1. Introduction

India is one of the crucial actors when international climate mitigation goals are to be met. Today, the country already contributes almost 18% to the world’s population and is set to account for around one-quarter of the projected rise in global energy demand by 2040 [

1].

In 2015, India emitted 1869 Mt CO

2 in total, of which 51% came from power and heat generation. At present, the Central Electricity Authority of India (CEA) projects total estimated CO

2 emissions of 983 million tons for the year 2021–2022 and 1165 million tons in 2026–2027 [

2]. The main driver of this absolute increase is expected growth of total energy demand. The projected peak demand is 235 GW, with an overall energy requirement of 1611 TWh at the end of the year 2022 [

2]. Energy consumption is expected to rise further by 32% from 2022 to 2027 [

2].

India submitted its Intended Nationally Determined Contribution (INDC) on 1 October 2015. On the national level for India, it implies three key goals to achieve this agreement:

- (i)

to reduce the emissions per gross domestic product (GDP) output by 33% to 35% by 2030 from 2005 levels;

- (ii)

to increase the cumulative electric power installed capacity from non-fossil fuel-based energy resources up to 40% by 2030;

- (iii)

to create an additional carbon sink of 2.5–3 billion tons of CO

2 equivalent through additional forest and tree cover by 2030 [

3].

The Draft National Electricity Plan by the CEA [

2] includes the INDCs, targeting a path of electricity generation and reduction of greenhouse gas (GHG) emissions in line with the Paris pledges.

By contributing to global climate efforts, India pursues international but also domestic objectives. The adverse consequences of climate change have a significant impact on the Indian population and economy, as weather extremes influence the important agriculture sector and the security of food supply [

4]. Furthermore, the rise of the world temperature affects India through climate migration, water scarcity, and famine. In addition, the energy sector is an important element of India’s future development strategy, seeking to reduce poverty, reduce local pollutants, and assure access to electricity for all [

5]. Along with the aim to achieve the sustainable development goals (SDG), especially SDG7 “Ensure access to affordable, reliable, sustainable and modern energy for all” and SDG13 “Take urgent action to combat climate change and its impacts” established by the United Nations (UN), India seeks to make its energy system sustainable, and thereby enhance the population’s living conditions.

According to the 2015 Paris climate agreement, India will revise and resubmit its INDCs by 2020. In this context, the potential contributions of sustainable energy supply have received particular interest, e.g., the future of coal as the baseload power, the potential role of natural gas as a “transformation fuel”, and the potential of renewable energy to contribute to sustainable energy development. Given the global acceleration of renewable deployment, in particular solar energy, the INDCs currently developed for 2020 may be more ambitions than those back in 2015, and perhaps not even more expensive.

In addition to meeting targeted climate goals, India may benefit from a fast energy transition from both a sustainable energy and a geopolitical perspective, due to its current dependency on fossil fuels and energy imports [

6].

There is a broad and growing literature base on the perspectives of the Indian energy system, to which our paper seeks to contribute. Bhushan [

7,

8] laid out the principle challenges to governance of energy resources for India that are still valid today, e.g., the energy–poverty challenge, central and regional coordination, the role of coal, nuclear, and renewables, and the insertion of India into global resource markets and innovation systems. Bhushan [

8] stressed that India is expected to fulfill its INDC targets for 2030 easily and the focus now lies on the long-term planning. Identifying challenges, such as the need for improvements in the transmission infrastructure and facilitating access to low cost finance, is important for successful development. Currently, there is a market shift towards renewable energy sources (RES) through decreasing prices for renewable power generation, including a rapid innovation in technology [

9,

10].

The role of coal, and the competition with other fuels for financial resources and policy considerations, is also addressed by the Boston Consulting Group (BCG) [

11] and Tripathi et al. [

12].

The Indian energy sector has also been subject to model-based analysis in the context of recent policy and technology developments. In the context of the global sustainability initiative launched by Sachs [

13] and Transport Scenarios by Dhar et al. [

14], both studies identify possible challenges and opportunities of a low-carbon transformation of the energy and economic systems.

Löffler et al. [

15] developed a cost-minimal path for the global energy system up to 2050, including India as part of ten global regions. The paper focuses on the interdependencies between traditionally segregated sectors, including electricity, transportation, and heating. Due to the scale of the referenced model, detail within the model node India is lost, which this paper will address.

A comparably different model-based approach is chosen by the Integrated Research and Action for Development (IRADe) [

16]. The IRADe’s low-carbon sustainable development (LCSD) model is a dynamic, multi-sectoral and intertemporal linear programming activity analysis model based on an input–output framework. In addition to scenarios which target the compliance with CO

2 budgets of 155 Gt (LC1 scenario) and 133 Gt (LC2 scenario) for India by 2050 and a baseline scenario “dynamics as usual (DAU)”, the IRADe also includes human development thresholds and well-being indicators within the “visionary development (VD)”. The results of the LC1 and LC2 scenarios conclude that the CO

2 budgets can be met by 2050, but cause a decrease in the overall GDP growth throughout the years.

The Massachusetts Institute of Technology (MIT) has developed a multi-sector applied general equilibrium model of the Indian economy that uses CO

2 emissions from burning fossil fuels to generate a 2030 reference case [

17]. Sectoral imports and exports capture transactions with the rest of the world. The MIT developed various scenarios, such as the “emission intensity” scenario, which imposes India’s NDCs, and the “non-fossil scenario”, corresponding to India’s non-fossil electricity capacity target of 40% installed non-fossil electricity capacity by 2030. The “combined” scenario simulates the jointly pursued targets of both “emission intensity” and non-fossil electricity. While both “emission intensity” and “combined scenario” lead to the same emission intensity in 2030, the combined scenario includes the additional constraints of non-fossil electricity targets.

Shukla et al. propose an integrated modeling framework [

18,

19] for analyzing alternative development pathways with equal cumulative CO

2 emissions within the first half of the 21st century. They provide a comparison of alternative development strategies on multiple indicators, including energy security, air quality, and technology stocks. Short and long-term drivers of decarbonization pathways for several regions, including Europe, the United States, China, and India are explored in a multi-model decomposition analysis by Marcucci and Fragkos [

20]. Their research finds that in the short term, energy efficiency improvements are the key strategy to achieving current climate targets. In a joint project between the Indian planning office National Institution for Transforming India (NITI Aayog) and MIT, Singh et al. [

17] employed a numerical economy-wide model of India with energy sector detail to simulate the impact of India’s commitments to the Paris Climate Agreement.

Focusing on India’s important renewable potentials, Gulagi et al. [

21] explored the conditions under which India could be supplied by 100% RES by 2050. Similar exercises, with a lower level of detail, for a 100% renewables-based energy supply for India were prepared by Teske et al. [

22], Jacobsen et al. [

23] and Löffler et al. [

24]. International organizations, too, have put a focus on India and its energy challenges, such as the International Energy Agency (IEA) [

25] World Energy Outlook (“India Focus”). Shortcomings of the above-mentioned research, however, include a limited focus on electric power (no sector coupling), which will be addressed in this paper.

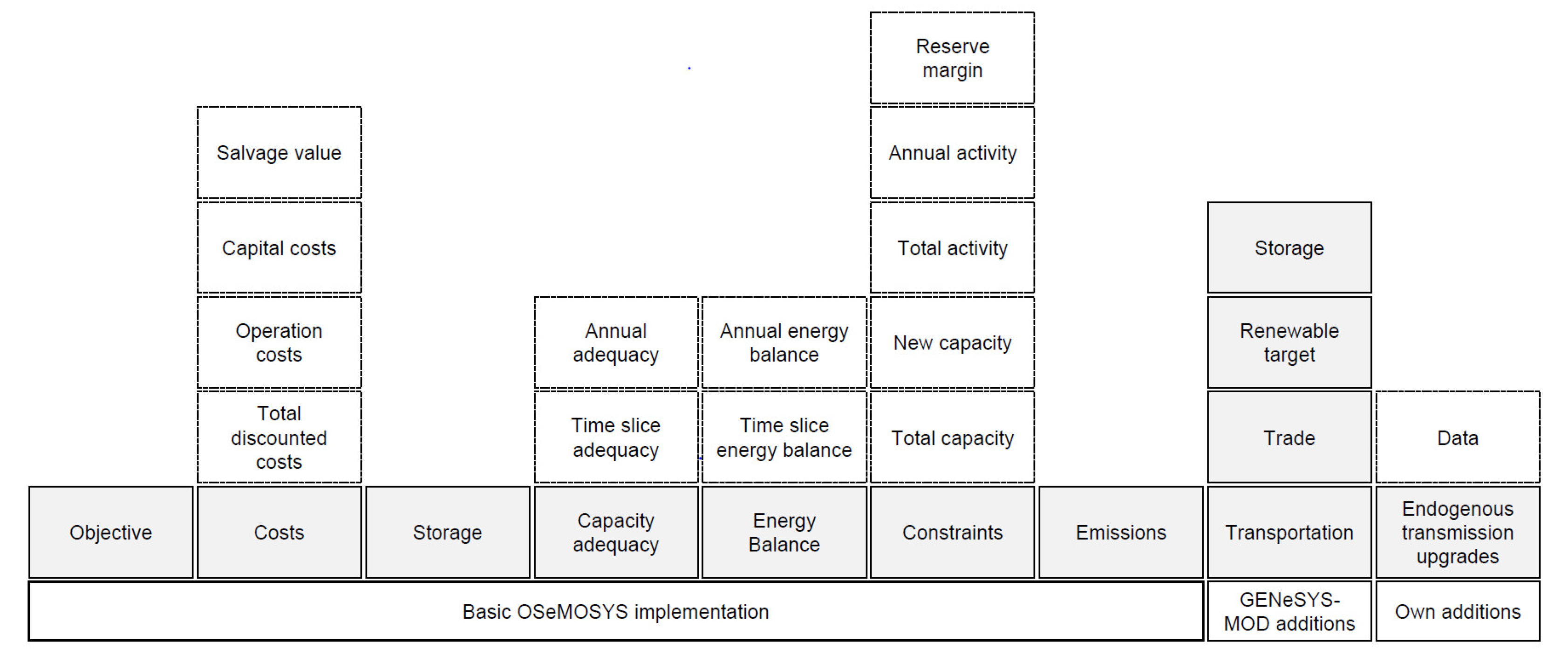

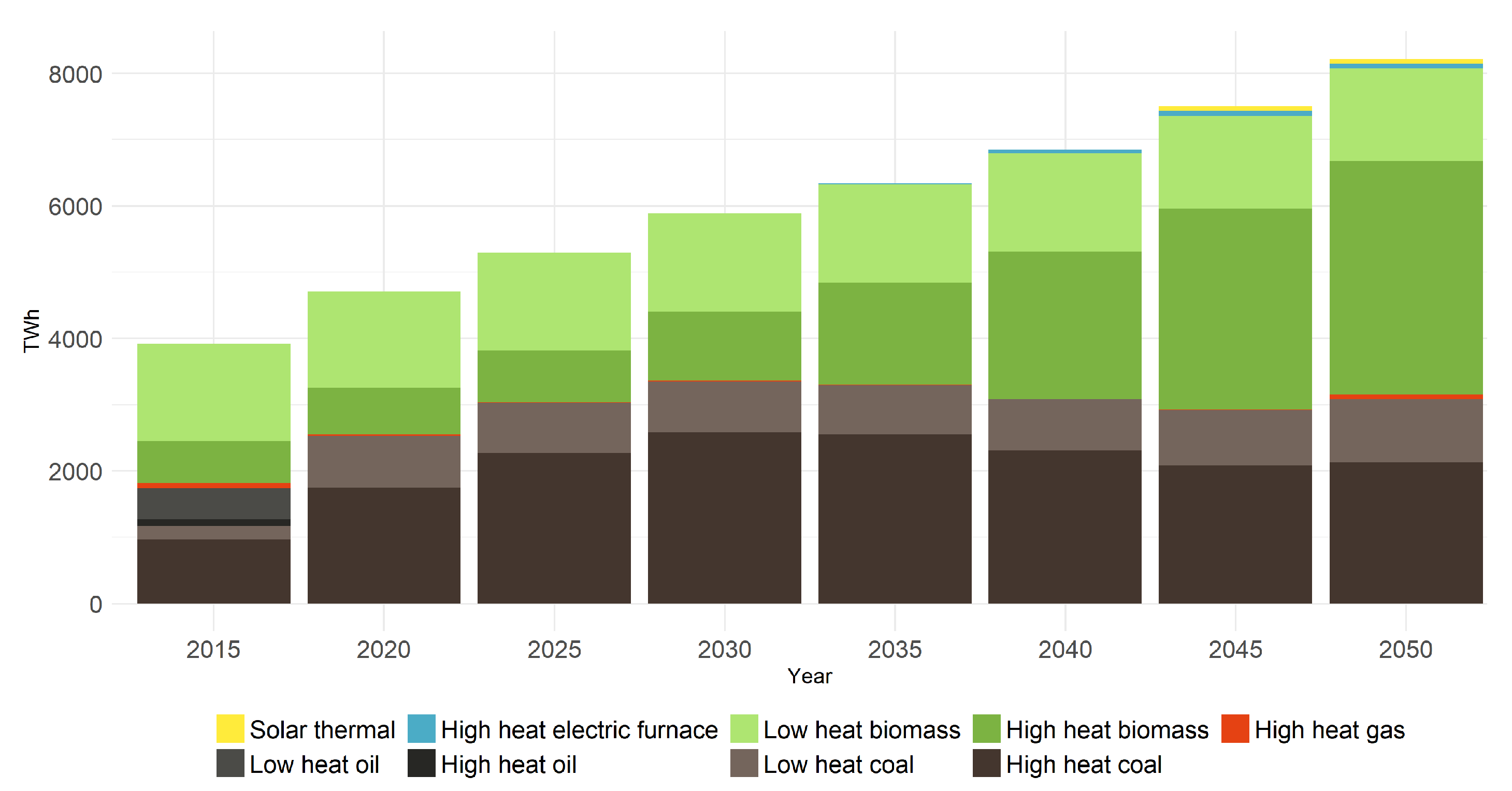

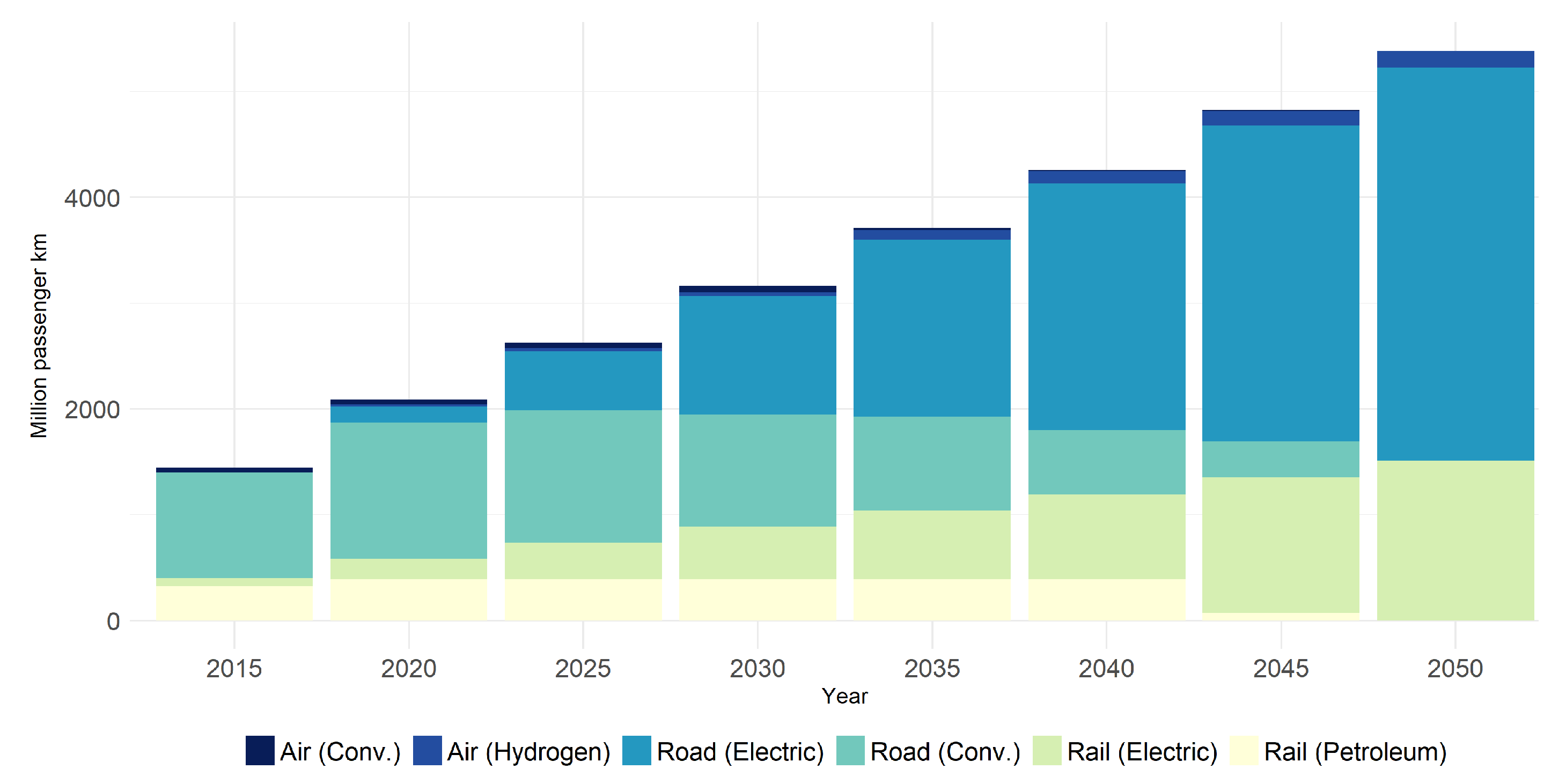

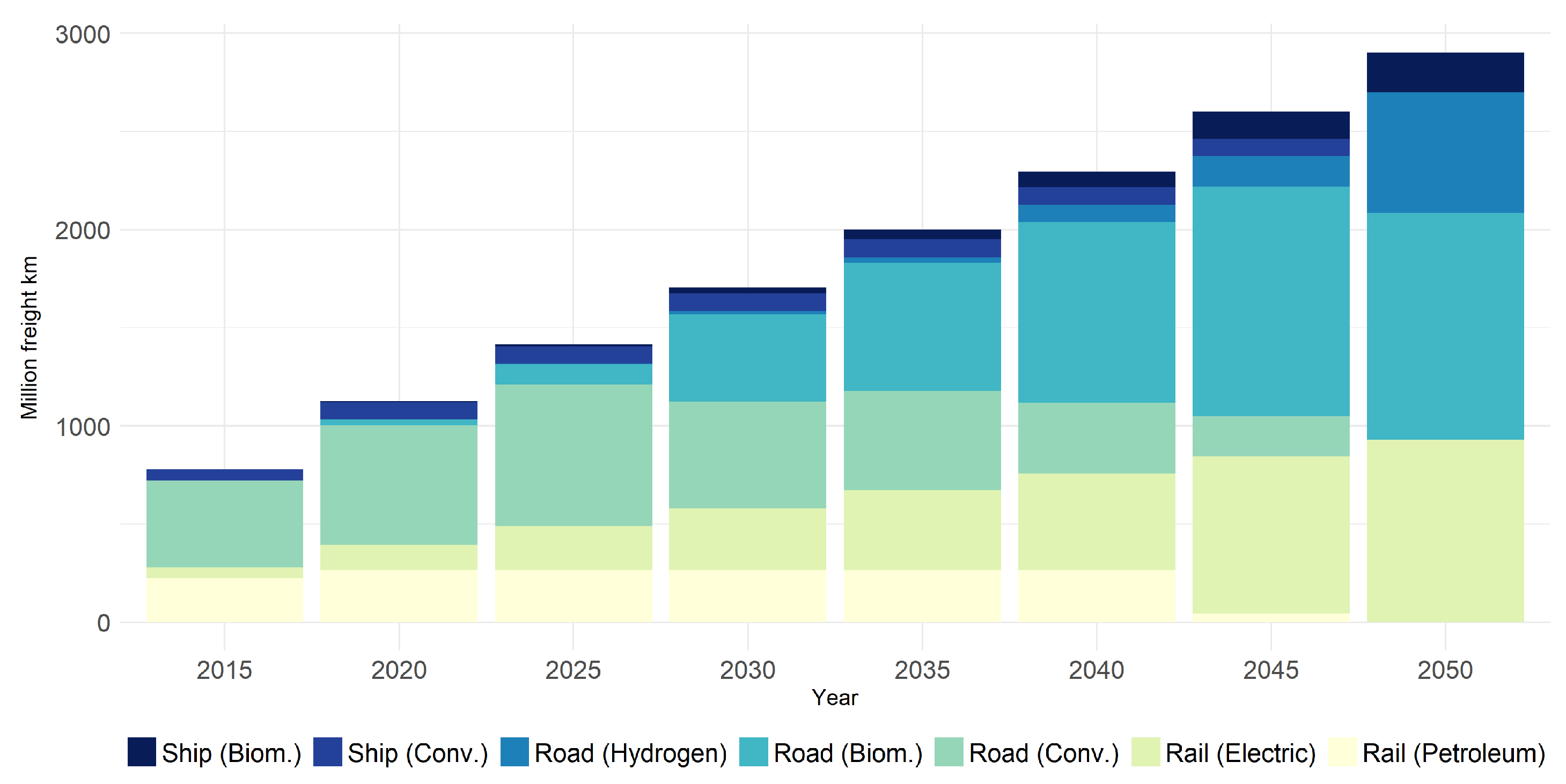

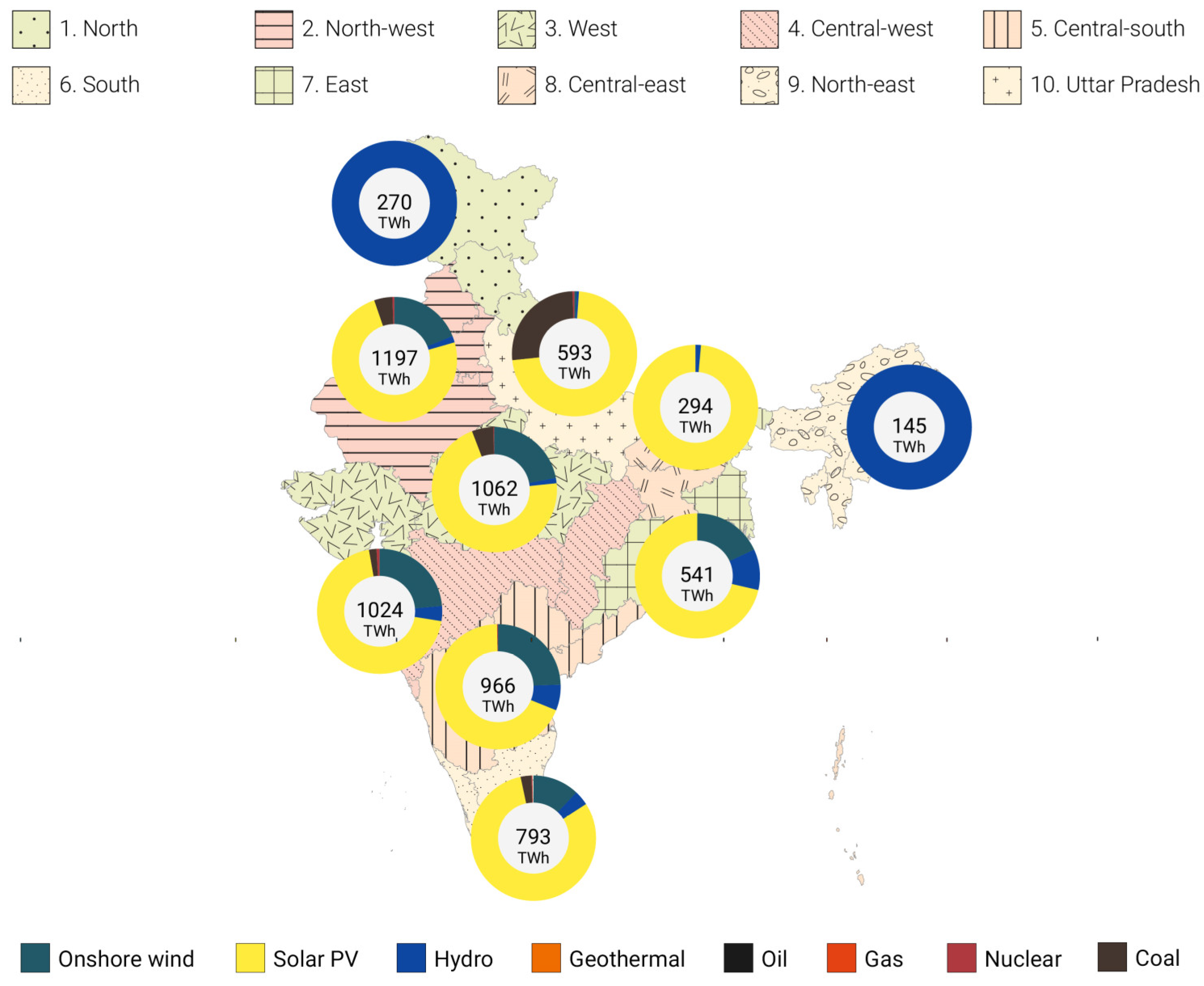

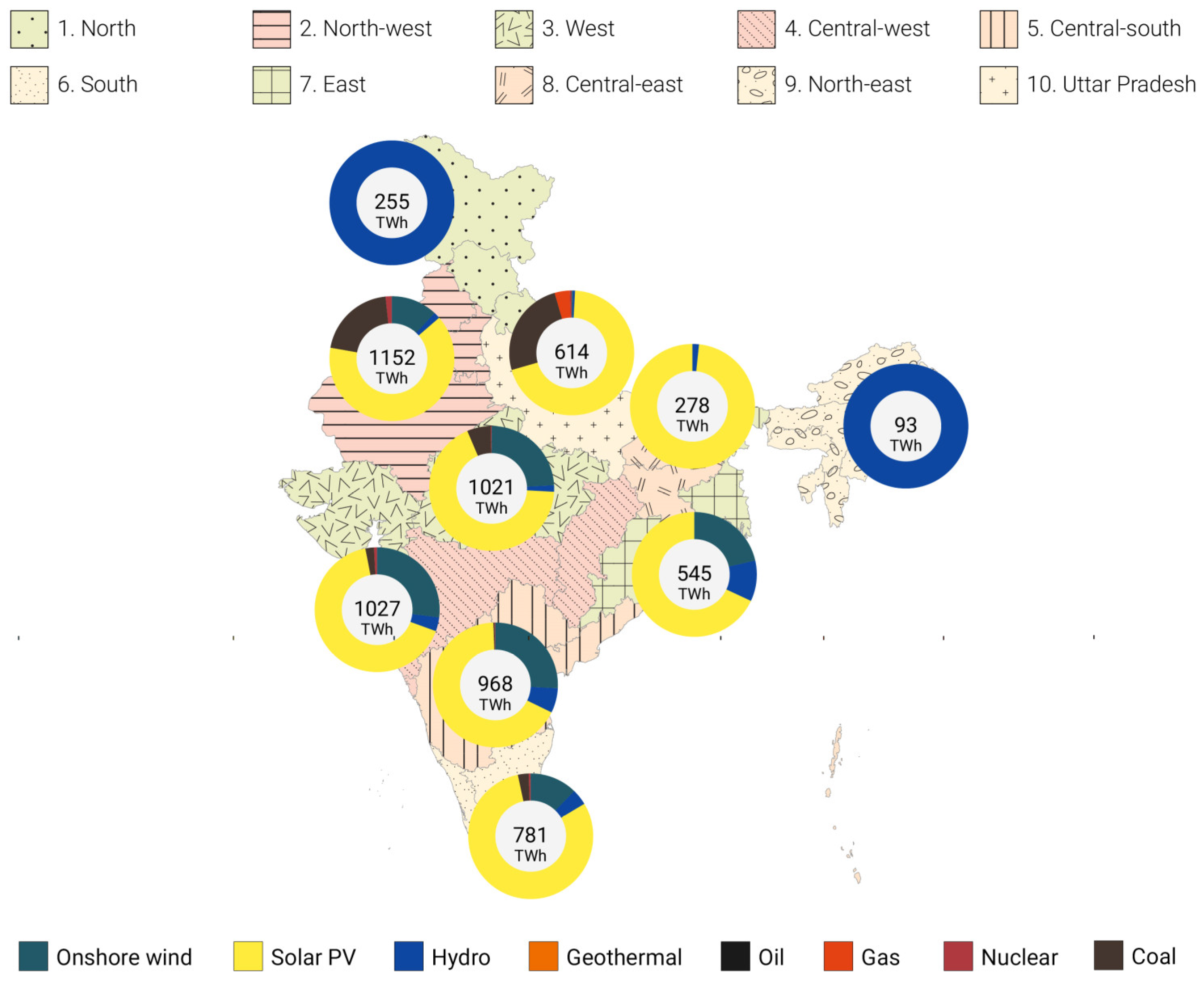

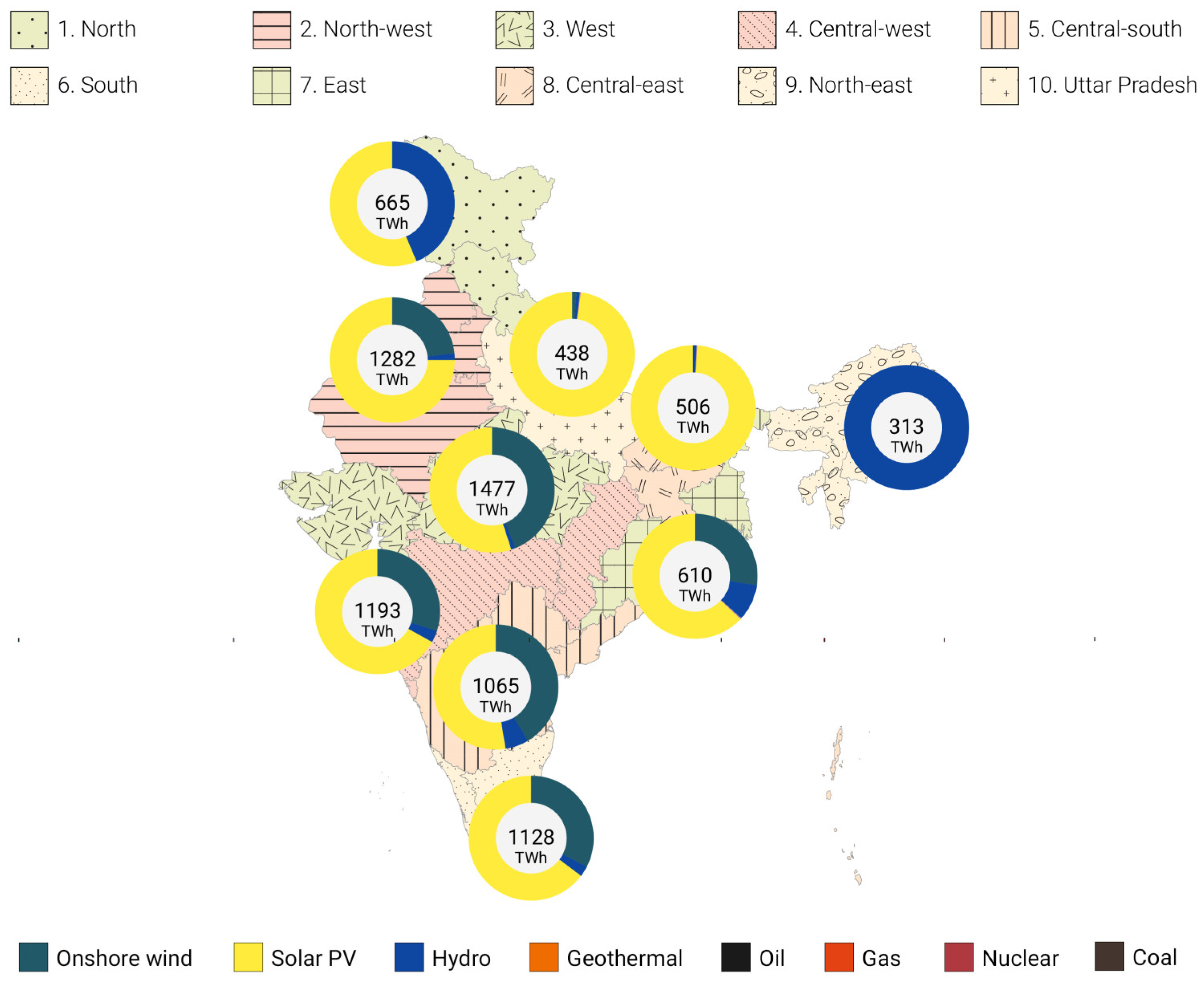

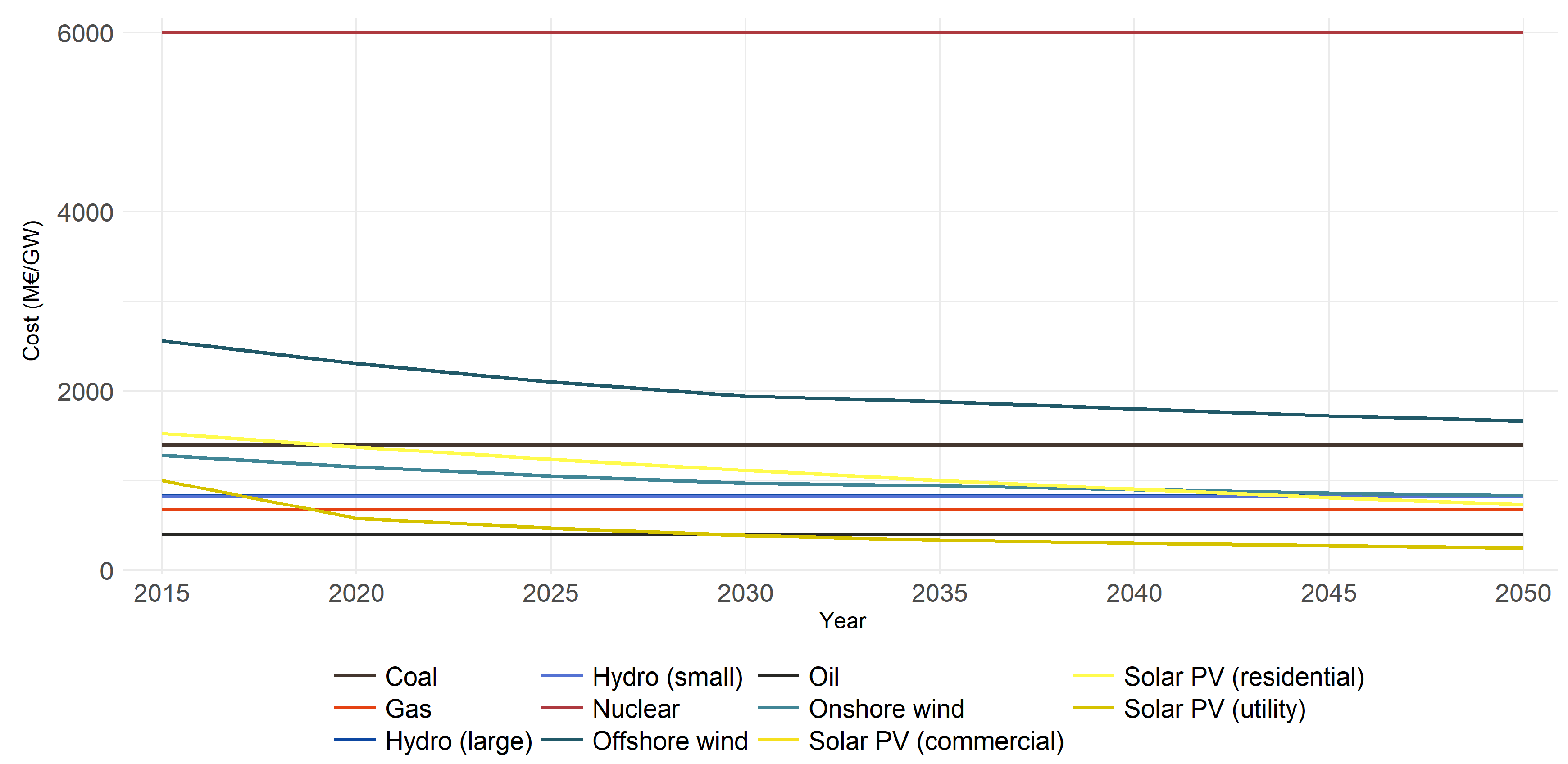

This paper adds to the existing literature by exploring alternative pathways to sustainable energy system development in India that respect both the specifics of the current energy system, but also stringent climate targets and global technological trends favoring non-fossil, low-cost solutions. We deploy an open-source linear cost-optimizing global energy system model (GENeSYS-MOD) to analyze different scenarios to meet increasing demand in India until 2050. A particular feature of the model is the regionalization of India into 10 regions. Thus, the model is able to illustrate regional idiosyncrasies, as well as potential imbalances, in the future energy system. The model not only focusses on the electricity sector, but also provides an in-depth analysis of the heat and transportation sectors. The implementation of different scenarios enables a qualitative comparison of the total cost for the specific optimized energy pathways until 2050. Thus, the results provide a comparability of the total cost of the different scenarios.

Projecting future energy scenarios for India also needs to account for other aspects besides the technical potential of renewables. An assessment of present literature and expert interviews is therefore used to set the modeled low-carbon energy transformation in context with the social, political and economic environment. The low-carbon transformation of the energy sector is not solely driven by climate consideration, but is inserted into a complex process of sustainable development that includes (amongst others) reducing health risk, affordable energy and a circular economy. In order to make an evaluation about whether the country is truly able to become mostly RES based in 2050, further implications on India’s energy transformation have to be considered. The main sources for the literature review regarding the contextualization of the model results were, in particular “The Political Economy of Clean Energy Transitions“ by Arent et al. [

26], which is a distilled compendium of cross-cutting academic projects on clean energy transitions, “India’s low carbon transition” by Pandey [

27], “India: Meeting Energy Needs for Development While Addressing Climate Change” by Joshi et al. [

28], and “Coal Transition in India-Assessing India´s energy transition options” by Vishwanathan et al. [

29].

After this introduction,

Section 2 sketches out the status quo of the energy system in India with respect to existing technologies and recent trends on policies and technological developments.

Section 3 provides a non-technical description of the model, and develops the three scenarios, the results of which are reported and discussed in

Section 4.

Section 5 identifies potential barriers to a low carbon transition and is followed by the concluding

Section 6.

6. Conclusions

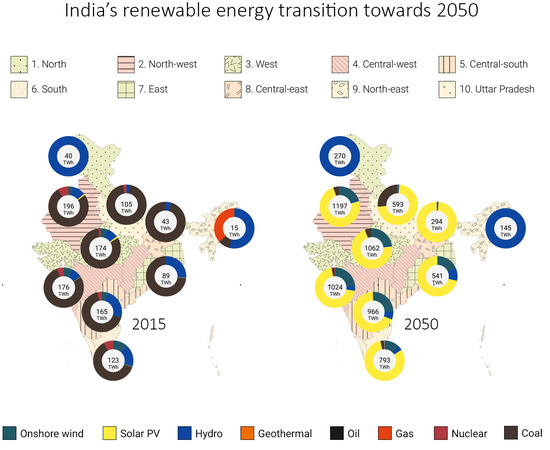

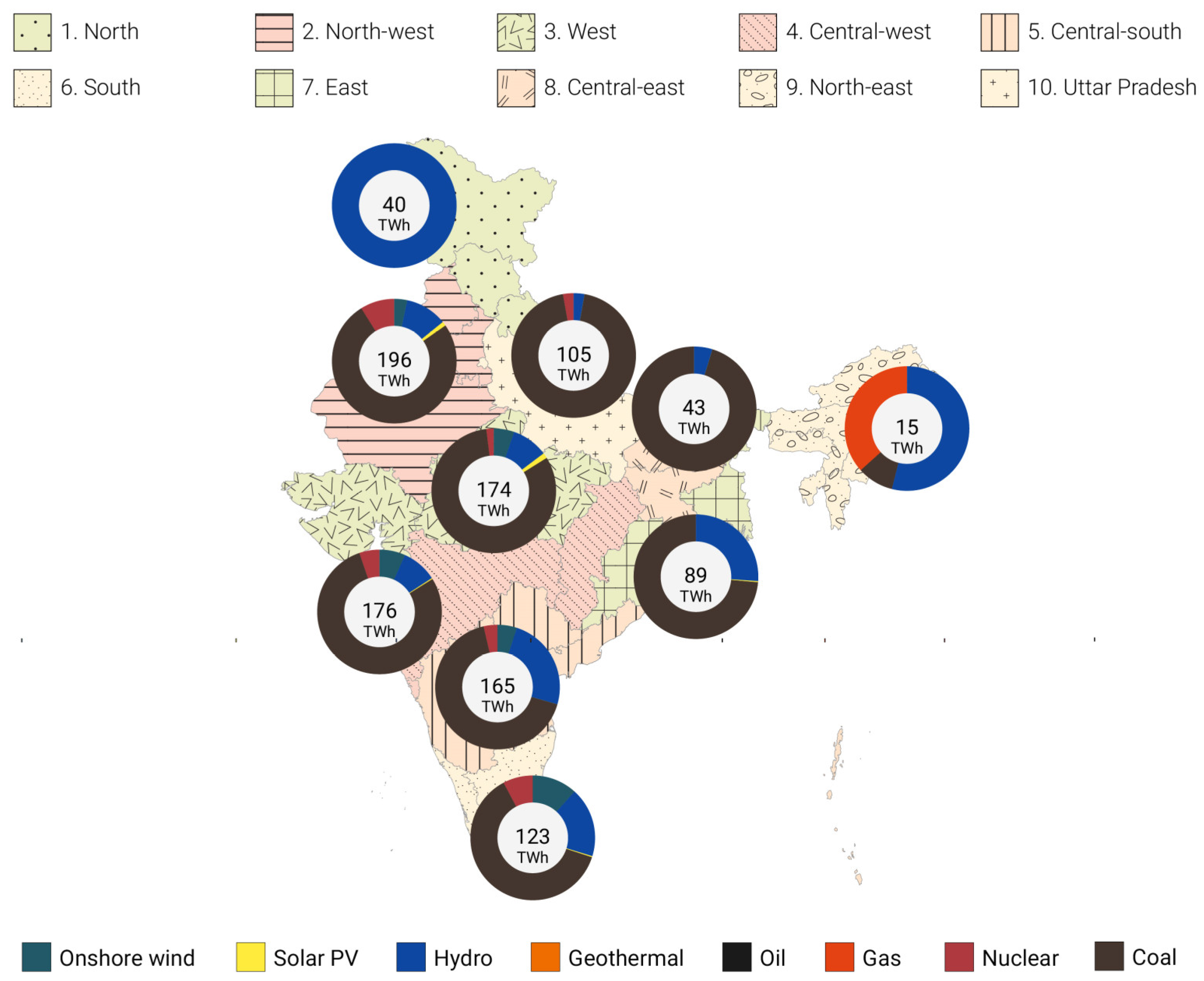

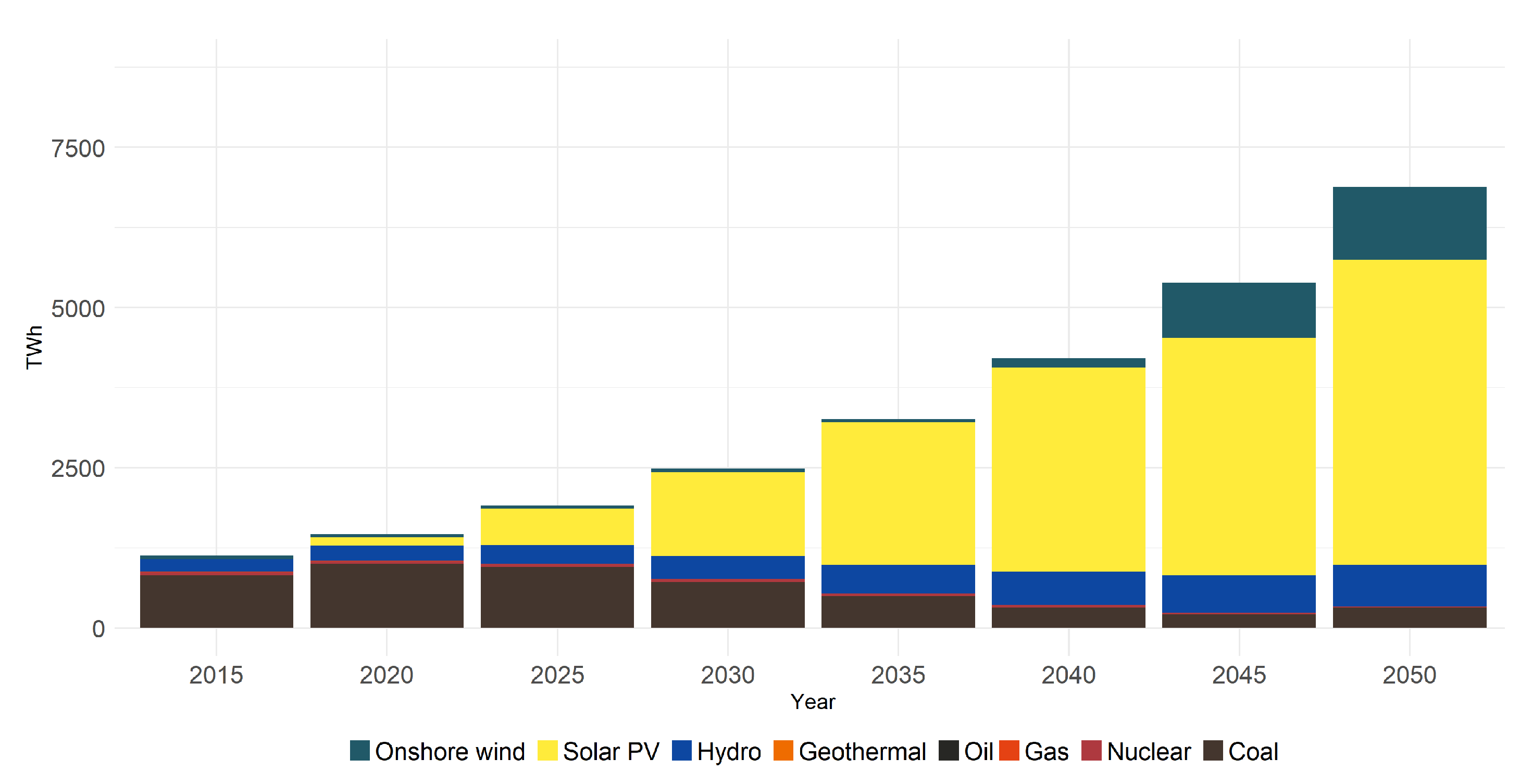

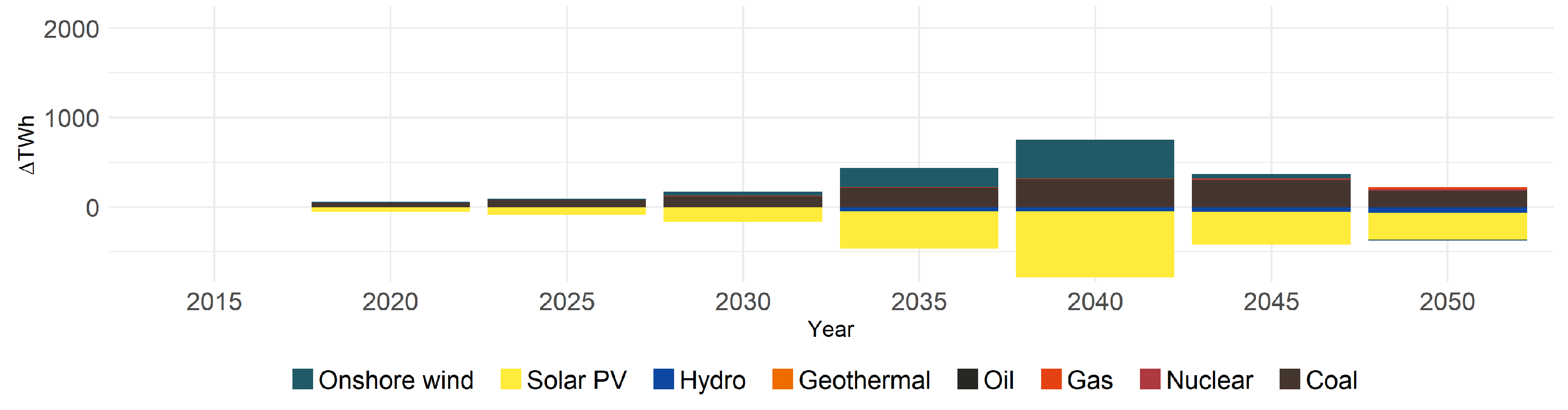

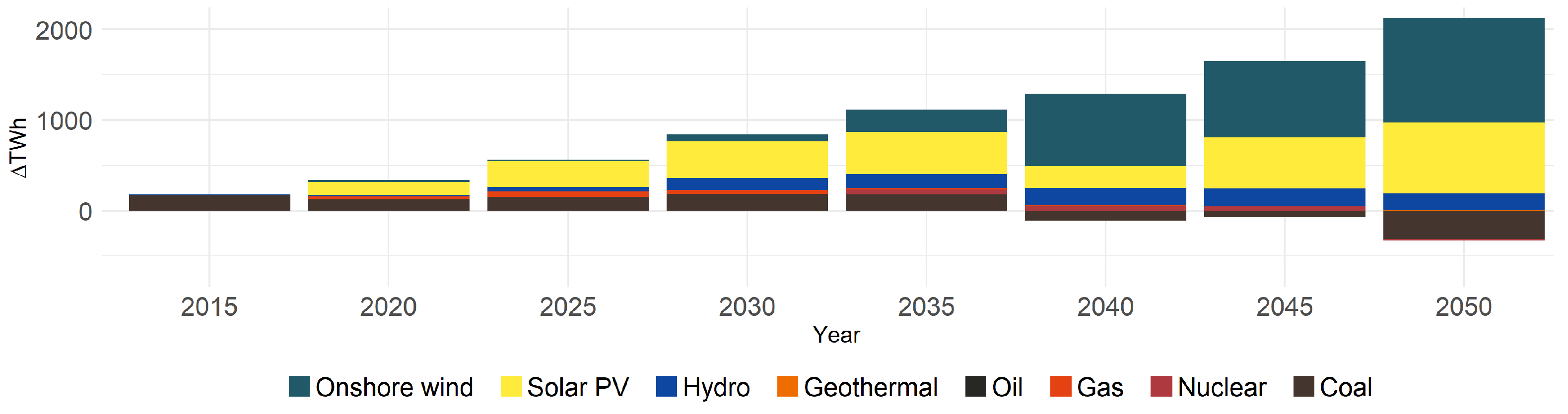

With 6% of global GHG emissions and a predicted future increase, India plays a determining role in future climate policies. In this paper, we explore energy pathways for India from 2015 to 2050 by applying the GENeSYS-MOD to different scenarios. The model results of the LEO scenario visualize the future importance of solar energy within the low-carbon transformation. Even without setting a strict restriction for using conventional energy sources in 2050, renewables (especially solar) will satisfy almost the whole energy demand in 2050, whereas conventional sources will have a negligible share of 2.8% (mainly located in densely populated regions, e.g., UP). In 2050, the share of solar takes over 67% of the whole power production, followed by wind (23%) and hydropower (6%) in the LEO scenario.

For progressive planning, crucial circumstances have to be kept in mind. First of all, India as a developing economy is facing an increasing demand in power, and energy access is an ongoing issue, especially in rural areas [

2]. Furthermore, within the conventional energy sources, the future of coal electrification depends on market design, the implementation of existing environmental norms, and regional development perspectives in affected areas. Apart from that, the recent growth of utility-scale solar needs to be accompanied by distributed solar (and batteries), both at the urban and the rural level, to become sustainable and extend the rural electrification progress. As current plans are perceived to be achieved before 2025, set goals submitted in the INDCs and the current Five-Year Plan are assessed as not ambitious enough. Moreover, it is illustrated within the BAU scenario that current electricity plans of the Indian government diverge from needed requirements to contribute to the global rising limit of 2 °C to pre-industrial levels. Tightening the government’s goals until 2030 would consequently both counterbalance and reduce the total cost of the path from there on to 2050, which is projected to be a largely renewable energy-based system. Consequently, fulfilling the Paris Agreement will require stronger efforts in India’s current policies, especially in the last two decades leading up to 2050 in comparison to a smoother and more cost-efficient increase of RES over time. While the model incorporates a high level of detail on a multitude of technologies, inter-sectoral-connections, and the resulting energy mix, its rather rough time disaggregation has to be noted. Variable renewable energy (VRE) technologies and their inherent unstableness, creating a need for flexibility options such as storage, might require a more detailed distinction between time slices. Future research should focus on how to implement such an assessment for even more detailed data on the different sectors and the effects of variable RES on the electricity system.

A reduction of the losses and tackling power theft within the power trade would ensure an efficient overcoming of imbalances in between the regions of different renewable energy potentials. Making up leeway in the transmission grid sector is one of the important actions. The results for the 100% RES scenario illustrate the cost-optimized pathway towards 2050 for a technically feasible energy system based on 100% RES, a finding which has been shown by Gulagi et al. [

21,

47] independently. Additionally, the difference between the LEO and 100% RES scenario in the use of conventional sources indicates that a 100% renewable energy supply is an ambitious goal for 2050. Noticing the negligibly higher total cost of an energy system based on 100% RES to the LEO benchmark or the BAU scenario, this goal may be ambitious but not impossible to achieve.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}