Distribution-Level Flexibility Markets—A Review of Trends, Research Projects, Key Stakeholders and Open Questions

Abstract

:1. Introduction and Motivation

1.1. Evolution of the Power Systems

1.2. Why Is Flexibility Needed?

- Intermittent sources penetration,

- Variable fuel prices,

- Environmental concerns,

- Orientation towards new technologies and approaches.

1.3. Paper Contribution and Structure

2. Status in the European Union

3. Overview of the Existing Markets

3.1. General Characteristics

3.2. Example: Denmark

4. Flexibility in General

- Power flexibility,

- Energy flexibility,

- Transfer capacity flexibility,

- Voltage flexibility.

- The energy capacity [MWh] that can be provided continuously,

- The maximum (and minimum) power output [MW],

- The ramp rate [MW/min] to indicate how fast an unit may change its power output.

- Congestion management,

- System balancing,

- Portfolio balancing (by balance responsible parties (BRPs)).

- Market prices (for how much the generated energy will be sold),

- Revenue stream (if there is little curtailment, it can be considered stable) [55].

5. Distribution Level-Markets

5.1. Architectures

- Peer-to-peer (P2P) trading,

- Trading through a mediator,

- Combination of the two previous cases.

5.1.1. Centralized Optimization Models

5.1.2. Auction-Theory Based Models

5.1.3. Simulation Models

5.1.4. Game-Theory Based Models

Cooperative Game Theory

Non-Cooperative Game Theory

5.1.5. What Design to Choose?

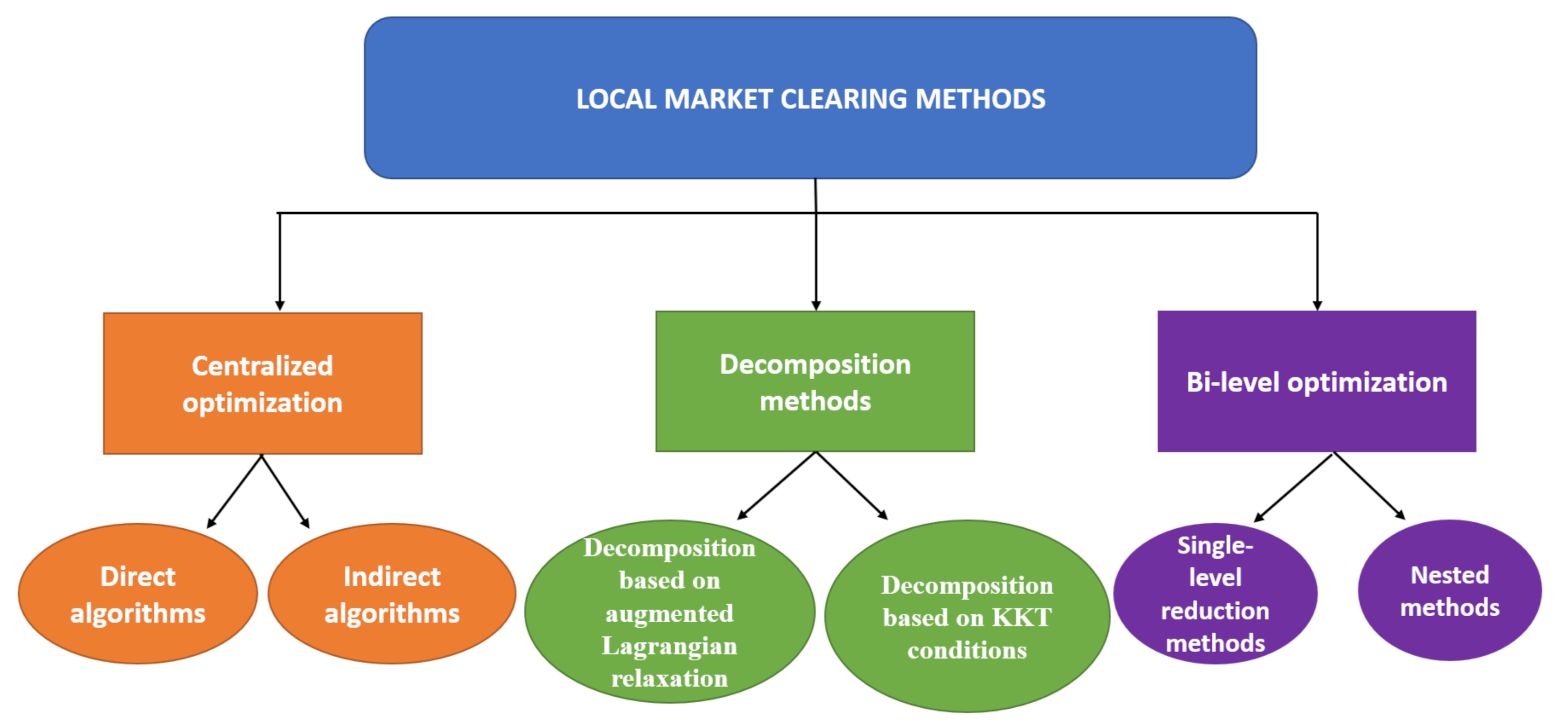

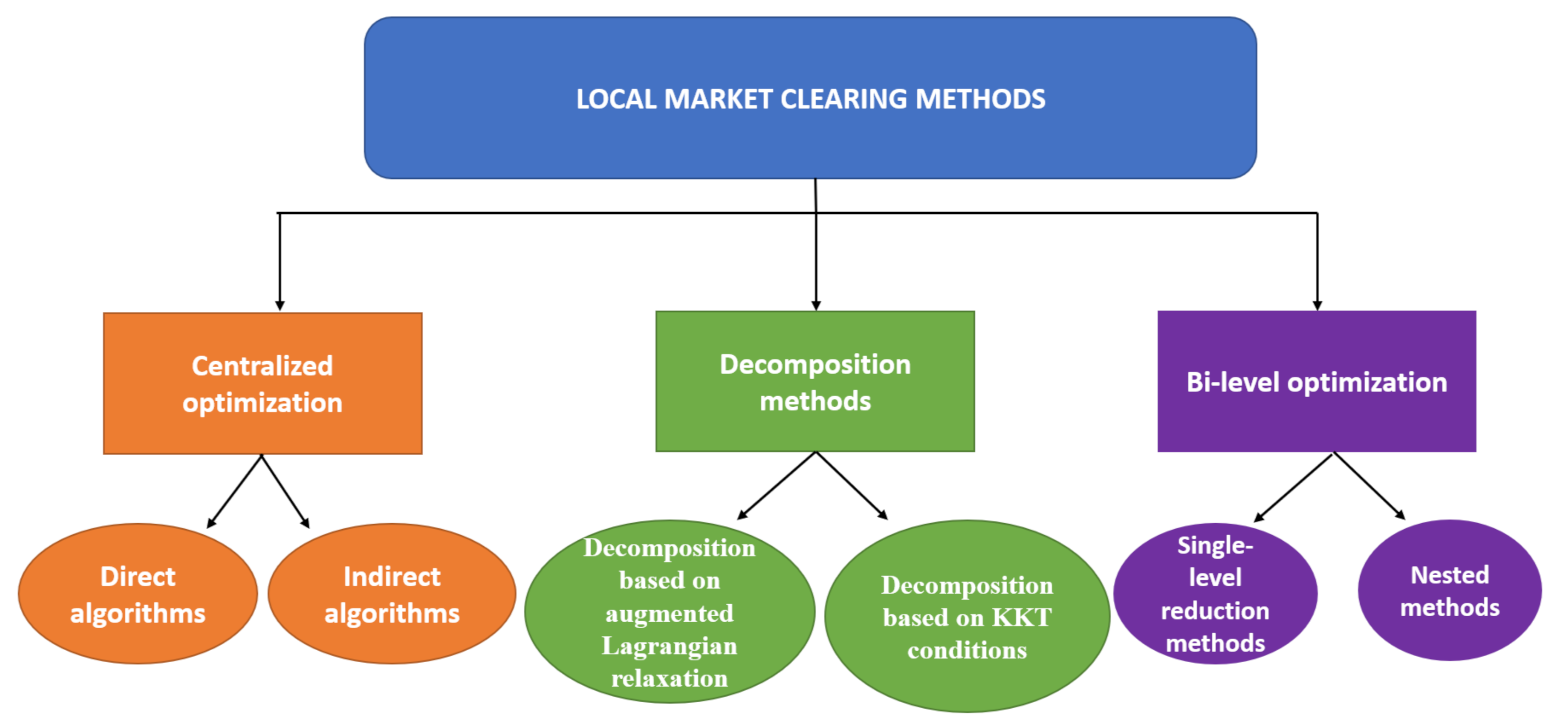

5.2. Market-Clearing Models

5.2.1. Centralized Optimization

5.2.2. Decomposition Methods

5.2.3. Bi-Level Optimization

5.3. Trading Services

- Congestion management,

- Voltage control,

- Support for network planning,

- Phase balancing,

- Support for extreme events,

- Support for planned/unplanned operations.

5.4. Alternatives to the Distribution-Level Markets

- Local flexibility markets,

- Local energy markets,

- Price-based control,

- Transactive energy.

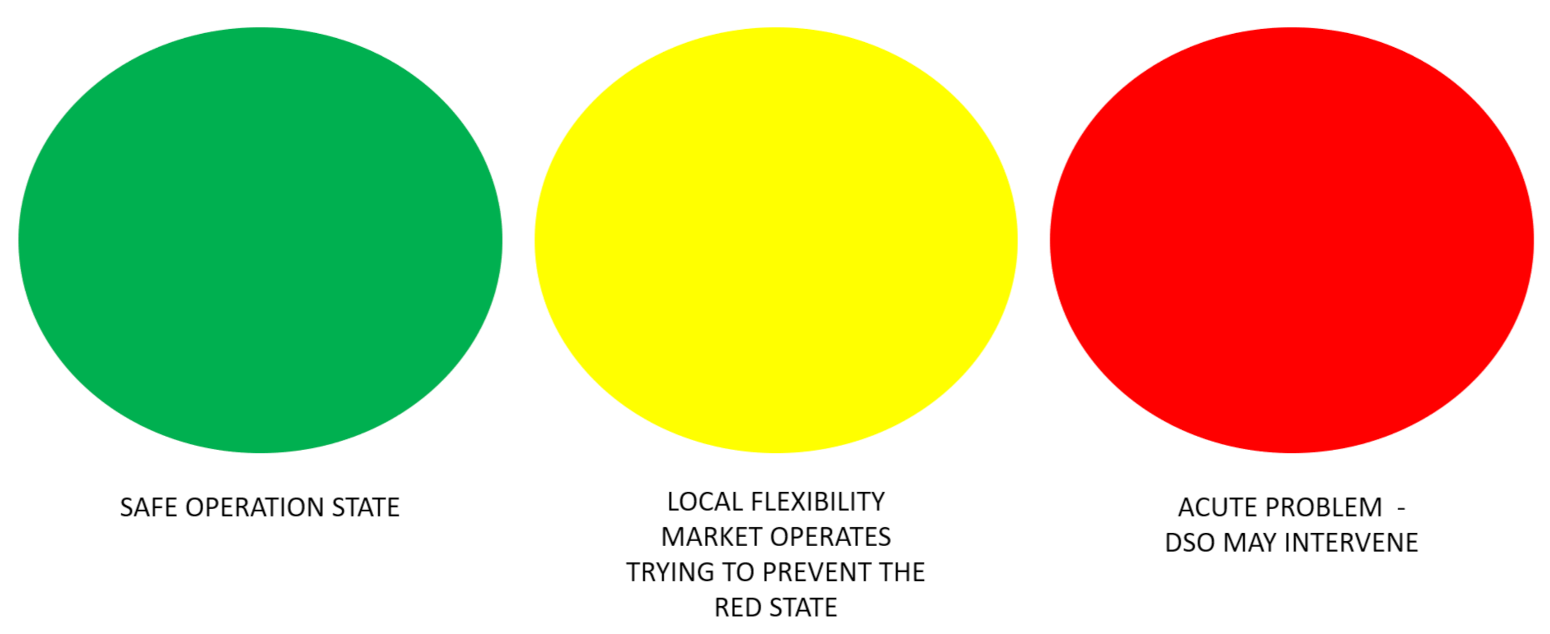

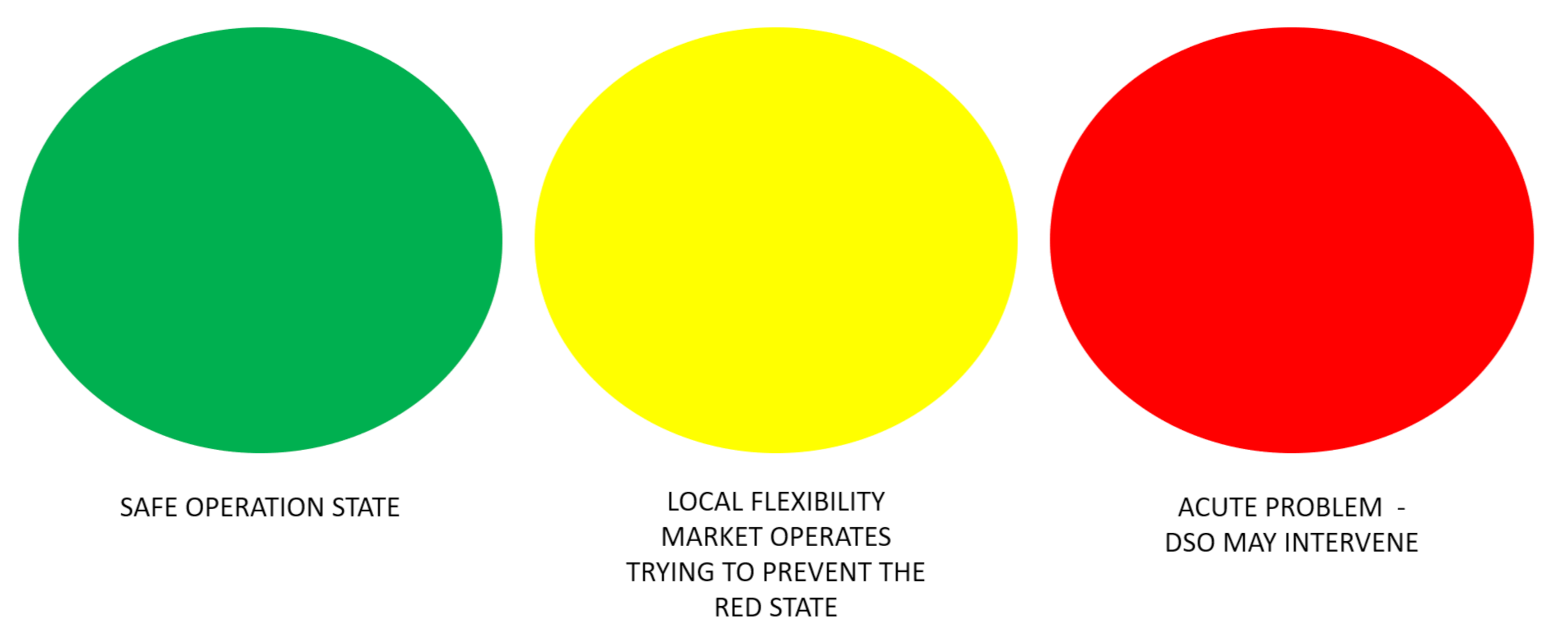

6. Wholesale Meets Local Markets and TSO Faces DSO

- Centralized ancillary services market model,

- Local ancillary services market model,

- Shared balancing responsibility model,

- Common TSO-DSO ancillary services market model,

- Integrated flexibility market model.

6.1. Centralized Ancillary Services Market Model

6.2. Local Ancillary Services Market Model

6.3. Shared Balancing Responsibility Model

- nominations of balance responsible parties taking the energy-only market as a base,

- nominations of balance responsible parties and historical forecasts at each TSO-DSO interconnection point.

6.4. Common TSO-DSO Ancillary Services Market Model

6.5. Integrated Flexibility Market

6.6. Alternative Grouping of TSO-DSO Coordination Mechanisms

7. Research Initiatives and Platforms

7.1. Projects

- local ancillary services real-time market,

- TSO-DSO ancillary services market model.

7.2. Platforms

- Cornwall Local Energy Market [114]

- -

- Owned by centrica and it encompasses the TSO-DSO level

- -

- Pricing method: Pay-as-clear

- Enera [115]

- -

- Owned by TSO, DSOs and EPEX SPOT, and it encompasses the TSO-DSO level

- -

- Pricing method: Pay-as-bid

- GOPACS [116]

- -

- Owned by TSO and DSOs and it encompasses the TSO-DSO level

- -

- Pricing method: Pay-as-bid

- NODES [117]

- -

- Owned by power exchange (NordPool) and encompasses the TSO-DSO level

- -

- Pricing method: Pay-as-bid

- Piclo Flex [118]

- -

- Owned by Piclo and encompasses only the DSO level

- -

- Pricing method: Pay-as-bid

- CoordiNet [104]

- -

- Owned by TSOs and DSOs and it encompasses the TSO-DSO level

- -

- Pricing method: Pay-as-bid and Pay-as-clear (depends from case to case)

- INTERRFACE [105]

- -

- The ownership is not yet decided, but the platform will encompass the TSO-DSO level

- -

- Pricing method: Pay-as-bid

- FLEXGRID ATP [98]

- -

- No market stakeholder or grid owner can be a major owner of the FLEXGRID marketplace, ideally it would be fully independent. It is focused on the DSO, but interaction with the is taken into account

- -

- Under development

- InteGrid [106]

- -

- Owned by TSOs and DSOs and encompasses the TSO-DSO level

- -

- Pricing method: Pay-as-bid

- EU-SysFlex [107]

- -

- Owned by TSOs and DSOs and it encompasses the TSO-DSO level

- -

- Pricing method: Pay-as-bid and Pay-as-clear

- GOFLEX [108]

- -

- Owned by smaller DSOs and local energy suppliers and encompasses the TSO-DSO level

- -

- Pricing method: no unambiguous answer

- DRES2Market [109]

- -

- The ownership is not yet decided, but it will encompass only the DSO level

- InterFlex [101]

- -

- Owned by DSOs and encompasses only the DSO level

- EUniversal [110]

- Flexible Power [119]

- sthlmflex [111]

- OneNet [112]

8. Conventions

9. Stakeholders and Role of the FMO

9.1. Prosumers

9.2. Aggregator

9.3. DSO

9.4. Local Flexibility Market Operator

10. Conclusions and Future Work

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| AC | Alternate-current |

| aFRR | automatic Frequency Restoration Reserve |

| BRP | Balance Responsible Party |

| CBA | Cost-Benefit Analysis |

| CCGT | Combined Cycle Gas Turbines |

| CHP | Combined Heat and Power |

| DER | Distributed Energy Resource |

| DSM | Demand Side Management |

| DSO | Distribution System Operator |

| EU | European Union |

| FCR | Frequency Containment Reserve |

| FMO | Flexibility Market Operator |

| HVAC | Heating, Ventilation, Air-Condition |

| KKT | Karush-Kuhn-Tucker |

| LFM | Local Flexibility Market |

| mFRR | manual Frequency Restoration Reserve |

| OPF | Optimal Power Flow |

| P2G | Power to Gas |

| P2P | Peer-to-Peer |

| PV | Photovoltaic |

| RES | Renewable Energy Source |

| TSO | Transmission System Operator |

| UMEI | Universal Market Enabling Interface |

References

- US EPA. Learn about Energy and Its Impact on the Environment. Available online: https://www.epa.gov/energy/learn-about-energy-and-its-impact-environment (accessed on 25 August 2021).

- Ibrahim, M.S.; Dong, W.; Yang, Q. Machine learning driven smart electric power systems: Current trends and new perspectives. Appl. Energy 2020, 272, 115237. [Google Scholar] [CrossRef]

- Thomas, S. Evolution of the Distribution System & the Potential for Distribution-Level Markets: A Primer for State Utility Regulators Association Utility; NARUC: Washington, DC, USA, 2018. [Google Scholar]

- Yeager, K. Evolution of the Smart Distribution Grid. Smart Grid Handbook. 2016, pp. 1–14. Available online: https://onlinelibrary.wiley.com/doi/10.1002/9781118755471.sgd017 (accessed on 29 September 2021).

- Ontario’s Power System. Distributed Energy Resources. Available online: https://www.ieso.ca/en/Learn/Ontario-Power-System/A-Smarter-Grid/Distributed-Energy-Resources (accessed on 25 August 2021).

- Impram, S.; Nese, S.V.; Oral, B. Challenges of renewable energy penetration on power system flexibility: A survey. Energy Strategy Rev. 2020, 31, 100539. [Google Scholar] [CrossRef]

- IEA. Status of Power System Transformation 2019; IEA Publications: Paris, France, 2019; Available online: https://www.iea.org/reports/status-of-power-system-transformation-2019 (accessed on 13 September 2021).

- Lannoye, E. Flexibility in Power Systems. 2010. Available online: http://www.eprg.group.cam.ac.uk/wp-content/uploads/2010/03/Eamonn-Lannoye.pdf (accessed on 25 August 2021).

- Meibner, A.C.; Dreher, A.; Knorr, K.; Vogt, M.; Zarif, H.; Jurgens, L.; Grasenack, M. A co-simulation of flexibility market based congestion management in Northern Germany. In Proceedings of the International Conference on the European Energy Market, Ljubljana, Slovenia, 18–20 September 2019. [Google Scholar]

- Energie Wende. 2021. Available online: https://www.schleswig-holstein.de/DE/Landesregierung/Themen/Energie/Energiewende/Strom/pdf/berichtEngpassmanagement.html (accessed on 25 August 2021).

- Schermeyer, H.; Vergara, C.; Fichtner, W. Renewable energy curtailment: A case study on today’s and tomorrow’s congestion management. Energy Policy 2018, 112, 427–436. [Google Scholar] [CrossRef]

- Electric Power Research Institute. Electric Power System Flexibility–Challenges and Opportunities; Electric Power Research Institute: Palo Alto, CA, USA, 2016; Available online: https://www.naseo.org/Data/Sites/1/flexibility-white-paper.pdf (accessed on 13 September 2021).

- Spiliotis, K.; Gutierrez, A.I.R.; Belmans, R. Demand flexibility versus physical network expansions in distribution grids. Appl. Energy 2016, 182, 613–624. [Google Scholar] [CrossRef]

- European Comission. Proposal for a Directive of the European Parliament and of the 585 Council on Common Rules for the Internal Market in Electricity (Recast); European Comission: Brussels, Belgium, 2016; Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:52016PC0864R(01)&from=EN (accessed on 25 August 2021).

- European Parliament. Regulation (EU) 2019/943 of the European Parliament and of the Council; European Parliament: Brussels, Belgium, 2019; Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32019R0943 (accessed on 25 August 2021).

- European Parliament. Directive (EU) 2019/944 of the European Parliament and of the Council; European Parliament: Brussels, Belgium, 2019; Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32019L0944 (accessed on 25 August 2021).

- Mendicino, L.; Menniti, D.; Pinnarelli, A.; Sorrentino, N.; Vizza, P.; Alberti, C.; Dura, F. DSO flexibility market framework for renewable energy community of nanogrids. Energies 2021, 14, 3460. [Google Scholar] [CrossRef]

- Olivella-Rosell, P.; Lloret-Gallego, P.; Munné-Collado, Í.; Villafafila-Robles, R.; Sumper, A.; Ottessen, S.; Rajasekharan, J.; Bremdal, B.A. Local flexibility market design for aggregators providing multiple flexibility services at distribution network level. Energies 2018, 11, 822. [Google Scholar] [CrossRef] [Green Version]

- Oxford Institute for Energy Studies. The EU “Target Model” for Electricity Markets–Fit for Purpose? Available online: https://www.oxfordenergy.org/publications/the-eu-target-model-for-electricity-markets-fit-for-purpose/ (accessed on 25 August 2021).

- European Parliament–Think Thank, Brussels, Belgium. Available online: https://www.europarl.europa.eu/thinktank/en/document.html?reference=EPRS_BRI(2016)593518 (accessed on 25 August 2021).

- Khajeh, H.; Firoozi, H.; Laaksonen, H.; Shafie-Khah, M. A new local market structure for meeting customer-level flexibility needs. In Proceedings of the SEST 2020–3rd International Conference on Smart Energy Systems and Technologies, Istanbul, Turkey, 7–9 September 2020. [Google Scholar]

- Verbong, G.P.; Beemsterboer, S.; Sengers, F. Smart grids or smart users? Involving users in developing a low carbon electricity economy. Energy Policy 2013, 52, 117–125. [Google Scholar] [CrossRef]

- Gadea, A.; Marinelli, M.; Zecchino, A. A market framework for enabling electric vehicles flexibility procurement at the distribution level considering grid constraints. In Proceedings of the 20th Power Systems Computation Conference, PSCC, Dublin, Ireland, 11–15 June 2018. [Google Scholar]

- Economic Consulting Associates Limited. European Electricity Forward Markets and Hedging Products–State of Play and Elements for Monitoring. Final. Rep. 2015, 4, 1–204. [Google Scholar]

- Ramos, A.; de Jonghe, C.; Gómez, V.; Belmans, R. Realizing the smart grid’s potential: Defining local markets for flexibility. Util. Policy 2016, 40, 26–35. [Google Scholar] [CrossRef]

- Kuiken, D.; Más, H.F. Integrating demand side management into EU electricity distribution system operation: A Dutch example. Energy Policy 2019, 129, 153–160. [Google Scholar] [CrossRef]

- Kirschen, D.S.; Strbac, G. Fundamentals of Power System Economics, 2nd ed.; John Wiley & Sons: Hoboken, NJ, USA, 2018. [Google Scholar]

- Glachant, J.M.; Leveque, F. Electricity Reform in Europe: Towards a Single Energy Market; Florence School of Regulation; Edward Elgar Publishing: Florence, Italy, 2009. [Google Scholar]

- Tierney, S.; Schatzki, T.; Mukerji, R. Uniform-Pricing versus Pay-as-Bid in Wholesale Electricity Markets: Does It Make a Difference? 2007. Available online: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.365.2514&rep=rep1&type=pdf (accessed on 25 August 2021).

- Caprabianca, M.; Falvo, M.C.; Papi, L.; Promutico, l.; Rossetti, V.; Quaglia, F. Replacement Reserve for the Italian Power System and Electricity Market. Energies 2020, 13, 2916. [Google Scholar] [CrossRef]

- Nord Pool Group. Lysaker, Norway. Available online: https://www.nordpoolgroup.com/ (accessed on 25 August 2021).

- Wind Energy. Power Markets. Available online: https://www.wind-energy-the-facts.org/power-markets.html (accessed on 25 August 2021).

- Holm, T.B. The Future Importance of Short Term Markets: An Analyse of Intraday Prices in the Nordic Intraday Market. Elbas. 2017. Available online: https://nmbu.brage.unit.no/nmbu-xmlui/handle/11250/2468078 (accessed on 25 August 2021).

- Energinet. Denmark. Available online: https://energinet.dk/ (accessed on 25 August 2021).

- Zegers, E.H.A.; Herndler, B.; Wong, S.; Pompee, J.; Bourmaud, J.Y.; Lehnhoff, S. Power Transmission & Distribution Systems Flexibility Needs in the Future Power System; Discussion Paper; ISGAN: Paris, France, 2019. [Google Scholar]

- Makarov, Y.V.; Loutan, C.; Ma, J.; de Mello, P. Operational impacts of wind generation on California power systems. IEEE Trans. Power Syst. 2009, 24, 1039–1050. [Google Scholar] [CrossRef]

- Dvorkin, Y.; Kirschen, D.S.; Ortega-Vazquez, M.A. Assessing flexibility requirements in power systems. IET Gener. Transm. Distrib. 2014, 8, 1820–1830. [Google Scholar] [CrossRef]

- Kirschen, D.S.; Rosso, A.; Ma, J.; Ochoa, L.F. Flexibility from the demand side. In Proceedings of the IEEE Power and Energy Society General Meeting, San Diego, CA, USA, 22–26 July 2012. [Google Scholar]

- Paterakis, N.G.; Erdinç, O.; Catalão, J.P. An overview of Demand Response: Key-elements and international experience. Renew. Sustain. Energy Rev. 2017, 69, 871–891. [Google Scholar] [CrossRef]

- Prognos, A.G. Berlin, Germany Flexibility in Thermal Power Plants. 2017. Available online: www.agora-energiewende.de%2Ffileadmin%2FProjekte%2F2017%2FFlexibility_in_thermal_plants%2F115_flexibility-report-WEB.pdf&clen=5012993&chunk=true (accessed on 25 August 2021).

- Nuclear Energy Agency. Technical and Economic Aspects of Load Following with Nuclear Power Plants; Nuclear Energy Agency: Paris, France, 2011. [Google Scholar]

- Deane, J.; Gallachóir, B.Ó.; McKeogh, E. Techno-economic review of existing and new pumped hydro energy storage plant. Renew. Sustain. Energy Rev. 2010, 14, 1293–1302. [Google Scholar] [CrossRef]

- COGEN Europe. What Is Cogen; COGEN Europe: Brussels, Belgium, 2021; Available online: https://www.cogeneurope.eu/knowledge-centre/what-is-cogeneration (accessed on 25 August 2021).

- IPIECA. Combined Cycle Gas Turbines; IPIECA: London, UK, 2013; Available online: https://www.ipieca.org/resources/energy-efficiency-solutions/power-and-heat-generation/combined-cycle-gas-turbines/ (accessed on 25 August 2021).

- Wulf, C.; Linssen, J.; Zapp, P. Power-to-gas-concepts, demonstration, and prospects. In Hydrogen Supply Chain: Design, Deployment and Operation; Academic Press: Cambridge, MA, USA, 2018. [Google Scholar]

- U.S. Department of Energy. Heat Pump Systems; U.S. Department of Energy: Washington DC, USA, 2021. Available online: https://www.energy.gov/energysaver/heat-pump-systems (accessed on 25 August 2021).

- Franco, A.; Miserocchi, L.; Testi, D. HVAC Energy Saving Strategies for Public Buildings Based on Heat Pumps and Demand Controlled Ventilation. Energies 2021, 14, 5541. [Google Scholar] [CrossRef]

- Clean Energy Wire. German Network Operators Plan with Long-Term Bottlenecks in Power Grid; Clean Energy Wire: Berlin, Germany, 2020; Available online: https://www.cleanenergywire.org/news/german-network-operators-plan-long-term-bottlenecks-power-grid (accessed on 25 August 2021).

- ENTSO-E. PowerFacts Europe; ENTSO-E: Brussels, Belgium, 2019. [Google Scholar]

- European Commission. Clean Energy for All Europeans Package; European Commission: Brussels, Belgium, 2019; Available online: https://ec.europa.eu/energy/topics/energy-strategy/clean-energy-all-europeans_en (accessed on 25 August 2021).

- Schittekatte, T.; Meeus, L. Flexibility markets: Q&A with project pioneers. Util. Policy 2020, 63, 101017. [Google Scholar]

- Roos, A. Designing a joint market for procurement of transmission and distribution system services from demand flexibility. Renew. Energy Focus 2017, 21, 16–24. [Google Scholar] [CrossRef]

- Smart Grid Task Force. Regulatory Recommendations for the Deployment of Flexibility; EG3 Report; Smart Grid Task Force: Brussels, Belgium, 2015. [Google Scholar]

- Vallés, M.; Reneses, J.; Cossent, R.; Frías, P. Regulatory and market barriers to the realization of demand response in electricity distribution networks: A European perspective. Electr. Power Syst. Res. 2016, 140, 689–698. [Google Scholar] [CrossRef]

- Miller, M.; Zinaman, O.; Milligan, M.; Arent, D.; Palmintier, B.; Tuohy, A.; Power, N.; Futch, M.; Hirscher, A. Flexibility in 21 st Century Power Systems. Available online: https://www.nrel.gov/docs/fy14osti/61721.pdf (accessed on 25 August 2021).

- Minniti, S.; Hque, N.; Nquyen, P.; Pemen, G. Local markets for flexibility trading: Key stages and enablers. Energies 2018, 11, 3074. [Google Scholar] [CrossRef] [Green Version]

- Bouhouras, A.S.; Christoforidis, G.C.; Parisses, C.; Labridis, D.P. Reducing network congestion in distribution networks with high DG penetration via network reconfiguration. In Proceedings of the 11th International Conference on the European Energy Market, Krakow, Poland, 28–30 May 2014. [Google Scholar]

- Khorasany, M.; Mishra, Y.; Ledwich, G. Market framework for local energy trading: A review of potential designs and market clearing approaches. IET Gener. Transm. Distrib. 2018, 12, 5899–5908. [Google Scholar] [CrossRef] [Green Version]

- Zhang, W.; Wang, X.; Huang, Y.; Qi, S.; Zhao, Z.; Lin, F. A Peer-To-Peer Market Mechanism for Distributed Energy Resources. In Proceedings of the 2019 IEEE Innovative Smart Grid Technologies–Asia (ISGT Asia), Chengdu, China, 21–24 May 2019. [Google Scholar]

- Lüth, A.; Zepter, J.M.; del Granado, P.C.; Egging, R. Local electricity market designs for peer-to-peer trading: The role of battery flexibility. Appl. Energy 2018, 229, 1233–1243. [Google Scholar] [CrossRef] [Green Version]

- Morstyn, T.; Teytelboym, A.; McCulloch, M.D. Designing decentralized markets for distribution system flexibility. IEEE Trans. Power Syst. 2019, 34, 1–12. [Google Scholar] [CrossRef]

- Ilieva, I.; Bremdal, B. Implementing local flexibility markets and the uptake of electric vehicles—The case for Norway. In Proceedings of the 6th IEEE International Energy Conference (ENERGYCon), Gammarth, Tunisia, 28 Sepember–1 October 2020. [Google Scholar]

- Prat, E.; Herre, L.; Kazempour, J.; Chatzivasileiadis, S. Design of a Continuous Local Flexibility Market with Network Constraints. 2020. Available online: https://arxiv.org/abs/2012.00505 (accessed on 25 August 2021).

- Torbaghan, S.S.; Blaauwbroek, N.; Nguyen, P.; Gibescu, M. Local market framework for exploiting flexibility from the end users. In Proceedings of the International Conference on the European Energy Market, Porto, Portugal, 6–9 June 2016. [Google Scholar]

- Köppl, S.; Lang, C.; Bogensperger, A.; Estermann, T.; Zeiselmair, A. Altdorfer Flexmarkt–Decentral flexibility for distribution network. In Proceedings of the ETG-Kongress 2019–Das Gesamtsystem im Fokus der Energiewende, Esslingen, Germany, 8–9 May 2019. [Google Scholar]

- iPower Project. Available online: https://ipower-net.weebly.com/ (accessed on 25 August 2021).

- Heussen, K.; Bondy, D.E.M.; Hu, J.; Gehrke, O.; Hansen, L.H. A clearinghouse concept for distribution-level flexibility services. In Proceedings of the 4th IEEE/PES Innovative Smart Grid Technologies Europe, ISGT Europe, Lyngby, Denmark, 6–9 October 2013. [Google Scholar]

- Khomami, H.P.; Fonteijn, R.; Geelen, D. Flexibility market design for congestion management in smart distribution grids: The dutch demonstration of the interflex project. In Proceedings of the IEEE PES Innovative Smart Grid Technologies Conference Europe, The Hague, The Netherlands, 26–28 October 2020. [Google Scholar]

- Jin, X.; Qu, Q.; Jia, H. Local flexibility markets: Literature review on concepts, models and clearing methods. Appl. Energy 2020, 261, 114387. [Google Scholar] [CrossRef] [Green Version]

- Siebers, P.O.; Aickelin, U. Introduction to Multi-Agent Simulation; School of Computer Science IT, University of Nottingham: Nottingham, UK, 2021; Available online: https://arxiv.org/pdf/0803.3905 (accessed on 14 September 2021).

- Sensfuß, F.; Ragwitz, M.; Genoese, M.; Möst, D. Agent-Based Simulation of Electricity Markets—A Literature Review. Working Paper Sustainability and Innovation. Available online: https://www.econstor.eu/bitstream/10419/28520/1/570113083.pdf (accessed on 14 September 2021).

- Shiflet, A.B.; Shiflet, G.W. An introduction to agent-based modeling for undergraduates. Procedia Comput. Sci. 2014, 29, 1392–1402. [Google Scholar] [CrossRef] [Green Version]

- Stanford Encyclopedia of Philosophy. Available online: https://plato.stanford.edu/entries/game-theory/ (accessed on 16 September 2021).

- Churkin, A.; Bialek, J.; Pozo, D.; Sauma, E.; Korgin, N. Review of Cooperative Game Theory applications in power system expansion planning. Renew. Sustain. Energy Rev. 2021, 145, 111056. [Google Scholar] [CrossRef]

- Kristiansen, M.; Korpas, M.; Swendsen, H.G. A generic framework for power system flexibility analysis using cooperative game theory. Appl. Energy 2018, 212, 223–232. [Google Scholar] [CrossRef]

- Marzband, M.; Javadi, M.; Dominguez-Garcia, J.L.; Moghaddam, M.M. Non-cooperative game theory based energy management systems for energy district in the retail market considering DER uncertainties. IET Gener. Transm. Distrib. 2016, 10, 2999–3009. [Google Scholar] [CrossRef] [Green Version]

- Haghifam, S.; Zare, K.; Abapour, M.; Munoz-Delgado, G.; Contreras, J. A Stackelberg Game-Based Approach for Transactive Energy Management in Smart Distribution Networks. Energies 2020, 13, 3621. [Google Scholar] [CrossRef]

- Bruninx, K.; Pandzic, H.; Cadre, H.L.; Delarue, E. On the Interaction Between Aggregators, Electricity Markets and Residential Demand Response Providers. IEEE Trans. Power Syst. 2019, 35, 840–853. [Google Scholar] [CrossRef]

- Gurobi Optimization. Available online: http://www.gurobi.com (accessed on 16 September 2021).

- IBM CPLEX Optimizer. Available online: https://www.ibm.com/an (accessed on 16 September 2021).

- IPOPT. Available online: https://coin-or.github.io/Ipopt/ (accessed on 16 September 2021).

- Sinha, A.; Malo, P.; Deb, K. A Review on Bilevel Optimization: From Classical to Evolutionary Approaches and Applications. IEEE Trans. Evol. Comput. 2018, 22, 276–295. [Google Scholar] [CrossRef]

- Silva, R.; Alves, E.; Ferreira, R.; Villar, J.; Gouveia, C. Characterization of TSO and DSO Grid System Services and TSO-DSO Basic Coordination Mechanisms in the Current Decarbonization Context. Energies 2021, 14, 4451. [Google Scholar] [CrossRef]

- EUniversal Consortium. D1.2 EUniversal—Observatory of Research and Demonstration Initiatives on Future Electricity Grids and Markets. 2021. Available online: https://euniversal.eu/wp-content/uploads/2021/02/EUniversal_D1.2.pdf (accessed on 15 September 2021).

- Antic, T.; Capuder, T.; Bolfek, M. A Comprehensive Analysis of the Voltage Unbalance Factor in PV and EV Rich Non-Synthetic Low Voltage Distribution Networks. Energies 2021, 14, 117. [Google Scholar] [CrossRef]

- The GridWise Architecture Council. GridWise Transactive Energy Framework Version. 2015. Available online: http://www.gridwiseac.org/pdfs/te_framework_report_pnnl-22946.pdf (accessed on 16 September 2021).

- Hu, J.; Yang, G.; Ziras, C.; Kok, K. Aggregator Operation in the Balancing Market Through Network-Constrained Transactive Energy. IEEE Trans. Power Syst. 2019, 34, 4071–4080. [Google Scholar] [CrossRef] [Green Version]

- Hu, J.; Yang, G.; Bindner, H.W.; Xue, Y. Application of Network-Constrained Transactive Control to Electric Vehicle Charging for Secure Grid Operation. IEEE Trans. Sustain. Energy 2017, 8, 505–515. [Google Scholar] [CrossRef] [Green Version]

- Bell, K.; Gill, S. Delivering a highly distributed electricity system: Technical, regulatory and policy challenges. Energy Policy 2018, 113, 765–777. [Google Scholar] [CrossRef]

- Givisiez, A.G.; Petrou, K.; Ochoa, L.F. A Review on TSO-DSO Coordination Models and Solution Techniques. Electr. Power Syst. Res. 2020, 189, 106659. [Google Scholar] [CrossRef]

- Moon, H.S.; Yoon, Y.T. Prequalification Scheme of a Distribution System Operator for Supporting Wholesale Market Participation of a Distributed Energy Resource Aggregator. IEEE Access 2021, 9, 80434–80450. [Google Scholar] [CrossRef]

- Iria, J.; Scott, P.; Attarha, A. Network-constrained bidding optimization strategy for aggregators of prosumers. Energy 2020, 207, 118266. [Google Scholar] [CrossRef]

- Gerard, H.; Puente, E.I.R.; Six, D. Coordination between transmission and distribution system operators in the electricity sector: A conceptual framework. Util. Policy 2018, 50, 40–48. [Google Scholar] [CrossRef]

- European Comission. What Is Horizon; European Comission: Brussels, Belgium, 2020; Available online: https://ec.europa.eu/programmes/horizon2020/what-horizon-2020 (accessed on 25 August 2021).

- Smartnet Project. Available online: http://smartnet-project.eu/ (accessed on 25 August 2021).

- Empower Project. Available online: http://empowerh2020.eu/ (accessed on 25 August 2021).

- Invade Project. Available online: https://h2020invade.eu/ (accessed on 25 August 2021).

- FLEXGRID Project. Available online: https://flexgrid-project.eu/ (accessed on 25 August 2021).

- FLEXGRID Project Promo Video. Available online: https://www.youtube.com/watch?v=D7FQXTTD1UE (accessed on 25 August 2021).

- Badanjak, D.; Pandzic, H. Battery Storage Participation in Reactive and Proactive Distribution-Level Flexibility Markets. IEEE Access 2021, 9, 122322–122334. [Google Scholar] [CrossRef]

- Interflex Project. Available online: https://interflex-h2020.com/ (accessed on 25 August 2021).

- Heinrich, C.; Ziras, C.; Syrri, A.L.; Bindner, H.W. EcoGrid 2.0: A large-scale field trial of a local flexibility market. Appl. Energy 2020, 261, 33. [Google Scholar] [CrossRef] [Green Version]

- Zhang, C.; Ding, Y.; Nordentoft, N.C.; Pinson, P.; Østergarrd, J. FLECH: A Danish market solution for DSO congestion management through DER flexibility services. J. Mod. Power Syst. Clean Energy 2014, 2, 126–133. [Google Scholar] [CrossRef] [Green Version]

- The CoordiNet Project. Available online: https://coordinet-project.eu/projects/project (accessed on 25 August 2021).

- Interrface Project. Available online: http://www.interrface.eu/ (accessed on 25 August 2021).

- InteGrid Project. Available online: https://integrid-h2020.eu/ (accessed on 25 August 2021).

- EU-SysFlex Project. Available online: https://eu-sysflex.com/ (accessed on 25 August 2021).

- GOFLEX Project. Available online: https://www.goflex-project.eu (accessed on 25 August 2021).

- DRES2Market Project. Available online: https://www.dres2market.eu/ (accessed on 25 August 2021).

- EUinversal Project. Available online: https://euniversal.eu/ (accessed on 25 August 2021).

- sthlmflex Project. Available online: https://www.svk.se/sthlmflex (accessed on 25 August 2021).

- OneNet Project. Available online: https://onenet-project.eu/ (accessed on 25 August 2021).

- Valarezo, O.; Gómez, T.; Chaves-Avila, J.P.; Lind, L.; Correa, M.; Ziegler, D.U.; Escobar, R. Analysis of new flexibility market models in Europe. Energies 2021, 14, 3521. [Google Scholar] [CrossRef]

- Cornwall Local Energy Market Project. Available online: https://www.centrica.com/innovation/cornwall-local-energy-market (accessed on 25 August 2021).

- Enera Project. Available online: https://projekt-enera.de/ (accessed on 25 August 2021).

- GOPACS Project. Available online: https://en.gopacs.eu/ (accessed on 25 August 2021).

- NODES Project. Available online: https://nodesmarket.com/ (accessed on 25 August 2021).

- Piclo Flex Project. Available online: https://picloflex.com (accessed on 25 August 2021).

- Flexible Power. Available online: https://www.flexiblepower.co.uk/ (accessed on 25 August 2021).

- Corporate Finance Institute. Standardization–Definition. Available online: https://corporatefinanceinstitute.com/resources/knowledge/economics/standardization/ (accessed on 25 August 2021).

- CEDEC; EDSO; Entsoe; Eurelectric; GEODE. TSO–DSO Report an Integrated Approach to Active System Management; Technical Report; GEOD: Brussels, Belgium, 2019. [Google Scholar]

- Li, R.; Wu, Q.; Oren, S.S. Distribution locational marginal pricing for optimal electric vehicle charging management. IEEE Trans. Power Syst. 2014, 29, 203–211. [Google Scholar] [CrossRef] [Green Version]

- Kornrumpf, T.; Meese, J.; Zdrallek, M.; Neusel-Lange, N.; Roch, M. Economic dispatch of flexibility options for Grid services on distribution level. In Proceedings of the 19th Power Systems Computation Conference (PSCC), Genoa, Italy, 20–24 June 2016. [Google Scholar]

- Universal Smart Energy Framework. Available online: https://www.usef.energy/ (accessed on 25 August 2021).

- Backers, A.; Bliek, F.; Broekmans, M.; Groosman, C.; de Heer, H.; van der Laan, M.; de Koning, M.; Nijtmans, J.; Nguyen, P.H.; Sanberg, T.; et al. An introduction to the Universal Smart Energy Framework. Arnhem, The Netherlands. 2014. Available online: https://ec.europa.eu/energy/sites/ener/files/documents/xpert_group3_summary.pdf (accessed on 25 August 2021).

- Esmat, A.; Usaola, J.; Moreno, M. A decentralized local flexibility market considering the uncertainty of demand. Energies 2018, 11, 2078. [Google Scholar] [CrossRef] [Green Version]

- ECRB, Vienna, Austria. Prosumers in the Energy Community. Available online: https://energy-community.org/dam/jcr:abacd12d-283c-492a-8aa4-6da5797d044a/ECRB_prosumers_regulatoryq_framework_032020.pdf (accessed on 25 August 2021).

- Energy Pool. Unlocking energy market flexibility and demand side response. In Proceedings of the CEER Annual Council of European Energy Regulators, Brussels, Belgium, 29 January 2015. [Google Scholar]

- Eid, C.; Codani, P.; Chen, Y.; Perez, Y.; Hakvoort, R. Aggregation of demand side flexibility in a smart grid: A review for European market design. In Proceedings of the International Conference on the European Energy Market, Lisbon, Portugal, 19–22 May 2015. [Google Scholar]

- FLEXITRICITY Project. Available online: https://www.flexitricity.com/ (accessed on 25 August 2021).

- Delaware Vehicle-To-Grid Project. Available online: https://www.greencarreports.com/news/1094990_delaware-vehicle-to-grid-test-lets-electric-cars-sell-power (accessed on 25 August 2021).

- Tiko Energy. Available online: https://tiko.energy/ (accessed on 25 August 2021).

- Equigy Project. Available online: https://equigy.com/ (accessed on 25 August 2021).

- Quartierstrom Project. Available online: https://quartier-strom.ch/index.php/en/homepage/ (accessed on 25 August 2021).

- Repsol Project. Available online: https://www.repsol.com/en/sustainability/circular-economy/our-projects/solmatch/index.cshtml (accessed on 25 August 2021).

- Eurelectric. Active Distribution System Management: A Key Tool for the Smooth Integration of Distributed Generation; Eurelectric: Brussels, Belgium, 2013. [Google Scholar]

- Bouloumpasis, I.; Alavijeh, N.M.; Steen, D.; Le, A.T. Local flexibility market framework for grid support services to distribution networks. Electr. Eng. 2021, 1–19. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Aggregator | Focus Group | Business Model | State |

|---|---|---|---|

| Energy Pool | Large industries and heavy electricity consumers | (1) DR flexibility–load reduction by making optimal decisions for each customer (2) Balancing markets, reserves, capacity and energy markets | France |

| Voltalis | Residential users | (1) Reductions in electric heating devices (2) Balancing markets and DR mechanism for TSO | Great Britain |

| Direct Energy | Pilot phase—users that used the same company as a retailer | Mainly users with water heaters and convector heaters Load-shedding programs | France |

| Flextricity | Large industrial and commercial customers | (1) Generation and load aggregation, (2) DR programs -triad management (3) Participating in the short-term operating reserve | United Kingdom |

| Delaware EV pilot | flexibility service providing Electric Vehicles (EVs) | (1) Vehicle to Grid (V2G) project (2) Frequency regulation | USA |

| Paper | DSO | Aggregator | 3rd Party |

|---|---|---|---|

| Olivella-Rosell et al. [18] | X | ||

| Esmat et al. [126] | X | ||

| Li et al. [122] | X | ||

| Heinrich et al. [102] | X | ||

| Morstyn et al. [61] | X | ||

| Ilieva et al. [62] | X | ||

| Khajeh et al. [21] | X | ||

| Zhang et al. [103] | X | ||

| Torbaghan et al. [64] | X | ||

| Spiliotis et al. [13] | X | ||

| Eid et al. [129] | X | ||

| Ramos et al. [25] | X | X | |

| Heussen et al. [67] | X | ||

| Kornrumpf et al. [123] | X | ||

| Köppl et al. [65] | X | ||

| Ross [52] | X | ||

| Vallés et al. [54] | X |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Badanjak, D.; Pandžić, H. Distribution-Level Flexibility Markets—A Review of Trends, Research Projects, Key Stakeholders and Open Questions. Energies 2021, 14, 6622. https://doi.org/10.3390/en14206622

Badanjak D, Pandžić H. Distribution-Level Flexibility Markets—A Review of Trends, Research Projects, Key Stakeholders and Open Questions. Energies. 2021; 14(20):6622. https://doi.org/10.3390/en14206622

Chicago/Turabian StyleBadanjak, Domagoj, and Hrvoje Pandžić. 2021. "Distribution-Level Flexibility Markets—A Review of Trends, Research Projects, Key Stakeholders and Open Questions" Energies 14, no. 20: 6622. https://doi.org/10.3390/en14206622

APA StyleBadanjak, D., & Pandžić, H. (2021). Distribution-Level Flexibility Markets—A Review of Trends, Research Projects, Key Stakeholders and Open Questions. Energies, 14(20), 6622. https://doi.org/10.3390/en14206622