2.1. ESTEA2—Model Structure

ESTEA2 is capable of modeling a single fermentation product to multiple end products, allowing a maximum of eight downstream unit operations for separation, catalytic conversion, and purification processes. Furthermore, new unit operations’ (drying, batch reactor) design and cost calculations are now included in the model. The capabilities of ESTEA2 were significantly improved by these added functionalities, and streamlining the model makes it easier for users to understand the data flow.

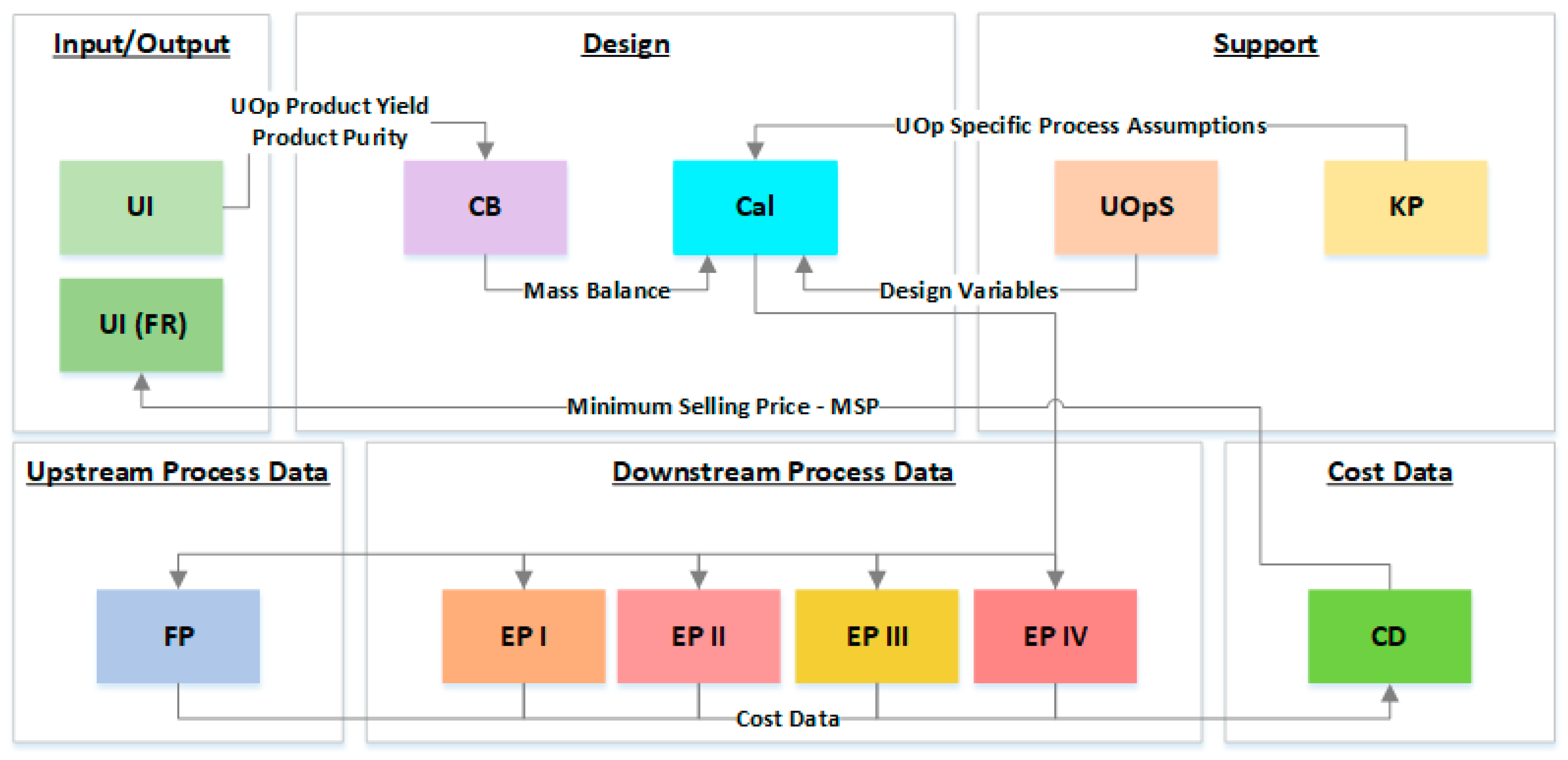

Table 1 and

Figure 1 summarize the structure and organization of ESTEA2. Based on functionality and role, the tool is divided into six brackets. The Input/Output bracket contains

Tab UI (User Interface), which serves as the front-end platform of the entire model. Here, the user controls the primary process parameters of the model. The Design bracket will include

Tab CB (Component Balance) and

Tab Cal (Calculations) for computations involving process modeling. The Downstream Process Data bracket comprises

Tab EP-I (End Product I),

Tab EP-II (End Product II),

Tab EP-III (End Product III), and

Tab EP-IV (End Product IV). The

Tabs EP-I‒IV integrate process the inputs, assumptions, design, and cost calculations of downstream unit operations involved with particular end products. For example, the downstream processing information for end product-I will be grouped and represented in

Tab EP-I. Similarly, Upstream Process Data bracket’s

Tab FP (Fermentation Process) displays all information related to the fermentation procedure. The

Tab CD of the Cost Data bracket is responsible for computations involving cost estimations. Here the expenditure per unit kg of product produced—i.e., the Minimum Selling Price (MSP)—is computed. This MSP estimate is reported in the Final Results section in

Tab UI. The Support bracket holds

Tab KP, which is the tool’s inventory comprising constants, unit conversions values, cost data for utilities and raw material, and process-specific assumptions. It provides unit operation specific information to the

Tab Cal and

Tab EPs. The other tab in the bracket is

Tab UOpS, containing all the information related to every individual unit operation. It performs the following operations: (1) Provide process variables for selected unit operations in

Tab UI; (2) Provide necessary process assumptions for respective unit operations from

Tab KP to perform design calculations in

Tab Cal; and (3) Create a data report table in

Tab EP for every end product.

The Tab UI is subdivided into Plant Properties, Fermentation, and Downstream and Final Results sections. First, the user provides the plant property information, including plant operating days, internal rate of return, and plant life, and chooses a Lang Factor. Then, the user provides values for the fermentation parameters of titer, productivity, and yield along with the fermented product density. As stated earlier, ESTEA2 is capable of handling downstream processing for multiple end products by catalytically converting fermentation products. ESTEA2 can handle up to four end products, all originating from the same fermentation system. The method for designing the downstream process happens in Tab UI, involving the following procedure: (1) Select the number of end products; (2) Specify the annual production and density for each end product; (3) Specify downstream unit operations details (separation/catalysis). Up to eight downstream processing options can be chosen for each end product. Once the unit operation or unit type is selected, the appropriate set of process parameters is displayed, and the user enters the requisite information.

After all the input information is provided, ESTEA2 performs mass balance calculations in Tab CB. Mass and volumetric flow rates for the entire process are calculated on an hourly basis. The end product flow rate (kg/h) is calculated using operating days (user input), assuming 24-h plant operation per day. The product yield value from Tab UI for every procedure/process is used to back-calculate product flow out of that unit operation.

Process input parameters from Tab UI, mass balance data from Tab CB, and other required process parameters (process assumptions) from Tab KP are utilized to perform process model calculations, which size each unit operation. The process design and mass balance calculations are performed in Tab Cal and Tab CB, respectively, for all end products’ downstream processing. Furthermore, they are methodically categorized for better understanding.

Tab EP-I–IV contain consolidated process details on each end product. Here, a data report is generated with information on process inputs, mass flows, process assumptions, and modeling calculation for end product downstream processing. The data report contains detailed design information subsectioned as follows: (1) Process Inputs—Unit operation-specific inputs provided by the user in Tab UI, (2) Process Assumptions—ESTEA2’s process-specific assumptions relevant to the respective unit operation, (3) Process Flows—Mass balance data from Tab CB, (4) Process Calculations—Stepwise unit operation design calculation (adapted from Tab Cal), (5) Cost Calculations—Unit operation cost calculations (direct cost) are performed.

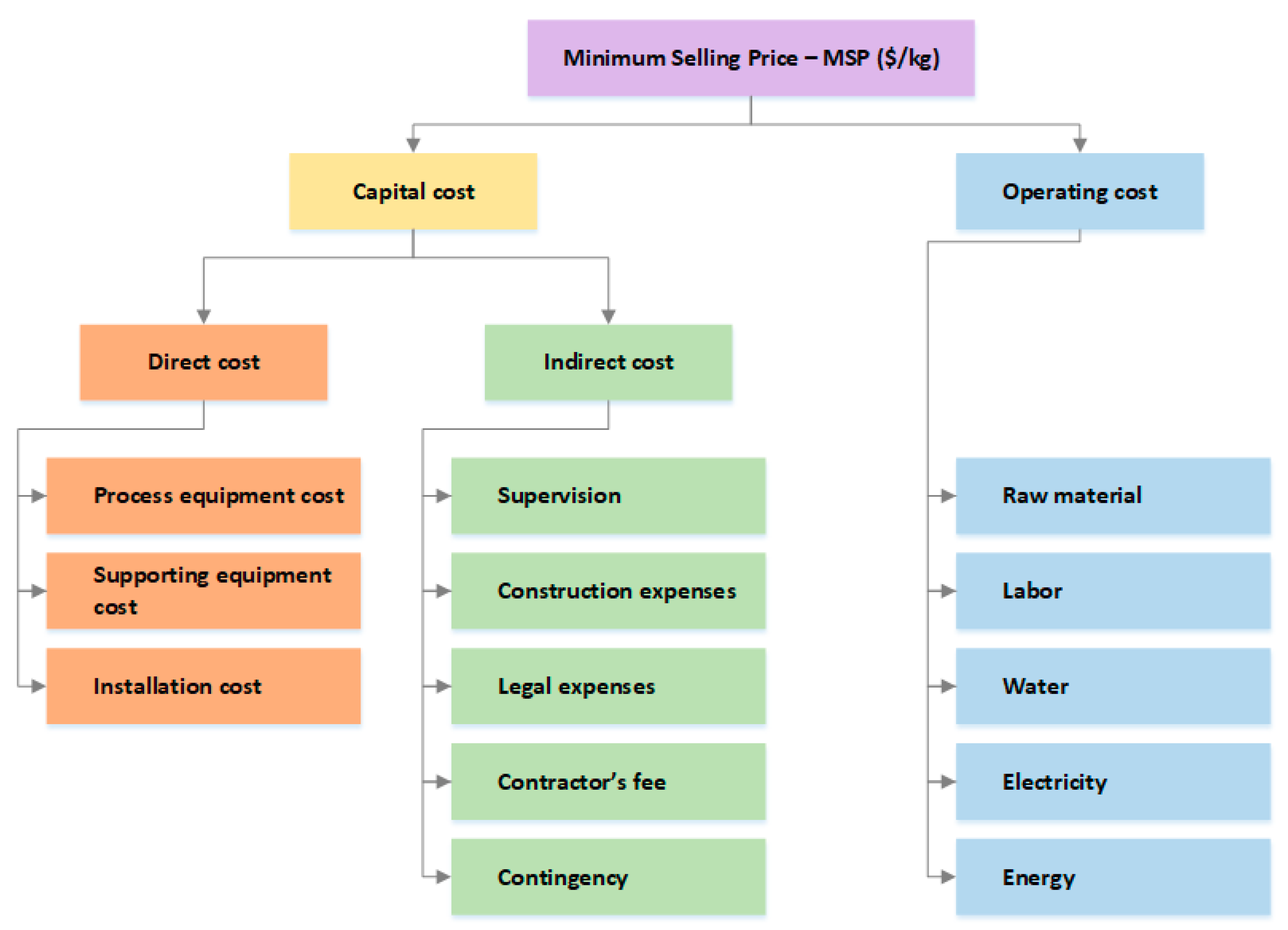

2.2. Cost Calculations

Cost calculations are performed on two different tabs. Costs directly related to unit operations (direct cost) and operating them are calculated in

Tab FP (in the case of fermentation) and

Tab Eps (in the case of the downstream process), whereas indirect costs are estimated in

Tab CD. As detailed in

Figure 2, the two primary components of MSP are the capital and operating costs. The capital cost is amortized to calculate the loan payment on purchased equipment costs and other construction expenses. Operating cost includes energy, labor, electricity, raw materials such as water, corn steep liquor serving as media for microbial growth, catalysts, and feedstock.

Capital cost is divided into direct and indirect costs. The direct cost is the total capital cost of all unit operations, which is the purchase equipment cost and installation cost for respective equipment. Scaling law is used to compute the raw capital cost of equipment [

15]. The equation is used to calculate the equipment cost is: C

n = (S

n/S

b)

n (C

b), where C

n—Cost of newly sized equipment, S

n—New size of equipment, S

b—Base size of equipment, C

b—Base cost of equipment, and n—Cost exponent. For all unit operations, ESTEA2 uses the base size, base cost, and cost component data from multiple literature resources. The Chemical Engineering Plant Cost Index (CEPCI) values [

19] are used to update the purchased equipment costs to 2018 (CEPCI for 2018: 603.1).

We then use the Lang Factor method to calculate installation cost by multiplying purchased equipment cost calculated by an approximation factor. Many literature references guide Lang Factors for process plants, including [

20,

21]. The tool allows the user to select Lang Factors in the range of 4–10, to account for equipment installation costs as well as additional supporting equipment costs (example: solvent recovery and recycling). The direct cost is computed as the sum of purchased equipment cost and installation cost. This value is then amortized to compute annual loan payment on capital (amortized capital cost), based on the user-provided interest rate and loan period (user information).

Indirect costs account for additional expenses that are not directly related to the capital and operation cost of the plant. They are estimated as the percent of purchased equipment costs. Construction and design (34%), engineering and supervision (32%), legal expenses (4%), contractor’s fee (19%), and contingency (37%) are the factors and respective percentage of purchased equipment cost used to calculate indirect cost [

15].

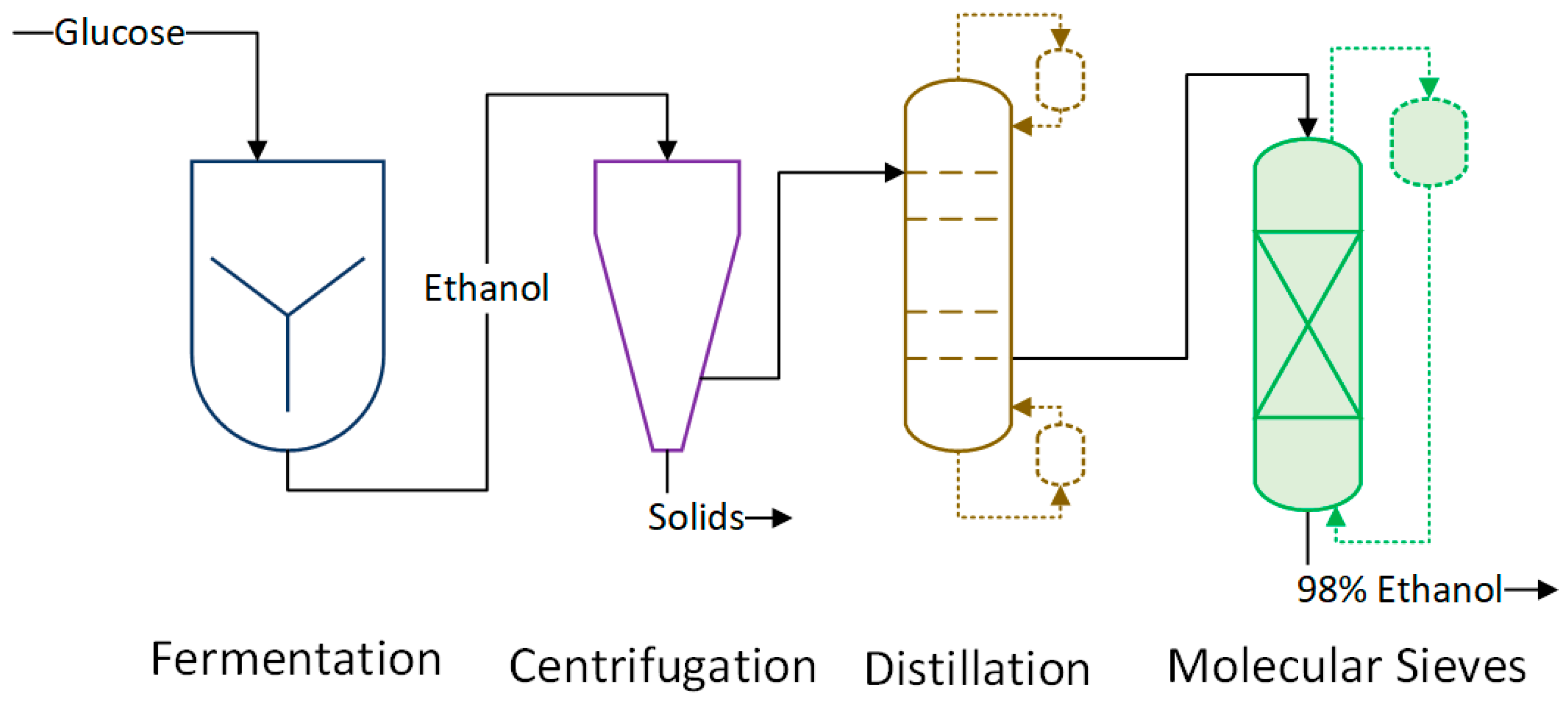

2.4. ESTEA2 Validation—Ethanol Process Model

We modeled an ethanol process in ESTEA2, as shown in

Figure 3, and compared the results with multiple literature resources. The process was built based on Kwiatkowski’s SuperPro model [

18]. The ethanol process was designed for 119.1 kTA (kilotons per annum) plant capacity.

The fermentation of glucose by Saccharomyces cerevisiae takes place over 56 h, producing ethanol at a rate of 2 g/L/h. We assume a product yield of 51% is achieved (90% of maximum theoretical yield), producing the final concentration of ethanol at 100 g/L. A fermentor with a maximum size of 3785 m3 is used, with a maximum usable percentage up to 80%. A downtime of 6 h is included to account for product discharge and cleanup.

Ethanol produced is recovered using distillation columns and molecular sieves. The first step of recovery is done by evaporating almost all of the products in distillation columns. The maximum amount of water is removed through this step. As ethanol and water form an azeotropic mixture, some water remains in ethanol after the distillation process. Molecular sieves are used as the final purification process to remove the remaining water. The smaller pores of zeolite absorb water from the ethanol‒water mixture, thereby producing 99% pure ethanol. Lang Factor of 6 is used to accommodate equipment installation as well as subsidiary equipment costs (e.g., holding tanks, heat transfer equipment).

No byproduct formation is assumed; hence, any design and cost calculation related to DDGS processing are not accounted for in the ethanol process modeling in ESTEA2. Similarly, pretreatment and processing of corn are not applicable to this design as glucose is used as the feedstock. Process parameters from the Hofstrand [

17] and Kwiatkowski [

18] models are used for modeling the fermentation and downstream processes.

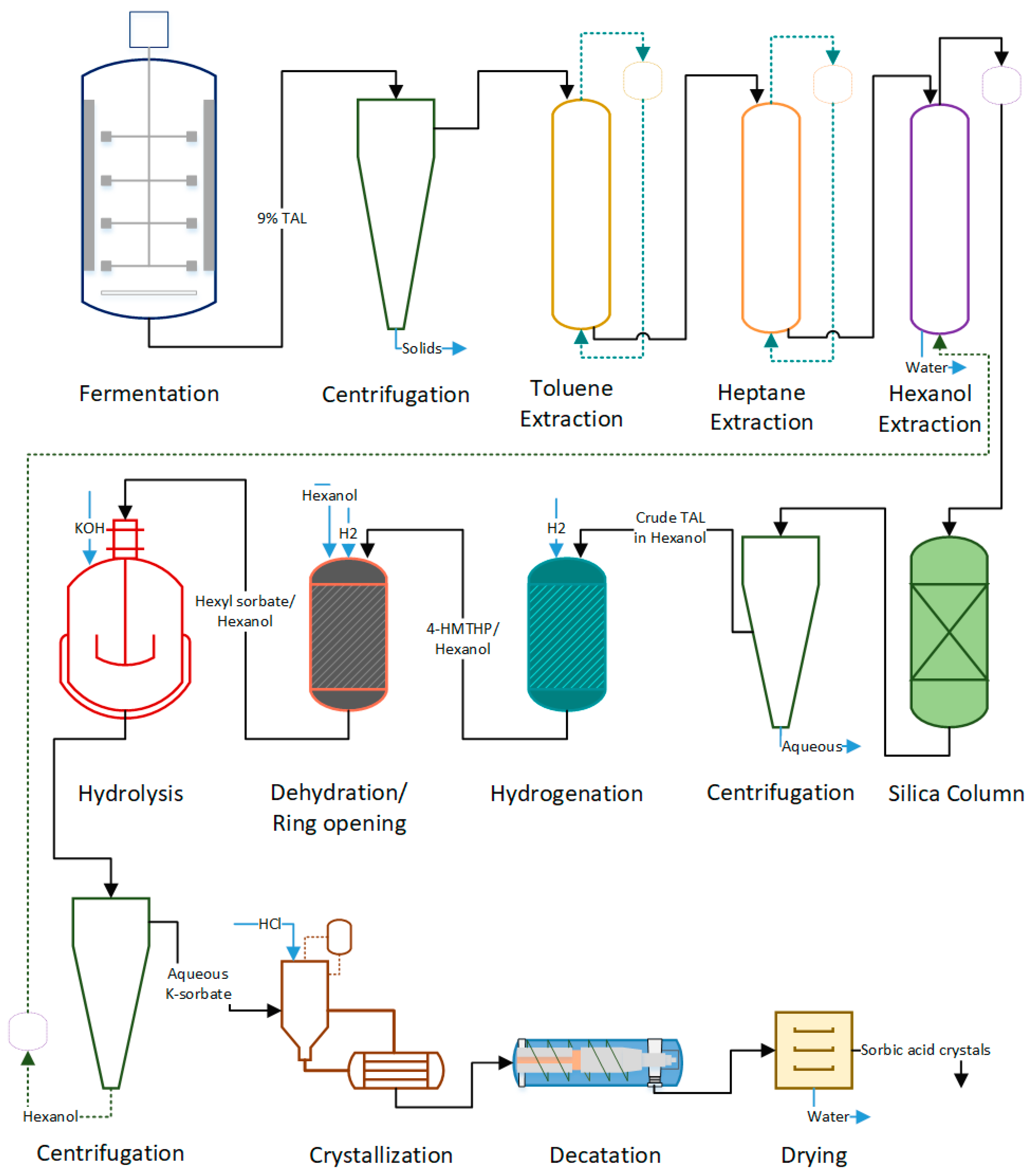

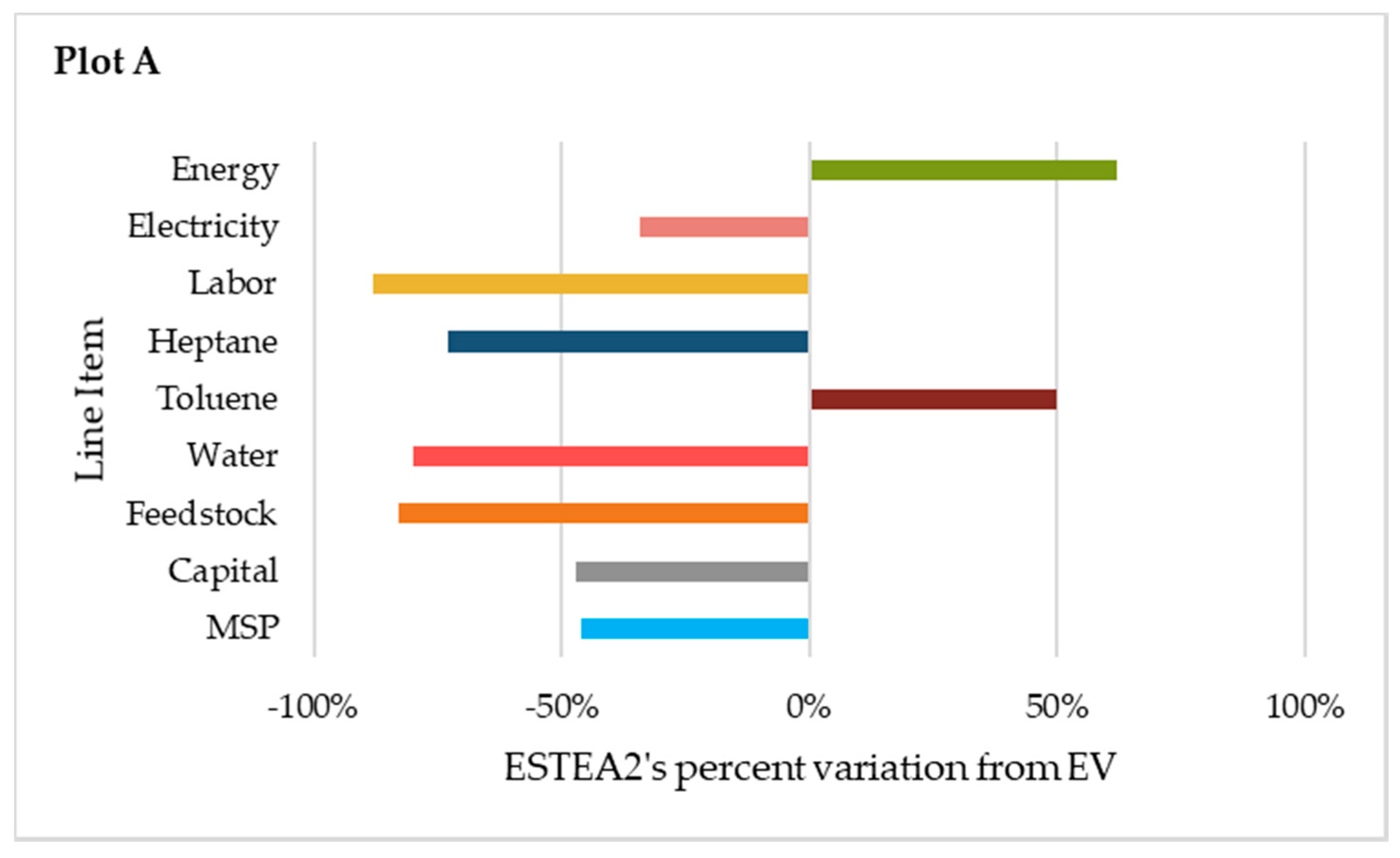

2.5. ESTEA2 Validation—Sorbic Acid Process Model

Furthermore, the tool was validated with a postulated biobased sorbic acid process. Triacetic acid lactone (TAL), a potential platform chemical, is produced through the fermentation of sugars [

28]. The biologically produced TAL is capable of undergoing chemical catalysis to form several molecules such as pogostone, dehydroacetic acid, katsumadin, acetylacetone, and sorbic acid. Sorbic acid is a high-volume commodity chemical used primarily in the food industry. Dumesic’s research group has successfully produced sorbic acid from TAL through a series of chemical reactions [

13]. We have utilized the available knowledge to design this hybrid process in ESTEA2 and performed its technoeconomic analysis. Since the process is still under lab-scale development, we used anticipated parametric values, instead of current values, to achieve realistic results. These data were unpublished results from CBiRC researchers working on this process (e.g., [

28,

29,

30]). The results from ESTEA2 were validated by comparing with design reports from an external vendor (name not specified; referred to as EV in this work).

The sorbic acid production process was modeled in ESTEA2 for 20 kTA plant capacity. The plant is operational for 330 days per year, with 10 years of operating life. A Lang Factor of 6 is considered to account for the unit process equipment installation.

Figure 4 is the process flow diagram of the sorbic acid process, which is detailed below.

Fermentation: The process begins with fermenting glucose to produce TAL. We assume a process yield of 43% (90% of theoretical yield). The fermented broth contains a TAL concentration of about 150 g/L produced at the rate of 2 g/L/h. We assume 6 h fermentor downtime for broth discharge and cleaning. We assume complete removal of cells and solid mass through centrifugation, which follows fermentation.

Toluene, Heptane, Hexanol Extraction: The purpose of this set of extraction procedures is to remove polar and nonpolar compounds, causing catalyst deactivation [

29,

30]. The concentration of these organic species is assumed as 1% of that of TAL. Toluene and heptane are the solvents used to remove long-chain fatty acids and other nonpolar compounds (TAL does not partition into hexane/toluene). To separate amino acids and other polar compounds, TAL in the broth is extracted into hexanol. TAL has a partition coefficient of 7 (approximately) into 1-hexanol at low pH. Extracted TAL is passed through a silica column to remove residual polar compounds.

Hydrogenation: Extracted TAL in hexanol undergoes catalytic hydrogenation in the presence of Au/Pd catalyst to form 4-hydroxy-6-methyltetrahydro-2-pyrone (4-HMTHP). Steam is supplied to heat the reaction mixture to 50 °C. Natural gas, required to produce steam, is included in the energy cost calculations. We assume a 2% catalyst loss per cycle and 98% product yield during the hydrogenation process. The process, as designed in ESTEA2, uses a tubular reactor with a catalyst inside the tubes, although EV uses a stirred pressure reactor.

Dehydration/Ring Opening and Hydrolysis: 4-HMTHP undergoes dehydration at 100 °C for 12 h, followed by ring-opening at 170 °C for 12 h producing hexyl sorbate, which is hydrolyzed with KOH at a 99% conversion to K-sorbate. Dow Amberlyst—70 is the catalyst used by EV; since the catalyst is unavailable in the ESTEA2, we used Raney nickel. The overall process yield (dehydration and ring-opening together) is assumed to be 90%.

Due to limited unit operations availability, we have combined the catalysis and hydrolysis processes to occur in the same reactor. Batch reactor with a combined residence time of 26 h for dehydration, ring-opening, and hydrolysis is considered.

Crystallization and Drying: Hydrolyzed K-sorbate is later crystallized at a 98% yield. Hydrochloric acid (HCl) is used as the separating agent. The sorbic acid crystals are separated using centrifugation; the leftover aqueous phase (KCl) is recycled. Sorbic acid crystals are then dried to remove any leftover moisture. The energy required for drying sorbic acid up to 2% final moisture is computed.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}