Living on the Edge: The Precariat Amid the Rental Crisis in the Metropolitan Area of Las Palmas de Gran Canaria (Spain)

, , and

, , and {kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Conceptual and Contextual Perspectives

2.1. The Two Faces of Housing: A Social Right or a Speculative Asset

2.2. Rental Market Situation in the European Union, Spain, and the Canary Islands

3. Sources and Methods

4. Results

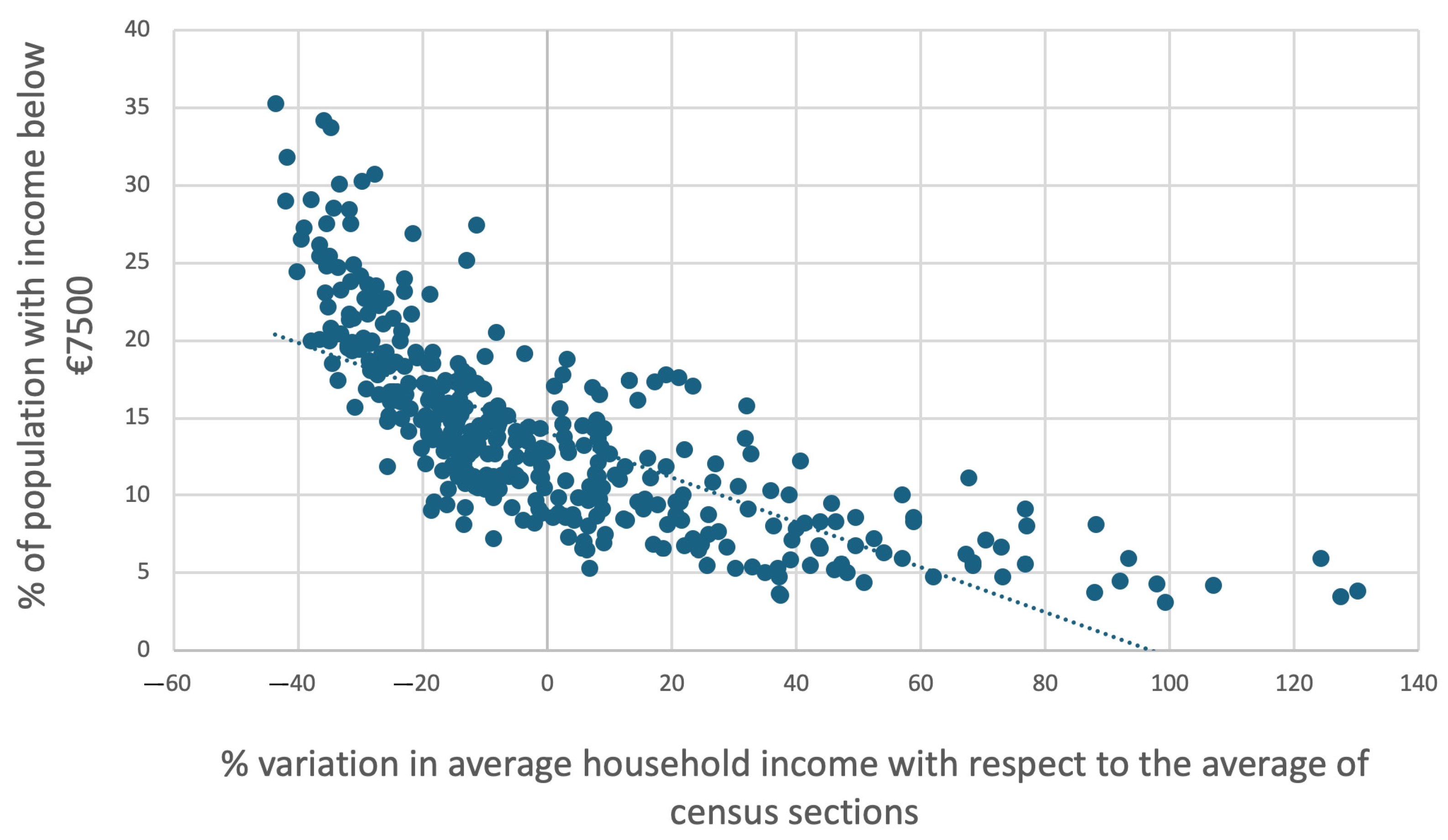

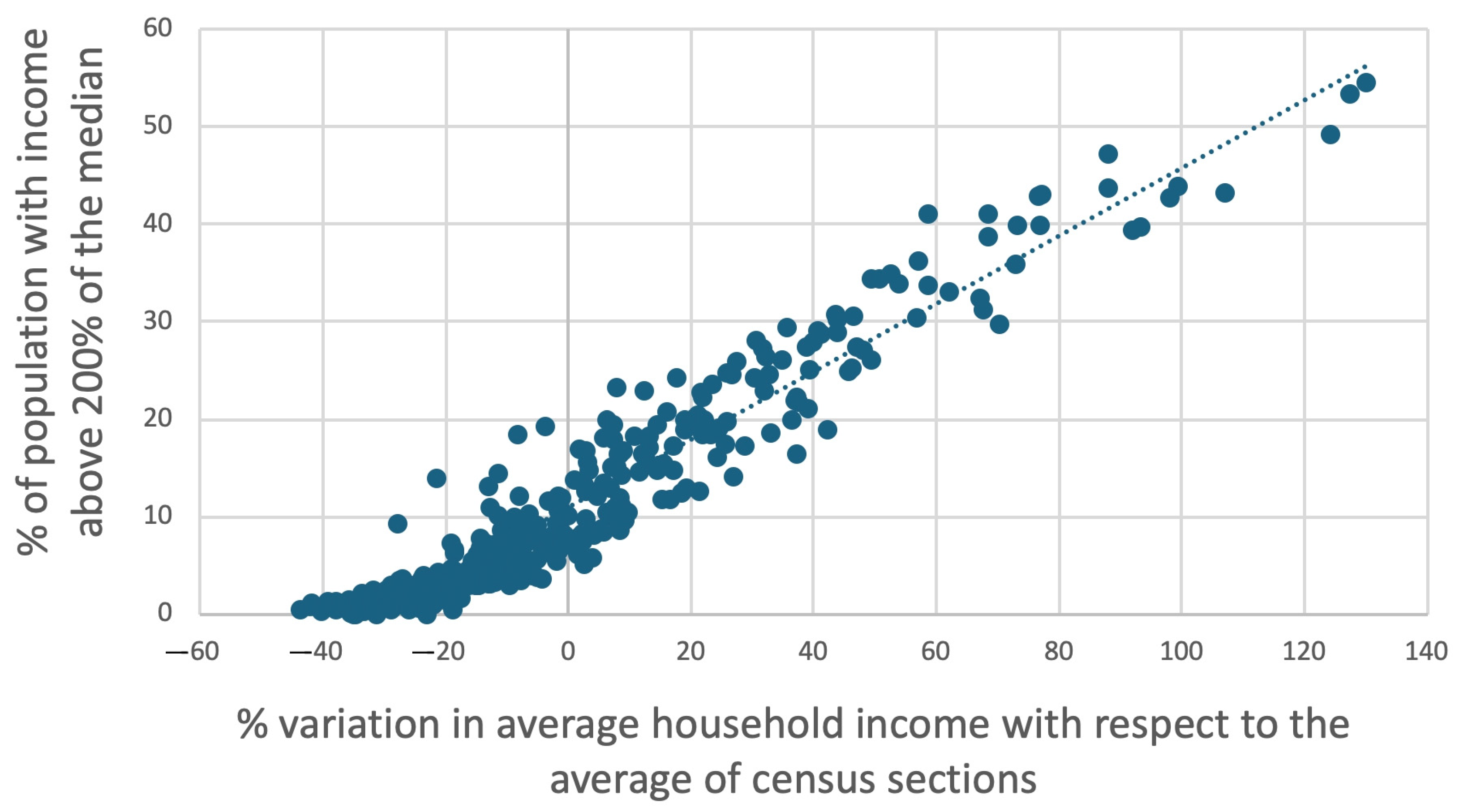

4.1. Income Distribution and Residential Rental Market

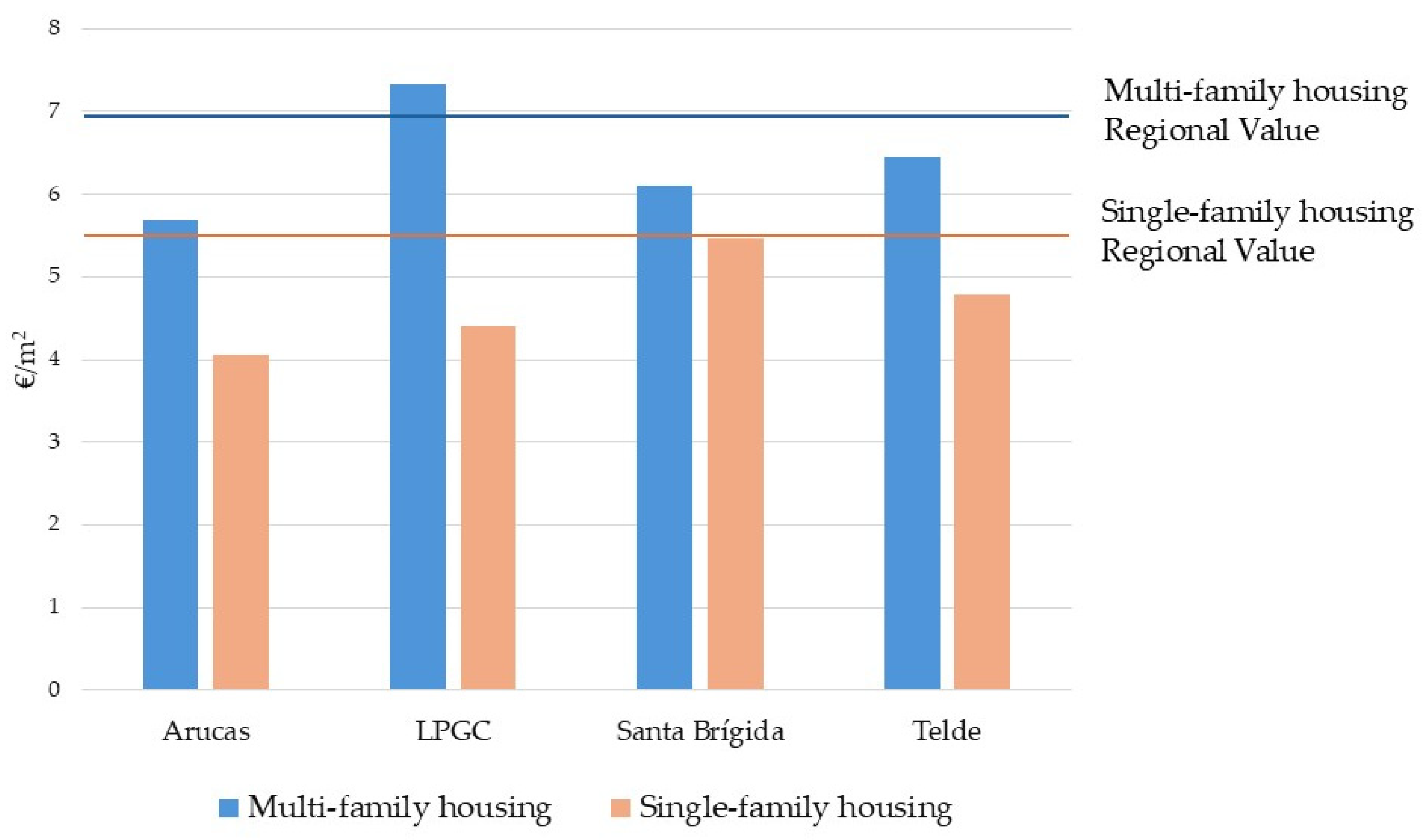

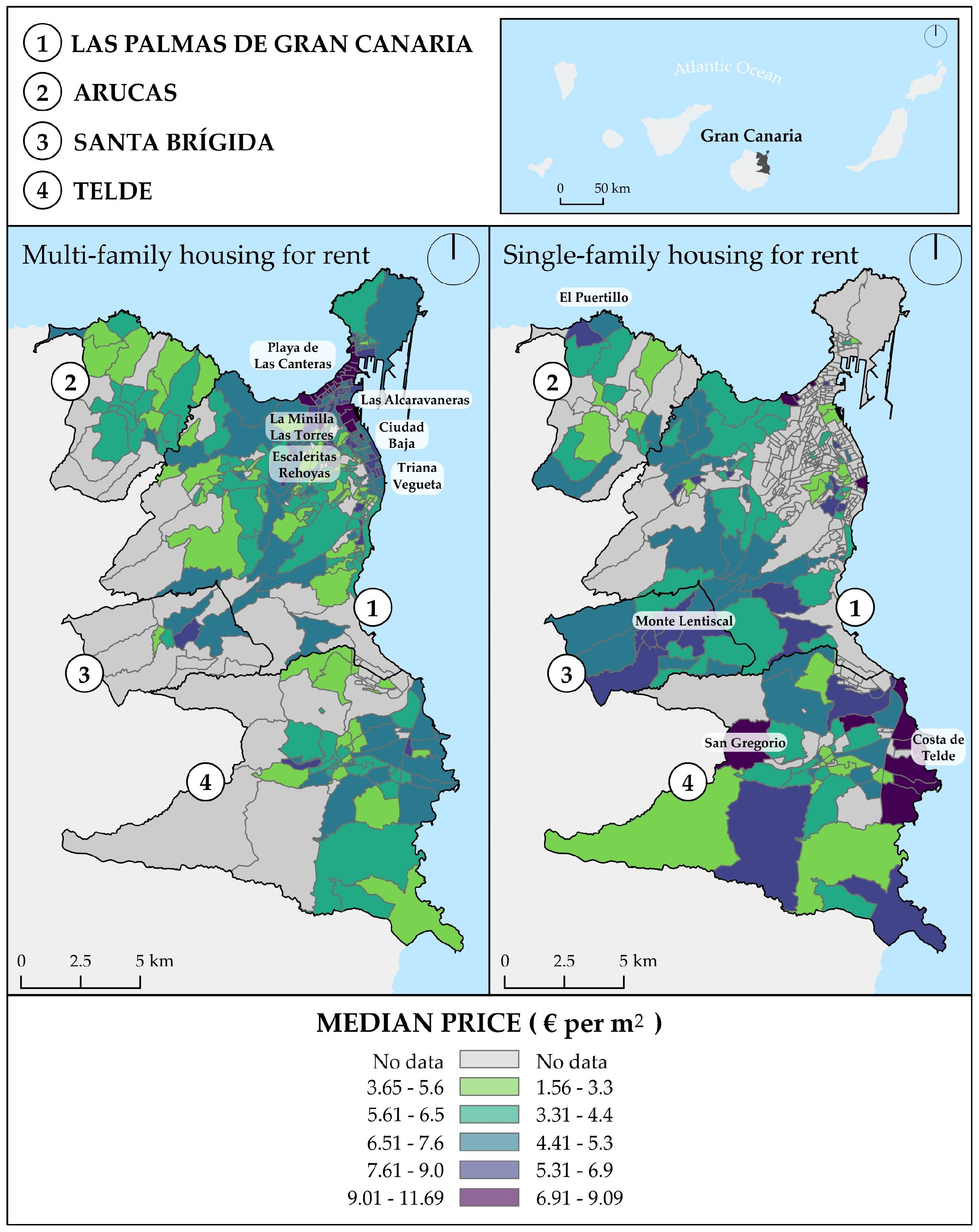

4.2. Rental Market Dynamics and Land Prices

4.3. Housing Affordability and Economic Effort in Access to Rental Housing

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Arundel, R.; Torrado, J.M.; Duque-Calvache, R. The spatial polarization of housing wealth accumulation across Spain. Environ. Plan. A Econ. Space 2024, 56, 1686–1709. [Google Scholar] [CrossRef]

- Nasrabadi, M.T.; Larimian, T.; Timmis, A.; Yigitcanlar, T. Mapping four decades of housing inequality research: Trends, insights, knowledge gaps, and research directions. Sustain. Cities Soc. 2024, 113, 105693. [Google Scholar] [CrossRef]

- Dewilde, C.; Lancee, B. Income Inequality and Access to Housing in Europe. Eur. Sociol. Rev. 2013, 29, 1189–1200. [Google Scholar] [CrossRef]

- Ben-Shahar, D.; Warszawski, J. Inequality in housing affordability: Measurement and estimation. Urban Stud. 2015, 53, 1–25. [Google Scholar] [CrossRef]

- Long, J.E.; Rasmussen, D.W.; Haworth, C.T. Income Inequality and City Size. Rev. Econ. Stat. 1977, 59, 244–246. [Google Scholar] [CrossRef]

- Baum-Snow, N.; Pavan, R. Inequality and City Size. Rev. Econ. Stat. 2013, 95, 1535–1548. Available online: http://www.jstor.org/stable/43554846 (accessed on 17 January 2025). [CrossRef]

- Hilman, R.M.; Iñiguez, G.; Karsai, M. Socioeconomic biases in urban mixing patterns of US metropolitan areas. EPJ Data Sci. 2022, 11, 32. [Google Scholar] [CrossRef]

- Standing, G. El Precariado: Una Nueva Clase Social, 2nd ed.; Editorial Pasado y Presente: Barcelona, Spain, 2013; p. 302. ISBN 9788494100819. [Google Scholar]

- Hey, A.P.; Grimaldi, A.I. New Class Divisions? Elites and the Precariat at the Extremes of Social Class in the UK. Rev. Bras. Ciênc. Soc. 2019, 34. [Google Scholar] [CrossRef]

- Oh, D.Y.; Park, J.; Kim, H.S. Emerging trends in housing policy in the UK: Focusing on its ongoing neoliberal transformation since 2010. Space Soc. 2015, 25, 227–266. [Google Scholar] [CrossRef]

- Di Feliciantonio, C.; Aalbers, M.B. The Prehistories of Neoliberal Housing Policies in Italy and Spain and Their Reification in Times of Crisis. Hous. Policy Debate 2017, 28, 135–151. [Google Scholar] [CrossRef]

- Macho Carro, A. El examen de proporcionalidad de los desalojos forzosos y su recepción en el ordenamiento español. Rev. Derecho Político 2023, 116, 297–335. [Google Scholar] [CrossRef]

- Biblioteca del Congreso Nacional de Chile. Comparador de Constituciones del Mundo: Derecho a la Vivienda. Available online: https://www.bcn.cl/procesoconstituyente/comparadordeconstituciones/materia/shelter (accessed on 6 November 2024).

- Sánchez Ballesteros, V. Los límites de la función social de la propiedad en la modelización de las facultades del propietario como garantía de acceso a la vivienda digna para todos y la libertad de empresa. Rev. Derecho Civ. 2023, 10, 141–174. Available online: https://www.nreg.es/ojs/index.php/RDC/article/view/832 (accessed on 23 January 2025).

- Image by Víctor Jiménez Barrado (a), and EFE Agency (b), 2024.

- Wang, X.-R.; Hui, E.C.-M.; Sun, J.-X. Population migration, urbanization and housing prices: Evidence from the cities in China. Habitat Int. 2017, 66, 49–56. [Google Scholar] [CrossRef]

- Arancibia, A. The Lifestyles of Space Standards: Concepts and Design Problems. Urban Plan. 2024, 9, 7800. [Google Scholar] [CrossRef]

- Luo, Y.; Chen, R.; Xiong, B.; Jia, N.; Guo, X.; Yin, C.; Song, W. The Impact of Household Dynamics on Land-Use Change in China: Past Experiences and Future Implications. Land 2024, 13, 124. [Google Scholar] [CrossRef]

- Díaz Cuevas, P.; Fernández Tabales, A. De la función residencial a la función turística en los espacios urbanos: Medición de los factores causantes a partir de herramientas digitales. Boletín Asoc. Geógrafos Españoles 2023, 99, 1–30. [Google Scholar] [CrossRef]

- McElroy, E. Digital nomads in siliconising Cluj: Material and allegorical double dispossession. Urban Stud. 2019, 57, 3078–3094. [Google Scholar] [CrossRef]

- Parreño Castellano, J.M.; Domínguez Mujica, J.; Moreno Medina, C. Reflections on Digital Nomadism in Spain during the COVID-19 Pandemic—Effect of Policy and Place. Sustainability 2022, 14, 16253. [Google Scholar] [CrossRef]

- Guerreiro, I.A.; Rolnik, R.; Marín-Toro, A. Gestão neoliberal da precariedade: O aluguel residencial como nova fronteira de financeirização da moradia. Cad. Metrópole 2022, 24, 451–475. [Google Scholar] [CrossRef]

- Banco de España-BdE. El mercado del alquiler de vivienda residencial en España: Evolución reciente, determinantes e indicadores de esfuerzo. In Documentos Ocasionales 2432; Banco de España: Madrid, Spain, 2024; pp. 1–50. [Google Scholar]

- Acioly, C.; Madhuraj, A. The Housing Rights Index: A Policy Formulation Support Tool; United Nations Human Settlements Programme-UN-Habitat: Nairobi, Kenya, 2018; p. 25. Available online: https://unhabitat.org/sites/default/files/2020/01/housing_rights_index_jan_7_low_resolution.pdf (accessed on 16 January 2025).

- López Ramón, F. El derecho subjetivo a la vivienda. Rev. Española Derecho Const. 2014, 102, 49–91. Available online: https://www.jstor.org/stable/2488729 (accessed on 21 January 2025).

- Castelo Vargas, B.A. Configuración constitucional do dereito á vivenda. Cad. Dereito Actual 2013, 1, 29–36. Available online: https://www.cadernosdedereitoactual.es/index.php/cadernos/article/view/2 (accessed on 31 January 2025).

- Barragán Robles, V.; Rodríguez Súárez, N.; Abellán Muñoz, J.C. Tenemos derecho, reivindicamos vivienda. La mercantilización como límite de los derechos humanos. Cuad. Relac. Laborales 2020, 38, 339–363. [Google Scholar] [CrossRef]

- Debruche, A.F. Le droit au logement au Brésil: Entre intervention gouvernementale et théorie civile-constitutionnelle engagée. Les Cah. Droit 2020, 61, 331–352. [Google Scholar] [CrossRef]

- Dall’Igna Ecker, D. Desnaturalizando o Direito Social à moradia no Brasil: Ocupações urbanas como estratégia de assistência ao social. Diálogo 2021, 46, 1–13. [Google Scholar] [CrossRef]

- Kurlat Aimar, J.S. El derecho a la vivienda en la jurisprudencia de la ciudad autónoma de Buenos Aires. Glosas hacia su reconocimiento pretoriano. Rev. Fac. Derecho 2021, 51, 1–46. [Google Scholar] [CrossRef]

- Lee, S.; Choeh, J.Y. Exploring the influence of online word-of-mouth on hotel booking prices: Insights from regression and ensemble-based machine learning methods. Data Sci. Financ. Econ. 2024, 4, 65–82. [Google Scholar] [CrossRef]

- Huerta Núñez, A.; Bélanger, H. Las desigualdades sociales y urbanas en la Ciudad de México: ¿Dónde queda el derecho a la vivienda? Kultur 2020, 7, 117–136. [Google Scholar] [CrossRef]

- Rubens Cenci, D.; Seffrin, G. Mercantilização do espaço urbano e suas implicações na concepção de cidades justas, democráticas, inclusivas e humanas. Rev. Direito Cidade 2019, 11, 418–442. [Google Scholar] [CrossRef]

- Li, Z.; Guo, F.; Du, Z. Learning from Peers: How Peer Effects Reshape the Digital Value Chain in China? J. Theor. Appl. Electron. Commer. Res. 2025, 20, 41. [Google Scholar] [CrossRef]

- Gil, J.; Martínez, P.; Sequera, J. The neoliberal tenant dystopia: Digital polyplatform rentierism, the hybridization of platform-based rental markets and financialization of housing. Cities 2023, 137, 104245. [Google Scholar] [CrossRef]

- Majerowitz, M.; Allweil, Y. Housing in the Neoliberal City: Large Urban Developments and the Role of Architecture. Urban Plan. 2019, 4, 43–61. [Google Scholar] [CrossRef]

- Mozo Carollo, I.; Morandeira-Arca, J.; Etxezarreta-Etxarri, A.; Izagirre-Olaizola, J. Is the effect of Airbnb on the housing market different in medium-sized cities? Evidence from a Southern European city. Urban Res. Pract. 2023, 17, 260–279. [Google Scholar] [CrossRef]

- Garay-Tamajón, L.; Lladós-Masllorens, J.; Meseguer-Artola, A.; Morales-Pérez, S. Analyzing the influence of short-term rental platforms on housing affordability in global urban destination neighborhoods. Tour. Hosp. Res. 2022, 22, 444–461. [Google Scholar] [CrossRef]

- Biljanovska, N.; Fu, C.; Igan, D. Housing Affordability: A New Dataset. IMF Working Paper, WP/23/247; International Monetary Fund: Washington, DC, USA, 2023; p. 33. [Google Scholar]

- Tulumello, S.; Dagkouli-Kyriakoglou, M. Housing Financialization and the State, in and Beyond Southern Europe: A Conceptual and Operational Framework. Hous. Theory Soc. 2024, 41, 192–215. [Google Scholar] [CrossRef]

- Kenyon, G.E.; Arribas-Bel, D.; Robinson, C.; Gkountouna, O.; Arbués, P.; Rey-Blanco, D. Intra-urban house prices in Madrid following the financial crisis: An exploration of spatial inequality. Npj Urban Sustain. 2024, 4, 26. [Google Scholar] [CrossRef]

- Muñoz, E.; López Martínez, A.; Ruíz Arias, M. Financiarización de la vivienda para alquiler y la precarización de las familias de bajos ingresos en Medellín (Colombia). Boletín Asoc. Geógrafos Españoles 2023, 96, 1–38. [Google Scholar] [CrossRef]

- DesBaillets, D.; Hamill, S.E. Coming in from the Cold: Canada’s National Housing Strategy, Homelessness, and the Right to Housing in a Transnational Perspective. Can. J. Law Soc./Rev. Can. Droit Société 2022, 37, 273–293. [Google Scholar] [CrossRef]

- Beaubrun-Diant, K.; Maury, T. Implications of homeownership policies on land prices: The case of a French experiment. Econ. Bul. 2021, 41, 1256–1265. Available online: https://www.accessecon.com/Pubs/EB/2021/Volume41/EB-21-V41-I3-P106.pdf (accessed on 13 January 2025).

- Forns i Fernández, M.V. El paper dels serveis socials locals en l’aplicació de les polítiques d’habitatge en un context de crisi de l’estat del benestar. Una mirada des de Catalunya. Rev. Catalana Dret Públic 2023, 66, 23–38. [Google Scholar] [CrossRef]

- Listerborn, C. The new housing precariat: Experiences of precarious housing in Malmö, Sweden. Hous. Stud. 2021, 38, 1304–1322. [Google Scholar] [CrossRef]

- Fernandes, E. Regularización de Asentamientos Informales en América Latina; Lincoln Institute of Land Policy: Boston, MA, USA, 2011; p. 52. ISBN 978-1-55844-202-3. [Google Scholar]

- Lima, V. The political frame of a housing crisis: Campaigning for the right to housing in Ireland. J. Civ. Soc. 2023, 19, 37–56. [Google Scholar] [CrossRef]

- Bonfert, B. “The real power must be in the base”—Decentralised collective intellectual leadership in the European Action Coalition for the Right to Housing and to the City. Cap. Cl. 2021, 45, 523–542. [Google Scholar] [CrossRef]

- Argelich Comelles, C. La nueva Ley por el derecho a la vivienda de España en el contexto europeo: Debilidades y fortalezas. THĒMIS Rev. Derecho 2023, 83, 107–119. [Google Scholar] [CrossRef]

- Housing Anywhere. Índice Internacional de Alquileres de HousingAnywhere del Segundo Trimestre de 2024. Available online: https://housinganywhere.com/es/indice-alquileres-segundo-trimestre-2024 (accessed on 25 November 2024).

- Martínez del Olmo, A. Dinámicas de los sistemas de vivienda en Europa: El caso de España. In Derecho a la Vivienda y a la Ciudad: Un Panorama; Garrido, R., Fernández Olit, B., Eds.; Economistas sin Fronteras, Dossieres EsF, 55: Madrid, Spain, 2024; pp. 7–13. Available online: https://ecosfron.org/wp-content/uploads/2024/10/Dossier-55_CAST.pdf (accessed on 1 February 2025).

- Eurostat. Housing Cost Overburden Rate by Tenure Status—EU-SILC Survey. 2024. Available online: https://ec.europa.eu/eurostat/databrowser/product/page/TESSI164 (accessed on 29 November 2024).

- Khametshin, D.; López Rodríguez, D.; Pérez García, L. El Mercado del Alquiler de Vivienda Residencial en España: Evolución Reciente, Determinantes e Indicadores de Esfuerzo. In Documentos Ocasionales 2432; Banco de España: Madrid, Spain, 2024; p. 66. [Google Scholar]

- Rodríguez-López, J. España: Mercado de vivienda, los precios crecen más que las ventas. Ciudad Territ. Estud. Territ. 2024, 222, 1409–1420. [Google Scholar] [CrossRef]

- Lajer Barón, A.; López Rodríguez, D.; San Juan, L. El Mercado de la Vivienda Residencial en España: Evolución Reciente y Comparación Internacional; Documentos Ocasionales 2433; Banco de España: Madrid, Spain, 2024; p. 43. Available online: https://repositorio.bde.es/handle/123456789/3787 (accessed on 8 January 2025).

- Carbó Valverde, S.; Rodríguez Fernández, F. El mercado de la vivienda en Europa: Viejas costumbres y nuevos desafíos. Cuad. Inf. Económica 2018, 266, 81–92. [Google Scholar]

- Macho Carro, A. Derecho a la vivienda y ordenación del mercado del alquiler turístico en la Unión Europea. Rev. Estud. Europeos 2022, 79, 668–686. [Google Scholar] [CrossRef]

- Blasco Redondo, A. Desarrollo de Una Aplicación para Facilitar la Convivencia en Pisos Compartidos. Master’s Thesis, Universitat Oberta de Catalunya, Barcelona, Spain, 2019; p. 50. Available online: http://hdl.handle.net/10609/9788 (accessed on 18 January 2025).

- Registro General Turístico de Canarias. Available online: https://datos.canarias.es/catalogos/general/dataset/establecimientos-extrahoteleros-de-tipologia-vivienda-vacacional-inscritos-en-el-registro (accessed on 25 November 2024).

- Kyle Barron, E.K.; Davide, P. The Effect of Home-Sharing on House Prices and Rents: Evidence from Airbnb. Mark. Sci. 2020, 40, 23–47. [Google Scholar] [CrossRef]

- Atlas de Distribución de la Renta en los Hogares. INE. Available online: https://www.ine.es/dyngs/Prensa/es/ADRH2022.htm (accessed on 28 November 2024).

- State Housing Rental Price Reference System-SERPAVI, Ministerio de Vivienda y Agenda Urbana. Available online: https://serpavi.mivau.gob.es (accessed on 15 November 2024).

- Castro Hernández, T.; Jiménez Barrado, V. ¡Barrios que gritan! Guanarteme como barómetro y brújula sociopolítica y urbanística. In La Ciudad “Veinte-Treinta” Miradas a los Espacios Urbanos del Siglo XXI; Andrés López, G., García Cuesta, J.L., Eds.; Asociación Española de Geografía: Valladolid, Spain, 2024; pp. 893–904. [Google Scholar] [CrossRef]

- Ortiz García, C.D. El turismo en los centros históricos de Canarias. Implicaciones en la vivienda. In La Vivienda en Canarias. Situación, Perspectivas y Propuestas; Parreño Castellano, J.M., Armas Díaz, A., Eds.; Fundación Fyde CajaCanarias: Santa Cruz de Tenerife, Spain, 2024; pp. 129–141. ISBN 978-84-09-66536-5. [Google Scholar] [CrossRef]

- Encuesta Anual de Estructura Salarial-INE. Available online: https://ine.es/jaxiT3/Datos.htm?t=28182 (accessed on 29 November 2024).

- Image by Claudio Moreno Medina.

- Idealista Real Estate Portal. Available online: https://www.idealista.com (accessed on 31 January 2025).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jiménez Barrado, V.; Hernández Luis, J.Á.; Ramón Ojeda, A.Á.; Moreno Medina, C. Living on the Edge: The Precariat Amid the Rental Crisis in the Metropolitan Area of Las Palmas de Gran Canaria (Spain). Urban Sci. 2025, 9, 156. https://doi.org/10.3390/urbansci9050156

Jiménez Barrado V, Hernández Luis JÁ, Ramón Ojeda AÁ, Moreno Medina C. Living on the Edge: The Precariat Amid the Rental Crisis in the Metropolitan Area of Las Palmas de Gran Canaria (Spain). Urban Science. 2025; 9(5):156. https://doi.org/10.3390/urbansci9050156

Chicago/Turabian StyleJiménez Barrado, Víctor, José Ángel Hernández Luis, Antonio Ángel Ramón Ojeda, and Claudio Moreno Medina. 2025. "Living on the Edge: The Precariat Amid the Rental Crisis in the Metropolitan Area of Las Palmas de Gran Canaria (Spain)" Urban Science 9, no. 5: 156. https://doi.org/10.3390/urbansci9050156

APA StyleJiménez Barrado, V., Hernández Luis, J. Á., Ramón Ojeda, A. Á., & Moreno Medina, C. (2025). Living on the Edge: The Precariat Amid the Rental Crisis in the Metropolitan Area of Las Palmas de Gran Canaria (Spain). Urban Science, 9(5), 156. https://doi.org/10.3390/urbansci9050156