly ventures [

10,

11]. Vis-à-vis, banks may increase lending to high-polluting sectors; this transition may incentivize corporations to shift to green innovations. This must be supported by a transition plan that guides their customers towards greater sustainability. For this transition to be credible and effective, the Central Banks and regulatory authorities in these economies have to implement and supervise it by continuously assessing the effect of banks on the environment and the vulnerabilities of their portfolio to climate-related risk.

Therefore, policymakers should initiate and facilitate environmental risk capacity development for banks to be able to measure and assess their own risk. Moreover, regulatory authorities should develop a framework incorporating climate-related financial risk into the risk management function of the banks. Thus, this will enable banks to analyze their own carbon footprints and that of potential investors [

68]. Likewise, the Basel Committee on Banking Supervision and Financial Stability Board should develop an international framework and risk matrix on climate-related risk to ensure harmonized policy coordination in abating ecological deprivation. Furthermore, as highlighted by Dasgupta’s Review of the Economics of Biodiversity notes, a significant portion of the responsibility for helping us to shift course will fall on the global financial system [

69,

70,

71,

72]. In light of this, as part of their core mandates, central banks, and regulatory authorities should promote financial innovation in the banking sector to mobilize the required capital to facilitate nature conservation and restoration. For example, this could be by offering green bond investment opportunities to the banks. Moreover, policymakers in these economies must use financial initiatives to promote ecological sustainability by providing lower finance costs for green investment. These financial initiatives will increase the productivity of green investment and improve energy efficiency, eventually mitigating the level of environmental pollution in the examined economies.

The lack of data for several studied items beyond 2018 is the main shortcoming of this study. However, the present study provided novel empirical evidence on the link between banking development and ecological pollution for high-emissions economies. Furthermore, the study provided significant implications to the examined economies that are on the way to reducing ecological pollution. Future empirical research should examine how the banking industry affects the degree of ecological sustainability using various panel approaches.

,

,

{kind=link}