Abstract

This paper offers an in-depth exploration into the intricate world of decentralized digital assets (DDAs), shedding light on their categorization as currencies, commodities, or securities. Building on foundational cases such as SEC v. Howey, the analysis delves into the current controversies surrounding assets like XRP and LBC, exploring the nuances in their classification. By highlighting the challenges of defining categories of DDAs within traditional legal frameworks, this study emphasizes the need for a simple taxonomy that encapsulates the dynamism of digital currencies while permitting flexibility. A proposed framework aims to simplify the categorization process while respecting recent jurisprudence, ensuring regulatory clarity for developers and users of DDAs.

Keywords:

cryptocurrency; virtual asset; decentralized digital asset; digital asset; Howey test; XRP; Ripple; Bitcoin; regulation 1. Introduction

In 2009, a person or group going by the pseudonym Satoshi Nakamoto established Bitcoin, a decentralized and permissionless system of exchange, and the first cryptocurrency was born [1]. Since then, the number and types of decentralized digital assets (DDAs) has exploded [2]. This expansion of the asset class was facilitated by the advent of smart contract capable chains that can support a variety of functions [3,4,5,6,7,8], governance tokens, and the creation of decentralized finance (DeFi) [9]. As a small asset class and associated industry, DDAs have been largely unregulated aside from the application of securities laws to initial coin offerings (ICOs) that were prominent around 2017 [10,11]. However, in late 2021, the market capitalization of the entire asset class reached approximately USD 3 trillion, with Bitcoin’s market cap at approximately USD 1.3 trillion [12,13], gaining the attention of governments around the world. Although organizations like the Financial Action Task Force (FATF) have established guidelines for regulation [14,15], few jurisdictions have adopted laws specific to the regulation of DDAs, instead relying on other legal frameworks that sometimes lead to internal power struggles over jurisdiction. At the core of these debates is whether assets are currencies, commodities, or securities [16,17]. Recent court decisions have added some clarity to the debate and justify a more simplified approach to categorizing DDAs to facilitate clear standards for developers, investors, and end users of various classes of DDAs. After providing a review of the literature addressing the classification of DDAs and the methodology, this paper first provides a basic technical background on the distributed ledger technology that underlies DDAs. It then discusses a simplified framework for categorizing DDAs and why, after recent court decisions, a simplified approach based on the intended use case will provide greater clarity. As DDAs are not located in any one jurisdiction, unlike physical assets, a simplified approach also assists in adding clarity between jurisdictions and in the establishment of more flexible model laws that can encourage the growth of the industry and the development of new technologies.

2. Literature Review

Absent specialized digital asset regulation, attempts to regulate DDAs ordinarily fall to agencies that regulate securities or commodities, often with political power struggles between government bodies [18,19]. As a result, much of the literature focuses on the role of security and commodity regulations [20,21,22,23,24,25], illustrating the importance of establishing a taxonomy [21]. ICOs have been a focus of much of the literature [2,25,26,27,28,29]. However, as ICOs are usually limited to qualified investors under securities laws and are a form of distribution, and not a type of asset, this paper excludes ICOs from its analysis. This article also does not address other regulatory frameworks aside from the classification of assets as currencies, commodities, or securities, and does not address concerns such as criminal activity and intellectual property protection [30].

The problem with jurisdiction-specific research is that if DDAs are categorized and regulated differently between jurisdictions [31], it may place undue hardship on smaller projects trying to comply with inconsistent regulatory regimes [32]. Decentralized projects, such as Bitcoin, are more resistant to these impacts. However, many projects begin centralized and heavy or inconsistent regulation may prevent the establishment and growth of new projects. A wide range of the literature has addressed categorizing DDAs, from the literature addressing the teaching of economics, to traditional business and legal literature. The proposed taxonomies have become increasingly complex, addressing the many characteristics of DDAs. For example, one framework considers 13 attributes, including going beyond legal considerations to issues such as burnability and supply [33] to a complicated framework involving 14 attributes, each with multiple characteristics [34]. While these complexities add value for economic studies, this paper argues for a simplified structure for regulatory purposes. This is similar to the approach adopted by the Swiss Financial Market Supervisory Authority to regulate ICOs in 2018 [34].

While complex taxonomies are logical in some contexts, this article advocates a simple approach based on a primary use case. This paper is the first to address taxonomy after the court’s determination, discussed below, that XRP is not inherently a security. It relies on the court’s reasoning that the type of transaction, rather than the nature of the underlying asset, is often what determines whether a transaction is a securities offering. This paper therefore makes two novel arguments. First, it argues that classification should be based on the primary purpose of an asset with a rebuttable presumption that sales of assets are for the assets’ intended use case. The use case should then be a question of fact rather than law. Second, it argues that based on the principle of comity, Bitcoin and other assets adopted as currencies in any country should at least be respected as a foreign currency in other jurisdictions, even where not adopted as a domestic medium of exchange.

3. Methodology

This article adopts a doctrinal approach to analyse recent cases involving the categorisation of decentralized digital assets, [35,36,37] the standard approach for most legal scholarship, along with a comparative analysis [35,38,39,40,41,42] examining cases, statutes, and the literature from multiple jurisdictions to propose a basic common taxonomy for DDAs. Doctrinal research focuses on legal principles and, by applying the methodology, this article undertakes a comprehensive and systematic analysis of legal doctrines in the emerging field. Doctrinal research traditionally involves the analysis of case law and statutes to critically interpret the law [43]. In addition to examining the existing literature, this article involves examining the existing legal frameworks including Bitcoin’s role as a currency in El Salvador, the first country to adopt Bitcoin as legal tender, and establishing a common taxonomy that works within existing legal frameworks.

4. An Overview of Blockchain Technology and Consensus Mechanisms

4.1. Distributed Ledger Technology

Blockchain is a distributed ledger that is hosted on multiple nodes, which can be located around the world [44,45]. A traditional ledger is held by only one party. For example, the bank keeps a record of all the transactions involving money going in or out of an account. For this to work, the bank must be trusted by customers in both its ability to keep an accurate ledger and its honesty in maintaining the ledger. Distributed ledger technology removes the need to trust a centralized party by allowing for anyone to hold a copy of the ledger, and it secures the ledger from unauthorized changes through cryptographic technology.

Each “block” comprises three types of data: transaction data, the hash for the current block, and the hash from the previous block. Hashes serve as digital fingerprints. They are unique to each block, and altering the data in a block would modify its hash [46]. Coupled with the fact that each block has the hash of the previous block, this makes it impossible to alter the data on a decentralized blockchain. This connection of each block of data by hashes is where the term blockchain is derived.

Sending or receiving assets takes the form of transactions that alter the ledger. Each user has an address, known as a public key, where others may send assets [47]. They also have a private key, akin to a password, which allows the user to send assets from the address. The Bitcoin private key is 64 characters, and the public key (address) is 26–35 characters. If a user makes a single digit error when sending a DDA, the asset can be lost. To manage addresses and private keys, digital wallets are used to interact with the chain [48]. To users, these wallets appear to hold balances, but only actually hold the user’s keys and reflect the balances held on nodes around the world.

4.2. Consensus Mechanisms

One way to categorize decentralized digital assets is through the consensus mechanism that secures the blockchain by ensuring only authorized transactions take place. There is a number of consensus mechanisms [49,50,51,52]. However, the two primary mechanisms are proof of work and proof of stake. These systems determine how the hashes are calculated to secure the blockchain.

4.2.1. Proof of Work

The proof of work consensus mechanism operates by slowing the rate at which computers can calculate the next hash to add a block to the blockchain. Bitcoin operates via proof of work, and a new block is added approximately once every ten minutes by computers, known as miners, that compete via calculations to update the blockchain. When successful, these miners are rewarded with Bitcoin, or other assets if mining on a different chain. By slowing the rate at which computers can calculate a hash, proof of work makes it difficult to alter past blocks. With a decentralized blockchain like Bitcoin, which has over 15,000 full nodes securing the blockchain worldwide, this provides such a high degree of security that the Bitcoin blockchain has never been hacked [32,53]. While highly secure, the high computational needs of proof of work have resulted in criticism over energy use [54,55]. However, Bitcoin, with its proof of work consensus mechanism, has also been argued to have positive environmental impacts such as reducing methane emission [56]. Due largely to environmental criticism, many projects have adopted the proof of stake model, including the Ethereum blockchain, which recently transitioned from proof of work.

4.2.2. Proof of Stake

Whereas proof of work relies on computing power to determine which nodes verify transactions and create a new block on the blockchain, proof of stake allows users of the chain’s native digital asset to determine which nodes update the chain by staking their tokens with nodes [57,58,59,60,61]. This reduces the computational power and thereby the energy required. The theory behind proof of stake is that those who hold assets will be incentivized to ensure the blockchain remains secure or the value of their digital assets will decrease. Some blockchains, such as Ethereum, which made the switch from proof of work to proof of stake in 2022 [62], also “slash” the staked assets if a node misbehaves to ensure no one tries to improperly alter the blockchain. The primary risk of proof of stake is the risk of centralization. Some centralized exchanges allow users who purchase DDAs and stake them through the centralized exchange, resulting in a high degree of centralization. While the interests of decentralized exchanges in maintaining the blockchain should be aligned with other users of the technology, pooling large quantities of an asset with one centralized exchange increases the risk of an attack by a hacker or other bad actor that would not exist in a truly decentralized environment.

Technical specifications, such as the consensus mechanism, is one way to categorize blockchains, but is of less legal significance when it comes to determining whether the sale of an asset constitutes a securities offering or whether the asset should be treated as a commodity or currency. Proof of stake, however, has a greater risk of centralization, which, in some circumstances, could signal reliance on an entity for development. There are benefits to proof of stake, especially for highly decentralized projects. For example, the high rate of staking of the native token ADA on the Cardano chain has resulted in a high degree of decentralization. The next session discusses the legal classification of DDAs.

5. Discussion

DDAs can be broadly placed into three categories: currencies, commodities and securities. See Table 1 below. In some circumstances, as will be discussed below, a DDA may be a currency or commodity in some context, but their sale, when completed with an expectation of profit from a third party, may constitute a security offering. This section begins by addressing the term cryptocurrency. Then, it discusses how, based on the principle of comity, assets that are legal tender in any country should be treated as a foreign currency in other jurisdictions. Finally, it addresses when DDAs may be deemed securities under recent jurisprudence.

Table 1.

Crypto asset categories.

5.1. Describing the Asset Class: Cryptocurrency, Virtual Assets, Digital Assets, or DDAs

Whether to use the term cryptocurrency to describe the entire asset class is a source of contention amongst many, with some proponents of the term cryptocurrency claiming the use of other terms, such as virtual assets, refuses to acknowledge the role of the asset class as a medium of exchange. While this may be true for some, even proponents could view the term as inappropriate for all decentralized digital assets. The first decentralized digital asset, Bitcoin, is certainly a cryptocurrency in that it was established to serve as a medium of exchange. Smart contract capable layer one chains, such as Ethereum, may be intended both as a medium of exchange and as a platform for smart contracts and web3 for a variety of commercial and non-commercial purposes [63,64,65,66,67,68]. Ether has been called “ultrasound money”, and in addition to its currency aspects, has utility in that it can be used to fund transactions, such as minting NFTs, beyond the limits of a traditional currency. Other tokens are used to fund transactions on DeFi protocols, and some are governance tokens that allow for holders to make decisions for decentralized autonomous organizations (DAOs). While they can be used as a medium of exchange, the focus of these tokens is a specific utility. As such, the term cryptocurrency could be seen to imply a more limited functionality than what exists for many decentralized digital assets. Some, of course, are currencies with Bitcoin legal tender in El Salvador.

Bitcoin is often described as an asset that serves as a store of value rather than primarily serving as a cryptocurrency, a characterization that has resulted in it often being called digital gold. While this may make sense from an investment perspective, with many individuals holding Bitcoin as a form of diversification rather than with the intent to use it, Bitcoin’s value flows from its ability to be easily and cheaply transferred. Unlike gold, which is tangible, Bitcoin is a distributed ledger, and its currency-related characteristics and the security of the chain underpin its value. While the court in the LBRY case was clear that a token with “both consumptive and speculative uses” can be an investment contract, a rebuttable presumption that the sale is for the intended use case would be a reasonable step in providing certainty and facilitate the development of decentralized projects without preventing regulatory oversight for actual securities.

In its examination of DDAs, the White House adopted the term “Digital Assets” and the Financial Action Task Force, an organization comprising 39 member states that set financial standards, adopted the term “Virtual assets” in its proposed regulatory framework [14]. However, these terms are even more ambiguous than cryptocurrency. Whereas being permissionless and decentralized are central tenets of what is generally considered a cryptocurrency, any digital file could be said to be a digital asset or virtual asset. Perhaps this terminology is meant to include central bank digital currencies, a form of digital asset that stands in stark contrast to permissionless and decentralized blockchains. It may also be intended to include assets such as NFTs, which are not themselves currencies and, due to the lack of fungibility, are distinct from other categories of decentralized digital assets.

The name cryptocurrency, referencing the cryptographic technology used to secure the blockchain, is perhaps an unfortunate label for distributed ledger-based digital assets. The term “crypto” carries a negative connotation, leading some to associate the technology with nefarious activity. While all tools can be used by nefarious actors, cryptography is also used by banks and email servers to protect accounts and ensure privacy. As such, the cryptography is not what is unique to decentralized digital assets, but rather the personal control of digital assets without the need to trust a third party to maintain and secure the ledger.

5.2. When Assets Are a Foreign Currency: The Principle of Comity

Comity is the “rules of politeness and courtesy observed by states in their mutual intercourse” [69]; it is a foundational principle in relations between states and is related to international public law. The principle, which has also been described as “respect” for other sovereigns, [70] has been said to have its origins in medieval law, ius gentium, or natural law [71]. The principle is employed both in the recognition of foreign laws, including some judgements, and as a basis of declining jurisdiction when it would encroach on the sphere of another sovereign. Comity does not employ strict legal requirements like the norms of international public law, which has resulted in it being called a “never-never land whose borders are marked by fuzzy lines of politics, courtesy and good faith” [72].

Although it may not be used as legal tender within a jurisdiction, foreign currency should be respected as currency based on comity. Indeed, even foreign currency controls have been argued to be protected on the basis of comity [73]. El Salvador and the Central African Republic both adopted Bitcoin as legal tender. However, the Central African Republic subsequently repealed the law. As Bitcoin is a legal currency in El Salvador, it should be respected, under the principle of comity, as a foreign currency in other nations. This does not mean other nations must use it as a medium of exchange, but that they treat it the same as other foreign currencies.

5.3. When an Asset Is a Security

If not a currency, an asset will generally be considered a commodity unless it meets the test to be deemed a security. To determine whether an asset is a security, a four-part test was established by the United States Supreme Court in the 1946 case of SEC v. Howey, which interpreted the Securities Act of 1933. Many other jurisdictions have established similar tests. Under the Howey test, an investment contract is considered a security if the following is present:

- There is an investment of money;

- Into a common enterprise;

- Where there is an expectation of profits;

- From the efforts of a promoter or other identifiable third party.

Most digital assets meet the first three parts of the Howey test, with the key issue being whether the desired profits are based on the efforts of a third party. If they are, the asset is deemed a security; if not, the asset is a commodity. Although regulators claim that most digital assets are securities, even the SEC has admitted that Bitcoin, being a highly decentralized digital asset, is not a security. However, many jurisdictions do not recognize it as a currency.

XRP, a DDA accused by the SEC of being a security, has a fixed supply of 100 billion, of which the three founders of Ripple, a related company, retained 20 billion and transferred 80 billion to Ripple. The goal of the network, for which XRP is the native token, is to serve as a fast and secure payment settlement system, putting it in competition with current financial payment systems such as SWIFT. As such, XRP is aimed largely at financial institutions and, shortly after the court’s decision, one country announced that XRP technology will be used in pilot central bank digital currency (CBDC) stable coin.

However, the judge rejected the classification of XRP as a security. Instead, the court held that “XRP, as a digital token, is not in and of itself a ‘contract transaction [,] or scheme’ that embodies the Howey requirements of an investment contract”. The court instead looked at each transaction, deciding that sales to institutional investors constituted securities offerings, but sales on the secondary market did not. The court reasoned that retail investors buying on exchanges and other secondary sales were not necessarily buying because of Ripple, and therefore did not have an expectation of profit from the activities of Ripple, whereas the institutional investors buying directly from Ripple did have this expectation.

The allegations against Ripple claimed that three categories of XRP sales constitute the unlicensed sale of securities. These include early sales made by Ripple to institutional buyers, XRP sales to digital asset exchanges, and the use of XRP by Ripple as payment to employees and developers.

In addressing these allegations, the court applied the Howey doctrine and clarified that the question is not whether an asset is a security for all purposes, but rather that the context of a transaction must be examined to determine whether an asset is the subject of an investment contract under the Howey test. The court stated that “ordinary assets”, such as gold, silver, and sugar, while ordinarily not securities, can also be sold as investment contracts in some circumstances. This shows that a commodity can, in some contexts, be the subject of an investment contract that constitutes a security. The court held that “[e]ven if XRP exhibits certain characteristics of a commodity or a currency, it may nonetheless be offered or sold as an investment contract”. As such, the court found that XRP “is not in and of itself a contract, transaction, or scheme” and therefore not inherently a security, but that some transactions could constitute a securities offering.

The court found that the sales to institutional investors constituted a security offering, but those made on exchanges to retail investors did not. Although retail investors were purchasing XRP as an investment and not for its utility, the court held that a “speculative motive” was insufficient to meet the Howey requirement that an expectation of profit must come from the efforts of others. Those who purchased XRP on exchanges were unaware of the sellers’ identities, and many purchasers were even unaware of the existence of Ripple, indicating they were not relying upon the efforts of Ripple for expected profits. However, this was not the case with institutional investors who purchased directly from Ripple and expected Ripple’s continued efforts to increase the value of XRP. Additionally, payments of XRP in consideration for services was held by the court not to constitute an investment, and therefore, these transactions were not found to be securities.

The outcome was a partial win for both sides and was hailed as a victory for Ripple by supporters of DDAs and a victory for the SEC by DDA’s detractors. However, the decision that XRP is not a not inherently a security and its sale on exchanges does not constitute a securities offering led to the immediate relisting of XRP on several exchanges and a jump in the token’s price. While the decision, subject to appeal, is binding on the parties, decisions by the District Court are merely persuasive, and not binding, on other courts. Therefore, the case provides clarity for XRP, but additional clarity for other projects will not be obtained until this case or others are appealed to higher courts that can establish a binding precedent for future cases. However, the fact that the court referred to XRP as having characteristics of a commodity or currency without explicitly assigning it a category may indicate a desire on behalf of the court to provide some certainty to investors and to those involved in the development of projects on distributed ledgers. The conclusion that the sale of XRP to institutional investors was not a sale of commodities but an investment contract was because the investors “understood the sale of XRP to be an investment in Ripple’s efforts”. This reasoning also provides a foundation to argue that DDAs provided with the intent that they be used as a medium of exchange and tokens provided for utility should be treated as currencies and commodities, respectively. A fact-based analysis considering the context of a sale will be necessary, but it would be reasonable to begin with a presumption based on the purpose of the token with assets such as Bitcoin, having a primary purpose of exchange, a currency, and the tokens used for other functionalities, such as using a decentralized exchange, presumed a commodity.

LBRY

The partial win for Ripple is the first for digital assets after a string of losses. After holding that Telegram violated securities laws through an initial coin offering [12] of its Gram token, in late 2022, the SEC also scored a victory over LBRY and its LBC token when the court held that despite not distributing tokens through an ICO, the LBC token sales were nevertheless a securities offering, violating Section 5 of the Securities Act of 1933.

LBRY operates a decentralized file sharing and payment network known for, among other things, providing the foundation for the decentralized YouTube competitor, Odyssey. The only disputed element of the Howey test was whether purchasers expected profits from the efforts of LBRY. While LBRY did not conduct an ICO, it sold these tokens and, in summary judgment, the court held that a reasonable purchaser would expect profit from the efforts of LBRY because LBRY “made no secret in its communications with potential investors that it expected LBC to grow in value through its managerial and entrepreneurial efforts”. The court also made it clear that disclaimers stating that the token was not an investment product do not negate the expectation of profit created by LBRY, which is an important lesson for future projects.

5.4. Establishing a Presumption Based on an Asset’s Purpose

As demonstrated above, the three major categories for regulatory purposes are already complicated, where the sale of the same asset may be viewed as a sale of a currency, commodity, or security in different contexts. For regulatory purposes, the trend towards more complex taxonomies will only further sow uncertainty and prevent development in the industry. To simplify the process, this article proposes building on the reasoning of the cases discussed above and establishes a rebuttable presumption that an asset is being used for a particular use case. Additionally, raising the standard for proof to rebut the presumption from a preponderance of the evidence to clear and convincing evidence would provide additional certainty within the industry.

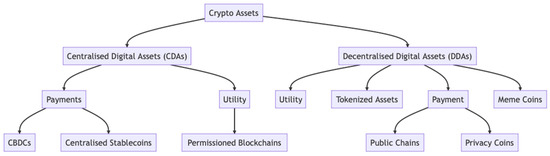

As can be seen from Figure 1, there are four large categories of DDAs identified, with payment and utility being the primary categories. Securities are not a specific category because the categorizations as a security would depend not just on the asset, but the intention at the sale to know whether it meets the Howey test. The term, cryptocurrency, is not adopted here due to the vagueness of the term. Some may view payment tokens as the correct place for the cryptocurrency label, while others would consider the DDA label the correct place. Some have even associated CDAs with cryptocurrency even though they contrast the decentralized principles of DDAs.

Figure 1.

Taxonomy of crypto assets.

Tokenized assets, which could arguably be placed under the CDA heading and/or grouped with centralized stable coins, is a complex area and beyond the scope of this article, as are meme coins. In this taxonomy, meme coins only include coins that have no value proposition aside from the meme, and not coins that have an intended function and are capitalized upon a meme for marketing purposes. For example, Pepe coin, which had no stated use case but was traded on pure speculation to a temporary market capitalization of over USD 1.6 billion, would fit in this category at the time of writing [74]. The sale of these tokens may constitute a securities offering, but the underlying asset is more akin to digital trading cards than a regulated commodity or other asset class. There is also an overlap between tokenized assets and NFTs [75]. However, NFTs can be used for a variety of purposes.

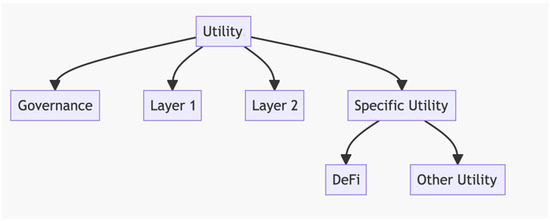

Utility tokens, which are meant to be used primarily for a purpose other than a medium of exchange, are perhaps the most complex category due to the diversity of use cases. Figure 2 illustrates the major use cases, which include governance tokens that allow the user to vote or make proposals regarding the project or DAO, native assets on layer 1 blockchains such as Ether and ADA, layer 2 scaling solutions to help increase the speed and capacity of layer 1s, and tokens for other specific utilities, such as decentralized finance (DeFi). While other types of regulations may be necessary depending on the use case, utility tokens, often used as “gas” to utilize the blockchain, are somewhat analogous to oil and should be viewed as commodities.

Figure 2.

Utility assets.

While some use-case-specific regulation may be necessary for certain assets, simplifying the structure with a basic descriptive taxonomy and a presumption that the sale of assets is for the assets’ intended use case will support the government’s interest in regulating while providing a greater degree of certainty for developers and users of DDAs. For assets that exist simultaneously on distributed ledgers around the world, this approach also strikes a balance between flexibility, in that countries can adopt more detailed regulations within sub-categories, and certainty for the industry. Perhaps most importantly, the approach is consistent with the recent jurisprudence, making its adoption feasible.

6. Conclusions

Since the creation of the first cryptocurrency in 2009, technological advances and the development of decentralized digital assets with varying use cases has increased ambiguity in terminology, which poses a challenge in establishing a coherent and adaptable regulatory framework that supports development within the industry. Traditional financial regulatory frameworks, designed in a pre-digital age, fail to consider the complexity of the asset class.

Recent decisions regarding the sale of LBC and XRP tokens make it clear that under the Howey test, the sale of an asset may constitute a security offering, even if the underlying asset is otherwise a currency or commodity. However, because decentralisation decreases the likelihood that a purchaser of a currency or commodity is relying on others to profit, the sales of truly decentralized assets, like Bitcoin, are less likely to be deemed securities offerings than assets that require substantial development. For developers and investors in DDAs, a lack of clear standards and varying standards between jurisdictions places uncertainty and potential compliance costs that may supress the development of new technologies. To avoid this and facilitate technological development while permitting the regulation of actual securities, a simplified framework should be adopted with a rebuttable presumption that the sale of an asset is for the asset’s intended use case. This framework would allow for developers of utility tokens to issue and sell tokens for use without the uncertainty from the current lack of a clear regulatory framework.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

No new data were created as part of this research.

Conflicts of Interest

The author does not own any decentralized digital assets and declares no conflicts of interest.

References

- Przytarski, D.; Stach, C.; Gritti, C.; Mitschang, B. Query Processing in Blockchain Systems: Current State and Future Challenges. Future Internet 2022, 14, 1. [Google Scholar] [CrossRef]

- Kshetri, N. The nature and sources of international variation in formal institutions related to initial coin offerings: Preliminary findings and a research agenda. Financ. Innov. 2023, 9, 9. [Google Scholar] [CrossRef]

- Ali, A.; Al-Rimy, B.A.S.; Alsubaei, F.S.; Almazroi, A.A.; Almazroi, A.A. HealthLock: Blockchain-Based Privacy Preservation Using Homomorphic Encryption in Internet of Things Healthcare Applications. Sensors 2023, 23, 6762. [Google Scholar] [CrossRef]

- Batista, D.; Mangeth, A.L.; Frajhof, I.; Alves, P.H.; Nasser, R.; Robichez, G.; Silva, G.M.; de Miranda, F.P. Exploring Blockchain Technology for Chain of Custody Control in Physical Evidence: A Systematic Literature Review. J. Risk Financ. Manag. 2023, 16, 360. [Google Scholar] [CrossRef]

- Sultana, S.A.; Rupa, C.; Malleswari, R.P.; Gadekallu, T.R. IPFS-Blockchain Smart Contracts Based Conceptual Framework to Reduce Certificate Frauds in the Academic Field. Information 2023, 14, 446. [Google Scholar] [CrossRef]

- Li, S.; Zhou, T.; Yang, H.; Wang, P. Blockchain-Based Secure Storage and Access Control Scheme for Supply Chain Ecological Business Data: A Case Study of the Automotive Industry. Sensors 2023, 23, 7036. [Google Scholar] [CrossRef] [PubMed]

- Uddin, M.; Selvarajan, S.; Obaidat, M.; Arfeen, S.U.; Khadidos, A.O.; Khadidos, A.O.; Abdelhaq, M. From Hype to Reality: Unveiling the Promises, Challenges and Opportunities of Blockchain in Supply Chain Systems. Sustainability 2023, 15, 12193. [Google Scholar] [CrossRef]

- Singh, A.; Ganesh, A.; Patil, R.R.; Kumar, S.; Rani, R.; Pippal, S.K. Secure Voting Website Using Ethereum and Smart Contracts. Appl. Syst. Innov. 2023, 6, 70. [Google Scholar] [CrossRef]

- Metelski, D.; Sobieraj, J. Decentralized Finance (DeFi) Projects: A Study of Key Performance Indicators in Terms of DeFi Protocols’ Valuations. Int. J. Financ. Stud. 2022, 10, 108. [Google Scholar]

- Miglo, A. STO vs. ICO: A Theory of Token Issues under Moral Hazard and Demand Uncertainty. J. Risk Financ. Manag. 2021, 14, 232. [Google Scholar] [CrossRef]

- Cumming, D.J.; Johan, S.; Pant, A. Regulation of the Crypto-Economy: Managing Risks, Challenges, and Regulatory Uncertainty. J. Risk Financ. Manag. 2019, 12, 126. [Google Scholar] [CrossRef]

- Bobovich, N. Analyzing Key Events & Causal Factors Impacting Cryptocurrency Lending Rates. Wharton Research Scholars. Program Thesis, University of Pennsylvania, Philadelphia, PA, USA, 2023. [Google Scholar]

- Forehand, A. Coin Rush in the Virtual Wild West: The SEC as the New Sheriff in Town. Seton Hall L. Rev. 2022, 53, 387. [Google Scholar]

- De Koker, L.; Ocal, T.; Casanovas, P. Where’s Wally? FATF, virtual asset service providers, and the regulatory jurisdictional challenge. In Financial Technology and the Law: Combating Financial Crime; Springer: Berlin/Heidelberg, Germany, 2022; pp. 151–183. [Google Scholar]

- Force, F.A.T. Guidance for a risk-based approach to virtual assets and virtual asset service providers. Retrieved. 2019, 12, 2023. [Google Scholar]

- Waheed Muhammad, U.Z.W. Legal Insights of Crypto-currency Market and State of Crypto-currency in Pakistan. Super. Law Rev. 2022, 2, 77–104. [Google Scholar]

- Elzweig, B.; Trautman, L.J. When Does a Non-Fungible Token (NFT) Become a Security? Ga. St. UL Rev. 2022, 39, 295. [Google Scholar]

- Guseva, Y.; Hutton, I. Digital Asset Innovations and Regulatory Fragmentation: The SEC versus the CFTC. Boston Coll. Law Rev. 2023; forthcoming. [Google Scholar]

- Moffett, T.A. CFTC & SEC: The Wild West of Cryptocurrency Regulation. U. Rich. L. Rev. 2022, 57, 713. [Google Scholar]

- Shurr, T.E. A False Sense of Security: How Congress and the SEC are Dropping the Ball on Cryptocurrency. Dickinson L Rev. 2020, 125, 253. [Google Scholar]

- Fokri, W.N.I.W.M. Classification of cryptocurrency: A review of the literature. Turk. J. Comput. Math. Educ. TURCOMAT 2021, 12, 1353–1360. [Google Scholar]

- Andersen, P. Will the FTX Collapse Finally Force US Policymakers to Wake up?: Regulatory Solutions for Cryptocurrency Tokens Not Classified as Securities under the Supreme Court’s Howey Analysis. J. Bus. Tech. L. 2022, 18, 251. [Google Scholar]

- Henderson, M.T.; Raskin, M. A regulatory classification of digital assets: Toward an operational Howey test for cryptocurrencies, ICOs, and other digital assets. Colum. Bus. L. Rev. 2019, 2019, 443–493. [Google Scholar] [CrossRef]

- Trotz, E.D. The Times They Are a Changin’: Surveying How the Howey Test Applies to Various Cryptocurrencies. Elon L. Rev. 2019, 11, 201. [Google Scholar]

- Van Adrichem, B. Howey Should be Distributing New Cryptocurrencies: Applying the Howey Test to Mining, Airdropping, Forking, and Initial Coin Offerings. Colum. Sci. Tech. L. Rev. 2018, 20, 388. [Google Scholar]

- Alshater, M.M.; Joshipura, M.; Khoury, R.E.; Nasrallah, N. Initial coin offerings: A hybrid empirical review. Small Bus. Econ. 2023, 1–18. [Google Scholar] [CrossRef]

- Di Matteo, G.; Za, S.; Ulrich, K. Initial Coin Offering: A Taxonomy Based Approach to Explore the Field. In Proceedings of the MENACIS2021, Agadir, Morocco, 11–14 November 2021. [Google Scholar]

- Holden, R.; Malani, A. An examination of velocity and initial coin offerings. Manag. Sci. 2022, 68, 9026–9041. [Google Scholar] [CrossRef]

- Momtaz, P.P. Token sales and initial coin offerings: Introduction. J. Altern. Invest. 2019, 21, 7–12. [Google Scholar] [CrossRef]

- Zhai, Y. Safeguarding Innovation: Exploring the Role of Criminal Justice Systems in Protecting Intellectual Property Rights, Combating Piracy, and Promoting Socio-Economic Stability. Int. J. Crim. Justice Sci. 2023, 18, 317–347. [Google Scholar]

- Wronka, C. Anti-money laundering regimes: A comparison between Germany, Switzerland and the UK with a focus on the crypto business. J. Money Laund. Control. 2022, 25, 656–670. [Google Scholar] [CrossRef]

- Watters, C. When Criminals Abuse the Blockchain: Establishing Personal Jurisdiction in a Decentralised Environment. Laws 2023, 12, 33. [Google Scholar] [CrossRef]

- Oliveira, L.; Zavolokina, L.; Bauer, I.; Schwabe, G. (Eds.) To Token or Not to Token: Tools for Understanding Blockchain Tokens; ICIS: Sutton, UK, 2018. [Google Scholar]

- Ankenbrand, T.; Bieri, D.; Cortivo, R.; Hoehener, J.; Hardjono, T. (Eds.) Proposal for a comprehensive (crypto) asset taxonomy. In Proceedings of the 2020 Crypto Valley Conference on Blockchain Technology (CVCBT), Rotkreuz, Switzerland, 11–20 June 2020; IEEE: Piscataway, NJ, USA, 2020. [Google Scholar]

- Roy, U. Doctrinal and Non-Doctrinal Methods of Research: A Comparative Analysis of Both within the Field of Legal Research. Issue 2 Indian JL Leg. Rsch 2023, 5, 1. [Google Scholar]

- Samuel, G. Can Doctrinal Legal Scholarship Be Defended? Amic. Curiae 2022, 4, 43. [Google Scholar] [CrossRef]

- Taekema, S.; van der Burg, W. Legal philosophy as an enrichment of doctrinal research–part II: The purposes of including legal philosophy. Law Method 2022, 1–19. [Google Scholar] [CrossRef]

- Adams, M. Doing what doesn’t come naturally. On the distinctiveness of comparative legal research. In Methodologies of Legal Research Which Kind of Method for What Kind of Discipline? Hart Publishing: Oxford, UK, 2011; pp. 229–240. [Google Scholar]

- Brand, O. Conceptual comparisons: Towards a coherent methodology of comparative legal studies. Brook J. Int. L. 2006, 32, 405. [Google Scholar]

- Gordley, J. Comparative legal research: Its function in the development of harmonized law. Am. J. Comp. L. 1995, 43, 555. [Google Scholar] [CrossRef][Green Version]

- Yntema, H.E. Comparative Legal Research: Some Remarks on" Looking out of the Cave". Mich. Law Rev. 1956, 54, 899–928. [Google Scholar] [CrossRef]

- Van Hoecke, M. Methodology of comparative legal research. Pravovedenie 2013, 121, 1–35. [Google Scholar] [CrossRef]

- Gawas, V.M. Doctrinal legal research method a guiding principle in reforming the law and legal system towards the research development. Int. J. Law 2017, 3, 128–130. [Google Scholar]

- Soltani, R.; Zaman, M.; Joshi, R.; Sampalli, S. Distributed Ledger Technologies and Their Applications: A Review. Appl. Sci. 2022, 12, 7898. [Google Scholar] [CrossRef]

- Pinto, F.; da Silva, C.F.; Moro, S. People-centered distributed ledger technology-IoT architectures: A systematic literature review. Telemat. Inform. 2022, 70, 101812. [Google Scholar] [CrossRef]

- Allenotor, D.; Oyemade, D. An Optimized Parallel Hybrid Architecture for Cryptocurrency Mining. Adv. Multidiscip. Sci. Res. J. Publ. 2021, 12, 95–104. [Google Scholar]

- Liu, Y.; Li, R.; Liu, X.; Wang, J.; Zhang, L.; Tang, C.; Kang, H. (Eds.) An efficient method to enhance Bitcoin wallet security. In Proceedings of the 2017 11th IEEE International Conference on Anti-Counterfeiting, Security, and Identification (ASID), Xiamen, China, 27–29 October 2017; IEEE: Piscataway, NJ, USA, 2017. [Google Scholar]

- Suratkar, S.; Shirole, M.; Bhirud, S. (Eds.) Cryptocurrency wallet: A review. In Proceedings of the 2020 4th International Conference on Computer, Communication and Signal Processing (ICCCSP), Virtual, 28–29 September 2020; IEEE: Piscataway, NJ, USA, 2020. [Google Scholar]

- Nijsse, J.; Litchfield, A. A taxonomy of blockchain consensus methods. Cryptography 2020, 4, 32. [Google Scholar] [CrossRef]

- Xie, M.; Liu, J.; Chen, S.; Lin, M. A survey on blockchain consensus mechanism: Research overview, current advances and future directions. Int. J. Intell. Comput. Cybern. 2023, 16, 314–340. [Google Scholar] [CrossRef]

- Yadav, A.K.; Singh, K.; Amin, A.H.; Almutairi, L.; Alsenani, T.R.; Ahmadian, A. A comparative study on consensus mechanism with security threats and future scopes: Blockchain. Comput. Commun. 2023, 201, 102–115. [Google Scholar] [CrossRef]

- Zheng, Q.; Wang, L.; He, J.; Li, T. KNN-Based Consensus Algorithm for Better Service Level Agreement in Blockchain as a Service (BaaS) Systems. Electronics 2023, 12, 1429. [Google Scholar] [CrossRef]

- Bailey, A.M.; Warmke, C. Bitcoin is King; J. Liebowitz: London, UK; New York, NY, USA, 2023; pp. 175–197. [Google Scholar]

- Rudd, M.A. 100 Important Questions about Bitcoin’s Energy Use and ESG Impacts. Challenges 2023, 14, 1. [Google Scholar]

- Sapra, N.; Shaikh, I.; Dash, A. Impact of Proof of Work (PoW)-Based Blockchain Applications on the Environment: A Systematic Review and Research Agenda. J. Risk Financ. Manag. 2023, 16, 218. [Google Scholar] [CrossRef]

- Rudd, M.A. Bitcoin Is Full of Surprises. Challenges 2023, 14, 27. [Google Scholar] [CrossRef]

- Auhl, Z.; Chilamkurti, N.; Alhadad, R.; Heyne, W. A Comparative Study of Consensus Mechanisms in Blockchain for IoT Networks. Electronics 2022, 11, 2694. [Google Scholar] [CrossRef]

- Zhou, S.; Li, K.; Xiao, L.; Cai, J.; Liang, W.; Castiglione, A. A Systematic Review of Consensus Mechanisms in Blockchain. Mathematics 2023, 11, 2248. [Google Scholar] [CrossRef]

- Chen, R.; Wang, L.; Zhu, R. Improvement of Delegated Proof of Stake Consensus Mechanism Based on Vague Set and Node Impact Factor. Entropy 2022, 24, 1013. [Google Scholar] [CrossRef] [PubMed]

- Hafid, A.; Hafid, A.S.; Makrakis, D. Sharding-Based Proof-of-Stake Blockchain Protocols: Key Components & Probabilistic Security Analysis. Sensors 2023, 23, 2819. [Google Scholar]

- Bachani, V.; Bhattacharjya, A. Preferential Delegated Proof of Stake (PDPoS)—Modified DPoS with Two Layers towards Scalability and Higher TPS. Symmetry 2023, 15, 4. [Google Scholar] [CrossRef]

- Kapengut, E.; Mizrach, B. An Event Study of the Ethereum Transition to Proof-of-Stake. Commodities 2023, 2, 96–110. [Google Scholar] [CrossRef]

- Liang, Y.; Watters, C.; Lemański, M.K. Responsible Management in the Hotel Industry: An Integrative Review and Future Research Directions. Sustainability 2022, 14, 17050. [Google Scholar] [CrossRef]

- Khezami, N.; Gharbi, N.; Neji, B.; Braiek, N.B. Blockchain Technology Implementation in the Energy Sector: Comprehensive Literature Review and Mapping. Sustainability 2022, 14, 15826. [Google Scholar] [CrossRef]

- Aloini, D.; Benevento, E.; Stefanini, A.; Zerbino, P. Transforming healthcare ecosystems through blockchain: Opportunities and capabilities for business process innovation. Technovation 2023, 119, 102557. [Google Scholar] [CrossRef]

- Wenhua, Z.; Qamar, F.; Abdali, T.-A.N.; Hassan, R.; Jafri, S.T.A.; Nguyen, Q.N. Blockchain technology: Security issues, healthcare applications, challenges and future trends. Electronics 2023, 12, 546. [Google Scholar] [CrossRef]

- Zanghi, E.; Do Coutto Filho, M.B.; de Souza, J.C.S. Collaborative smart energy metering system inspired by blockchain technology. Int. J. Innov. Sci. 2023; ahead of print. [Google Scholar]

- Mololoth, V.K.; Saguna, S.; Åhlund, C. Blockchain and machine learning for future smart grids: A review. Energies 2023, 16, 528. [Google Scholar] [CrossRef]

- Hall, W.E. A Treatise on International Law, 7th ed.; Clarendon Press: Oxford, UK, 1917. [Google Scholar]

- Garner, B.A. Black’s Law Dictionary; Thomson West: Eagan, MN, USA, 2014. [Google Scholar]

- Paul, J.R. Comity in International Law. Harv. Int. Law J. 1991, 31, 1–80. [Google Scholar]

- Maier, H. Extraterritorial Jurisdiction at a Crossroads: The Intersection Between Public and Private International Law. Am. J. Int. Law 1982, 76, 280. [Google Scholar] [CrossRef]

- Gianviti, F. Current Legal Aspects of Monetary Sovereignty. In Current Developments in Monetary and Financial Law; International Monetary Fund: Washington, DC, USA, 2004. [Google Scholar]

- Weiss, B. How the Pepe coin, ‘fueled by pure memetic power,’ soared past a $1.6 billion market cap in 3 weeks—And then tumbled. Fortune. 9 May 2023. Available online: https://fortune.com/crypto/2023/05/09/how-the-pepe-token-fueled-by-pure-memetic-power-soared-past-a-1-6-billion-market-cap-in-3-weeks-and-then-tumbled/ (accessed on 28 September 2023).

- Zarifis, A.; Castro, L. The NFT Purchasing Process and the Challenges to Trust at Each Stage. Sustainability 2022, 14, 16482. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).