1. Introduction

Agriculture activity is risky, and farmers are risk-averse by nature. However, risk aversion is a relative concept, and can vary according to the context and circumstances (

Iyer et al. 2020). In fact, farmers face different kind of risks, including those related to yield and price variability, which impact profitability (

Trestini et al. 2017). As shown by

Spiegel et al. (

2020), farmers mainly worry about economic challenges, rather than environmental, social, and institutional challenges.

According to economic theory, price volatility should incentivise farmers to adopt risk management tools (RMTs), and increasing uncertainty should increase the latent demand for RMTs (

Coletta et al. 2018). These authors investigated behavioural aspects linked to choices under risk and ambiguity, accounting for time preferences in order to mimic the scenario faced by potential adopters of the subsidised crop insurance contracts in Italy. An important aspect is to educate farmers, in order to improve their awareness of the possibility and importance of agriculture insurance, as outlined by

Njegomir et al. (

2016). However, the farms most at risk are more likely to have insurance, and this decision is positively related to the past number of claims (

Enjolras and Sentis 2011). Moreover, as highlighted by

Biagini et al. (

2020), increasing farm income is a way to improve farm welfare, even if, under certain circumstances, risk management has a significant impact on farm productivity (

Vigani and Kathage 2019). The Common Agricultural Policy (CAP) is playing an increasingly important role in this, through tools aimed at stabilising farm income. Authors such as

Bozzola and Finger (

2021) have studied farmers’ risk attitudes, which change over time as a function of both climate shocks and political regimes. Their analysis indicates that risk-aversion coefficients tend to increase with each introduction of a policy change.

In recent years, many other authors have analysed the risk management system, given the growing interest based on the need to stabilise farmers’ incomes. In this regard,

Trestini et al. (

2017) aimed at identifying potential beneficiaries of Income Stabilisation Tool (IST) compensation within the Italian agricultural population, focusing on the Veneto region.

Severini et al. (

2019) examined the impact of the IST and found that its introduction would lead to a significant reduction in income variability in Italian agriculture. Furthermore, farming systems are increasingly facing the unknown, with uncertainty and surprises; this led

Meuwissen et al. (

2019) to explore the broader issue of the resilience of farming systems, particularly the arable farming system in the Netherlands.

In this work, we focus on the new revenue insurance products and their potential in Italy, starting from studies on the topic performed in the USA, according to

Skees et al. (

1998). In fact, the USA has consolidated experience with risk management, and specifically with the revenue insurance policy. This tool was first available in 1996 under the federal crop insurance program, and was initially used for corn, soybeans, wheat, and cotton in a limited number of counties. In the late 1990s, the availability of revenue insurance increased, and by 2006 it represented 57% of all surfaces insured under the federal crop insurance program (

Dismukes and Coble 2007). In this regard, some authors have investigated the effects of federal insurance provision on the acreage and yield of specific crops, as outlined by

Shi et al. (

2019), considering five major types of specialty crops in California (apples, wine grapes, dry plums, English walnuts, and dry beans).

In recent years, new products have emerged to help farmers with risk management. Among them, we cite the revenue insurance products, the effects of which have been studied in the southern USA. While there are reasons to believe that revenue insurance should be attractive in this part of the country, any revenue products that use existing crop insurance rates face difficulties, as poor actuarial performance in the southern USA has resulted in relatively high rates. Other authors have made important contributions to the topic; for example,

Zhu et al. (

2008) took a close look at the efficiency of whole-farm insurance using a copula model approach, and analysed the case where a crop producer growing corn and soybeans faces both yield and price risk.

We studied this topic by considering a new model of risk management in agriculture, starting from the considerations of

Markovic and Kokot (

2018). Those authors present a novel insurance model that has been applied in the USA since 2015. In this model, each farm insures its expected total revenue, which can be endangered due to the effects of natural and climate risks, as well as market risks, which can arise through fluctuations in market prices. According to the authors, by using a clear strategy on the state level and establishing a legal framework and financial incentives, the insurance model could be successfully implemented in other parts of the world, and thus insure a larger number of farmers, especially those whose activity takes place in climatically unstable areas. Moreover, using a multi-commodity agricultural market model,

Pieralli et al. (

2021) investigated the potential budgetary consequences of introducing two specific risk management schemes into the CAP that were already investigated in the USA, the Agriculture Risk Coverage and Price Loss Coverage.

The emergence of modern risk management in agriculture is becoming increasingly focused on insuring total farm revenue (

Turvey 2012). The aim of whole-farm insurance is to cover all risks that threaten the farm under a unique insurance policy, according to

Markovic and Kokot (

2018). Although multiple risks are considered simultaneously, this approach may be more efficient, but also more complicated, as shown by

Huirne et al. (

2007).

In this paper, we aim to contribute to the debate on risk management, in particular on the revenue insurance policy recently adopted in Italy. In this country, although still not very widespread, the policy has shown high potential for development, attracting the attention of farmers, especially in the sectors mainly exposed to price volatility. However, there is no similar approach in the literature for studying the revenue insurance policy, as it is an innovative income stabilisation tool, in some ways comparable to other experiences, such as the IST provided by the 2014–2020 CAP (

Trestini et al. 2017;

Severini et al. 2019) or by the risk management system in the USA (

Skees et al. 1998;

Zhu et al. 2008), but it is defined by a national Ministerial Decree and is not present in other countries.

We first simulate how the revenue insurance policy works with a sample of farms from the Italian Farm Accountancy Data Network (FADN). Second, we probe the convenience of the policy for both farmers and insurance companies. To summarise, from the point of view of economic analysis at the national level, with this paper we aim to investigate and evaluate the numbers and types of farms that may have an economic interest in the revenue insurance policy, starting from business and market variables and showing the economic sustainability of this new insurance product.

This paper is organised as follows.

Section 2 describes risk management policies in Italy and the CAP.

Section 3 introduces the methodology used to study the feasibility of the revenue insurance policy using data collected from the Italian FADN on farms growing common and durum wheat.

Section 4 reports the results of this study, and shows the economic sustainability of the revenue insurance policy over the long term.

Section 5 presents the conclusions of this paper.

2. Risk Management in the Italian System

In Italy, public intervention in agricultural risk management has a long tradition. The Fondo di Solidarietà Nazionale (FSN) was developed in the 1970s with the aim of compensating farmers whose farms were affected by natural disasters (

Santeramo et al. 2016). Since the 1990s, the national policy has been redefined, passing through contributory and credit operations to insurance coverage (

Capitanio and Pin 2018a). Later, with the implementation of Legislative Decree 102/2004, national agricultural insurance plans have paved the way for new guarantees and new types of policies, such as single-risk and multi-risk insurance policies. In this way, all adverse climate conditions are insurable in all regions.

With the introduction of the Health Check, the topic of risk management in agriculture (and the subsequent public support for the instrument) began to be discussed at the European level (

Capitanio and Pin 2018b). In particular, Article 68 of Reg. (EC) 73/2009 no longer represents a form of partial decoupling, but rather a specific support. Member States can use a ceiling of up to 10% of the national ceiling for direct payments for some new measures proposed by the regulation, including two related to risk management (

Frascarelli 2016): (i) measure (d) provides for contributions to harvest insurance premiums that cover the risks of natural disasters (Art. 70, Reg. (EC) 73/2009), and (ii) measure (e) concerns contributions to mutual funds for damage arising from plant or animal diseases (Art. 71, Reg. (EC) 73/2009). Therefore, the subsidised insurance tool has become an integral part of the CAP, under Article 68 of Reg. (EC) 73/2009, and of the wine, fruit, and vegetable section of the Common Market Organisation (Reg. (EC) 479/2008 and Reg. (EC) 1234/2007).

In recent planning in 2014–2020, the European Union supported risk management systems among its six intervention priorities. With this reform, the risk management tools have been transferred to the second pillar under the regulation on support for rural development (

García Azcárate et al. 2016). Reg. (EU) 1305/2013 laid down three specific measures that Member States can include in their 2014–2020 Rural Development Programmes: (i) crop, animal, and plant insurance (art. 37), (ii) mutual funds for epizootic and plant diseases and environmental emergencies (art. 38), and (iii) income stabilisation tools (art. 39).

Agricultural insurance is an important risk management tool for farmers and is becoming increasingly important as an agricultural policy tool, both in Europe and the USA (

Cordier 2015). In particular, Italy has paid close attention to insurance tools and is one of the European countries making a greater effort to support the subsidised insurance market, which remains the basis of the risk management system. In fact, the other Member States have different attitudes towards risk management in agriculture. Suffice it to say that only 11 Member States have decided to activate the risk management tools offered by the second pillar of the 2014–2020 CAP. Among these, only France, Italy, and Portugal have offered EU support for mutual funds and only Italy and Hungary have also activated IST.

However, in recent years, the subsidised risk management system in Italy has been characterised by (i) gradual disaffection of farmers, (ii) a low penetration of insurance in the arable sector, and (iii) a greater need for insurance coverage against market risks. For these reasons, starting in 2017, the National Agricultural Insurance Plan has provided new possibilities for covering risks (

ISMEA 2018). In fact, although subsidised insurance is part of the risk management system foreseen by measure 17 of the 2014–2020 CAP, Italy decided to launch, through national funding, an experiment on the dissemination of two innovative policies, the revenue and index-based insurance policies, providing, in addition to the public contribution to the cost, a financial line specifically for the reinsurance of these policies.

3. Revenue Insurance Policy in Italy

In Italy, the revenue insurance policy was introduced in 2017 within the field of risk management in agriculture. Ministerial Decree 10405/2017 defined revenue insurance policies as insurance contracts that cover the loss of revenue from insured production. The loss is determined by a combination of yield reduction due to catastrophic events (ice and frost, drought, and flood), frequency (excess snow and rain, hail, and strong wind), accessory (sunstroke and hot wind, temperature changes), and reduced market prices. This type of insurance policy, therefore, is aimed at guaranteeing certain revenue for farmers, as it also covers price variability in addition to damage due to adverse weather conditions. The possibility that the loss of revenue could also be associated with the price component places this particular insurance policy at the boundary between insurance and financial products.

Farmers can subscribe to this policy, which is still experimental, exclusively for generic common wheat (Code H11, ID variety 2) and generic durum wheat (Code H10, ID variety 1). The policy is facilitated with resources from the FSN, and the public contribution is equal to a maximum of 65% of the eligible expenditure, within the limits of budget availability. Compensation is provided for a revenue reduction exceeding a threshold of 20%, to be applied to the insured revenue, and the policy is paid based on product-municipality and not plot of land. Further details on how the revenue insurance policy works are given in the next section.

3.1. Data and Methodology

This research is based on data from the Farm Accountancy Data Network (FADN), the only harmonised European source on farm management. It is a sample survey carried out in all Member States of the European Union about agricultural farms as regards income evolution and economic structural dynamics.

Specifically, this data source allows us to focus on several farms operating in the common and durum wheat sectors in the period 2008–2018. In order to have a homogeneous sample, we decided to consider only those farms that, in the considered period, had cultivated wheat (common or durum) for at least 7 out of 11 years (not necessarily consecutive). Finally, our analysis focused on 583 farms operating in the common wheat sector and 643 farms in the durum wheat sector. Data extracted from FADN deal with the surface (in hectares, ha) assigned by the sampled farms for cultivation of wheat in each year, as well as declared production. Given these two pieces of information, final yield is calculated in terms of tonnes per hectare (t/ha) for each farm and each year.

According to Ministerial Decree 10405/2017, which introduced the revenue insurance policy in Italy, we propose some notations and formulas that allow us to detail its operation.

First of all, the revenue insurance policy is based on the following four quantities:

Final (or actual) yield of farm i in year t, denoted by Y1it, obtained as mentioned above;

Potential yield of farm i, denoted by Y0i. In the absence of details on the benchmark yields per municipality, we approximated the potential yield of farm i as the Olympic mean of its final yield over the considered period. This is considered as the insurable yield. As is known, the Olympic mean is computed as the mean of a series after removing the minimum and the maximum values;

Initial prices, denoted by

P0t. These represent the maximum insurable prices equal to the average prices over the three years prior to the insurance campaign. They are provided by a specific ministerial decree with regard to identifying the maximum unit prices of agricultural production applicable to determining insurable values on the subsidised market (see

Table 1);

Final prices, denoted by

P1t; these represent the prices actually achieved by farmers and are obtained as mean prices detected by the Institute of Services for the Agricultural and Food Market (ISMEA) in the period July–September of the harvest year (see

Table 1).

According to the four quantities described above, for each farm

i and each year

t, it is possible to compute the insured and actual revenue, denoted by

R0it and

R1it, respectively, as follows:

where

Sit is the surface used for wheat cultivation by farm

i in year

t.

The revenue policy operates as any typical insurance policy. First, if a farm does not cultivate wheat in a certain year (deducible by the missing values in the surface and/or the final yield for a certain year), the farm does not stipulate the revenue insurance policy in that year. Otherwise, the farm ensures potential income R0it, obtained according to potential yield Y0i (computed for the whole period) and initial prices P0t. Then, when actual yield Y1it and final prices P1t are available, effective income R1it can be obtained and compared with the insured value.

Therefore, the farm is eligible for compensation if the damage (in terms of percentage decrease in actual revenue with respect to insured revenue) is greater than 20% (threshold); in the formula, we have the following:

In this case, the amount of compensation,

Cit, is the difference between insured and actual income after considering a 20% allowance:

Regardless of eligibility for reimbursement, the farm bears a cost for the policy (i.e., the premium, denoted by

PRit), obtained by applying a rate

r to the insured income:

Finally, the government covers part of this cost, by providing public funding to the farm equal to 65% of the premium. Consequently, the effective cost for insurance, denoted by

ECit, is as follows:

3.2. Optimal Rate (Economic Convenience of Policy)

The main focus of this paper is to evaluate the economic convenience of the revenue insurance policy. Specifically, the purpose is to identify a rate r such that the policy stipulation is overall sustainable for both farms and insurance companies. In order to determine the optimal rate, denoted by ropt, an analysis of economic convenience is performed on both sides of the market.

On the insurance company side, economic advantage is measured through the loss ratio indicator, obtained by dividing reimbursements paid over premiums cashed in. From the long-term perspective, it should be close to 0.7 (this benchmark was obtained based on interviews with five of the main insurance companies in Italy), so that the insurance company exceeds its break-even point, hence the insurance premiums are greater than the compensations paid. In fact, 30% of the premium is allocated to expenses related to experts, commissions for the sellers of the policies, administrative management of the company, reinsurance, and profit for the insurance company. In order to determine the optimal rate, the long-term loss ratio (

LR) is computed as the mean of the average loss ratios per year (

LRt), which in turn are obtained as the mean of the “individual” loss ratios: both mean computations are weighted through the cultivated surface, as shown in the following. Specifically, the individual (i.e., farm- and year-specific) loss ratio, denoted by

LRit, is calculated as the ratio between compensation and premium related to farm

i and year

t: The average loss ratio per year is the mean of

LRit, weighted by the surface cultivated by farm

i in year

t, Sit:

where the summation is over farms with policies in year

t, and

Finally, the long-term loss ratio,

LR, is obtained as the mean of

LRt, weighted by the total surface cultivated in year

t, St:

where

, and the summation is over the whole period.

If we consider this global index as a function of rate

r, the convenience function for insurance companies,

I(r), can be written, after some mathematical manipulations, as follows:

This function decreases with respect to rate

r (the greater the rate, the lower the overall loss ratio) and depends on the quantity within the square brackets, that is, the mean of the means of the ratios between compensations and insured revenues, over farms and years. By denoting this latter quantity by

A and equating Function (9) to 0.7 (the benchmark), we can analytically obtain the optimal rate,

ropt, as follows:

On the other hand, economic advantage from the farm’s point of view can be measured by the ratio between obtained compensation and actual cost of insurance (hence, net of public funding). In this regard, the long-term index is, again, the mean of the means of individual ratios (

Cit/

ECit) over farms and years and weighted by the cultivated surface. It is denoted by

F(r) and computed as follows:

As we can see, F(r) and I(r) are very similar functions, differing only as regards the quantity involved in the summation over farms (index i). Hence, their ratio, F(r)/I(r), is constant and equal to B/A = 1/0.35. For this reason, if ropt is such that I(ropt) = 0.7, then the ratio reimbursements/actual costs, F(ropt), is equal to 0.7(1/0.35) = 2, that is, the compensation received is twice the actual cost of the policy, on average.

To summarise, the optimal rate is initially obtained by ensuring the economic convenience from the insurance company side (overall loss ratio equal to 0.7). This rate is also convenient from the farmers’ side, as it allows double remuneration to be obtained for the cost of the policy.

4. Results

The quantities reported in

Section 3.1 were computed (if possible) for each farm

i and each year

t (from 2008 to 2018) separately for the two species of wheat (common and durum). First, revenues

R0it and

R1it were calculated according to the formulas in (1). As outlined before, these are the most important quantities, as they determine whether an individual farm is eligible for reimbursement in a specific year.

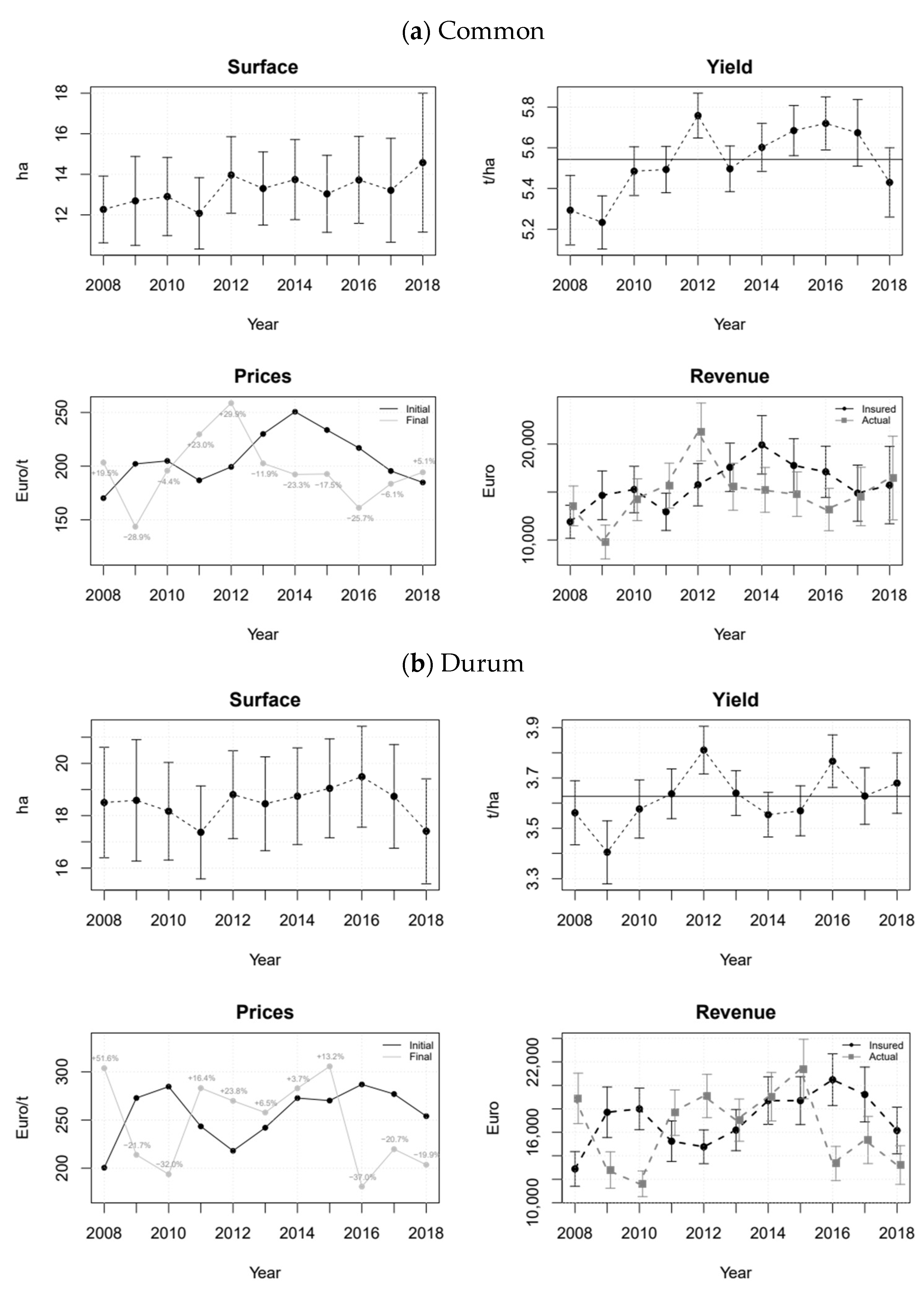

A summary of initial and actual revenues is reported in the bottom right panel of

Figure 1a (common wheat) and

Figure 1b (durum wheat), together with the other quantities that contribute to their calculation: cultivated surfaces (top left panel), average yields (top right) and prices (bottom left). For each one (except for prices), the mean value is depicted, together with its 95% confidence interval. By inspecting these plots, it can be observed that, for common wheat, the cultivated surface exhibited a slight increasing trend (from 12 to 14.5 ha, on average), although the mean surfaces in 2008 and 2018 were not significantly different. As far as the actual yield is concerned, in 2008 and 2009 the average yield was significantly lower than the mean of insurable yields over the whole period (horizontal line), while in 2012 it was significantly higher. However, in 2008, despite a lower actual than insurable yield, on average, actual revenues were similar (again, on average) to insured revenues, due to an increase in final prices (+19.5%). Consequently, we would expect a small share of compensated farms. In fact, by observing

Table 2, the effective number of farms that received reimbursement in 2008 was 31 out of 394 farms with a policy. In 2009, a yield below the average was coupled with a decrease in final prices (−28.9%), leading to significantly lower actual than insured revenues. Consequently, in that year we would expect a high percentage of farms eligible for compensation (in particular, 379 out of 425 farms had access to compensation; see again

Table 2). Conversely, in 2012, as the real yield was above the average and the prices exhibited a large increase (+29.9%), actual revenues were greater than insured revenues, and we would expect a small share of compensated farms. In fact, according to

Table 2, only 5 out of 536 farms were eligible for compensation in 2012.

As far as the durum wheat sector is concerned, the cultivated surface was almost constant (around 18.5 ha) over the considered period, except for 2011 and 2018, when it was close to 17.5 ha. Regarding actual yields, a fluctuating trend can be outlined. Specifically, in 2009 the real yield was significantly lower than the average, while in 2012 and 2016 it was significantly higher. In fact, in 2009, insured revenues were significantly greater than actual revenues, probably due to a drop in final prices (−21.7%); consequently, a high percentage of farms eligible for compensation would be expected. In fact, as shown in

Table 3, the effective number of farms that received reimbursement in 2009 was 264 out of 391 farms with a policy.

Two opposite situations occurred in 2012 and 2016, despite above-average yields. In 2012, actual revenues were much greater than insured revenues, based on an increase in final prices (+23.8%) together with real yields greater than the average. That year, a smaller share of compensated farms would be expected: only 7 out of 616 farms received compensation de facto (see

Table 3). On the other hand, in 2016, a drop in final prices (−37%) jeopardised real yields above the insurable mean, leading to much lower actual than insured revenues, which in turn involved compensation for 472 out of 544 farms (

Table 3). Moreover, other situations, not directly deducible from the yield panel (due to differences in prices), are related to 2008 and 2010, when actual and insured revenues differed significantly (greater and lower, respectively) due to important changes in final prices with respect to initial prices (+51.6% and −32%, respectively). Therefore, we would expect a small share of compensated farms in 2008 (8 out of 375 farms, effectively), and a large share in 2010 (417 out of 480 farms de facto).

According to the revenue insurance policy operational mode (described in

Section 3.1), and given the insured and actual revenues just summarised, we evaluated the eligibility for compensation for each farm

i in each year

t. This assessment is outlined in

Table 2 and

Table 3, where for each year we report the number of stipulated policies and farms with access to compensation, and the total and mean of initial income (equivalent to total insured value), final income and compensation per hectare.

Looking at the descriptive statistics reported in

Table 2, related to the common wheat market, we note that in almost every year, more than 80% of farms would have obtained the insurance policy. It is important to note that the share of non-insured farms did not grow wheat in the considered period; this is why they did not obtain a policy.

The only exceptions were in 2008, 2009, 2017, and 2018, although the percentage never goes below 50%. We then determined the shares of farms that would have received compensation by dividing the number of farms with reimbursement by the amount of policies. We can observe three evident peaks related to 2009, 2014, and 2016 (89.2, 57.5, and 66.2% of farms, respectively, received reimbursement). In those three years, as shown in

Figure 1a, a large discrepancy between insured and actual revenues is evident, also with reference to the mean per hectare (on average, 1121 vs. 752 in 2009, 1389 vs. 1077 in 2014, and 1206 vs. 922 in 2016). Finally, 2009 represents the year with the greatest average compensation (2015), followed by 2014 and 2016 (1170 and 1115, respectively, on average). On the other hand, in 2011 and 2012, a very small share of farms received reimbursement (3.1 and 0.9%, respectively). In those years, it can be seen that actual income was higher than insured income (1262 vs. 1038 in 2011 and 1490 vs. 1105 in 2012 per ha, on average).

Regarding the durum wheat market (

Table 3), we can observe a similar trend to that for common wheat. A very high percentage of farms would have obtained the revenue insurance policy from 2010 to 2017 (with the highest percentage, 95.8%, in 2012), while the share was lower (although greater than 50%) at the beginning and end of the considered period (2008, 2009, and 2018). Regarding farms eligible for compensation, we can observe a percentage of reimbursed farms greater than or around 50% in five years (2009, 2010, 2016, 2017, and 2018), while in the remaining years this share almost never goes beyond 10%. In particular, in 2009, 2010, and 2016, as seen in

Figure 1b, there was a considerable difference between insured and actual revenues (992 vs. 728 in 2009, 1027 vs. 692 in 2010, and 1040 vs. 681 in 2016 per ha, on average). The highest average compensation was obtained in 2016 (3233), followed by 2010 and 2009 (2980 and 1850, respectively, on average). On the other hand, in 2012 and 2008 a very small share of farms received reimbursement (1.1 and 2.1%, respectively).

4.1. Optimal Rate

The procedure for obtaining the optimal rate, described in

Section 3.2, was applied separately to farms operating in the common and durum wheat sectors. Regarding the common wheat market, Equation (10) allows us to obtain an optimal rate equal to 0.051, as

A is about 0.0357. The optimal rate for durum wheat is equal to 0.0709 (A ≈ 0.0496). As outlined above, the optimal rate is such that the long-term loss ratio is equal to 0.7; consequently, this leads to a long-term compensation/actual cost ratio equal to 2.

Considering the optimal rates,

Table 4 shows the (weighted) means of the economic convenience indicators for insurance companies and farms for each year

t. In the last column, an indicator related to the public sector is also shown: the individual index (i.e., for each farm and each year), labelled

PSit, is computed as the relative difference between the compensation obtained by farm

i in year

t and the public funding received:

where

Fit = 0.65

PRit is the public funding received by farm

i in year

t. Overall, this index assumes a positive value if reimbursement is greater than funding, and it becomes −1 if there is no compensation.

Regarding the common wheat sector, even if the (weighted) long-period loss ratio is equal to the break-even point (0.7), we note very different situations from year to year. In particular, the policy stipulation was almost always advantageous for insurance companies, as the average loss ratio indicator was lower than 0.7 in all years but 2009, 2014, and 2016 (with values of 2.69, 1.23, and 1.30, respectively). In fact, in those three years the average loss ratio was largely beyond the break-even point, due to the large proportion of reimbursed farms (and total amount of compensation), which led to negative results for insurance companies. Of course, on the other hand, those three years are characterised by high economic convenience from the farms’ point of view (the average ratio between compensation and actual costs was 7.69 in 2009, 3.51 in 2014, and 3.72 in 2016), due to a large amount of farms with compensation. In the remaining years, the reimbursement/actual cost ratio is well below 1, with the exception of 2015, which reflects long-term ratios with an average loss ratio almost equal to the break-even point and an average compensation/actual cost ratio almost equal to 2. Finally, regarding the public sector, the indicator runs approximately the same as that of farms, with positive values in 2009 (indicator equal to 3.23), 2014 (0.82), 2015 (0.06), and 2016 (1.25), which means that reimbursements were greater than public funding, and negative values in the other years.

Regarding the durum wheat sector, similar conclusions can be drawn. In particular, in 2009, 2010, and 2016, due to a very large share of farms eligible for compensation (see

Table 3), the average loss ratio is consistently above the break-even point (1.51, 2.41, and 2.19, respectively) but, on the other hand, they were very advantageous years for farms (average ratio between compensation and actual cost is 4.30 in 2009, 6.88 in 2010, and 6.26 in 2016), as well as for the public sector. As we can see, the related indicator runs approximately in tandem with that of farms, with positive values (hence, reimbursements greater than public funding) in 2009 (equal to 1.21), 2010 (2.13), and 2016 (2.40).

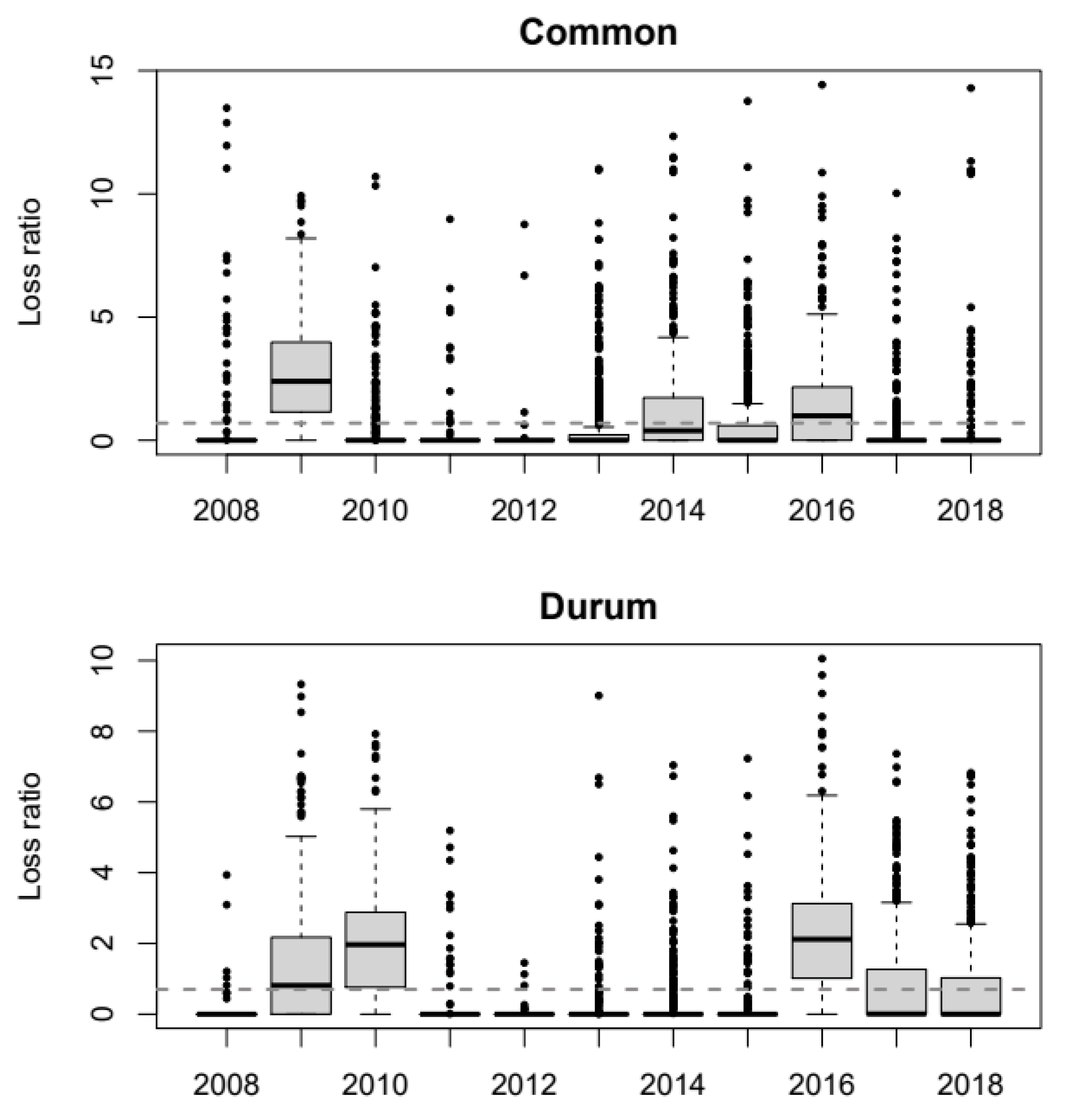

As a final remark on this heterogeneity from year to year, the graph reported in

Figure 2 is useful. It shows boxplots of the individual loss ratio distribution for each year separately for each wheat sector. Although the long-term (2008–2018) loss ratio is equal to 0.7 in both wheat sectors, the situations are very heterogeneous. The same also applies if we consider the distribution of compensation/actual cost ratio (farm’s side), as it is proportional to the loss ratio.

By inspecting the boxplots, we note that, in certain years, the box is very narrow and only outliers draw attention. This means that the distribution “shrinks” around 0 (the median, but also the minimum value). In other years, the boxplot is clearly “visible”, evidence that the distribution is far from 0. As an example, regarding the common wheat sector, in 2009, 2014, 2015, and 2016 we can observe very high values (i.e., far from 0) of the individual loss ratio, although in 2009 the box lies far above the 0.7 level (dashed grey line).

Regarding the durum wheat sector, similar conclusions can be drawn. In 2009, 2010, 2016, 2017, and 2018 we note very high values (i.e., far from 0) of the individual loss ratio, although in 2010 and 2016 the box is far above the 0.7 level.

4.2. Yield and Price Effect

The revenue insurance policy is a contract that covers the loss of revenue from insured production, as outlined in

Section 3. The loss is determined by a combination of yield reduction due to climate adversity and market price reductions. For this reason, it is interesting to assess the impact of yield and price on compensation, for both common and durum wheat. In particular, we consider two extreme situations: (i) by setting the final prices equal to the initial ones (i.e.,

P1t =

P0t), it is possible isolate the yield effect, and (ii) the price effect is highlighted by equating actual and insured yield (i.e.,

Y1it =

Y0i).

For each year, we computed the total amount of compensation in the two extreme situations, that is, the sum of compensation received by farms under the “only yield” effect (i.e., constant prices) or the “only price” effect (constant yield, then actual yield equal to insured yield). Furthermore, we assume that if the price and yield effect occur at the same time, the final compensation would be the sum of the “only yield” and “only price” compensation.

Results are reported in

Table 5, which shows, for each year and each type of wheat, the share (in percentage) of compensation due to price and yield effect. For example, looking at the common wheat market, in 2009 we can observe a yield effect share equal to 15.4%; this means that in that year, if we isolated the two effects (yield and price), around 15% of total compensation would be due to reductions in yield (due to climate adversity), while most of the reimbursement is generated by price reductions. To summarise, we note that adverse climate events occurred with lesser or greater intensity and frequency within the considered period; however, the price effect significantly weighed on compensation in three years (2009, around 85%; 2014, around 80%; and 2016, around 91%). In all other years, compensation was exclusively linked to the yield effect.

Regarding the durum wheat market, we can observe a similar trend to that observed for common wheat. In this case, the price effect has an impact on durum wheat only in four out of nine years (2009, 2010, 2016, and 2017), in which it weighs on compensation by around 32, 80, 95, and 33%, respectively. In all other years, the compensation is exclusively due to reduction in yield.

5. Conclusions

All economic activities are subject to multiple sources of risk, especially in the agricultural sector, as it is particularly sensitive to climate change (

Mendelsohn et al. 1994). An analysis carried out by the Intergovernmental Panel on Climate Change estimated that human activities have caused approximately 1.0 °C of global warming above pre-industrial levels, and it is believed that this will reach 1.5 °C between 2030 and 2052 (

IPCC 2018). Climatic models project many differences in regional climate characteristics and predict increased average temperature, increased extreme hot events, and heavy rainfall. As a direct consequence of climate adversity, negative variations in outputs over the agricultural year often occur, which, combined with the rigidity of supply and demand, tend to also determine a certain volatility of agricultural markets.

Furthermore, agricultural commodity prices are also affected by economic cycles, in particular by financial crises. Over the last 15 years, agricultural commodity markets have been characterised by greater volatility and unprecedented price fluctuations, especially over the period 2007–2009. Such price volatility is not caused by a single element; rather, several factors influence the dynamics of agricultural commodity demand and supply curves (

Algieri 2014;

Baffes and Haniotis 2016).

In this context, the revenue insurance policy may be considered a very suitable tool, with the aim of guaranteeing certain revenue to farmers, as it is also able to cover price variability, in addition to damage due to adverse weather conditions.

This kind of insurance, widely used and studied, particularly in the USA (

Skees et al. 1998;

Zhu et al. 2008), has only recently been adopted in Italy. For this reason, the focus of the present paper was to verify the applicability in Italy of the revenue insurance policy, defined under Ministerial Decree 10405/2017, which is still experimental and applicable only to generic durum wheat and common wheat. Towards this aim, Italian FADN data allowed us to simulate the underwriting of the revenue insurance policy by considering a sample of farms operating in the common and durum wheat sectors during 2008–2018.

The main purpose of this work is to identify a rate such that the policy is overall sustainable for both farms and insurance companies. From the insurance company side of the market, economic advantage is measured through the loss ratio indicator (computed as the ratio between compensations paid and premiums cashed in), which should be close to 0.7. In this way, the insurance company exceeds its break-even point, hence the premiums are greater than the compensations paid. Looking at the farm side of the market, economic sustainability can be measured by the ratio between reimbursements obtained and actual costs (net of public funding). Therefore, if we first determine the policy rate by achieving the insurance company benchmark (overall loss ratio equal to 0.7), we demonstrate that the policy stipulation is also convenient for farms, as the compensation received is, on average, twice the actual cost of the policy.

To summarise, the results show that the implementation of the revenue insurance policy could be sustainable for insurance companies, which would obtain higher premiums than they pay out in reimbursements. It is also advantageous for farms as, in the time interval considered in this paper (2008–2018), they obtained, on average, double remuneration for the actual cost paid for the policy (thanks to the public contribution). The achievement of this twofold objective is fundamental, and our findings support effective adoption of the revenue insurance policy, as is the case for the other tools made available from the CAP.

In the literature, we can find some connections to the insurance revenue policy, for example, with reference to studies which have dealt with IST (

Trestini et al. 2017;

Severini et al. 2019) and insurance in the USA market (

Skees et al. 1998;

Zhu et al. 2008). However, the particular insurance tool analysed in this paper is innovative and a comparison with other studies is therefore not feasible.

In conclusion, in this context of uncertainty and unpredictability, it is the task of public intervention to continue to support farmers in risk management, directing them towards innovative policies on yields or revenues according to a holistic approach to risk management, as shown by

OECD (

2009). On the other hand, it is up to farmers to consider risk management tools as indispensable technical means to protect and stabilise their income, not only as accessories to farm activity.

Thanks to our findings, the paper provides a theoretical and practical contribution to the lively debate on risk management in agriculture. It is theoretical as this work enriches the current literature on income stabilisation (

Skees et al. 1998;

Dismukes and Coble 2007;

Zhu et al. 2008;

Trestini et al. 2017;

Markovic and Kokot 2018;

and Severini et al. 2019). Given the growing importance of considering, not only the risks related to adverse weather conditions, but also other types of risk, we analysed contracts covering the loss caused by a combination of yield reduction due to climate adversity and market price reductions. From a practical point of view, this kind of insurance policy for cereals is a novelty within EU countries, as Italy was the first country to adopt it. Our paper explored the main characteristics, the operating conditions, and the implementation methods of the policy in a sample of Italian farms and it showed the convenience of this innovative tool for both insurance companies and farmers, with the hope of stimulating the debate on risk management in agriculture and the attention of other authors towards this new insurance method.

This work has some limitations. One is related to the potential yield, namely Y0i; as outlined in the paper, it is approximated with the Olympic mean of the final yields over the considered period. As such, it does not represent the exact potential insurable yield but is only a proxy, and it results from applying a function (the Olympic mean in our case) to actual yields. As a consequence, changing the way of computing or, in general, obtaining the potential yield could modify the results. In this regard, a sensitivity analysis (by changing how to obtain potential yield) could be performed in order to better investigate this issue.

A second drawback consists in the “deterministic” facet of the analysis reported in this paper. In fact, a “probabilistic” approach could be very useful, by means of statistical modelling of quantities of interest, such as the probability of receiving compensation by farms or the total amount of compensation obtained. In this way, for example, one could investigate whether there are some farm characteristics that significantly affect the distribution of outcomes.

Finally, it is important to recall that agricultural commodity prices are affected by economic cycles. In this paper, we consider the main data (yields and prices) as given, without investigating in detail the reasons for their trends. In future development of this work, we aim to explore the impact of economic cycles on the topic.

{kind=link}

{kind=link}