Green Activity-Based Costing Production Decision Model for Recycled Paper

Abstract

1. Introduction

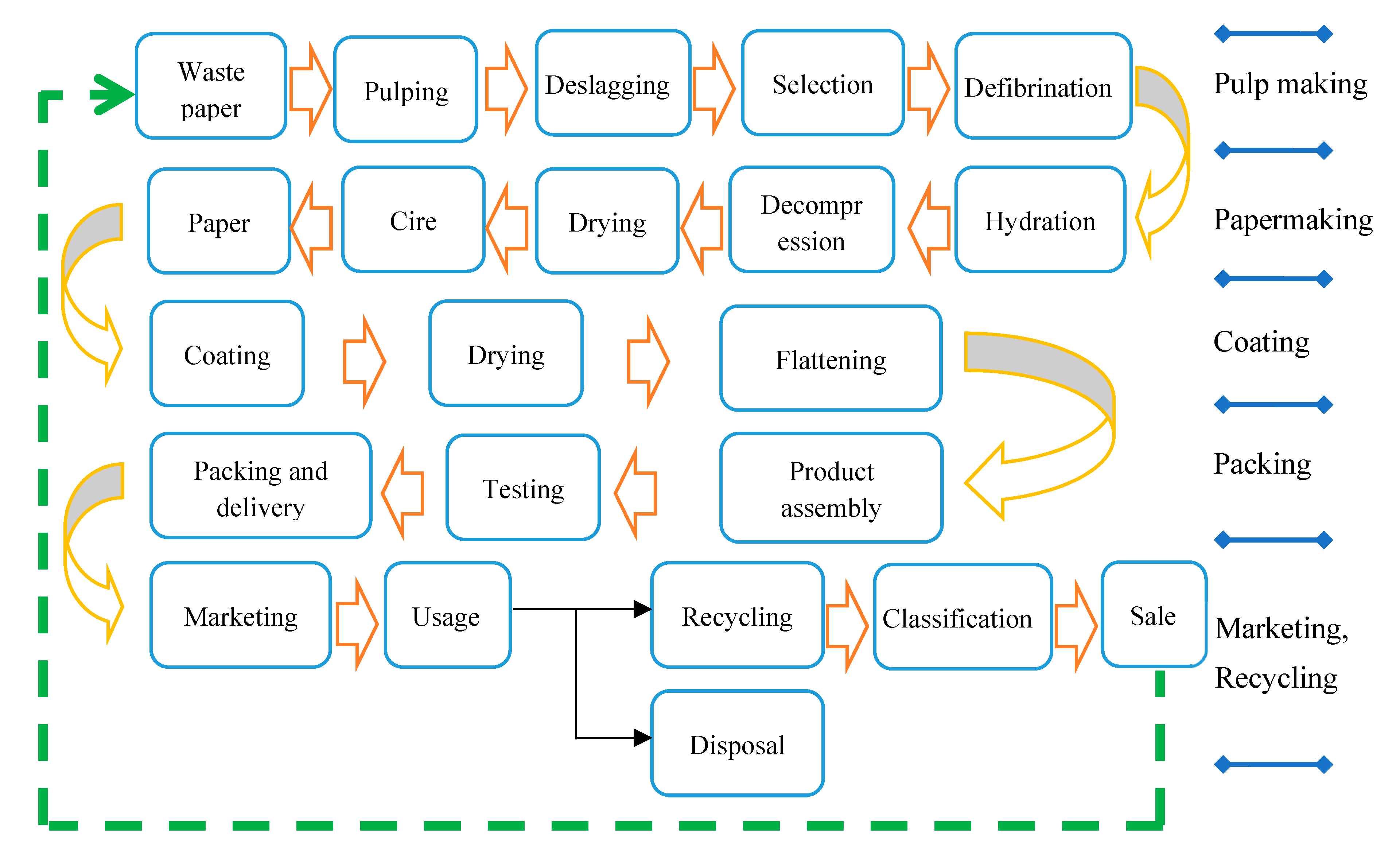

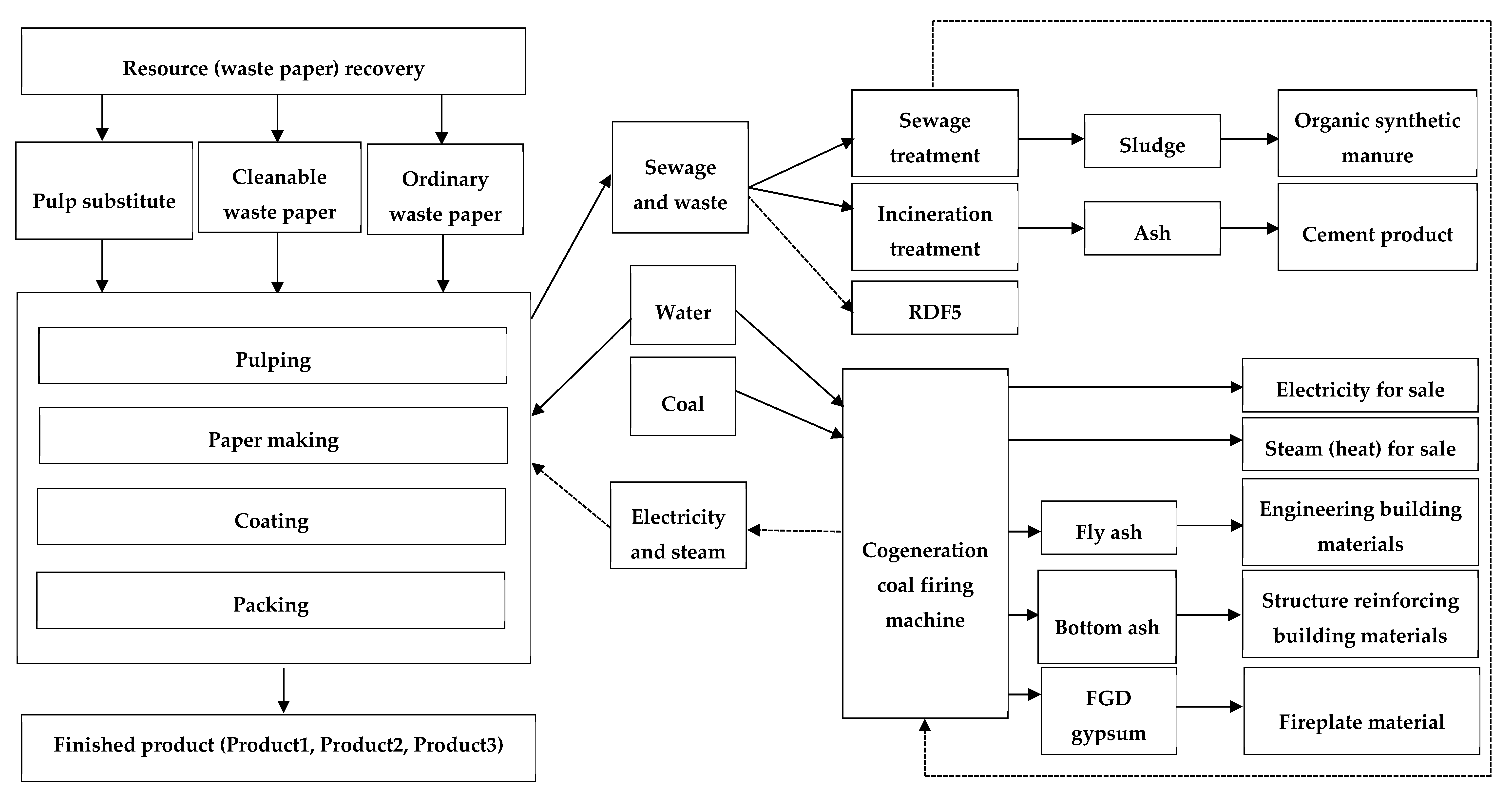

2. Sustainable Management under Green Paper Industry

2.1. Green Innovation in Paper Industry

2.2. MIP Model for Green Paper Industry

2.3. ABC and TOC

3. Problem Statement and Model Formulation

3.1. The Objective Function

3.2. Revenue of Main Products and Byproducts

3.3. Direct Material and Expense

3.4. Unit-Level Activity Cost

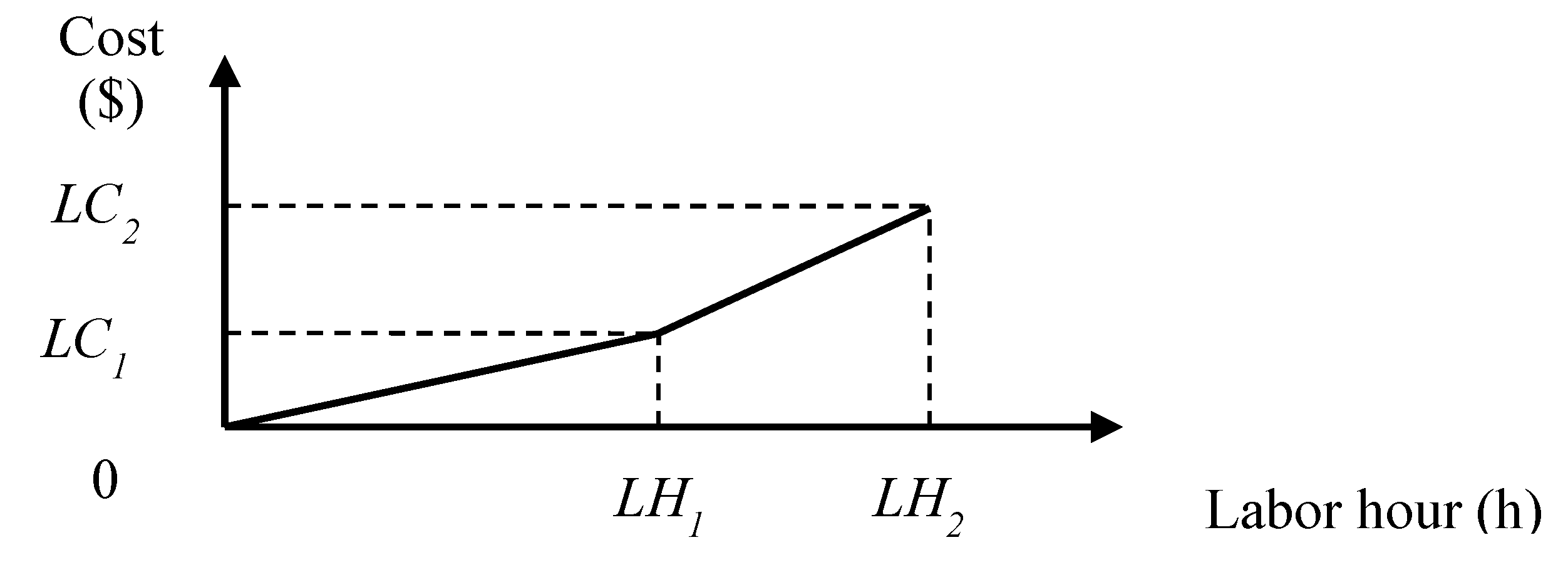

3.5. Direct Labor Cost

3.6. Batch-Level Activity Cost

3.7. Product-Level Activity Cost

3.8. Machine Cost

3.9. Benefit of Using RDF-5

4. Numerical Example

4.1. Description of the Case Problem

4.2. Analysis

4.3. Sensitivity Analysis

5. Discussion

5.1. Managerial Implications

5.2. Limitations

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Notations

| Corporate profit; | |

| Xi | Quantity of product i; |

| Unit price of product i; | |

| cs | Unit price of byproduct s |

| bis | The quantity of byproduct s of one unit of product i |

| Saved pth steam costs, when p = 1, the preferential rate is applicable; when p = 2, the basic preferential rate is applicable; when p = 3, the excess rate is applicable; | |

| Saved pth steam machine hours, when p = 1, the preferential rate is applicable; when p = 2, the basic preferential rate is applicable; when p = 3, the excess rate is applicable; | |

| Saved qth electric power costs, when q = 1, the preferential rate is applicable; when q = 2, the basic preferential rate is applicable; when q = 3, the excess rate is applicable; | |

| Saved qth generating machine hours, when q = 1, the preferential rate is applicable; when q = 2, the basic preferential rate is applicable; when q = 3, the excess rate is applicable; | |

| Saved activity driver demands of unit-level activity j (j ∈ U) for steam machine hours of one-unit product i; | |

| Saved activity driver demand of unit-level activity j (j ∈ U) for generating machine hours of one-unit product i; | |

| Unit cost of mth raw material; | |

| Unit cost of mth raw material; mth raw material demand of one-unit product I; | |

| Available quantity of raw material Q. | |

| Running activity cost per activity driver for activity j; | |

| Activity driver demand of unit-level activity j (j ∈ U) of one-unit product i; | |

| Total direct labor cost in (see Figure 2); | |

| Total direct labor cost in (see Figure 2); | |

| Total labor hours needed for the company; | |

| Upper limit of total direct labor hours of normal work (see Figure 2); | |

| Upper limit of total direct labor hours including overtime work (see Figure 2); | |

| The quantity of resource used by each batch-level activity j (j ∈ B) for product i; | |

| The number of batches for batch-level activity j (j ∈ B) used by product i; | |

| The quantity of product i for each batch-level activity j (j ∈ B); | |

| The quantity available for the activity driver of batch-level activity j (j ∈ B). | |

| Demand of activity driver needed by product-level activity j (j ∈ P) for product i; | |

| Production indicator of product i; If (Ri = 1), then product i will be produced. Otherwise, (Ri = 0); | |

| Maximum demand for product i; | |

| The quantity available for the activity driver of activity j (j ∈ P). | |

| Total machine cost in (see Figure 3); | |

| Machine hours of kth level capacity (see Figure 3); | |

| SOS1 set of 0–1 variables (special order of the first kind), where one and only one variable must be nonzero; = 1 means that machine hour is expanded to . | |

| Machine hour demand for one unit of product i; | |

| Environmental management cost; | |

| Processed gas p; | |

| The total quantity of gas p from product i.; | |

| G | The quantity of carbon equivalent of various gases allowed to be emitted from the mill paper-making process. |

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Z = [(income from main paper products) + (relevant byproducts) + (saved electric power cost) + (saved steam cost)] − [(unit-level activity cost: total material cost + total expense + total direct labor cost+ total machine cost) + (batch-level activity cost) + (product-level activity cost) + (total facility-level activity cost) + environmental management cost] | ||

| =(320 + 280 + 250) + {[0.8*(5 + 6 + 7)] + [0.5*( + 2 + 3)] + [0.035*(10 + 12 + 15)] + [0.02*(10 + 12 + 15)] + [0.2*(23 + 25 + 30)] + [0.05*(23 + 25 + 30)] + [0.7*(23 + 25 + 30)]} + (92,000 + 101,200 + 108,100) + (32,000 + 35,200 + 37,600) − {[(20*3 + 15*4 + 5*2) + (20*2 + 15*3 + 5*4) + (20*1 + 15*2 + 5*7)] + [(1*10 + 2*23) + (1*12 + 2*25) + (1*15 + 2*30)] + (38,204 + 62,082) + [(6*1) + (6*2) + (6*3)] + [(14*2) + (14*3) + (14*4)] + (2*3) + (2*4) + (2*5)] + [(1*2) + (1*2) + (1*3)] + [(100*15) + (100*12) + (100*18)] + (85,600 + 98,975 + 115,025) + 20,000 = 160.9 + 143.21 + 126.425 + 92,000 + 101,200 + 108,100 + 32,000 + 35,200 + 37,600 − 38,204 − 62,082 − 85,600 − 98,975 − 115,025 − 6 − 12 − 18 − 28 − 42 − 56 − 6 − 8 − 10 − 2 − 2 − 3 − 1500 − 1200 − 1800 − 20,000 | ||

| Subject to: | ||

| Raw material and expense constraints: | Stepwise facility-level machine hour constraints: Direct labor constraints: | Batch-level production activity constraints: Batch-level preparation activity constraints: |

| Batch-level treatment activity constraints: | Batch-level cutting activity constraints: Product-level constraints: Saved electric power cost = Constraints: Saved steam cost = Constraints: | Estimated data of different gases emitted from the mill paper-making process: NOx: 0.0006*(23 + 25 + 30) CO2: 0.54*(23 + 25 + 30) SO2: 0.0000024*(23 + 25 + 30) CO: 0.00012*(23 + 25 + 30) COD: 0.0009*(23 + 25 + 30) BOD: 0.00006*(23 + 25 + 30) SS: 0.000075*(23 + 25 + 30) AOX: 0.0000009*(23 + 25 + 30) In order to conform to the environmental protection policy, the carbon equivalent of the company should not exceed 80,000 units. |

References

- United Nations Framework on Climate Change (UNFCC). Adoption of the Paris Agreement. In the Report of the Conference of the Parties on its twenty-first session (held in Paris from 30 November to 13 December 2015), Addendum, Report No. FCCC/CP/2015/10/Add.1. United Nations, 29 January 2016. Available online: http://unfccc.int/resource/docs/2015/cop21/eng/10a01.pdf (accessed on 29 April 2020).

- Tsai, W.-H.; Yang, C.-H.; Chang, J.-C.; Lee, H.-L. An Activity-Based Costing decision model for life cycle assessment in green building projects. Eur. J. Oper. Res. 2014, 238, 607–619. [Google Scholar] [CrossRef]

- Georgiadis, P.; Vlachos, D. The effect of environmental parameters on product recovery. Eur. J. Oper. Res. 2004, 157, 449–464. [Google Scholar] [CrossRef]

- Chen, W.Y.; Jim, C.Y. Resident valuation and expectation of the urban greening project in Zhuhai, China. J. Environ. Plan. Manag. 2011, 54, 851–869. [Google Scholar] [CrossRef]

- Srivastava, S. Green Supply Chain Management: A State-of-The-Art Literature Review. Int. J. Manag. Rev. 2007, 9, 53–80. [Google Scholar] [CrossRef]

- Liu, L.; Ma, X. Technology-based industrial environmental management: A case study of electroplating in Shenzhen, China. J. Clean. Prod. 2010, 18, 1731–1739. [Google Scholar] [CrossRef]

- Christmann, P. Effects of “Best Practices” of Environmental Management on Cost Advantage: The Role of Complementary Assets. Acad. Manag. J. 2000, 43, 663–680. [Google Scholar]

- Bansal, P.; Roth, K. Why Companies Go Green: A Model of Ecological Responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar]

- Majumdar, S.K.; Marcus, A.A. Rules versus Discretion: The Productivity Consequences of Flexible Regulation. Acad. Manag. J. 2001, 44, 170–179. [Google Scholar]

- Collado-Ruiz, D.; Ostad-Ahmad-Ghorabi, H. Comparing LCA results out of competing products: Developing reference ranges from a product family approach. J. Clean. Prod. 2010, 18, 355–364. [Google Scholar] [CrossRef]

- Yu, S.; Zhang, R. Life Cycle Assessment in Different Product Design Stages—A Coffee Pot Case Study. Appl. Mech. Mater. 2010, 34, 988–994. [Google Scholar] [CrossRef]

- Pati, R.K.; Vrat, P.; Kumar, P. Economic analysis of paper recycling vis-a-vis wood as raw material. Int. J. Prod. Econ. 2006, 103, 489–508. [Google Scholar] [CrossRef]

- Berglund, C.; Söderholm, P. An econometric analysis of global waste paper recovery and utilization. Environ. Resour. Econ. 2003, 26, 429–456. [Google Scholar] [CrossRef]

- Brandenburg, M.; Rebs, T. Sustainable supply chain management: A modeling perspective. Ann. Oper. Res. 2015, 229, 213–252. [Google Scholar] [CrossRef]

- Ilgin, M.A.; Gupta, S.M. Environmentally conscious manufacturing and product recovery (ECMPRO): A review of the state of the art. J. Environ. Manag. 2010, 91, 563–591. [Google Scholar] [CrossRef] [PubMed]

- Seuring, S. A review of modeling approaches for sustainable supply chain management. Decis. Support Syst. 2013, 54, 1513–1520. [Google Scholar] [CrossRef]

- Chen, Y.-S. The Driver of Green Innovation and Green Image – Green Core Competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Chen, Y.-S.; Lai, S.-B.; Wen, C.-T. The Influence of Green Innovation Performance on Corporate Advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Alsmadi, M.; Almani, A. Implementing an integrated ABC and TOC approach to enhance decision making in a Lean context. Int. J. Qual. Reliab. Manag. 2014, 31, 906–920. [Google Scholar] [CrossRef]

- Hui, I.K.; Chan, A.H.S.; Pun, K.F. A study of the Environmental Management System implementation practices. J. Clean. Prod. 2001, 9, 269–276. [Google Scholar] [CrossRef]

- Ambec, S.; Lanoie, P. Does it pay to be green? A systematic overview. Acad. Manag. Perspect. 2008, 22, 45–62. [Google Scholar]

- Gavronski, I.; Klassen, R.D.; Vachon, S.; do Nascimento, L.F.M. A resource-based view of green supply management. Transp. Res. Part E Logist. Transp. Rev. 2011, 47, 872–885. [Google Scholar] [CrossRef]

- Granek, F. Business value of toxics reduction and pollution prevention planning. J. Clean. Prod. 2011, 19, 559–560. [Google Scholar] [CrossRef]

- Repoussis, P.P.; Paraskevopoulos, D.C.; Vazacopoulos, A.; Hupert, N. Optimizing emergency preparedness and resource utilization in mass-casualty incidents. Eur. J. Oper. Res. 2016, 255, 531–544. [Google Scholar] [CrossRef]

- Russell, R.A.; Urban, T.L. Offsetting inventory replenishment cycles. Eur. J. Oper. Res. 2016, 254, 105–112. [Google Scholar] [CrossRef]

- Lei, L.; Lee, K.; Dong, H. A heuristic for emergency operations scheduling with lead times and tardiness penalties. Eur. J. Oper. Res. 2016, 250, 726–736. [Google Scholar] [CrossRef]

- Boonmee, A.; Sethanan, K. A GLNPSO for multi-level capacitated lot-sizing and scheduling problem in the poultry industry. Eur. J. Oper. Res. 2016, 250, 652–665. [Google Scholar] [CrossRef]

- Esmaeilbeigi, R.; Charkhgard, P.; Charkhgard, H. Order acceptance and scheduling problems in two-machine flow shops: New mixed integer programming formulations. Eur. J. Oper. Res. 2016, 251, 419–431. [Google Scholar] [CrossRef]

- Todosijević, R.; Benmansour, R.; Hanafi, S.; Mladenović, N.; Artiba, A. Nested general variable neighborhood search for the periodic maintenance problem. Eur. J. Oper. Res. 2016, 252, 385–396. [Google Scholar] [CrossRef]

- Amorim, P.; Curcio, E.; Almada-Lobo, B.; Barbosa-Póvoa, A.P.; Grossmann, I.E. Supplier selection in the processed food industry under uncertainty. Eur. J. Oper. Res. 2016, 252, 801–814. [Google Scholar] [CrossRef]

- Hästbacka, M.; Westerlund, J.; Westerlund, T. MISPT: A user friendly MILP mixed-time based production planning tool. In Computer Aided Chemical Engineering; Elsevier: Amsterdam, The Netherlands, 2007; Volume 24, pp. 637–642. [Google Scholar]

- Björk, K.-M.; Carlsson, C. The effect of flexible lead times on a paper producer. Int. J. Prod. Econ. 2007, 107, 139–150. [Google Scholar] [CrossRef]

- Korpunen, H.; Paltakari, J. Testing an activity-based costing model with a virtual paper mill. Nord. Pulp Pap. Res. J. 2013, 28, 146–155. [Google Scholar] [CrossRef]

- Jiang, X.-Y.; Wu, H.-H. Optimization of setup frequency for TOC supply chain replenishment system with capacity constraints. Neural Comput. Appl. 2013, 23, 1831–1838. [Google Scholar] [CrossRef]

- Andelkovic, P.; Andelkovic, A.; Dasic, P. The theory of constraints as a basis for production process improvement model. Актуальні Прoблеми Екoнoміки 2013, 10, 251–260. [Google Scholar]

- Lockhart, J.; Taylor, A. Environmental considerations in product mix decisions using ABC and TOC. Manag. Account. Q. 2007, 9, 13. [Google Scholar]

- Tsai, W.-H.; Chen, H.-C.; Leu, J.-D.; Chang, Y.-C.; Lin, T.W. A product-mix decision model using green manufacturing technologies under activity-based costing. J. Clean. Prod. 2013, 57, 178–187. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Chang, Y.-C.; Lin, S.-J.; Chen, H.-C.; Chu, P.-Y. A green approach to the weight reduction of aircraft cabins. J. Air Transp. Manag. 2014, 40, 65–77. [Google Scholar] [CrossRef]

- Dessureault, S.; Benito, R. Data mining and activity based costing for equipment replacement decisions Part 1–establishing the information infrastructure. Min. Technol. 2012, 121, 73–82. [Google Scholar] [CrossRef]

- Baptista, E.A.; Lucato, W.C.; Coppini, N.L.; Fortunato, F.A.D.S. Profit optimization in machining service providers using principles of the Theory of Constraints. J. Braz. Soc. Mech. Sci. Eng. 2013, 35, 347–355. [Google Scholar] [CrossRef]

- Cannon, J.N.; Cannon, H.M.; Low, J.T. Modeling tactical product-mix decisions: A theory-of-constraints approach. Simul. Gaming 2013, 44, 624–644. [Google Scholar] [CrossRef]

- Huang, S.-Y.; Chen, H.-J.; Chiu, A.-A.; Chen, C.-P. The application of the theory of constraints and activity-based costing to business excellence: The case of automotive electronics manufacture firms. Total Qual. Manag. Bus. Excell. 2014, 25, 532–545. [Google Scholar] [CrossRef]

- Yang, H.-L.; Chen, Z.-J.; Ji, Y.-F.; Zhang, Y. Operation optimization of distribution center based on time-driven activity-based costing. J. Dalian Marit. Univ. 2012, 4, 26. [Google Scholar]

- Tsai, W.-H. Green production planning and control for the textile industry by using mathematical programming and industry 4.0 techniques. Energies 2018, 11, 2072. [Google Scholar] [CrossRef]

- Tsai, W.-H. Carbon Taxes and Carbon Right Costs Analysis for the Tire Industry. Energies 2018, 11, 2121. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Hung, S.-J. A fuzzy goal programming approach for green supply chain optimisation under activity-based costing and performance evaluation with a value-chain structure. Int. J. Prod. Res. 2009, 47, 4991–5017. [Google Scholar] [CrossRef]

- Zeferino, J.A.; Antunes, A.P.; Cunha, M.C. Multi-objective model for regional wastewater systems planning. Civ. Eng. Environ. Syst. 2010, 27, 95–106. [Google Scholar] [CrossRef]

- Arribas, C.A.; Blazquez, C.A.; Lamas, A. Urban solid waste collection system using mathematical modelling and tools of geographic information systems. Waste Manag. Res. 2010, 28, 355–363. [Google Scholar] [CrossRef]

- Galante, G.; Aiello, G.; Enea, M.; Panascia, E. A multi-objective approach to solid waste management. Waste Manag. 2010, 30, 1720–1728. [Google Scholar] [CrossRef]

- Tsai, W.-H. A Green Quality Management Decision Model with Carbon Tax and Capacity Expansion under Activity-Based Costing (ABC)—A Case Study in the Tire Manufacturing Industry. Energies 2018, 11, 1858. [Google Scholar] [CrossRef]

- LINDO SYSTEMS INC. Archives—LINGO 15.0. Available online: https://www.lindo.com/index.php/2-uncategorised/160-archives-lingo-15-0 (accessed on 22 April 2020).

- Kim, Y.-W.; Han, S.-H.; Yi, J.-S.; Chang, S. Supply chain cost model for prefabricated building material based on time-driven activity-based costing. Can. J. Civ. Eng. 2016, 43, 287–293. [Google Scholar] [CrossRef]

- Mark, T.; Niraj, R.; Dawar, N. Uncovering customer profitability segments for business customers. J. Bus. Bus. Mark. 2012, 19, 1–32. [Google Scholar] [CrossRef]

- Askarany, D.; Yazdifar, H. An investigation into the mixed reported adoption rates for ABC: Evidence from Australia, New Zealand and the UK. Int. J. Prod. Econ. 2012, 135, 430–439. [Google Scholar] [CrossRef]

- Salim, I. Analyzing usage of activity based costing in commercial banking institutions of Tripoli Libya: A technological acceptance model approach. J. Appl. Sci. Res. 2012, 8, 414–419. [Google Scholar]

- Dwyer, R.; Lamond, D.; Lee, K.H. Why and how to adopt green management into business organizations? Manag. Decis. 2009, 47, 1101–1121. [Google Scholar]

- Liu, Z.L.; Anderson, T.D.; Cruz, J.M. Consumer environmental awareness and competition in two-stage supply chains. Eur. J. Oper. Res. 2012, 218, 602–613. [Google Scholar] [CrossRef]

- Muriana, C. An EOQ model for perishable products with fixed shelf life under stochastic demand conditions. Eur. J. Oper. Res. 2016, 255, 388–396. [Google Scholar] [CrossRef]

- Tanskanen, J.-H. Strategic planning of municipal solid waste management. Resour. Conserv. Recycl. 2000, 30, 111–133. [Google Scholar] [CrossRef]

- Zhu, D.-S.; Lin, Y.-P.; Huang, S.-Y.; Lu, C.-T. The effect of competitive strategy, task uncertainty and organisation structure on the usefulness and performance of management accounting system (MAS). Int. J. Bus. Perform. Manag. 2009, 11, 336–363. [Google Scholar] [CrossRef]

| (a) Example Data | ||||||||

|---|---|---|---|---|---|---|---|---|

| Data Category | Index & Activity-Driver | Activity | Parameter | Product 1 | Product 2 | Product 3 | Available Capacity | |

| Selling price | j | pi | 320 | 280 | 250 | |||

| Unit cost/price | ||||||||

| Material (Unit-level) | m = 1(pulp substitute) | $20.00/unit | ai1 | 3 | 2 | 1 | Q1 = 11,310 | |

| m = 2(cleanable waste paper) | $15.00/unit | ai2 | 4 | 3 | 2 | Q2 = 17,020 | ||

| m = 3(ordinary waste paper) | $5.00/unit | ai3 | 2 | 4 | 7 | Q3 = 24,750 | ||

| Expense | m = 4(water) | $1.00/unit | ai4 | 10 | 12 | 15 | Q4 = 70,400 | |

| m = 5(coal) | $2.00/unit | ai5 | 23 | 25 | 30 | Q5 = 147,960 | ||

| Selling byproduct | s = 1(electricity) | $0.80/unit | bi1 | 5 | 6 | 7 | ||

| s = 2(steam) | $0.50/unit | bi2 | 1 | 2 | 3 | |||

| s = 3(organic compost) | $0.035/unit | bi3 | 10 | 12 | 15 | |||

| s = 4(cement products) | $0.02/unit | bi4 | 10 | 12 | 15 | |||

| s = 5(building materials) | $0.20/unit | bi5 | 23 | 25 | 30 | |||

| s = 6(reinforced structural building materials) | $0.05/unit | bi6 | 23 | 25 | 30 | |||

| s = 7(fireplates) | $0.70/unit | bi7 | 23 | 25 | 30 | |||

| Unit-level activity | Machine hours | 1 | λi1 | 6 | 7 | 8 | ||

| Labor hours | 2 | λi2 | 4 | 5 | 6 | |||

| RDF5 saved cost | Electric energy | 3 | λi3 | 5 | 6 | 7 | ||

| Steam (heat) energy | 4 | λi4 | 1 | 2 | 3 | |||

| Batch-level activity | Activity-driver | Cost per activity driver | ||||||

| Pulping | Blending | $6 | 5 | αi5 μi5 | 1 3 | 2 2 | 3 1 | T5 = 7750 |

| Papermaking | Papermaking | $14 | 6 | αi6 μi6 | 2 8 | 3 6 | 4 3 | T6 = 12,470 |

| Coating | Treatment | $2 | 7 | αi7 μi7 | 3 5 | 4 4 | 5 3 | T7 = 6100 |

| Packing | Packing | $1 | 8 | αi8 μi8 | 2 3 | 2 2 | 3 1 | T8 = 5400 |

| Product-level activity-Design | Drawings | $100 | 9 | ρi9 | 15 | 12 | 18 | D6 = 50 |

| Maximum demand | Vi | 2000 | 2500 | 3000 | ||||

| (b) Example data—facility level cost | ||||||||

| Environmental Management Cost | Total Cost | $20,000 | ||||||

| Machine hours constraint-Cost | MC0 = $85,600 | MC1 = $98,975 | MC2 = $115,025 | |||||

| Machine hours | MH0 = 42,800 | MH1 = 48,150 | MH2 = 53,500 | |||||

| Machine cost rate | mr0 = $2/h | mr1 = $2.5/h | mr2 = $3/h | |||||

| Direct labor constraint-Cost | LC1 = $38,204 | LC2 = $62,082 | ||||||

| Labor hours | LH1 =19,102 | LH2 = 28,653 | ||||||

| Wage rate | wr1 = $2/h | wr2 = $2.5/h | ||||||

| Power constraint | ||||||||

| Cost | SEC1 = $92,000 | SEC2 = $101,200 | SEC3 = $108,100 | |||||

| Hour | SGH1 = 36,800 | SGH2 = 41,400 | SGH3 = 46,000 | |||||

| Rate | PT1 = $2.5/10 thousand kWh | PT2= $2/10 thousand kWh | PT3 = $1.5/10 thousand kWh | |||||

| Steam(heat) constraint | ||||||||

| Cost | SSC1 = $32,000 | SSC2 = $35,200 | SSC3 = $37,600 | |||||

| Hour | SSH1 = 12,800 | SSH2 = 14,400 | SSH3 = 16,000 | |||||

| Rate | ST1 = $2.5/10 thousand kWh | ST2 = $2/10 thousand kWh | ST3 = $1.5/10 thousand kWh | |||||

| Symbol | Value | Symbol | Value | Symbol | Value | Symbol | Value |

|---|---|---|---|---|---|---|---|

| Z | $643,193.80 | 1250 batches | CO2 | 65,620.8 t | 0 | ||

| 1940 t | 480 batches | SO2 | 0.291648 t | 0 | |||

| 2500 t | 243 batches | CO | 14.5824 t | 0.577217 | |||

| 480 t | 417 batches | COD | 109.368 t | 0.422783 | |||

| $22,448.00 | 160 batches | BOD | 7.2912 t | 0 | |||

| $4190.00 | 388 batches | SS | 9.114 t | 1 | |||

| $1981.00 | 625 batches | AOX | 0.109368 t | 0 | |||

| $1132.00 | 160 batches | 1 | 0 | ||||

| $24,304.00 | 647 batches | 1 | 1 | ||||

| $6076.00 | 1250 batches | 1 | 0 | ||||

| $85,064.00 | 480 batches | 1 | 0 | ||||

| 647 batches | NOx | 72.912 t | 0 | 1 |

| Cost Decrease/Increase Ratio (%) | Profit | Increase/Decrease (Compared with the Initial Value) | Increase Profit | |

|---|---|---|---|---|

| pulp substitute | −30% | 710,993.8 | 10.54% | 67,800.0 |

| pulp substitute | −25% | 699,693.8 | 8.78% | 56,500.0 |

| pulp substitute | −20% | 688,393.8 | 7.03% | 45,200.0 |

| pulp substitute | −15% | 677,093.8 | 5.27% | 33,900.0 |

| pulp substitute | −10% | 665,793.8 | 3.51% | 22,600.0 |

| pulp substitute | −5% | 654,493.8 | 1.76% | 11,300.0 |

| pulp substitute | 0% | 643,193.8 | 0.00% | 0.0 |

| pulp substitute | 5% | 631,893.8 | −1.76% | −11,300.0 |

| pulp substitute | 10% | 620,593.8 | −3.51% | −22,600.0 |

| pulp substitute | 15% | 609,293.8 | −5.27% | −33,900.0 |

| pulp substitute | 20% | 597,993.8 | −7.03% | −45,200.0 |

| pulp substitute | 25% | 586,693.8 | −8.78% | −56,500.0 |

| pulp substitute | 30% | 575,393.8 | −10.54% | −67,800.0 |

| Cost Decrease/Increase Ratio (%) | Profit | Increase/Decrease (Compared with the Initial Value) | Increase Profit | |

|---|---|---|---|---|

| Cleanable waste paper | −30% | 716,183.8 | 11.35% | 72,990.0 |

| Cleanable waste paper | −25% | 704,018.8 | 9.46% | 60,825.0 |

| Cleanable waste paper | −20% | 691,853.8 | 7.57% | 48,660.0 |

| Cleanable waste paper | −15% | 679,688.8 | 5.67% | 36,495.0 |

| Cleanable waste paper | −10% | 667,523.8 | 3.78% | 24,330.0 |

| Cleanable waste paper | −5% | 655,358.8 | 1.89% | 12,165.0 |

| Cleanable waste paper | 0% | 643,193.8 | 0.00% | 0.0 |

| Cleanable waste paper | 5% | 631,028.8 | −1.89% | −12,165.0 |

| Cleanable waste paper | 10% | 618,863.8 | −3.78% | −24,330.0 |

| Cleanable waste paper | 15% | 606,698.8 | −5.67% | −36,495.0 |

| Cleanable waste paper | 20% | 594,533.8 | −7.57% | −48,660.0 |

| Cleanable waste paper | 25% | 582,368.8 | −9.46% | −60,825.0 |

| Cleanable waste paper | 30% | 570,203.8 | −11.35% | −72,990.0 |

| Cost Decrease/Increase Ratio (%) | Profit | Increase/Decrease (Compared with the Initial Value) | Increase Profit | |

|---|---|---|---|---|

| Ordinary waste paper | −30% | 669,252.8 | 4.05% | 26,059.0 |

| Ordinary waste paper | −25% | 664,882.8 | 3.37% | 21,689.0 |

| Ordinary waste paper | −20% | 660,512.8 | 2.69% | 17,319.0 |

| Ordinary waste paper | −15% | 656,142.8 | 2.01% | 12,949.0 |

| Ordinary waste paper | −10% | 651,813.8 | 1.34% | 8620.0 |

| Ordinary waste paper | −5% | 647,503.8 | 0.67% | 4310.0 |

| Ordinary waste paper | 0% | 643,193.8 | 0.00% | 0.0 |

| Ordinary waste paper | 5% | 638,883.8 | −0.67% | −4310.0 |

| Ordinary waste paper | 10% | 634,573.8 | −1.34% | −8620.0 |

| Ordinary waste paper | 15% | 630,263.8 | −2.01% | −12,930.0 |

| Ordinary waste paper | 20% | 625,953.8 | −2.68% | −17,240.0 |

| Ordinary waste paper | 25% | 621,643.8 | −3.35% | −21,550.0 |

| Ordinary waste paper | 30% | 617,333.8 | −4.02% | −25,860.0 |

| Increasing Ratio | Profit | Increase/Decrease (Compared with the Initial Value) | Increase Profit | |

|---|---|---|---|---|

| Pulp substitute | 0% | 643,193.8 | 0.00% | 0.0 |

| Pulp substitute | 5% | 654,512.8 | 1.76% | 11,319.0 |

| Pulp substitute | 10% | 654,512.8 | 1.76% | 11,319.0 |

| Pulp substitute | 15% | 654,512.8 | 1.76% | 11,319.0 |

| Pulp substitute | 20% | 654,512.8 | 1.76% | 11,319.0 |

| Pulp substitute | 25% | 654,512.8 | 1.76% | 11,319.0 |

| Pulp substitute | 30% | 654,512.8 | 1.76% | 11,319.0 |

| Increasing Ratio | Profit | Increase/Decrease (Compared with the Initial Value) | Increase Profit | |

|---|---|---|---|---|

| Clean waste paper | 0% | 643,193.8 | 0.00% | 0.0 |

| Clean waste paper | 5% | 654,512.8 | 1.76% | 11,319.0 |

| Clean waste paper | 10% | 654,512.8 | 1.76% | 11,319.0 |

| Clean waste paper | 15% | 654,512.8 | 1.76% | 11,319.0 |

| Clean waste paper | 20% | 654,512.8 | 1.76% | 11,319.0 |

| Clean waste paper | 25% | 654,512.8 | 1.76% | 11,319.0 |

| Clean waste paper | 30% | 654,512.8 | 1.76% | 11,319.0 |

| Increasing Ratio | Profit | Increase/Decrease (Compared with the Initial Value) | Increase Profit | |

|---|---|---|---|---|

| Ordinary waste paper | 0% | 643,193.8 | 0.00% | 0.0 |

| Ordinary waste paper | 5% | 643,193.8 | 0.00% | 0.0 |

| Ordinary waste paper | 10% | 643,193.8 | 0.00% | 0.0 |

| Ordinary waste paper | 15% | 643,193.8 | 0.00% | 0.0 |

| Ordinary waste paper | 20% | 643,193.8 | 0.00% | 0.0 |

| Ordinary waste paper | 25% | 643,193.8 | 0.00% | 0.0 |

| Ordinary waste paper | 30% | 643,193.8 | 0.00% | 0.0 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hsieh, C.-L.; Tsai, W.-H.; Chang, Y.-C. Green Activity-Based Costing Production Decision Model for Recycled Paper. Energies 2020, 13, 2413. https://doi.org/10.3390/en13102413

Hsieh C-L, Tsai W-H, Chang Y-C. Green Activity-Based Costing Production Decision Model for Recycled Paper. Energies. 2020; 13(10):2413. https://doi.org/10.3390/en13102413

Chicago/Turabian StyleHsieh, Chu-Lun, Wen-Hsien Tsai, and Yao-Chung Chang. 2020. "Green Activity-Based Costing Production Decision Model for Recycled Paper" Energies 13, no. 10: 2413. https://doi.org/10.3390/en13102413

APA StyleHsieh, C.-L., Tsai, W.-H., & Chang, Y.-C. (2020). Green Activity-Based Costing Production Decision Model for Recycled Paper. Energies, 13(10), 2413. https://doi.org/10.3390/en13102413