Rethinking Economic Measurement Using Statistical Ensembles

Abstract

1. Introduction

1.1. Isomorphisms

1.2. Background of Ensembles in Economics

1.3. What Changed to Now Allow Using Ensembles?

2. Materials and Methods

2.1. What Is an Ensemble?

2.2. The Distinction Between Classical and Quantum

2.3. Thermodynamics

They are led by an Invisible Hand to make nearly the same distribution of the necessaries of life, which would have been made, had the earth been divided into equal portions among all its inhabitants [16].(Part 4, Ch. 1)

By preferring the support of domestic to that of foreign industry, he intends only his own security; and by directing that industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this, as in many other cases, led by an Invisible Hand to promote an end which was no part of his intention [11].(Book 4, Ch. 2)

3. Results

3.1. The Allais Paradox

- Win $7 with certainty.

- Win $7 with 75% chance, $10 with 20% chance, and $0 with 5% chance.

- Win $7 with 25% chance and $0 with 75% chance.

- Win $10 with 20% chance and $0 with 80% chance.

- 1.

- Novices use simple heuristics when confronted with complex games.

- 2.

- People have a quantifiable preference for the “sure thing”.

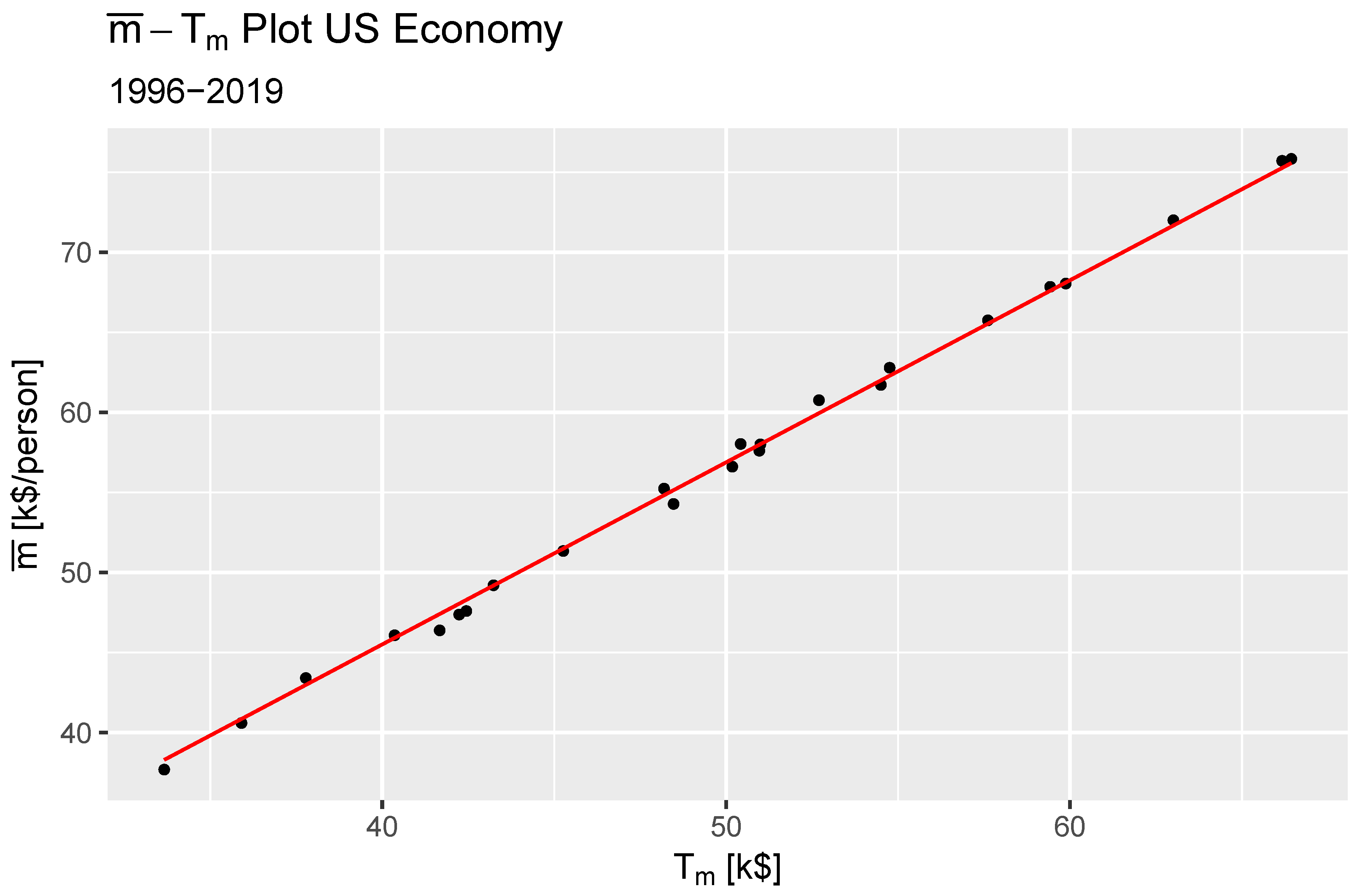

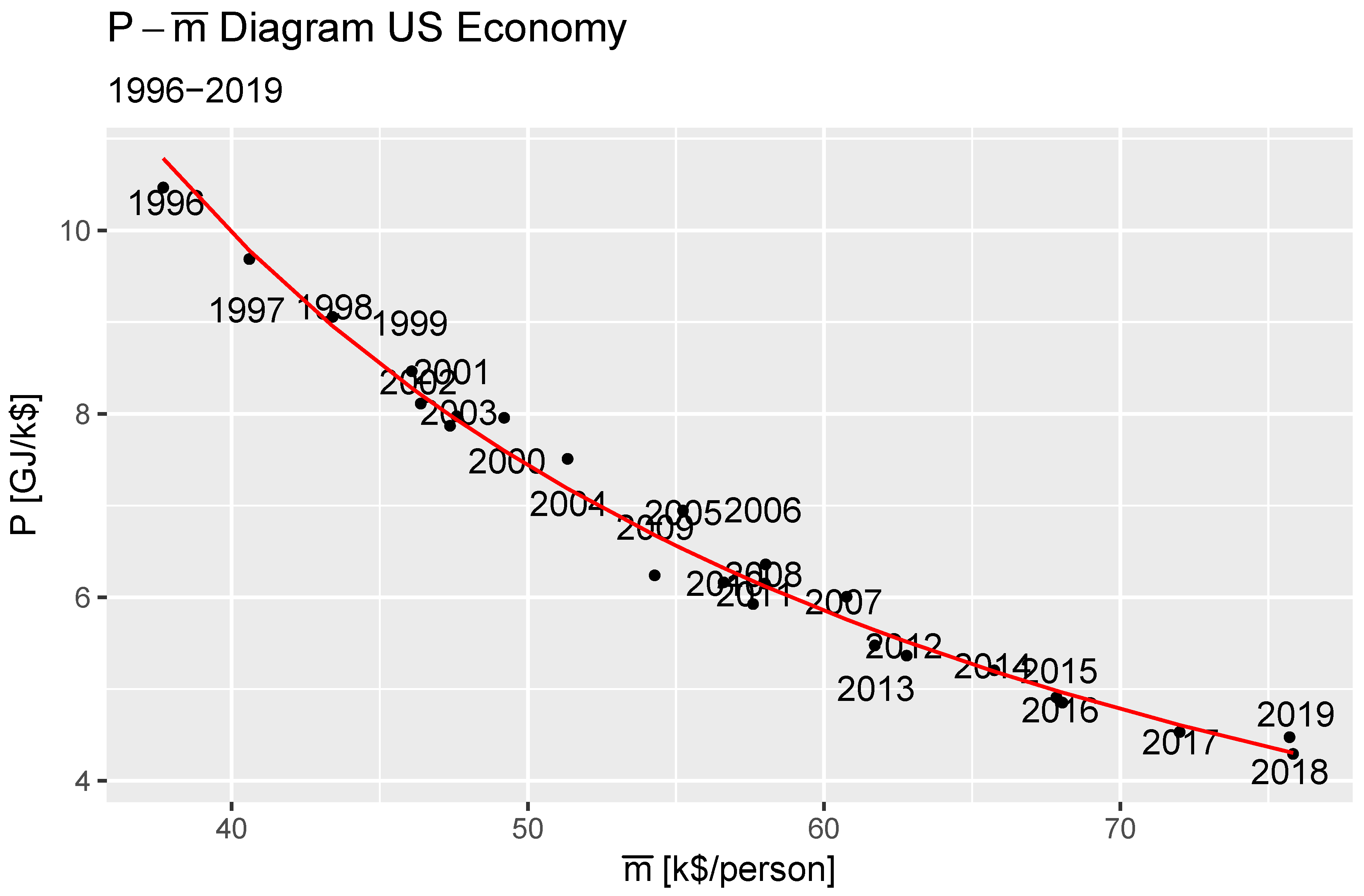

3.2. Econometric Analysis

3.2.1. Data

3.2.2. Model

4. Discussion

- 1.

- Equality of opportunity.

- 2.

- Equality of outcome.

4.1. Equality of Opportunity

4.2. Equality of Outcome

The law that entropy always increases holds, I think, the supreme position among the laws of Nature. If someone points out to you that your pet theory of the universe is in disagreement with Maxwell’s equations—then so much the worse for Maxwell’s equations. If it is found to be contradicted by observation—well, these experimentalists do bungle things sometimes. But if your theory is found to be against the Second Law of Thermodynamics, I can give you no hope; there is nothing for it to collapse in deepest humiliation [25].

5. Conclusions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| AGI | Adjusted Gross Income |

| API | Application Programming Interface |

| EIA | Energy Information Agency |

| EU | Expected Utility Hypothesis |

| HMC | Hamiltonian Monte Carlo |

| IRS | Internal Revenue Service |

| LLC | Limited Liability Company |

| NUTS | No U-Turn Sampling |

| QGT | Quantum Game Theory |

| SEU | Subjective Expected Utility |

| US | United States |

| vNM | von Neumann—Morgenstern |

Appendix A

{kind=link}

{kind=link}

| Year | Z | |||

|---|---|---|---|---|

| 1996 | 33,424.95 | 120,921.4 | 1.197789 | 32,783.57 |

| 1997 | 35,533.71 | 127,040.7 | 1.137222 | 34,999.70 |

| 1998 | 42,384.76 | 118,780.6 | 1.272331 | 40,485.83 |

| 1999 | 39,053.37 | 135,461.6 | 1.105257 | 38,521.05 |

| 2000 | 39,552.88 | 129,135.1 | 1.195418 | 38,577.32 |

| 2001 | 40,889.55 | 131,838.8 | 1.309683 | 39,434.20 |

| 2002 | 41,338.96 | 133,736.0 | 1.363438 | 39,692.01 |

| 2003 | 39,862.09 | 123,672.2 | 1.346527 | 38,181.91 |

| 2004 | 41,206.12 | 126,851.5 | 1.273806 | 39,714.94 |

| 2005 | 42,661.85 | 128,592.3 | 1.227064 | 41,236.77 |

| 2006 | 44,281.24 | 130,389.2 | 1.223103 | 42,733.78 |

| 2007 | 45,653.34 | 135,186.9 | 1.207421 | 44,153.72 |

| 2008 | 46,083.54 | 142,474.8 | 1.251603 | 44,528.59 |

| 2009 | 45,865.92 | 146,023.1 | 1.332454 | 44,095.15 |

| 2010 | 46,247.19 | 147,527.9 | 1.277674 | 44,690.98 |

| 2011 | 47,286.28 | 144,684.1 | 1.302614 | 45,422.53 |

| 2012 | 48,434.39 | 144,688.4 | 1.231663 | 46,758.26 |

| 2013 | 50,636.73 | 149,014.3 | 1.322918 | 48,356.20 |

| 2014 | 52,275.46 | 150,729.5 | 1.289789 | 49,987.84 |

| 2015 | 53,713.46 | 156,673.1 | 1.278110 | 51,487.21 |

| 2016 | 55,070.56 | 159,914.6 | 1.310235 | 52,585.58 |

| 2017 | 57,066.31 | 164,395.7 | 1.282268 | 54,608.08 |

| 2018 | 59,700.10 | 170,770.0 | 1.279972 | 57,100.77 |

| 2019 | 61,345.95 | 169,178.0 | 1.321514 | 58,167.35 |

| Year | P [GJ/k$] | m [k$/person] | N [people] | e [GJ/person] | T [GJ] | s [1/person] |

|---|---|---|---|---|---|---|

| 1996 | 10.467146 | 37.68948 | 120,351,210 | 392.1858 | 352.3444 | 11.51733 |

| 1997 | 9.687384 | 40.59687 | 122,421,993 | 387.1879 | 347.8541 | 11.59368 |

| 1998 | 9.056673 | 43.40742 | 124,770,661 | 380.8353 | 342.1469 | 11.75771 |

| 1999 | 8.463946 | 46.07878 | 127,075,147 | 380.2339 | 341.6066 | 11.70065 |

| 2000 | 7.956918 | 49.20155 | 129,373,502 | 382.9225 | 344.0221 | 11.69841 |

| 2001 | 7.869127 | 47.37317 | 130,255,240 | 369.9594 | 332.3759 | 11.70397 |

| 2002 | 8.111589 | 46.38492 | 130,076,442 | 376.23 | 338.0094 | 11.70206 |

| 2003 | 7.973448 | 47.5919 | 130,423,630 | 376.7065 | 338.4376 | 11.67136 |

| 2004 | 7.508802 | 51.34242 | 132,226,043 | 378.2977 | 339.8671 | 11.72381 |

| 2005 | 6.945434 | 55.23813 | 134,372,680 | 372.5771 | 334.7277 | 11.77325 |

| 2006 | 6.358212 | 58.02852 | 138,394,756 | 356.8393 | 320.5886 | 11.81362 |

| 2007 | 6.004935 | 60.76228 | 142,978,808 | 352.2324 | 316.4497 | 11.84845 |

| 2008 | 6.149047 | 58.0051 | 142,450,569 | 349.0134 | 313.5578 | 11.8414 |

| 2009 | 6.238692 | 54.28291 | 140,494,129 | 336.5923 | 302.3985 | 11.814 |

| 2010 | 6.162976 | 56.61016 | 142,892,054 | 344.2103 | 309.2426 | 11.83573 |

| 2011 | 5.925432 | 57.60562 | 145,370,240 | 336.1274 | 301.9808 | 11.85409 |

| 2012 | 5.363138 | 62.7905 | 144,928,473 | 326.8532 | 293.6487 | 11.89954 |

| 2013 | 5.474273 | 61.71394 | 147,351,299 | 332.075 | 298.3401 | 11.91875 |

| 2014 | 5.202737 | 65.75103 | 148,606,578 | 333.6133 | 299.7221 | 11.96088 |

| 2015 | 4.907715 | 67.84563 | 150,493,262 | 324.588 | 291.6137 | 11.9909 |

| 2016 | 4.850748 | 68.04946 | 150,272,156 | 323.2772 | 290.436 | 12.00673 |

| 2017 | 4.530385 | 72.00567 | 152,903,232 | 317.7014 | 285.4267 | 12.05083 |

| 2018 | 4.473874 | 75.71772 | 153,774,296 | 329.4796 | 296.0083 | 12.09697 |

| 2019 | 4.291296 | 75.83724 | 157,796,805 | 317.3104 | 285.0754 | 12.11267 |

References

- Abel, C. The Quantum Foundations of Utility and Value. Phil. Trans. R. Soc. A 2023, 381, 20220286. [Google Scholar] [CrossRef] [PubMed]

- Jakimowicz, A. The Role of Entropy in the Development of Economics. Entropy 2020, 22, 452. [Google Scholar] [CrossRef] [PubMed]

- Pfanzagl, J. Theory of Measurement; John Wiley and Sons: New York, NY, USA, 1968. [Google Scholar]

- McGilchrist, I. The Master and His Emissary: The Divided Brain and the Making of the Western World; Yale University Press: New Haven, CT, USA, 2009. [Google Scholar]

- Yakovenko, V.M. Econophysics, Statistical Mechanics Approach to. In Encyclopedia of Complexity and Systems Science; Meyers, R.A., Ed.; Springer: New York, NY, USA, 2009; pp. 2800–2826. [Google Scholar] [CrossRef]

- Bernoulli, D. Exposition of a New Theory on the Measurement of Risk. Econometrica 1954, 22, 23–36. [Google Scholar] [CrossRef]

- Savage, L.J. The Foundations of Statistics, 2nd ed.; Dover Publications: New York, NY, USA, 1954. [Google Scholar]

- Stanley, E.H. Interview with Eugene H. Stanley. IIM Kozhikode Soc. Manag. Rev. 2013, 2, 73–78. [Google Scholar] [CrossRef]

- Szilard, L. On entropy reduction in a thermodynamic system by interference by intelligent subjects [NASA TT F-16723]. Zhurnal Phys. 1976, 53, 840–856. [Google Scholar]

- Ayers, R.U.; Warr, B. The Economic Growth Engine: How Energy and Work Drive Material Prosperity; International Institute for Applied Systems Analysis: Northhampton, MA, USA, 2009. [Google Scholar]

- Smith, A. The Wealth of Nations; W. Strahan and T. Cadell: London, UK, 1776. [Google Scholar]

- Peterson, J.B. We Who Wrestle with God: Perceptions of the Divine; Penguin: London, UK, 2024. [Google Scholar]

- Morgenstern, O. Some Reflections on Utility. In Expected Utility Hypothesis and the Allais Paradox: Contemporary Discussions of Decisions Under Uncertainty with Allais’ Rejoinder.; D. Reidel Publishing Company: Boston, MA, USA, 1979; pp. 175–183. [Google Scholar]

- Jaynes, E.T. Information Theory and Statistical Mechanics. Phys. Rev. 1957, 106, 620–630. [Google Scholar] [CrossRef]

- Matsoukas, T. Generalized Statistical Thermodynamics; Springer: Cham, Switzerland, 2018. [Google Scholar] [CrossRef]

- Smith, A. The Theory of Moral Sentiments; Andrew Millar: London, UK, 1759. [Google Scholar]

- List, J.A.; Haigh, M.S. A simple test of expected utility theory using professional traders. Proc. Natl. Acad. Sci. USA 2005, 102, 945–948. [Google Scholar] [CrossRef] [PubMed]

- Friston, K.; Schwartenbeck, P.; FitzGerald, T.; Moutoussis, M.; Behrens, T.; Dolan, R.J. The anatomy of choice: Active inference and agency. Front. Hum. Neurosci. 2013, 7, 598. [Google Scholar] [CrossRef] [PubMed]

- Callen, H.B. Thermodynamics and an Introduction to Thermostatistics, 2nd ed.; John Wiley & Sons: New York, NY, USA, 1985. [Google Scholar]

- Banerjee, A.; Yakovenko, V.M. Universal patterns of inequality. New J. Phys. 2010, 12, 1–25. [Google Scholar] [CrossRef]

- Tao, Y.; Wu, X.; Zhou, T.; Yan, W.; Huang, Y.; Yu, H.; Mondal, B.; Yakovenko, V.M. Exponential structure of income inequality: Evidence from 67 countries. J. Econ. Interact. Coord. 2019, 14, 345–376. [Google Scholar] [CrossRef]

- Internal Revenue Service. IRS SOI Tax Stats—Individual Statistical Tables by Size of Adjusted Gross Income, Individual Complete Report (Publication 1304), Table 1.1. United States Treasury Department 1996–2019. Available online: https://www.irs.gov/statistics/soi-tax-stats-individual-statistical-tables-by-size-of-adjusted-gross-income (accessed on 14 March 2023).

- Energy Information Agency. Open Data API. 2022. Available online: https://api.eia.gov/ (accessed on 14 March 2023).

- Lawrence Livermore National Laboratory. Energy Flow Charts: United States. 2022. Available online: https://flowcharts.llnl.gov/commodities/energy (accessed on 14 March 2023).

- Eddington, A.S. The Nature of the Physical World: Gifford Lectures; Cambridge University Press: Cambridge, UK, 1927; Volume 74. [Google Scholar]

| Game | Occupancy | Basis | Cohort |

|---|---|---|---|

| A | 15, 17 | , | Student |

| A | 8, 19 | , | Trader |

| B | 8, 24 | , | Student |

| B | 3, 24 | , | Trader |

| 4, 13, 3, 10 | , , , | Student | |

| 8, 7, 9, 30 | , , , | Trader |

| Game | Cohort | N | |||

|---|---|---|---|---|---|

| A | Student | 32 | |||

| A | Trader | 27 | |||

| B | Student | 32 | |||

| B | Trader | 27 | |||

| Student | 30 | ||||

| Trader | 54 | ||||

| Canonical | 54 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abel, C. Rethinking Economic Measurement Using Statistical Ensembles. Entropy 2025, 27, 265. https://doi.org/10.3390/e27030265

Abel C. Rethinking Economic Measurement Using Statistical Ensembles. Entropy. 2025; 27(3):265. https://doi.org/10.3390/e27030265

Chicago/Turabian StyleAbel, Cal. 2025. "Rethinking Economic Measurement Using Statistical Ensembles" Entropy 27, no. 3: 265. https://doi.org/10.3390/e27030265

APA StyleAbel, C. (2025). Rethinking Economic Measurement Using Statistical Ensembles. Entropy, 27(3), 265. https://doi.org/10.3390/e27030265