Biomass Availability in Europe as an Alternative Fuel for Full Conversion of Lignite Power Plants: A Critical Review

, ,

, ,

Abstract

:1. Introduction

1.1. Policy Issues of Climate Change

Reducing Carbon Emissions: EU Targets

1.2. The Transition to the Post-Lignite Era

2. Lignite Sector in the EU

2.1. Lignite Production

2.1.1. National Coal Phase-Out Announcements in Europe

2.1.2. Studies on Biomass Availability and Co-Firing in Lignite Boilers

2.2. Worldwide Biomass Availability

2.3. Biomass Availability in Main Lignite-producer countries

2.3.1. Germany

2.3.2. Poland

2.3.3. Czech Republic

2.3.4. Greece

2.3.5. Bulgaria

2.3.6. Romania

3. Biomass Conversion Technologies for Electricity Production: Focus on Full Conversion of Power Plants

4. Biomass Cost

- -

- In the case of straw and stubbles—like cereal straw and maize stover—only the harvesting, fertilization (due to nutrient removal with the straw), baling and collecting to the roadside farm/gate are taken into account [60].

- -

- In the case of prunings from permanent crops, the cost of collecting branches left on the soil, as shredded material at the roadside, is included.

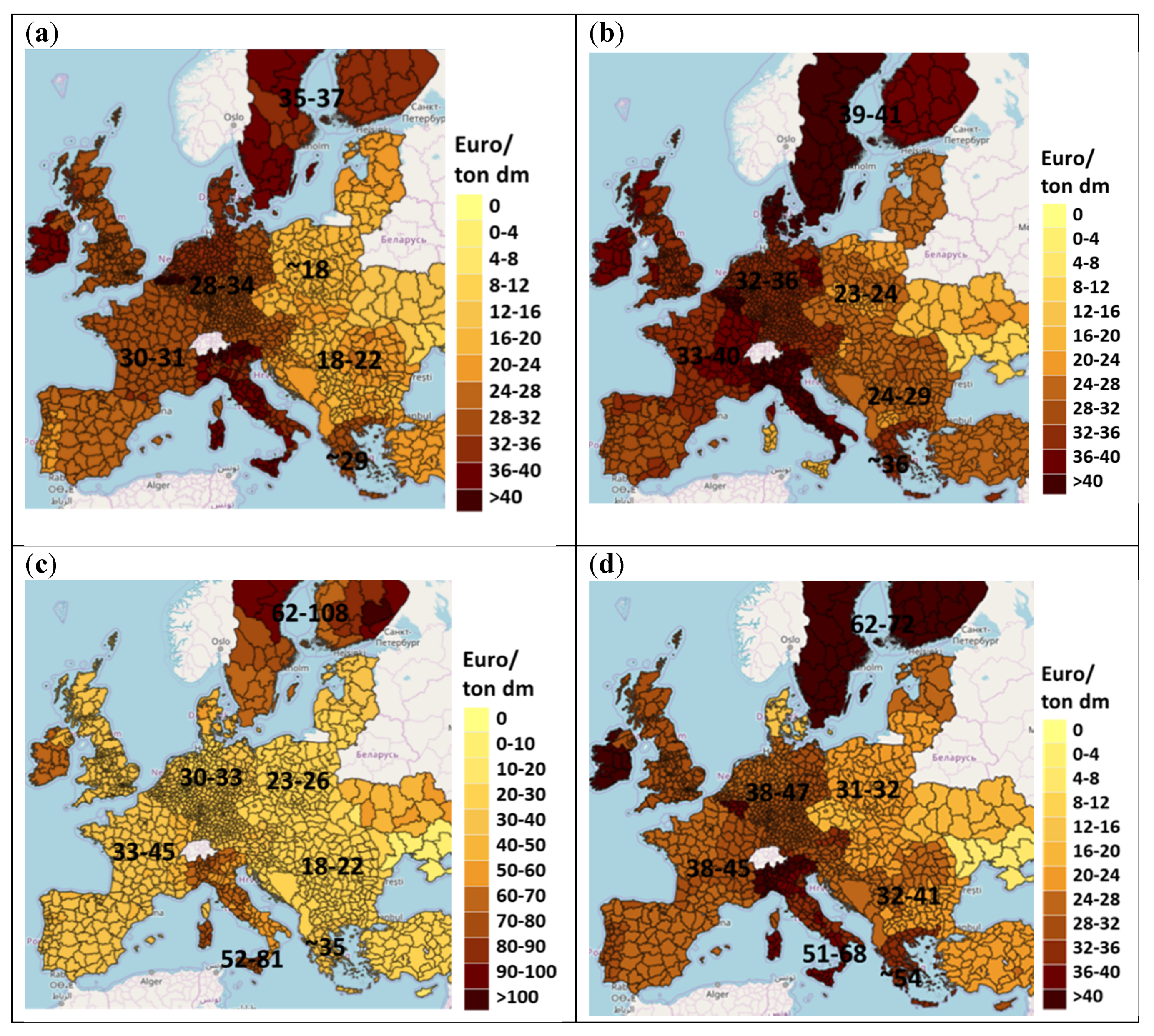

4.1. Roadside Cost

- -

- Cereal straw is estimated to have high values in Greece (~45 EUR/kton dry), in Italy (36–42 EUR/kton dry), Germany (28–29 EUR/kton dry), France (30–31 EUR/kton dry) and Sweden/Finland (37–42 EUR/kton dry). The lowest prices are traced in Poland (17–21 EUR/kton dry) and southeastern countries like Bulgaria, Hungary and Romania.

- -

- For the rest of the crops (maize stover, sunflower straw and oil seed rape straw), the situation is more or less the same, with the highest prices observed in Central (except for Poland), Southwest and North Europe, and the lowest prices traced in Southeast Europe.

- -

- In general, stemwood originating from coniferous trees has a higher roadside cost, compared to that originating from non-conifer trees. The same applies to the logging residues.

- -

- Stemwood from non-conifer trees is estimated to have (as in the case of agricultural crops) the lowest prices in Poland (18–26 EUR/kton dry) and southeastern countries, such as Bulgaria, Hungary and Romania. In the same areas, the price of stemwood from coniferous trees will be approximately 23–32 EUR/kton dry.

4.2. Plant Gate Cost and Market Price

5. SWOT Analysis

5.1. Strengths

5.2. Weaknesses

5.3. Opportunities

5.4. Threats

5.5. Overview

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Disclaimer

References

- EUTL Database. Available online: https://sandbag.org.uk/project/ets-emissions-2018/ (accessed on 31 January 2020).

- Balan, V. Current Challenges in Commercially Producing Biofuels from Lignocellu-Losic Biomass; International Scholarly Research Notices; Hindawi Publishing Corporation: London, UK, 2014; pp. 1–31. [Google Scholar] [CrossRef]

- Schoenmaker, D.; Van Tilburg, R.; Wijffels, H. What Role for Financial Supervisors in Addressing Systemic Environmental Risks? UNEP Inquiry, Utrecht Sustainable Finance Lab: Utrecht, The Netherlands, 2015. [Google Scholar]

- McGlade, C.; Ekins, P. The Geographical Distribution of Fossil Fuels Unused when Limiting Global Warming to 2 Degrees. Nature 2015, 517, 187–190. [Google Scholar] [CrossRef] [PubMed]

- Economist Intelligence Unit. The Cost of Inaction: Recognising the Value at Risk from Climate Change; Economist Intelligence Unit: London, UK, 2015; p. 63. [Google Scholar]

- United Nations Climate Change. Economic Diversification. Available online: https://unfccc.int/topics/resilience/resources/economic-diversification (accessed on 17 December 2019).

- International Energy Agency (IEA). Coal 2018. Analysis and Forecasts to 2023. Available online: https://www.iea.org/coal2018 (accessed on 14 January 2020).

- Erb, K.H.; Krausmann, F.; Lucht, W.; Haberl, H. Embodied HANPP: Mapping the Spatial Disconnect between Global Biomass Production and Consumption. Ecol. Econ. 2009, 69, 328–334. [Google Scholar] [CrossRef]

- European Biomass Associtation. Forest Sustainability and Carbon Balance of EU Importation of North American Forest Biomass for Bioenergy Production; Aebiom: Brussels, Belgium, 2013. [Google Scholar]

- Europe beyond Coal. Overview: National Coal Phase-Out Announcements in Europe. 2019. Available online: https://beyond-coal.eu/ (accessed on 14 January 2020).

- Amelang, S.; Appunn, K.; Egenter, S.; Sherman, L.; Wehrmann, B.; Wettengel, J. Commission Watch-Managing Germany’s Coal Phase-Out. 2019. Available online: https://www.cleanenergywire.org/news/commission-watch-managing-germanys-coal-phase-out (accessed on 11 February 2020).

- Parra, P.; Ganti, G.; Brecha, R.; Hare, B.; Schaeffer, M.; Fuentes, U. Global and Regional Coal Phase-Out Requirements of the Paris Agreement: Insights from the IPCC Special Report on 1.5 °C. Climate Analytics. 2019. Available online: https://climateanalytics.org/publications/2019/coal-phase-out-insights-from-the-ipcc-special-report-on-15c-and-global-trends-since-2015/ (accessed on 20 December 2019).

- Flisowska, J.; Moore, C. Just Transition or Just Talk? Draft National Energy and Climate Plans Reveal Some EU Countries are Planning to Stick with Coal Power beyond 2030; Climate Action Network (CAN) Europe and Sandbag: Brussels, Belgium; London, UK, 2019. [Google Scholar]

- Roni, M.S.; Chowdhury, S.; Mamun, S.; Marufuzzaman, M.; Lein, W.; Johnson, S. Biomass co-firing technology with policies, challenges, and opportunities: A global review. Renew. Sustain. Energy Rev. 2017, 78, 1089–1101. [Google Scholar] [CrossRef]

- Welfle, A. Balancing growing global bioenergy resource demands—Brazil’s biomass potential and the availability of resource for trade. Biomass Bioenergy 2017, 105, 83–95. [Google Scholar] [CrossRef]

- Ozcan, M.; Oztürk, S.; Oguz, Y. Potential evaluation of biomass-based energy sources for Turkey. Eng. Sci. Technol. 2015, 18, 178–184. [Google Scholar] [CrossRef] [Green Version]

- Drosatos, P.; Nikolopoulos, N.; Karampinis, E.; Grammelis, P.; Kakaras, E. Comparative investigation of a co-firing scheme in a lignite-fired boiler at very low thermal-load operation using either pre-dried lignite or biomass as supporting fuel. Fuel Process. Technol. 2018, 180, 140–154. [Google Scholar] [CrossRef]

- Nikolopoulos, N.; Agraniotis, M.; Violidakis, I.; Karampinis, E.; Nikolopoulos, A.; Grammelis, P.; Papapavlou, C.; Tzivenis, S.; Kakaras, E. Parametric investigation of a renewable alternative for utilities adopting the co-firing lignite/biomass concept. Fuel 2013, 113, 873–897. [Google Scholar] [CrossRef]

- WBA GLOBAL BIOENERGY STATISTICS 2018; World Bioenergy Association: Stockholm, Sweden, 2018.

- N. Statista. Capacity of Biomass Power Plants in Selected Countries and Worldwide in 2018. 2019. Available online: https://www.statista.com/statistics/264637/world-biomass-energy-capacity/ (accessed on 30 March 2020).

- Li, Y.; Rezgui, Y.; Zhu, H. District heating and cooling optimization and enhancement—Towards integration of renewables, storage and smart grid. Renew. Sustain. Energy Rev. 2017, 72, 281–294. [Google Scholar] [CrossRef]

- Bottcher, H.; Frank, S.; Havlik, P. Biomass Availability & Supply Analysis, Deliverable 3.4 of Biomass Futures Project; International Institute for Applied Systems Analysis, Biomass Futures: Laxenburg, Austria, 2012. [Google Scholar]

- Sikkema, R.; Steiner, M.; Junginger, M.; Heigl, W.; Hansenm, M.; Faaij, A. The european wood pellet markets: Current status & prospects for 2020. Biofuels. Bioprod. Biorefining 2011, 5, 250–278. [Google Scholar] [CrossRef]

- Spelter, H.; Toth, D. North America’s Wood Pellet Sector; United States Department of Agriculture: Madison, WI, USA, 2009.

- Thrän, D.; Dotzauer, M.; Lenz, V.; Liebetrau, J.; Ortwein, A. Flexible bioenergy supply for balancing fluctuating renewables in the heat and power sector—A review of technologies and concepts. Energy Sustain. Soc. 2015. [CrossRef] [Green Version]

- FAO. FAO Statistics Forestry Datasets. Rome. 2013. Available online: http://faostat.fao.org/site/626/DesktopDefault.aspx?PageID=626#ancor (accessed on 3 February 2020).

- Thiry, M.C. Playing with Fire. AATCC Review. 2002, 2, 16–20. [Google Scholar]

- S2Biom project. Available online: https://www.s2biom.eu/en/ (accessed on 18 March 2020).

- Ernst & Young Company. European Lignite Mines Benchmarking Sanitized Report; Ernst & Young: London, UK, 2014. [Google Scholar]

- Andruleit, H.; Bahr, A.; Babies, H.G.; Franke, D.; Meßner, J.; Pierau, R.; Schauer, M.; Schmidt, S.; Weihmann, S. Reserves, Resources and Availability of Energy Resources; Energy study; Federal Institute for Geosciences and Natural Resources: Hannover, Germany, 2016. [Google Scholar]

- Weiser, C.; Zeller, V.; Reinicke, F.; Wagner, B.; Majer, S.; Vetter, A.; Thraen, D. Integrated assessment of sustainable cereal straw potential and different straw-based energy applications in Germany. Appl. Energy 2014, 114, 749–762. [Google Scholar] [CrossRef]

- Agricultural census in GermanyEuropean Union. Available online: http://ec.europa.eu/eurostat/statistics-explained/index.php/Agricultural_census_in_Germany (accessed on 11 February 2020).

- Federal Ministry of Food Agriculture and Consumer Protection. German Forests—Nature and Economic Factor; Federal Ministry of Food Agriculture and Consumer Protection: Berlin, Germany, 2011.

- Widera, M. Genetic classification of Polish lignite deposits: A review. Int. J. Coal Geol. 2016, 158, 107–118. [Google Scholar] [CrossRef]

- Rafał, B.; Wajszczuk, K.; Pepliński, B.; Wawrzynowicz, J. Potential For Agricultural Biomass Production for Energy Purposes in Poland: A Review, Contemporary Economics; SSRN: New York, NY, USA, 2014; Volume 7, pp. 63–74. Available online: https://ssrn.com/abstract=2253173 (accessed on 17 June 2020).

- Statista, M. Production of Lignite Worldwide from 1990 to 2016 (in Million Metric Tons). Available online: https://www.statista.com/statistics/267894/global-lignite-production-since-1990/ (accessed on 20 December 2019).

- Milewski, W.; Beasley, A. Forests in Poland 2015; The State Forests Information Centre: Warsaw, Polonia, 2015; ISBN 978-83-63895-79-2. [Google Scholar]

- International Energy Agency, Greece. Available online: https://www.iea.org/countries/Greece (accessed on 27 March 2020).

- Eurocoal. Eurocoal the Voice of Coal in Europe—Greece. Bruxelles, Belgium. Available online: https://euracoal.eu/info/country-profiles/greece/ (accessed on 14 January 2020).

- Karampinis, E.; Grammelis, P. Biomass Co-Firing in Lignite-Fired Power Plants as a Means of Mobilizing Agro-Biomass Resources; Project Report. S2BIOM—a project funded under the European Union 7th Frame Programme; Centre for Research and Technology Hellas: Athens, Greece, 2017. [Google Scholar]

- Kavouridis, K. Lignite industry in Greece within a world context: Mining, energy supply and environment. Energy Policy 2008, 36, 1257–1272. [Google Scholar] [CrossRef]

- World Energy Council. World Energy Resources Coal; World Energy Council: London, UK, 2016. [Google Scholar]

- EURACOAL. Coal Industry Across Europe, 6th ed.; European Association for Coal and Lignite: Brussels, Belgium, 2017; ISBN 2034-5682. [Google Scholar]

- Bulgaria Forest Information and Data. Available online: https://rainforests.mongabay.com/deforestation/2000/Bulgaria.htm (accessed on 27 January 2020).

- Jones, D.; Sakhel, A.; Buck, M.; Graichen, P. The European Power Sector in 2017; Agora Energiewende: Berlin, Germany, 2018; p. 49. [Google Scholar]

- Boshnakova, M. Wood Products Sector Update-Bulgaria. USDA Foreign Agricultural Service; Global Agricultural Information Network: Warsaw, Bulgaria, 2017. Available online: https://www.fas.usda.gov/data/bulgaria-wood-products-sector-update (accessed on 15 June 2020).

- FAO. 2019. Available online: http://www.fao.org/3/j4504E/j4504e06.htm (accessed on 30 March 2020).

- Li, S.; Zheng, H.; Zheng, Y.; Tian, J.; Jing, T.; Chang, J.-S.; Ho, S.-H. Recent advances in hydrogen production by thermo-catalytic conversion of biomass. Int. J. Hydrogen Energy 2019, 44, 14266–14278. [Google Scholar] [CrossRef]

- Liu, P.; Wang, Y.; Zhou, Z.; Yuan, H.; Zheng, T.; Chen, Y. Effect of carbon structure on hydrogen release derived from different biomass pyrolysis. Fuel 2020, 271, 117638. [Google Scholar] [CrossRef]

- Chianese, S.; Fail, S.; Binder, M.; Rauch, R.; Hofbauer, H.; Molino, A.; Blasi, A.; Musmarra, D. Experimental investigations of hydrogen production from CO catalytic conversion of tar rich syngas by biomass gasification. Catal. Today 2016, 277, 182–191. [Google Scholar] [CrossRef]

- WIP Renewable Energies. Technical options for retrofitting industries with bioenergy—A Handbook, 2020Biofit. Available online: https://www.biofit-h2020.eu/news-and-events/handbook-published/ (accessed on 30 March 2020).

- Savat, P. Activities at Rodenhuize Power Plant: Advanced and Max Green Projects; Topic Orientated Technical Meeting 35—Co-firing secondary fuels in power generation: From fuel characterization to full scale testing; IFRF: Pisa, Italy, 2010. [Google Scholar]

- Drax Group plc. Annual report and accounts 2018. 2018. Available online: https://www.drax.com/wp-content/uploads/2019/03/Drax-Annual-report-accounts-2018.pdf (accessed on 30 March 2020).

- Zhang, F.; Johnson, D.M.; Sutherland, J.W. A GIS-based method for identifying the optimal location for a facility to convert forest biomass to biofuel. Biomass Bioenergy 2011, 35, 3951–3961. [Google Scholar] [CrossRef]

- Rentizelas, A.A.; Tolis, A.J.; Tatsiopoulos, I.P. Logistics issues of biomass: The storage problem and the multi-biomass supply chain. Renew. Sustain. Energy Rev. 2009, 13, 887–894. [Google Scholar] [CrossRef] [Green Version]

- Sansaniw, S.K.; Rosen, M.A.; Tyagi, S.K. Global challenges in the sustainable development of biomass gasification: An overview. Renew. Sustain. Energy Rev. 2017, 80, 23–43. [Google Scholar] [CrossRef]

- An, H.; Wilhelm, W.E.; Searcy, S.W. A mathematical model to design a lignocellulosic biofuel supply chain system with a case study based on a region in Central Texas. Bioresour. Technol. 2011, 102, 7860. [Google Scholar] [CrossRef]

- Zhu, X.; Li, X.; Yao, Q.; Chen, Y. Challenges and models in supporting logistics system design for dedicated-biomass-based bioenergy industry. Bioresour. Technol. 2011, 102, 1344–1351. [Google Scholar] [CrossRef]

- Badger, P.C. Biomass transport system. Encycl. Agric. Food Biol. Eng. 2003, 1, 94–98. [Google Scholar]

- Dees, M.; Forsell, N.; Fitzerald, J.; Vis, M.; Forsell, N.; Datta, P.; Gallaun, H.; Dawar, S.; Glavonjic, B.; Garcia, D.; et al. Best Practice Guidelines on the Maintenance and Regular Up-Date of the Biomass Cost Supply Data for EU, Western Balkan Countries, Moldavia, Turkey and Ukraine; Project Report. S2BIOM—A project funded under the European Union 7th FrameworkProgramme for Research. Grant Agreement n°608622; Institute of Forest Sciences, University of Freiburg: Baden-Württemberg, Germany, 2017. [Google Scholar]

- Piotrowski, S.; Carus, M.; NOVA. Deliverable D1.2: Assessment of procurement costs for the preferred feedstocks. 2012. Available online: http://www.biocore-europe.org/file/D1_2%20Assessment%20of%20procurement%20costs%20for%20the%20preferred%20feedstocks.pdf (accessed on 15 June 2020).

- German Biofuel Portal. Wood pellet prices in the European Union. 2015. Available online: http://biomassa.de/news-wood-pellet-prices-in-the-european-union-18.html (accessed on 3 April 2020).

- Biocore. Available online: http://www.biocore-europe.org/ (accessed on 20 February 2020).

- Biomasud Plus. Available online: http://biomasudplus.eu/en_GB/ (accessed on 20 February 2020).

- Carbon Brief. Global Coal Power. Available online: https://www.carbonbrief.org/mapped-worlds-coal-power-plants (accessed on 6 April 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Mass (Mt) | Electricity (TWh) | Total Electricity (TWh) | Lignite-Based Electricity Generation Share (%) |

|---|---|---|---|---|

| Germany | 166.3 | 146 | 595 | 24.54 |

| Poland | 58.5 | 49 | 175 | 28 |

| Czech. Rep. | 39.2 | 37 | 73 | 50.68 |

| Greece | 36.5 | 17 | 61 | 27.87 |

| Bulgaria | 30.3 | 19 | 38 | 50 |

| Romania | 23.5 | 16 | 62 | 25.81 |

| Hungary | 7.9 | 5 | 46 | 10.87 |

| Slovak. Rep. | 1.5 | 1 | 30 | 3.33 |

| Slovenia | 3.2 | 4 | 15 | 26.67 |

| Country | Coal Phase-Out Status | |

|---|---|---|

| Germany | Phase-out announced but not ambitious enough | Coal phase-out by 2038 with option of 2035. Germany has not achieved its 2020 climate target, because the use of coal was not limited in time, yet the country needs to comply with the 2030 climate goal. According to a report released earlier in 2019 by Germany’s multi-stakeholder government commission [11], a phase-out of coal by 2038 is possible, with the alternative of bringing it forward to 2035, short-term closing of 12.5 GW coal capacity by 2022, and review points in 2023, 2026, 2029 and 2032. The suggested 2038 end date is too late to comply [12] with the Paris Climate Agreement. For this reason, the civil society supports a coal phase-out by 2030. |

| Poland | No phase-out discussion | In Poland, aging coal power plants encounter difficulties of being in line with the air pollution restrictions. Five units are constructed currently. The mining sector poses considerable economic problems. The government supports coal, but market forces are unpredictable. Several Polish opposition parties support coal exit in the period 2035 to 2040. The EU 2030 climate targets and framework in the energy market may promote an accelerated shift. |

| Czech Republic | Phase-out under discussion | In the summer of 2019, a stakeholder “coal commission” was set to evaluate the capability of accelerated coal exit in the country. This Commission claimed to have monthly meetings, and ought to end in September 2020 with suggestions for the government. |

| Greece | Phase-out announced | Coal phase-out by 2028. In September 2019, at the United Nations Climate Action Summit in New York, the prime minister made public that Greece will close all its coal-fired power plants by 2028. Due to the high potentiality in renewable energy, Greece should ensure that the transition away from lignite is in the direction of a 100% share in renewable energy consumption. However, an additional coal power plant is already under construction in North-West Greece [13]. The regional authority of West Macedonia in Greece, where most of the lignite power plants are located, participates in Transition Platform for Coal Regions, in order to be involved in coal-free concepts. |

| Bulgaria | No phase-out discussion | The country does not have a long-term policy about its energy policy yet, and a coal phase-out has not been discussed so far. Aging coal-fired power plants are still operating. The government counts on derogations from EU legislation to keep the power plants in operation and avoid a transition scenario. |

| Romania | No phase-out discussion | Aging coal power plants are struggling to be in line with policy requirements about air pollution. The National Energy Strategy of the country recommends a yearly production of electricity from coal of 15 TWh within the 2030–2050 period, which is only 1 TWh lower compared to the respective level in 2018. A new unit at Rovinari plant has been scheduled since 2013, to be made in synergy with a Chinese investor, and recently has been emphasized as the highest consideration in the National Energy Strategy. The mining sector deals with important economic obligations. |

| Power Plant/Unit | Country | Finalization of Retrofits | Installed Capacity (MW Electrical) | Fuels Used | Combustion Technology |

|---|---|---|---|---|---|

| Les Awirs 4 | Belgium | 2005 | 80 | Wood pellets | PF |

| Helsingborg | Sweden | 2006 | 126 | Wood pellets | PF |

| Västhamnsverket | Sweden | 2006 | 69 | Wood pellets | PF |

| Herning | Denmark | 2009 | 75 | 44% wood chips, 44% wood pellets, 12% top-gas | GF (chips)/PF (pellets) |

| Rodenhuize 4 | Belgium | 2011 | 180 | Wood pellets | PF |

| Tilbury * | United Kingdom | 2011 | 750 | Wood pellets | PF |

| Ironbridge * | United Kingdom | 2012 | 740 | Wood pellets | PF |

| Drax 1 | United Kingdom | 2013 | 660 | Wood pellets | PF |

| Polaniec Green Unit | Poland | 2013 | 195 | 80% wood chips, 20% agrobiomass | CFB |

| Drax 2 | United Kingdom | 2014 | 645 | Wood pellets | PF |

| Atikokan | Canada | 2014 | 205 | Wood pellets | PF |

| Drax 3 | United Kingdom | 2015 | 645 | Wood pellets | PF |

| Thunder Bay 3 * | Canada | 2015 | 160 | Arbacore wood pellets (steam explosion) | PF |

| Avedore 1 | Denmark | 2016 | 258 | Wood pellets | PF |

| Studstrup 3 | Denmark | 2016 | 362 | Wood pellets | PF |

| Yeongdong 1 | South Korea | 2017 | 125 | Wood pellets | PF |

| Drax 4 | United Kingdom | 2018 | 645 | Wood pellets | PF |

| Amer 9 | Netherlands | 2019 | 631 | 80% wood pellets, 20% coal | PF |

| Asnæs 6 | Denmark | 2019 | 25 | Wood chips | BFB |

| Suzukawa | Japan | 2020 (expected) | 112 | Wood pellets | PF |

| Uskmouth | United Kingdom | 2021 (expected) | 240 | Subcoal® pellets (RDF pellets) | PF |

| Country | Plant | Capacity of Plant (MWe) | Annual Thermal Input (TWh) | Total Biomass Potential(kton) | Biomass Energy Content (TWh) | Remarks | |

|---|---|---|---|---|---|---|---|

| Scenario 1 | Scenario 2 | ||||||

| Germany | Hamburg Moorburg | 1730 | 40 | 8000 | 39 | 11.7 | Feasible in 1st scenario |

| Luenen-Stummhafen | 810 | 18 | 10,000 | 47 | 14 | Feasible in 1st scenario | |

| Schwarze Pumpe | 1600 | 36 | 7000 | 33 | 10 | Not feasible in both scenarios | |

| Lippendorf | 1866 | 42 | 5500 | 27 | 8 | Not feasible in both scenarios | |

| Zoilling | 474 | 10 | 8500 | 42 | 12.6 | Feasible in both scenarios | |

| Poland | Kozienice | 1075 | 24 | 12,500 | 60 | 18 | Feasible in 1st scenario |

| Greece | Florina | 330 | 8 | 1500 | 6 | 2 | Not feasible in both scenarios |

| Ptolemaida-Unit 5* | 660 | 15 | 1500 | 6 | 2 | Not feasible in both scenarios | |

| Strengths | Weaknesses |

|---|---|

|

|

| Opportunities | Threats |

|

|

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tzelepi, V.; Zeneli, M.; Kourkoumpas, D.-S.; Karampinis, E.; Gypakis, A.; Nikolopoulos, N.; Grammelis, P. Biomass Availability in Europe as an Alternative Fuel for Full Conversion of Lignite Power Plants: A Critical Review. Energies 2020, 13, 3390. https://doi.org/10.3390/en13133390

Tzelepi V, Zeneli M, Kourkoumpas D-S, Karampinis E, Gypakis A, Nikolopoulos N, Grammelis P. Biomass Availability in Europe as an Alternative Fuel for Full Conversion of Lignite Power Plants: A Critical Review. Energies. 2020; 13(13):3390. https://doi.org/10.3390/en13133390

Chicago/Turabian StyleTzelepi, Vasiliki, Myrto Zeneli, Dimitrios-Sotirios Kourkoumpas, Emmanouil Karampinis, Antonios Gypakis, Nikos Nikolopoulos, and Panagiotis Grammelis. 2020. "Biomass Availability in Europe as an Alternative Fuel for Full Conversion of Lignite Power Plants: A Critical Review" Energies 13, no. 13: 3390. https://doi.org/10.3390/en13133390

APA StyleTzelepi, V., Zeneli, M., Kourkoumpas, D.-S., Karampinis, E., Gypakis, A., Nikolopoulos, N., & Grammelis, P. (2020). Biomass Availability in Europe as an Alternative Fuel for Full Conversion of Lignite Power Plants: A Critical Review. Energies, 13(13), 3390. https://doi.org/10.3390/en13133390