Investigation of Egyptian Banks’ Competition through a Riesz–Caputo Fractional Model

Abstract

:1. Introduction

2. Preliminaries

- -

- It is more general than the Caputo fractional derivative and can be easily transformed into the Caputo fractional derivative definition.

- -

- It sets a generalization to the Euler–Lagrange equation, as in (13), which is more general than the classical Euler–Lagrange equation.

- -

- It transforms into a Riesz fractional derivative in the same interval, while the left Caputo derivative transforms into the right Caputo and vice versa, and this can be easily proved using fractional integration by parts rules in [24].

3. Governing Model

3.1. Stability Analysis and Equilibrium Points

3.2. Existence and Uniqueness

4. Optimal Control of Banks’ Profits

5. Numerical Solution Procedure

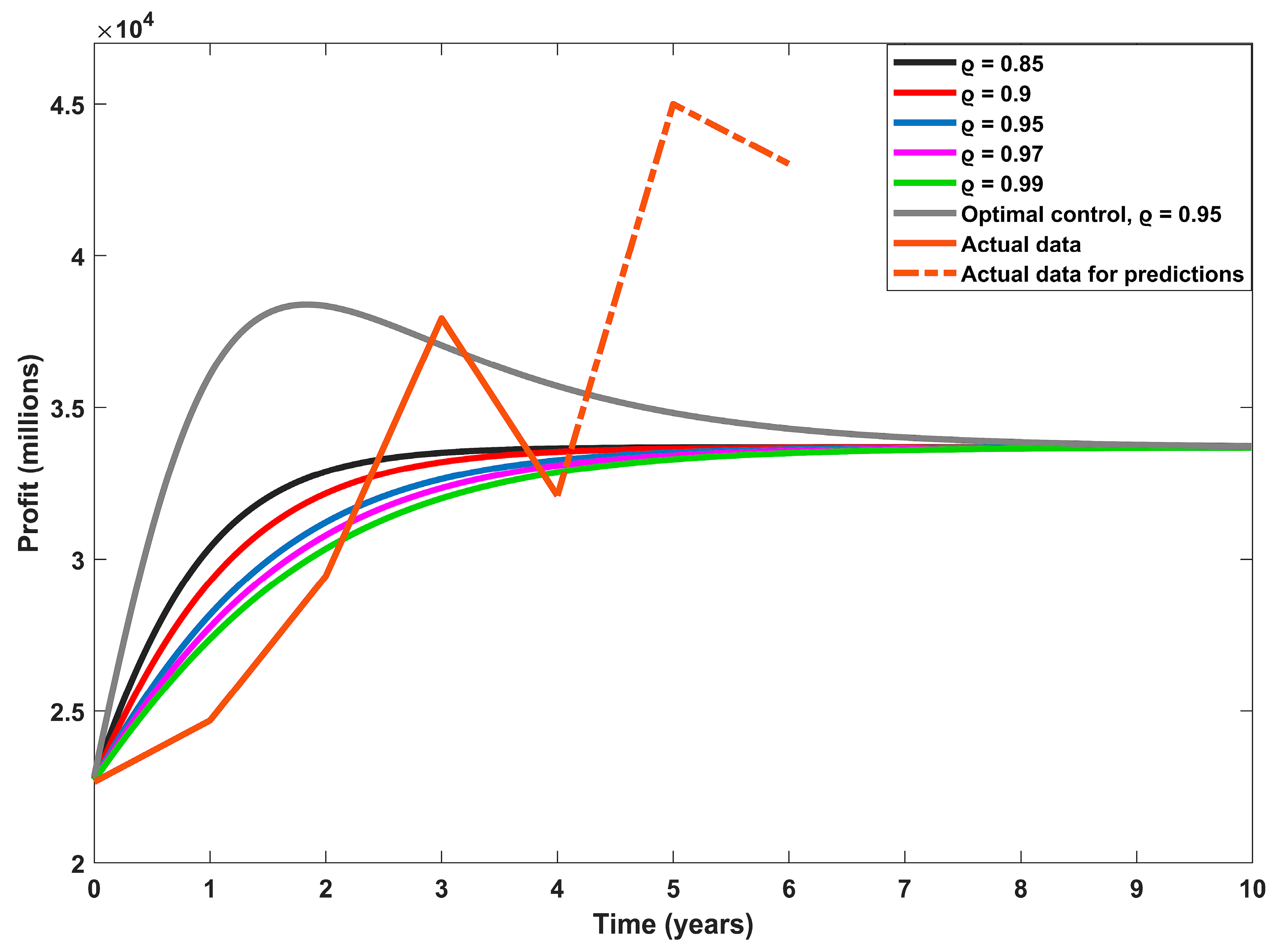

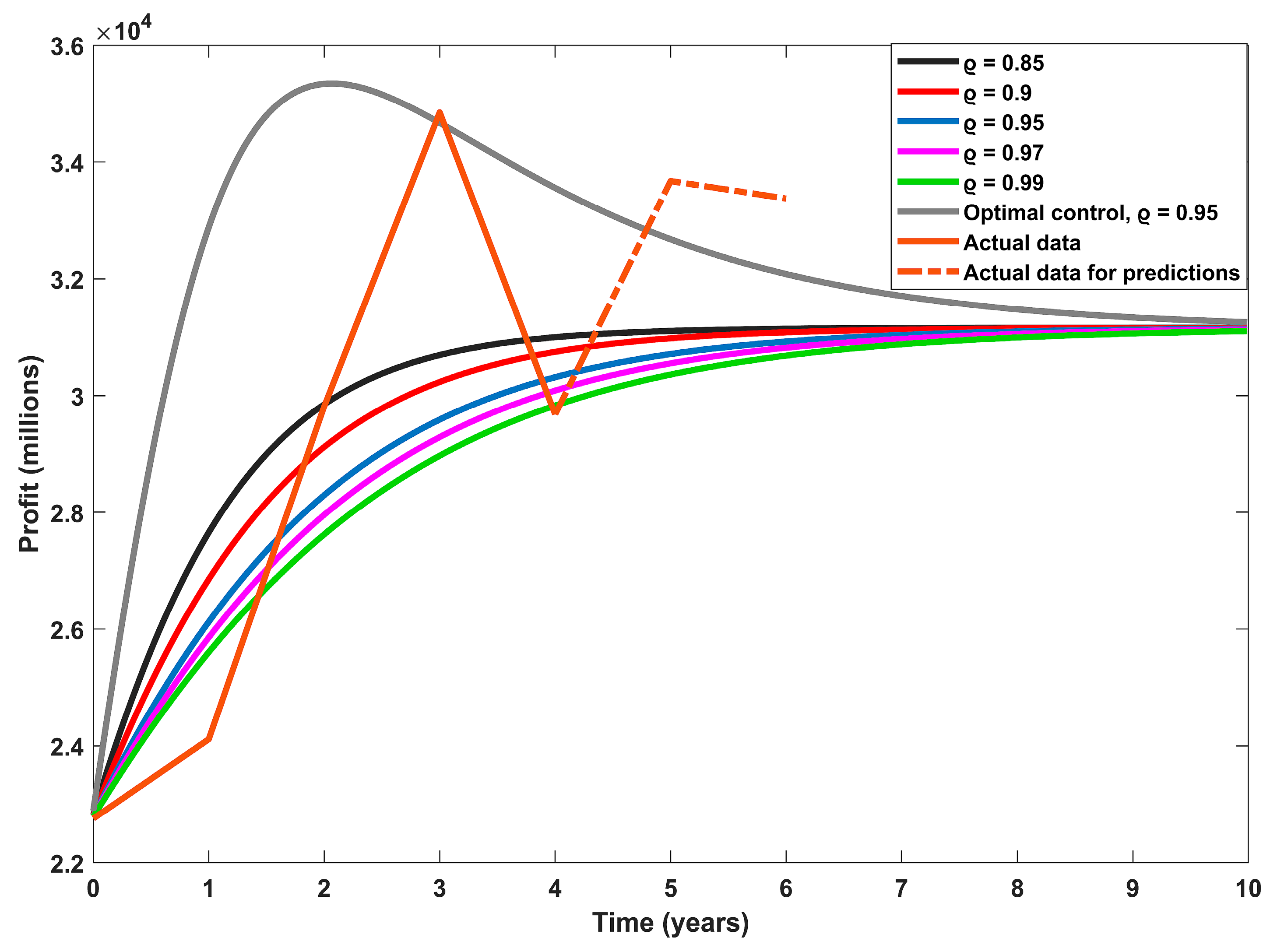

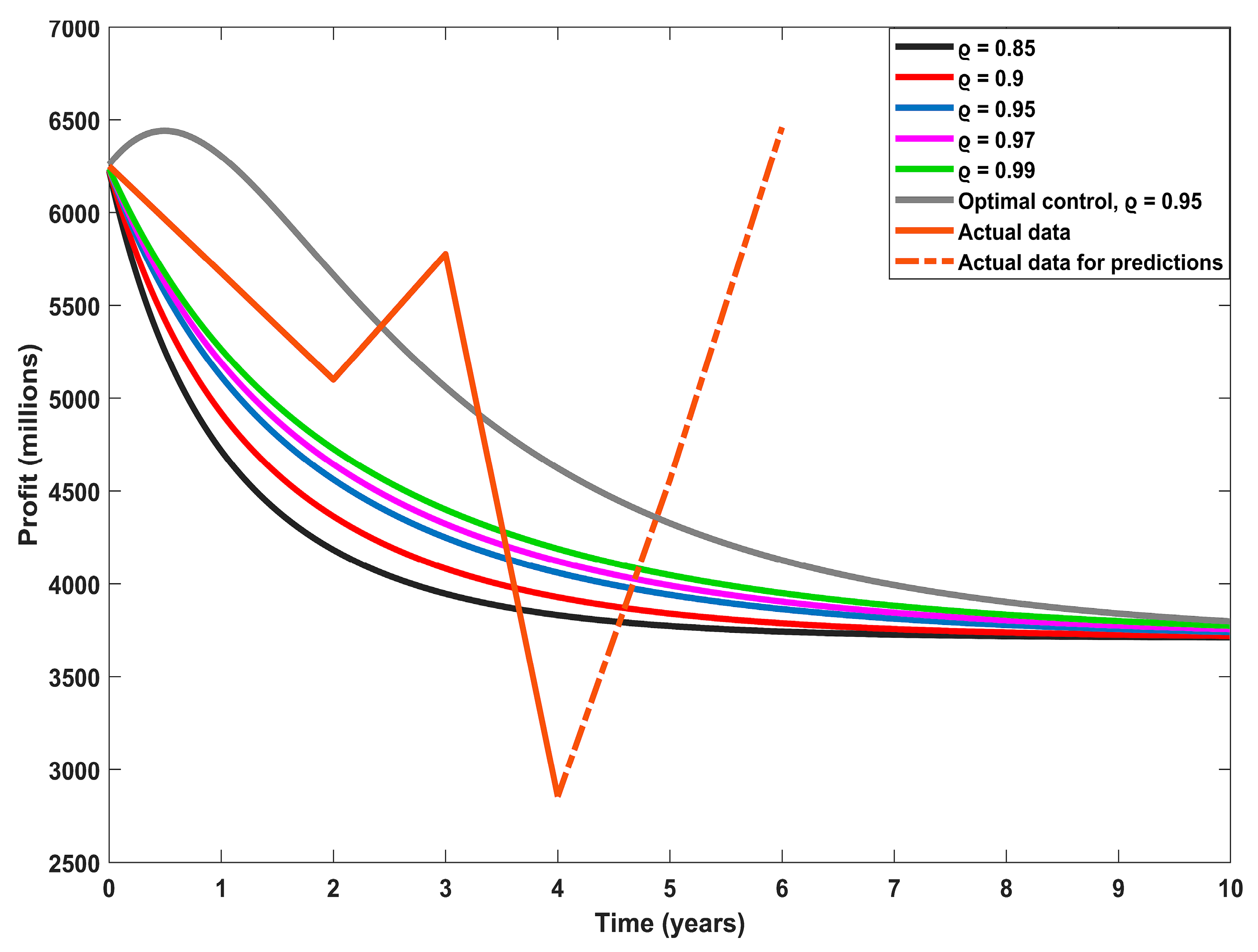

6. Results and Discussion

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Kahshan, M.; Lu, D.; Rahimi-Gorji, M. Hydrodynamical study of flow in a permeable channel: Application to flat plate dialyzer. Int. J. Hydrog. Energy 2019, 44, 17041–17047. [Google Scholar] [CrossRef]

- Uddin, S.; Mohamad, M.; Rahimi-Gorji, M.; Roslan, R.; Alarifi, I.M. Fractional electro-magneto transport of blood modeled with magnetic particles in cylindrical tube without singular kernel. Microsyst. Technol. 2019, 26, 405–414. [Google Scholar] [CrossRef]

- Michalakelis, C.; Christodoulos, C.; Varoutas, D.; Sphicopoulos, T. Dynamic estimation of markets exhibiting a prey–predator behavior. Expert Syst. Appl. 2012, 39, 7690–7700. [Google Scholar] [CrossRef]

- Lakka, S.; Michalakelis, C.; Varoutas, D.; Martakos, D. Competitive dynamics in the operating systems market: Modeling and policy implications. Technol. Forecast. Soc. Chang. 2013, 80, 88–105. [Google Scholar] [CrossRef]

- Atangana, A.; Gómez-Aguilar, J.F. Numerical approximation of riemann-liouville definition of fractional derivative: From riemann-liouville to atangana-baleanu. Numer. Methods Partial Differ. Equ. 2018, 34, 1502–1523. [Google Scholar] [CrossRef]

- Saad, K.M.; Khader, M.M.; Gómez-Aguilar, J.F.; Baleanu, D. Numerical solutions of the fractional fishers type equations with atangana-baleanu fractional derivative by using spectral collocation methods. Chaos Interdiscip. J. Nonlinear Sci. 2019, 29, 023116. [Google Scholar] [CrossRef]

- Solis-Perez, J.E.; Gómez-Aguilar, J.F. Variable-order fractalfractional time delay equations with power, exponential and mittag-leffler laws and their numerical solutions. Eng. Comput. 2020, 38, 555–577. [Google Scholar] [CrossRef]

- Safdari, H.; Aghdam, Y.E.; Gómez-Aguilar, J.F. Shifted chebyshev collocation of the fourth kind with convergence analysis for the space–time fractional advection-diffusion equation. Eng. Comput. 2020, 38, 1409–1420. [Google Scholar] [CrossRef]

- Atangana, A.; Gómez-Aguilar, J.F. Decolonisation of fractional calculus rules: Breaking commutativity and associativity to capture more natural phenomena. Eur. Phys. J. Plus 2018, 133, 166. [Google Scholar] [CrossRef]

- Gómez-Aguilar, J.F.; Yépez-Martínez, H.; Escobar-Jiménez, R.F.; Olivares-Peregrino, V.H.; Reyes, J.M.; Sosa, I.O. Series solution for the time-fractional coupled mkdv equation using the homotopy analysis method. Math. Probl. Eng. 2016, 2016, 7047126. [Google Scholar] [CrossRef]

- Omar, O.A.; Elbarkouky, R.A.; Ahmed, H.M. Fractional stochastic models for COVID-19: Case study of Egypt. Results Phys. 2021, 23, 104018. [Google Scholar] [CrossRef]

- Shikongo, A.; Nuugulu, S.M.; Elago, D.; Salom, A.T.; Owolabi, K.M. Fractional derivative operator on quarantine and isolation principle for COVID-19. In Advanced Numerical Methods for Differential Equations: Applications in Science and Engineering; Singh, H., Singh, J., Purohit, S.D., Kumar, D., Eds.; CRC Press: Boca Raton, FL, USA, 2021; pp. 205–226. [Google Scholar]

- Omar, O.A.; Alnafisah, Y.; Elbarkouky, R.A.; Ahmed, H.M. COVID-19 deterministic and stochastic modelling with optimized daily vaccinations in Saudi Arabia. Results Phys. 2021, 28, 104629. [Google Scholar] [CrossRef]

- Lu, J.; Ma, L. Numerical analysis of a fractional nonlinear oscillator with coordinate-dependent mass. Results Phys. 2022, 43, 106108. [Google Scholar] [CrossRef]

- Kumar, S.; Ghosh, S.; Samet, B.; Goufo, E.F.D. An analysis for heat equations arises in diffusion process using new Yang-Abdel-Aty-Cattani fractional operator. Math. Methods Appl. Sci. 2020, 43, 6062–6080. [Google Scholar] [CrossRef]

- Fatmawati; Khan, M.A.; Azizah, M.; Windarto; Ullah, S. A fractional model for the dynamics of competition between commercial and rural banks in Indonesia. Chaos Solitons Fractals 2019, 122, 32–46. [Google Scholar] [CrossRef]

- Wang, W.; Khan, M.A. Analysis and numerical simulation of fractional model of bank data with fractal-fractional atangana-baleanu derivative. J. Comput. Appl. Math. 2019, 369, 112646. [Google Scholar] [CrossRef]

- Gong, X.; Fatmawati; Khan, M.A. A new numerical solution of the competition model among bank data in caputo-fabrizio derivative. Alex. Eng. J. 2020, 59, 2251–2259. [Google Scholar] [CrossRef]

- Li, Z.; Liu, Z.; Khan, M.A. Fractional investigation of bank data with fractal-fractional caputo derivative. Chaos Solitons Fractals 2020, 131, 109528. [Google Scholar] [CrossRef]

- Qureshi, S.; Atangana, A. Mathematical analysis of dengue fever outbreak by novel fractional operators with field data. Phys. A Stat. Mech. Appl. 2019, 526, 121–127. [Google Scholar] [CrossRef]

- Qureshi, S.; Yusuf, A. Fractional derivatives applied to mseir problems: Comparative study with real world data. Eur. Phys. J. Plus 2019, 134, 171. [Google Scholar] [CrossRef]

- Central Bank of Egypt (CBE). Available online: https://www.cbe.org.eg/en/Pages/default.aspx (accessed on 10 February 2023).

- Kilbas, A.A.; Trujillo, J.J.; Srivastava, H.M. Theory and Applications of Fractional Differential Equations; Elsevier: Amsterdam, The Netherlands, 2006. [Google Scholar]

- Agrawal, O.P. Fractional variational calculus in terms of Riesz fractional derivatives. J. Phys. A 2007, 40, 6287–6303. [Google Scholar] [CrossRef]

- Zhu, C.; Yin, G. On competitive Lotka–Volterra model in random environments. J. Math. Anal. Appl. 2009, 357, 154–170. [Google Scholar] [CrossRef]

- Comes, C.A. Banking system: Three level Lotka-Volterra model. Procedia Econ. Finance 2012, 3, 251–255. [Google Scholar] [CrossRef]

- Omar, O.A.; Elbarkouky, R.A.; Ahmed, H.M. Fractional stochastic modelling of COVID-19 under wide spread of vaccinations: Egyptian case study. Alex. Eng. J. 2022, 61, 8595–8609. [Google Scholar] [CrossRef]

- Precup, R. Theorems of Leray-Schauder Type and Applications; CRC Press: Boca Raton, FL, USA, 2002. [Google Scholar]

- Ye, H.; Gao, J.; Ding, Y. A generalized Gronwall inequality and its application to a fractional differential equation. J. Math. Anal. Appl. 2007, 328, 1075–1081. [Google Scholar] [CrossRef]

- Sharp, R.S.; Peng, H. Vehicle dynamics applications of optimal control theory. Veh. Syst. Dyn. 2011, 49, 1073–1111. [Google Scholar] [CrossRef]

- Atangana, A.; Owolabi, K.M. New numerical approach for fractional differential equations. Math. Model. Nat. Phenom. 2021, 16, 47. [Google Scholar] [CrossRef]

- Biala, T.; Jator, S.N. Block backward differentiation formulas for fractional differential equations. Int. J. Eng. Math. 2015, 2015, 650425. [Google Scholar] [CrossRef]

- Zabidi, N.A.; Majid, Z.A.; Kilicman, A.; Ibrahim, Z.B. Numerical solution of fractional differential equations with Caputo derivative by using numerical fractional predict–correct technique. Adv. Contin. Discret. Model. 2022, 2022, 26. [Google Scholar] [CrossRef]

- FirstBank Indicator. Indicators of Financial Performance of Egyptian Banks. Available online: https://www.firstbankeg.com (accessed on 9 June 2023).

- Almal Daily Egyptian Newspaper. Available online: https://almalnews.com (accessed on 9 June 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter Name | Symbol | Estimated Value |

|---|---|---|

| Public banks’ growth rate | 0.7 | |

| Private and Arab banks’ growth rate | 0.5 | |

| Foreign banks’ growth rate | 0.45 | |

| Investment collaboration banks’ growth rate | 0.3 | |

| Public banks’ max. profit | 33,696 | |

| Private and Arab banks’ max. profit | 31,162 | |

| Foreign banks’ max. profit | 11,679 | |

| Investment collaboration banks’ max. profit | 3710 | |

| Public banks’ competition parameter | 1.9 10−18 | |

| Private and Arab banks’ competition parameter | 2.3 10−18 | |

| Foreign banks’ competition parameter | 1.02 10−18 | |

| Investment collaboration competition parameter | 5 10−18 | |

| Public banks’ max. level of investment | 0.392 | |

| Private and Arab banks’ max. level of investment | 0.327 | |

| Foreign banks max. level of investment | 0.245 | |

| Investment collaboration banks’ max. level of investment | 0.295 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Omar, O.A.M.; Ahmed, H.M.; Hamdy, W. Investigation of Egyptian Banks’ Competition through a Riesz–Caputo Fractional Model. Fractal Fract. 2023, 7, 473. https://doi.org/10.3390/fractalfract7060473

Omar OAM, Ahmed HM, Hamdy W. Investigation of Egyptian Banks’ Competition through a Riesz–Caputo Fractional Model. Fractal and Fractional. 2023; 7(6):473. https://doi.org/10.3390/fractalfract7060473

Chicago/Turabian StyleOmar, Othman A. M., Hamdy M. Ahmed, and Walid Hamdy. 2023. "Investigation of Egyptian Banks’ Competition through a Riesz–Caputo Fractional Model" Fractal and Fractional 7, no. 6: 473. https://doi.org/10.3390/fractalfract7060473

APA StyleOmar, O. A. M., Ahmed, H. M., & Hamdy, W. (2023). Investigation of Egyptian Banks’ Competition through a Riesz–Caputo Fractional Model. Fractal and Fractional, 7(6), 473. https://doi.org/10.3390/fractalfract7060473