COVID-19 Influence on Developments in the Global Beef and Sheep Sectors

Abstract

:1. Introduction

2. Materials and Methods

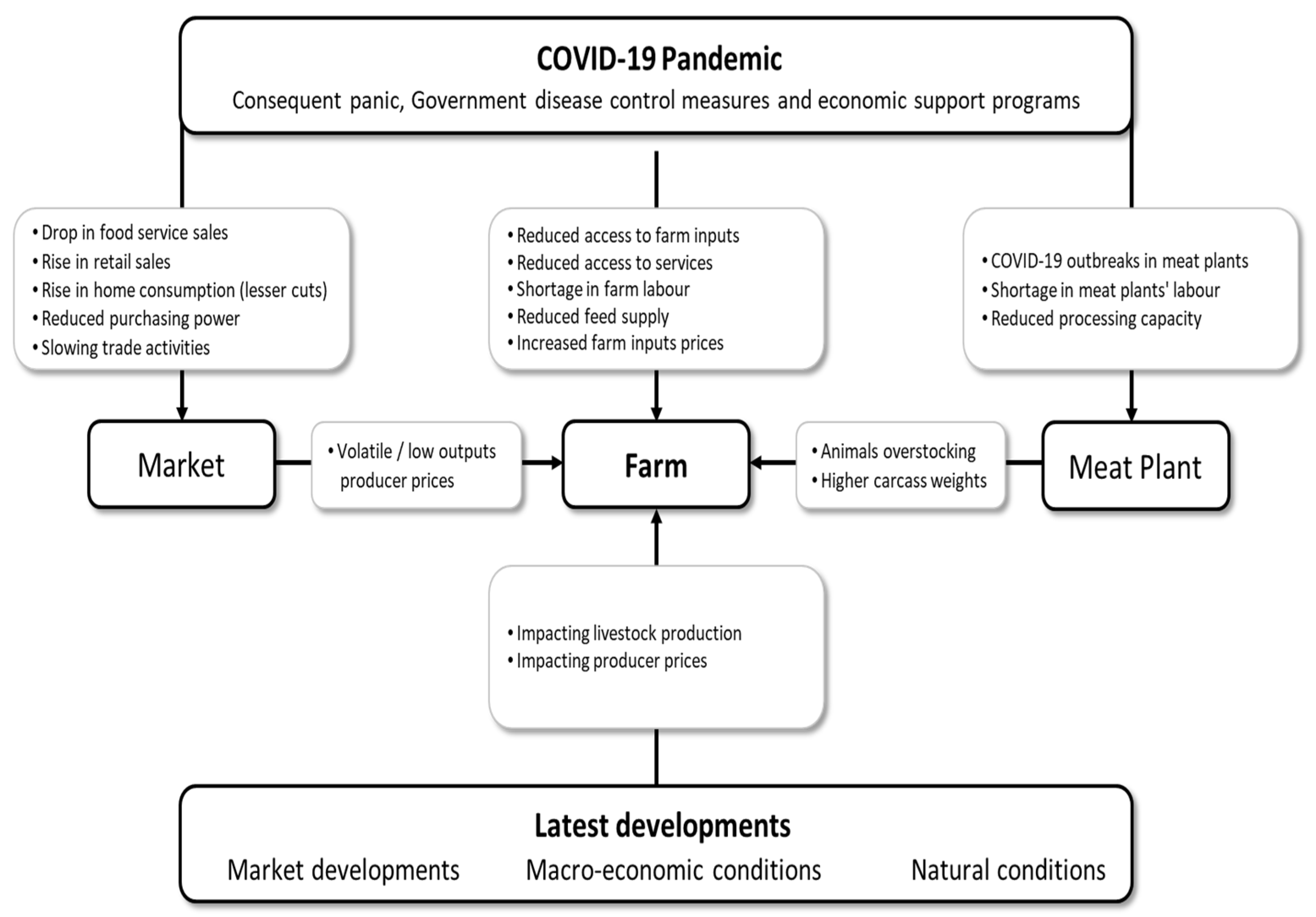

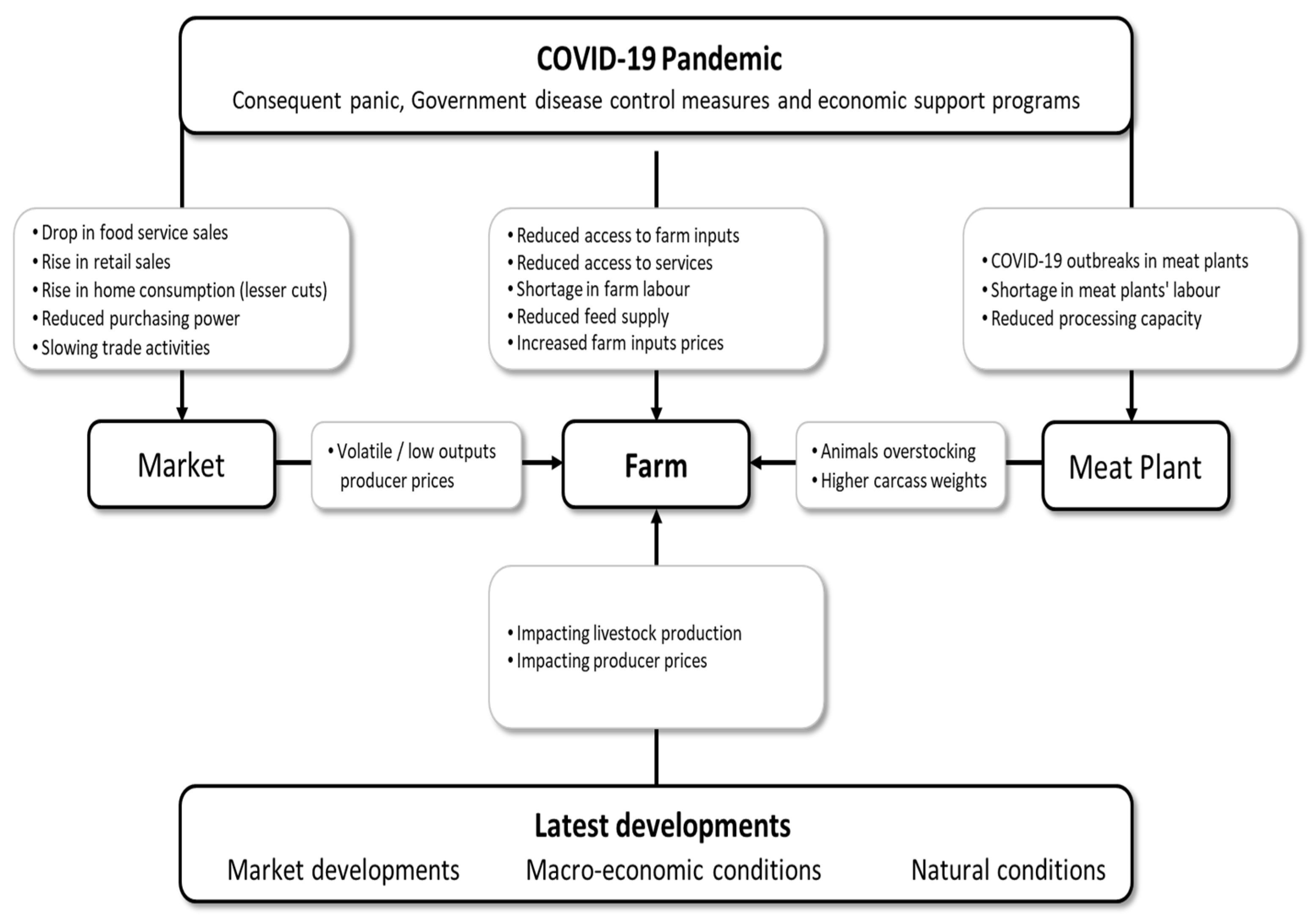

2.1. Research Framework

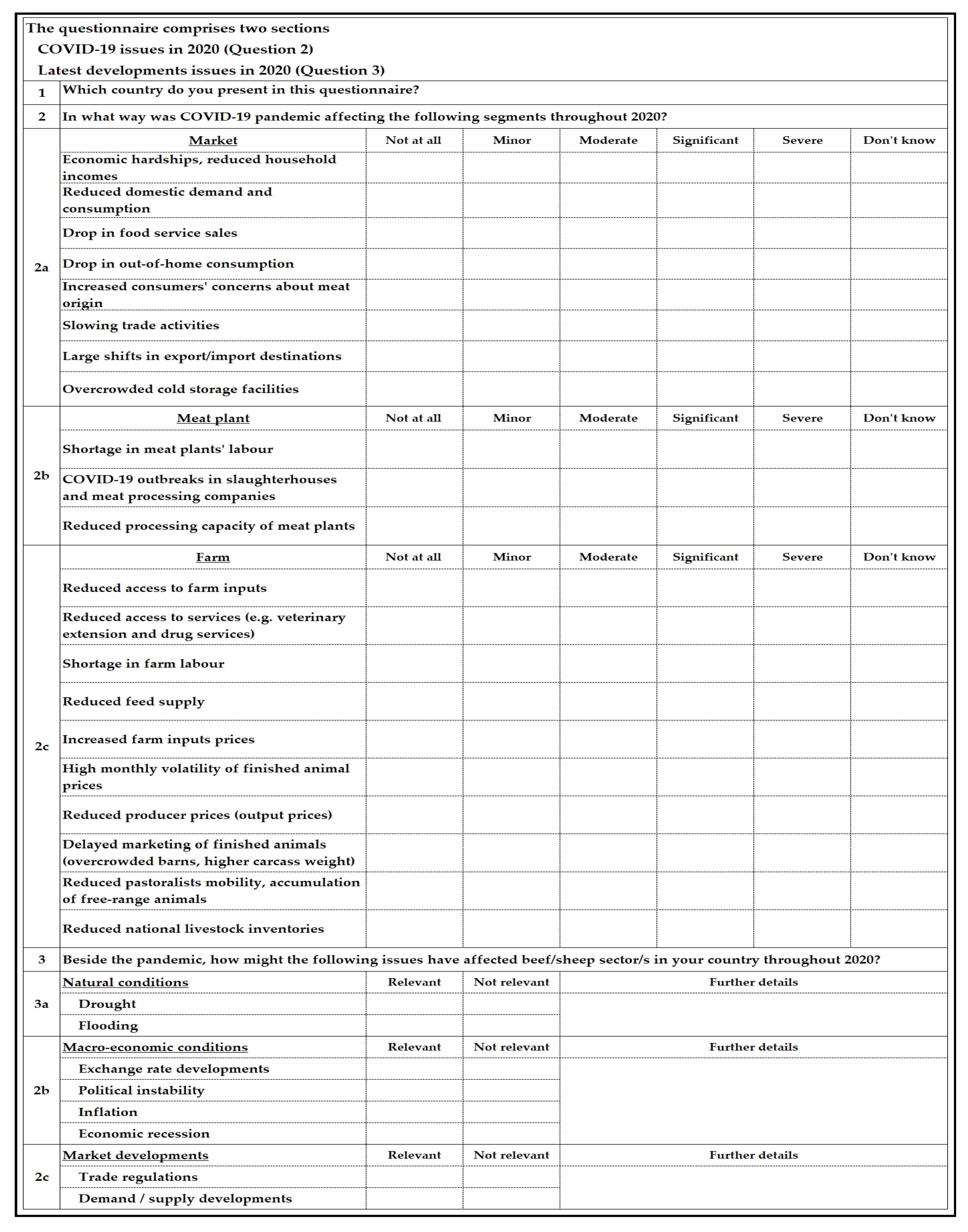

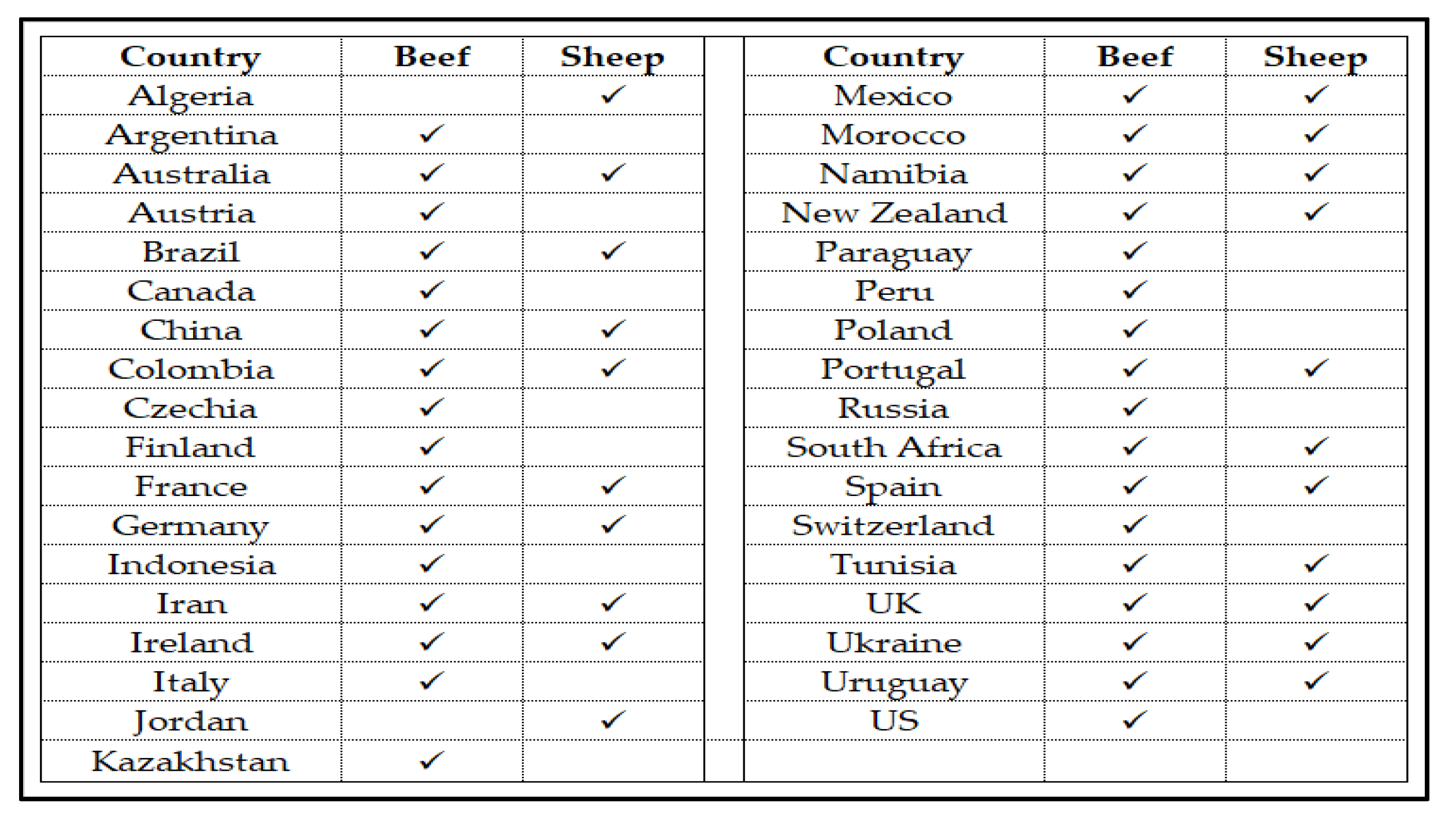

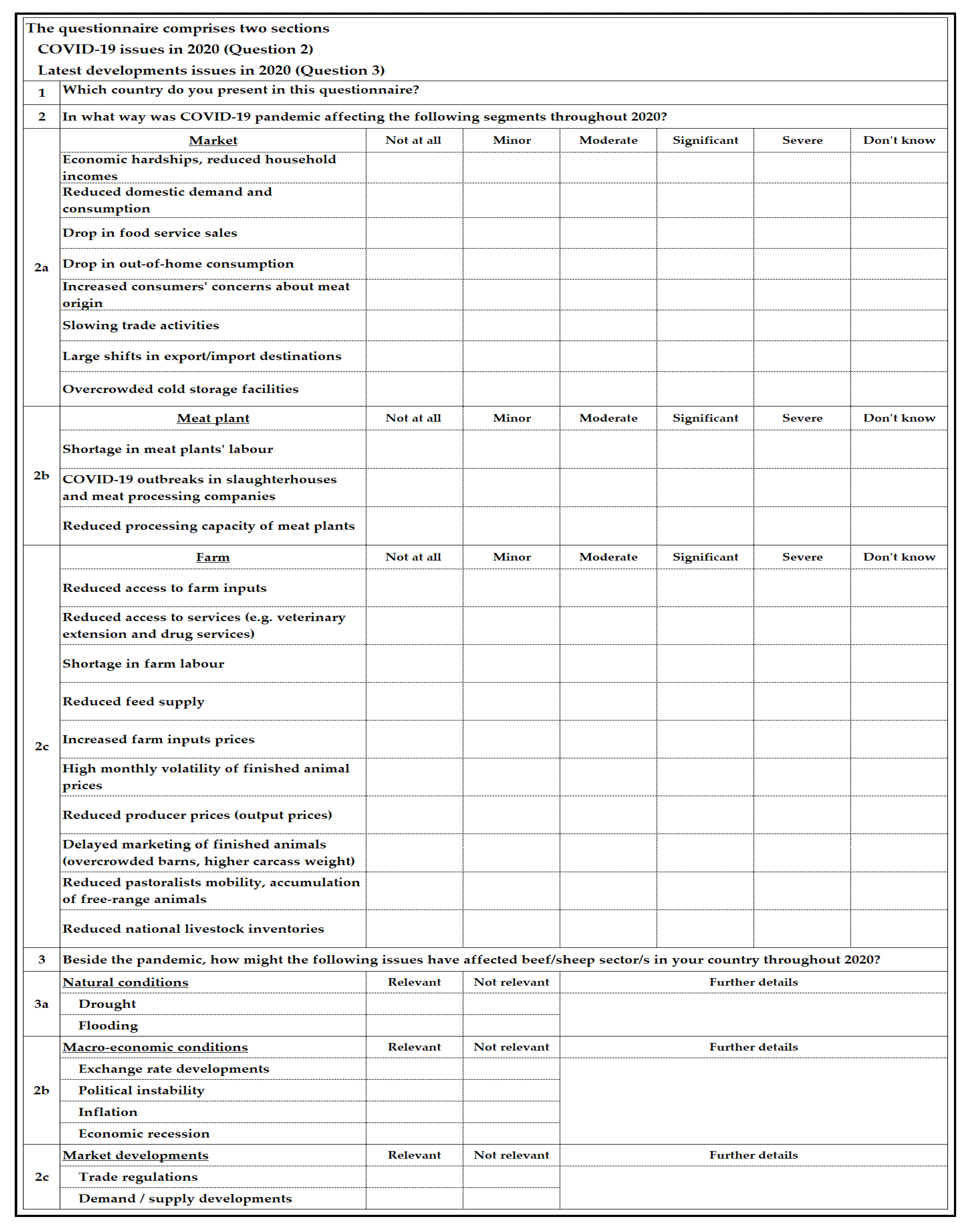

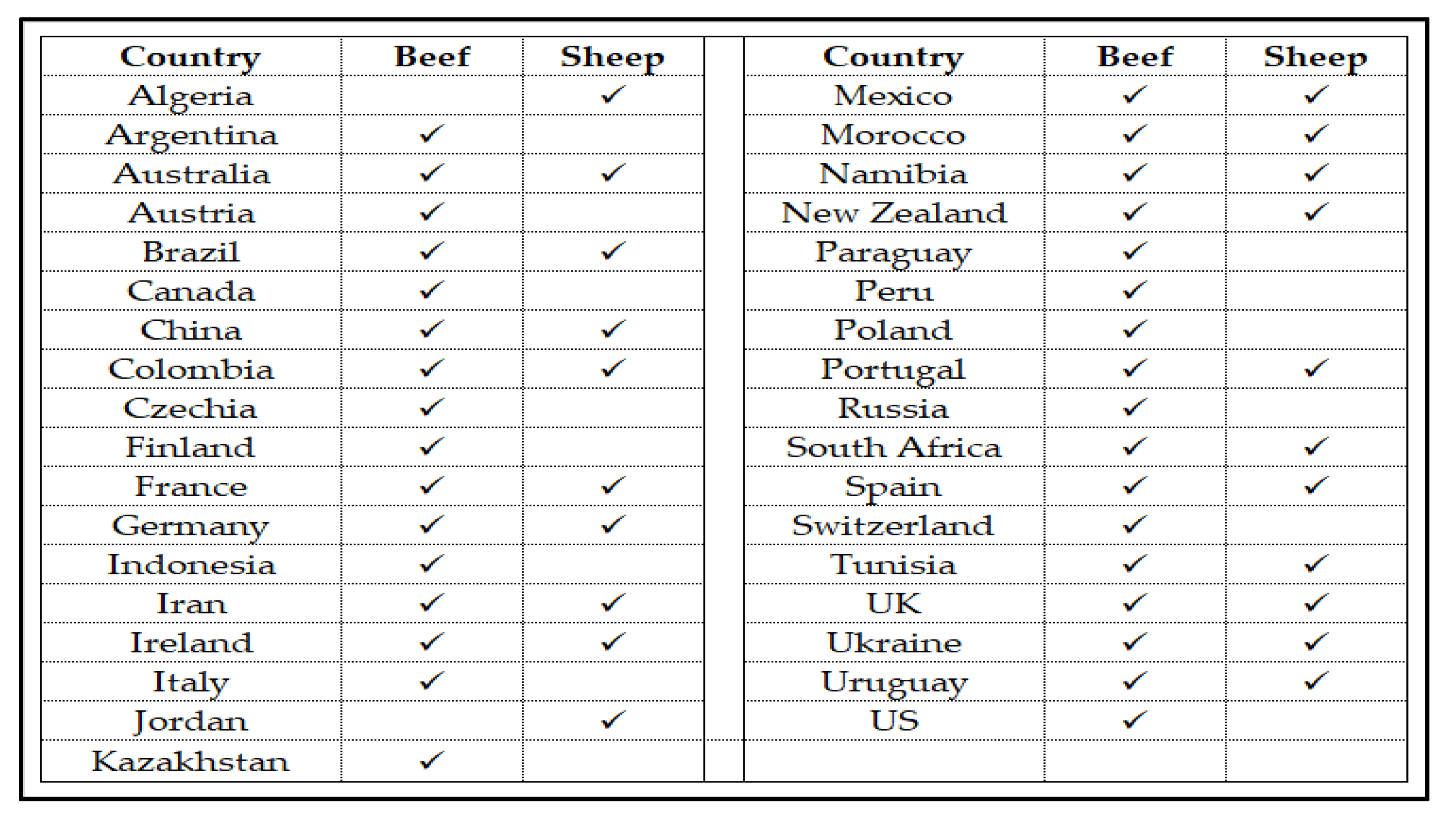

2.2. Data Sources and Analysis

3. Results and Discussion

3.1. COVID-19 and Global Beef and Sheep Meat Markets

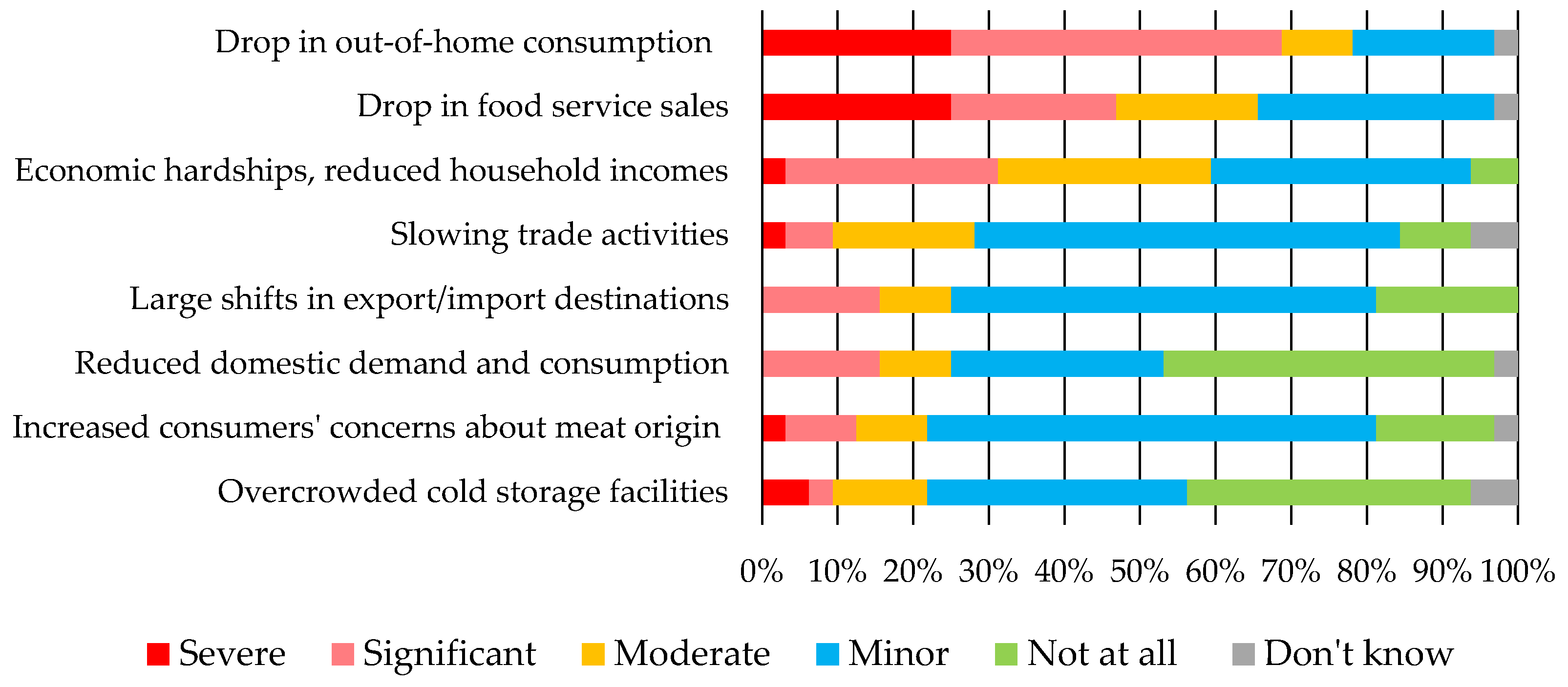

3.1.1. Survey Results on Meat Markets

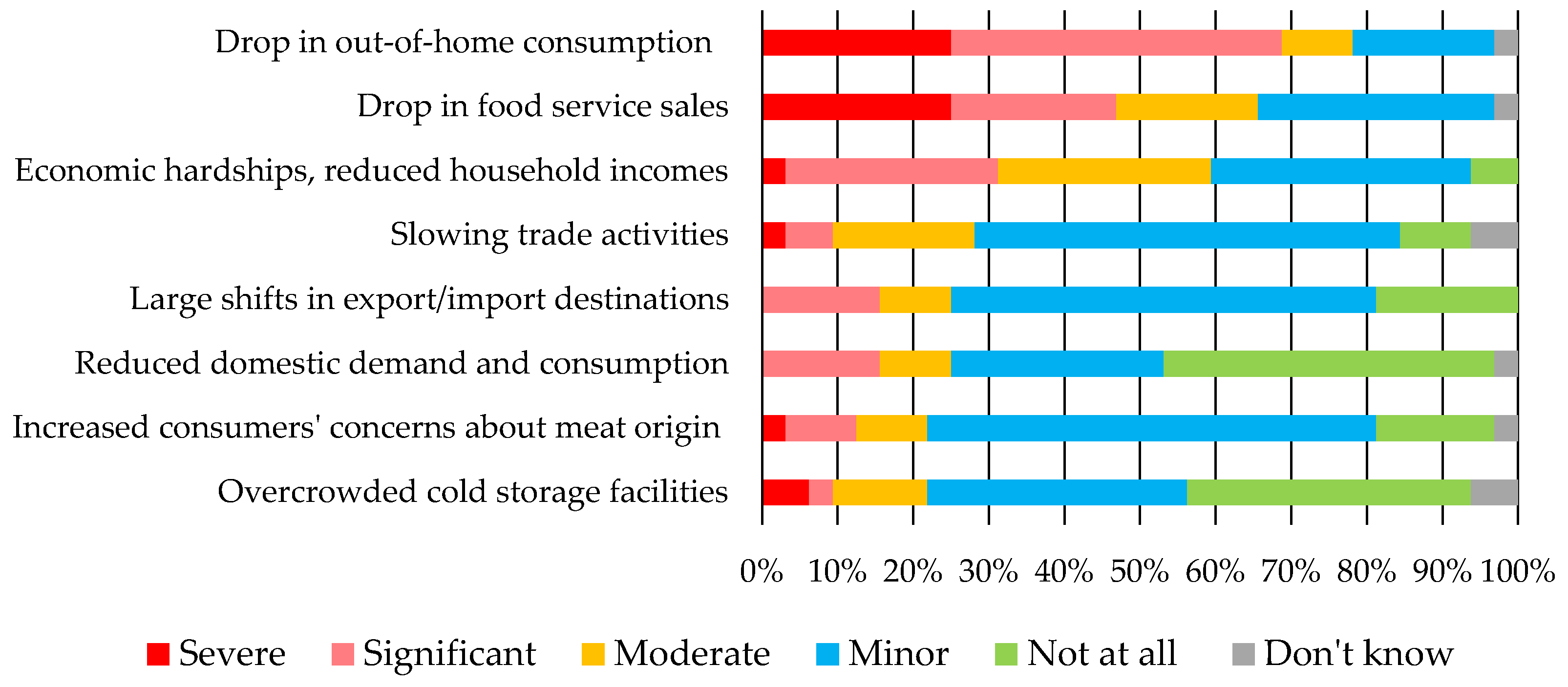

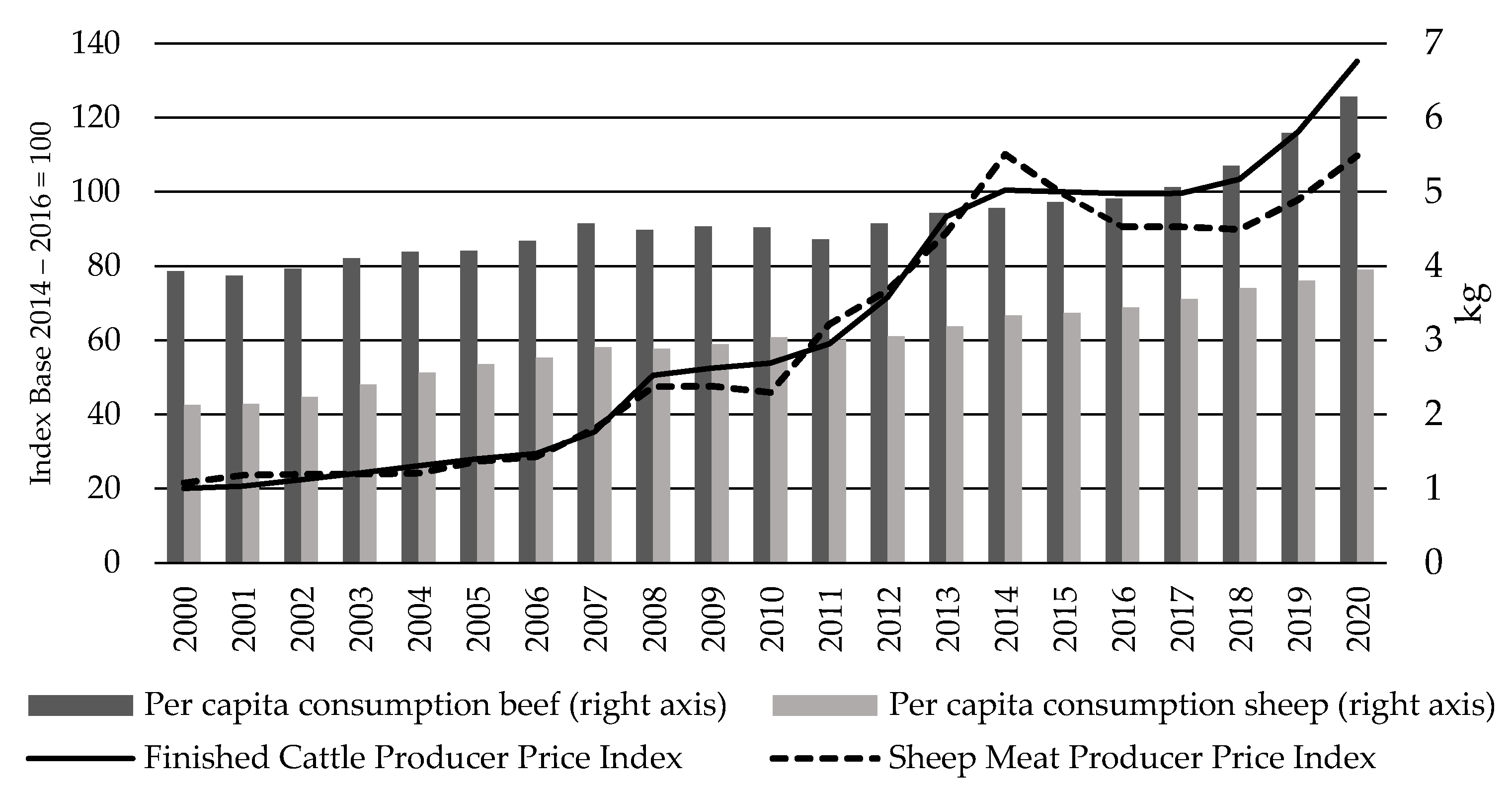

3.1.2. Discussion on Domestic Meat Demand and Consumption

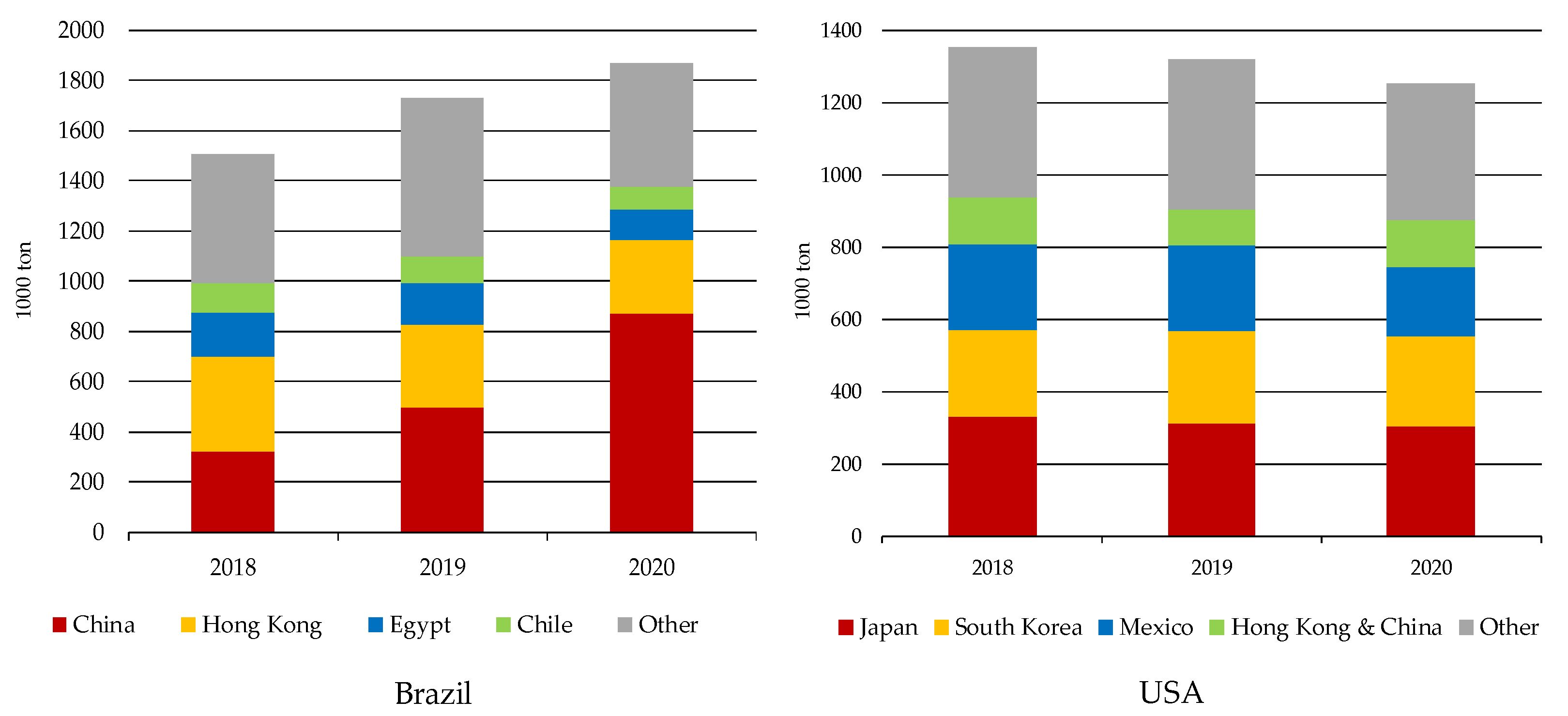

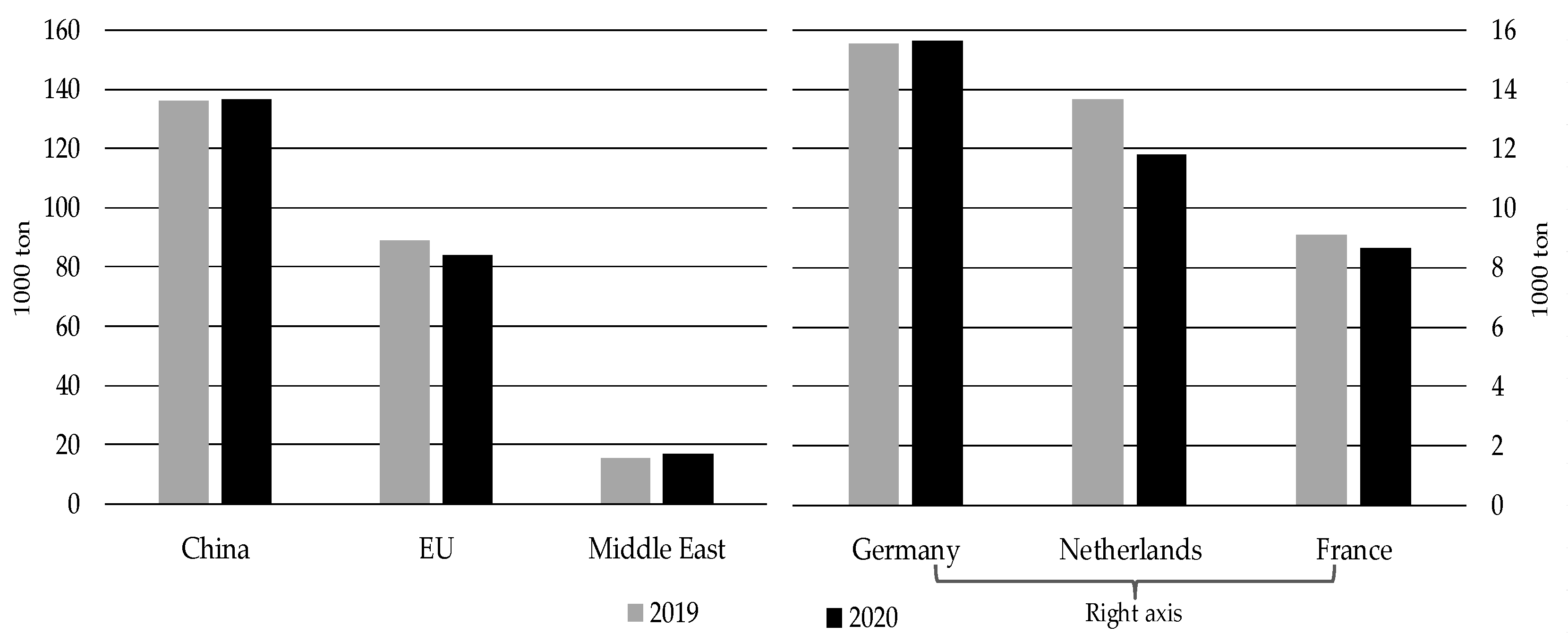

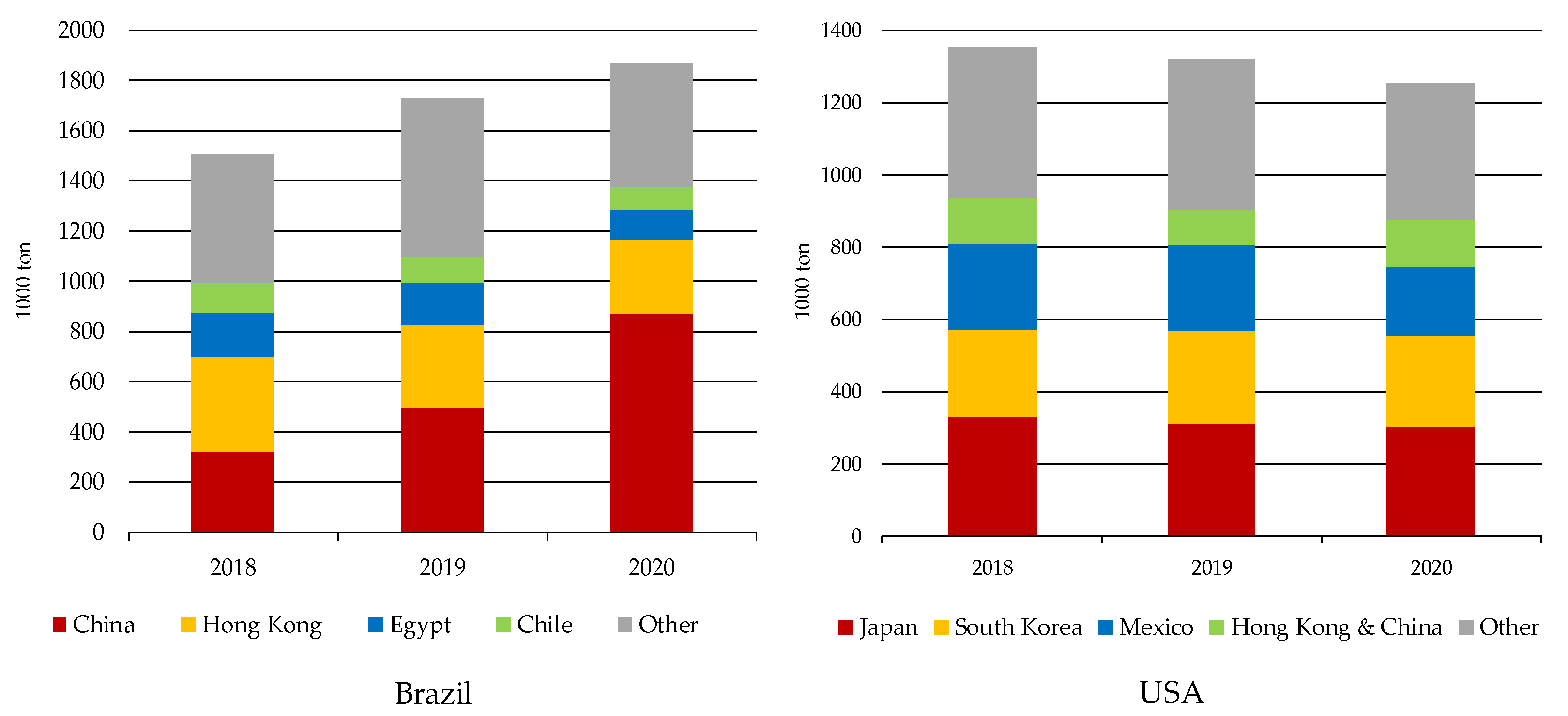

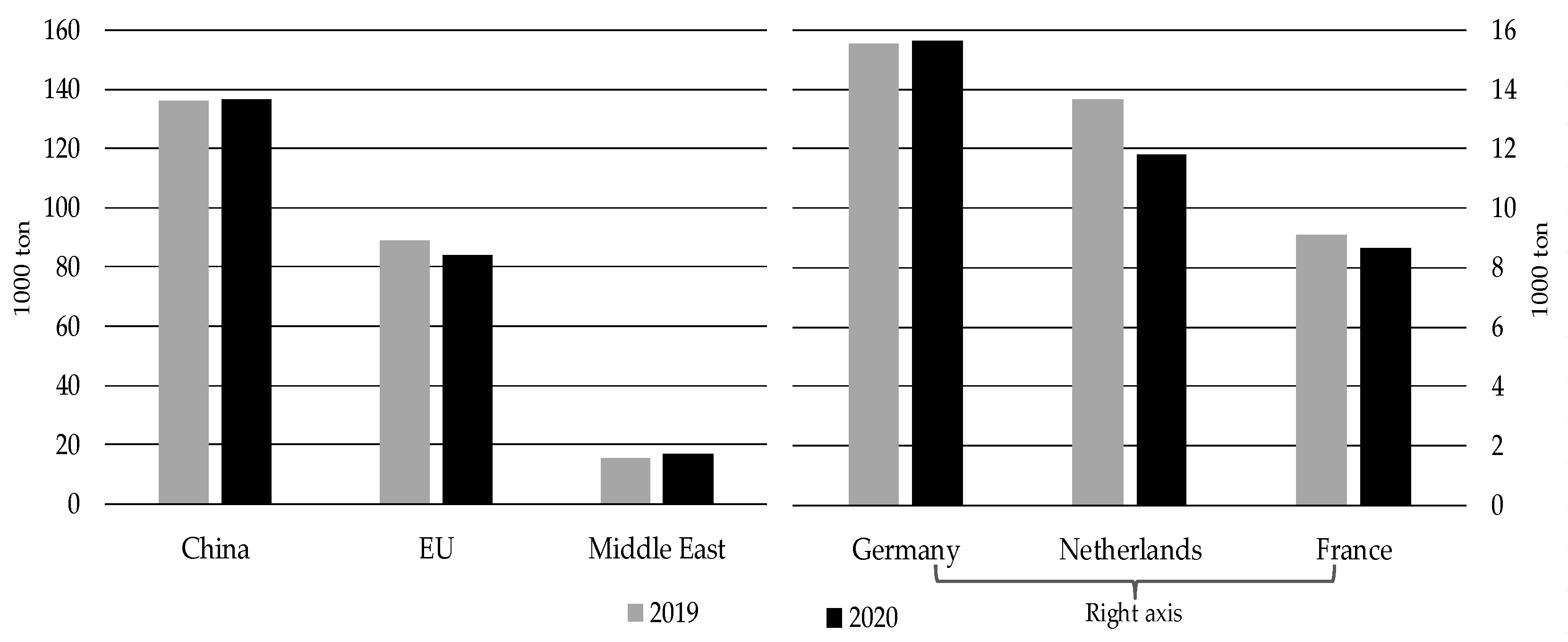

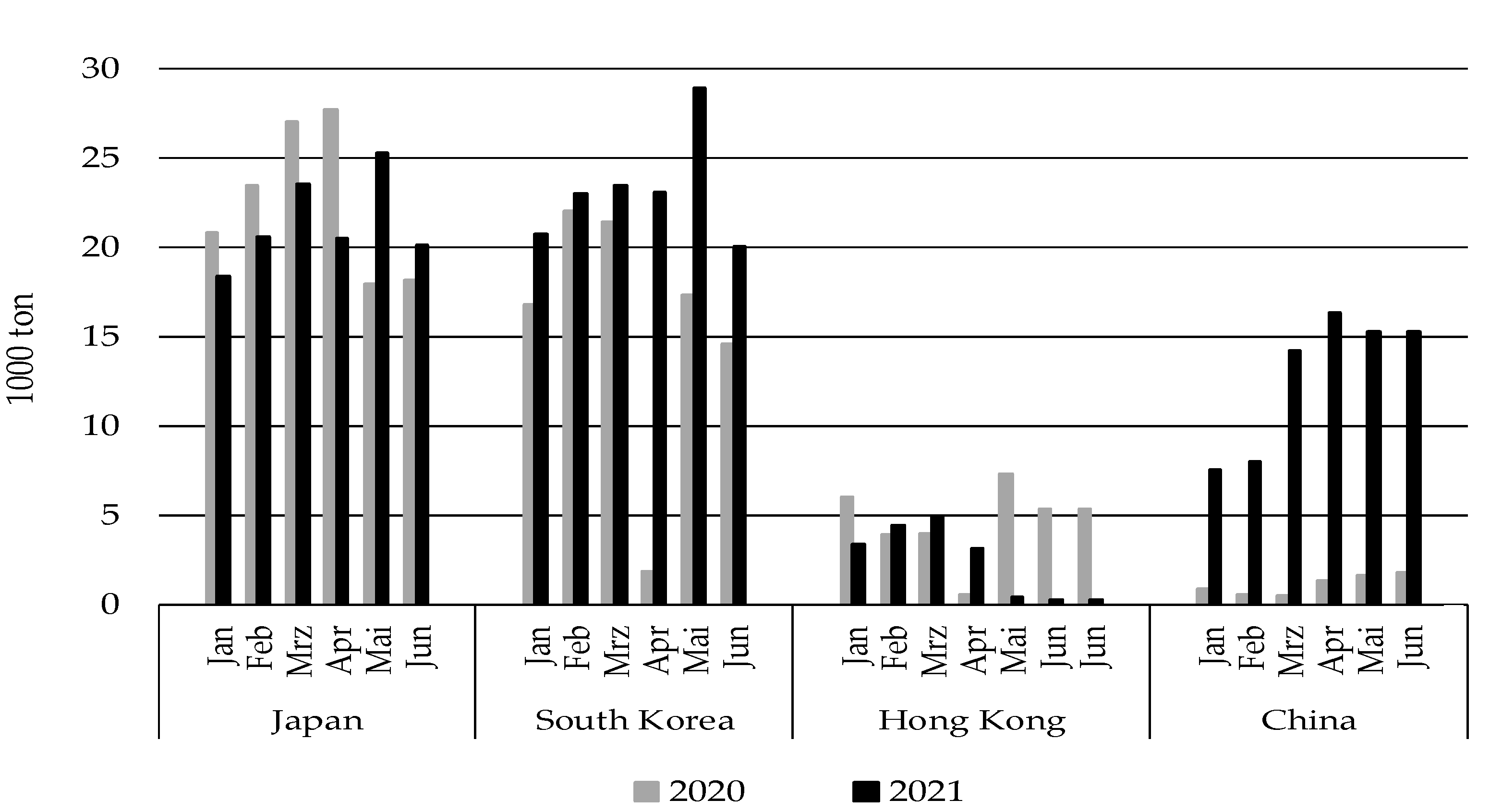

3.1.3. Discussion on International Trade

3.2. COVID-19 and Global Beef and Sheep Meat Processing Plants

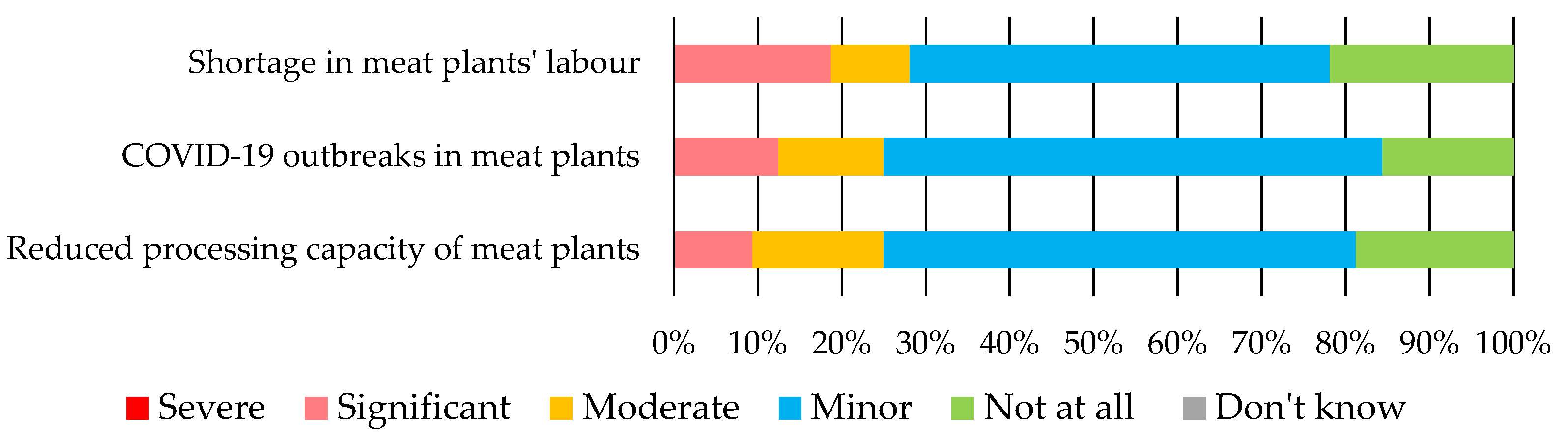

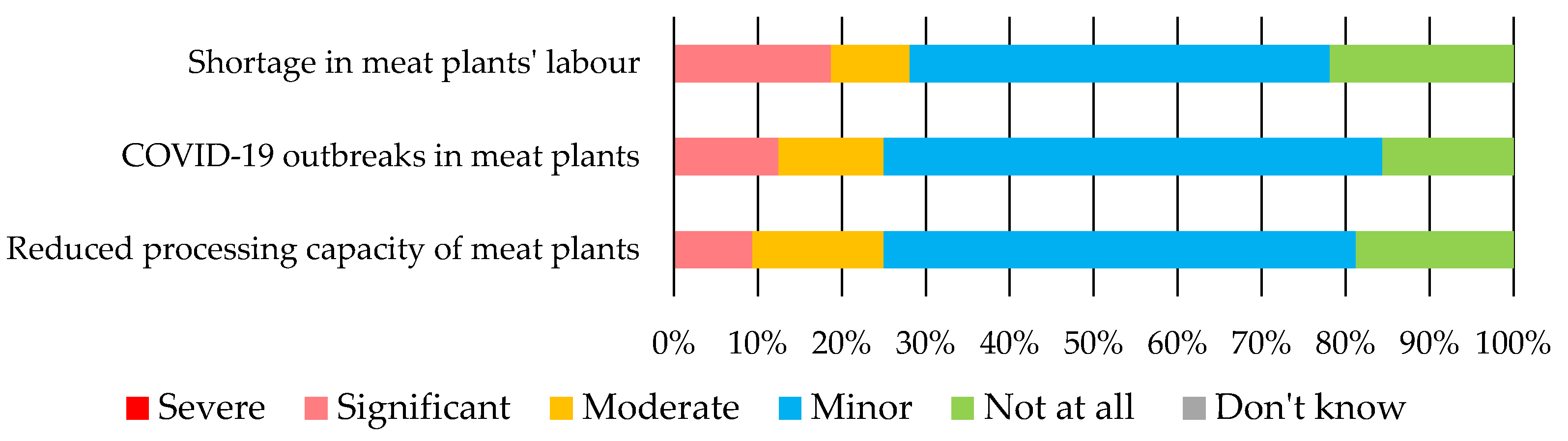

3.2.1. Survey Results on Meat Processing Plants

3.2.2. Discussion on Meat Processing Plants

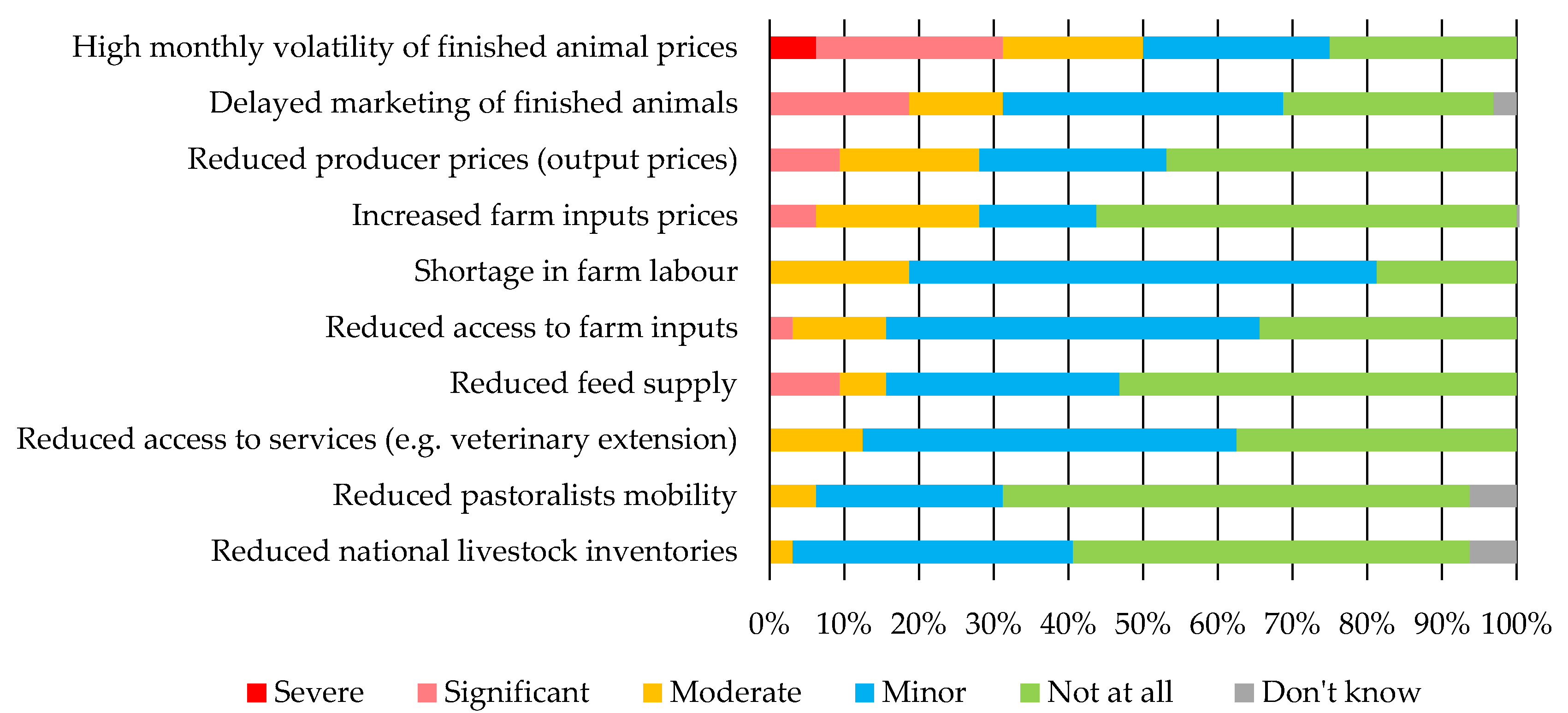

3.3. COVID-19 and Global Beef and Sheep Farming

3.4. Latest Developemnt Issues Infleuencing Global Beef and Sheep Sectors

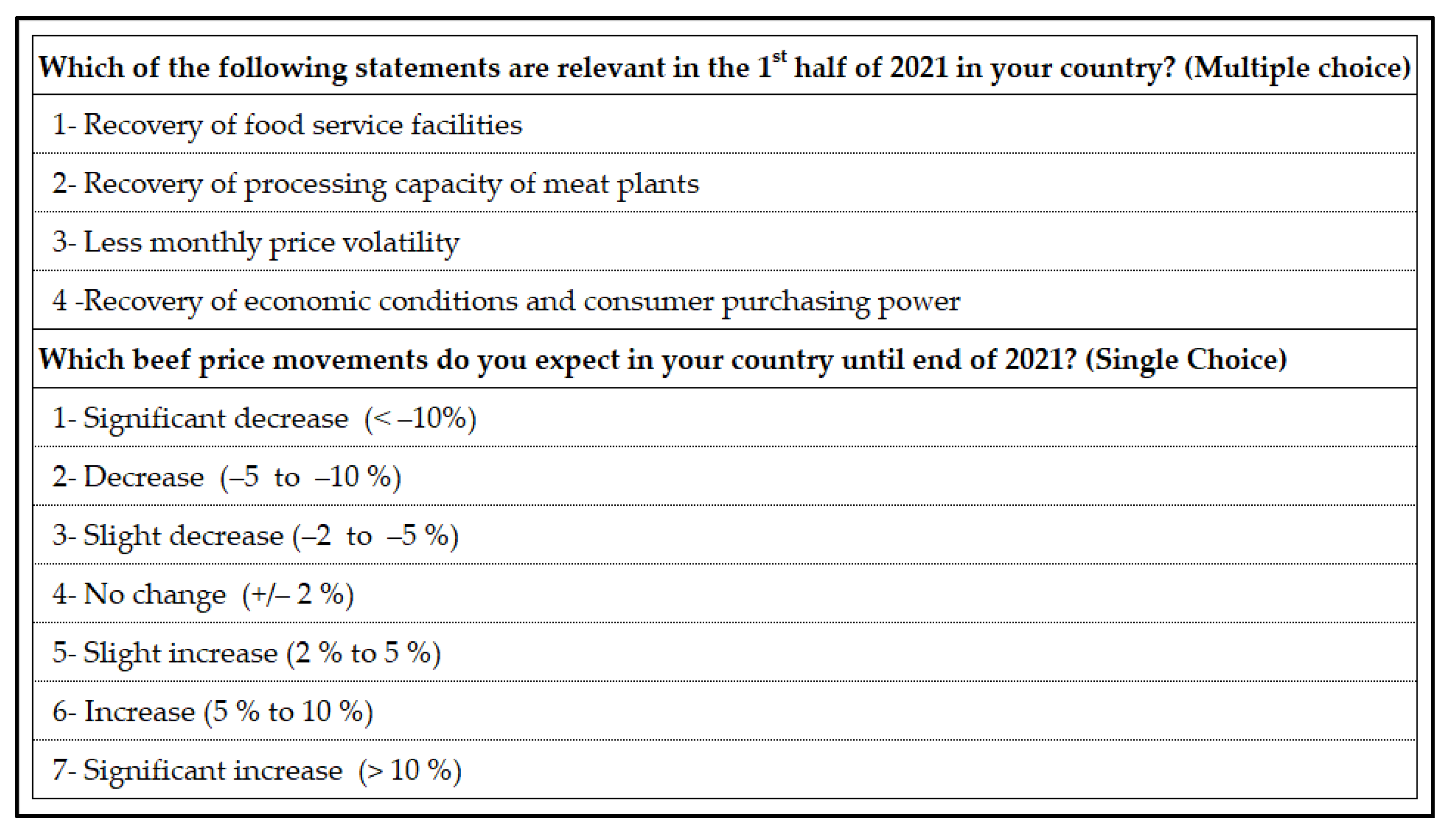

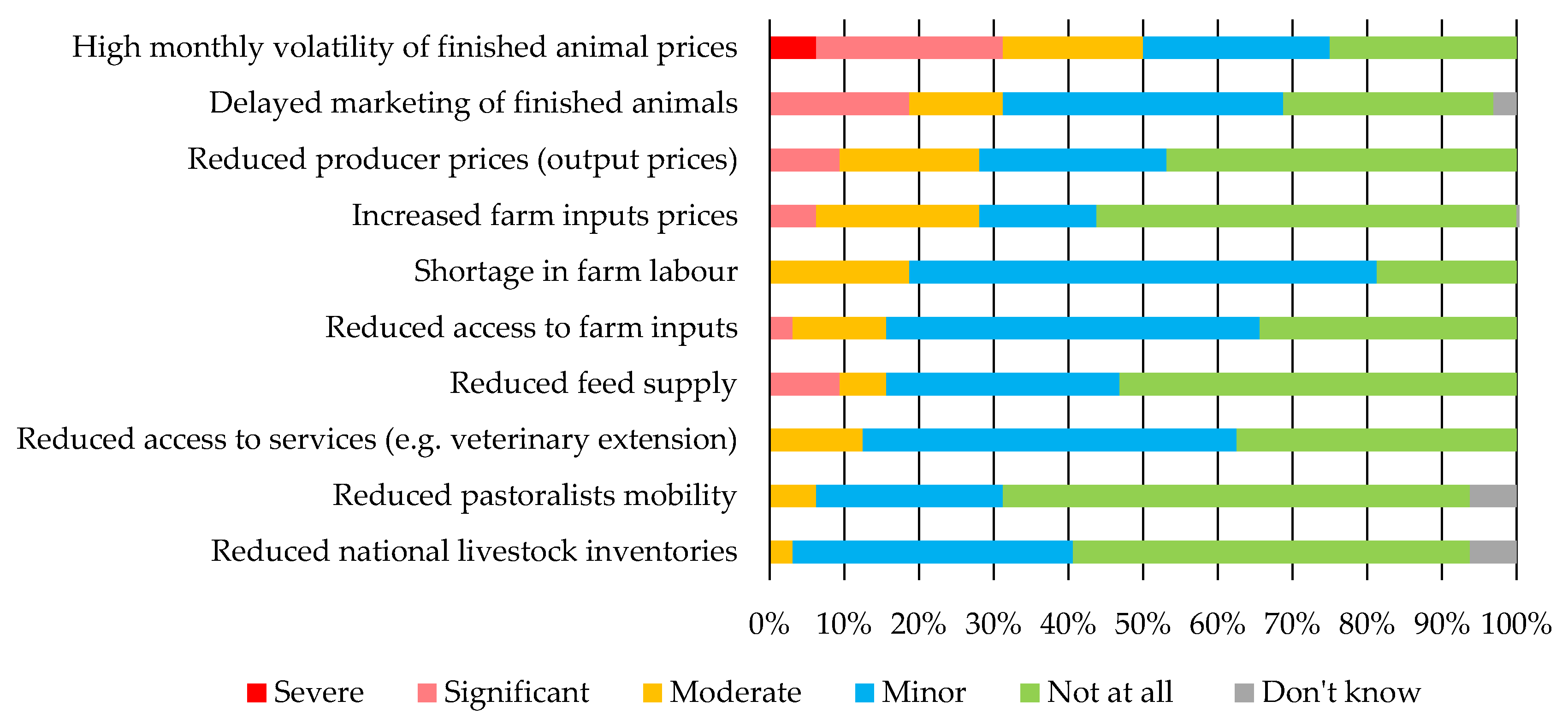

3.4.1. Survey Results on Latest Developments

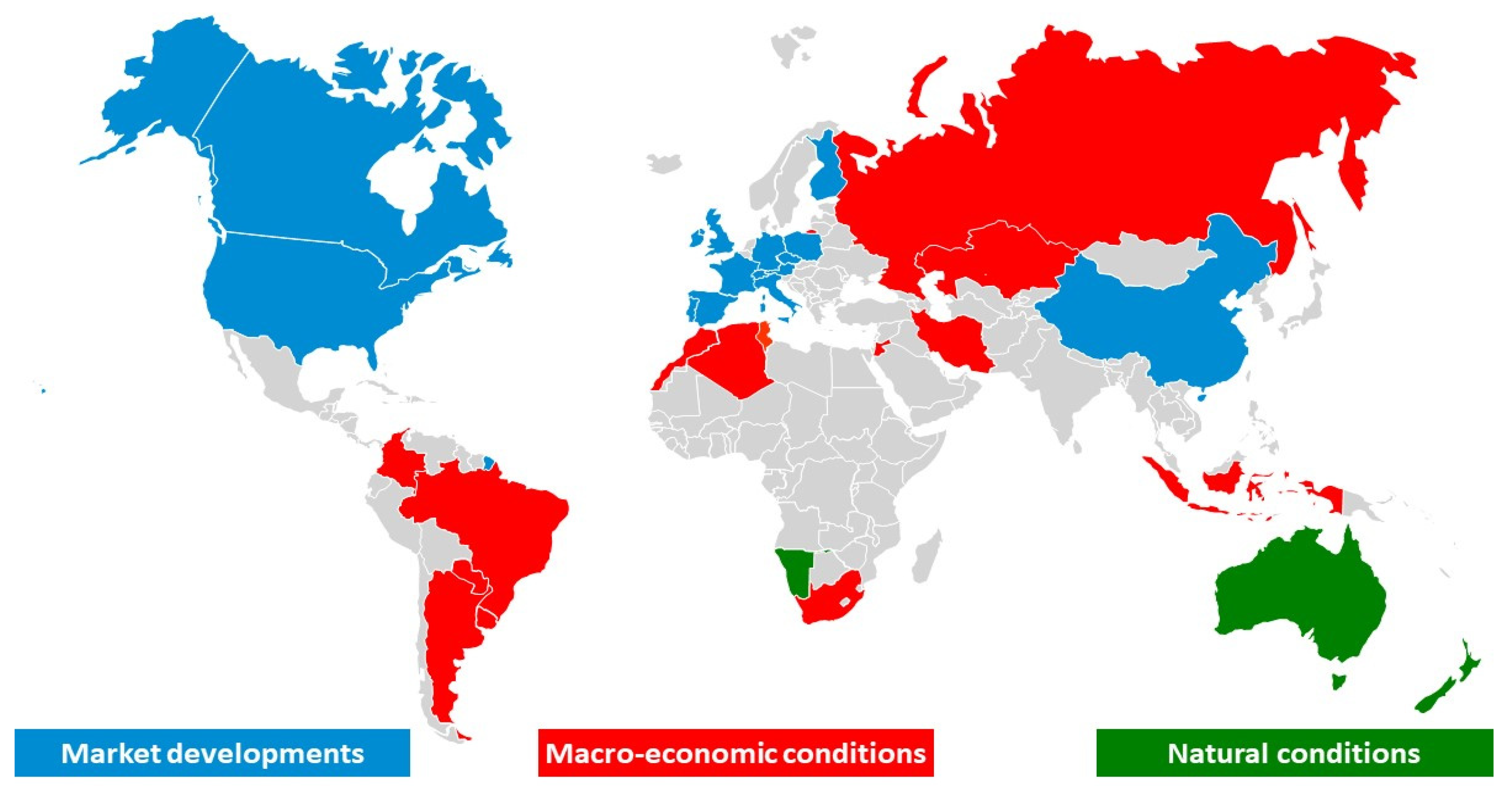

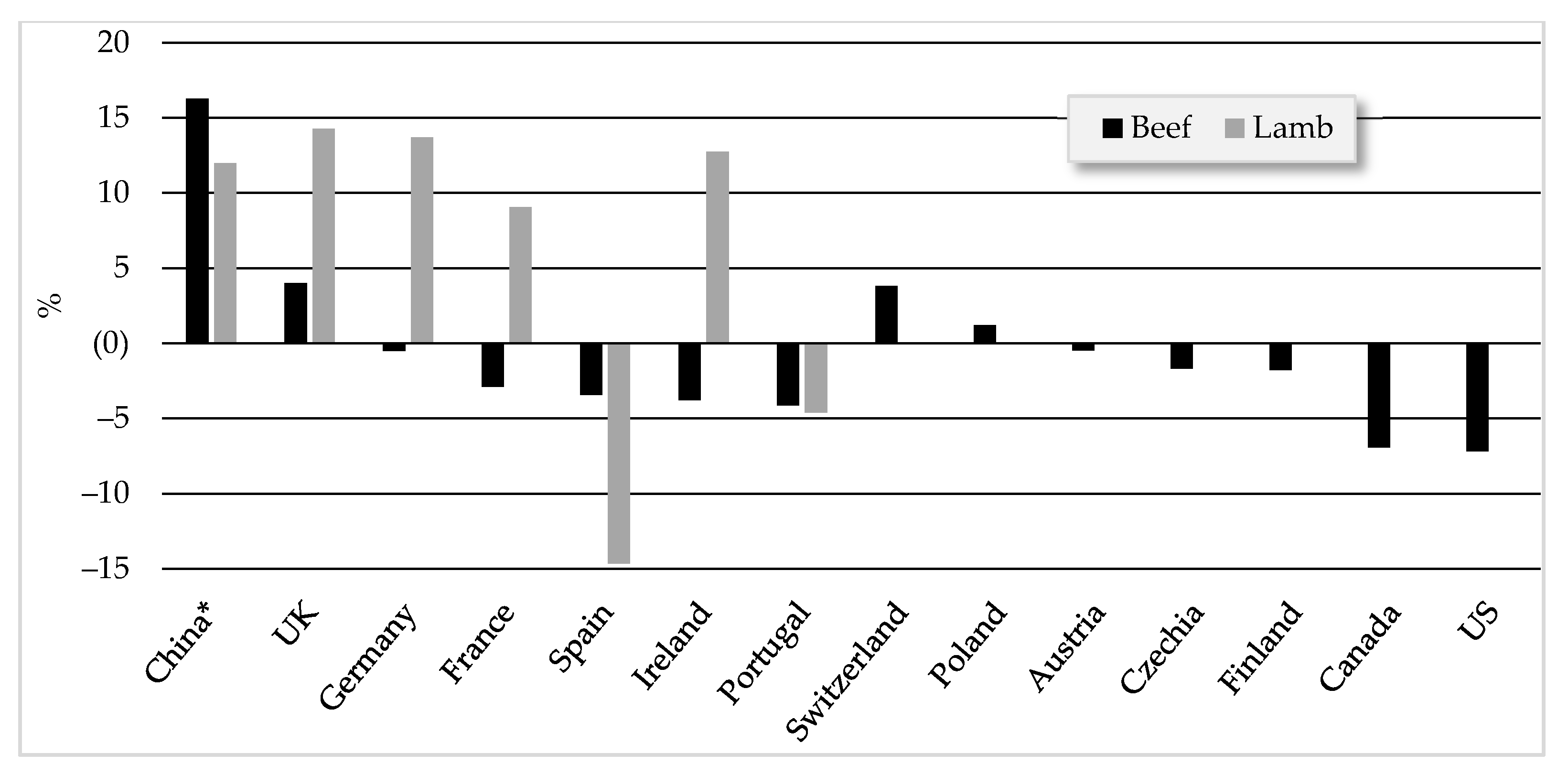

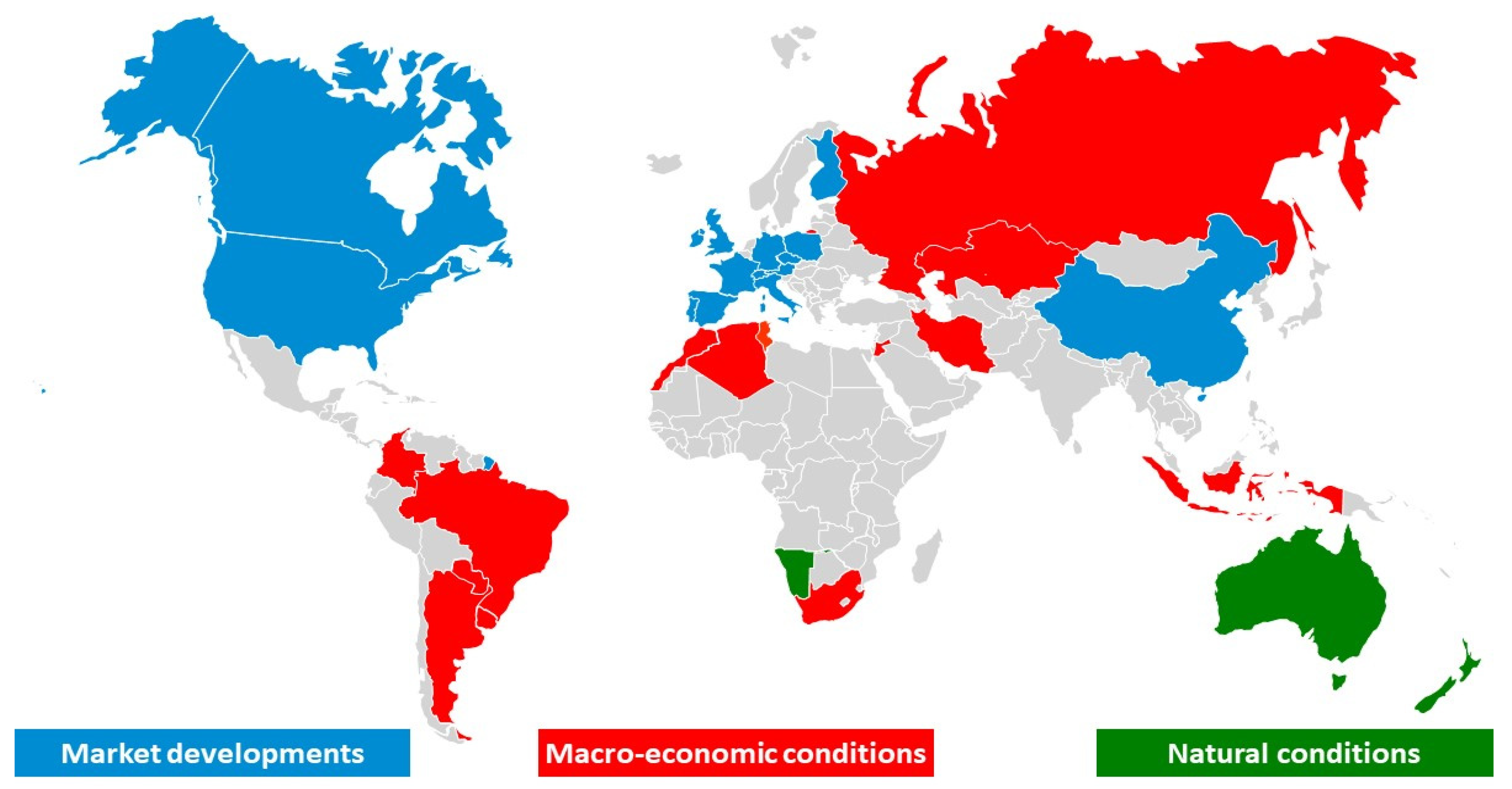

3.4.2. Discussion on Market Developments

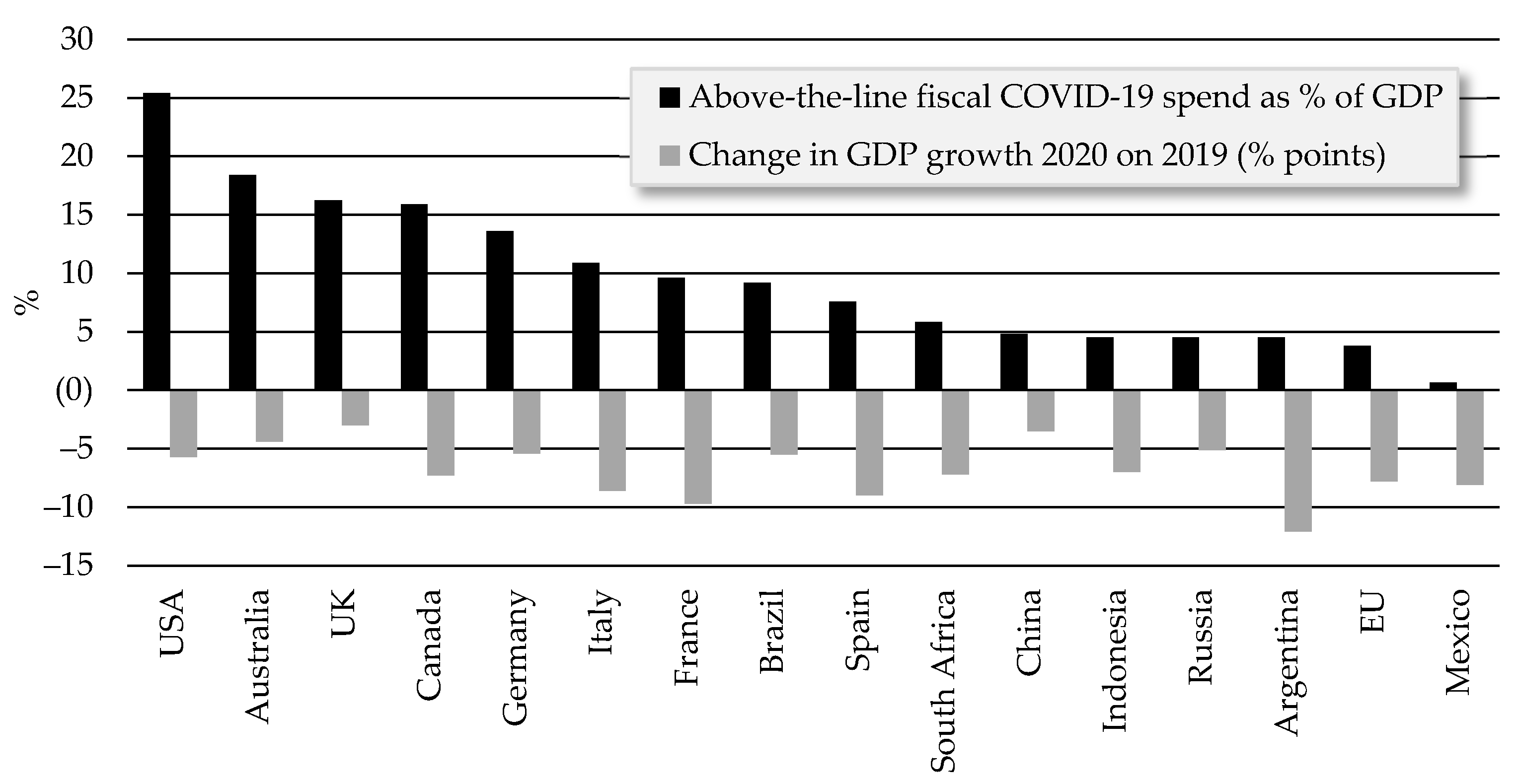

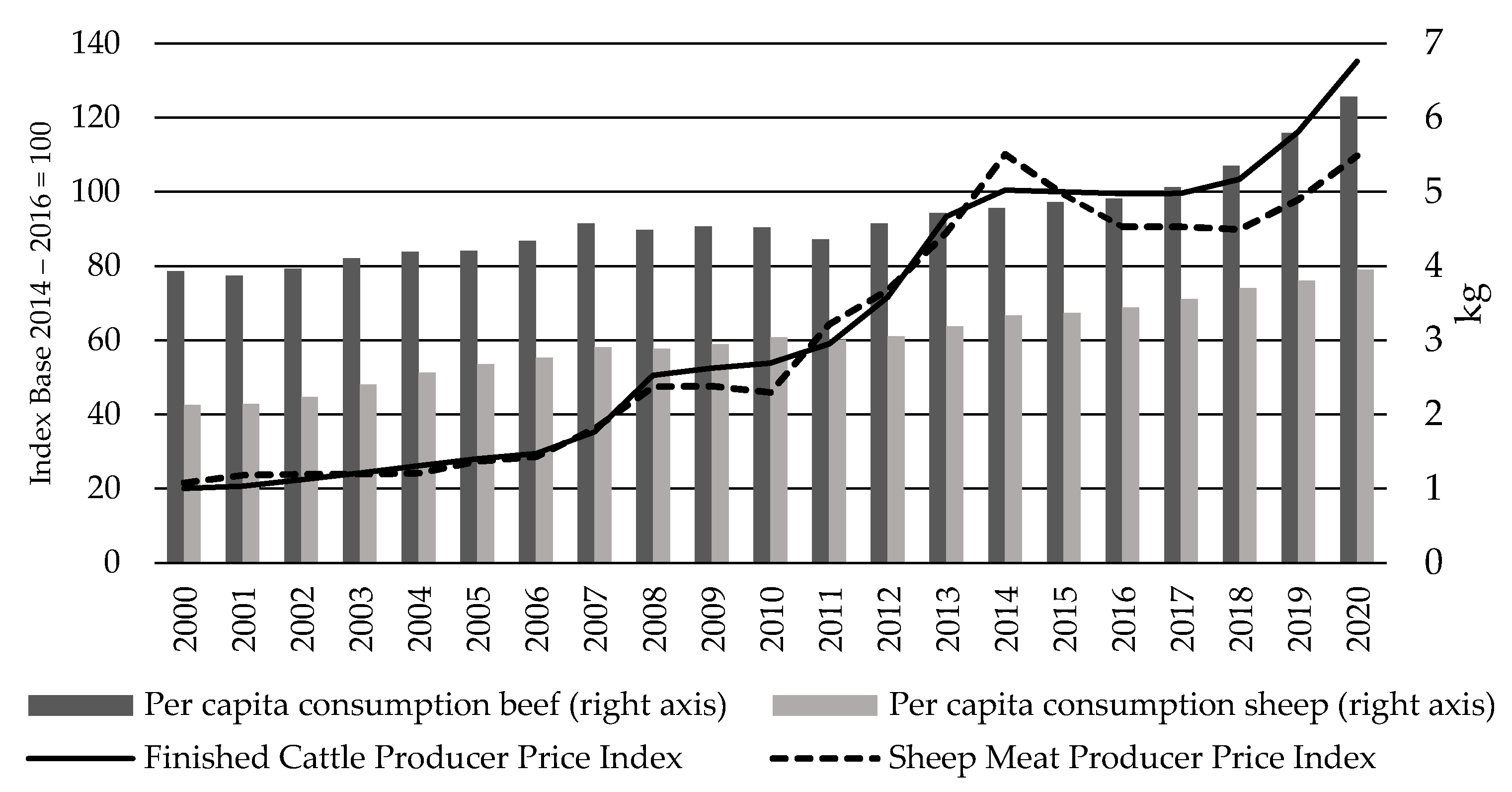

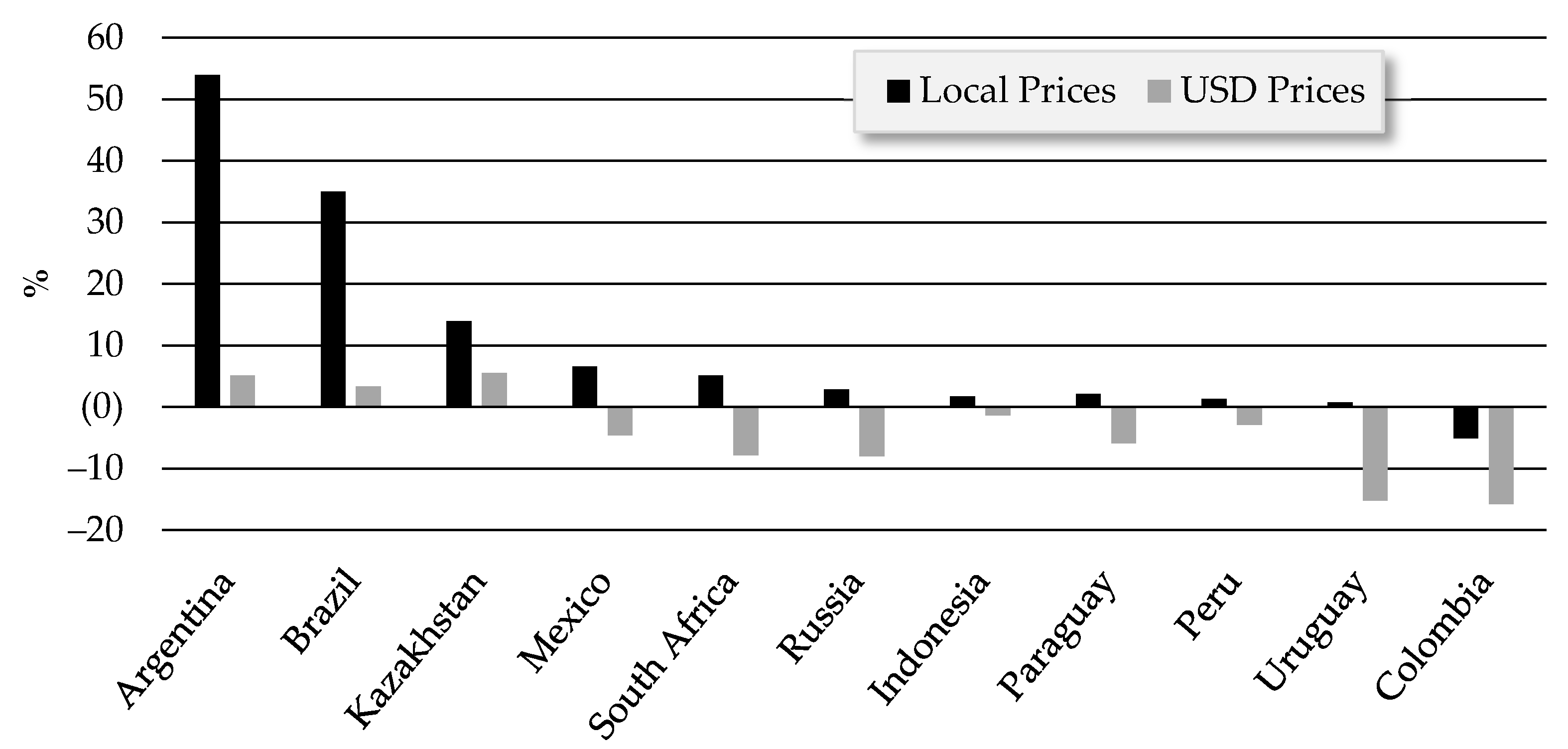

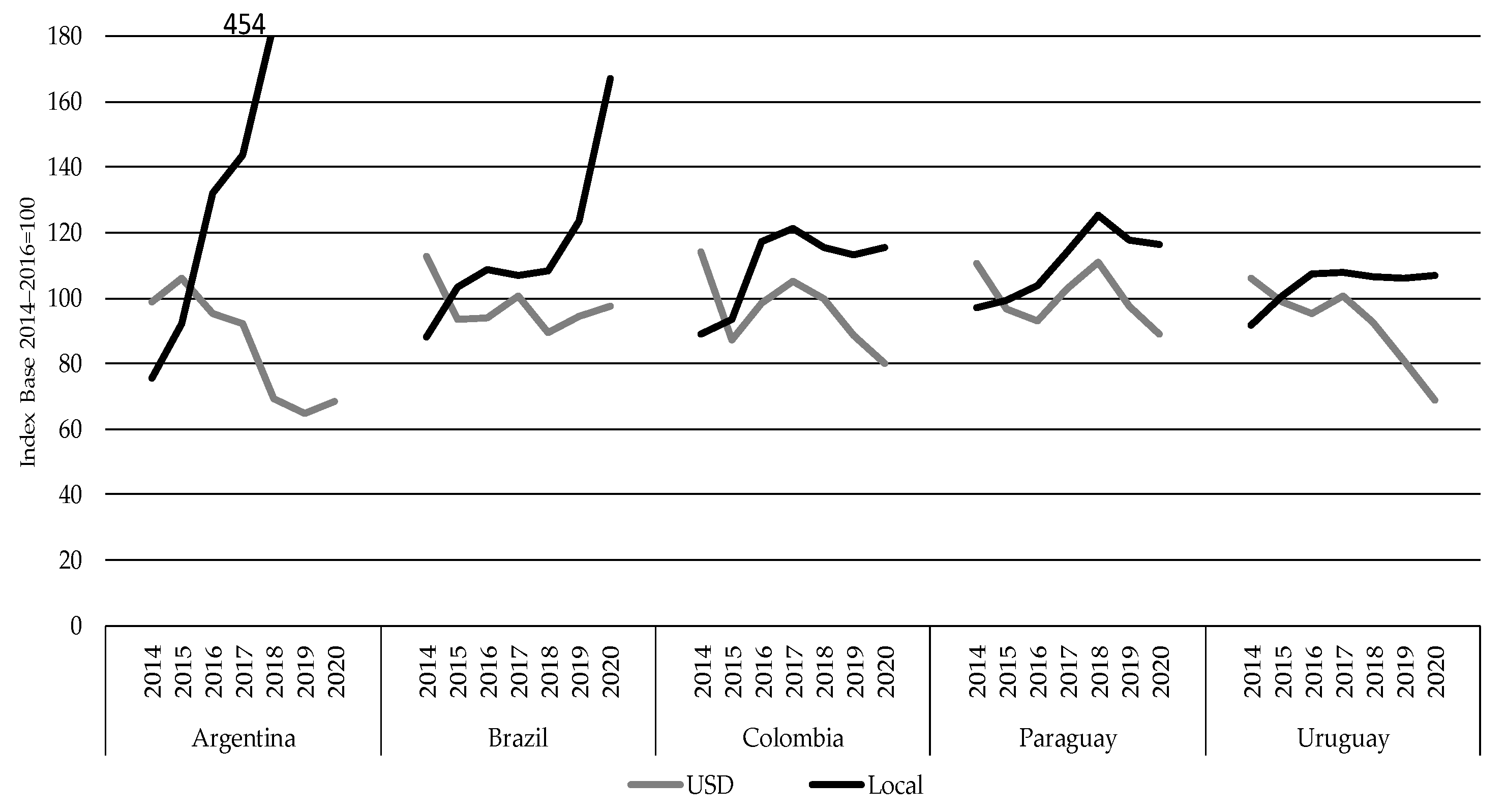

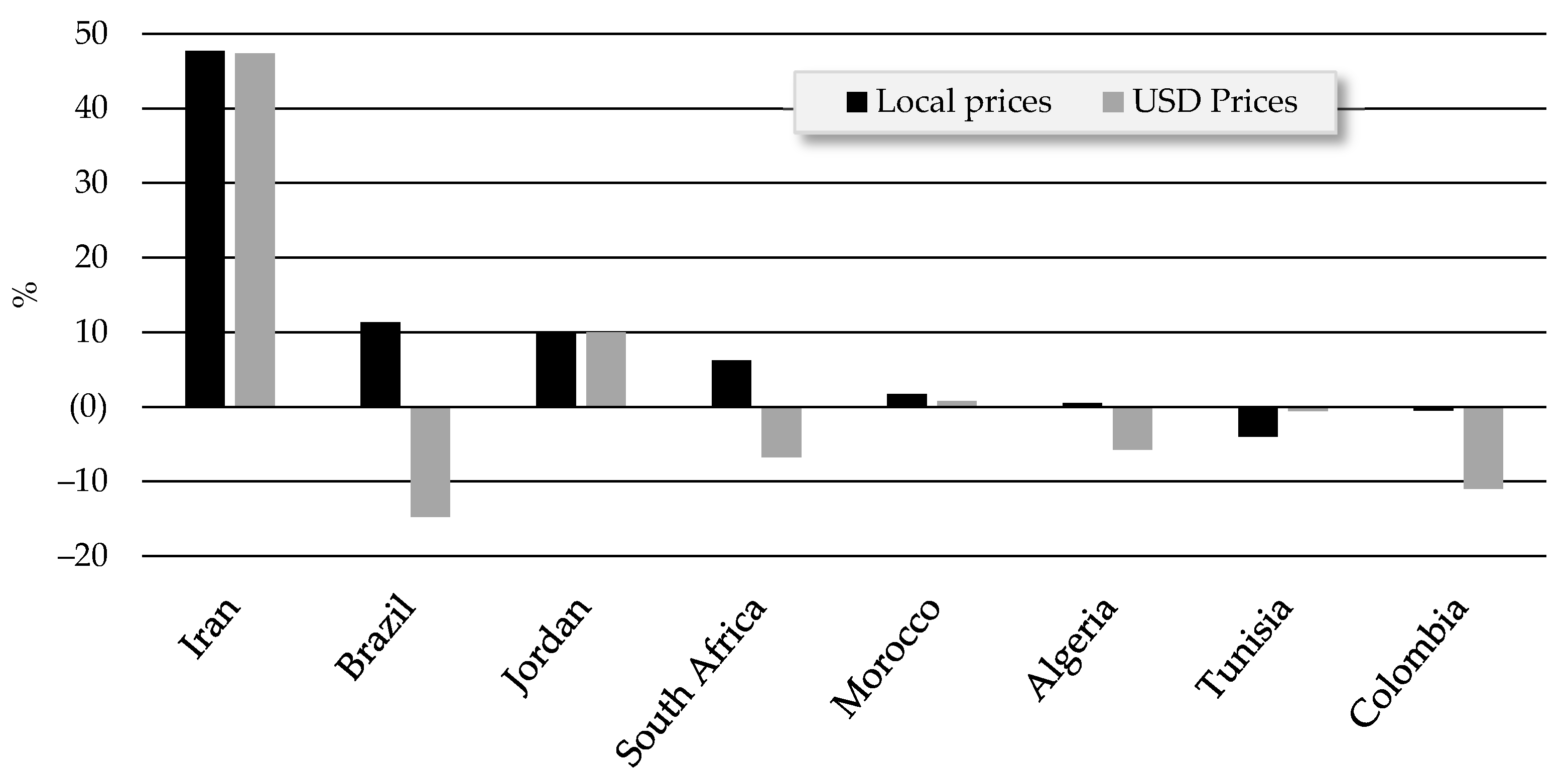

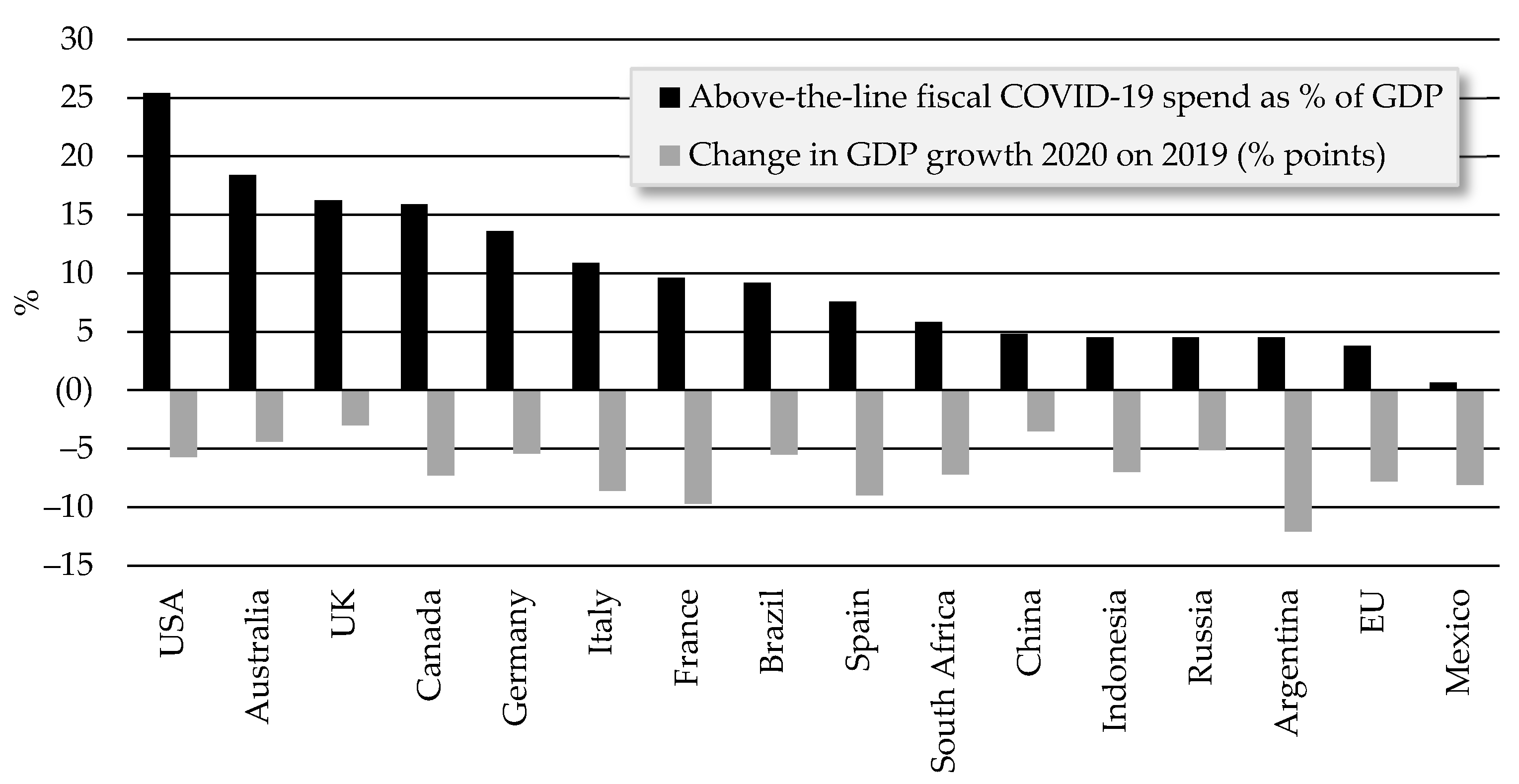

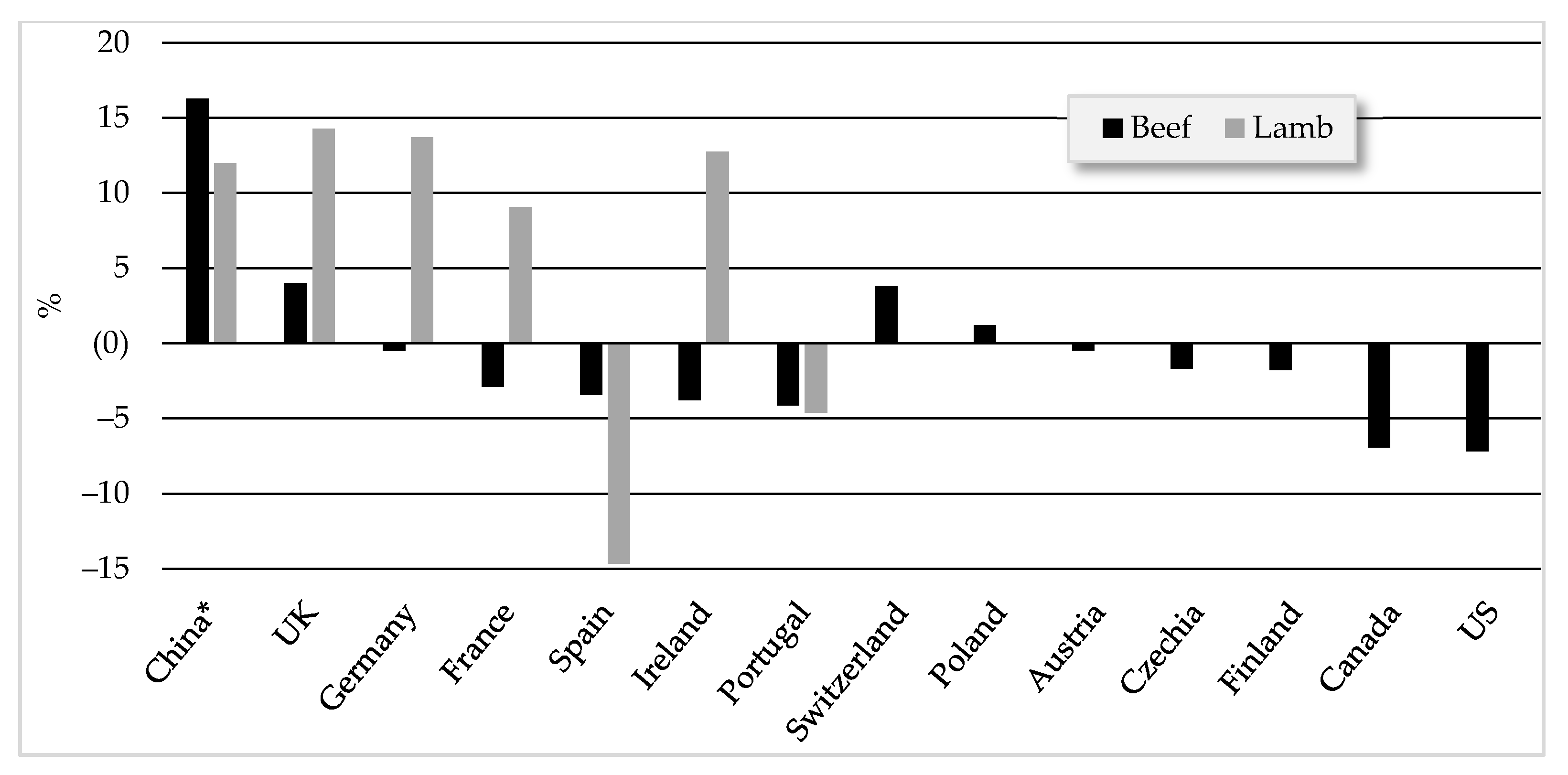

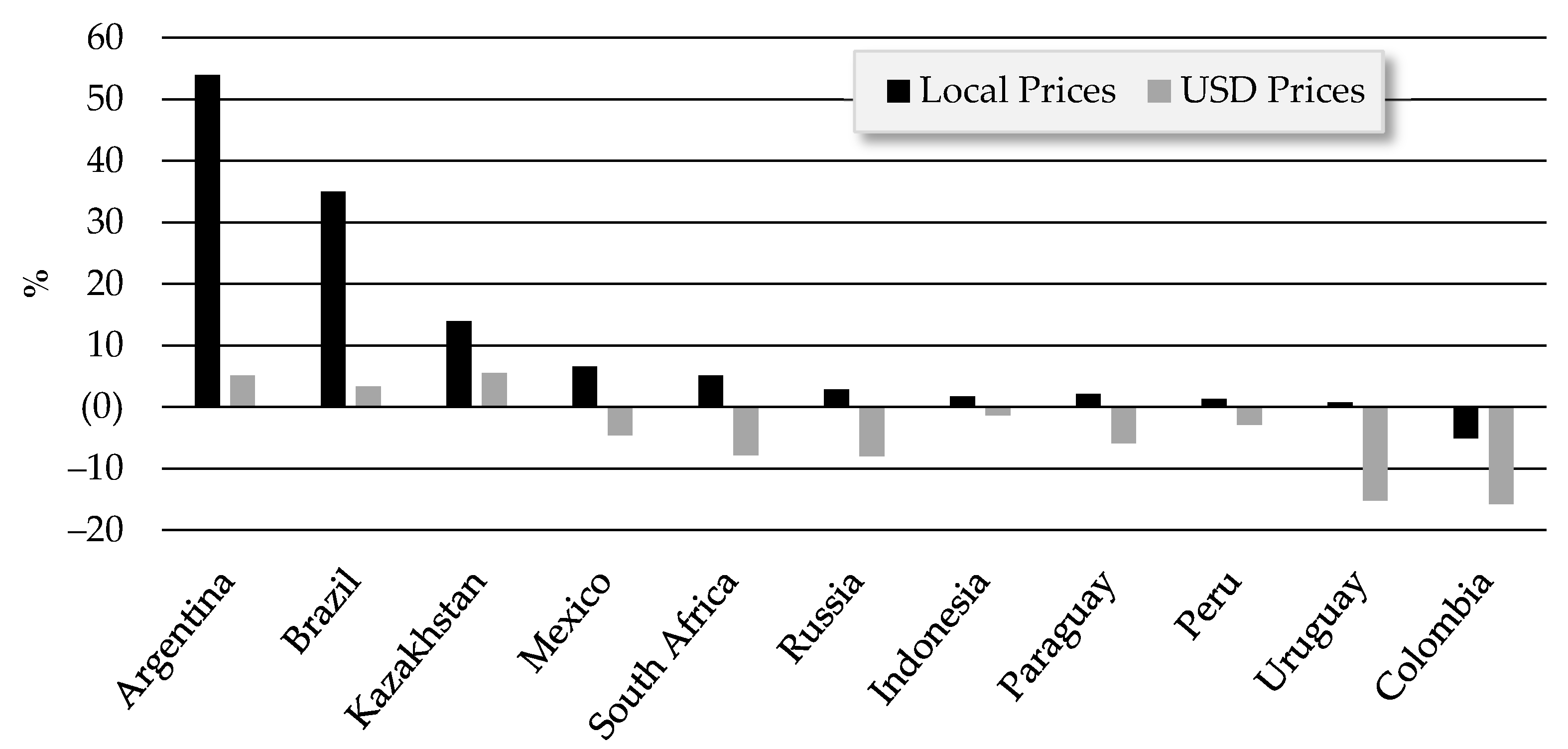

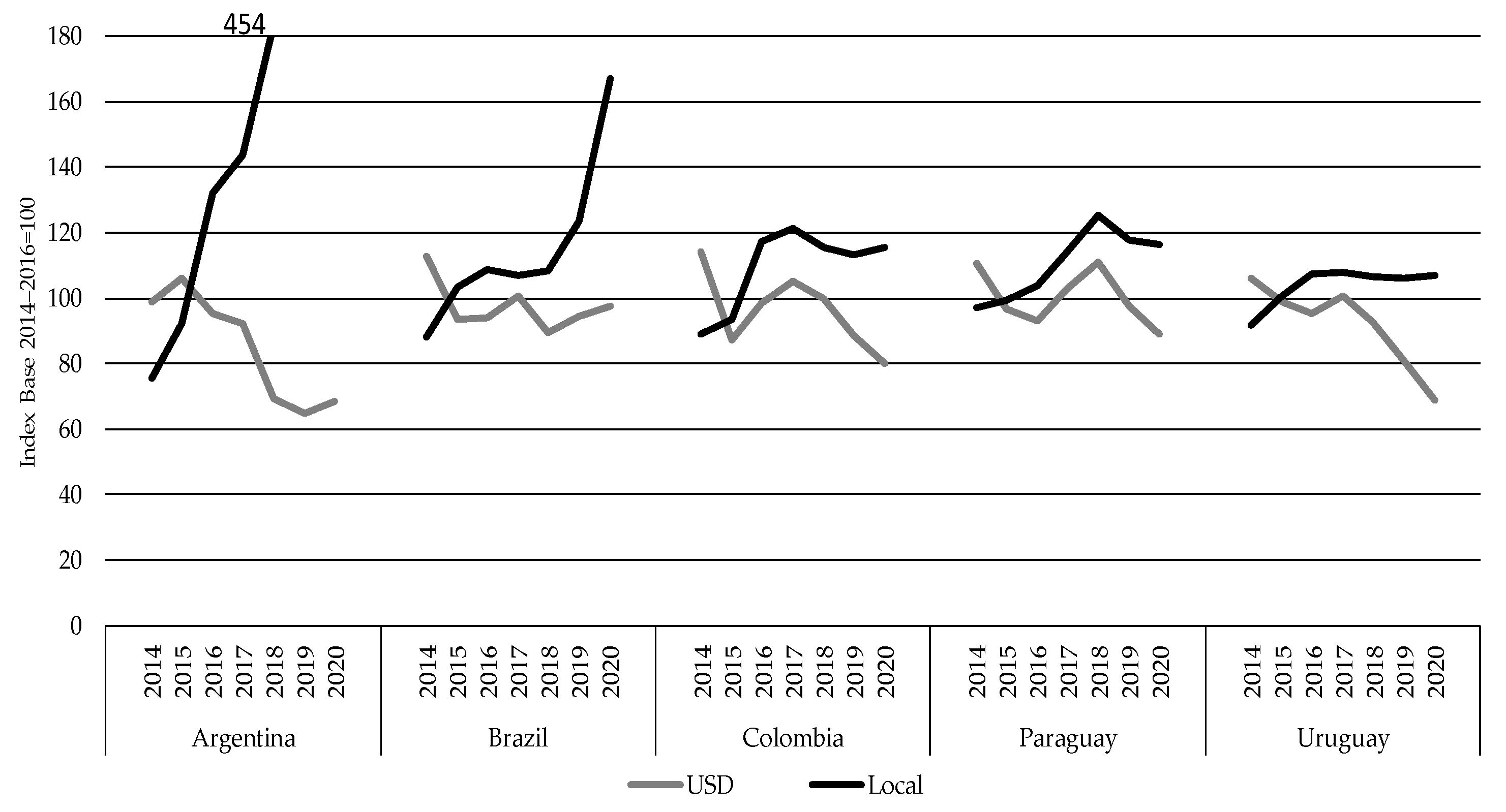

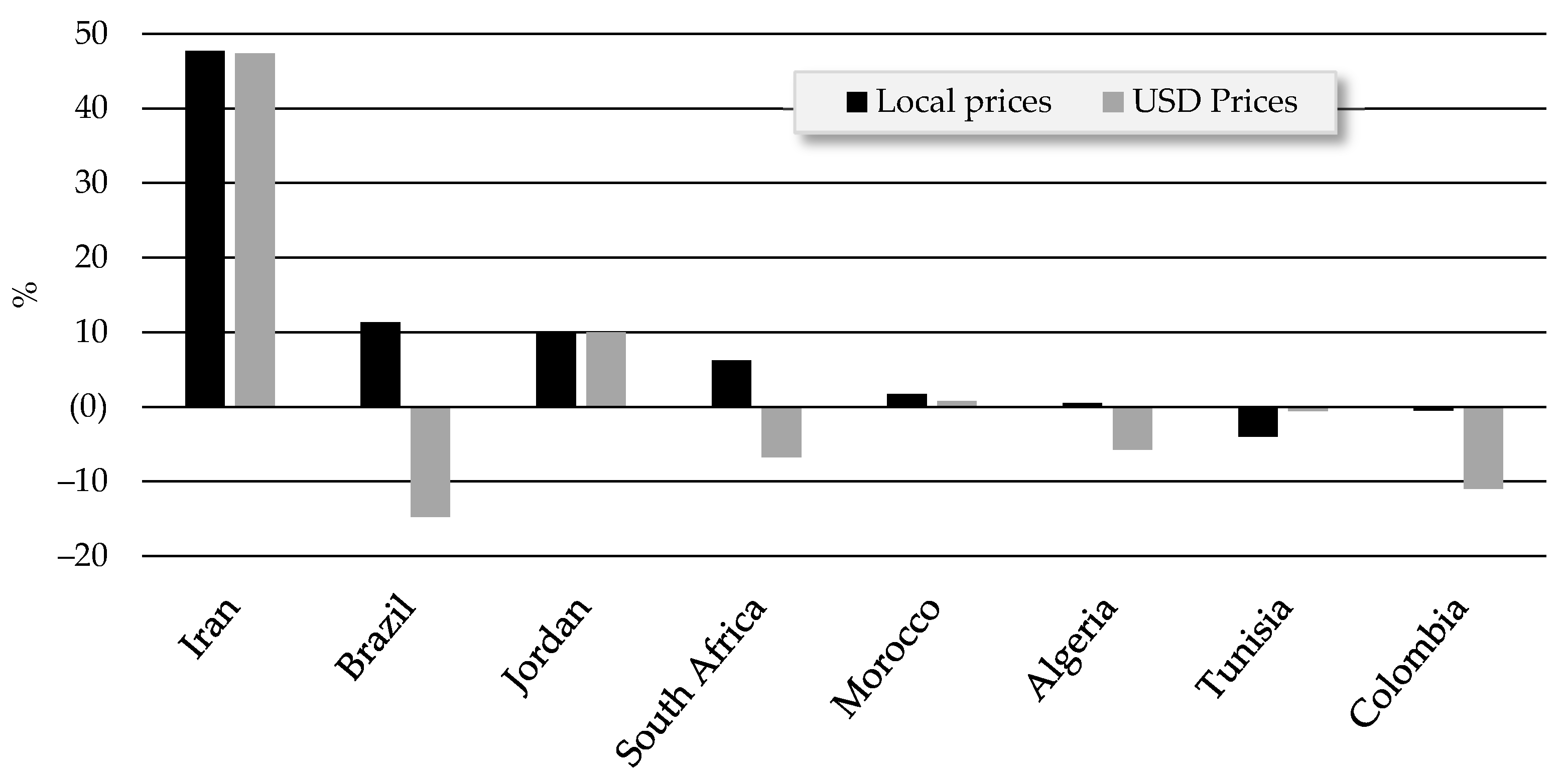

3.4.3. Discussion on Macro-Economic Conditions

- Beef producer countries

- Sheep producer countries:

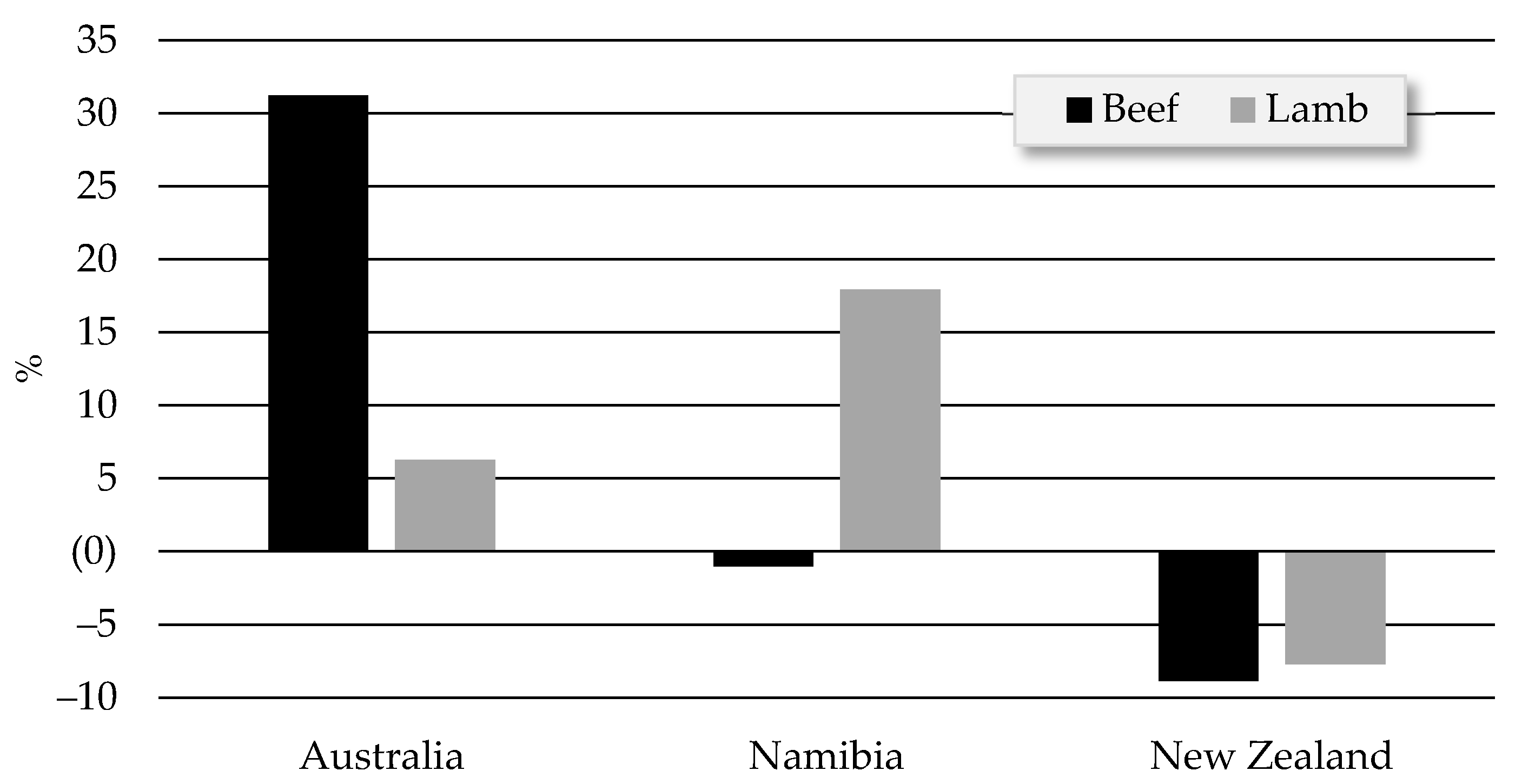

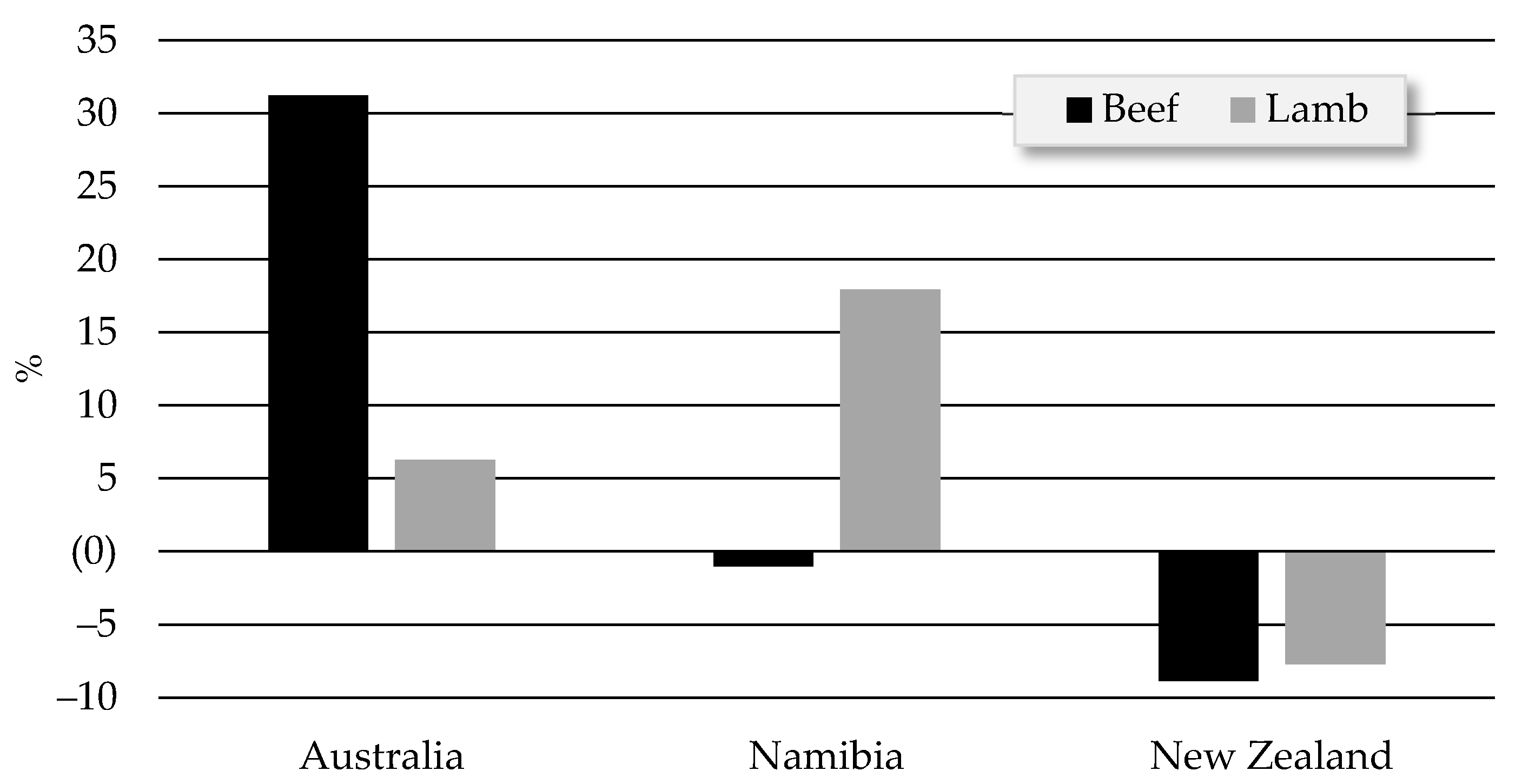

3.4.4. Discussion on Natural Conditions

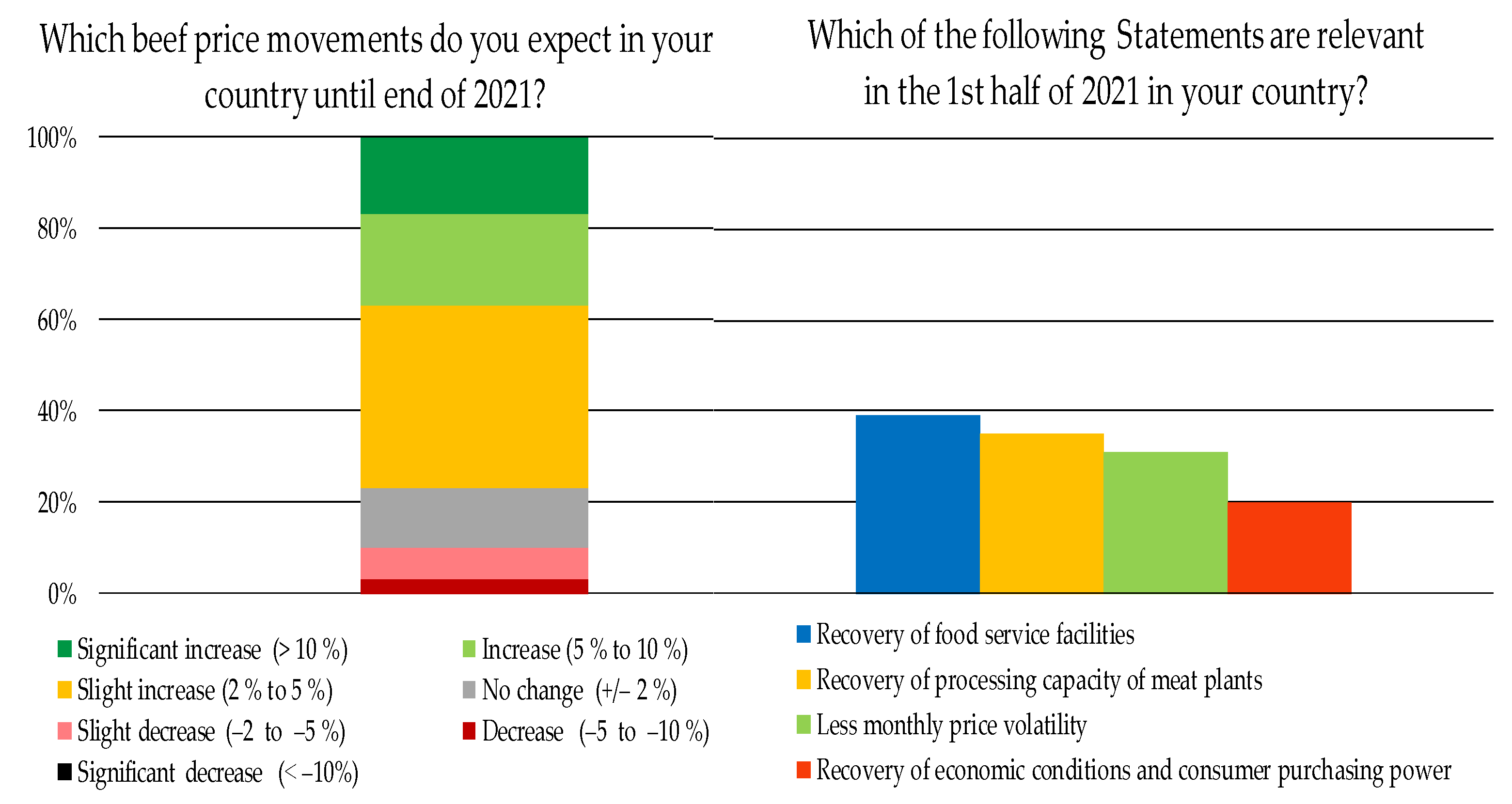

3.5. Potential Developments in 2021

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- Hashem, N.M.; González-Bulnes, A.; Rodriguez-Morales, A.J. Animal welfare and livestock supply chain sustainability under the COVID-19 outbreak: An overview. Front. Vet. Sci. 2020, 7, 679. [Google Scholar] [CrossRef] [PubMed]

- World Bank. Protecting People and Economies: Integrated Policy Responses to COVID-19; World Bank: Washington, DC, USA, 2020; Available online: https://openknowledge.worldbank.org/handle/10986/33770 (accessed on 18 November 2021).

- Allain-Dupré, D.; Chatry, I.; Michalun, V.; Moisio, A. The Territorial Impact of COVID-19: Managing the Crisis across Levels of Government; OECD: Paris, France, 2020; Available online: https://www.oecd.org/coronavirus/policy-responses/the-territorial-impact-of-covid-19-managing-the-crisis-across-levels-of-government-d3e314e1/ (accessed on 19 November 2021).

- Diaz, E.A.; Scudiero, L.; Schneider, F.; Steinfeld, H. GASL Stakeholder Consultation on COVID10 in the Livestock Sector in April–May; Food and Agriculture Organization of the United Nations (FAO): Rome, Italy, 2020; Global Agenda for Sustainable Livestock (GASL); Available online: http://www.livestockdialogue.org/fileadmin/templates/res_livestock/docs/2020_GASL_Global_Consultation_report_COVID-19_Impacts.pdf (accessed on 19 January 2021).

- Organization for Economic Co-operation and Development (OECD). COVID-19 and the Food and Agriculture Sector: Issues and Policy Responses; Policy Brief: Paris, France, 2020; Available online: https://www.oecd.org/coronavirus/policy-responses/covid-19-and-the-food-and-agriculture-sector-issues-and-policy-responses-a23f764b/ (accessed on 5 May 2021).

- Jámbor, A.; Czine, P.; Balogh, P. The impact of the coronavirus on agriculture: First evidence based on global newspaper. Sustainability 2020, 12, 4535. [Google Scholar] [CrossRef]

- Seleiman, M.F.; Selim, S.; Alhammad, B.A.; Alharbi, B.M.; Juliatti, F.C. Will novel coronavirus (Covid-19) pandemic impact agriculture, food security and animal sectors? Biosci. J. 2020, 36, 4. [Google Scholar] [CrossRef]

- Aday, S.; Aday, M.S. Impact of COVID-19 on the food supply chain. Food Qual. Saf. 2020, 4, 167–180. [Google Scholar] [CrossRef]

- Mardones, F.O.; Rich, K.M.; Boden, L.A.; Moreno-Switt, A.I.; Caipo, M.L.; Zimin-Veselkoff, N.; Alateeqi, A.M.; Baltenweck, I. The COVID-19 pandemic and global food security. Front. Vet. Sci. 2020, 7, 928. [Google Scholar] [CrossRef]

- Beckman, J.; Baquedano, F.; Countryman, A. The impacts of COVID-19 on GDP, food prices, and food security. Q Open 2021, 1, qoab005. [Google Scholar] [CrossRef]

- FAO. Impact of COVID-19 on Agriculture, Food Systems and Rural Livelihoods in Eastern Africa: Policy and Programmatic Options; FAO Subregional Office for Eastern Africa (SFE): Addis Ababa, Ethiopia, 2020. [Google Scholar] [CrossRef]

- Éliás, B.A.; Jámbor, A. Food Security and COVID-19: A Systematic Review of the First-Year Experience. Sustainability 2021, 13, 5294. [Google Scholar] [CrossRef]

- Gilmour, B.; Lin, T.; Lee, S. COVID-19 Pandemic Implications on Agriculture and Food Consumption, Production and Trade in ASEAN Member States; Asia Pacific Foundation of Canada: Vancouver, BC, Canada, 2021; Available online: https://www.asiapacific.ca/sites/default/files/publication-pdf/COVID-19%20Pandemic%20Implications%20on%20Agriculture%20and%20Food%20Consumption%2C%20Prod....pdf (accessed on 14 July 2021).

- Weersink, A.; von Massow, M.; Bannon, N.; Ifft, J.; Maples, J.; McEwan, K.; McKendree, M.G.S.; Nicholson, C.; Novakovic, A.; Rangarajan, A.; et al. COVID-19 and the agri-food system in the United States and Canada. Agric. Syst. 2021, 188, 103039. [Google Scholar] [CrossRef]

- Oyeagu, C.E.; Ezeuko, A.S.; Lewu, F.B.; Akuru, E.A.; Ogwuegbu, M.C.; Osita, C.O.; Ani, A.O.; Mlambo, V. The impact of Covid-19 on the livestock industry and the way forward. Adv. Anim. Vet. Sci. 2021, 9, 941–955. [Google Scholar] [CrossRef]

- Ijaz, M.; Yar, M.K.; Badar, I.H.; Ali, S.; Islam, M.; Jaspal, M.H.; Hayat, Z.; Sardar, A.; Ullah, S.; Guevara-Ruiz, D. Meat production and supply chain under COVID-19 scenario: Current trends and future prospects. Front. Vet. Sci. 2021, 8, 432. [Google Scholar] [CrossRef]

- Abu Hatab, A.; Krautscheid, L.; Boqvist, S. COVID-19, Livestock Systems and Food Security in Developing Countries: A Systematic Review of an Emerging Literature. Pathogens 2021, 10, 586. [Google Scholar] [CrossRef] [PubMed]

- Mercy Corps. COVID-19 and Livestock Market Systems: The Impact of COVID-19 on Livestock-Based Economies in the Horn of Africa; Mercy Corps: Portland, OR, USA, 2020; Available online: https://www.mercycorps.org/sites/default/files/2020-08/MC-HoA-COVID-Impact-Livestock-Mrkts-Aug-2020.pdf (accessed on 2 April 2021).

- Aariözkan, S.; Akçay, A.; Küçükoflaz, M.; Güngör, G. The short-term impact of the Covid-19 pandemic on livestock products and feed prices in Turkey. Ank. Üniversitesi Vet. Fakültesi Derg 2021, 68, 337–342. [Google Scholar] [CrossRef]

- Marchant-Forde, J.N.; Boyle, L.A. COVID-19 effects on livestock production: A One Welfare issue. Front. Vet. Sci. 2020, 7, 734. [Google Scholar] [CrossRef]

- Sartin, J.L. COVID-19 and How it Affects the World of Livestock. Anim. Front. 2021, 11, 71. [Google Scholar] [CrossRef]

- Patrice, T.; Lamboni, D. COVID-19 and the Beef Supply Chain: An Overview; Statistics Canada: Ottawa, ON, Canada, 2020; Available online: https://www150.statcan.gc.ca/n1/en/catalogue/45280001 (accessed on 5 July 2021).

- Rude, J. COVID-19 and the Canadian cattle/beef sector: Some preliminary analysis. Can. J. Agric. Econ. 2020, 68, 207–213. [Google Scholar] [CrossRef]

- Fleming, O.M. Modeling the US Beef Industry’s Response to COVID-19. Undergrad. Econ. Rev. 2020, 17, 14. Available online: https://digitalcommons.iwu.edu/uer/vol17/iss1/14 (accessed on 5 July 2021).

- Peel, D.S.; Aherin, D.; Blach, R.; Burdine, K.; Close, D.; Hagerman, A.; Maples, J.; Robb, J.; Tonsor, G. Economic Damages to the US Beef Cattle Industry Due to COVID-19; Oklahoma Cooperative Extension Service: Oklahoma City, OK, USA, 2020; Available online: https://extension.okstate.edu/fact-sheets/economic-damages-to-the-u-s-beef-cattle-industry-due-to-covid-19.html (accessed on 5 July 2021).

- Vidaurreta, I.; de la Fe, C.; Orengo, J.; Gómez-Martín, Á.; Benito, B. Short-term economic impact of COVID-19 on Spanish small ruminant flocks. Animals 2020, 10, 1357. [Google Scholar] [CrossRef]

- Meuwissen, M.P.M.; Feindt, P.H.; Slijper, T.; Spiegel, A.; Finger, R.; de Mey, Y.; Paas, W.; Termeer, K.J.A.M.; Poortvliet, P.M.; Peneva, M.; et al. Impact of Covid-19 on farming systems in Europe through the lens of resilience thinking. Agric. Syst. 2021, 191, 103–152. [Google Scholar] [CrossRef]

- Balagtas, J.; Cooper, J. The Impact of COVID-19 on United States Meat and Livestock Markets; U.S. Department of Agriculture, Office of the Chief Economist: Washington, DC, USA, 2021. Available online: https://www.usda.gov/sites/default/files/documents/covid-impact-livestock-markets.pdf (accessed on 5 July 2021).

- Martinez, C.C.; Maples, J.G.; Benavidez, J. Beef cattle markets and COVID-19. Appl. Econ. Perspect. Policy 2021, 43, 304–314. [Google Scholar] [CrossRef]

- Mallory, M.L. Impact of COVID-19 on medium-term export prospects for soybeans, corn, beef, pork, and poultry. Appl. Econ. Perspect. Policy 2021, 43, 292–303. [Google Scholar] [CrossRef]

- Ramsey, A.F.; Goodwin, B.K.; Hahn, W.F.; Holt, M.T. Impacts of COVID-19 and price transmission in US meat markets. Agric. Econ. 2021, 52, 441–458. [Google Scholar] [CrossRef] [PubMed]

- OECD/FAO. OECD-FAO Agricultural Outlook 2020-2029; FAO: Rome, Italy; OECD Publishing: Paris, France, 2020. [Google Scholar] [CrossRef]

- Almadani, M.I.; Weeks, P.; Deblitz, C. Introducing the World’s First Global Producer Price Indices for Beef Cattle and Sheep. Animals 2021, 11, 2314. [Google Scholar] [CrossRef] [PubMed]

- Peel, D. Beef supply chains and the impact of the COVID-19 pandemic in the United States. Anim. Front. 2021, 11, 33–38. [Google Scholar] [CrossRef] [PubMed]

- FAO. Guidelines to Mitigate the Impact of the COVID-19 Pandemic on Livestock Production and Animal Health; FAO: Rome, Italy, 2020; Available online: http://www.fao.org/in-action/kore/publications/publications-details/en/c/1277631/ (accessed on 12 November 2020).

- Chibanda, C.; Agethen, K.; Deblitz, C.; Zimmer, Y.; Almadani, M.I.; Garming, H.; Rohlmann, C.; Schütte, J.; Thobe, P.; Verhaagh, M.; et al. The typical farm approach and its application by the Agri Benchmark network. Agriculture 2020, 10, 646. [Google Scholar] [CrossRef]

- Agethen, K.; Weeks, P. Climate Change Adaptation Strategies in Beef and Sheep Production; Thünen Institute of Farm Economics: Braunschweig, Germany, 2020; Available online: http://www.agribenchmark.org/agri-benchmark/news-and-results/einzelansicht/artikel//climate-chan-1.html (accessed on 12 November 2020).

- Hobbs, J.E. Food supply chains during the COVID-19 pandemic. Can. J. Agric. Econ. 2020, 68, 171–176. [Google Scholar] [CrossRef] [Green Version]

- Malhotra, S.; Chhibber-Goel, J.; Krishnan, N.M.A.; Sharma, A. The profiles of first and second SARS-CoV-2 waves in the top ten COVID-19 affected countries. J. Glob. Health Rep. 2021, 5, e2021082. [Google Scholar] [CrossRef]

- Tonsor, G.T.; Lusk, J.L.; Tonsor, S.L. Meat Demand Monitor during COVID-19. Animals 2021, 11, 1040. [Google Scholar] [CrossRef] [PubMed]

- USDA. Meat Supply and Disappearance; U.S. Department of Agriculture, Economic Research Service, Livestock & Meat Domestic Data: Washington, DC, USA, 2021. Available online: https://www.ers.usda.gov/webdocs/DataFiles/51875/MeatSDFull.xlsx?v=8992.5 (accessed on 12 August 2021).

- Agri Benchmark Beef and Sheep Network, Database; Thünen Institute of Farm Economics: Braunschweig, Germany, 2020; Available online: http://www.agribenchmark.org/beef-and-sheep.html (accessed on 12 July 2021).

- Gladman, R. Retail Gains Offset Cautious Return to out-of-Home Dining; Agriculture and Horticulture Development Board AHDB: Kenilworth, Warwickshire, UK, 2020; Available online: https://ahdb.org.uk/news/consumer-insight-retail-gains-offset-cautious-return-to-out-of-home-dining (accessed on 11 July 2021).

- MLA. Market Snapshot: Beef and Sheepmeat—Greater China; Meat & Livestock Australia MLA: North Sydney, NSW, Australia, 2020; Available online: https://www.mla.com.au/globalassets/mla-corporate/prices--markets/documents/os-markets/red-meat-market-snapshots/2020/greater-china_2020-mla-mi-snapshot-28092020-distribution.pdf (accessed on 17 May 2021).

- FAO. Mitigating the Impacts of COVID-19 on the Livestock Sector; FAO: Rome, Italy, 2020; ISBN 978-92-5-132512-4. Available online: http://www.fao.org/documents/card/en/c/ca8799en/ (accessed on 20 June 2021).

- IMF. Database of Fiscal Policy Responses to COVID-19; IMF Fiscal Affairs Department, International Monetary Fund: Washington DC, USA, 2021; Available online: https://www.imf.org/en/Topics/imf-and-covid19/Fiscal-Policies-Database-in-Response-to-COVID-19 (accessed on 19 September 2021).

- Arelovich, H.M. Facts and thoughts on how the COVID-19 pandemic has affected animal agriculture in Argentina. Anim. Front. 2021, 11, 28–32. [Google Scholar] [CrossRef]

- MAGYP. Principales Indicadores del Sector Bovino; Ministerio de Agricultura, Ganadería y Pesca—Argentina MAGYP: Buenos Aires, Argentina, 2021; Available online: https://www.magyp.gob.ar/sitio/areas/bovinos/informacion_sectorial/_archivos/000030_Indicadores/000001-%20Indicadores%20bovinos%20mensuales.pdf (accessed on 20 August 2021).

- MAGYP. Evolución mensual y anual de los indicadores: Porcinos; Ministerio de Agricultura, Ganadería y Pesca—Argentina MAGYP: Buenos Aires, Argentina, 2021; Available online: https://www.magyp.gob.ar/sitio/areas/porcinos/estadistica/_archivos//000007_Evoluci%C3%B3n%20de%20los%20Indicadores/000000_Evoluci%C3%B3n%20mensual%20y%20anual%20de%20los%20indicadores.pdf (accessed on 20 August 2021).

- CEPEA. Valuations of Fed Cattle and Beef in 2021 Are Practically the Same; Center for Advanced Studies on Applied Economics CEPEA: São Paulo, Brazil, 2021; Available online: https://www.cepea.esalq.usp.br/en/brazilian-agribusiness-news/valuations-of-fed-cattle-and-beef-in-2021-are-practically-the-same.aspx (accessed on 20 August 2021).

- ABPA. Consumo Per Capita de Carne de Frango no Brasil (Kg/Hab); Estatística do Setor, Aves, Associação Brasileira de Proteína Animal ABPA: São Paulo, Brazil, 2021; Available online: https://abpa-br.org/mercados/ (accessed on 20 August 2021).

- USMEF. November Beef Exports Largest in More than a Year; 2020 Pork Exports Top Previous Annual Record; U.S. Meat Export Federation USMEF: Denver, CO, USA, 2021; Available online: https://www.usmef.org/news-statistics/press-releases/november-beef-exports-largest-in-more-than-a-year-2020-pork-exports-top-previous-annual-record/ (accessed on 11 July 2021).

- MDIC. Brazilian Foreign Trade Statistics; Ministério da Indústria, Comércio Exterior e Serviços MDIC: Brasília, Brazil, 2021. Available online: http://comexstat.mdic.gov.br/en/home (accessed on 15 June 2021).

- USMEF. Export Statistics; U.S. Meat Export Federation USMEF: Denver, CO, USA, 2021; Available online: https://www.usmef.org/news-statistics/statistics/?stat_year=2020 (accessed on 11 July 2021).

- B+LNZ. Meat Export Tool; Beef + Lamb New Zealand: Wellington, New Zealand, 2021; Available online: https://beeflambnz.com/data-tools/meat-export-tool (accessed on 19 August 2021).

- Mano, A. Special Report: How COVID-19 Swept the Brazilian Slaughterhouses of JBS, World’s Top Meatpacker; Thomson Reuters: London, UK, 2020; Available online: https://www.reuters.com/article/uk-health-coronavirus-jbs-specialreport-idUKKBN25Z1I4 (accessed on 11 July 2021).

- Lusk, J.L.; Tonsor, G.T.; Schulz, L.L. Beef and pork marketing margins and price spreads during COVID-19. Appl. Econ. Perspect. Policy 2021, 43, 4–23. [Google Scholar] [CrossRef]

- Waltenburg, M.A.; Victoroff, T.; Rose, C.E.; Butterfield, M.; Jervis, R.H.; Fedak, K.M.; Gabel, J.A.; Feldpausch, A.; Dunne, E.M.; Austin, C.; et al. Update: COVID-19 Among Workers in Meat and Poultry Processing Facilities—United States, April–May 2020; US Department of Health and Human Services/Centers for Disease Control and Prevention: Washington, DC, USA, 2020; pp. 887–892. [Google Scholar] [CrossRef]

- Hobbs, J.E. The Covid-19 pandemic and meat supply chains. Meat Sci. 2021, 181, 108459. [Google Scholar] [CrossRef]

- Dyal, J.W.; Grant, M.P.; Broadwater, K.; Bjork, A.; Waltenburg, M.A.; Gibbins, J.D.; Hale, C.; Silver, M.; Fischer, M.; Steinberg, J.; et al. COVID-19 Among Workers in Meat and Poultry Processing Facilities—19 States, April 2020; US Department of Health and Human Services/Centers for Disease Control and Prevention: Washington, DC, USA, 2020; pp. 557–561. [Google Scholar] [CrossRef]

- World Farmers’ Organization (WFO). COVID-19 Pandemic Outbreak: Overview of the Impact on the Agricultural Sector. A Technical Assessment of the Undergoing Situation; WFO: Rome, Italy, 2020; Available online: https://www.wfo-oma.org/wp-content/uploads/2020/05/COVID19-WFO-technical-assessment_005082020.pdf (accessed on 30 September 2020).

- Lee, G. Coronavirus: What went wrong at Germany’s Gütersloh meat factory? BBC News: London, UK, 2020. Available online: https://www.bbc.com/news/world-europe-53177628 (accessed on 1 July 2020).

- BBC News. Coronavirus: German Outbreak Sparks Fresh Local Lockdowns; BBC News: London, UK, 2020; Available online: https://www.bbc.com/news/world-europe-53149762 (accessed on 1 July 2020).

- Business and Human Rights Resource Centre. Germany: Cabinet Proposes New Regulations to Better Protect Meatpacking Workers Following COVID-19 Outbreaks at Slaughterhouses; Business and Human Rights Resource Centre: London, UK, 2020; Available online: https://www.business-humanrights.org/en/latest-news/germany-cabinet-proposes-new-regulations-to-better-protect-meatpacking-workers-following-covid-19-outbreaks-at-slaughterhouses/ (accessed on 5 July 2021).

- Deutsche Welle. German Government Approves Stricter Rules for Meat Industry; Deutsche Welle (DW): Bonn, Germany, 2020; Available online: https://www.dw.com/en/german-government-approves-stricter-rules-for-meat-industry/a-55750116 (accessed on 28 January 2021).

- USDA. Prices Received: Cattle Prices Received by Month, US; U.S. Department of Agriculture, National Agricultural Statistics Service: Washington, DC, USA, 2021. Available online: https://www.nass.usda.gov/Charts_and_Maps/Agricultural_Prices/priceca.php (accessed on 6 August 2021).

- USDA/FAS. Market and Trade Data; U.S. Department of Agriculture, Foreign Agricultural Service FAS: Washington, DC, USA, 2021. Available online: https://apps.fas.usda.gov/psdonline/app/index.html#/app/advQuery (accessed on 6 August 2021).

- Wright, R. Lamb Market Outlook; Agriculture and Horticulture Development Board AHDB: Kenilworth, UK, 2021; Available online: https://ahdb.org.uk/lamb-market-outlook (accessed on 30 August 2021).

- Murray, M. Brexit ‘No Deal’ Scenario Poses Serious Threat to Irish Farmers; Special Report, The Irish Times: Dublin, Ireland, 2020; Available online: https://www.irishtimes.com/special-reports/the-future-of-farming/brexit-no-deal-scenario-poses-serious-threat-to-irish-farmers-1.4346742 (accessed on 30 August 2021).

- Tragsa Group, Madrid, Spain. Personal communication, 2021.

- Frezal, C.; Gay, S.; Nenert, C. The Impact of the African Swine Fever Outbreak in China on Global Agricultural Markets; OECD: Paris, France, 2021. [Google Scholar] [CrossRef]

- Spilimbergo, M.A.; Srinivasan, M.K. Brazil: Boom, Bust, and the Road to Recovery; International Monetary Fund: Washington, DC, USA, 2019; ISBN 9781484339749. [Google Scholar] [CrossRef]

- Dwyer, B. Latin America: An End to Boom and Bust? Euromoney Institutional Investor PLC: London, UK, 2019; Available online: https://www.euromoney.com/article/b1dd4cf9mv160j/latin-america-an-end-to-boom-and-bust (accessed on 13 January 2021).

- OANDA Corporation. Historical Exchange Rates; OANDA Corporation: New York, NY, USA, 2020; Available online: https://www.oanda.com/fx-for-business/historical-rates (accessed on 15 May 2020).

- CEPEA. Center for Advanced Studies on Applied Economics; CEPEA: São Paulo, Brazil, 2021; Personal communication. [Google Scholar]

- Deutsche Welle. Argentina Cerró 2020 con una Inflación de 36%; Deutsche Welle (DW): Bonn, Germany, 2021; Available online: https://www.dw.com/es/argentina-cerr%C3%B3-2020-con-una-inflaci%C3%B3n-de-36/a-56229478 (accessed on 15 May 2020).

- FAO. FAOSTAT Statistical Database; FAO: Rome, Italy, 2020. [Google Scholar]

- Allouche, Y. Algerians Are Hurting: Dinar’s Dramatic Fall Deepens Economic Woes; Middle East Eye MEE: London, UK, 2020; Available online: https://www.middleeasteye.net/news/algeria-dinar-record-low-economic-collapse (accessed on 17 August 2021).

- Trading Economics. Brent Crude Oil; Trading Economics: New York, NY, USA, 2021; Available online: https://tradingeconomics.com/commodity/brent-crude-oil (accessed on 9 September 2021).

- USDA. Grain and Feed Annual—Jordan; U.S. Department of Agriculture, Foreign Agricultural Service: Washington, DC, USA, 2021. Available online: https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Grain%20and%20Feed%20Annual_Amman_Jordan_03-15-2021 (accessed on 9 September 2021).

- Weeks Consulting Services Pty Ltd., Sydney, NSW, Australia. Personal communication, 2021.

- B+LNZ. New Season Outlook 2020–2021; Beef + Lamb New Zealand: Wellington, New Zealand, 2020; Available online: https://beeflambnz.com/sites/default/files/data/files/B%2BLNZ%20New%20Season%20Outlook%202020-21.pdf (accessed on 9 September 2021).

- B+LNZ. Mid-Season Update 2020–2021; Beef + Lamb New Zealand: Wellington, New Zealand, 2021; Available online: https://beeflambnz.com/sites/default/files/data/files/MidSeason%20Update%20%28MSU%29%202020-21%20Report.pdf (accessed on 9 September 2021).

- Nyaungwa, N. Severe Drought to Hit Namibia’s Meat Industry after Cattle Herds Decimated. Thomson Reuters: London, UK, 2020. Available online: https://www.reuters.com/article/ozatp-uk-namibia-meat-idAFKBN28M09M-OZATP (accessed on 25 August 2021).

- Ackermann, B. Namibia: Sheep Production Figures Drop Due to Drought; ProAgri: Pretoria, South Africa, 2021. Available online: https://www.proagri.co.za/en/namibia-sheep-production-figures-drop-due-to-drought/ (accessed on 25 August 2021).

- USDA. Argentina: 30-Day Beef Export Ban; U.S. Department of Agriculture, Foreign Agricultural Service: Washington, DC, USA, 2021. Available online: https://www.fas.usda.gov/data/argentina-argentina-imposes-30-day-beef-export-ban (accessed on 12 September 2021).

- FAO. Meat Market Review: Price and Policy Update; FAO: Rome, Italy, 2021; Available online: https://www.fao.org/3/cb6127en/cb6127en.pdf (accessed on 10 September 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Data Source | Purpose | |

|---|---|---|

| Five-point Likert scale | Quantify the pandemic impact |

| Closed questions (relevant/not relevant) | Explore the relevance of the latest development issues | |

| Observe any improvements regarding beef and sheep meat supply chains and producer prices during the 1st half, 2021 | |

| Drive deeper insights into the developments of beef and sheep sectors in 2020 across the globe | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almadani, M.I.; Weeks, P.; Deblitz, C. COVID-19 Influence on Developments in the Global Beef and Sheep Sectors. Ruminants 2022, 2, 27-53. https://doi.org/10.3390/ruminants2010002

Almadani MI, Weeks P, Deblitz C. COVID-19 Influence on Developments in the Global Beef and Sheep Sectors. Ruminants. 2022; 2(1):27-53. https://doi.org/10.3390/ruminants2010002

Chicago/Turabian StyleAlmadani, Mohamad Isam, Peter Weeks, and Claus Deblitz. 2022. "COVID-19 Influence on Developments in the Global Beef and Sheep Sectors" Ruminants 2, no. 1: 27-53. https://doi.org/10.3390/ruminants2010002

APA StyleAlmadani, M. I., Weeks, P., & Deblitz, C. (2022). COVID-19 Influence on Developments in the Global Beef and Sheep Sectors. Ruminants, 2(1), 27-53. https://doi.org/10.3390/ruminants2010002