4.1. Discussion and Results Regarding the Correlation of Variables

At both the European and Romanian levels, the regulations regarding the implementation of an internal control system in the public sector have evolved significantly. Public awareness was raised in relation to the importance of internal control mechanisms, the need for maturity in risk management, and the rising need for appropriate procedures and policies in public entities [

52]. In fact, the annual reports issued by the Romanian Court of Accounts present a distinct chapter for the assessment of internal control [

30].

In order to achieve a thorough analysis of the selected reference points, this study focused on investigating the correlations between errors reported by external public auditors on internal control systems and the rest of the corporate governance assessment variables. The statistical method used was principal component analysis (PCA). The results indicated a strong correlation between the chosen variables as per the graphic representation of the calculated main components. The study took into consideration the number of identified errors and not also the value of such errors, because of the major differences between the categorized nonconformities identified by value. As per the reports of the Romanian Court of Accounts, the nonconformities attributed to internal control have no or insignificant value attributed, thus cannot contribute to a comparable analysis of indicators. The situation is somewhat interesting and points to a need to regulate the situation, as per the lack of sanction in case of errors or flaws in the implementation of corporate governance systems in public entities.

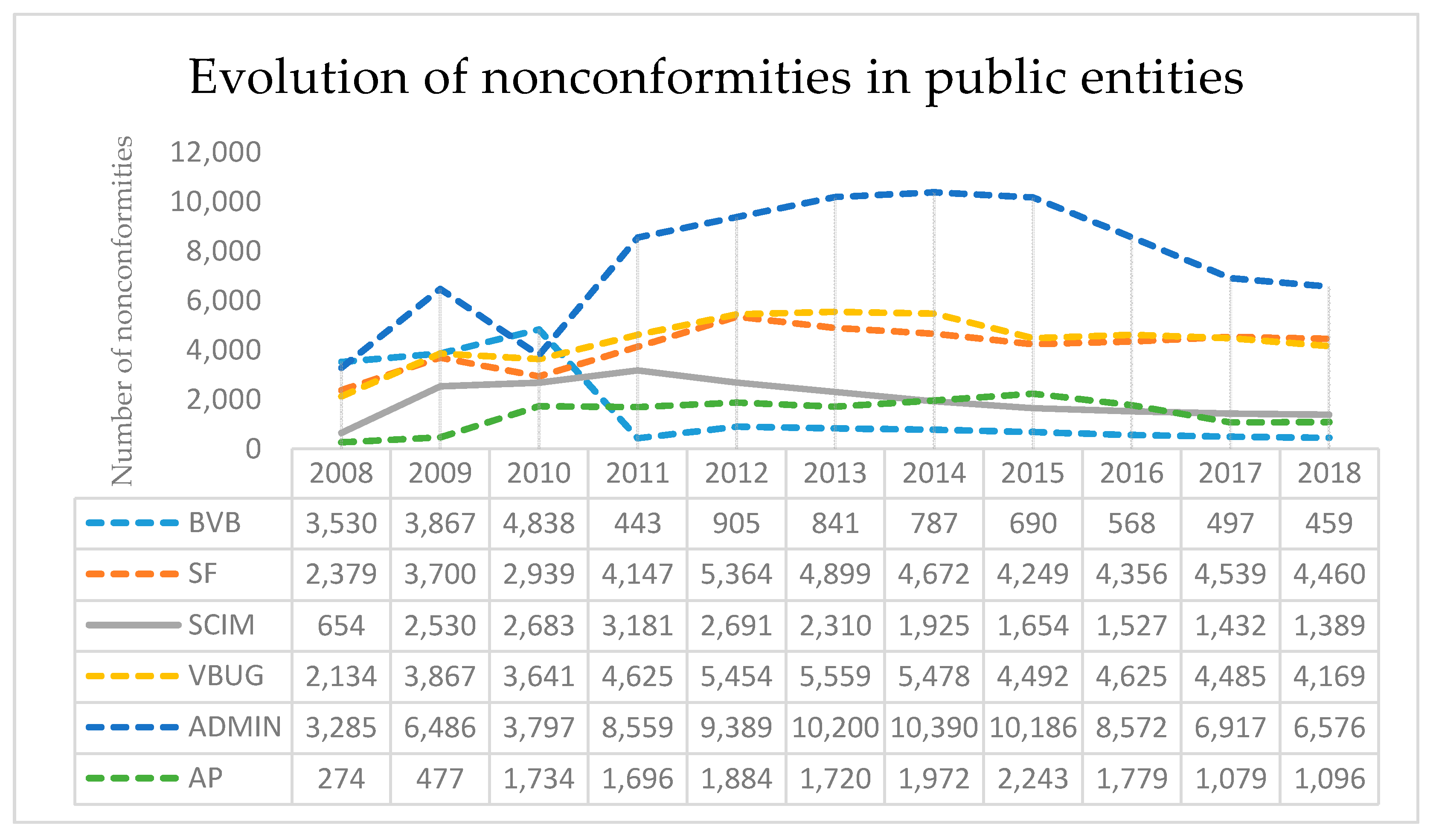

The most common errors identified during the public audits, that constitute the population of analyzed variables in the current study, were:

Nonconformities described as BVC (regarding creation and assessment of budget execution) consist mainly of flaws concerning the provisions of salaries and personnel revenue, nonconformities in the evaluation of revenue dimension related to forecasted expenses, and flaws in the authorization or report of budget execution.

Nonconformities described as FS (accuracy of financial statements) consist mainly of poor accounting evidence regarding assets, provisions, debt and receivables recognitions, and nonconformities in recognition of income and expenses.

Nonconformities described as IBUG (procedures of collection of government revenues) consist mainly of failure to enforce measures of collection of public revenue according to legal regulations and hierarchical attributions, flaws of highlighting in accounting evidence, and lack of collection of own revenues, deficiencies in the pursuit for purpose of collection of own revenues.

Nonconformities described as ADMIN (attributions concerning sound financial management of public patrimony) consist mainly of payment of budgetary expenses with disregard of legal procedures concerning payment procedures and authorization, illegal payments, and flaws of nonconformity during procedures of patrimony inventory.

Nonconformities described as PAQ (public procurement operations) consist mainly of poor implementation of public procurement procedures, illegal transactions, and acquisitions that do not benefit the actual objectives of public entities.

Nonconformities described as SCIM (internal control systems) consist mainly of flaws or formal behavior of managerial decision making during the implementation or development of internal control mechanisms.

The correlation matrix indicates a series of statistically significant connections between the variables considered, represented in black in the following table format. The variables represented in red suggest a low statistical connection between the compiled indicators (

Table 1).

The statistical data reported by the Court of Accounts for the period 2008–2018 indicates that the errors reported on the creation and assessment of budget execution (BVC) evolved in a reverse proportion to the faults in the collection of government revenues (IBUG), ineffectiveness in sound financial management (ADMIN), or public procurement errors (PAQ). It seems that a greater focus of financial auditors on creation and assessment of budget execution (BVC) led to a smaller number of errors reported for the remaining reference points.

There is also a strong link between the errors in financial statements (FS) and the faults in the collection of government revenues (IBUG), ineffectiveness in sound financial management (ADMIN), or public procurement errors (PAQ). It seems that better collection of governance revenues, effectiveness in financial management, or increased compliance in public procurement resonated with more accurate financial statements. The same strong link of correlation in the same sense was also found in the relationship between ADMIN and IBUG, PAQ and IBUG, and PAQ and ADMIN.

An interesting result revealed by the correlation matrix is the relationship between the number of errors regarding internal control systems (SCIM) and the rest of the analyzed elements. According to

Table 1, the correlation of the deviations reported by the external public auditors related to SCIM with the rest of governance reference points is less than +/−0.5. Practically, the matrix indicates a link gap between internal control systems and the rest of the governance valuation points. The very low correlation (marked red in

Table 1) seems to indicate a very low impact of internal control systems implemented in Romanian public entities. The low result suggests that the effect of implementing and maintaining internal control measures is predominantly formal and has no significant statistical impact or practical utility for other governance processes carried out in public entities. The implementation of internal control seems to be carried out mainly for compliance with the regulatory framework. The practical utility of internal control may not be accomplished apparently for lack of proper understanding.

The statistical relevance of the model was checked using the Kaiser–Meyer–Olkin (KMO) indicator, which reveals that the values obtained by computation (0.708) are acceptable according to Kaiser [

53]. The result of the KMO test is supported by Bartlett’s Test of Sphericity (

p-value = 0.000), which indicates the suitability of the indicators set for the analyzed model. (see

Table 2)

The result of the KMO test can also be correlated with the anti-image correlation table, with the individual variables calculated on the diagonal of

Table 3.

The results of the anti-image correlation matrix, in agreement with the KMO table, confirm that the main component analysis method is appropriate to interpret the correlation between the different valuation results of corporate governance measurements.

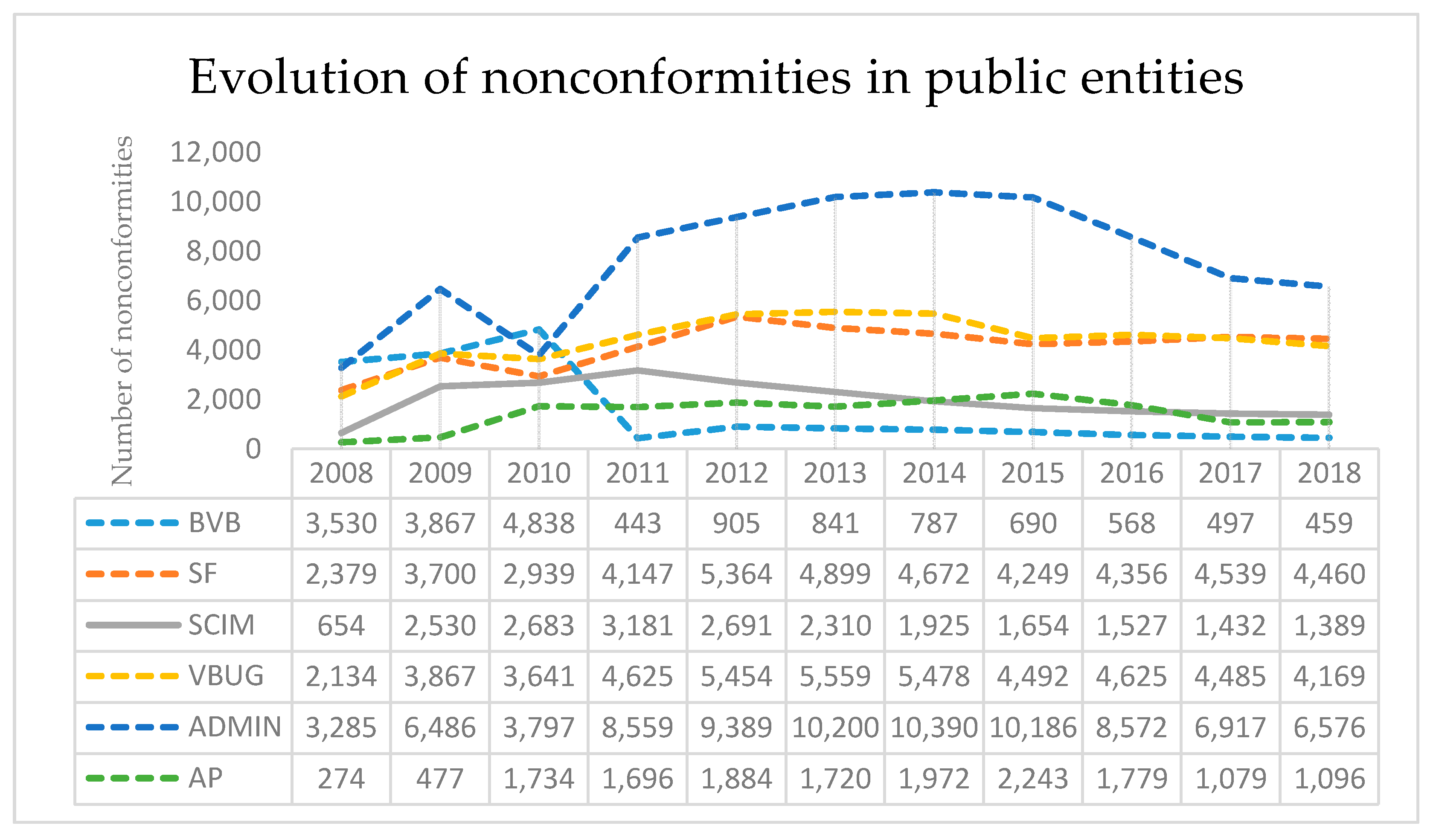

The patterns of the compiled indicators reported by the Court of Accounts are presented in

Figure 2.

According to the graphical representation of the compiled data, the reported errors for SCIM have an oscillating trajectory until 2011. After 2011, the level of errors found in this domain had a sustained downward trajectory, while the evolution of the remaining indicators was oscillating. In practice, a decreasing number of deviations of SCIM indicates a growing degree of compliance of public institutions with the implementation of internal control management systems. Starting with 2011, the uniform trajectory of the SCIM indicator, analyzed along with the oscillating trajectory of the other indicators, seems to confirm the formal grounds of the internal control processes, rather than suggest a real practical applicability.

The dilemma that arises in this situation seems to be: “Why 2011? What is the reason for the new pattern of SCIM?” A brief analysis of the relevant events in this direction revealed that in 2011, the Romanian Court of Accounts published the "Guidelines for the assessment of the internal control system in public entities". The paper aimed to support the external public auditors of the National Court of Accounts in the process of evaluating the internal control systems implemented at the level of the audited public entities. At the same time, the guide strove for an outcome of better understanding of the internal control system in public institutions [

54].

From the graphical representation analysis in

Figure 2, it can be noticed that the role of the guideline for internal control assessment has uniformized the reported results of audits in the period following 2011. The explanation seems to be that the audited subjects complied formally with the recommendations of public auditors (the number of errors reported decreased). The real utility of internal control, however, does not resonate by harmonizing the evolution of the remaining benchmarks analyzed by external public auditors. The rest of the governance assessment indicators do not seem to be influenced by compliance with the implementation of internal control systems.

With respect to the use of principal components analysis, it is very important to understand how sample size influences the results. The literature shows divergent opinions regarding the dimension of the analyzed sample in order to obtain a more precise estimate of population loadings and more stable results. In this study, the sample size was limited by statistical registration, but it respects the MacCallum et al. recommendation according to which “the minimum level of N or the minimum N:p ratio… is dependent on some aspects of the variable… the level of communality plays a crucial role” and the mean level of communalities must “be at least 0.7, preferably higher”, [

55] see

Table 4.

The compiled communalities show the percentage of variance explained by the extracted components. The “extraction” column shows high values for the variables, thus indicating a very good representation of variables by the extracted components.

Table 5 indicates that two main components were extracted out of the six variances analyzed, the first two account for 87.295% of the total variance.

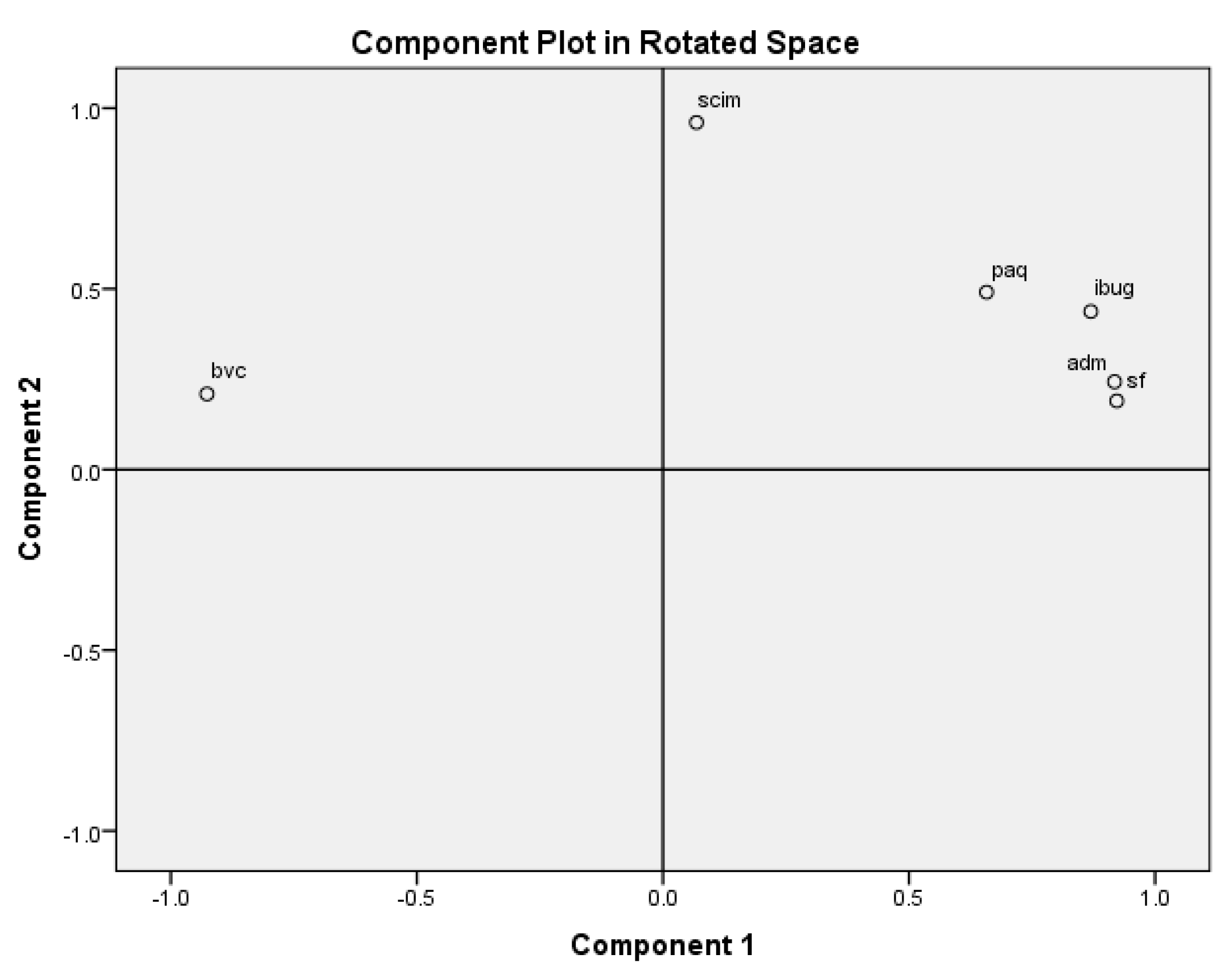

The first two components are clearly represented in the scree plot compiled with the PCA model (

Figure 3) and prove to be quintessential in explaining the model [

56] (

Table 6). The inflection point suggests the appropriate use of PCA. The first compiled main component is strongly correlated with five of the original variables and accounts for the maximum amount of total variance in the observed variable. The first component increases with the decrease in the number of errors in creating and assessing budget execution (BVC). The increase in the first major component is directly proportional to the increase of the original FS, IBUG, ADMIN, and PAQ variables. The second component accounts for the maximum amount that is left to be explained. The second component increases relative to a single value, respectively the increase in the number of reporting errors regarding the managerial internal control.

The conclusions drawn in the preceding paragraphs can also be graphically explained by the component plot in

Figure 4.

In conclusion, the statistical interpretation of the first research stage indicates the need to further research the correlation between the reported errors in the implementation and maintenance of the internal control and the evolution of other corporate governance benchmarks.

4.2. Discussion and Results Regarding the Efficiency Corporate Governance Index and Its Influence on Government Income

The next stage of the study focused on whether the nonconformities signaled by the Court of Accounts, assembled into an efficiency corporate governance index (ECGI), may be transposed into an effective economic sustainability measurement tool for public entities. The observations and flaws in compliance signaled by public financial auditors create a global assessment image on the performance and financial efficiency of public governance, which can be modeled, as the present study showed, into a single indicator pointing to a certain level of trust regarding sustainable reporting of public revenue and the accuracy of financial statements.

In the public sector, the creation, evolution, and reporting of income are of utmost importance for socio-economic activities. The financial performance and sustainable reporting of public entities are core elements that shape the lives of citizens [

27], and the literature shows that empirical studies concerning this topic need to be developed [

57,

58,

59]. Hence, exploring the links between the efficiency corporate governance index (ECGI) and institutional revenue, from a global economic perspective, may facilitate the understanding of public managers’ approach towards equity, efficiency, resilience, compliance, and prudence, as part of the economic sustainability process.

Studies on compliance and disclosure level with regard to financial statements [

60,

61], as well as the importance of improving the credibility of the information reported by auditors [

62], represent an active concern of academics. A global perspective on public financial statements analyzed with the help of ECGI broadens the picture of compliant sustainable reporting.

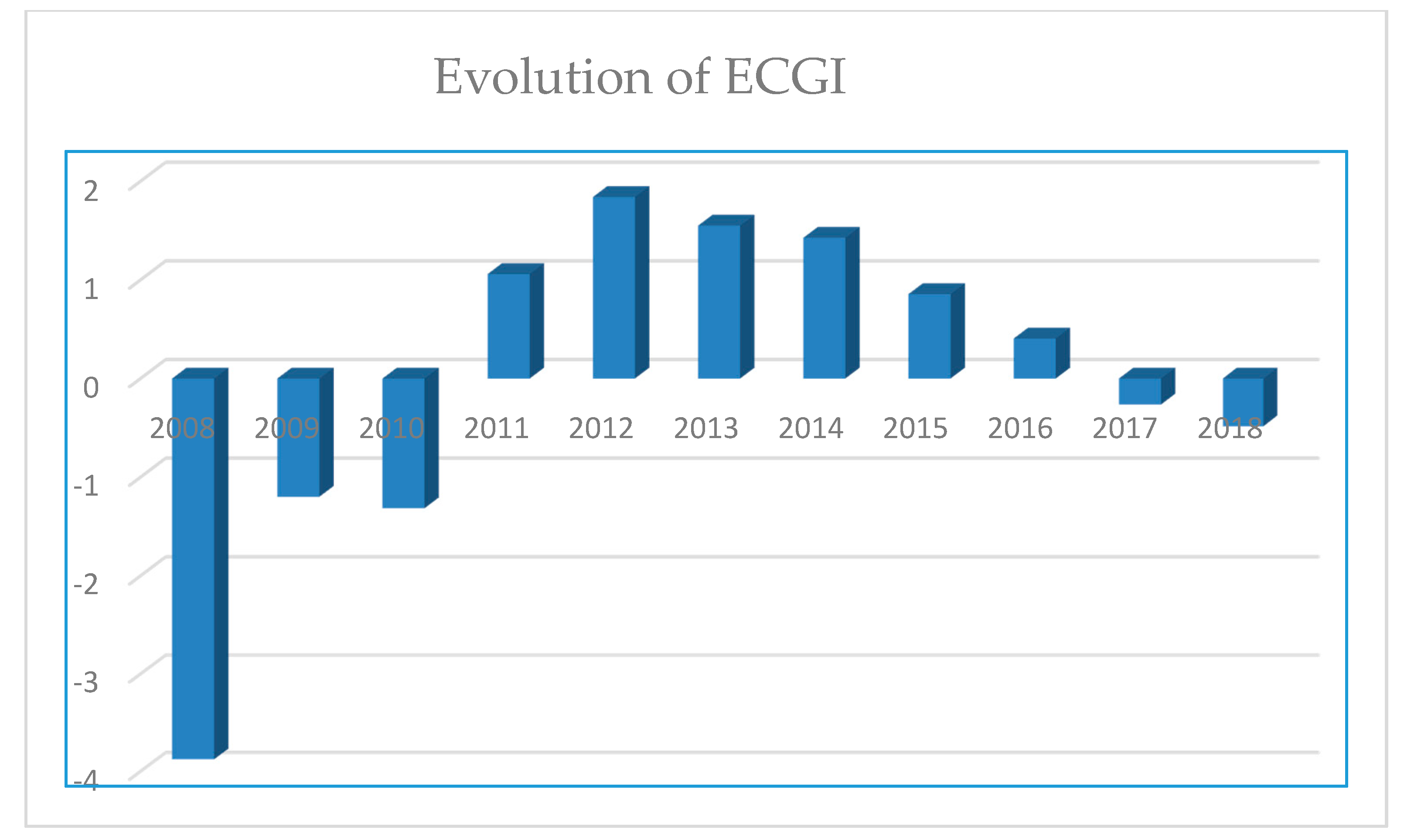

The results of the first research stage were furtherly acknowledged and used in this stage. The authors’ consideration is that managerial accountability can be measured by the benchmark indicators presented by public auditors’ reports, aggregated into a single indicator. Principal component analysis helps us understand the extent to which errors reported by external public auditors have revealed an influence on the declared income of public institutions and to construct an efficiency corporate governance index (ECGI). Considering that a small value of ECGI indicates good governance at the institutional level, the indicator is able to efficiently concentrate the contribution of the benchmark indicators followed by the public auditors and thus offers incentives on possible influence towards a sustainable revenue of public entities.

Using the principal component techniques, we constructed an efficiency corporate governance index (ECGI) that describes the aggregate influence of errors reported by external public auditors. In computing the two principal components (noted PC1 and PC2), we used the popular alternative so we consider the scores and the loading to be equal.

In computing the ECGI, we applied Equation (1):

The value of indices may be positive or negative, which may induce difficulties in interpretation but, nevertheless, also represents a good signal for the management to improve its’ efficiency.

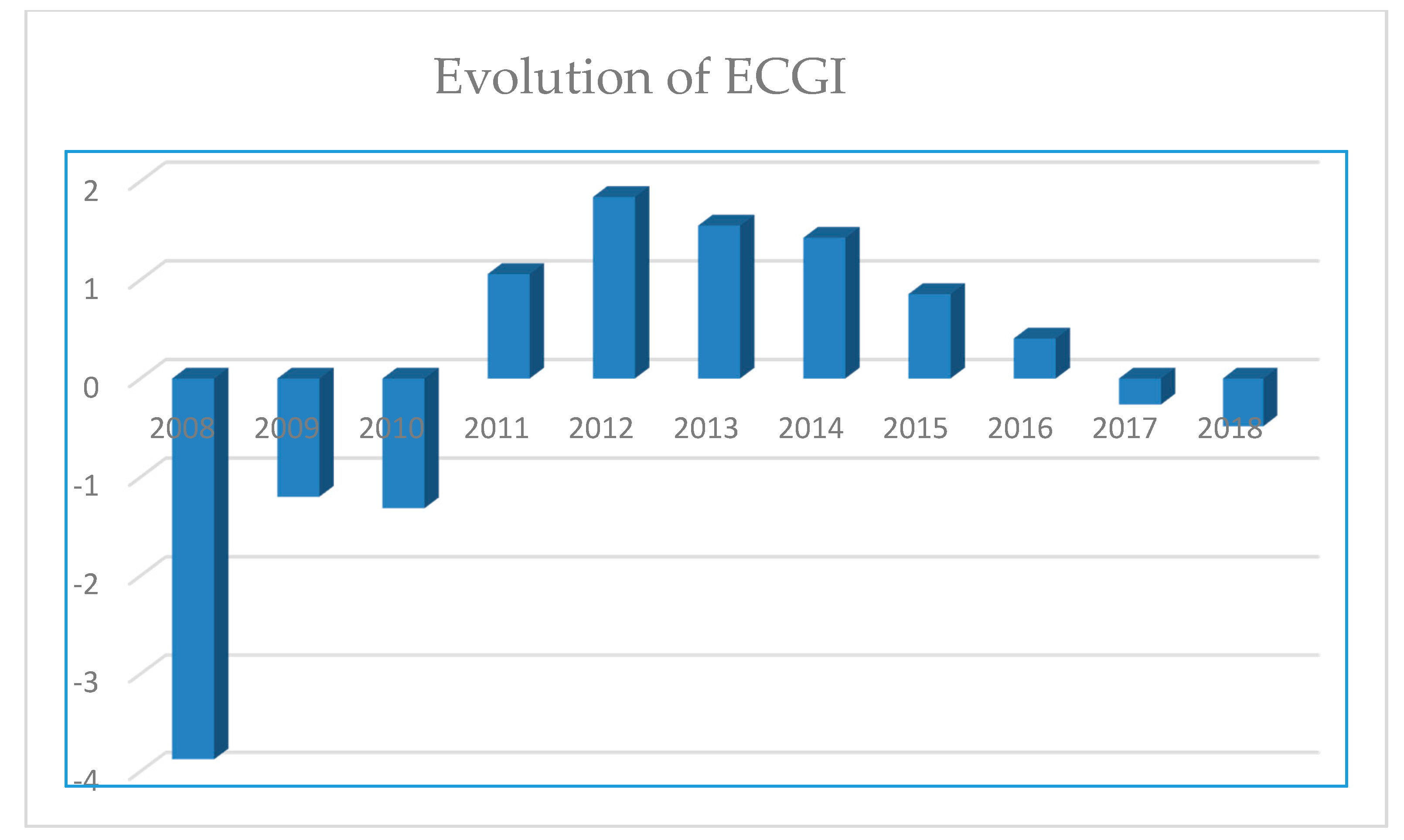

The value of the ECGI during the 2008–2018 period is presented in

Figure 5.

The higher the compliance of managerial assessment, the lower the value of ECGI obtained and the more accurate the income statements seem to be. A decreasing level of nonconformities SCIM was registered in 2012 and 2013 and the ECGI shows this tendency with a decreased trajectory after a period of practice in the implementation of “Guidelines for the assessment of the internal control system in public entities " (2011) when the process of evaluating the internal control system become formally compliant. We can consider that after 2011, the efficiency of corporate governance increased based on new procedures implemented. Now we can look at ECGI in relation to the revenue indicator and total nonconformities reported by the Romanian Court of Accounts in the period 2008–2018 in order to see a simple picture of management efficiency.

The revenue indicator (INC) reported by the public institutions in the period 2008–2018 was compiled from the reports of the Romanian Court of Accounts, in correspondence with the public reports of the official website of the Romanian Ministry of Finance. The evolution of reported financial indicators (revenue—INC, expenditure—EXP, and the profit/loss indicator—PROF) during the analyzed period is presented graphically in

Figure 6.

According to the available data, the total income reported by the Romanian public institutions had an oscillatory pattern with slight growth tendencies during the analyzed period. The public revenues were exceeded by total public cost, thus resulting in a negative result of public profit and loss statement. Our study focused on studying the reported income, primarily because in the public sector it is considered an important performance indicator for stability measurement when it comes to public governance [

63].

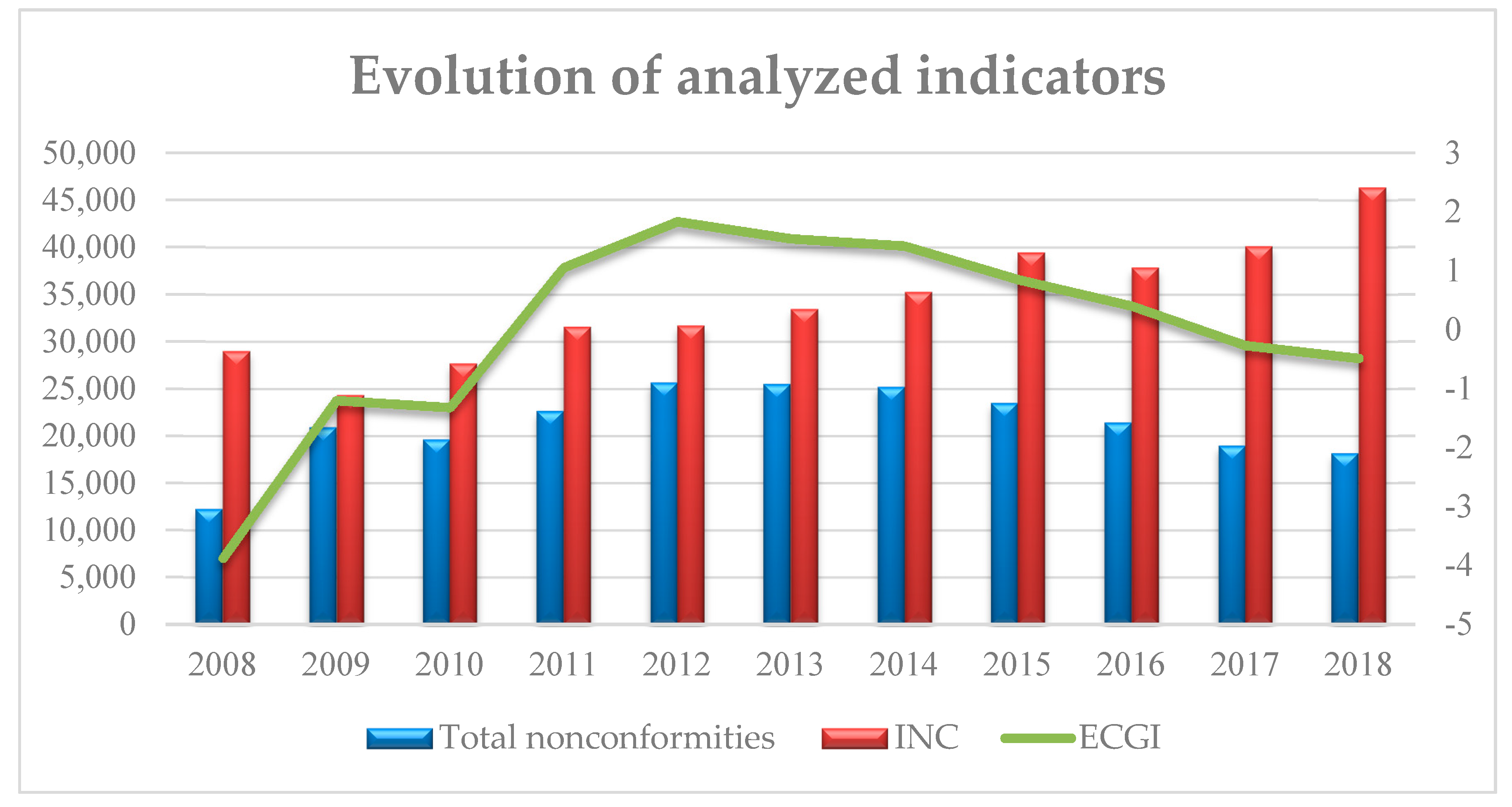

The evolution of the total nonconformities, the ECGI, and the income of public institutions are presented graphically in

Figure 7.

The Granger causality test may offer an image of the statistical causal relation between ECGI and income. According to the data graphically presented in

Table 7, we cannot reject the hypothesis that INC does not Granger-cause, in the statistical sense, ECGI at lag 1. We do reject the hypothesis that EGCI does not Granger-cause INC, so we can consider that Granger causality runs from ECGI to INC as we expected with a lag of one period. This lag may be explained as the time elapsed between the issuance of recommendations by the Court of Accounts and the implementation or appeal against those recommendations.

The research revealed that the total income reported by public institutions was influenced by governance factors included in ECGI, such as problems in the creation and assessment of budget execution, inaccurate financial statements, poor implementation and development of internal control systems, and faults in the collection of government revenues. In other words, when problems signaled in the public audit reports tend to increase in number, the indicator of public general income reported by public institutions tend to decrease or stagnate, especially during the first years of analysis. The situation suggested that the directions of assessment of corporate governance audited by the Romanian Court of Accounts are very effective in detecting situations of misleading income statements, of fault, or intention of managers to diminish reported public incomes. The scandal provoked by the public auditors’ report on the Romanian Financial Guard (a former institution invested with operative control attributions) led to the dissolution of the audited institution, because significant failure in collecting governance taxes and corruption incentives were revealed.

Nevertheless, it seemed that the decrease of reported situations of ineffectiveness in sound financial management and non-compliance in the process of public procurement, which is strongly correlated with the trajectory of ECGI, lead to a certain increase of public general income. The situation is interesting, since the decrease of ECGI indicates better compliance in sustainable reporting of revenues in the public sector. The result can be interpreted as an indicator of the fact that errors reported in the specific directions calculated with ECGI are connected with the managerial attitude towards compliance and efficiency in better strategies meant to increase public institutional revenue. Thus, ECGI incorporates the dimension of errors and flows that globally manifest in the public sector and, at the same time, is an indicator that may give important insights on the possible trajectory of public income.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}