Risk Factors Affecting Bancassurance Development in Poland

Abstract

1. Introduction

2. Bancassurance—Literature Overview

3. Meaning and Specificity of Bancassurance in Insurance Distribution in Poland

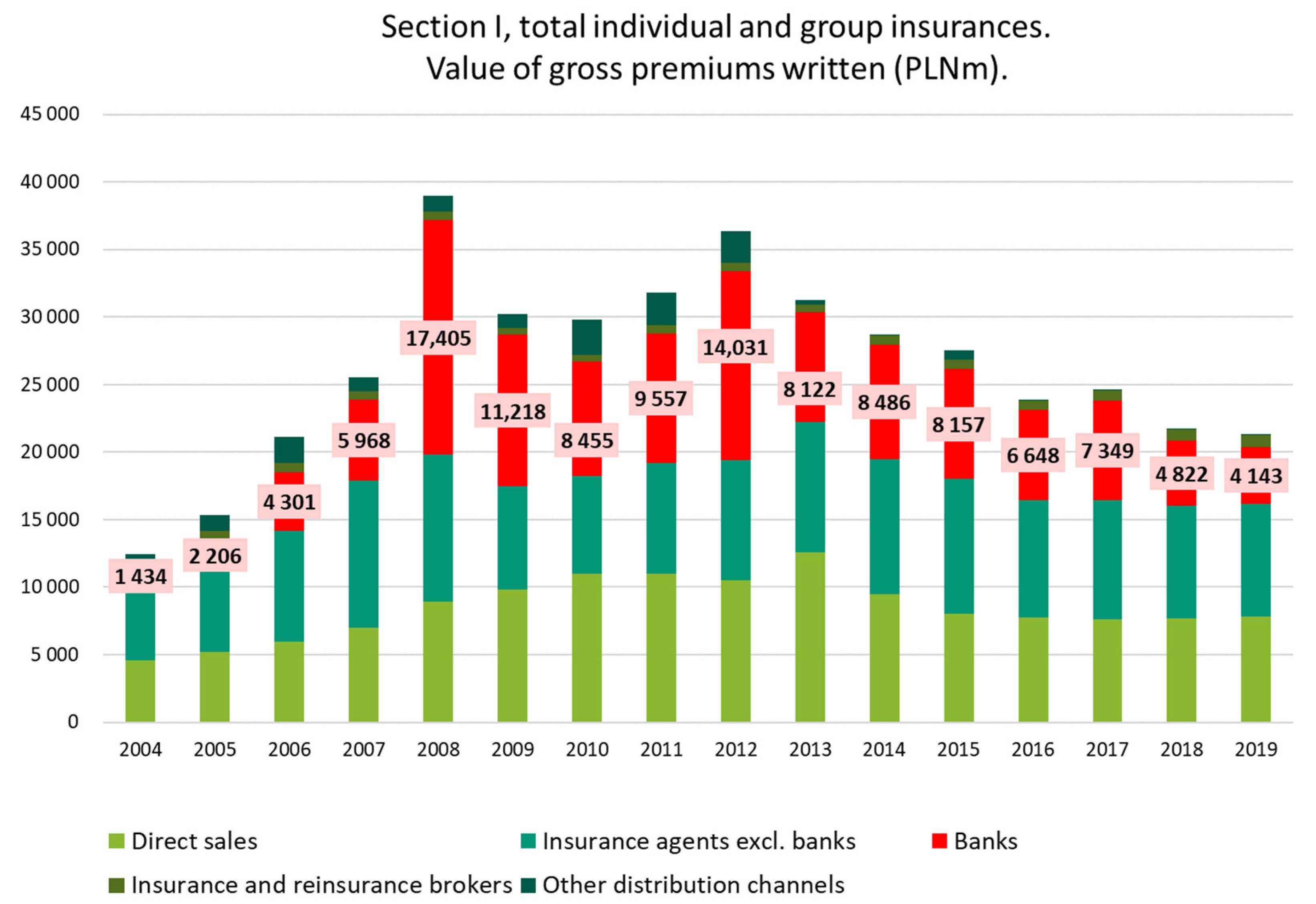

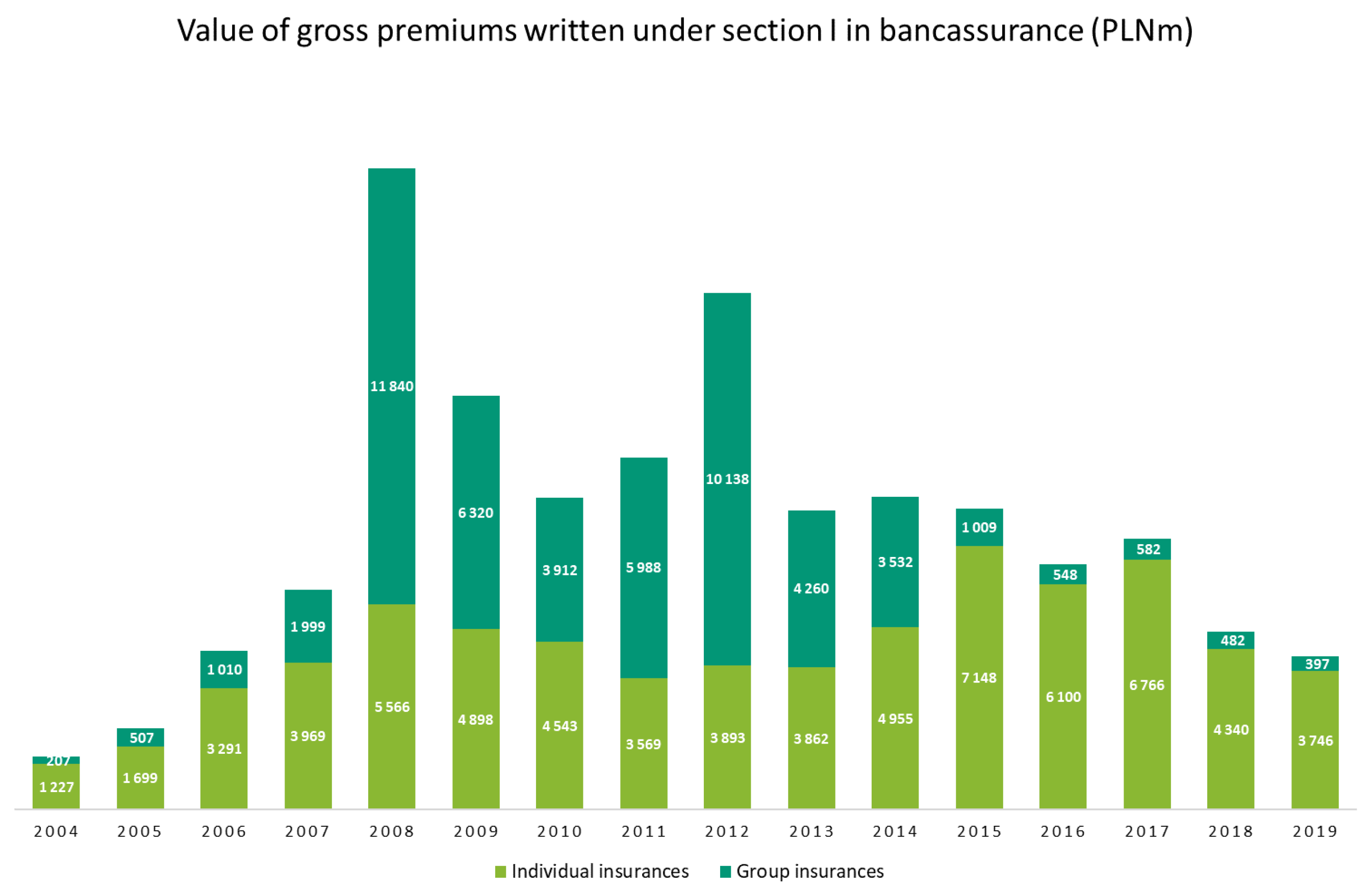

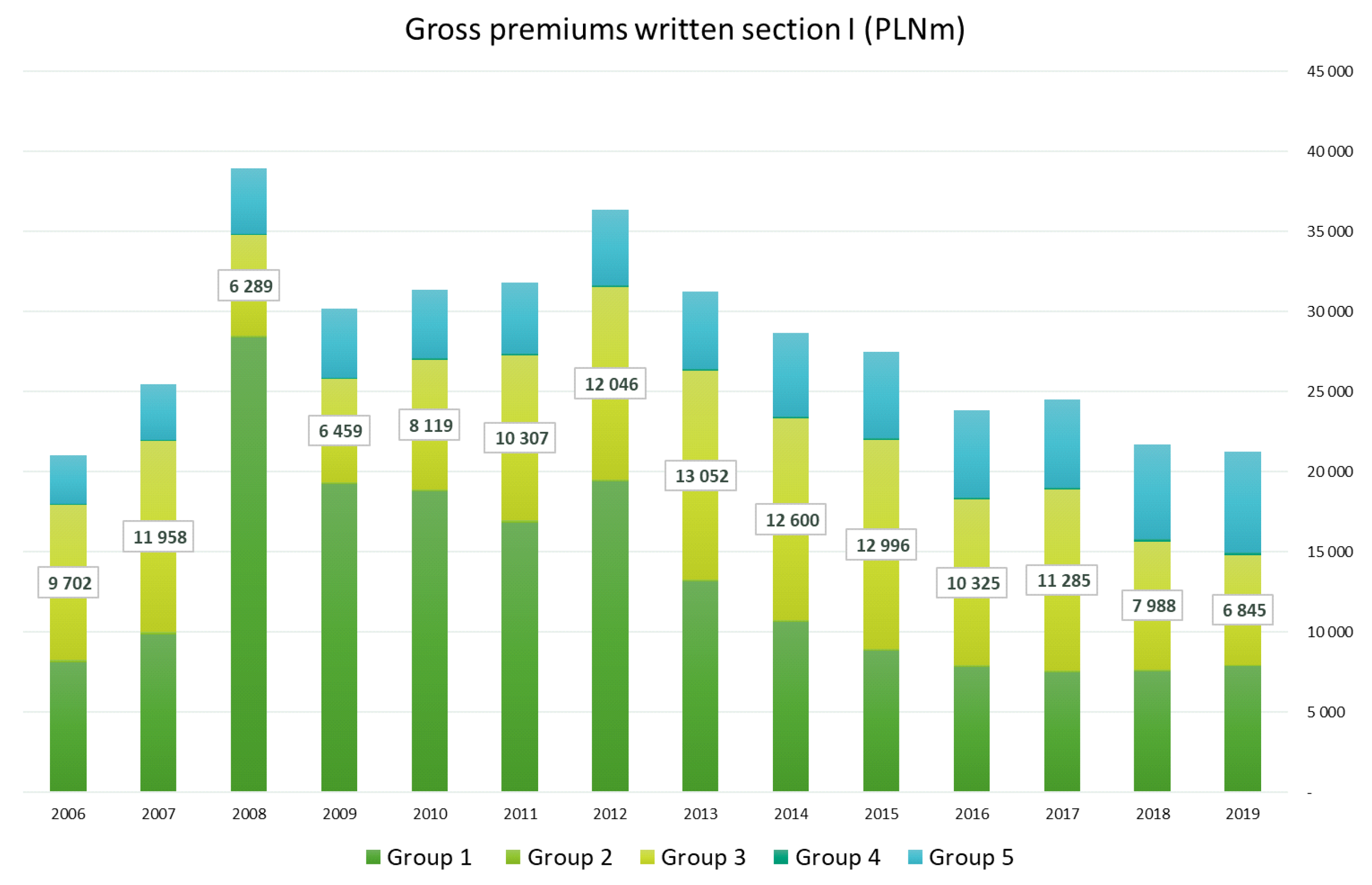

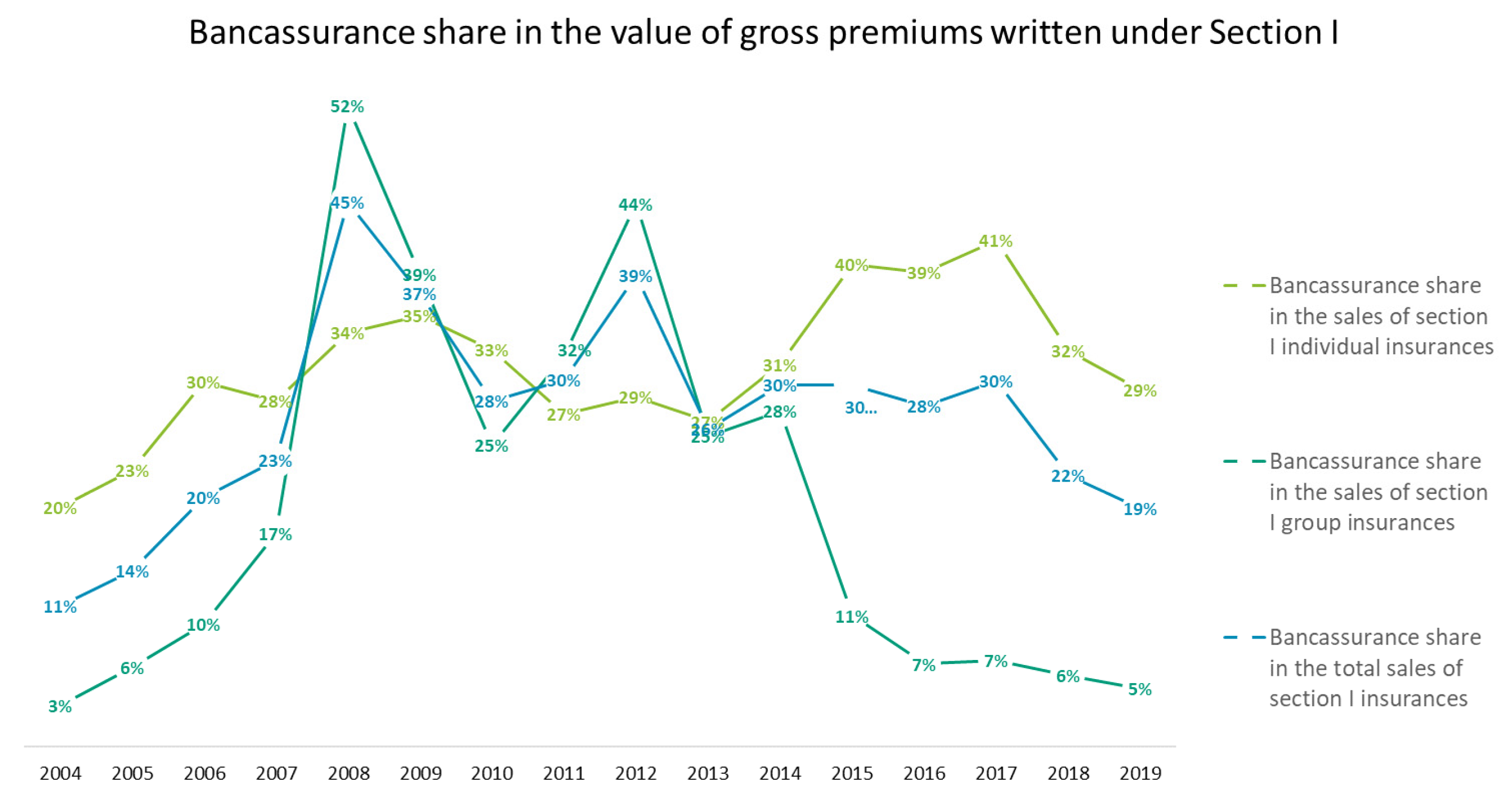

3.1. Life Insurances in Bancassurance

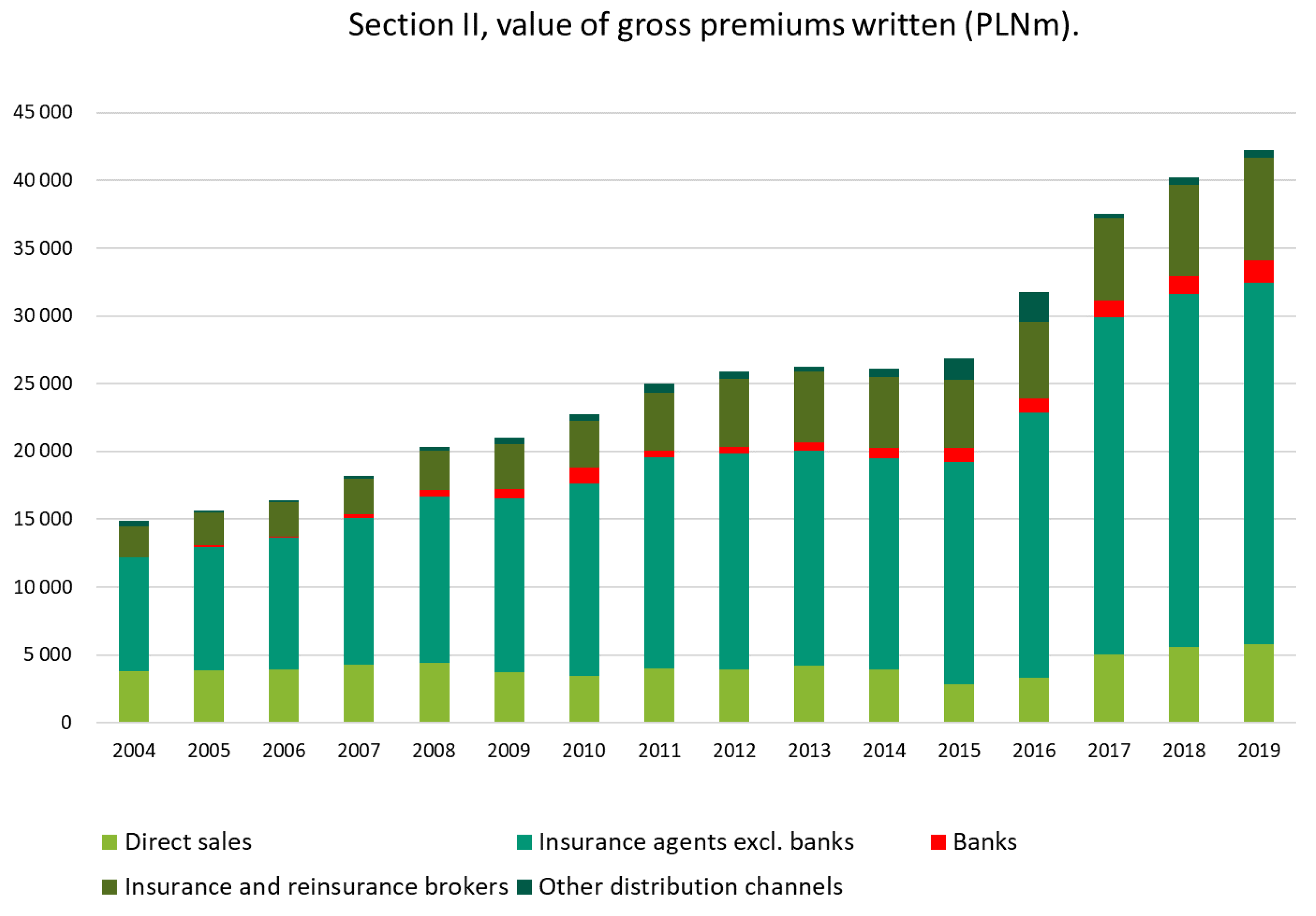

3.2. Other Personal and Property Insurances

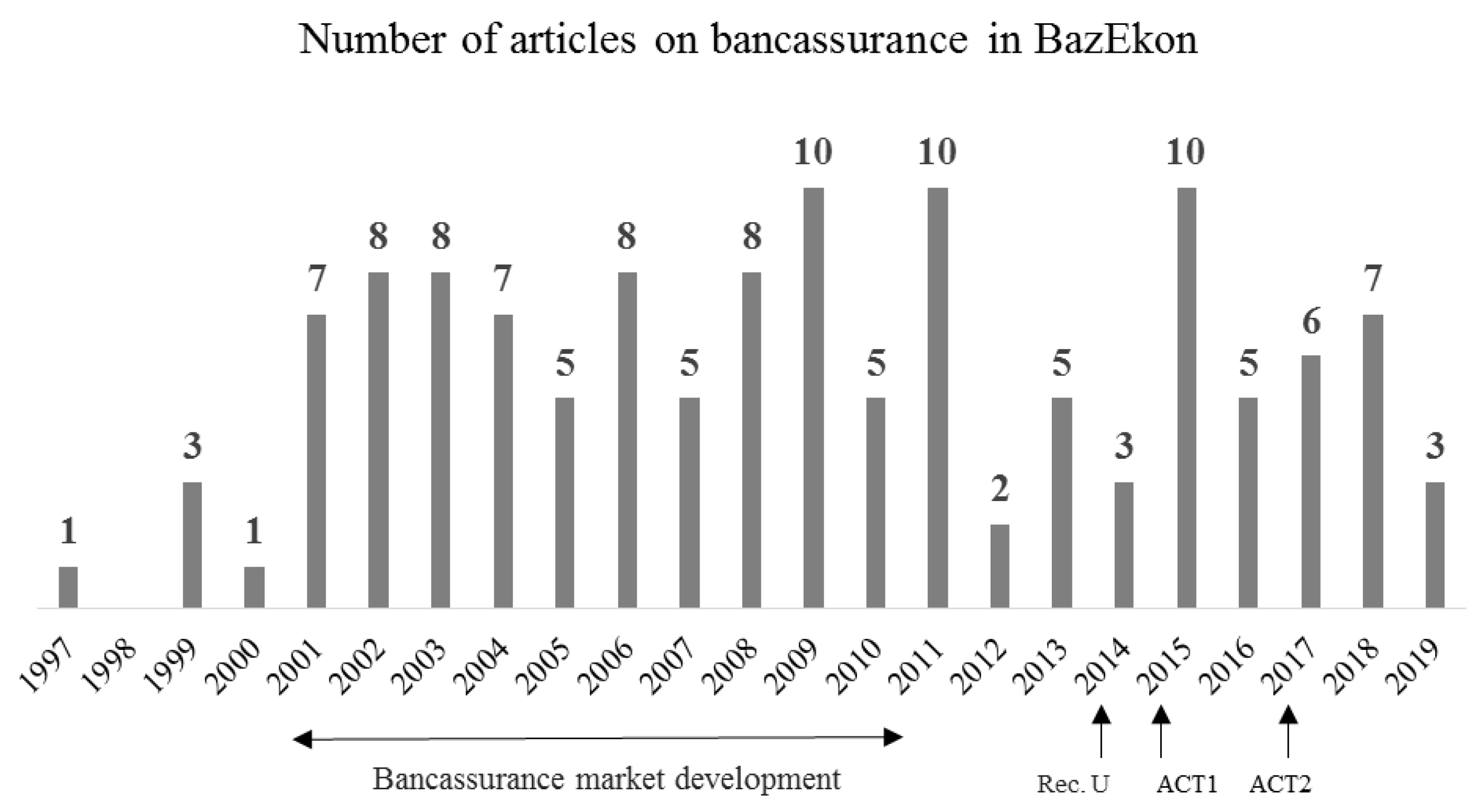

4. The Research Method and Database

5. Results and Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Survey on Bancassurance

- Your current role relating to insurance distribution:

- Natural person performing agency activities (in Polish: OFWCA)

- Expert in Agent’s Headquarters

- Management staff in Agent’s Headquarters

- Expert in the Insurance Company Headquarters

- Management staff in the Insurance Company Headquarters

- How strongly do you agree or disagree with the following statements:Key demographic, economic, market factors affecting the premiums written in bancassurance are:

I Strongly Disagree I Rather Disagree I Neither Agree Nor Disagree I Rather Agree I Strongly Agree I Have No Opinion Policyholder’s age Policyholder’s gender Policyholder’s family size (number of children, dependants) Policyholder’s earnings Policyholder’s assets Real properties owned by policyholder Insurance price Inflation Unemployment Situation on the stock exchange (e.g., WIG20 quotations) Exchange rate (EUR/PLN, CHF/PLN, etc.) Interest rate (WIBOR, etc.) - Other demographic, economic, market factors affecting premiums written in bancassurance (which ones—please list them).

- How much do you agree or not agree with the following statements:Key factors specific for the bancassurance sector affecting premiums written are:

I Strongly Disagree I Rather Disagree I Neither Agree Nor Disagree I Rather Agree I Strongly Agree I Have No Opinion Demand on cash loans Demand on mortgage loans Level of bank deposits Link of insurance with banking product (loan, payment card, etc.) Agent’s commission Caps in insurance products construction (e.g., max cost of exit in PRIIPs 4%) Changes in legal environment (e.g., ECJ judgment on returning commissions in case of early loan repayment) - Other factors specific for the bancassurance sector affecting premiums written in bancassurance (which ones—please list them):

Appendix B. Role of Banks in Insurance Distribution in Poland

| Type of Insurance Distribution Entity | Application of Banks’ Role in Insurance Distribution in Poland |

| Insurance company | No |

| Insurance agent | Yes |

| Agent offering supplementary insurance | Yes |

| Insurance broker | No |

| Policyholder in insurance contract for other party’s account | Yes |

| Source: own study. |

Appendix C. Section I (Life Insurance) Polish Market and Bancassurance Specification

References

- Act on Insurance and Reinsurance Activities. 2015. Act on Insurance and Reinsurance Activities of 11 September 2015. Polish Journal of Laws 2015, Item 1844. Available online: https://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU20150001844/U/D20151844Lj.pdf (accessed on 14 February 2020).

- Act on Mortgage Loan and Supervision over Mortgage Loan Intermediaries and Agents. 2017. Act on Mortgage Loan and Supervision over Mortgage Loan Intermediaries and Agents of 23 March 2017, Polish Journal of Laws 2017, Item 819. Available online: http://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU20170000819/U/D20170819Lj.pdf (accessed on 14 February 2020).

- Auerbach, Alan, and Laurence Kotlikoff. 1989. How Rational Is the Purchase of Life Insurance? Working Paper No. 3063. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Berekson, Leonard. 1972. Birth Order, Anxiety, Affiliation and the Purchase of Life Insurance. Journal of Risk and Insurance 39: 93–108. [Google Scholar] [CrossRef]

- Bernheim, Douglas. 1991. How Strong Are Bequest Motives? Evidence Based on Estimates of the Demand for Life Insurance and Annuities. Journal of Political Economy 99: 899–927. [Google Scholar] [CrossRef]

- Białas, Małgorzata. 2015. Polskie realia współpracy banków z ubezpieczycielami. Studia Ekonomiczne/Uniwersytet Ekonomiczny w Katowicach 225: 28–37. [Google Scholar]

- Breś-Błażejczyk, Jadwiga. 2005. Bancassurance—Sukces czy porażka? Studia i Prace Kolegium Zarządzania i Finansów, Szkoła Główna Handlowa 62: 31–40. [Google Scholar]

- Browne, Mark J., and Kihong Kim. 1993. An International Analysis of Life Insurance Demand. Journal of Risk and Insurance 60: 616–34. [Google Scholar] [CrossRef]

- Burnett, John J., and Bruce A. Palmer. 1984. Examining Life Insurance Ownership Through Demographic and Psychographic Characteristics. Journal of Risk and Insurance 51: 453–67. [Google Scholar] [CrossRef]

- Chen, Tsai-Jyh. 2019. Marketing channel, corporate reputation, and profitability of life insurers: Evidence of bancassurance in Taiwan. Geneva Papers on Risk and Insurance-Issues and Practice 44: 679–701. [Google Scholar] [CrossRef]

- Choudhury, Mousumi, and Ranjit Singh. 2021. Identifying factors influencing customer experience in bancassurance: A literature review. Journal of Commerce & Accounting Research 10: 10–22. [Google Scholar]

- Dharmaraj, Senthil. 2019. Customer perception towards bancassurance—A study of select banks in Tamilnadu. Smart Journal of Business Management Studies 15: 47–57. [Google Scholar] [CrossRef]

- Directive of the European Parliament and of the Council (EU). 2016. Directive of the European Parliament and of the Council (EU) 2016/97 of 20 January 2016 on Insurance Distribution. Available online: https://eur-lex.europa.eu/legal-content/PL/TXT/PDF/?uri=CELEX:32016L0097&from=en (accessed on 14 February 2021).

- Dobrucka, Marta. 2004. Bancassurance jako czynnik rozwoju sektora finansowego. Zeszyty Naukowe/Akademia Ekonomiczna w Krakowie 637: 127–39. [Google Scholar]

- Fan, Chiang Ku, Li-Tze Lee, Yu-Chieh Tang, and Yu Hsuang Lee. 2011. Factors of cross-buying intention—Bancassurance evidence. African Journal of Business Management 5: 7511–15. [Google Scholar]

- Ferber, Robert, and Lucy Chao Lee. 1980. Acquisition and Accumulation of Life Insurance in Early Married Life. Journal of Risk and Insurance 47: 713–34. [Google Scholar] [CrossRef]

- Gajdek, Magdalena. 2016. Bancassurance, nowe zjawisko we współczesnej bankowości. Journal of Modern Management Process 1: 18–26. [Google Scholar]

- Ganapathy, Venkatesh. 2021. Digital Bancassurance Business Models. IBM Pune Research Journal 21: 48–62. [Google Scholar]

- Gigerenzer, Greg. 2014. Risk Savvy. How to Make Good Decisions. London: Penguin Books, pp. pp. 97–99, 255–56. [Google Scholar]

- Gostomski, Eugeniusz. 2011. Perspektywy rozwoju bancassurance w Europie. Prace Naukowe Wyższej Szkoły Bankowej w Gdańsku 9: 119–30. [Google Scholar]

- GUS. 2020. Statistics of Poland. Available online: https://stat.gov.pl/ (accessed on 23 December 2020).

- Gwizdała, Jerzy. 2018. Perspektywy funkcjonowania koncepcji bancassurance w Polsce. Annales Universitatis Mariae Curie-Skłodowska, Sectio H Oeconomia 52: 61–69. [Google Scholar] [CrossRef]

- Hota, Sweta Leena. 2016. Bancassurance: Convergence of banking and insurance—A saga. International Journal of Research and Development—A Management Review 5: 11–15. [Google Scholar]

- Insurance Distribution Act. 2017. Insurance Distribution Act of 15 December 2017, Polish Journal of Laws 2017, Item 2486. Available online: http://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU20170002486/U/D20172486Lj.pdf (accessed on 14 February 2020).

- InsuranceData. 2020. Available online: https://www.insuranceeurope.eu/insurancedata (accessed on 23 December 2020).

- IZFA. 2020. Chamber of Fund and Asset Managers. Available online: https://www.izfa.pl/ (accessed on 23 December 2020).

- Jaspersen, Johannes. 2016. Hypothetical Surveys and Experimental Studies of Insurance Demand: A Review. The Journal of Risk and Insurance 83: 217–55. [Google Scholar] [CrossRef]

- Karimian, Paniz Haji. 2017. The effect of bancassurance on bank productivity and profitability, ARDL approach (evidences from banking industry in Iran). American Journal of Economics 7: 177–85. [Google Scholar]

- Kowalski, Jacek, and Elżbieta Kowalska. 2015. Ubezpieczenia grupowe a Rekomendacja U. Zeszyty Naukowe Wyższej Szkoły Bankowej w Poznaniu 59: 99–115. [Google Scholar]

- Košík, Oto, and Peter Poliak. 2011. Sprzedaż produktów bankowo-ubezpieczeniowych w kontekście kryzysu finansowego i postępującej globalizacji. Zeszyty Naukowe Wyższej Szkoły Bankowej w Poznaniu 35: 159–72. [Google Scholar]

- Kramaric, Tomislava Pavicz. 2019. Does bancassurance affect performance of non-life insurance sector-case of EU Countries. International Journal of Economic Sciences 8: 96–108. [Google Scholar] [CrossRef]

- Łada, Monika, and Małgorzata Białas. 2017. Financial Settlements as A Core of Inter-Organizational Management Accounting—Case Study of Bancassurance Cooperation. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 474: 77–84. [Google Scholar] [CrossRef]

- Lewis, Frank. 1989. Dependents and the Demand for Life Insurance. American Economic Review 79: 452–67. [Google Scholar]

- Liang, Hsin-Yu. 2015. Suggestions for Bancassurance Markets in China: Implications from European Countries. Geneva Papers on Risk and Insurance-Issues and Practice 40: 279–94. [Google Scholar] [CrossRef]

- Lisowski, Jacek, and Anna Chojan. 2020. InsurTech in CEE Region—Where Are We? In Global, Regional and Local Perspectives on the Economies of Southeastern Europe. Edited by Alexandra Horobet, Lucian Belascu, Persefoni Polychronidou and Anastasios Karasavvoglou. Springer Proceedings in Business and Economics. Berlin: Springer. [Google Scholar]

- Łosiewicz-Dniestrzańska, Ewa. 2016. Rola jednostki zapewnienia zgodności z regulacjami w procesie wprowadzania nowego produktu bankowego na rynek. Studia Ekonomiczne/Uniwersytet Ekonomiczny w Katowicach. Współczesne Finanse 275: 107–18. [Google Scholar]

- Malinowski, Artur. 2011. Zastosowanie bancassurance w Polsce. Zeszyty Naukowe Uniwersytetu Przyrodniczo-Humanistycznego w Siedlcach. Administracja i Zarządzanie 89: 137–46. [Google Scholar]

- Monkiewicz, Jan. 2000. Podstawy ubezpieczeń. Warszawa: Wydawnictwo POLTEXT. [Google Scholar]

- NBP (National Bank of Poland). 2020. Available online: https://www.nbp.pl/ (accessed on 23 December 2020).

- Recommendation U on Best Practice in Bancassurnace. 2014. Recommendation U on Best Practice in Bancassurnace. Available online: https://www.knf.gov.pl/knf/pl/komponenty/img/Rekomendacja_U_38338.pdf (accessed on 14 February 2020).

- Ociepa-Kicińska, Elżbieta. 2019. Produkty bancassurance w bankowości detalicznej w Polsce. Rozprawy Ubezpieczeniowe. Konsument na rynku usług finansowych 33: 53–67. [Google Scholar]

- Pajewska, Renata. 2000. Sojusze bankowo-ubezpieczeniowe. w: J., Monkiewicz, (red), Podstawy ubezpieczeń, tom I—Mechanizmy i funkcje. Poltext: Warszawa, pp. 306–8. [Google Scholar]

- Pajewska-Kwaśny, Renata, and Ilona Tomaszewska. 2009. Tendencje rozwoju bancassurance na rynku polskim. Myśl Ekonomiczna i Prawna 4: 174–83. [Google Scholar]

- Pielichaty, Edward. 2014. Zasady rachunkowości Banku w Świetle Rekomendacji U. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 373: 208–16. [Google Scholar] [CrossRef]

- Pielichaty, Edward. 2015. Rozpoznawanie przychodów ze sprzedaży produktów ubezpieczeniowych w księgach rachunkowych banków. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 390: 191–202. [Google Scholar] [CrossRef][Green Version]

- Pielichaty, Edward. 2017. Accounting Rules for Revenues Arising from Insurance Products Offered in Banks. Central European Review of Economics and Management 1: 85–105. [Google Scholar]

- Pisarewicz, Piotr. 2013. Struktura sprzedaży ubezpieczeń na krajowym rynku bancassurance. Zeszyty Naukowe Uniwersytetu Szczecińskiego. Finanse, Rynki Finansowe, Ubezpieczenia 62: 419–31. [Google Scholar]

- Pisarewicz, Piotr. 2014. Nowe standardy rynku bancassurance w zakresie ubezpieczeń z elementem inwestycyjnym lub oszczędnościowym. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 342: 206–15. [Google Scholar] [CrossRef][Green Version]

- PIU. 2019. PIU Report—Polish Market Bancassurance 4th Quarter 2019. Available online: https://piu.org.pl/wp-content/uploads/2020/04/Prezentacja-Rynek-BA-2019Q4.pdf (accessed on 9 May 2020).

- Polish Financial Supervision Authority. Annual Bulletin. Insurance Market. Warsaw: Polish Financial Supervision Authority, 2001–2019.

- Preckova, Lenka. 2017. Evaluation of Bancassurance Functioning in Selected Countries of the Financial Group KBC Group. In European Financial Systems 2017: Proceedings of the 14th International Scientific Conference. Edited by Josef Nesleha, Tomáš Plihal and Karel Urbanovsky. Brno: Masaryk University, pp. 192–98. [Google Scholar]

- Puja, Dua, Namita Sahay, and Onkar Singh Deol. 2019. Bancassurance model and its impact on Financial Inclusion: Review and Analysis. International Journal of Research and Analytical Reviews 6: 2. [Google Scholar]

- Reddy, Venkatanarsi Narsi, Seelam Marulu Reddy, and Peela Appala Naidu. 2020. Determinants of Life Insurance at Household Level: An Empirical Analysis of Andhra Pradesh, India. Waffen-Und Kostumkunde Journal XI: 49–61. [Google Scholar]

- Ricci, Ornella, and Franco Fiordelisi. 2010. Efficiency in the Life Insurance Industry: What Are the Efficiency Gains from Bancassurance? EMFI Working Paper No. 2. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Ricci, Ornella, and Franco Fiordelisi. 2011. Bancassurance Efficiency Gains: Evidence from the Italian Banking and Insurance Industries. The European Journal of Finance 17: 789–810. [Google Scholar]

- Ricci, Ornella, and Franco Fiordelisi. 2012. Bancassurance in Europe. Past, Present and Future. London: Palgrave Macmillan. [Google Scholar]

- Sadurska, Małgorzata. 2019. Bancassurance jako sposób generowania efektów synergicznych na rynku bankowo-ubezpieczeniowym. Zeszyty Naukowe Wyższej Szkoły Bankowej w Poznaniu 84: 75–84. [Google Scholar]

- Saha, Shyamasree, and Anirban Dutta. 2019. Factors Influencing Service Quality Perception in Indian Life Insurance Sector. Global Business Review 20: 1010–25. [Google Scholar] [CrossRef]

- Sereda, Paweł. 2015. Wpływ Rekomendacji U na funkcjonowanie rynku bancassurance. Zeszyty Naukowe Uniwersytetu Szczecińskiego. Finanse, Rynki Finansowe, Ubezpieczenia 2: 647–55. [Google Scholar]

- Showers, Vince, and Joyce Shotick. 1994. The Effects of Household Characteristics on Demand for Insurance: A Tobit Analysis. Journal of Risk and Insurance 61: 492–502. [Google Scholar] [CrossRef]

- Śliperski, Marek. 1998. Związki banków z firmami ubezpieczeniowymi i perspektywy ich rozwoju w Polsce. Ruch Prawniczy, Ekonomiczny i Socjologiczny 60: 213–34. [Google Scholar]

- Śliwiński, Adam. 2016. Popyt na ubezpieczenia na życie- przegląd badań światowych. In Polski Rynek Ubezpieczeń na tle kryzysów społeczno-gospodarczych. Edited by Stanisław Nowak, Alojzy Nowak and Andrzej Sopoćko. Warsaw: Wydawnictwo naukowe Wydziału Zarządzania Uniwersytetu Warszawskiego. [Google Scholar]

- Śliwiński, Adam. 2019. Rola ubezpieczeń w gospodarce. Wydawnictwo: Oficyna Wydawnicza SGH. [Google Scholar]

- Śliwiński, Adam, Tomasz Michalski, and Małgorzata Rószkiewicz. 2013. Demand for Life Insurance—An Empirical Analysis in the Case of Poland. The Geneva Papers on Risk and Insurance-Issues and Practice 38: 62–87. [Google Scholar] [CrossRef]

- Song, In Jung, Heejung Park, Narang Park, and Wookjae Heo. 2019. The effect of experiencing a death on life insurance ownership. Journal of Behavioral and Experimental Finance 22: 170–76. [Google Scholar] [CrossRef]

- Sreesha, C. H., and M. A. Joseph. 2011. Financial performance of banks in bancassurance: A study with special reference to State Bank of India. Indian Journal of Finance 5: 10–17. [Google Scholar]

- Staszczyk, Mateusz. 2013. Ubezpieczenie kart płatniczych jako sposób ochrony klienta banku przed finansowymi skutkami nagłych zdarzeń. Acta Universitatis Lodziensis. Folia Oeconomica 284: 195–207. [Google Scholar]

- Swacha-Lech, Magdalena. 2003. Społeczno-ekonomiczne determinanty atrakcyjności działalności bancassurance na rynku finansowym w Polsce (z punktu widzenia banków komercyjnych). Prace Naukowe Akademii Ekonomicznej we Wrocławiu 982: 144–55. [Google Scholar]

- Swacha-Lech, Magdalena. 2006. Bancassurance w mBanku—przyczyny podjęcia współpracy z firmami ubezpieczeń, sposoby realizacji strategii oraz jej pierwsze efekty. Prace Naukowe, Akademia Ekonomiczna w Katowicach. Współczesne problemy finansów, bankowości i ubezpieczeń w teorii i praktyce 1: 243–52. [Google Scholar]

- Szewieczek, Daniel. 2011. Finansowe konsekwencje oferty produktowej w warunkach dynamicznych zmian na rynku bancassurance. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 175: 138–49. [Google Scholar]

- Wierzbicka, Ewa. 2009. Kierunki ewolucji bancassurance. Zeszyty Naukowe, Uniwersytet Ekonomiczny w Poznaniu 127: 737–43. [Google Scholar]

- Wierzbicka, Ewa. 2016. Misselling barierą rozwoju ubezpieczeń w Polsce. Zeszyty Naukowe Wyższej Szkoły Humanitas. Zarządzanie 2: 315–27. [Google Scholar]

- Zharikova, Olena, and Katerina Cherkesenko. 2021. Integration of banks and insurance companies activities in Ukraine. Journal of Scientific Papers ‘Social Development and Security’ 11: 42–57. [Google Scholar] [CrossRef]

- Zietz, Emily Norman. 2003. An examinantion of demand for life insurance. Risk Management and Insurance Review 6: 159–91. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 7p Marketing Mix Dimension | Key Factors Influencing Customer Experience in Bancassurance |

|---|---|

| Product | Product variety, receiving maturity benefit, the facility to get the claim payments, designing of service offering, ease of buying, after-sale services, past experiences. |

| Price | Price, designing of service offering. |

| Promotion | Price, designing of service offering. |

| Place | Image, reliability of the channel, responsiveness of the channel, accuracy of the channel, opinion about staff, multiple service delivery channels, service quality (service convenience), |

| People | Interpersonal relationships, trust, satisfaction on service, friendliness of the bank personnel, recommendation for business, past experiences. |

| Process | Ease of buying, after-sale services, digitisation of the process, receiving stock market-related information, recommendation for business, past experiences. |

| Physical evidence | Image, brand, trust, pleasant and welcoming branch environment, friendliness of the bank personnel. |

| Area of Bancassurance | Number of Publications |

|---|---|

| General rules of functioning | 39 |

| Legal aspects | 9 |

| Financial aspects | 8 |

| Consumer aspects | 2 |

| Sales analysis | 8 |

| Product analyses | 8 |

| Development premise | 11 |

| Bank | Insurance Company | Customer |

|---|---|---|

|

|

|

| No. | Variable Name Used for the Model | Variable | Detailed Data Description | Total Score from Survey among Professionals |

|---|---|---|---|---|

| 1 | Age | Policyholder’s age | Average life expectancy for women and men in Poland, data source: own calculation based on Statistic of Poland (GUS) | 49 |

| 2 | Policyholder’s gender | 7 | ||

| 3 | Fam | Size of policyholder’s family (number of children, dependants) | Average number of people in a household in Poland, data source: Statistic of Poland (GUS) | 49 |

| 4 | Sal | Policyholder’s earnings | Average disposable income, data source: Statistic of Poland (GUS) | 69 |

| 5 | Wealth | Policyholder’s assets | Assets accumulated in investment funds, data source: chamber of fund and asset managers (IZFA) | 54 |

| 6 | RealEst | Real properties owned by policyholder | Average usable floor space per 1 person in Poland, data source: Statistic of Poland (GUS) | 50 |

| 7 | P | Insurance price | CPI for insurance, data source: Statistic of Poland (GUS) | 64 |

| 8 | Inflation | 19 | ||

| 9 | Unemp | Unemployment | Average unemployment rate in a given year, data source: own calculation based on Statistic of Poland (GUS) | 40 |

| 10 | Situation of the stock exchange (e.g., WIG20 quotations) | 12 | ||

| 11 | Exchange rate (EUR/PLN, CHF/PLN, etc.) | 12 | ||

| 12 | Interest rates (WIBOR, etc.) | 26 | ||

| 13 | Cash | Demand on cash loans | Consumer bank loans for households, data source: National Bank of Poland (NBP) | 56 |

| 14 | Mort | Demand on mortgage loans | Bank housing loans for households, data source: National Bank of Poland (NBP) | 59 |

| 15 | Dep | Level of bank deposits | Deposits and other liabilities of banks to households, data source: National Bank of Poland (NBP) | 36 |

| 16 | Link of insurance and banking product (loan, payment card, etc.) | 53 | ||

| 17 | Wka | Agent’s commission | The ratio of acquisition costs to gross written premium, data source: own calculation based on Polish Financial Supervision Authority (PFSA) | 54 |

| 18 | DUM1 | Caps in insurance products construction | Dummy variable, value −1 for every year since the restriction has been in force, and the 0 value for the earlier ones, data source: own calculation | 58 |

| 19 | DUM2 | Changes in legal environment | 39 | |

| Quartile 1 | 31 | |||

| Model | |

|---|---|

| Dependent variable (Y) | ∆(GWP_total) |

| Explanatory variables (Xi) | ∆(Age), ∆(Fam), ∆(Sal), ∆ (Wealth), ∆(RealEst), ∆(P), ∆(Unemp), ∆(Cash), ∆(Mort), ∆(Dep), ∆(Wka), DUM1, DUM2 |

| Regression equation | |

| Additional explanations | Ai- estimated regression coefficients, C constant |

| Model | ||

|---|---|---|

| Final form of the model | ∆(GWP_total) = A1 × ∆(Fam) + A2 × ∆(Mort) + A3 × ∆(Wka) + C | |

| Values of model parameters | A1 = −118,491,660.79 A2 = 65.35 A3 = −221,466,185.71 C = −4,269,523.78 | |

| Regression statistics | R2 = 0.846 Adjusted R2 = 0.804 | |

| Regression parameter statistics | A1: Standard error: 30,981,328.09 t-stat: −3.83 p-value 0.0028 < 0.05 A2: Standard error: 25.52 t-stat: 2.56 p-value = 0.0265 < 0.05 | A3: Standard error: 40,025,754.19 t-stat: −5.53 p-value = 0.0002 < 0.05 C: Standard error: 1,389,088.16256004 t-stat: −3.07361612839268 p-value = 0.0106 < 0.05 |

| Variance analysis | F: 20.12 Significance F: < 0.05 | |

| Stationarity of variables | KPSS Test for the ∆(GWP_total), ∆(Fam), ∆(Mort), ∆(Wka) variables shows p-value > 0.05, no basis for rejecting the series stationarity hypothesis | |

| Residuals randomness | α = 0.05, (+): 8, (-) 7, (#):8, critical values of series test: (D): 3; (G): 13, no basis for rejecting the residuals randomness hypothesis (although the value at the test limit) | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Śliwiński, A.; Dropia, J.; Duczkowski, N. Risk Factors Affecting Bancassurance Development in Poland. Risks 2021, 9, 130. https://doi.org/10.3390/risks9070130

Śliwiński A, Dropia J, Duczkowski N. Risk Factors Affecting Bancassurance Development in Poland. Risks. 2021; 9(7):130. https://doi.org/10.3390/risks9070130

Chicago/Turabian StyleŚliwiński, Adam, Joanna Dropia, and Norbert Duczkowski. 2021. "Risk Factors Affecting Bancassurance Development in Poland" Risks 9, no. 7: 130. https://doi.org/10.3390/risks9070130

APA StyleŚliwiński, A., Dropia, J., & Duczkowski, N. (2021). Risk Factors Affecting Bancassurance Development in Poland. Risks, 9(7), 130. https://doi.org/10.3390/risks9070130