Towards a More Realistic Cost–Benefit Analysis—Attempting to Integrate Transaction Costs and Energy Efficiency Services

, ,

, ,

Abstract

1. Introduction

2. Materials and Methods

2.1. Review of Literature

- Search costs and information processing (including search costs for providers of energy services): identifying credible information on technologies (e.g., on performance or investment costs), funding schemes, and crafts businesses for installation

- Decision-making costs: (i) deciding whether an investment will be adopted/rejected and (ii) comparing different technology options, i.e., consultation between different decision-making units (e.g., management vs. operating director) on the perceived relative advantage

- Capital costs or costs for having the investment financed: interests for debt-financed investments

- Negotiating costs or costs for negotiating contractual issues: legal disputes due to increasing rents as a result of energy efficiency investments

- Permitting and certification costs, or costs for having measures permitted or certified by an agency/body: filling in a funding application or an application for having a heritage-protected building refurbished

- Costs for collecting energy-related data for verifying the effectiveness of the measure: monitoring meters and processing data

- Realization costs, or costs for monitoring and enforcement to have energy efficiency investments correctly installed: supervision and time taken to receive goods

- Adaptation costs or costs for making proper use of energy efficiency investments: capacity building/trainings and employment of new staff

- Opportunity costs or costs for lost alternative investments: capital or staff used for energy efficiency investment “lost” for alternative decisions such as production increases

2.2. Objectives and Methodological Approach

3. Results

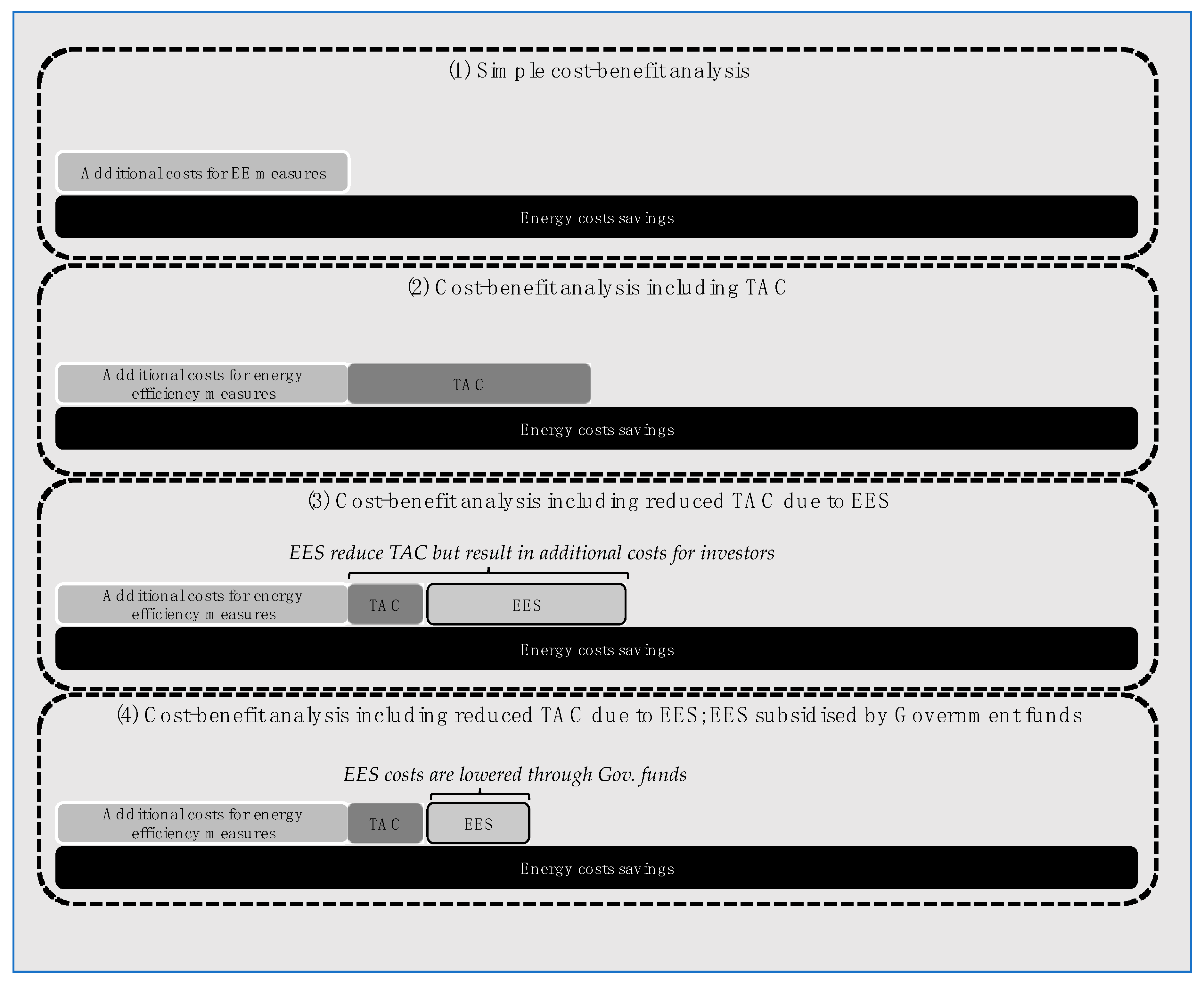

3.1. Quantification of Transaction Costs

3.2. Costs of Energy Efficiency Services and Government Support Schemes

3.3. Reduction of TAC through EES

3.4. Integration of Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- California Public Utilities Commission (CPUC). California Standard Practice Manual. Economic Analysis of Demand-Side Programs and Projects; Governor’s Office of Planning and Research: Sacramento, CA, USA, 2001. Available online: http://www.calmac.org/events/SPM_9_20_02.pdf (accessed on 15 November 2020).

- National Action Plan for Energy Efficiency. Understanding Cost-Effectiveness of Energy Efficiency Programs: Best Practices, Technical Methods, and Emerging Issues for Policy-Makers. Energy and Environmental Economics Inc. and Regulatory Assistance Project; 2008. Available online: https://19january2017snapshot.epa.gov/sites/production/files/2015-08/documents/understanding_cost-effectiveness_of_energy_efficiency_programs_best_practices_technical_methods_and_emerging_issues_for_policy-makers.pdf (accessed on 15 November 2020).

- Levine, M.; Ürge-Vorsatz, D.; Blok, K.; Geng, L.; Harvey, D.; Lang, S.; Levermore, G.J.; Mongameli Mehlwana, A.; Mirasgedis, S.; Novikova, A.; et al. Residential and commercial buildings. In Climate Change 2007: Mitigation. Constribution of Working Group III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change; IPCC: New York, NY, USA; Cambridge University Press: Cambridge, UK, 2007. [Google Scholar]

- Adisorn, T.; Luetkehaus, H.; Thema, J.; Tholen, L.; Braungardt, S.; Huenecke, K.; Schumacher, K. Towards a More Realistic Cost-Benefits Analysis—Attempting to Integrate Transaction Costs and Energy Efficiency Services. 2020. Available online: https://elib.dlr.de/136983/ (accessed on 15 November 2020).

- Wuppertal Institut für Klima, Umwelt, Energie; Öko-Institut e.V. Erweiterung von Kosten-Nutzen-Analysen zu Ausgewählten Energieeffizienzmaßnahmen um Erkenntnisse zum Markt für Energieeffizienzdienstleistungen und zum Aufwand von Investitionen in Energieeffizienz. 2018. Available online: https://www.bfee-online.de/SharedDocs/Downloads/BfEE/DE/Energiedienstleistungen/studie_kostennutzen.html (accessed on 15 November 2020).

- Huenecke, K.; Thema, J.; Tholen, L.; Adisorn, T.; Luetkehaus, H.; Braungart, S.; Schumacher, K. What Role do Transaction Costs Play in Energy Effiency Improvements and How Can They Be Reduced? eceee summer study 2019. 2019, pp. 675–684. Available online: https://www.eceee.org/library/conference_proceedings/eceee_Summer_Studies/2019/4-monitoring-and-evaluation-for-greater-impact/what-role-do-transaction-costs-play-in-energy-efficiency-improvements-and-how-can-they-be-reduced/ (accessed on 15 November 2020).

- Thema, J.; Thomas, S.; Teubler, J.; Chatterjee, S.; Bouzarovski, S.; Mzavandaze, N.; von Below, D. More than Energy Savings: Quantifying the Multiple Impacts of Energy Efficiency in Europe. eceee summer study 2017. 2017. Available online: https://www.eceee.org/library/conference_proceedings/eceee_Summer_Studies/2017/8-monitoring-and-evaluation-building-confidence-and-enhancing-practices/more-than-energy-savings-quantifying-the-multiple-impacts-of-energy-efficiency-in-europe/ (accessed on 15 November 2020).

- Jaffe, A.B.; Stavins, R.N. The energy-efficiency gap. What does it mean? Energy Policy 1994, 10, 804–810. [Google Scholar] [CrossRef]

- Moya, J.A. A Natural Analogy to the Diffusion of Energy-Efficient Technologies. Energies 2016, 9, 471. [Google Scholar] [CrossRef]

- Fleiter, T.; Plötz, P. Diffusion of Energy-Efficient Technologies. In Encyclopedia of Energy, Natural Resource, and Environmental Economics, Vol. 1 Energy; Elsevier: Amsterdam, The Netherlands, 2013; Volume 1, pp. 63–73. [Google Scholar]

- Gerarden, T.D.; Newell, R.G.; Stavins, R.N. Assessing the Energy-Efficiency Gap. J. Econ. Lit. 2017, 55, 1486–1525. [Google Scholar] [CrossRef]

- König, W.; Loebbe, S.; Büttner, S.; Schneider, C. Establishing Energy Efficiency—Drivers for Energy Efficiency in German Manufacturing Small- and Medium-Sized Enterprises. Energies 2020, 13, 5144. [Google Scholar] [CrossRef]

- Thollander, P.; Backlund, S.; Trianni, A.; Cagno, E. Beyond barriers—A case study on driving forces for improved energy efficiency in the foundry industries in Finland, France, Germany, Italy, Poland, Spain, and Sweden. In Applied Energy; Elsevier: Amsterdam, The Netherlands, 2013; Volume 111, pp. 636–643. [Google Scholar] [CrossRef]

- Marchi, B.; Zanoni, S. Supply Chain Management for Improved Energy Efficiency: Review and Opportunities. Energies 2017, 10, 1618. [Google Scholar] [CrossRef]

- Parker, C.M.; Redmond, J.; Simpson, M. A Review of Interventions to Encourage SMEs to Make Environmental Improvements. Environ. Plan. C Politics Space 2009, 279–301. [Google Scholar] [CrossRef]

- Trianni, A.; Accordini, D.; Cagno, E. Identification and Categorization of Factors Affecting the Adoption of Energy Efficiency Measures within Compressed Air Systems. Energies 2020, 13, 5116. [Google Scholar] [CrossRef]

- United Nations Framework Convention on Climate Change (UNFCCC). Paris Agreement; United Nations: Paris, France, 2015. [Google Scholar]

- European Commission. The European Green Deal; European Commission: Brussels, Belgium, 2019; Available online: https://ec.europa.eu/commission/presscorner/detail/en/IP_19_6691 (accessed on 15 November 2020).

- Bundesministerium für Wirtschaft und Energie (BMWi). Energieeffizienzstrategie 2050; Bundesministerium für Wirtschaft und Energie (BMWi): Berlin, Germany, 2019; Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Energie/energieeffiezienzstrategie-2050.pdf?__blob=publicationFile&v=12 (accessed on 15 November 2020).

- Campbell, N.; Ryan, L.; Rozite, V.; Lees, E.; Heffner, G. Capturing the Multiple Benefits of Energy Efficiency; IEA: Paris, France, 2014. [Google Scholar]

- Thema, J.; Suerkemper, F.; Couder, J.; Mzavanadze, N.; Chatterjee, S.; Treubler, J.; Rasch, J. The multiple benefits of the 2030 EU energy efficiency potential. Energies 2019, 12, 2798. [Google Scholar] [CrossRef]

- Killip, G.; Cooremans, C.; Krishnan, S.; Fawcett, T.; Grijns-Gaus, W.; Voswinkel, F. Multiple Benefits of Energy Efficiency at the Firm Level: A Literature Review. eceee Summer Study Proceedings Paper. 2019. Available online: https://www.eceee.org/library/conference_proceedings/eceee_Summer_Studies/2019/2-whats-next-in-energy-policy/multiple-benefits-of-energy-efficiency-at-the-firm-level-a-literature-review/ (accessed on 15 November 2020).

- Simas, M.; Pacca, S. Socio-economic Benefits of Wind Power in Brazil. J. Sustain. Dev. Energy Water Environ. Syst. 2013, 1, 27–40. [Google Scholar] [CrossRef][Green Version]

- Shakya, S.R. Benefits of Low Carbon Development Strategies in Emerging Cities of Developing Country: A Case of Kathmandu. J. Sustain. Dev. Energy Water Environ. Syst. 2016, 4, 141–160. [Google Scholar] [CrossRef]

- van der Meulen, S.H. Costs and Benefits of Green Roof Types for Cities and Building Owners. J. Sustain. Dev. Energy Water Environ. Syst. 2018, 7, 55–71. [Google Scholar] [CrossRef]

- Institute for European Environmental Policy (IEEP). Review of Costs and Benefits of Energy Savings, Task 1 Report “Energy Savings 2030”; Institute for European Environmental Policy (IEEP): London, UK, 2013.

- Behi, B.; Baniasadi, A.; Arefi, A.; Goriy, A.; Jennings, P.; Pivrikas, A. Cost–Benefit Analysis of a Virtual Power Plant Including Solar PV, Flow Battery, Heat Pump, and Demand Management: A Western Australian Case Study. Energies 2020, 13, 2614. [Google Scholar] [CrossRef]

- Moser, S.; Mayrhofer, J.; Schmidt, R.; Tichler, R. Socioeconomic cost-benefit-analysis of seasonal heat storages in district heating systems with industrial waste heat integration. In Energy; Elsevier: Amsterdam, The Netherlands, 2018; pp. 868–874. [Google Scholar] [CrossRef]

- Thomas, S. Aktivitäten der Energiewirtschaft zur Förderung der Energieeffizienz auf der Nachfrageseite in Liberalisierten Strom- und Gasmärkten Europäischer Staaten: Kriteriengestützter Vergleich der Politischen Rahmenbedingungen; Kommunalwirtschaftliche Forschung und Praxis; Europäischer Verlag der Wissenschaft: Berlin, Germany, 2007; Volume 13, ISBN 1435-8468. [Google Scholar]

- Bundesministerium für Umwelt, Naturschutz und nukleare Sicherheit (BMU). Beschluss der Bundesregierung zum Klimaschutzprogramm der Bundesrepublik Deutschland auf der Basis des Vierten Berichts der IMA “CO2-Reduktion”; Bundesministerium für Umwelt, Naturschutz und nukleare Sicherheit (BMU): Bonn, Germany, 1997. [Google Scholar]

- Gillingham, K.; Palmer, K. Bridging the Energy Efficiency Gap: Policy Insights from Economic Theory and Empirical Evidence. Rev. Environ. Econ. Policy 2014, 8, 18–38. [Google Scholar] [CrossRef]

- Mundasca, L.; Mansoz, M.; Neij, L.; Timilsina, G. Transaction Costs of Low Carbon Technologies and Policies. The Diverging Literature; Policy Research Paper 6565; World Bank: Washington, DC, USA, 2013. [Google Scholar]

- Kiss, B. Exploring transaction costs in passive house-oriented retrofitting. J. Clean. Prod. 2016, 123, 65–76. [Google Scholar] [CrossRef]

- Kube, M.; Schimmel, M.; Rhiemeier, J.M.; Barckhausen, A.; Fehr, J.; Büttner, S.; Unger, M.; Bottner, F.; Piégsa, A. Marktverfügbare Innovationen mit hoher Relevanz für die Energieeffizienz in der Industrie. 2017. Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Energie/marktverfuegbare-innovationen-mit-hoher-relevanz-fuer-energieeffizienz-in-der-industrie.pdf (accessed on 22 December 2020).

- Dena. Elektrische Motoren in Industrie und Gewerbe—Energieeffizienz- und Ökodesign-Richtlinie; Dena: Berlin, Germany, 2010. [Google Scholar]

- Bieniek, K. “Life-Cycle Costs” of Industrial Electric Drives in the Process Industry—Energy Consumption and Economics of Electric Drives. In Energy Efficiency Improvements in Electronic Motors and Drives; Springer: Heidelberg/Berlin, Germany, 2000. [Google Scholar] [CrossRef]

- Hein, L.; Blok, K. Transaction Costs of Energy Efficiency Improvement. eceee summer study 1995. 1995. Available online: https://www.eceee.org/library/conference_proceedings/eceee_Summer_Studies/1995/Panel_2/p2_12/ (accessed on 15 November 2020).

- Ostertag, K. Re-Assessing No-Regret Potentials—The Example of High Efficiency Electric Motors. eceee summer study 2001. 2001. Available online: http://publica.fraunhofer.de/dokumente/N-9797.html (accessed on 15 November 2020).

- Mai, M.; Gebhardt, T.; Wahl, F.; Dann, D.; Jochem, E. Transaktionskosten bei Energieeffizienz-Investitionen in Unternehmen. Zeitschrift für Energiewirtschaft 2014, 38, 269–279. [Google Scholar] [CrossRef][Green Version]

- Irrek, W.; Suerkemper, F.; Rochas, C. Energy Efficiency Services. Good Practice and Successful Market Developments; Change Best Project; Ekodoma: Riga, Latvia, 2012. [Google Scholar]

- Mai, M.; Gruber, E.; Holländer, E.; Roser, A.; Gerspacher, A.; Fleiter, T.; Hirzel, S.; Ostrander, B.; Schleich, J.; Schlomann, B. Evaluation des Förderprogramms „Energieberatung im Mittelstand; Institut für Ressourceneffizienz und Energiestrategien GmbH (IREES); Fraunhofer-Institut für System- und Innovationsforschung ISI: Karlsruhe, Germany, 2014.

- Adisorn, T.; Vondung, F. Behind Closed Windows—An Actor-Centred Analysis of Barriers for the Diffusion of Energy Efficient Ventilation Systems in Residential Buildings. eceee summer study 2019. 2019, pp. 1459–1468. Available online: https://www.eceee.org/library/conference_proceedings/eceee_Summer_Studies/2019/8-buildings-technologies-and-systems-beyond-energy-efficiency/behind-closed-windows-an-actor-centred-analysis-of-barriers-for-the-diffusion-of-energy-efficient-ventilation-systems-in-residential-buildings/ (accessed on 15 November 2020).

- Verbraucherzentrale Bundesverband. Unsere Themen. Available online: https://verbraucherzentrale-energieberatung.de/?cn-reloaded=1 (accessed on 14 December 2020).

- Bayerisches Landesamt für Umweltschutz. Druckluft im Handwerk. Untersuchung von Druckluftanlagen in Handwerksbetrieben; Bayerisches Landesamt für Umweltschutz: Augsburg, Germany, 2004. [Google Scholar]

- Kiss, B.; Mundasca, L. Transaction Costs of Energy Efficiency in Buildings: An Overview. IAEE Energy Forum 2013, 22, 31–32. [Google Scholar]

- Bundesamt für Wirtschaft und Ausfuhrkontrolle; Bundesstelle für Energieeffizienz. Empirische Untersuchung des Marktes für Energiedienstleistungen, Energieaudits und andere Energieeffizienzmaßnahmen im Jahr 2018; BfEE 17/2017; Bundesamt für Wirtschaft und Ausfuhrkontrolle; Bundesstelle für Energieeffizienz: Eschborn, Germany, 2018. [Google Scholar]

- Zangheri, P.; Economidou, M.; Labanca, N. Progress in the Implementation of the EU Energy Efficiency Directive through the Lens of the National Annual Reports. Energies 2019, 12, 1107. [Google Scholar] [CrossRef]

- Deutsche Energie-Agentur. Dena-Analyse—Kommunale Nichtwohngebäude; Deutsche Energie-Agentur GmbH: Berlin, Germany, 2018. [Google Scholar]

- Kazak, J.K.; Kamińska, J.A.; Madej, R.; Bochenkiewicz, M. Where Renewable Energy Sources Funds are Invested? Spatial Analysis of Energy Production Potential and Public Support. Energies 2020, 13, 5551. [Google Scholar] [CrossRef]

- Valentová, M. Barriers to Energy Efficiency—Focus on Transaction Costs. Acta Polytechnica 2010, 50. Available online: https://ojs.cvut.cz/ojs/index.php/ap/article/view/1247 (accessed on 15 November 2020).

{kind=link}

{kind=link}

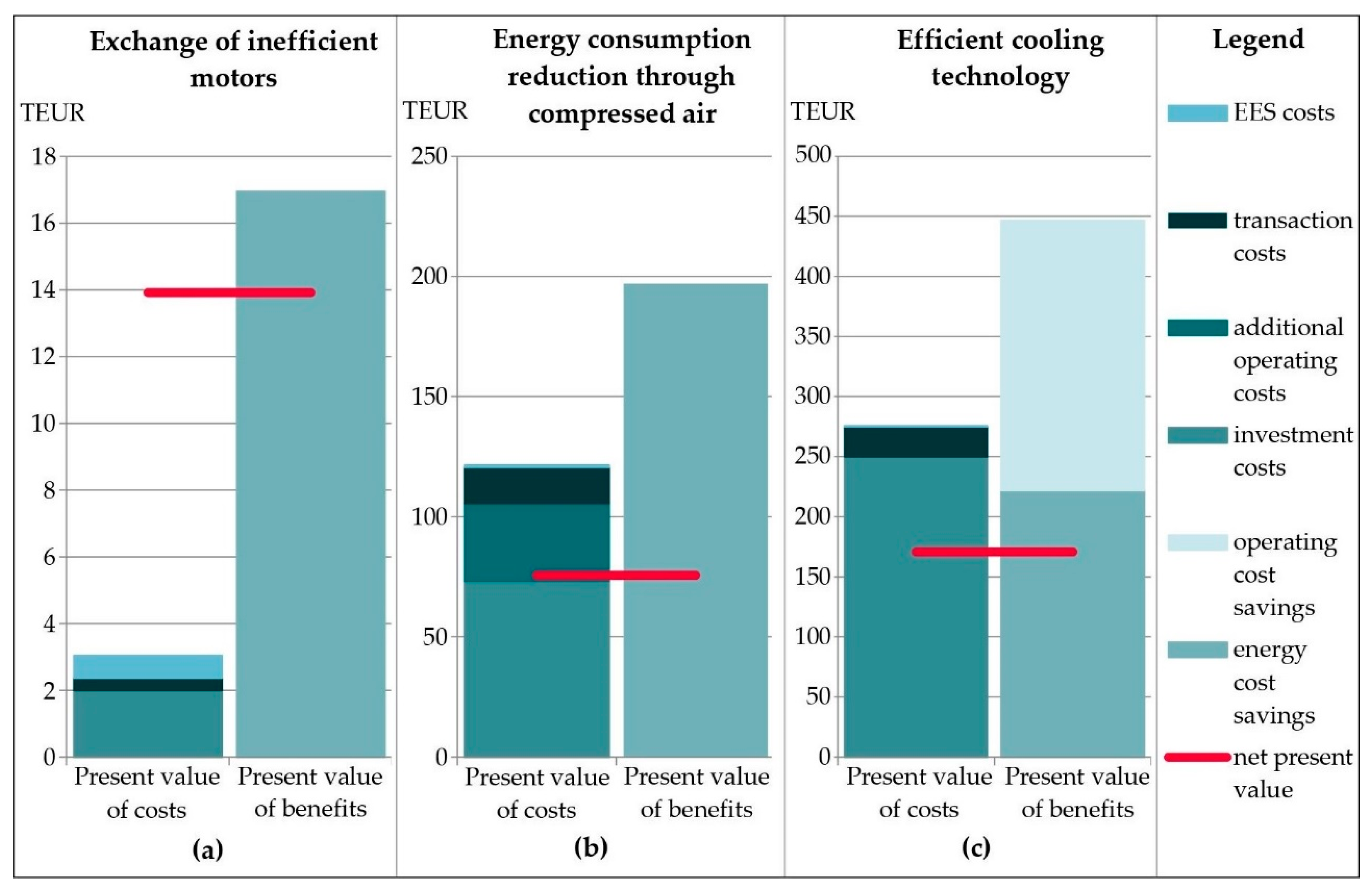

| Case | Exchange of Inefficient Motors (M1) | Energy Consumption Reduction through Compressed Air (M2) | Efficient Cooling Technology (M3) |

|---|---|---|---|

| Case description | (Early) replacement of an older motor (4-pole, 30 kW, efficiency class EFF3, efficiency of 85%) with an efficient motor of class IE3. | Use of compressed air station with a total energy consumption of 1000 MWh per year (before modernization). | Use of an innovative system using water as a refrigerant and the use of free cooling |

| Investment costs (€) | 2000 | 73,000 | 250,000 |

| Energy cost savings over life span (€) | 16,994.98 | 196,928.45 | 221,869.85 |

| Case | Exchange of Inefficient Motors (M1) (€) | Energy Consumption Reduction through Compressed Air (M2) (€) | Efficient Cooling Technology (M3) (€) |

|---|---|---|---|

| Investment costs | 2000 | 73,000 | 250,000 |

| Additional operating costs | 0 | 32,359.96 | 0 |

| Transaction costs | 366.67 | 15,000 | 25,000 |

| EES costs 1 | 2666.67 | 2666.67 | 2666.67 |

| Government funding for EES | 2000 | 2000 | 2000 |

| Investor costs for EES | 666.67 | 666.67 | 666.67 |

| Operation costs savings | 0 | 0 | 224,564.63 |

| Energy costs savings | 16,994.98 | 196,928.45 | 221,869.85 |

| Reduction of TAC through EES | n.a. | n.a. | n.a. |

| Net present value | 13,911.64 | 75,601.83 | 170,767.80 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Adisorn, T.; Tholen, L.; Thema, J.; Luetkehaus, H.; Braungardt, S.; Huenecke, K.; Schumacher, K. Towards a More Realistic Cost–Benefit Analysis—Attempting to Integrate Transaction Costs and Energy Efficiency Services. Energies 2021, 14, 152. https://doi.org/10.3390/en14010152

Adisorn T, Tholen L, Thema J, Luetkehaus H, Braungardt S, Huenecke K, Schumacher K. Towards a More Realistic Cost–Benefit Analysis—Attempting to Integrate Transaction Costs and Energy Efficiency Services. Energies. 2021; 14(1):152. https://doi.org/10.3390/en14010152

Chicago/Turabian StyleAdisorn, Thomas, Lena Tholen, Johannes Thema, Hauke Luetkehaus, Sibylle Braungardt, Katja Huenecke, and Katja Schumacher. 2021. "Towards a More Realistic Cost–Benefit Analysis—Attempting to Integrate Transaction Costs and Energy Efficiency Services" Energies 14, no. 1: 152. https://doi.org/10.3390/en14010152

APA StyleAdisorn, T., Tholen, L., Thema, J., Luetkehaus, H., Braungardt, S., Huenecke, K., & Schumacher, K. (2021). Towards a More Realistic Cost–Benefit Analysis—Attempting to Integrate Transaction Costs and Energy Efficiency Services. Energies, 14(1), 152. https://doi.org/10.3390/en14010152