1. Introduction

Granting loans is a fundamental area for commercial banking operations. Even though this activity brings the largest income, it is also burdened with the highest risk. Thus, banks undertake a series of various actions meant to minimise its negative results. One of the most important methods aimed at limiting the credit risk and assessment of the future solvency of the borrower is the analysis of their credit check and their creditworthiness at every stage of the loan agreement (

Spuchláková et al. 2015). Reliable credit check assessment is a significant matter both for the bank and the borrower. It protects both parties in the loan agreement from negative consequences resulting from a failure to repay the contracted liability. A properly conducted analysis of the credit check has, in addition, been deemed as a key condition for the stability of the financial system (

Herring 1999). In their practice, banks use different methods to serve the analysis of the credit check. However, until now, a uniform template has not been created in this regard (

Genriha and Voronova 2012). The provisions of the acts in force in Poland do not impose a method or the criteria for creditworthiness, something which banks ought to follow. Consequently, this practice varies significantly depending on the credit provider, which in consequence can lead to differences in the final assessment.

The quality of credit exposure has been one of the most important issues in the banking literature for many years. It is also considered to be an important indicator in assessing the condition of banks and the entire banking sector. Deterioration in the quality of banks’ loan portfolios also represents one of the biggest threats of the COVID-19 pandemic.

Considering the changes in Europe in the level and dynamics of impaired loans, Polish cooperative banks represent a very interesting object of analysis. They comprise a group of 530 entities (a number ten times bigger than the number of commercial banks, but with only a 7.8% share of banking sector assets). These entities are highly diversified in terms of size, area of operation, and financial condition. The average level of nonperforming loans (NPL-the share of impaired loans in the bank’s total loan portfolio) at cooperative banks in Poland increased by 220% (from 2.8% to 8.8%) between 2009 and 2020. This upward trend is essentially continuous (a stabilization of values was observed between 2018 and 2020). This tendency is different than in commercial banks operating in Poland and cooperative banks in other countries with a significant role of cooperative bank sectors (Germany, France), as well as for the entire population of banks in the European Union countries. Undoubtedly, one of the reasons for this phenomenon is the fact that during the 2007–2009 crisis Polish cooperative banks sustained lending activity, entering (at the same time) into the segment of small and medium enterprises where they hardly had experience. The negative effects of decisions made at that time could be observed in subsequent years. Additionally, cooperative banks were much less interested in using scoring models (both external or their own) in the credit risk assessment process. This process may also explain the rise in the level of NPL ratio in this banking sector.

The main objective of the paper is to assess the impact of the use of scoring models by Polish cooperative banks on the quality of their loan portfolio (measured by the NPL ratio) between 2004 and 2020. The authors try to verify two research hypotheses:

- (1)

The use of scoring models by Polish cooperative banks in the credit risk assessment process results in a statistically significant reduction in the scale of credit risk materialization;

- (2)

The effectiveness of internally built scoring models by Polish cooperative banks is lower than the effectiveness of general models offered by BIK.

Biuro Informacji Kredytowej (BIK-Polish Credit Information Bureau, which is established to collect, integrate and share data on the credit history of bank customers).

This article has been divided into three basic parts, including a literature review on the significance of scoring models in the process of mitigating bank credit risk, a description of the research method and sample, and the presentation of conclusions and recommendations resulting from the studies.

2. Literature Overview

The basic tool for limiting credit risk in the banking activity on the pre-contractual and contractual stages is the credit check assessment. In the literature, two basic categories are distinguished relating to the credit check: formal and legal capacity and substantive capacity. The substantive check is a broader and more complex concept since it contains in itself two significant aspects of assessment, personal and economic (

Caplinsk and Tvaronavičienė 2020). In the personal dimension of assessment, the elements are analysed that determine the confidence in a borrower himself. These characteristics include, among others, the character, family status, previous experience, acquired professional qualifications, reputation, and managerial skills. What’s more, this category of credit check also contains the ethical and moral assessment of personal responsibility and reliability of the borrower relating to the interests of the business they run. The economic dimension of the substantive capacity assessment focuses on the analysis of the mostly objectified elements that characterize the previous, current, and future financial and economic situation of the borrower (

Ritonga et al. 2017).

The most common method used by banks to assess the creditworthiness of a homogeneous group of borrowers is credit scoring (

Emel et al. 2003). In the functioning of any bank, this is considered to be a key element that has a real impact on future financial results. Initially, the concept of credit scoring referred only to simple expert scoring cards. However, with the development of technology, simple scoring turned into predictive models with a high degree of advancement. Credit scoring has been defined as a method of assessing the amount of credit risk of a customer who applies for a loan. By using historical data and various statistical techniques, the scoring system is designed to distinguish the impact of individual characteristics of applicants that significantly affect the timely payment of their obligations. This method generates a certain point (called a cut-off point) by means of which the bank can easily classify applicants or borrowers into groups showing a different level of risk. In order to build an effective scoring model, historical data (collected on the basis of previously granted loans) and selected features helpful in predicting the repayment of the liability are analysed. A well-constructed scoring model should give a higher rating to customers who will, in the future, settle their liabilities in accordance with contractual terms and a lower rating to borrowers who have difficulties with it (

Mester 1997).

In the literature on the subject, three types of credit scoring are distinguished most frequently: application, behavioural, and profit. Credit scoring has many advantages, not only for the lenders but also for the borrowers. Most often, scoring models are used to make credit decisions in relation to loan applications. In addition, modern scoring models are also used when setting credit limits, managing existing accounts, and forecasting the financial credibility of clients (

Fensterstock 2005). As the main advantage resulting from the use of scoring models in the banking activity, the speed of analysis, simplicity of application, and its versatility are indicated. The evaluation process takes place in a comprehendible manner, and the obtained results are clear and easy to interpret (

Mutie 2005).

An important advantage of the scoring system is its impartiality and possibility of standardizing the criteria in the process of loan decision-making. The model’s objectivity guarantees a feeling among the borrowers that each of them is treated equally, regardless of race, gender, religion, and other discriminatory factors. What is more, this system is characterized by high flexibility, which allows using by the bank almost any loan policy that has an application in the scoring algorithm (

Wysiński 2013). A correctly constructed scoring model also allows one to significantly limit the number of bad loans at the bank, leading to an improvement of its loan portfolio. This tool is also characterized by better effects. As with the use of credit scoring system, the number of loans with the loss of value is lower than in the situation when the loan decision is made in a traditional way of clients’ verification, often by the employees with varied levels of qualifications (

Blöchlinge and Leippold 2006). Barefoot points to several key advantages of credit scoring. For example, credit scoring lowers the cost of the loan since it reduces the human involvement in the assessment of a loan application (

Barefoot and Walika 1996). According to

Ponicki (

1996), credit scoring provides a standard technique for assessing loans throughout the banking sector, an effective way of conducting transactions, and facilitates the collection of receivables from customers. Scoring models also benefit customers of credit institutions by offering a simple application process, ensuring that the clients receive a timely response to their loan application and access to credit when they need it.

At the same time, the literature indicates certain threats related to the use of credit rating as a tool for examining creditworthiness. The scoring system used in a bank often becomes obsolete quickly, which forces the management to enter new borrowers’ data on an ongoing basis as well as to systematically update the scoring card used. It is also indicated that the credit scoring method may adversely affect the number of new borrowers. This is due to the high probability that customers who do not have a credit history will obtain a negative creditworthiness assessment, resulting in a refusal to grant a loan. Moreover, a lower borrower’s rating makes the cost of the loan increase, making it less attractive (

Kinda and Achonu 2012). Despite the risks associated with the use of scoring models,

Samreen and Zaidi (

2012) in their article on the banking sector in Pakistan strongly recommend that commercial banks use a scoring model to assess creditworthiness as part of the credit process. By adopting this model, banks can reduce the number of non-performing loans. These recommendations emphasize the fact that the advantages of using credit scoring in the credit process outweigh the negative aspects of their implementation.

There are many research studies that include scoring models. However, the impact of differentiation of scoring models on the quality of banks’ loan portfolios is not sufficiently described in the literature, and it is almost impossible to find studies regarding the Polish banking sector.

The impact of the use of credit scoring on the parameters of the lending policy and the quality of the portfolio of receivables from the non-financial sector is the subject of research in many countries.

Frame et al. (

2001) have shown in their research that, thanks to the use of scoring models to estimate the credit risk of borrowers, the number of loans granted to individual clients (but also to small and medium-sized enterprises) also increased.

Berger et al. (

2005) in their article state that a greater increase in lending can be seen in banks that buy the “results” of scoring by third parties, as opposed to banks that use their own scoring models.

Deyoung et al. (

2006) provide additional evidence that loans from banks that use their own credit risk assessment models are of inferior quality. Their research suggests that using ‘proprietary’ scoring models is associated with higher borrower default rates, but using this technology tends to mitigate some of the additional risk associated with ‘longer distance’ loans.

Blöchlinge and Leippold (

2006) in their studies on the economic benefits of using credit scoring showed that the profitability of the rating model also depends on the discriminatory power of other competitors. The use of “weak” scoring models by banks in the credit process attracts more “bad” borrowers and, therefore, a competitor with a low power of discrimination will incur lower revenues and greater losses. In such a situation, by judging debtors on the basis of a weak and unreliable system of credit ratings, banks grant more loans to those who fail to repay their loan, at the same time rejecting solid potential borrowers.

Blöchlinge and Leippold (

2006), in quantitative terms, show that these banks are unknowingly becoming a market leader in the segment of non-performing loans. Common to all the banks analysed by the authors is the fact that the better the scoring model used in the credit process, the lower the risk of unfavourable selection and the higher the added value for the bank. A lender can significantly increase its loan portfolio by upgrading its rating system with the positive side effect of a decline in its non-performing loan portfolio.

Comparison of credit scoring models such as the Statistical-based Credit Scoring Models Artificial Intelligence-based/Machine Learning Methods, made by

Eddy and Engku Abu Bakar (

2017), indicates that although some techniques (especially those based on artificial intelligence) allow one to apply better credit scoring models, these techniques still lag behind statistically based techniques since they are not user-friendly and are difficulty of use. Consequently, statistical-based techniques of scoring model continue to be the more common methods of choice for banks. Among these techniques, logistic regression is the most popular one.

Based on the research of

Koh et al. (

2006), who in their paper discussed and illustrated the application of data mining techniques to combine different scoring models together, it can be stated that although this process can lead to creation of a single model that is more effective in predicting credit risk, this process also has pitfalls. One of these may be that it is difficult, and sometimes impossible, to combine several scoring models in such a way that the credit risk prediction results significantly exceed those shown by the individual models on which it is based.

The results of study, conducted by

Dierkes et al. (

2013), who sought to determine the effect of using a business credit information sharing system on the credit risk associated with these entities, indicates that the application of credit information by banks sharing systems affected a significant increase in the accuracy of default forecasts both in aggregate and for individual firms.

Kerage and Jagongo’s (

2014) findings also prove a positive relationship between the use of available information regarding potential borrowers’ credit history by loan companies and banking sector performance. As banks increased their sharing of information about their customers’ credit histories their performance improved, including a reduction in non-performing loan ratios.

Giannopoulos (

2018) studies the effectiveness of artificial credit scoring models in predicting SMEs default. Comparing a neural network model (multilayer perceptron) and a decision tree model with the credit scoring model applied by the bank, he found that the bank’s model had a relatively worse performance in predicting loans default.

Fu et al. (

2020) conducted a comparative analysis of methods from the machine learning repertoire. They found that machine learning methods can improve the empirical understanding of consumer credit defaults. Additionally, they demonstrated the validity of developing a comprehensive credit scoring system using data sources in the form of digital traces, especially in countries with high levels of digitization

Empirical analysis, presented by

Berger et al. (

2011) suggests that the use by community banks of consumer credit scoring is associated with an increase in small business lending without any significant change in the quality of the banks’ loan portfolio. Moreover, the use of credit scores by community banks for small business lending is associated with an initial decline in profitability that moderates over time.

Kipyego and Wandera (

2013), based on their study on the effect of credit information sharing on the level of non-performing loans in banks in Kenya, concluded that the introduction of credit information sharing system has led to a reduction in non-performing loans in the banking sector of Kenya.

Mutesi (

2011), in a study on commercial banks in Uganda, found a positive correlation between credit information sharing, and quality of risk management and financial efficiency. Based on this, he concluded that banks, in order to increase the efficiency and relevance of their credit information and minimize the credit risk they incur, should build “strong” credit information systems (credit information bureaus).

3. Data and Methodology

3.1. The Quality of the Credit Portfolio of Cooperative Banks in Poland

Cooperative banks in Poland constitute a very heterogeneous group of credit institutions operating mainly on the local market. At the end of 2020, 530 cooperative banks were operating in Poland, of which 518 under the institutional protection systems of two associations: the IPS BPS and the IPS SGB.

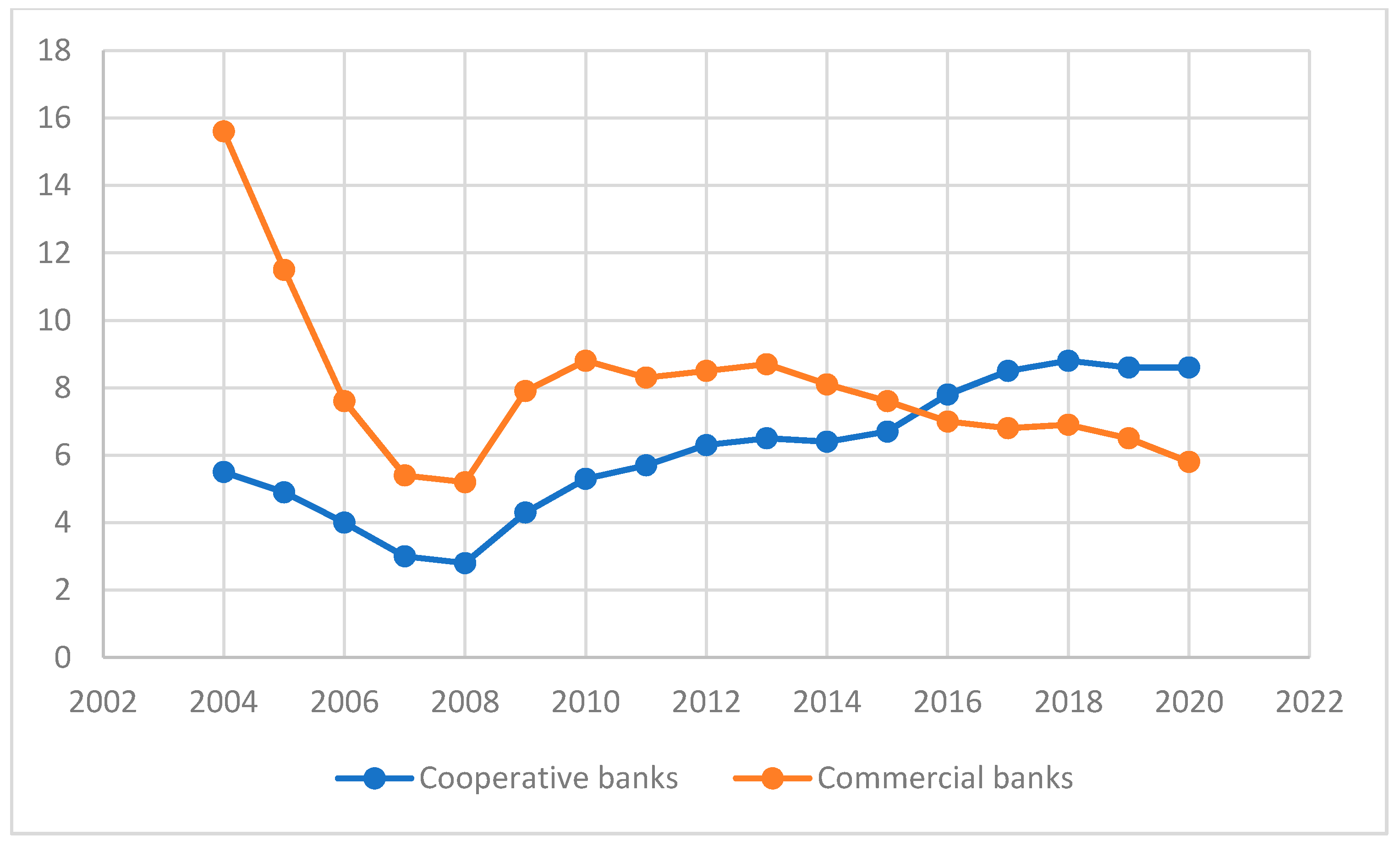

As indicated in the introduction, the cooperative bank sector in Poland has been characterized recently by a significantly worse quality of loan portfolio than the loan portfolio of commercial banks. The NPL growth trend in the Polish cooperative bank sector is also different than the one in the cooperative bank sectors in other European Union countries. The share of impaired loans in the sector of polish cooperative banks at the end of 2020 was on average by nearly three percentage points higher than in the sector of commercial banks operating in Poland and by about five percentage points higher than the average value for cooperative banks operating in Germany and France (

Figure 1).

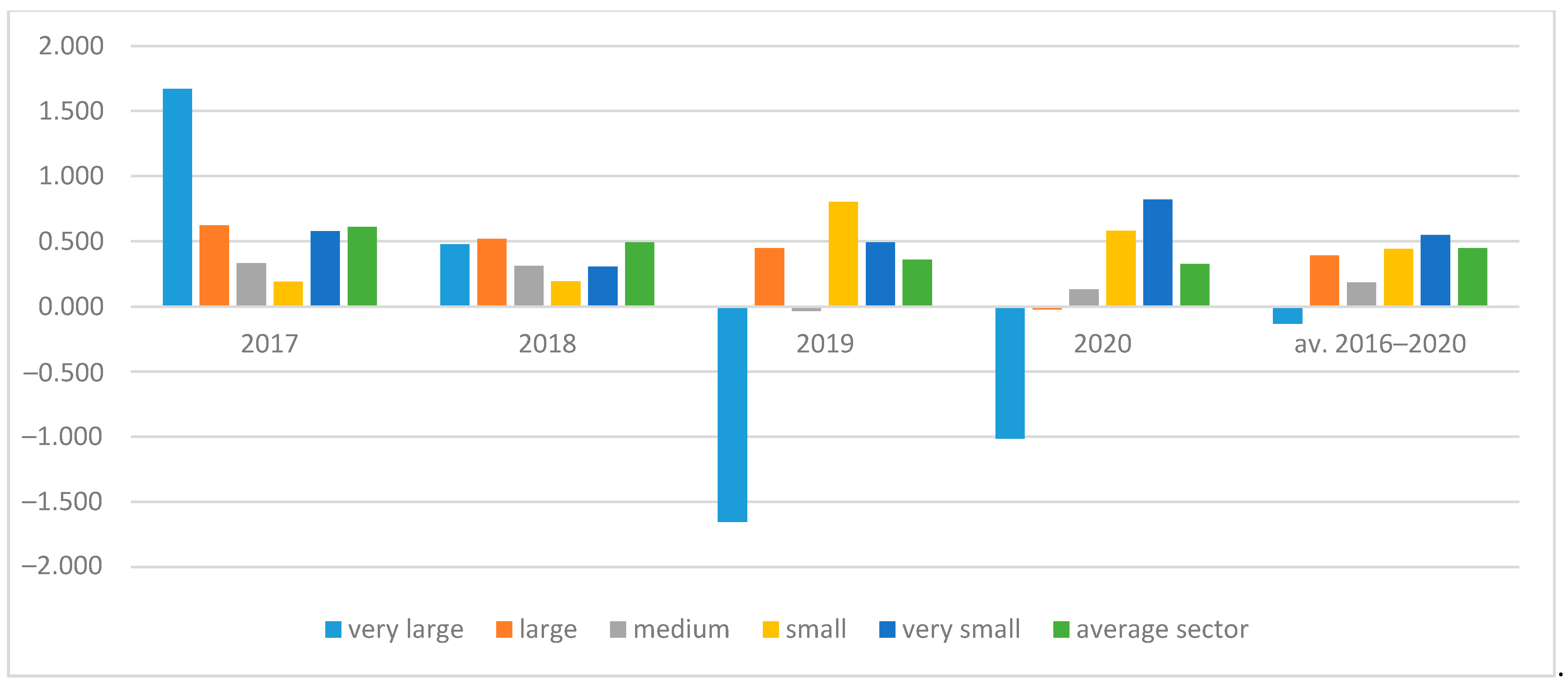

The analysis of the quality of the loan portfolio of these banks was carried out and broken down into five groups of entities, distinguished based on the value of assets at the end of 2020 according to the following scheme:

- -

Very large banks with a balance sheet total exceeding PLN 1 billion (14 entities);

- -

Large banks with a balance sheet total of PLN 500–1000 million (62 entities);

- -

Medium-sized banks with a balance sheet total of PLN 200–500 million (201 entities);

- -

Small banks with assets in the PLN 100–200 million range (153 entities);

- -

Very small banks with a balance sheet total of up to PLN 100 million (83 entities).

Moreover, for the purposes of some analyses, a group of acquiring banks (17 banks) and acquired banks (19 entities) was separated. The research results for the years 2016–2020 are presented in

Table 1 and

Figure 2.

Cooperative banks operating in Poland are characterized by strong differentiation of the quality of credit portfolio. On average, in the years 2016–2020, the value of NPL in the sector equaled 4.7%, whilst in very large banks the share of impaired loans equaled nearly 11%, whilst in the small banks it was 3.7%. However, in 2020, amongst other results from the COVID-19 pandemic, a strong deterioration of the quality of loan portfolios was observed in small and very small banks (increase of NPL accordingly 0.58 percentage points, i.e., 14% and 0.82 percentage points, i.e., 23.5%). At the same time, the improvement of this indicator was noted in 2020 in large and very large cooperative banks. However, it should be emphasised that very small and small banks still remain the leaders in terms of relatively low level of NPL at the end of 2020. Simultaneously, quite strong geographical differentiation is noted in the quality of banks’ credit portfolio at the end of 2020, as well as changes that took place at the level of NPLs in 2020 (compared to 2019). As a result of analyses, no significant differentiation was observed in the financial condition of cooperative banks by voivodeship.

3.2. The Use of Scoring Models in Lending in the Light of a Survey of the Management of Cooperative Banks in Poland

Cooperative banks operating in Poland, due to the lack of the obligation to apply international financial reporting standards, present a fairly limited scope of information on credit risk management tools. In particular, they generally do not present data on the use of scoring models in this process. One of the tools for assessing the scale and role of the use of scoring models in the credit risk management process in cooperative banks in Poland was therefore a survey conducted by the authors and addressed to bank managers in 2020. The questionnaire was distributed by traditional means (postal correspondence) and by electronic means (remote form distributed by e-mail). Seventeen cooperative banks participated in the survey. They were diversified in terms of: bank size (three small banks, eleven medium banks, and three large banks); the area of operation (Polish law makes the size of the territory in which cooperative banks may operate dependent on the value of their own capital); and their financial condition. The share of these banks in the assets of the cooperative bank sector was 3.4%. The form contained questions relating mainly to credit risk management methods and tools used in this process, with particular emphasis on scoring models between 2004 and 2020. In addition to general information, there were also questions about the advantages, disadvantages and the most important components of scoring models, as well as the subjective opinion of management about the applied credit risk mitigation tools.

Building an effective scoring model is a complicated task and is usually closely related to the careful design of the entire undertaking. The accuracy of the scoring depends on the elements built into the model and, therefore, largely depends on the reliability and quality of the collected data (

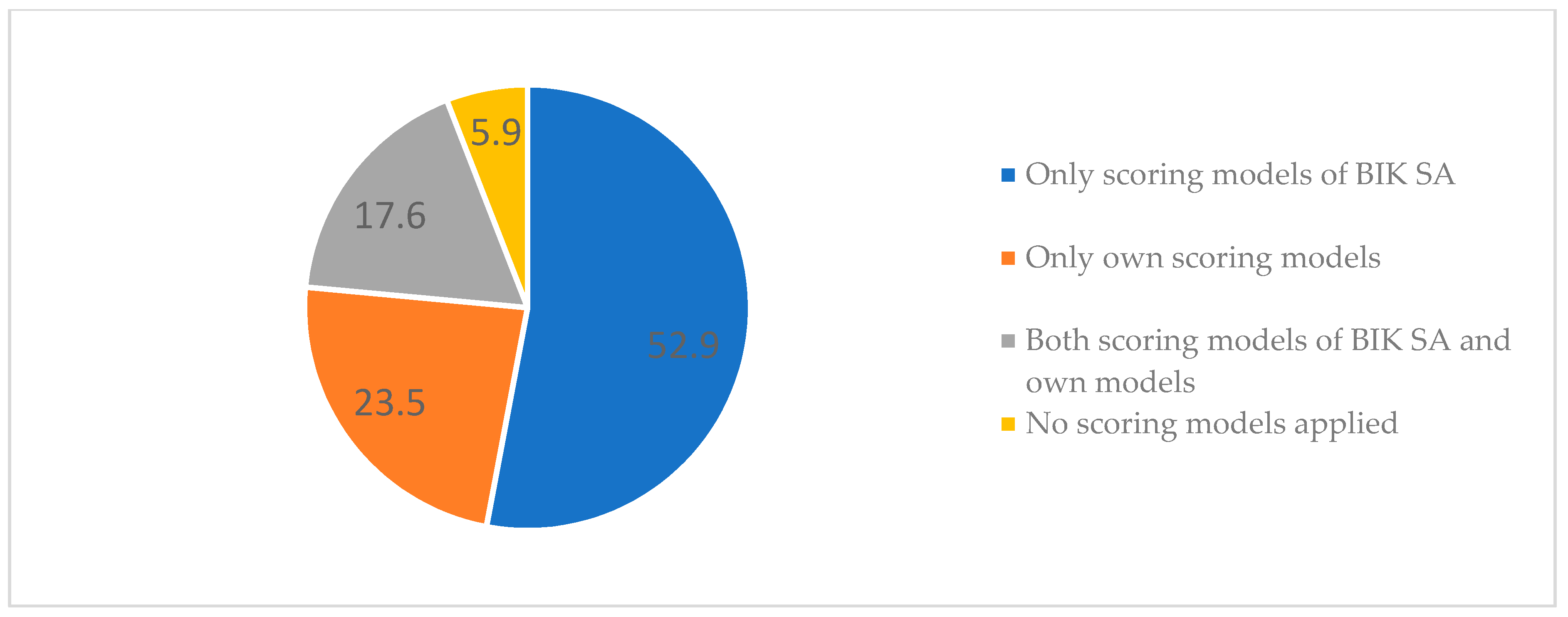

Yap et al. 2011). As a result of the survey, it can be indicated that cooperative banks belonging to the association in BPS S.A., participating in the analysis, mostly use the scoring models offered by BIK S.A. (Polish Credit Information Bureau) in the credit risk management process (the first scoring model was introduced to the BIK offer already in 2004 (BIKSco). At the time of its construction, data for BIK was provided by only about 20 banks, as a result of which this model very quickly proved to be inadequate. There was a dynamic development of the BIK database in the following years. Scoring models offered by BIK are constantly verified, upgraded, and adjusted to current regulatory requirements. The most common and best recognised model is BIKSco CreditRisk). Among the surveyed institutions, 58.8% declared that they use these models in their lending activities.

The percentage of banks associated in BPS S.A. participating in the study, who only use the models developed by BIK S.A. to analyse the borrower’s ability and credibility, is 52.9%. It is worth noting that only 5.9% of the surveyed cooperative banks use both BIK scoring models and their own models, which in the literature are usually referred to as proceedings based on hybrid models (

Wysiński 2013). A relatively large percentage of the banks (17.6%) declared that they use only models developed in-house. A very important observation resulting from the survey is that over 20% share of affiliated banks that do not use any scoring models in their activities (

Figure 3).

Among the banks belonging to the BPS S.A. association, 80% of the analysed cooperative institutions introduced BIK scoring models to the credit risk management system in 2008–2012 (i.e., during the crisis and the following post-crisis period). 10% of the surveyed institutions started using the models in 2014, and the remaining 10% started in 2019.

The introduction of BIK scoring models to the credit risk management system in cooperative banks associated with BPS was accompanied by various motives. As many as 90% of the surveyed institutions indicated the use of these models as an additional tool contributing to the reduction of credit risk as the main reason. In the case of half of the banks participating in the study, they were prompted by the excessively high costs of building individual models to use the BIK offer. Models developed by BIK are characterized by lower costs, universal availability and universal use. However, they have been accused of lower accuracy than in the case of individual models (

Wysiński 2013). Another aspect that influenced the introduction of BIK models in cooperative banks was the influence of other banks belonging to the association, which may indicate activities contributing to the unification of the business model. The remaining indicated factors relate to the recommendations of the BION and the KNF Office, as well as the high effectiveness of the models.

The surveyed banks affiliated to BPS indicated that their high efficiency is maintained in relation to the models developed by BIK. In the case of 60% of cooperative institutions, high efficiency in reducing credit risk was indicated, while 30% of the respondents believe that these models are effective but contain some drawbacks. 10% of the banks participating in the survey state that the BIK scoring models are operating poorly.

The credit-scoring system is not an ideal tool for limiting credit risk. It has both a number of advantages and various drawbacks. According to the associated cooperative banks, which in their activities use scoring models developed by BIK, their fundamental advantage is a well-developed database of information about borrowers. BIK has data on approximately 145 million accounts belonging to 24.6 million retail clients (

Biuro 2020). As a result, banks can easily verify the information obtained from the client and validate its correctness. Other very important advantages of BIK’s scoring analysis tools include the availability and credibility (i.e., one of the most desirable features of scoring models). BIK’s experience in creating and adapting scoring models to the currently applicable legal regulations and economic conditions is also an undoubted value.

The activities of cooperative banks are distinguished primarily by their relational nature, based on maintaining close and long-term relationships with customers (

Bank 2020). The strength of cooperative institutions is also the multitude of roles played by their members, as well as their strong embedding in the social and economic local environment. All of these aspects make it much easier for banks to mitigate the limitations resulting from information asymmetry, and also contribute to increasing trust in the institution and building its good reputation (which in turn affects profitability).

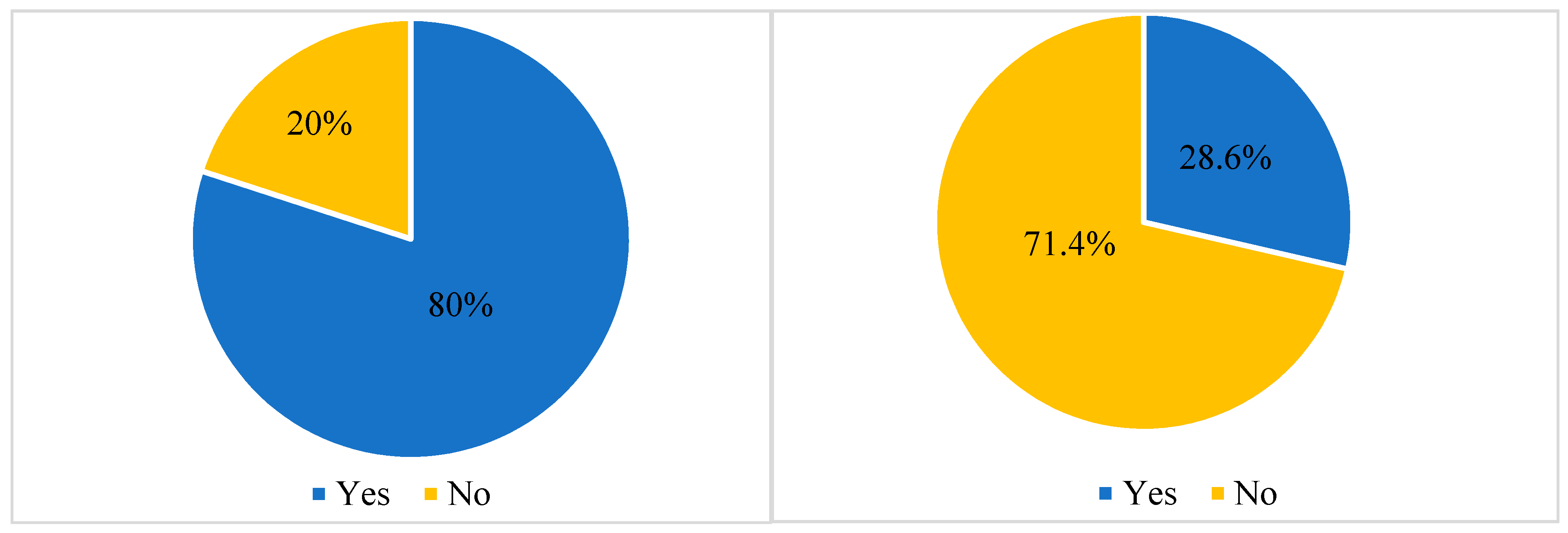

The results of the survey revealed different views of the management of cooperative banks belonging to the BPS S.A. association on the impact of the relational nature of cooperative institutions on the lower importance of scoring models used to analyse the customer’s creditworthiness. In the case of banks using BIK scoring models, as many as 80% of cases indicated that the relational nature of cooperative banks reduces the importance of scoring models. With regard to the remaining cooperative banks, the opposite answer was indicated, negating the impact of the relational character on the reduction of the importance of scoring models in banking activity (

Figure 4).

3.3. Econometric Model-Research Method and Results

In order to verify the research hypotheses, the authors used a panel data regression model. The analysis relating to the quality of the credit portfolio of cooperative institutions was carried out on the basis of the obtained individual data of banks belonging to the BPS S.A. association and the results of the self-survey. The research period covered the years 2004–2020 and was largely conditioned by the availability of reporting data and the willingness of management staff of cooperative banks to participate in the survey.

The data used for the analysis are panel data, which are a special case of cross-sectional-time samples. The use of panel data for the construction and then estimation of econometric models contributes to easier verification of hypotheses and a reduction of the problem of collinearity of data, as well as completely eliminating or significantly reducing the bias of the estimators. These aspects are considered to be the main advantages of using this type of data.

At the end of 2020, the cooperative banks of the BPS S.A. association that were included in the analysis accounted for 3.4% of the total number of cooperative banks operating in the Polish banking sector and 5.4% of all banks associated with BPS S.A. Static panel models were used for the tests, and in order to select the appropriate model the results obtained from the Hausman test were used. Due to the level of Hausman’s statistics, models taking into account random individual effects were used. Their general notation takes the form:

where NPL determines the share of non-performing loans (overdue payments over 90 days) in the credit portfolio, ZM.MAKRO

i (t,t-1) represents vector of values of macroeconomic/regional control variables in period t or t−1, ZM.MIKRO

it represents the vector of control variables relating to the specificity of the operation of a particular affiliated bank in period t, ZM.SCOR

i,t represents the experimental binary variable characterizing the use of scoring models (BIK or own) in a given year by the bank, and vit represents a random component, which is the sum of the individual effect unchanging in time u

i and the pure random error ε

i,t (

Verbeek 2000).

The variables described in

Table 2 were used to conduct the analysis. The authors selected control variables based on a review of the literature on NPL determinants. The descriptive statistics of the variables are presented in

Table 3.

Due to the possibility of a correlation between the independent variables, which in turn leads to the occurrence of collinearity, correlation coefficients were calculated (

Table 4). The obtained results served as the basis for the preparation of the model.

4. Results of Econometric Model

Based on the presented method, a panel study was carried out and the obtained results are presented in

Table 5.

Based on the results of the panel study, some interesting observations should be highlighted. Among the macroeconomic factors analysed, the interest rate and GDP dynamics in the region have the greatest impact on the quality of the loan portfolio, measured by the NPL ratio. In this case, a significant negative impact of the short-term interest rate and the scale of economic growth on the value of the NPL ratio was demonstrated. In the case of remaining analysed macroeconomic variables, there was generally no significant impact on the value of the impaired loan ratio.

The study also showed a significant influence of microeconomic factors on the value of the NPL ratio. The relationship between the size of the bank and the share of loans delayed in the repayment period exceeding 90 days was confirmed. Therefore, it can be pointed out that larger cooperative banks are characterized by a much lower level of impaired loans and, thus, a better quality of the loan portfolio (regardless of the type of scoring model used). At the same time, it should be emphasized, as mentioned in the previous part of the publication, that in 2020 a strong change in the trend was observed, manifested by a high increase in impaired loans in small banks along with an average small reduction of the NPL ratio in large cooperative banks.

A statistically significant microeconomic determinant in the analysed models is also the size of the bank’s relative credit exposure. A statistically significant negative impact of this variable on the share of non-performing loans in the bank was demonstrated, which means that the quality of its loan portfolio improves with the increase in the bank’s credit exposure. It may be a consequence of banks’ greater specialization in this area.

Based on the results of the panel study, the negative impact of the scoring model developed by BIK on the quality of the loan portfolio was shown. At a significance level of 5%, it was demonstrated that cooperative banks which use BIK scoring to minimize credit risk, during the period of using this group of models, are characterized by a better quality of the loan portfolio which results from lower NPL values. It should therefore be noted that this analysis showed the effectiveness of the use of scoring models built by BIK. If individual models were used by cooperative banks, the study showed a significant positive impact on the quality of loan portfolios (at the 90% confidence level), which should be interpreted from the angle of their ineffectiveness.

5. Conclusions

This article presents the results of research confirming the efficacy of using the scoring models as a tool for limiting the credit risk in cooperative banks in Poland. It also indicates that a more advantageous solution for small, relational, and local banks is to apply standard models developed by a credit reference bureau at the sectoral level rather than models created individually on small samples, the effectiveness of which has not been confirmed.

As shown in

Section 3.3, the statistically significant (at the 90% confidence level) effect of the variables SC_IN and SC_BIK on the NPL level of the banks included in the sample allows for a positive verification of the hypothesis regarding the statistical significance of the effect of using the scoring model on the quality of the loan portfolio. These results are intuitively obvious (particularly for commercial banks), as shown in the literature overview. However, they are in opposition to some studies on community banking, (e.g., to the findings presented by

Berger et al. (

2011), who showed that the use by community banks of consumer credit scoring is associated with an increase in small business lending without any significant change in the quality of the banks’ loan portfolio). At the same time, the positive direction of the relationship between SC_IN and NPL indicators and the negative direction of the relationship between SC_BIK and NPL indicators provides evidence to support the hypothesis of the lower effectiveness in mitigating credit risk of internally built scoring models in relation to models offered by the Polish credit information exchange office (BIK). These results are in line with the current research on the role of credit information exchange systems in reducing the number of nonperforming loans in the banking sector. These findings are supported by research conducted by

Mutesi (

2011) and

Kipyego and Wandera (

2013).

The results regarding the impact of internal scoring models are in contrast with most previous studies, such as the analysis of Frederic

Nyasaka (

2017) who showed that a group of commercial banks that the use of Internal Appraisal Credit Rating Systems resulted in a reduction of the NPL ratio. This difference is very likely due to the specifics of Polish cooperative banks, which are small and local entities. Moreover, they often do not have enough financial resources to build individual, highly effective scoring tools.

As a consequence of the coronavirus pandemic, it is highly likely that banks will be severely affected by a recession which will result from the declining creditworthiness of retail clients as well as bankruptcies of corporate clients. The quality of the loan portfolios of the Polish banking sector institutions will largely depend on the duration of the crisis. In the light of the first negative consequences arising from the effects of the COVID-19 pandemic, the need for cooperative banks to use effective mechanisms to reduce the materialisation of credit risk is even stronger (so that the 2007–2009 crisis scenario would not repeat), given that the cooperative banks in Poland, fulfilling the function of a catalyst and supporting the credit action lines (in particular in relation to enterprises) to this day bear the consequences of the financial crisis. Having demonstrated the effectiveness of BIK’s scoring tools in limiting NPL level, we are prompted to pay special attention to the legitimacy of applying these tools, especially in light of the current threat of a financial crisis and its consequences for the future timeliness of repayments by the clients.

The conclusions presented in this article have a statistical justification. However, it should be taken into account that they were developed on the basis of a relatively small sample. The reason for its limitation was the somewhat low return of the survey addressed to the management staff of cooperative banks of the BPS S.A. association. If the research is continued in the future, it is necessary to increase the research sample.

{kind=link}

{kind=link}

{kind=link}

{kind=link}