Incentives and Barriers to Homeowners’ Uptake of FireSmart® Canada’s Recommended Wildfire Mitigation Activities in the City of Fort McMurray, Alberta

Abstract

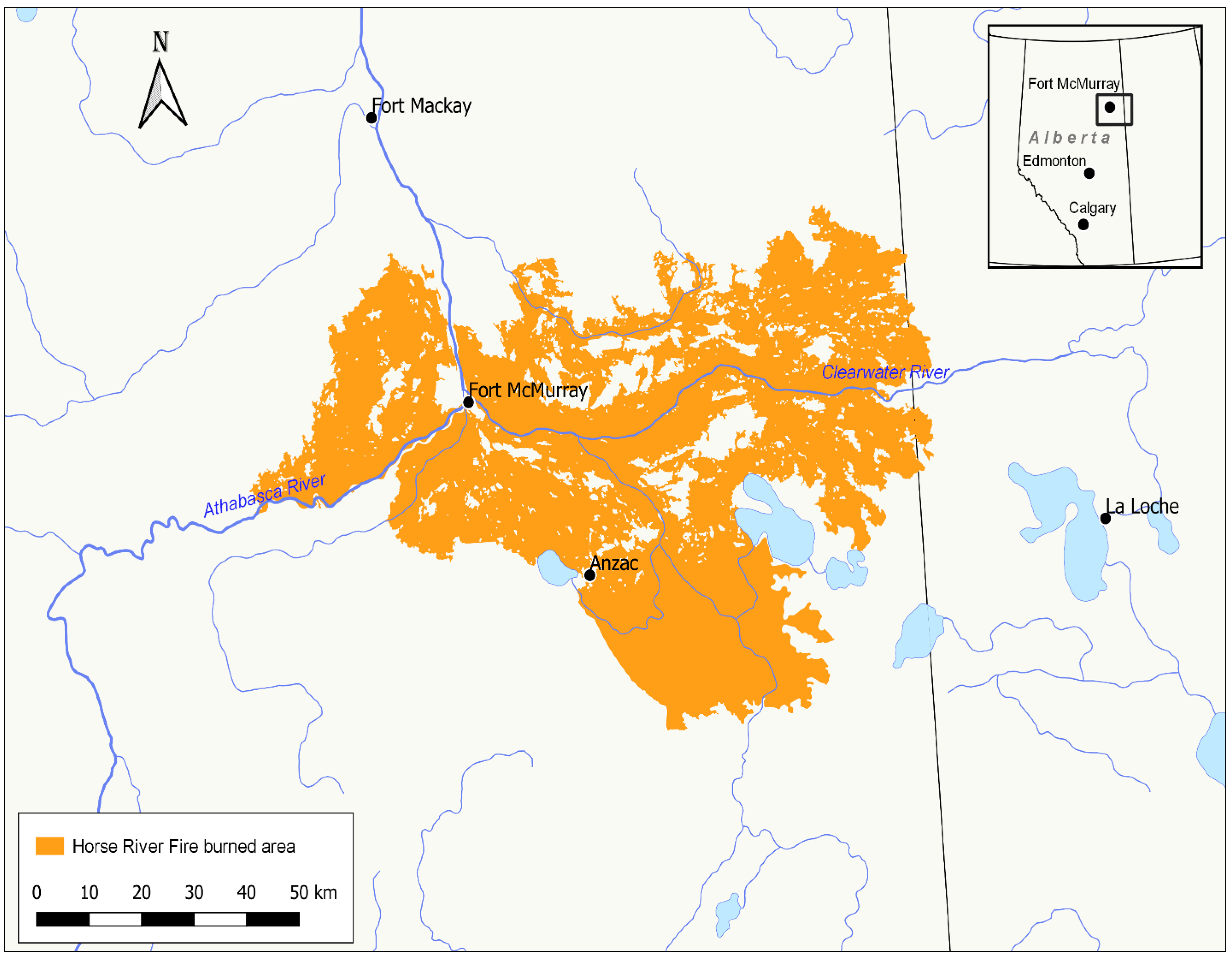

:1. Introduction

- Assess perceptions and attitudes of Fort McMurray residents of wildfire risk and mitigation following the Horse River wildfire.

- Examine the extent to which FireSmart activities are known, understood, and applied by homeowners.

- Explore the factors affecting homeowners’ uptake of FireSmart Canada.

2. Literature Review

3. Research Methods

3.1. Sampling

3.2. The Survey Instruments

3.3. Data Collection

3.4. Data Analysis

4. Result

4.1. Socio-Economic and Demographic Background of the Participants

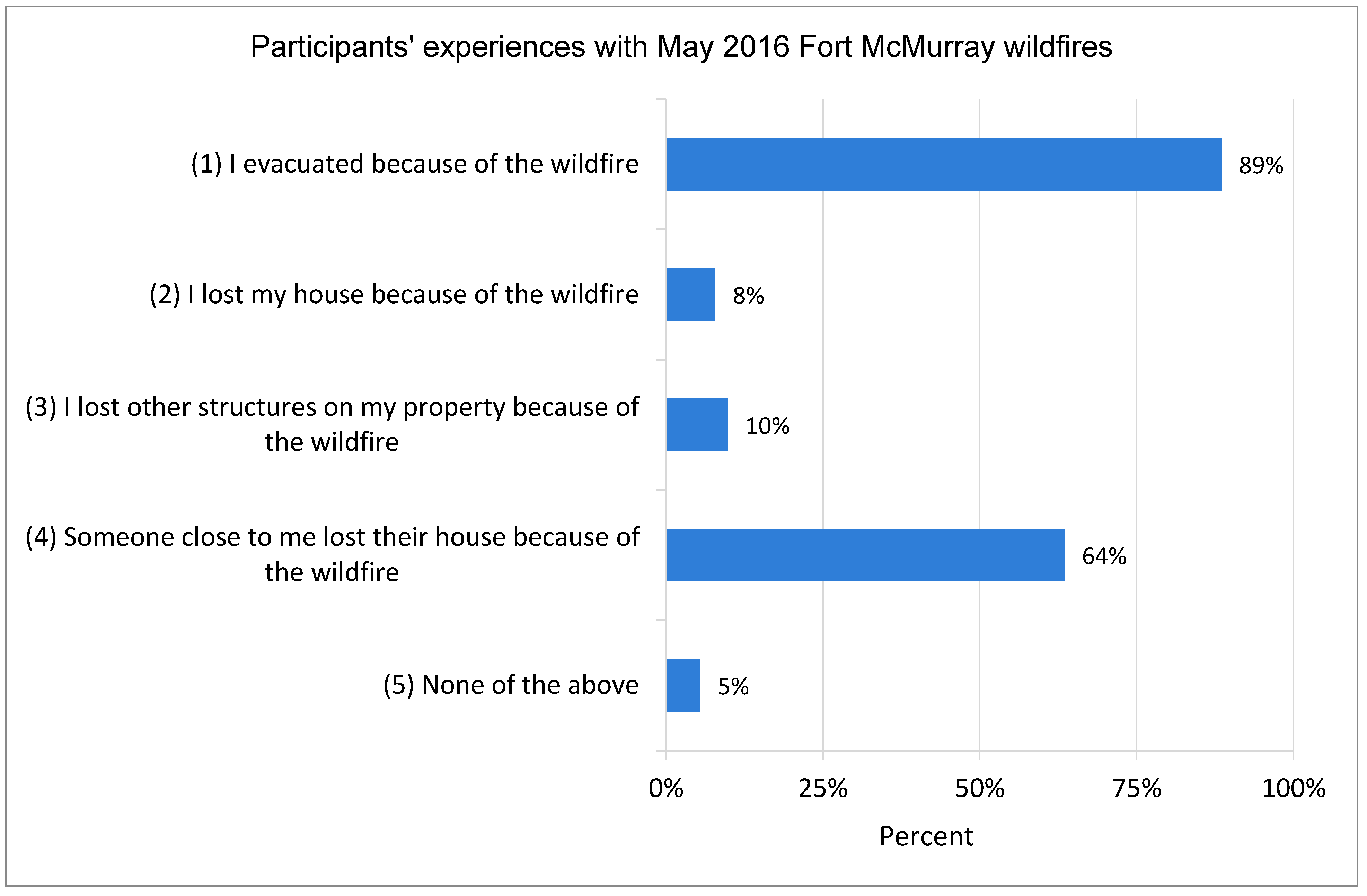

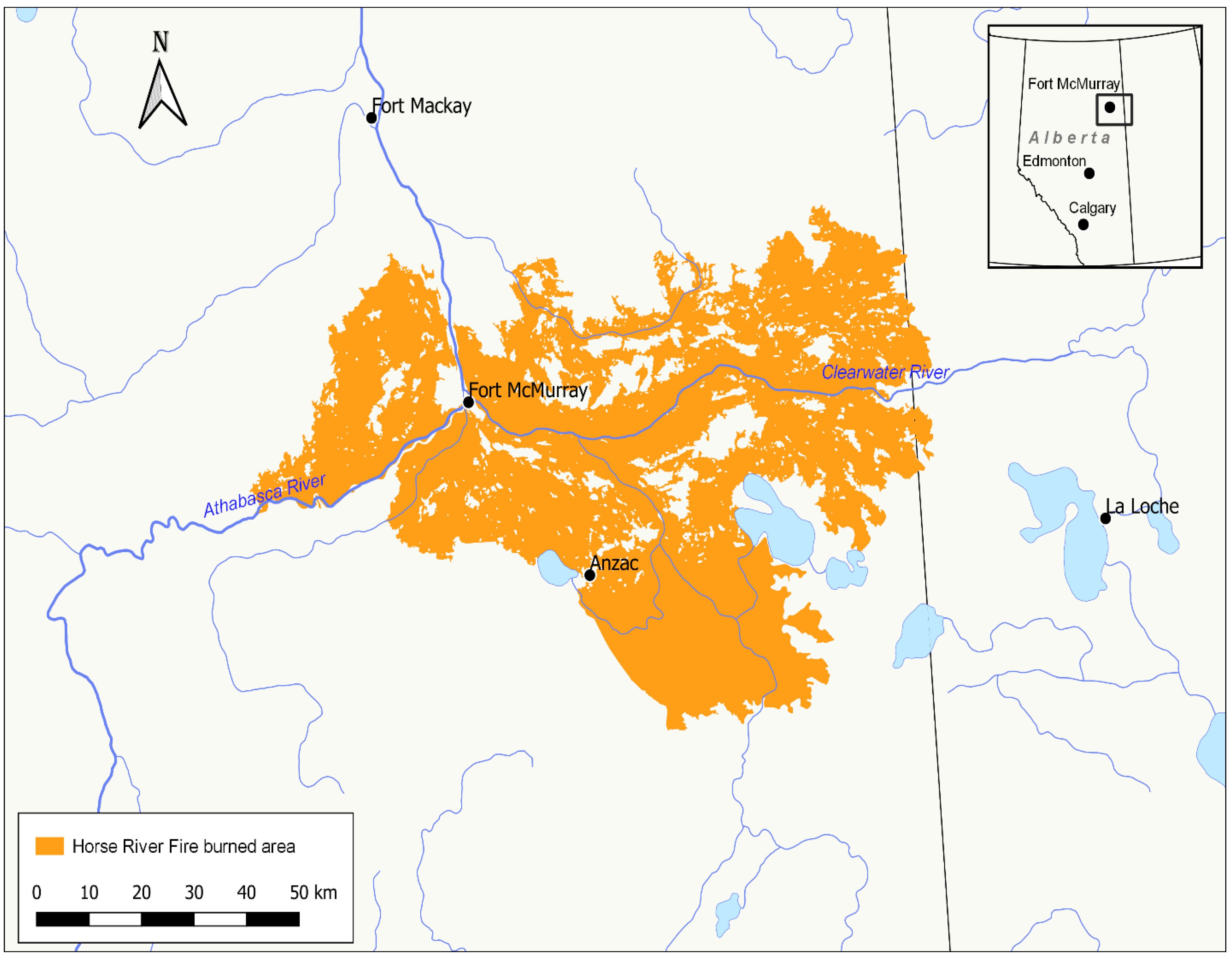

4.2. Experience with the Horse River Wildfire

4.3. Perceived Risk

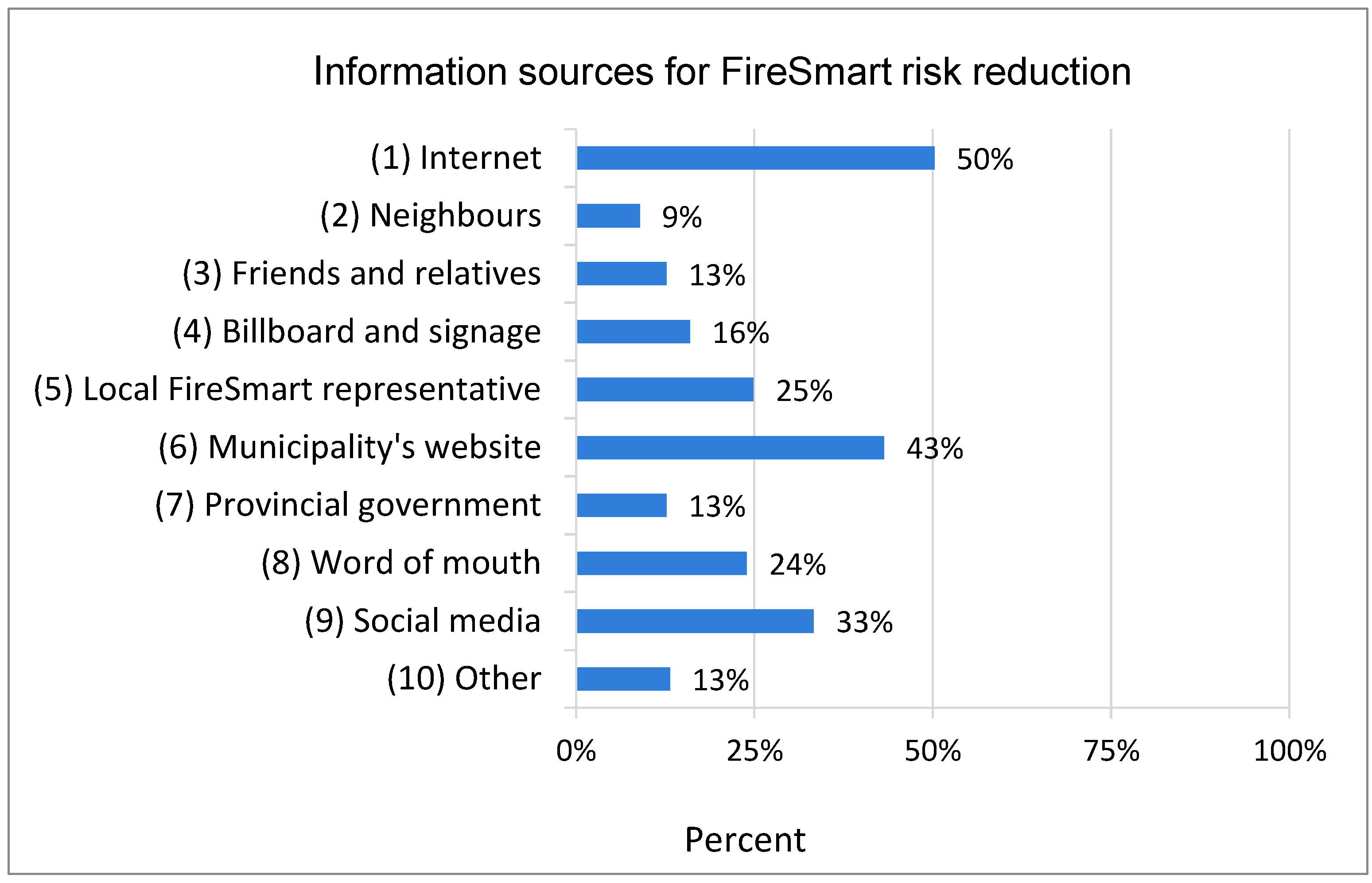

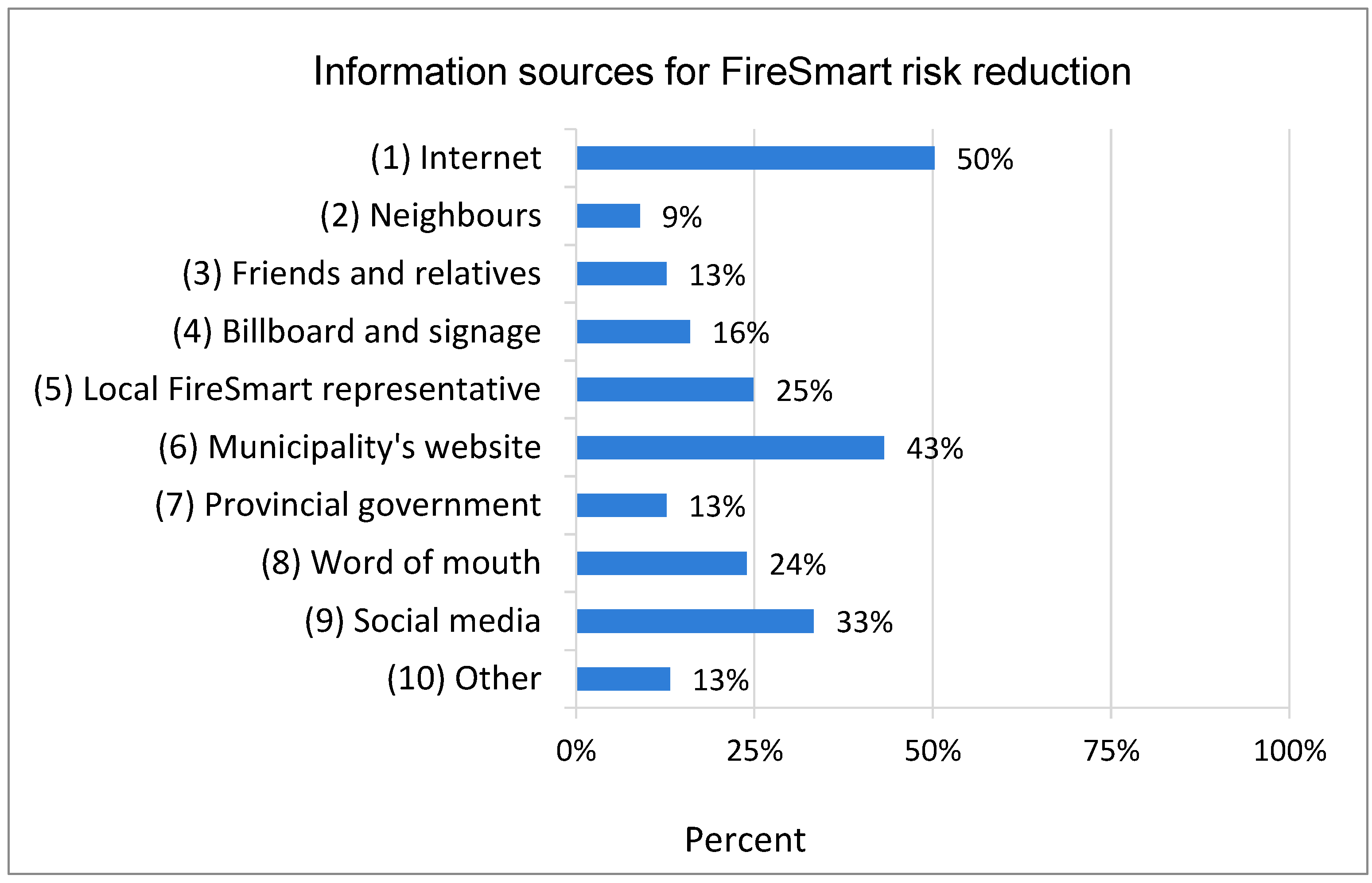

4.4. FireSmart Mitigation Awareness

4.5. FireSmart Mitigation Activities Known and Implemented in Post-Fire Recovery

4.5.1. Vegetation Management and Fuel-Reduction Activities

4.5.2. Structural Mitigation Measures

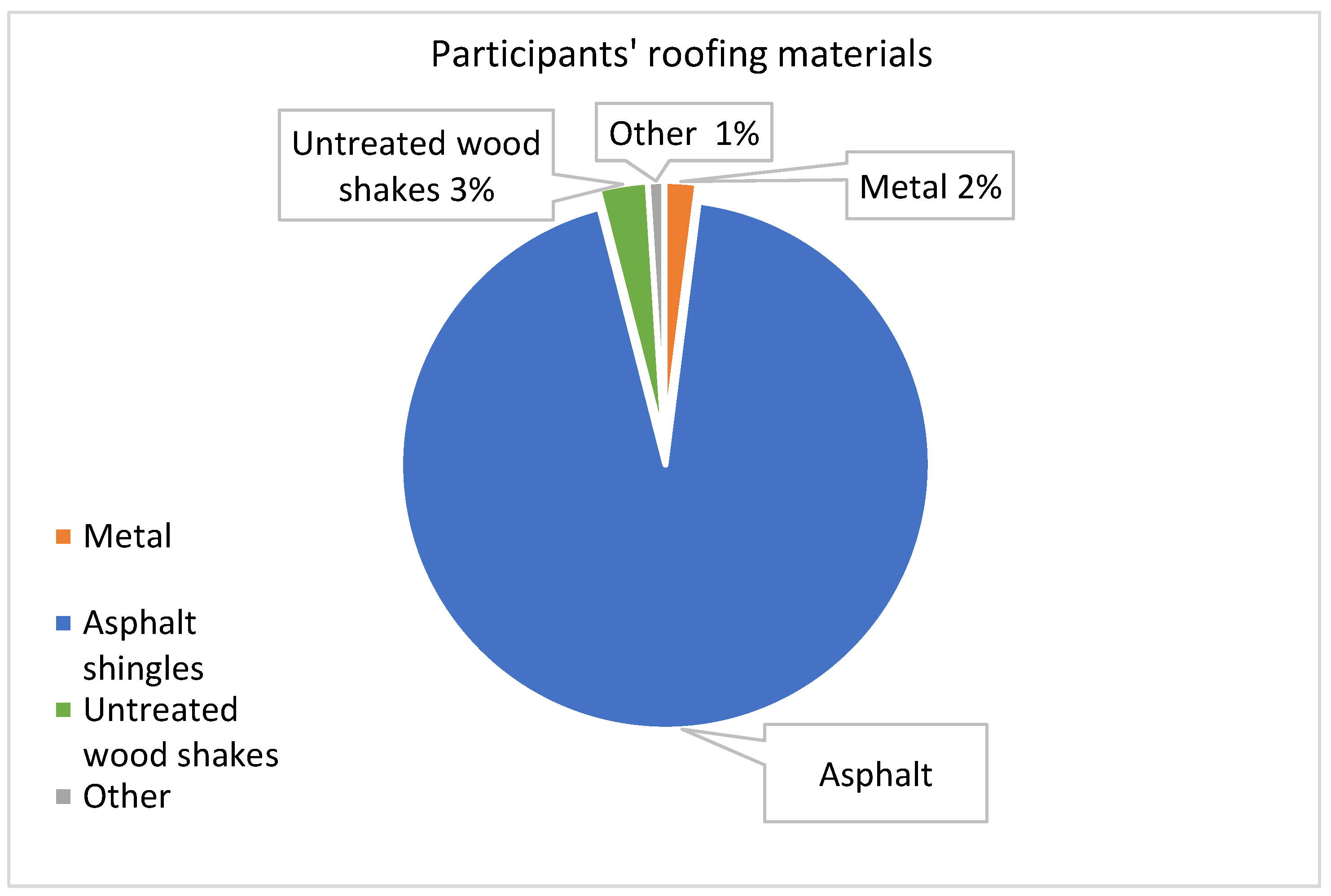

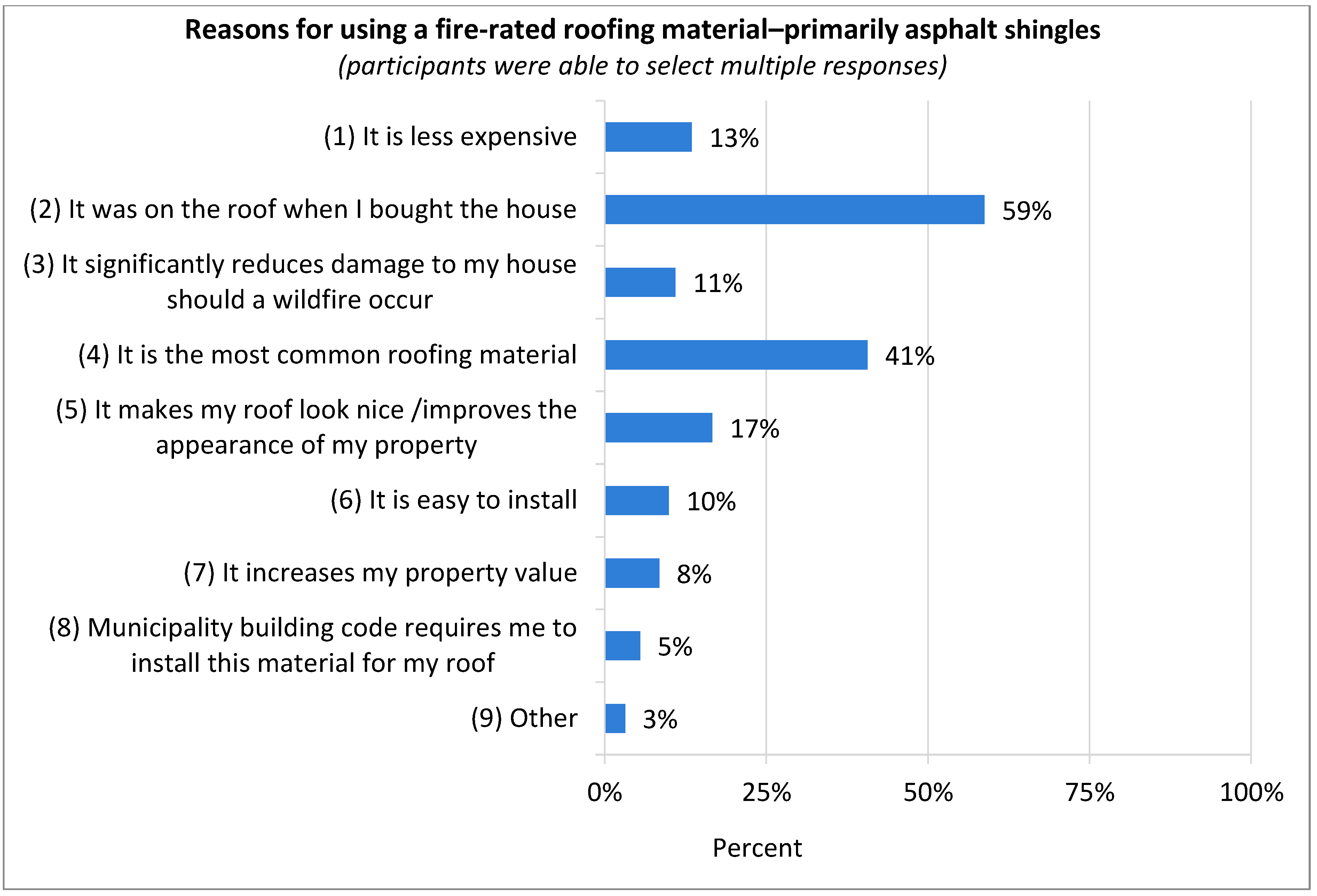

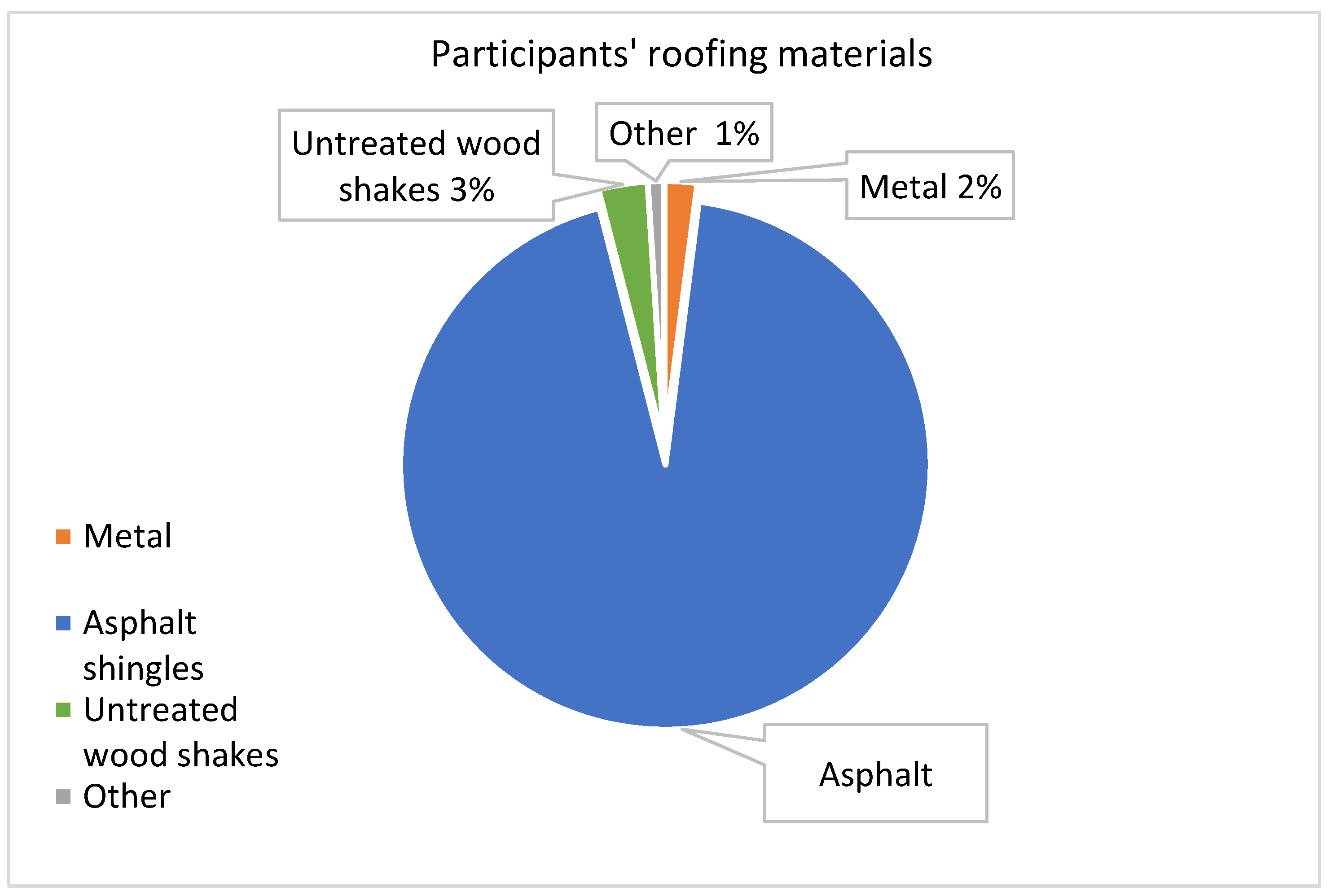

Roofing Material

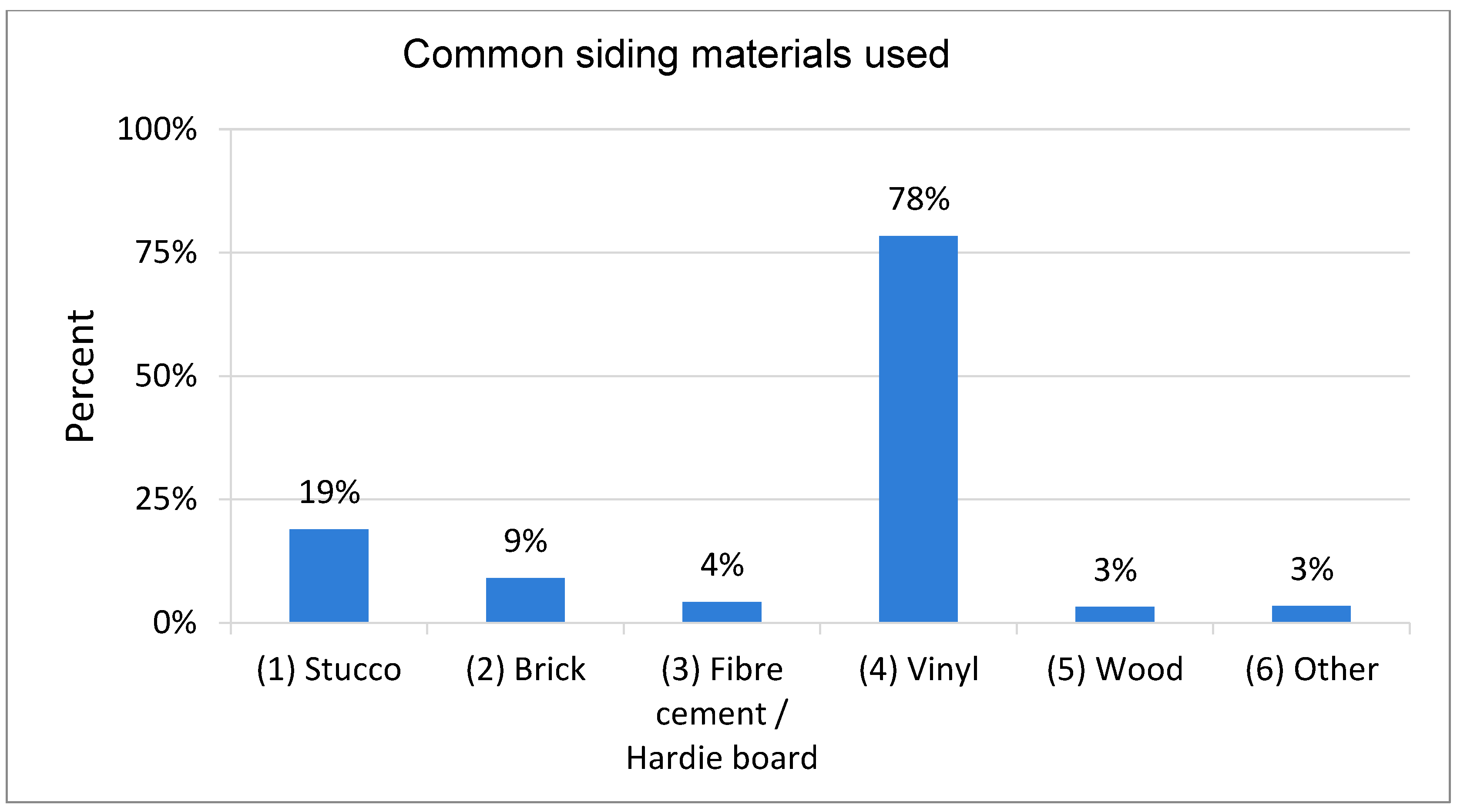

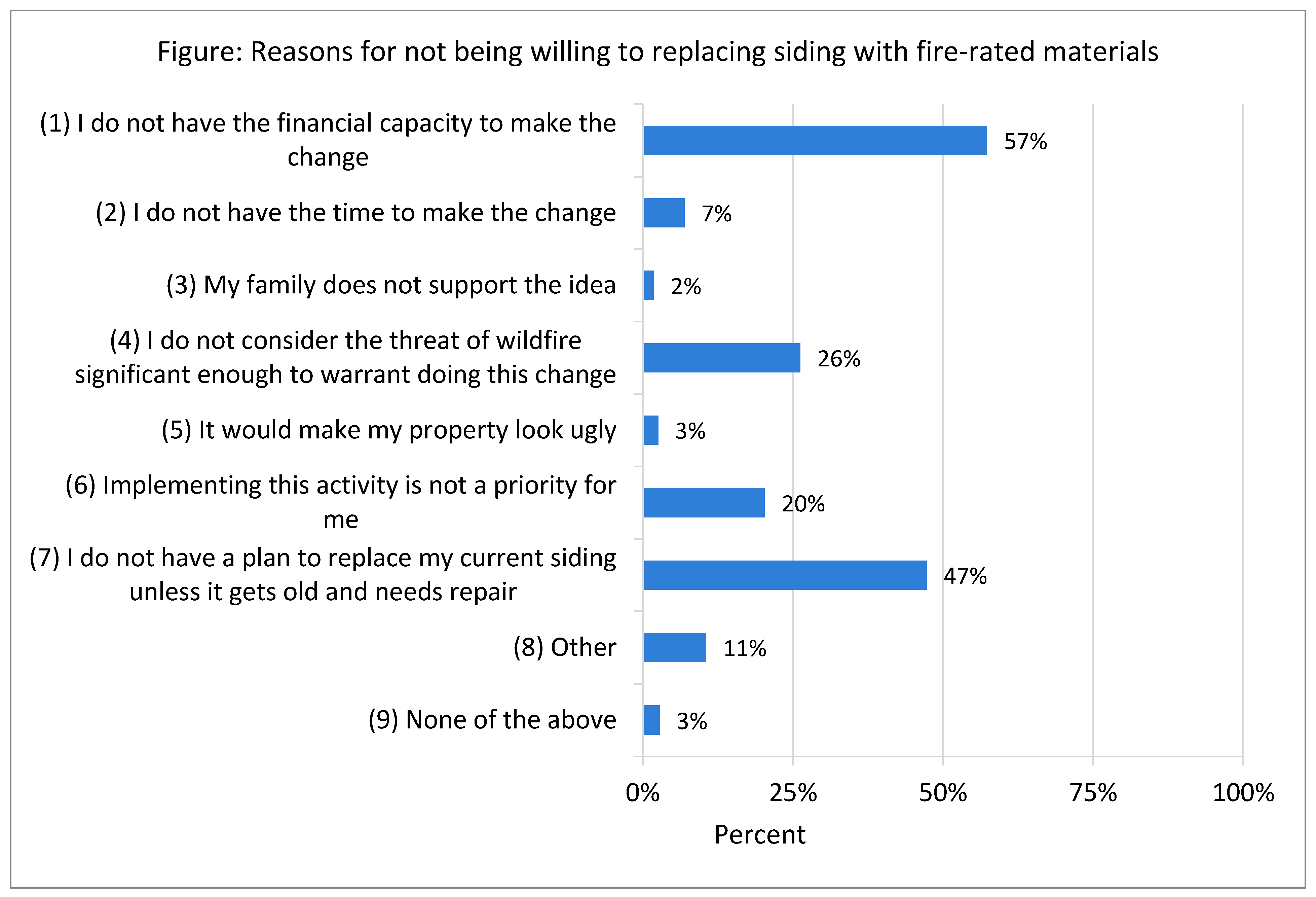

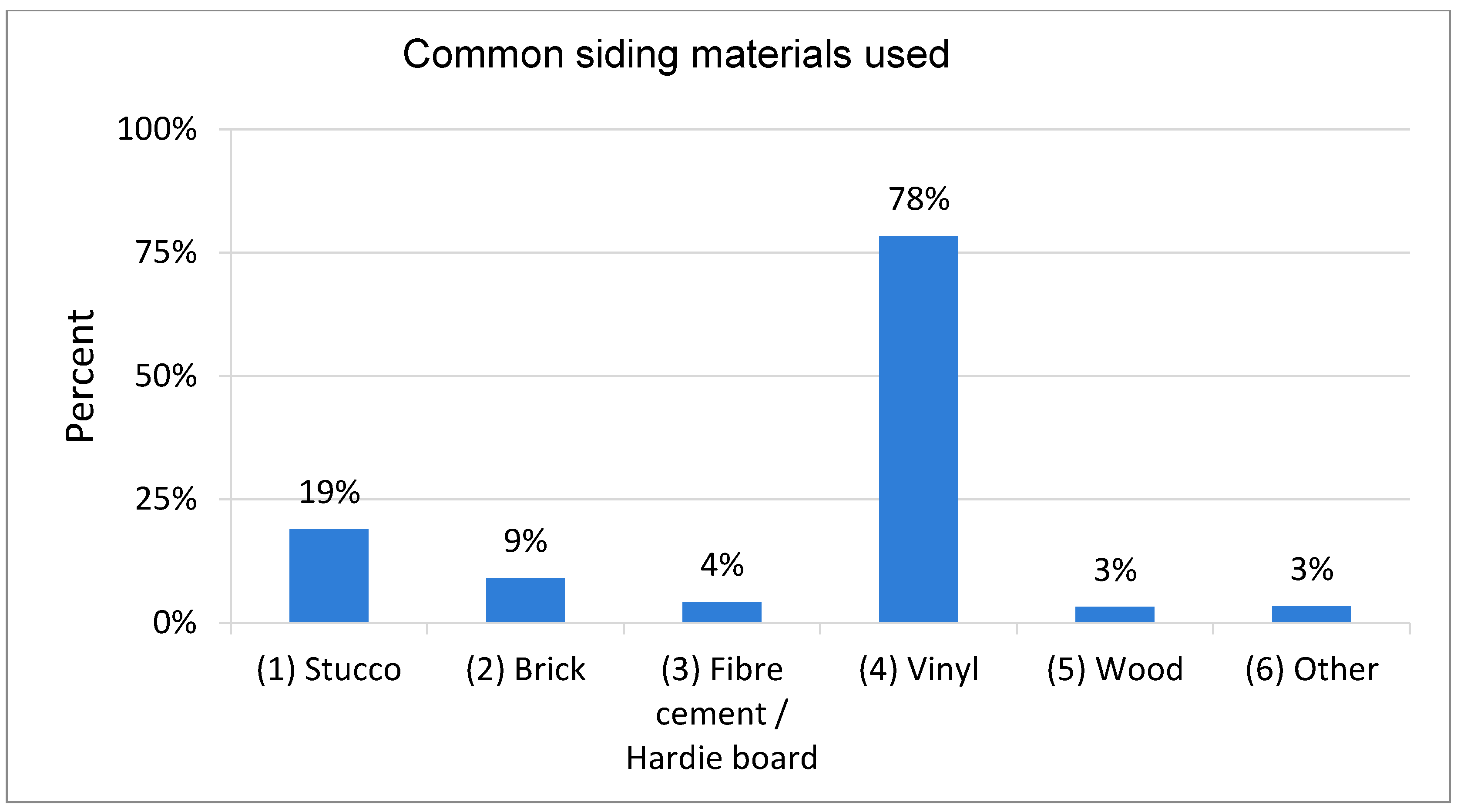

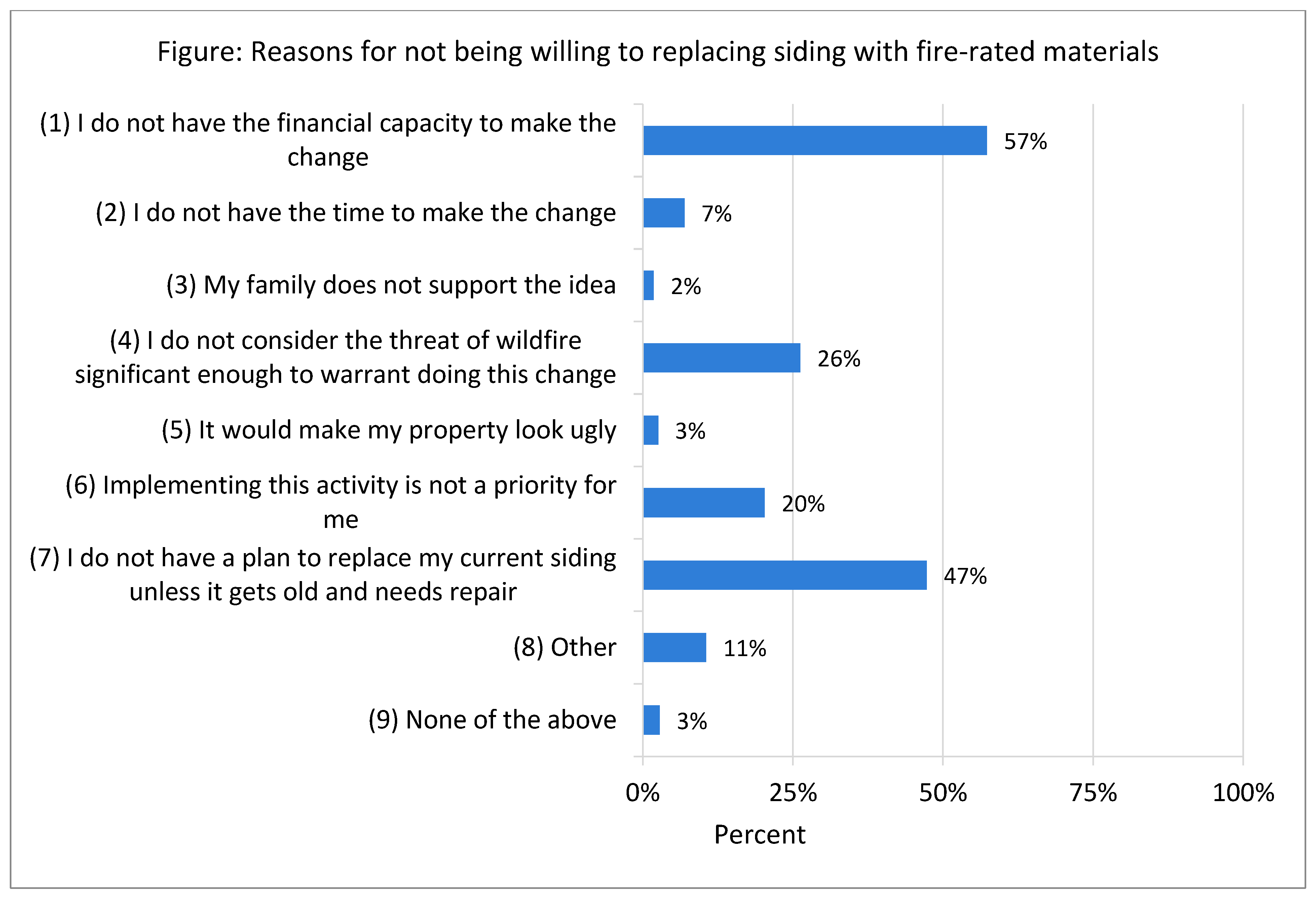

Siding Material

“I strongly disliked the suggestion of being forced to do anything to my home at my expense. I owned this home before the fire. According to all current and previous laws my home is fine the way it is. I’d leave Fort McMurray if I had to replace my siding for a more “preferable and fire smart exterior”. If they want to imposesuch laws on new builds be my guest.”

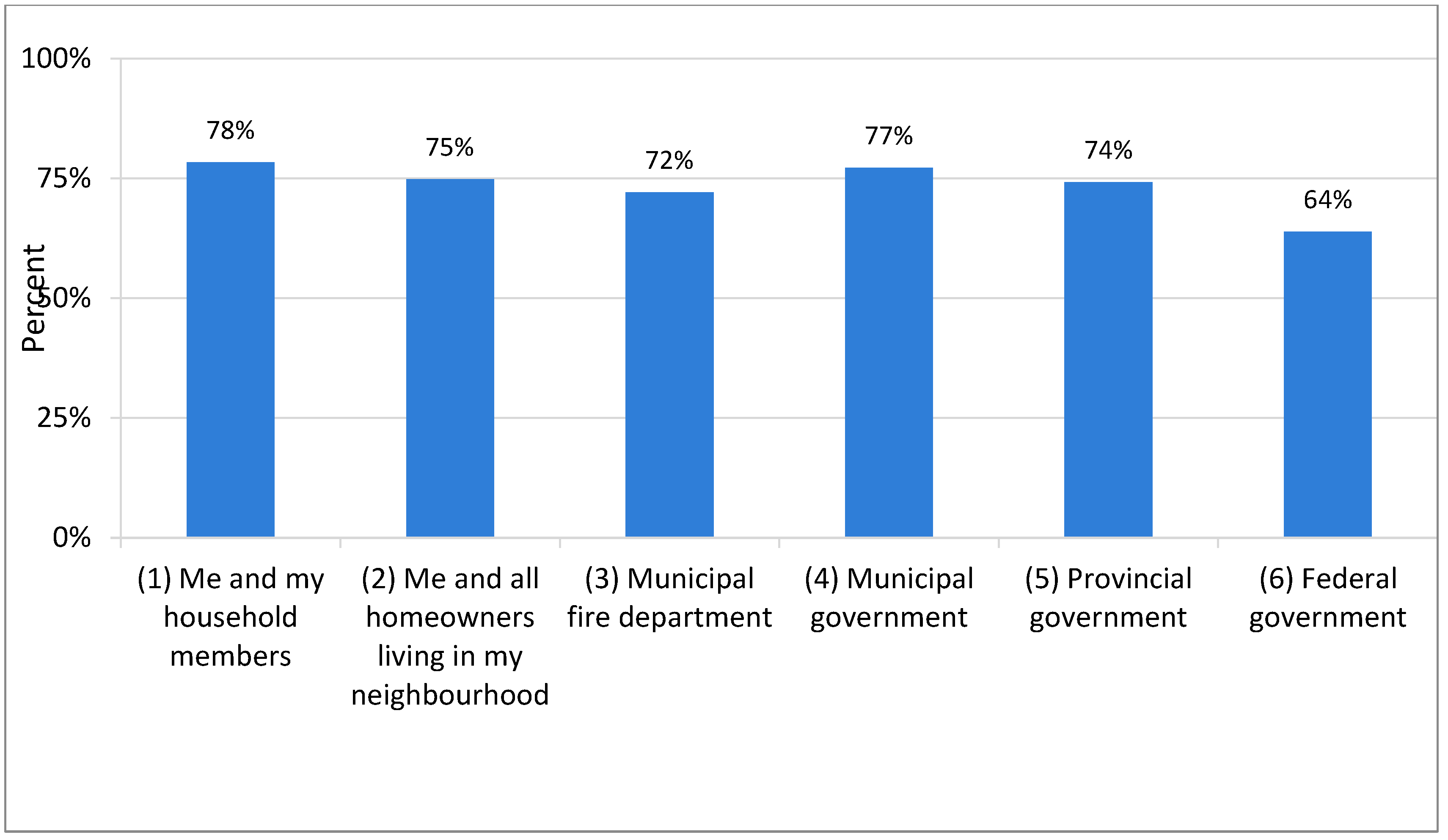

4.6. Sense of Responsibility

4.7. Social Pressure

“I live on a small property with only one tree on my property that has been trimmed to remove all dead branches. Neighbours have trees that are dead and/or have dead branches that requireremoval but that hasn’t happened. We all have to work together to mitigate this ever happening again.”

“I find efforts on my property is limited by the numerous rental homes in my area that are never maintained. For example, there are yards that have not been maintained since the homes were built ten or more years ago. The homes are builtclose together and I worry that during a wildfire there would not be adequate resources to prevent structure fires from spreading.”

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Mamuji, A.A.; Rozdilsky, J.L. Wildfire as an increasingly common natural disaster facing Canada: Understanding the 2016 Fort McMurray wildfire. Nat. Hazards 2019, 98, 163–180. [Google Scholar] [CrossRef]

- Government of Alberta. Home Again: Recovery after the Wood Buffalo Wildfire. A Report of the Alberta Office of the Minister of Municipal Affairs. 2016. Available online: https://www.alberta.ca/documents/Wildfire-Home-Again-Report.pdf (accessed on 2 February 2019).

- MNP. A Review of the 2016 Horse River Wildfire: Alberta Agriculture and Forestry Preparedness and Response; MNP: Edmonton, AB, Canada, 2017. [Google Scholar]

- KPMG. Regional Municipality of Wood Buffalo Lessons Learned and Recommendations from the 2016 Horse River Wildfire; Final Report; KPMG: Amstelveen, The Netherlands, 2017. [Google Scholar]

- Insurance Bureau of Canada. Northern Alberta Wildfire Costliest Insured Natural Disaster in Canadian History. 2016. Available online: http://www.ibc.ca/bc/resources/media-centre/media-releases/northern-alberta-wildfire-costliest-insured-natural-disaster-in-canadian-history (accessed on 26 May 2018).

- Walkinshaw, S. Regional Municipality of Wood Buffalo Wildfire Mitigation Strategy; Montane Forest Management Ltd.: Canmore, AB, Canada, 2017; Available online: https://www.rmwb.ca/Assets/Recovery/2017%2bWildfire%2bMitigation%2bStrategy.pdf (accessed on 16 October 2019).

- Partners in Protection (Canada). About FireSmart Canada. 2018. Available online: https://www.firesmartcanada.ca/about-firesmart/ (accessed on 16 October 2019).

- Firewise Communities. About Firewise. Available online: http://www.Firewise.org/index.php (accessed on 1 February 2020).

- Collins, T.W.; Bolin, B. Situating hazard vulnerability: People’s negotiations with wildfire environments in the U.S. Southwest. Environ. Manag. 2009, 44, 441–455. [Google Scholar] [CrossRef] [PubMed]

- McCaffrey, S. Prescribed fire: What influences public approval? In Fire in Eastern Oak Forests: Delivering Science to Land Managers, Proceedings of a Conference, Columbus, OH, USA, 15–17 November 2005; Dickinson, M.B., Ed.; Gen. Tech. Rep. NRS-P-1; U.S. Department of Agriculture, Forest Service; Northern Research Station: Newtown Square, PA, USA, 2006; pp. 192–198. [Google Scholar]

- McFarlane, B.L.; McGee, T.K.; Faulkner, H. Complexity of homeowner wildfire risk mitigation: An integration of hazard theories. Int. J. Wildland Fire 2011, 20, 921–931. [Google Scholar] [CrossRef] [Green Version]

- McCaffrey, S.; McGee, T.K.; Coughlan, M.; Tedim, F. Understanding wildfire mitigation and preparedness in the context of extreme wildfires and disasters: Social science contributions to understanding human response to wildfire. In Extreme Wildfire Events and Disasters; Tedim, F., Leone, V., McGee, T.K., Eds.; Elsevier: Amsterdam, The Netherlands, 2020; pp. 22–28. [Google Scholar]

- Brenkert-Smith, H.; Champ, P.A.; Flores, N. Insights into wildfire mitigation decisions among wildland-urban interface residents. Soc. Nat. Resour. 2006, 19, 759–768. [Google Scholar] [CrossRef]

- Martin, W.E.; Martin, I.M.; Kent, B. The role of risk perceptions in the risk mitigation process: The case of wildfire in high-risk communities. J. Environ. Manag. 2009, 91, 489–498. [Google Scholar] [CrossRef]

- McCaffrey, S.; Toman, E.; Stidham, M.; Shindler, B. Social science research related to wildfire management: An overview of recent findings and future research needs. Int. J. Wildland Fire 2013, 22, 15–24. [Google Scholar] [CrossRef] [Green Version]

- McCaffrey, S.M.; Olsen, C.S. Research Perspectives on the Public and Fire Management: A Synthesis of Current Social Science on Eight Essential Questions; General Technical Report NRS-104; United States Department of Agriculture Forest Service, Northern Research Station: Newtown Square, PA, USA, 2012. [Google Scholar]

- McCaffrey, S. Community wildfire preparedness: A global state-of-the-knowledge summary of social science research. Curr. For. Rep. 2015, 1, 81–90. [Google Scholar] [CrossRef] [Green Version]

- Cohn, P.J.; Williams, D.R.; Carroll, M.S. Wildland-urban interface residents’ views on risk and attribution. In Wildfire Risk: Human Perceptions and Management Implications; Martin, W.E., Raish, C., Kent, B., Eds.; RFF Press: Washington, DC, USA, 2008; pp. 23–43. [Google Scholar]

- Gordon, J.S.; David, M.-C.; Stedman, R.C.; Luloff, A.E. Wildfire perception and community change. Rural Sociol. 2010, 75, 455–477. [Google Scholar] [CrossRef]

- Absher, J.D.; Vaske, J.J. The role of trust in residents’ fire wise actions. Int. J. Wildland Fire 2011, 20, 318–325. [Google Scholar] [CrossRef]

- McGee, T.K.; McFarlane, B.L.; Harris, L.; Faulkner, H. Human Dimensions of Fire Management at the Wildland-Urban Interface in Alberta: A Summary Report; ICLR Research Paper Series—Number 46; Institute for Catastrophic Loss Reduction: Toronto, ON, Canada, 2009. [Google Scholar]

- McGee, T.K. Public engagement in neighbourhood level wildfire mitigation and preparedness: Case studies from Canada, the US and Australia. J. Environ. Manag. 2011, 92, 2524–2532. [Google Scholar] [CrossRef]

- Quinn, S. Regional Municipality of Wood Buffalo FireSmart Engagement Survey; Unpublished Report; Regional Municipality of Wood Buffalo: Wood Buffalo, AB, USA, 2018. [Google Scholar]

- Tierney, K.J.; Lindell, M.K.; Perry, R.W. Facing the Unexpected: Disaster Preparedness and Response in the United States; Joseph Henry Press: Washington, DC, USA, 2001. [Google Scholar]

- Miller, R.K.; Field, C.B.; Mach, K.J. Barriers and enablers for prescribed burns for wildfire management in California. Nature Sustainability 2020, 3, 101–109. [Google Scholar] [CrossRef]

- Kolden, C.A.; Henson, C. A socio-ecological approach to mitigating wildfire vulnerability in the wildland urban interface: A case study from the 2017 Thomas fire. Fire 2019, 2, 9. [Google Scholar] [CrossRef] [Green Version]

- Wolters, E.A.; Steel, B.S.; Weston, D.; Brunson, M. Determinants of residential Firewise behaviors in Central Oregon. Soc. Sci. J. 2017, 54, 168–178. [Google Scholar] [CrossRef]

- Tierney, K. The Social Roots of Risk: Producing Disasters, Promoting Resilience; Stanford University Press: Redwood City, CA, USA, 2014. [Google Scholar]

- Brenkert-Smith, H.; Champ, P.A.; Flores, N. Trying not to get burned: Understanding homeowners’ wildfire risk–mitigation behaviors. Environ. Manag. 2012, 50, 1139–1151. [Google Scholar] [CrossRef] [PubMed]

- McLennan, J.; Elliott, G.; Omodei, M.; Whittaker, J. Householders’ safety-related decisions, plans, actions and outcomes during the 7 February 2009 Victorian (Australia) wildfires. Fire Saf. J. 2013, 61, 175–184. [Google Scholar] [CrossRef] [Green Version]

- McNeill, I.M.; Dunlop, P.D.; Heath, J.B.; Skinner, T.C.; Morrison, D.L. Expecting the unexpected: Predicting physiological and psychological wildfire preparedness from perceived risk, responsibility, and obstacles. Risk Anal. 2013, 33, 1829–1843. [Google Scholar] [CrossRef]

- Champ, P.A.; Brenkert-Smith, H. Is seeing believing? Perceptions of wildfire risk over time. Risk Anal. 2016, 36, 816–830. [Google Scholar] [CrossRef]

- Gordon, J.S.; Luloff, A.; Stedman, R.C. A multisite qualitative comparison of community wildfire risk perceptions. J. For. 2012, 110, 74–78. [Google Scholar] [CrossRef]

- Schulte, S.; Miller, K.A. Wildfire risk and climate change: The influence on homeowner mitigation behavior in the wildland–urban interface. Soc. Nat. Res. 2010, 23, 417–435. [Google Scholar] [CrossRef]

- McCaffrey, S.; Toman, E.; Stidham, M.; Shindler, B. Social science findings in the United States. In Wildfire Hazards, Risks and Disasters; Elsevier: Amsterdam, The Netherlands, 2015; pp. 15–34. [Google Scholar]

- Reams, M.A.; Haines, T.K.; Renner, C.R.; Wascom, M.W.; Kingre, H. Goals, obstacles and effective strategies of wildfire mitigation programs in the wildland–urban interface. For. Policy Econ. 2005, 7, 818–826. [Google Scholar] [CrossRef]

- Champ, P.A.; Donovan, G.H.; Barth, C.M. Living in a tinderbox: Wildfire risk perceptions and mitigating behaviours. Int. J. Wildland Fire 2013, 22, 832–840. [Google Scholar] [CrossRef]

- McGee, T.K.; McFarlane, B.L.; Varghese, J. An examination of the influence of hazard experience on wildfire risk perceptions and adoption of mitigation measures. Soc. Nat. Resour. 2009, 22, 308–323. [Google Scholar] [CrossRef]

- Christianson, A.; McGee, T.; Jardine, C. Canadian wildfire communication strategies. Aust. J. Emerg. Manag. 2011, 26, 40–51. [Google Scholar]

- Westhaver, A. Why Some Homes Survived: Learning from the Fort McMurray Wildland/Urban Interface Fire Disaster; Institute for Cata-strophic Loss Reduction: Toronto, ON, Canada, 2017. [Google Scholar]

- Regional Municipality of Wood Buffalo. Municipal Census Report. Available online: https://www.rmwb.ca/en/permits-and-development/resources/Documents/Latest-Census-Report-2018.pdf (accessed on 10 February 2020).

- Dillman, D.A.; Smyth, J.D.; Christian, L.M. Internet, Phone, Mail, and Mixed-Mode Surveys: The Tailored Design Method, 4th ed.; Willy & Sons, Inc.: Hoboken, NJ, USA, 2004. [Google Scholar]

- Partners in Protection (Canada). FireSmart: Protecting Your Community from Wildfire; Firesmart: Edmonton, AB, Canada, 2003. [Google Scholar]

- Statistics Canada. Census Profile, 2016 Census. Available online: https://www12.statcan.gc.ca/census-recensement/2016/dp-pd/prof/details/page.cfm?Lang=E&Geo1=CSD&Code1=4816037&Geo2=PR&Code2=48&SearchText=Wood%20Buffalo&SearchType=Begins&SearchPR=01&B1=All&GeoLevel=PR&GeoCode=4816037&TABID=1&type=0 (accessed on 20 September 2019).

- McCaffrey, S.; Kumagai, Y. No need to reinvent the wheel: Applying existing social science theories to wildfire. In People, Fire, and Forests: A Synthesis of Wildfire Social Science; Daniel, T.C., Carroll, M., Moseley, C., Raish, C., Eds.; Oregon State University Press: Corvallis, OR, USA, 2007; pp. 55–69. [Google Scholar]

- Nelson, K.C.; Monroes, M.C.; Fingerman, J.; Bowers, A. Living with fire: Homeowner assessment of landscape values and defensible space in Minnesota and Florida, USA. Int. J. Wildland Fire 2004, 13, 413–425. [Google Scholar] [CrossRef]

- Eriksen, C.; Gill, N.; Head, L. The gendered dimensions of bushfire in changing rural landscapes in Australia. J. Rural Stud. 2010, 26, 332–342. [Google Scholar] [CrossRef]

- Whittaker, J.; Haynes, K.; Handmer, J.; McLennan, J. Community safety during the 2009 Australian ‘Black Saturday’ bushfires: An analysis of household preparedness and response. Int. J. Wildland Fire 2013, 22, 841–849. [Google Scholar] [CrossRef] [Green Version]

- Hesseln, H.; Ergibi, M. Draft Final Report: National FireSmart Survey. Unpublished Report Prepared for CIFFC and FireSmart. November 2017. Available online: C:/Users/you/Downloads/104738-FIRESMART_survey_results_-_November_2017.pdf (accessed on 22 February 2019).

- McGee, T.K. Completion of recommended WUI fire mitigation measures within urban households in Edmonton, Canada. Environ. Hazards 2005, 6, 147–157. [Google Scholar] [CrossRef]

- Shindler, B. Public Acceptance of Wildland Fire Conditions and Fuel Reduction Practices: Challenges for Federal Forest Managers. In People, Fire, and Forests: A Synthesis of Wildfire Social Science; Daniel, T.C., Carroll, M.S., Moseley, C., Eds.; Oregon State University Press: Corvallis, OR, USA, 2007. [Google Scholar]

- Faulkner, H.; McFarlane, B.L.; McGee, T.K. Comparison of homeowners’ response to wildfire risk among towns with and without wildfire management. Environ. Hazards Hum. Policy Dimens. 2009, 8, 38–51. [Google Scholar] [CrossRef]

- Winter, G.; Fried, J. Homeowner perspectives on fire hazard, responsibility, and management strategies at the wildland-urban interface. Soc. Nat. Resour. 2000, 13, 33–49. [Google Scholar]

- Nelson, K. The look of the land: Homeowner landscape management and wildfire preparedness in Minnesota and Florida. Soc. Nat. Resour. 2005, 18, 321–336. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations, 3rd ed.; Free Press of Glencoe: New York, NY, USA, 1995. [Google Scholar]

- Nox, R.; Myles, C.C. Wildfire mitigation behavior on single family residential properties near Balcones Canyonlands Preserve wildlands in Austin, Texas. Appl. Geogr. 2017, 87, 222–233. [Google Scholar] [CrossRef]

- Weisshaupt, B.R.; Jakes, P.J.; Carroll, M.S.; Blatner, K.A. Northern Inland West Land/Homeowner perceptions of fire risk and responsibility in the wildland-urban interface. Hum. Ecol. Rev. 2007, 14, 177–187. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sample * N = 496 | Population ** N = 71,590 | |||

|---|---|---|---|---|

| Background of the participants | Freq. | % | Freq. | % |

| Gender n = 480 | ||||

| Male | 244 | 50 | 38,555 | 54 |

| Female | 236 | 48 | 33,040 | 46 |

| Other | 2 | 0.4 | ||

| Age groups n = 465 | ||||

| <25 | 3 | 0.65 | 22,215 | 31 |

| 25–34 | 70 | 15 | 16,555 | 23 |

| 35–44 | 146 | 31 | 13,110 | 18 |

| 45–54 | 130 | 28 | 10,855 | 15 |

| 55–64 | 81 | 17 | 6930 | 10 |

| 65–74 | 32 | 7 | 1470 | 2 |

| >75 | 3 | 0.6 | 480 | 0.6 |

| Education n = 487 | ||||

| Some grade school or high school education | 5 | 1 | 3470 | 7 |

| High school graduate | 59 | 12 | 12,810 | 27 |

| Some post-secondary education | 57 | 12 | *** | |

| College or trades certificate or diploma | 180 | 37 | 21,770 | 46 |

| University or post-graduate certificate, diploma or degree | 186 | 38 | 10,305 | 22 |

| Employment status n = 496 | ||||

| Full-time paid employment | 317 | 64 | 31,005 | 54 |

| Part-time paid employment | 34 | 7 | 15,470 | 27 |

| Self-employed | 39 | 8 | 2260 | 10 |

| Unemployed | 20 | 4 | 3115 | 6 |

| Retired | 59 | 12 | 1955 | 3 |

| Domestic parenting duties | 35 | 7 | *** | |

| Household Income n = 441 | ||||

| Less than $40,000 | 11 | 3 | 2010 | 8 |

| $40,001–$60,000 | 13 | 3 | 1015 | 4 |

| $60,001–$80,000 | 12 | 3 | 1150 | 4 |

| $80,001–$100,000 | 34 | 8 | 1230 | 5 |

| More than $10,000 | 371 | 84 | 20,255 | 79 |

| Perception of Risk Variables | Mean | Standard Deviation |

|---|---|---|

| a How likely is it you will experience damage to your property from wildfires within in the next 5 years | 3.3 | 1.6 |

| b How likely is it there will be a wildfire near by/in surrounding city’s environ within the next 5 years | 4.1 | 1.5 |

| c How controllable are wildfires in terms of people’s ability to control the effects | 4.6 | 1.7 |

| d How likely is it firefighters could protect your home if it were threatened by a wildfire | 3.7 | 1.1 |

| e Threat is not significant enough to warrant mitigation | 2.7 | 1.0 |

| f Wildfires are too destructive to bother preparing for | 2.0 | 0.8 |

| Variables | * Perception of Risk to Property from Wildfires Over the Next Five Years | t-Value | |

|---|---|---|---|

| Mean | Standard Deviation | ||

| Gender | 0.007 *** | ||

| Male | 3.1 | 1.5 | |

| Female | 3.6 | 1.6 | |

| Experience with the 2016 Fort McMurray wildfire | 0.7 | ||

| Direct experience ** | 3.3 | 1.5 | |

| No experience | 3.4 | 1.9 | |

| Length of residency | 0.1 | ||

| <10 years | 3.5 | 1.6 | |

| >10 years | 3.3 | 1.6 | |

| Vegetation Managementand Fuel-Reduction Activities | Yes | No | |||

|---|---|---|---|---|---|

| Frequency | % | Frequency | % | N | |

| In the past year, I have kept my rain gutters and roof free of leaves, needles, and branches for reasons that include protecting my home from wildfires. | 385 | 78% | 107 | 22% | 492 |

| In the past year, I have cleared the area within 10 m of my house of flammable trees, other vegetation, and combustible materials for reasons that include protecting my home from wildfires. | 277 | 56% | 218 | 44% | 495 |

| In the past year, I have kept my tree limbs pruned at least 2 m from the ground and have spaced my trees 3 m apart for reasons that include protecting my home from wildfires. | 293 | 60% | 203 | 41% | 496 |

| In the past year, I have moved woodpiles or other combustible materials more than 10 m from my home for reasons that include protecting my home from wildfires. | 291 | 60% | 202 | 40% | 493 |

| In the past year, I have cleaned up fallen branches, dry grass, and needles from within 10 m of my home for reasons that include protecting my home from wildfires. | 401 | 81% | 94 | 19% | 495 |

| In the past year, I have done something not listed above in order to protect my home from wildfires. (Please list other wildfire protection measures you have taken in the past year.) | 129 | 26% | 363 | 74% | 492 |

| Mean a | SD | Agree b | Disagree c | |

|---|---|---|---|---|

| I need more information before I can complete some of these activities. | 2.8 | 0.9 | 28% | 40% |

| If I made all or some of the suggested changes, my family or neighbors would like it. | 3.3 | 0.8 | 37% | 16% |

| I do not have the financial capacity to make these changes. | 2.6 | 1.1 | 19% | 51% |

| Implementing these activities is a priority for me. | 3.3 | 0.8 | 41% | 16% |

| For physical reasons I am unable to complete some of these activities without assistance. | 2.3 | 1.1 | 18% | 68% |

| I do not have the skills to complete some of these recommended activities. | 2.5 | 1.0 | 19% | 62% |

| If I made those changes I would not feel as connected to nature. | 2.4 | 1.0 | 16% | 62% |

| I do not consider the threat of wildfire significant enough to warrant doing some of these activities. | 2.6 | 1.0 | 24% | 48% |

| Wildfires are too destructive to bother preparing for. | 2.0 | 0.8 | 8% | 80% |

| If I made these changes, it would make firefighters’ jobs easier when responding to future wildfires. | 3.7 | 0.9 | 69% | 10% |

| Mean a | SD | Agree b | Disagree c | |

|---|---|---|---|---|

| Most people in my neighborhood take measures such as those listed above in order to protect their homes from wildfires. | 3.2 | 0.8 | 39% | 24% |

| Residents in my neighborhood work together to solve local problems. | 3.1 | 0.9 | 32% | 25% |

| Those who own rental properties in my neighborhood are equally interested in mitigating wildfire risk as other residents. | 2.7 | 1.0 | 20% | 11% |

| Seasonal residents in my neighborhood are equally interested in mitigating wildfire risk as other residents. | 2.7 | 0.9 | 15% | 37% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Asfaw, H.W.; Christianson, A.C.; Watson, D.O.T. Incentives and Barriers to Homeowners’ Uptake of FireSmart® Canada’s Recommended Wildfire Mitigation Activities in the City of Fort McMurray, Alberta. Fire 2022, 5, 80. https://doi.org/10.3390/fire5030080

Asfaw HW, Christianson AC, Watson DOT. Incentives and Barriers to Homeowners’ Uptake of FireSmart® Canada’s Recommended Wildfire Mitigation Activities in the City of Fort McMurray, Alberta. Fire. 2022; 5(3):80. https://doi.org/10.3390/fire5030080

Chicago/Turabian StyleAsfaw, Henok Workeye, Amy Cardinal Christianson, and David O T Watson. 2022. "Incentives and Barriers to Homeowners’ Uptake of FireSmart® Canada’s Recommended Wildfire Mitigation Activities in the City of Fort McMurray, Alberta" Fire 5, no. 3: 80. https://doi.org/10.3390/fire5030080

APA StyleAsfaw, H. W., Christianson, A. C., & Watson, D. O. T. (2022). Incentives and Barriers to Homeowners’ Uptake of FireSmart® Canada’s Recommended Wildfire Mitigation Activities in the City of Fort McMurray, Alberta. Fire, 5(3), 80. https://doi.org/10.3390/fire5030080