In this section, we discuss the option pricing model using the CGMYSV model. We define the model and calibrate its parameters using the European style, S&P 500 index option (SPX option) data, and the American style S&P 100 index option (OEX option) data.

Let

r and

q be the risk-free rate of return and the continuous dividend rate of a given underlying asset, respectively. The risk-neutral price process

of the underlying asset is assumed to be

where

is the CGMYSV process with parameters

,

,

,

,

,

,

,

. By (

6), we also have

4.1. Calibration to European Options

For the risk-neutral price process

defined by (

10), the European call and put prices, with strike price

K and time to maturity

T, are given by

and

, respectively. Using the fast Fourier transform (FFT) method of

Carr and Madan (

1999), we can calculate European call/put prices numerically. We calibrate the CGMYSV parameters

,

,

,

,

,

,

,

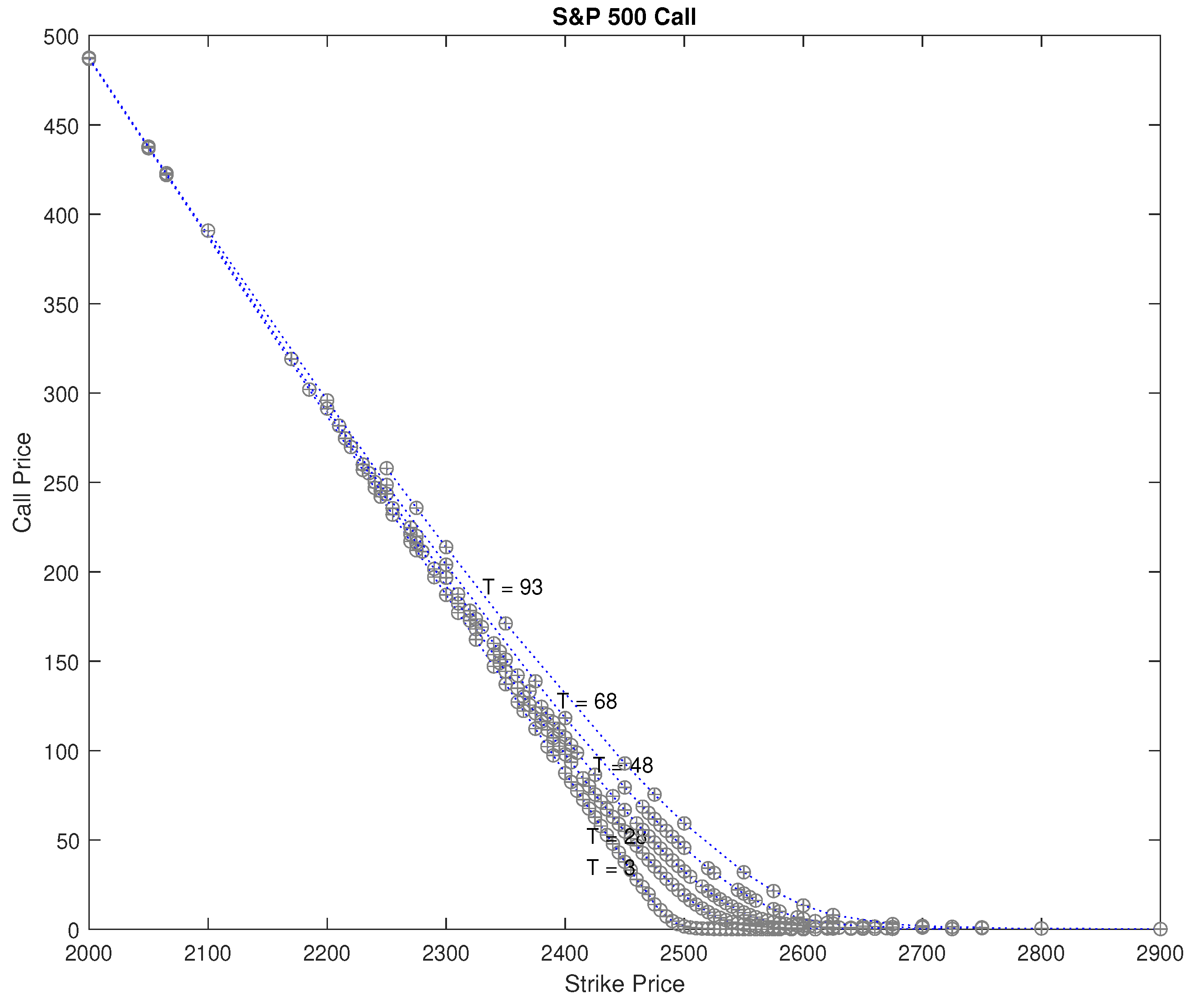

using the SPX option prices for 11 September 2017. We observed 247 call prices and 289 put prices on that day. The S&P 500 price,

, risk-free rate of return,

r, and continuous dividend rate,

q, on that day were

,

, and

. The calibration results for SPX calls and puts are provided in

Table 2.

Figure 3 shows observed SPX call and put prices, and calibrated CGMYSV prices using the FFT.

We recalculate the European call and put prices using the MCS method with the calibrated parameters from

Table 2. The sample paths of the MCS method are generated by Algorithm 1. We used 10,000 sample paths. To compare the MCS method with the FFT method, we use the four error estimators: the average absolute error (AAE), the average absolute error as a percentage of the mean price (APE), the average relative percentage error (ARPE), and the root mean square error (RMSE) (see

Schoutens (

2003)).

3 The measured values for these error estimators, for the FFT method and the MCS method, are in

Table 3. In all cases but one, for both the call and put cases, the MCS method has larger error values than the FFT method. This is not surprising because we calibrated the parameters using the FFT method. However, while larger, the error values for the MCS method are similar to those of the FFT method. That means the sample path generation with Algorithm 1 performs well, and prices by the MCS perform similarly to those for the FFT method.

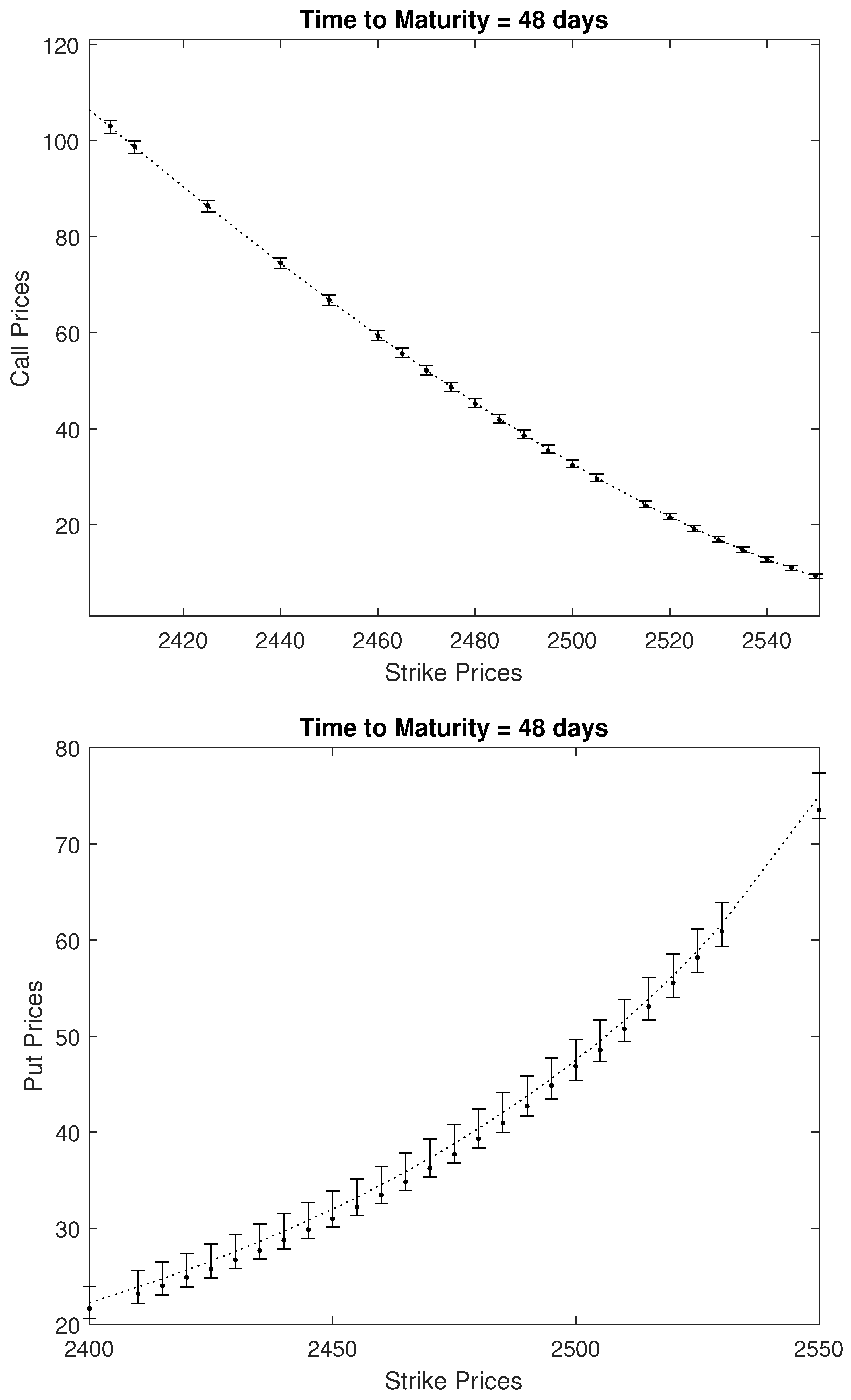

For the option prices computed with the MCS method, we obtain standard error estimates for each 247 call and 289 put option. (Not presented due to page limitations.) Instead, in

Figure 4, we plot MCS prices and the 95% confidence intervals for case

, and time to maturity

.

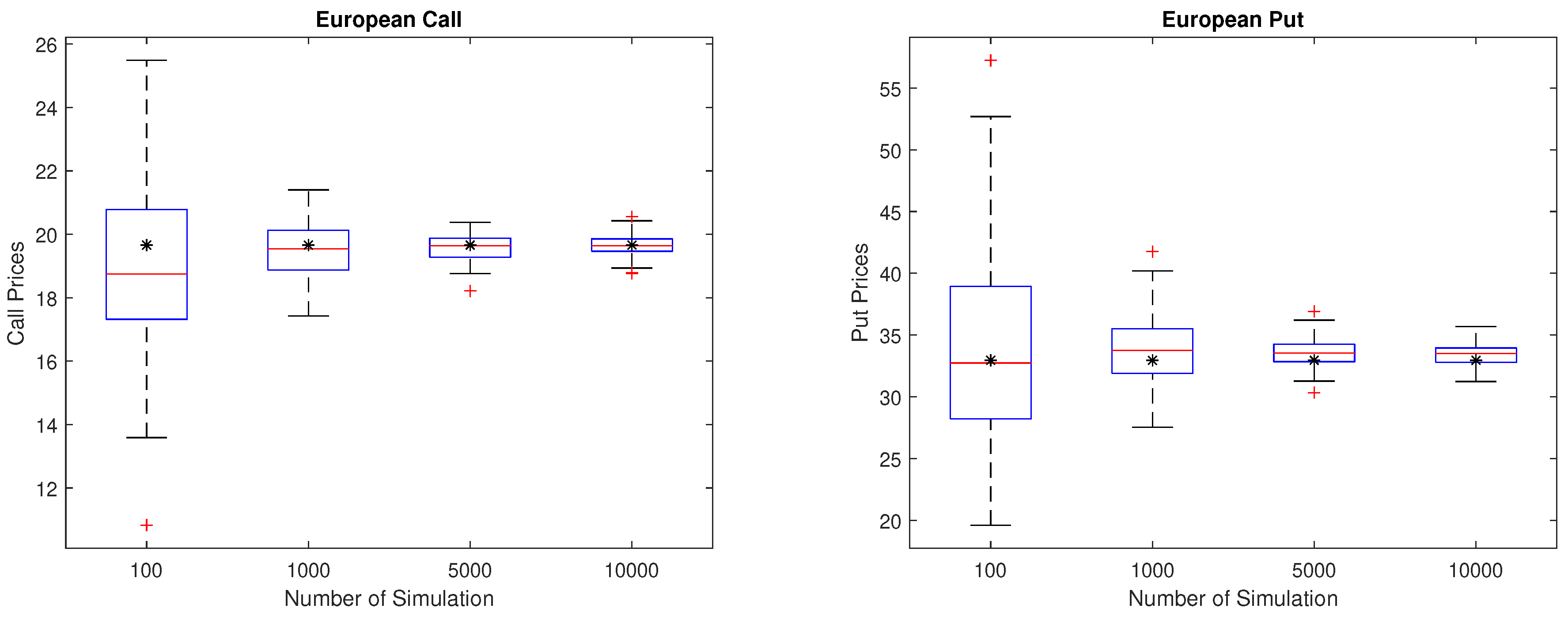

Finally, we perform the bootstrapping. We select an at-the-money call, and an at-the-money put of

and

as examples, and calculate call and put prices with the MCS parameters in

Table 2.

Table 4 shows that the MCS prices and their standard errors for 100, 1000, 5000, and 10,000 sample paths. We repeat this process 100 times. Boxplot summaries of the statistics for the resulting call and put prices for each number of sample paths are presented in

Figure 5. We also show (by the symbol ’*’) the call/put prices computed using the FFT method. We observe that, as the number of sample paths increases, the interquartile distance of MCS prices narrows to that of the FFT price and dispersions are reduced.

4.2. Calibration to American Options

In

Section 4.1, we have seen that the sample path generation method using the series representation works for the MCS method for European option pricing. In this section, we discuss the American option pricing with the same sample path generation method. We use the least squares regression method (LSM) of

Longstaff and Schwartz (

2001) for American option pricing with the MCS method. When we perform the regression for the expected value of an option, we consider

,

,

,

, and

as independent variables, following the idea in Chapter 15 of

Rachev et al. (

2011).

For empirical illustration, we use market prices of the American style OEX option. We calibrate the parameters of the CGMYSV model with fixed seed numbers for each random number generation. That is, we fix the seed value for the chi-square random number generator in the CIR process, and generate uniform and exponential random numbers

,

,

,

, and

with the predefined seed values. Then we set the model parameters, generate

sample paths using Algorithm 1 with the fixed seed number and the fixed random number sets, and then calculate American option price using LSM. We find the optimal model parameters to minimize RMSE. As a benchmark, we calibrate the parameters of the CGMY option pricing model (See

Carr et al. (

2002)) with the OEX option price data using LSM, with sample paths generated by the series representation explained in

Section 2.3.

The calibration results are presented in

Table 5. We calibrate the CGMY and the CGMYSV model parameters for 12 Wednesdays in 2015 and 2016. Values for the four error estimators, AAE, APE, ARPE, and RMSE, are provided in

Table 6. As smaller error values imply better calibration performance, smaller errors are written in bold letters.

Table 6 shows that the CGMYSV calibration performs better than the CGMY calibration, except for 10 February 2016, and 10 June 2015. On 9 March 2016, AAE and APE values for the CGMY model are less than those of CGMYSV, but ARPE and RMSE values for CGMY are larger than those for CGMYSV. The ARPE value for CGMY is smaller than that of CGMYSV on 10 November 2015, but the other three error values for CGMY are larger than that for CGMYSV. Therefore, we can conclude that, in this investigation, the CGMYSV option pricing model typically performs better than the CGMY option pricing model, except in a few cases. Hence, the LSM with Algorithm 1 works well for the American option calibration.

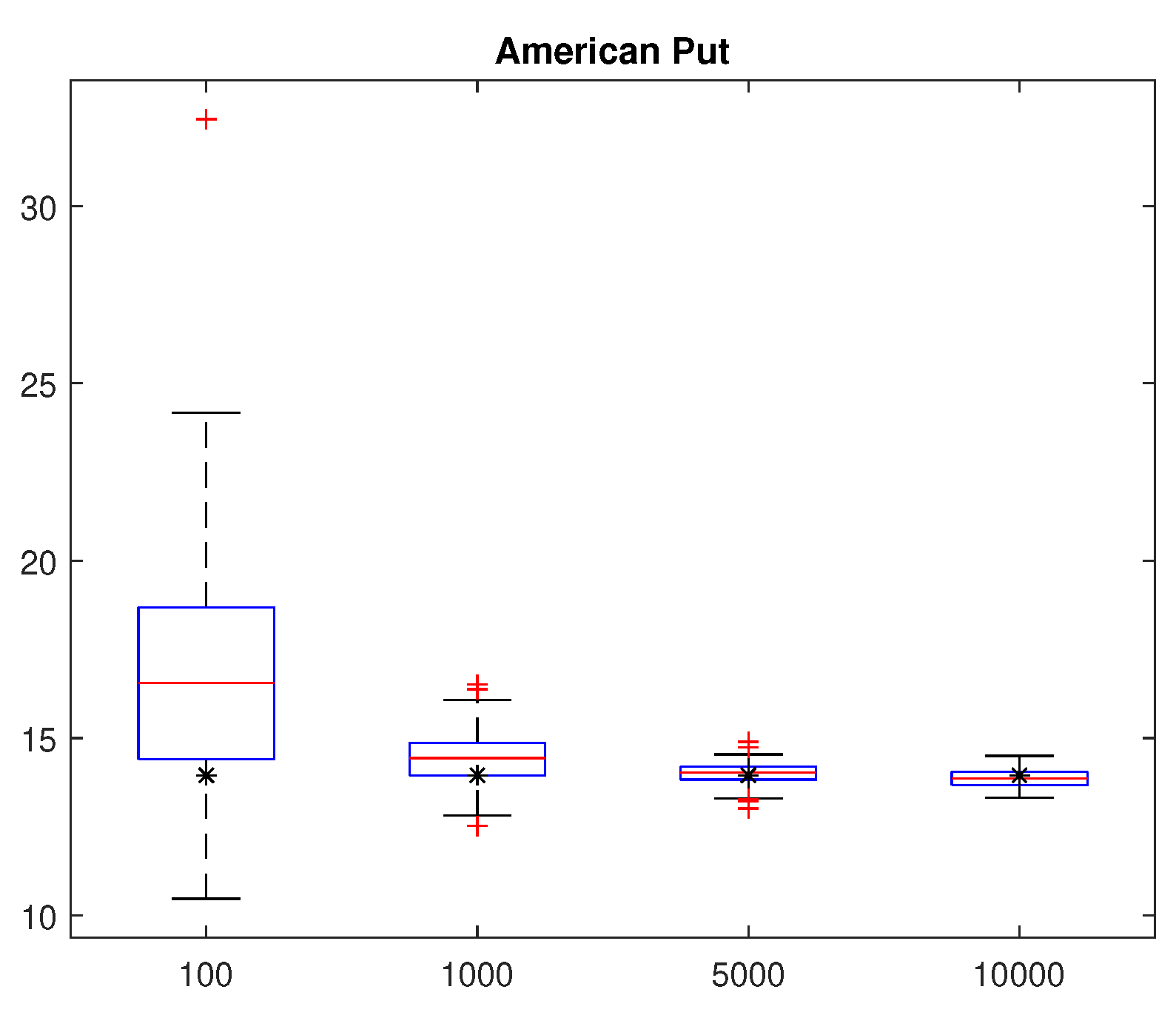

Finally, we perform bootstrapping. We selected the at-the-money, 6 April 2016 put option with strike price

and

days to maturity. Put prices were obtained by LSM using the parameters calibrated for that day in

Table 5. On that day, the underlying S&P 100 index price was 918.21, and the market put price was 13.95.

Table 7 shows the LSM prices and their standard errors for simulation using 100, 1000, 5000, and 10,000 sample paths. The LSM prices approach the market price, and the standard error decreases as the number of sample paths increases. We repeated these simulations 100 times, and present numerical summaries for the statistics for those 100 prices in

Table 8. As the number of sample paths increases, means and medians approach the market put price, while the standard deviations and ranges are decreased. We present boxplot summaries in

Figure 6 for those 100 prices. Market put prices are also represented (’*’ symbols) with the boxplots. We observe that the interquartile distance of LSM prices narrows to that of the market price, and dispersions are reduced as the number of sample paths increase.

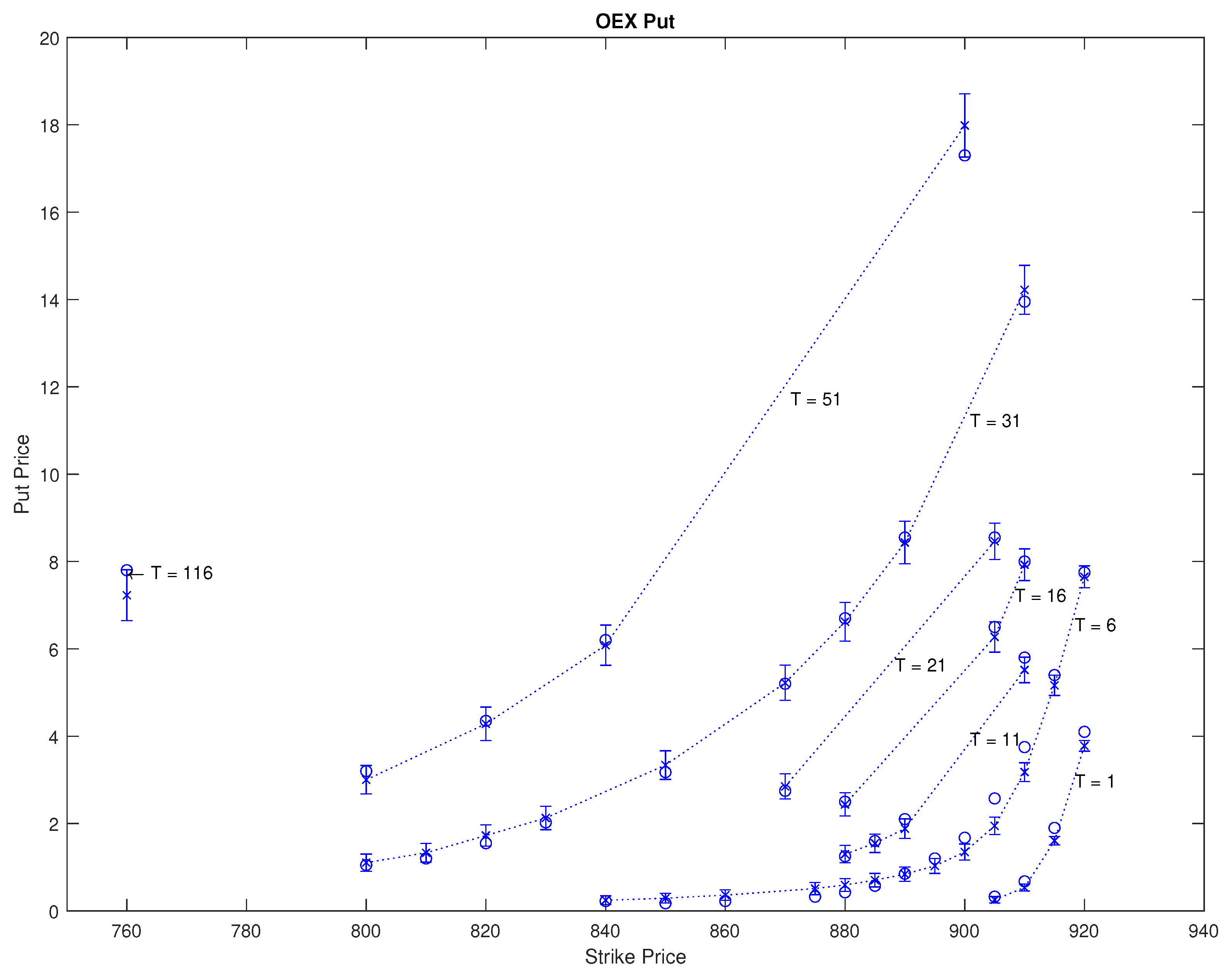

Figure 7 provides a graphical illustration of the calibration for 6 April 2016. Calibrated CGMYSV prices are drawn by "×", the market observed prices are drawn by "∘", and the 95% confidence intervals are marked by a "I" shape. The days to maturities

T are written on the plate.

4.3. Asian and Barrier Options

The sample path generation method for the CGMYSV model can also be used for Asian and Barrier option pricing. In this section, we briefly show examples of Asian and Barrier option pricing using the MCS, with sample paths generated by Algorithm 1. We generated 10,000 sample paths of the CGMYSV model with parameters

,

,

,

,

,

,

, and

. Then, we generated the underlying price process

using (

10), where

,

, and

.

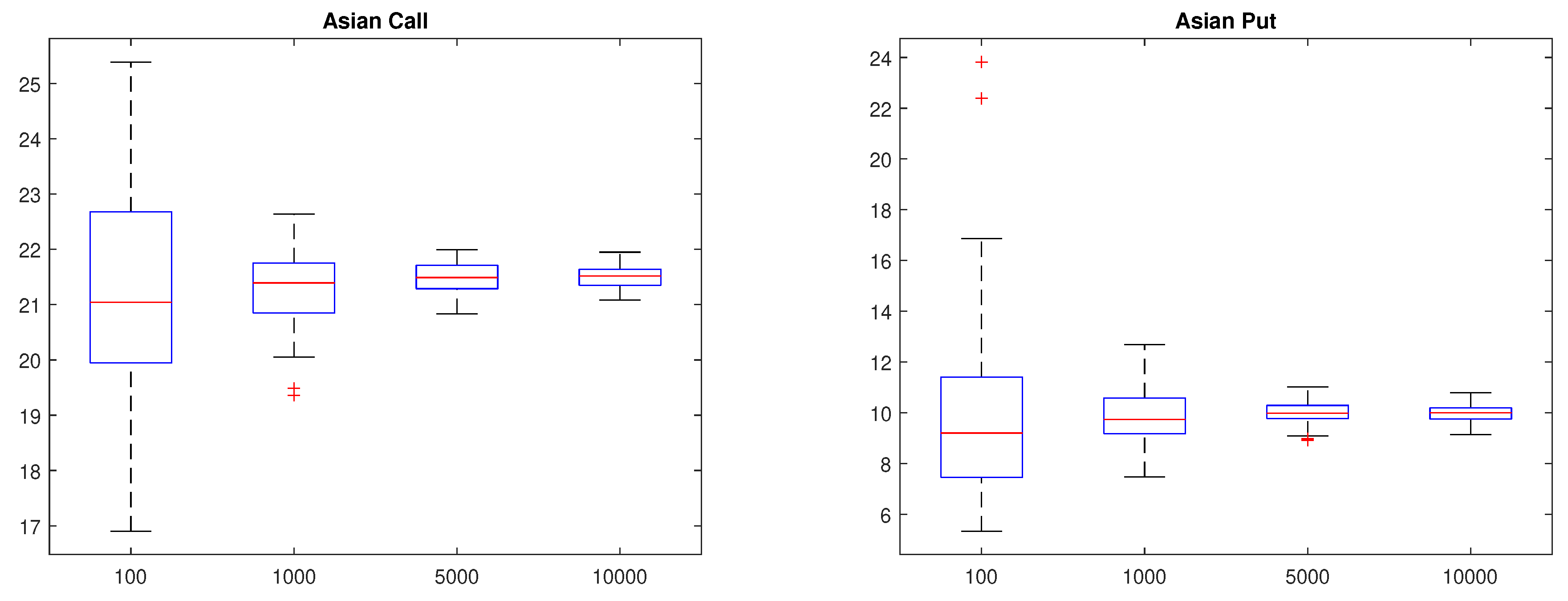

For the Asian option, we consider the arithmetic average call and put prices for strike price

and a time to maturity of

.

Table 9 shows the MCS prices for Asian call & put prices and their standard errors for simulations with 100, 1000, 5000, and 10,000 sample paths. The standard error of the MCS prices decreased as the number of sample paths increased. We repeated this process 100 times, and present boxplots for those 100 prices in

Figure 8. We observe that the MCS prices converge, and dispersions are reduced as the number of sample paths increase.

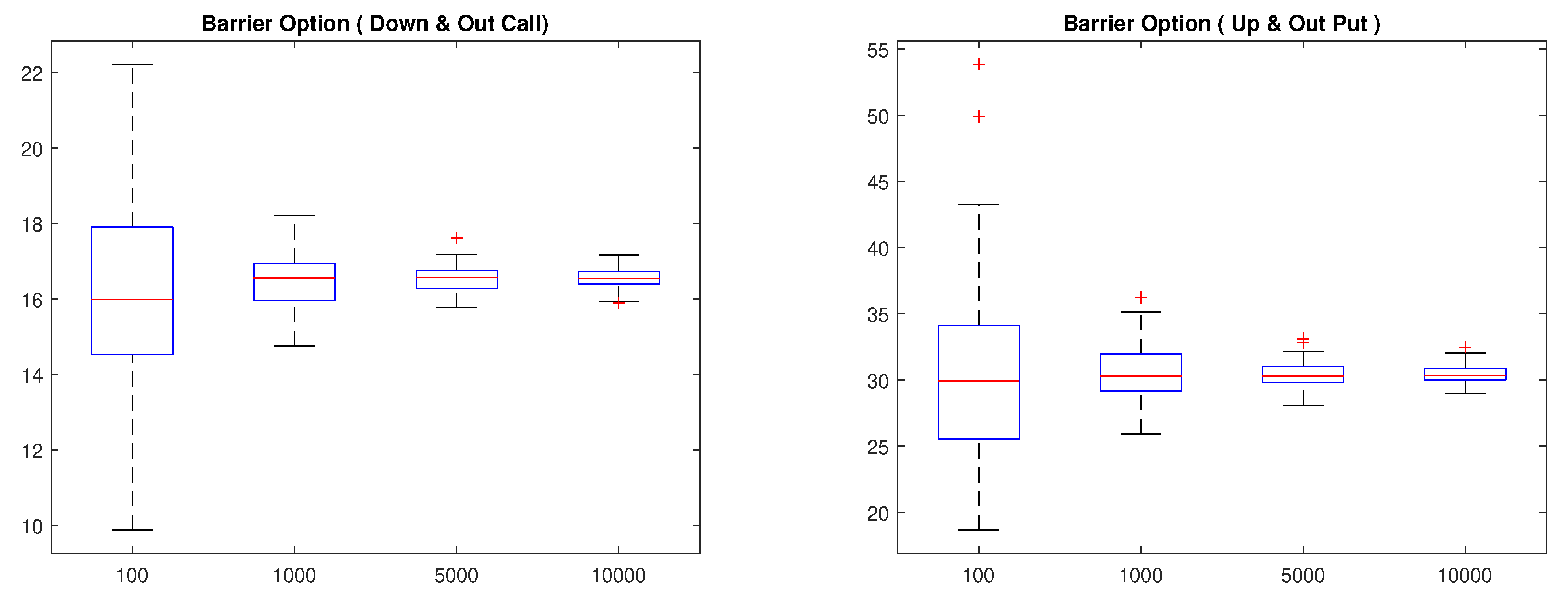

Similarly, we found the MCS price for Barrier options. We considered the down-and-out call and the up-and-out put Barrier options having a strike price of

and time to maturity of

. Barriers of the down-and-out call and the up-and-out put are 2400, and 2750, respectively.

Table 10 shows the MCS prices and their standard errors for simulations with 100, 1000, 5000, and 10,000 sample paths. The standard error of the MCS prices decreased as the number of sample paths increased. We repeated this process 100 times, and present boxplots for those 100 prices in

Figure 9. We also observe that the MCS prices converged, and dispersions are reduced as the sample paths increase.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}