Sustainability Reporting in Cooperatives

Abstract

1. Introduction

2. Literature Review

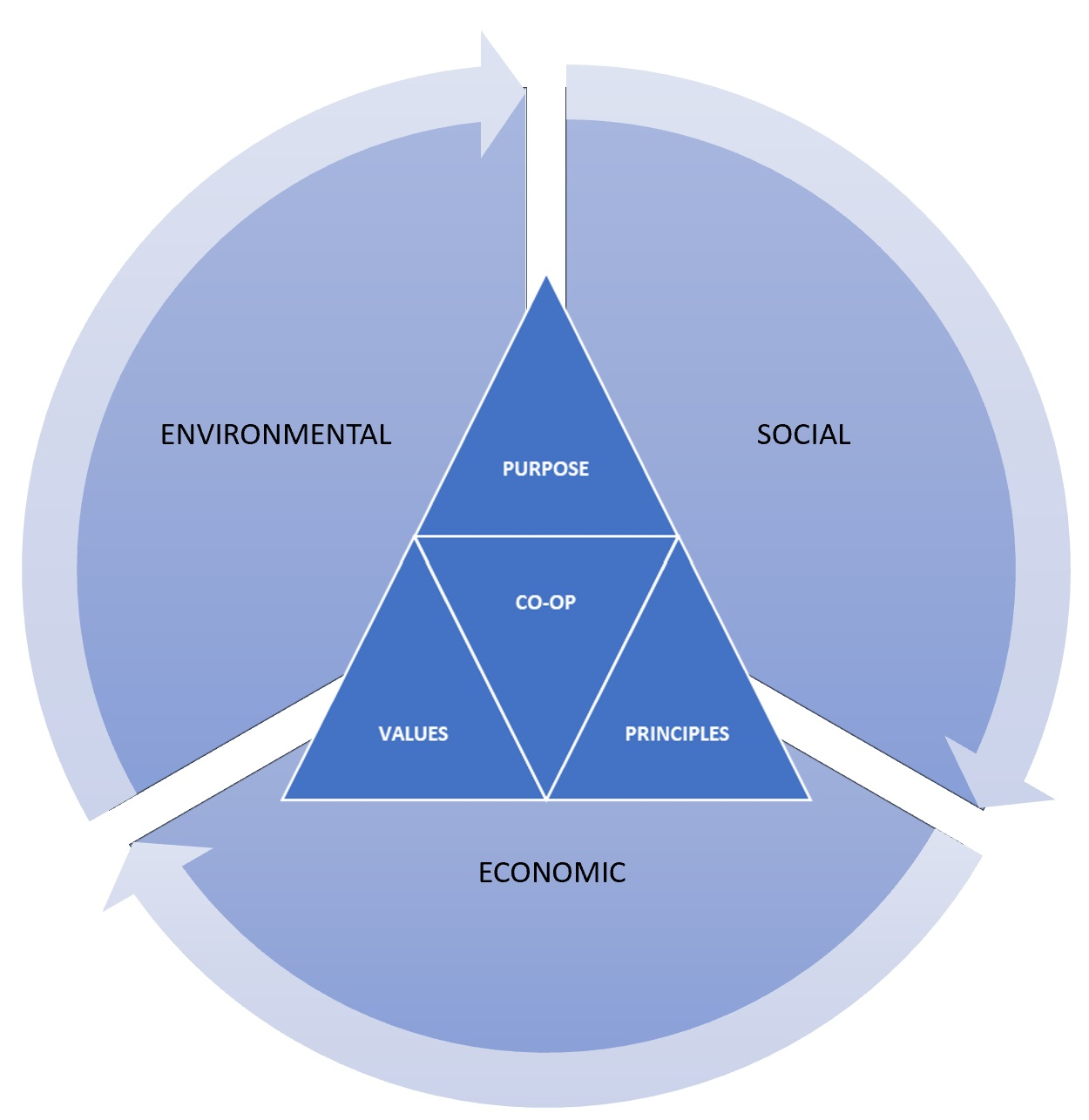

2.1. The Concept of Cooperative Values and Principles

2.2. Sustainability Reporting and the Global Reporting Initiative Framework

3. Methodology and Data

3.1. Research Question

3.2. Methodology of the Study

3.3. Sample of the Study

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Al-Tuwaijri, Sulaiman A., Theodore E. Christensen, and K. E. Hughes, II. 2004. The Relations among Environmental Disclosure, Environmental Performance, and Economic Performance: A Simultaneous Equations Approach. Accounting, Organizations and Society 29: 447–71. [Google Scholar] [CrossRef]

- Barton, David. 1989. What Is a Cooperative. Cooperatives in Agriculture. Edited by David Cobia. Hoboken: Prentice-Hall, Inc. [Google Scholar]

- Battaglia, Massimo, Lara Bianchi, Marco Frey, and Emilio Passetti. 2015. Sustainability Reporting and Corporate Identity: Action Research Evidence in an Italian Retailing Cooperative. Business Ethics: A European Review 24: 52–72. [Google Scholar] [CrossRef]

- Birchall, Johnston, and Richard Simmons. 2009. Co-operatives and Poverty Reduction. Manchester: Co-op College. [Google Scholar]

- Bollas-Araya, Helena María, and Elíes Seguí-Mas. 2014. Sustainability Reporting in Cooperative Banks: An Analysis of Their Disclosure in Europe. Available online: http://www.aeca1.org/pub/on_line/comunicaciones_xviicongresoaeca/cd/72h.pdf (accessed on 24 May 2019).

- Brown Leslie, Chiara Carini, Jessica Gordon Nembhard, Lou Hammond Ketilson, Elizabeth Hicks, John McNamara, Sonja Novkovic, Daphne Rixon, and Richard Simmons. 2015. Co-Operatives for Sustainable Communities: Tools to Measure Co-Operative Impact and Performance. Saskatoon: Centre for the Study of Co-operatives, University of Saskatchewan. [Google Scholar]

- Carnevale, Concetta, and Maria Mazzuca. 2014. Sustainability Report and Bank Valuation: Evidence from European Stock Markets. Business Ethics: A European Review 23: 69–90. [Google Scholar] [CrossRef]

- Collis, Jill, and Roger Hussey. 2014. Business Research: A Practical Guide for Undergraduate and Postgraduate Students. Basingstoke: Palgrave Macmillan. [Google Scholar]

- Dahlsrud, Alexander. 2008. How Corporate Social Responsibility Is Defined: An Analysis of 37 Definitions. Corporate Social Responsibility and Environmental Management 15: 1–13. [Google Scholar] [CrossRef]

- Dale, Anne, Fiona Duguid, Melissa Garcia Lamarca, Peter Hough, Petronella Tyson, Rebecca Foon, Robert Newell, and Yuill Herbert. 2013. Co-Operatives and Sustainability: An Investigation into the Relationship. Brussels: International Co-Operative Alliance, Community Research Connections, Sustainable Solutions Group, pp. 1–71. [Google Scholar]

- Daub, Claus-Heinrich. 2007. Assessing the Quality of Sustainability Reporting: An Alternative Methodological Approach. Journal of Cleaner Production 15: 75–85. [Google Scholar] [CrossRef]

- Etzion, Dror, and Fabrizio Ferraro. 2010. The Role of Analogy in the Institutionalization of Sustainability Reporting. Organization Science 21: 1092–107. [Google Scholar] [CrossRef]

- Filley, Horace Clyde. 1929. Cooperation in Agriculture. New York: John Wiley & Sons. Inc. London: Chapman & Hall Limited. [Google Scholar]

- Fonseca, Alberto, Mary Louise McAllister, and Patricia Fitzpatrick. 2014. Sustainability Reporting Among Mining Corporations: A Constructive Critique of the GRI Approach. Journal of Cleaner Production 84: 70–83. [Google Scholar] [CrossRef]

- Gladwin, Thomas N., James J. Kennelly, and Tara-Shelomith Krause. 1995. Shifting Paradigms for Sustainable Development: Implications for Management Theory and Research. Academy of Management Review 20: 874–907. [Google Scholar] [CrossRef]

- Global Reporting Initiative (GRI). 2013. G4 Sustainability Reporting Guidelines: Reporting Principles and Standard Disclosures. Amsterdam: Global Reporting Initiative, pp. 7–14. [Google Scholar]

- GRI Sustainability Disclosure Database. 2016. SDD-GRI Database. Available online: https://database.globalreporting.org/ (accessed on 24 May 2019).

- Hąbek, Patrycja, and Radosław Wolniak. 2016. Assessing the Quality of Corporate Social Responsibility Reports: The Case of Reporting Practices in Selected European Union Member States. Quality & Quantity 50: 399–420. [Google Scholar]

- Haffar, Merriam, and Cory Searcy. 2018. The Use of Context-Based Environmental Indicators in Corporate Reporting. Journal of Cleaner Production 192: 496–513. [Google Scholar] [CrossRef]

- Hahn, Rüdiger, and Michael Kühnen. 2013. Determinants of Sustainability Reporting: A Review of Results, Trends, Theory, and Opportunities in an Expanding Field of Research. Journal of Cleaner Production 59: 5–21. [Google Scholar] [CrossRef]

- Hasan, Iftekhar, Krzysztof Jackowicz, Robert Jagiełło, Oskar Kowalewski, and Łukasz Kozłowski. 2021. Local Banks as Difficult-to-Replace SME Lenders: Evidence from Bank Corrective Programs. Journal of Banking & Finance 123: 106029. [Google Scholar]

- Herbert, Yuill. 2015. Leadership in Hegemony: Sustainability Reporting and Cooperatives. In Co-Operatives for Sustainable Communities: Tools to Measure Cooperative Impact and Performance. Saskatoon: Co-Operatives and Mutuals Canada Centre for the Study of Co-Operatives, pp. 294–310. [Google Scholar]

- Holyoake, George Jacob. 1908. The History of Co-Operation. London: TF Unwin. [Google Scholar]

- International Cooperative Alliance (ICA). 1995. Statement on the Co-Operative Identity. Available online: https://www.ica.coop/coop/principles.html (accessed on 24 April 2018).

- International Cooperative Alliance (ICA). 2013. Blueprint for a Co-Operative Decade. Available online: https://www.ica.coop/sites/default/files/publication-files/ica-blueprint-final-feb-13-english-569977274.pdf (accessed on 1 March 2019).

- International Cooperative Alliance (ICA). 2015. Guidance Notes to the Co-Operative Principles. Available online: https://www.ica.coop/sites/default/files/publication-files/ica-guidance-notes-en-310629900.pdf (accessed on 24 April 2018).

- International Cooperative Alliance (ICA). 2016. Sustainability Reporting for Co-operatives: A Guidebook. Sustainability Solutions Group. Available online: https://www.ica.coop/sites/default/files/publication-files/ica-sustainability-reporting-guidebook-1497476007.pdf (accessed on 1 October 2018).

- International Labour Organization (ILO), and International Cooperative Alliance (ICA). 2014. Cooperatives and the Sustainable Development Goals—A Contribution to the Post-2015 Development Debate. Available online: https://www.ilo.org/wcmsp5/groups/public/---ed_emp/documents/publication/wcms_240640.pdf (accessed on 9 October 2018).

- Internatıonal Labour Organization (ILO). 2013. Cooperatives Today: Challenges and Opportunities. Available online: https://www.ilo.org/actrav/media-center/pr/WCMS_213266/lang--en/index.htm (accessed on 2 May 2021).

- Isaksson, Raine, and Ulrich Steimle. 2009. What Does GRI-Reporting Tell Us About Corporate Sustainability. The TQM Journal 21: 168–81. [Google Scholar] [CrossRef]

- Jenkins, Heledd, and Natalia Yakovleva. 2006. Corporate Social Responsibility in the Mining Industry: Exploring Trends in Social and Environmental Disclosure. Journal of Cleaner Production 14: 271–84. [Google Scholar] [CrossRef]

- Joseph, Corina, and Ross Taplin. 2011. The Measurement of Sustainability Disclosure: Abundance Versus Occurrence. In Accounting Forum 35: 19–31. [Google Scholar] [CrossRef]

- Joseph, Corina. 2010. Content Analysis of Sustainability Reporting on Malaysian Local Authority Websites. The Journal of Administrative Science 7: 101–25. [Google Scholar]

- Kolk, Ans. 2010. Trajectories of Sustainability Reporting by MNCs. Journal of World Business 45: 367–74. [Google Scholar] [CrossRef]

- KPMG. 2017. The KPMG Survey of Corporate Responsibility Reporting 2017. Available online: http://www.kpmg.com/crreporting (accessed on 13 April 2021).

- Krippendorff, Klaus. 2013. Content Analysis: An Introduction to Its Methodology. Southend Oaks: Sage Publications. [Google Scholar]

- Kumar, Kishore, and Ajai Prakash. 2019. Examination of Sustainability Reporting Practices in Indian Banking Sector. Asian Journal of Sustainability and Social Responsibility 4: 1–16. [Google Scholar] [CrossRef]

- Laliberté, Pierre. 2013. Growth and Development: Back to First Principles. In Cooperative Growth for the 21st Century. Brussels: ICA and CICOPA, pp. 11–13. [Google Scholar]

- Lee, Sun Young, and Craig E. Carroll. 2011. The Emergence, Variation, and Evolution of Corporate Social Responsibility in the Public Sphere, 1980–2004: The Exposure of Firms to Public Debate. Journal of Business Ethics 104: 115–31. [Google Scholar] [CrossRef]

- Marcis, Jaqueline, Edson Pinheiro de Lima, and Sérgio Eduardo Gouvêa da Costa. 2019. Model for Assessing Sustainability Performance of Agricultural Cooperatives. Journal of Cleaner Production 234: 933–48. [Google Scholar] [CrossRef]

- Milne, Markus J., and Ralph W. Adler. 1999. Exploring the Reliability of Social and Environmental Disclosures Content Analysis. Accounting, Auditing & Accountability Journal 12: 237–56. [Google Scholar]

- Moldavska, Anastasiia, and Torgeir Welo. 2017. The Concept of Sustainable Manufacturing and Its Definitions: A Content-Analysis Based Literature Review. Journal of Cleaner Production 166: 744–55. [Google Scholar] [CrossRef]

- NACE. 2008. NACE Rev.2: Statistical Classification of Economic Activities in the European Community. Luxembourg: Office for Official Publications of the European Communities. Available online: https://ec.europa.eu/eurostat/documents/3859598/5902521/KS-RA-07–015-EN.PDF (accessed on 20 June 2019).

- Nilsson, Jerker. 1996. The Nature of Cooperative Values and Principles: Transaction Cost Theoretical Explanations. Annals of Public and Cooperative Economics 67: 633–53. [Google Scholar] [CrossRef]

- Rehber, Erkan. 2011. Kooperatifçilik. Bursa: Ekin Yayınevi. [Google Scholar]

- Riding, Allan, Barbara J. Orser, Martine Spence, and Brad Belanger. 2012. Financing New Venture Exporters. Small Business Economics 38: 147–63. [Google Scholar] [CrossRef]

- Sahin, Zeynep, and Fikret Cankaya. 2018. Türkiye’de GRI Rehberine Göre Hazırlanan Sürdürülebilirlik Raporlarının Icerik Analizi. Muhasebe Bilim Dünyası Dergisi 20: 860–79. [Google Scholar]

- Schotanus, Fredo, and Jan Telgen. 2007. Developing A Typology of Organisational Forms of Cooperative Purchasing. Journal of Purchasing and Supply Management 13: 53–68. [Google Scholar] [CrossRef]

- Seguí-Mas, Elíes, Helena María Bollas Araya, and Paula Asensi Peiró. 2016. Why Do Cooperatives Assure Their CSR Reports? An Analysis of the Motivations and Benefits in a Big Retail Cooperative. CIRIEC-España, Revista de Economía Pública, Social y Cooperativa 87: 39–68. [Google Scholar] [CrossRef]

- Seguí-Mas, Elies, Helena-María Bollas-Araya, and Fernando Polo-Garrido. 2015. Sustainability Assurance on the Biggest Cooperatives of the World: An Analysis of Their Adoption and Quality. Annals of Public and Cooperative Economics 86: 363–83. [Google Scholar] [CrossRef]

- Simmons, Richard, Bob Yuill, and Jim Booth. 2015. Governing Resilient Co-operatives: Agricultural Co-operation in Scotland. In Co-Operative Governance Fit to Build Resilience in the Face of Complexity. Brussels: International Co-Operative Alliance, pp. 35–48. [Google Scholar]

- Steinhöfel, Erik, Mila Galeitzke, Holger Kohl, and Ronald Orth. 2019. Sustainability Reporting in German Manufacturing SMEs. Procedia Manufacturing 33: 610–17. [Google Scholar] [CrossRef]

- Stocki, Ryszard, and Peter Hough. 2016. CoopIndex: Human Dignity as the Essence of Co-operative Values. Journal of Co-Operative Accounting and Reporting 4: 79–104. [Google Scholar]

- Tajbakhsh, Alireza, and Azam Shamsi. 2019. Sustainability Performance of Countries Matters: A Non-parametric Index. Journal of Cleaner Production 224: 506–22. [Google Scholar] [CrossRef]

- Turley-McIntyre, Barbara, Ashleigh Marchl, and Brenda Stasuik. 2016. Sustainability Reporting in Canada’s Financial Institutions. Journal of Co-Operative Accounting and Reporting 4: 35–58. [Google Scholar]

- United Nations (UN). 2015. Transforming Our World: The 2030 Agenda for Sustainable Development. United Nations General Assembly. Available online: http://www.un.org/ga/search/view_doc.asp?symbol=A/RES/70/1&Lang=E (accessed on 15 March 2019).

- Vormedal, Irja, and Audun Ruud. 2009. Sustainability Reporting in Norway—An Assessment of Performance in the Context of Legal Demands and Socio-political Drivers. Business Strategy and the Environment 18: 207–22. [Google Scholar] [CrossRef]

- Weber, Robert Philip. 1990. Basic Content Analysis. New York: Sage. [Google Scholar]

- Yadav, Shiv Shankar Kumar, Naseem Abidi, and Asit Bandyopadhayay. 2017. Development of the Environmental Sustainability Indicator Profile for ITeS Industry. Procedia Computer Science 122: 423–30. [Google Scholar] [CrossRef]

- Lu Yalin, Erli Dan, Yiwei Guo, Xiaohua Song, and Xiaoyan Liu. 2019. Government-led Sustainability Reporting by China’s HEIs. Journal of Cleaner Production 230: 445–59. [Google Scholar] [CrossRef]

{kind=link}

| GRI-G4 Indicators | Number of Indicators |

|---|---|

| Economic (EC) | 9 |

| Environmental (EN) | 34 |

| Social | - |

| -Sub-Category: Labor Practices and Decent Work (LA) | 16 |

| -Sub-Category: Human Rights (HR) | 12 |

| -Sub-Category: Society (SO) | 11 |

| -Sub-Category: Product Responsibility (PR) | 9 |

| Total | 91 |

| Criteria | Characteristics of Sample | Frequency | Percent |

|---|---|---|---|

| Size | Large | 116 | 69.0 |

| MNE | 28 | 16.7 | |

| SME | 24 | 14.3 | |

| Total | 168 | 100.0 | |

| Sector | Wholesale and Retail Trade | 38 | 22.6 |

| Agriculture | 13 | 7.7 | |

| Healthcare Services | 33 | 19.6 | |

| Financial Services | 56 | 33.3 | |

| Other | 28 | 16.8 | |

| Total | 168 | 100.0 | |

| Assurance | Unapplied | 114 | 67.9 |

| Applied | 54 | 32.1 | |

| Total | 168 | 100.0 | |

| Report Year | 2014 | 15 | 8.9 |

| 2015 | 37 | 22.0 | |

| 2016 | 49 | 29.2 | |

| 2017 | 51 | 30.4 | |

| 2018 | 16 | 9.5 | |

| Total | 168 | 100.00 | |

| Report Page | 100 page or less | 83 | 49.4 |

| 101 pages or more | 85 | 50.6 | |

| Total | 168 | 100.0 |

| Country | Frequency | Percent |

|---|---|---|

| Argentina | 6 | 3.6 |

| Austria | 3 | 1.8 |

| Belgium | 3 | 1.8 |

| Brazil | 36 | 21.4 |

| Canada | 12 | 7.1 |

| Chile | 2 | 1.2 |

| China | 2 | 1.2 |

| Colombia | 4 | 2.4 |

| Croatia | 2 | 1.2 |

| Ecuador | 4 | 2.4 |

| Egypt | 1 | 0.6 |

| Finland | 10 | 6.0 |

| France | 1 | 0.6 |

| Germany | 8 | 4.8 |

| India | 3 | 1.8 |

| Indonesia | 1 | .6 |

| Italy | 7 | 4.2 |

| Malaysia | 3 | 1.8 |

| Morocco | 2 | 1.2 |

| Netherlands | 11 | 6.5 |

| Norway | 3 | 1.8 |

| Pakistan | 1 | 0.6 |

| Peru | 1 | 0.6 |

| South Korea | 1 | 0.6 |

| Spain | 16 | 9.5 |

| Sweden | 7 | 4.2 |

| Switzerland | 10 | 6.0 |

| Taiwan | 3 | 1.8 |

| UK | 2 | 1.2 |

| USA | 1 | 0.6 |

| Vietnam | 2 | 1.2 |

| Total | 168 | 100.0 |

| Economic Performance Indicators | Unreported | Reported | ||

|---|---|---|---|---|

| Frequency | Percent | Frequency | Percent | |

| EC1 | 21 | 12.5 | 147 | 87.5 |

| EC2 | 103 | 61.3 | 65 | 38.7 |

| EC3 | 93 | 55.4 | 75 | 44.6 |

| EC4 | 120 | 71.4 | 48 | 28.6 |

| EC5 | 104 | 61.9 | 64 | 38.1 |

| EC6 | 118 | 70.2 | 50 | 29.8 |

| EC7 | 100 | 59.5 | 68 | 40.5 |

| EC8 | 82 | 48.8 | 86 | 51.2 |

| EC9 | 85 | 50.6 | 83 | 49.4 |

| Environmental Performance Indicators | Unreported | Reported | Environmental Performance Indicators | Unreported | Reported | ||||

|---|---|---|---|---|---|---|---|---|---|

| Frequency | Percent | Frequency | Percent | Frequency | Percent | Frequency | Percent | ||

| EN1 | 89 | 53.0 | 79 | 47.0 | EN18 | 89 | 53.0 | 79 | 47.0 |

| EN2 | 107 | 63.7 | 61 | 36.3 | EN19 | 87 | 51.8 | 81 | 48.2 |

| EN3 | 31 | 18.5 | 137 | 81.5 | EN20 | 138 | 82.1 | 30 | 17.9 |

| EN4 | 109 | 64.9 | 59 | 35.1 | EN21 | 130 | 77.4 | 38 | 22.6 |

| EN5 | 91 | 54.2 | 77 | 45.8 | EN22 | 128 | 76.2 | 40 | 23.8 |

| EN6 | 71 | 42.3 | 97 | 57.7 | EN23 | 62 | 36.9 | 106 | 63.1 |

| EN7 | 115 | 68.5 | 53 | 31.5 | EN24 | 149 | 88.7 | 19 | 11.3 |

| EN8 | 78 | 46.4 | 90 | 53.6 | EN25 | 140 | 83.3 | 28 | 16.7 |

| EN9 | 139 | 82.7 | 29 | 17.3 | EN26 | 148 | 88.1 | 20 | 11.9 |

| EN10 | 139 | 82.7 | 29 | 17.3 | EN27 | 101 | 60.1 | 67 | 39.9 |

| EN11 | 157 | 93.5 | 11 | 6.5 | EN28 | 143 | 85.1 | 25 | 14.9 |

| EN12 | 151 | 89.9 | 17 | 10.1 | EN29 | 96 | 57.1 | 72 | 42.9 |

| EN13 | 150 | 89.3 | 18 | 10.7 | EN30 | 103 | 61.3 | 65 | 38.7 |

| EN14 | 160 | 95.2 | 8 | 4.8 | EN31 | 119 | 70.8 | 49 | 29.2 |

| EN15 | 44 | 26.2 | 124 | 73.8 | EN32 | 110 | 65.5 | 58 | 34.5 |

| EN16 | 56 | 33.3 | 112 | 66.7 | EN33 | 122 | 72.6 | 46 | 27.4 |

| EN17 | 83 | 49.4 | 85 | 50.6 | EN34 | 144 | 85.7 | 24 | 14.3 |

| Labor Practices and Decent Work (LA) | Unreported | Reported | Labor Practices and Decent Work (LA) | Unreported | Reported | ||||

| Frequency | Percent | Frequency | Percent | Frequency | Percent | Frequency | Percent | ||

| LA1 | 31 | 18.5 | 137 | 81.5 | LA9 | 44 | 26.2 | 124 | 73.8 |

| LA2 | 63 | 37.5 | 105 | 62.5 | LA10 | 66 | 39.3 | 102 | 60.7 |

| LA3 | 103 | 61.3 | 65 | 38.7 | LA11 | 75 | 44.6 | 93 | 55.4 |

| LA4 | 110 | 65.5 | 58 | 34.5 | LA12 | 40 | 23.8 | 128 | 76.2 |

| LA5 | 90 | 53.6 | 78 | 46.4 | LA13 | 87 | 51.8 | 81 | 48.2 |

| LA6 | 45 | 26.8 | 123 | 73.2 | LA14 | 113 | 67.3 | 55 | 32.7 |

| LA7 | 118 | 70.2 | 50 | 29.8 | LA15 | 125 | 74.4 | 42 | 25.0 |

| LA8 | 114 | 67.9 | 54 | 32.1 | LA16 | 115 | 68.5 | 53 | 31.5 |

| Human Rights (HR) | Unreported | Reported | Human Rights (HR) | Unreported | Reported | ||||

| Frequency | Percent | Frequency | Percent | Frequency | Percent | Frequency | Percent | ||

| HR1 | 124 | 73.8 | 44 | 26.2 | HR7 | 143 | 85.1 | 25 | 14.9 |

| HR2 | 113 | 67.3 | 55 | 32.7 | HR8 | 156 | 92.9 | 12 | 7.1 |

| HR3 | 103 | 61.3 | 65 | 38.7 | HR9 | 153 | 91.1 | 15 | 8.9 |

| HR4 | 138 | 82.1 | 30 | 17.9 | HR10 | 115 | 68.5 | 53 | 31.5 |

| HR5 | 129 | 76.8 | 39 | 23.2 | HR11 | 134 | 79.8 | 34 | 20.2 |

| HR6 | 136 | 81.0 | 32 | 19.0 | HR12 | 133 | 79.2 | 35 | 20.8 |

| Society (SO) | Unreported | Reported | Society (SO) | Unreported | Reported | ||||

| Frequency | Percent | Frequency | Percent | Frequency | Percent | Frequency | Percent | ||

| SO1 | 60 | 35.7 | 108 | 64.3 | SO7 | 126 | 75.0 | 42 | 25.0 |

| SO2 | 127 | 75.6 | 41 | 24.4 | SO8 | 91 | 54.2 | 77 | 45.8 |

| SO3 | 113 | 67.3 | 55 | 32.7 | SO9 | 126 | 75.0 | 42 | 25.0 |

| SO4 | 77 | 45.8 | 91 | 54.2 | SO10 | 145 | 86.3 | 22 | 13.1 |

| SO5 | 109 | 64.9 | 59 | 35.1 | SO11 | 144 | 85.7 | 24 | 14.3 |

| SO6 | 129 | 76.8 | 39 | 23.2 | - | - | - | - | - |

| Product Responsibility (PR) | Unreported | Reported | Product Responsibility (PR) | Unreported | Reported | ||||

| Frequency | Percent | Frequency | Percent | Frequency | Percent | Frequency | Percent | ||

| PR1 | 89 | 53.0 | 79 | 47.0 | PR6 | 113 | 67.3 | 55 | 32.7 |

| PR2 | 104 | 61.9 | 64 | 38.1 | PR7 | 94 | 56.0 | 74 | 44.0 |

| PR3 | 108 | 64.3 | 60 | 35.7 | PR8 | 81 | 48.2 | 87 | 51.8 |

| PR4 | 95 | 56.5 | 73 | 43.5 | PR9 | 87 | 51.8 | 81 | 48.2 |

| PR5 | 47 | 28.0 | 121 | 72.0 | - | - | - | - | - |

| Scale | Size of Co-op | n | Mean | SD | F | p |

|---|---|---|---|---|---|---|

| Economic Performance | Large | 116 | 3.97 | 2.77 | 0.873 | 0.419 |

| MNE | 28 | 4.68 | 2.29 | |||

| SME | 24 | 3.92 | 2.15 | |||

| Environmental Performance | Large | 116 | 12.13 | 7.81 | 1.558 | 0.214 |

| MNE | 28 | 10.78 | 7.62 | |||

| SME | 24 | 9.29 | 6.10 | |||

| Labor Practices and Decent Work | Large | 116 | 8.06 | 4.30 | 0.486 | 0.616 |

| MNE | 28 | 8.46 | 3.39 | |||

| SME | 24 | 7.33 | 4.44 | |||

| Human Rights | Large | 116 | 2.68 | 2.95 | 2.637 | 0.075 |

| MNE | 28 | 3.32 | 3.49 | |||

| SME | 24 | 1.46 | 2.36 | |||

| Society | Large | 116 | 3.91 | 3.09 | 3.589 | 0.030 * |

| MNE | 28 | 3.32 | 2.02 | |||

| SME | 24 | 2.25 | 2.03 | |||

| Product Responsibility | Large | 116 | 4.41 | 2.81 | 2.924 | 0.057 |

| MNE | 28 | 4.00 | 2.67 | |||

| SME | 24 | 2.92 | 2.75 | |||

| Social Performance (Overall) | Large | 116 | 19.06 | 11.75 | 2.137 | 0.121 |

| MNE | 28 | 19.11 | 9.83 | |||

| SME | 24 | 13.96 | 9.94 |

| Scale | Sector | n | Mean | SD | F | p |

|---|---|---|---|---|---|---|

| Economic Performance | Wholesale and Retail Trade | 38 | 3.63 | 2.78 | 3.045 | 0.019 * |

| Agriculture | 13 | 2.92 | 2.18 | |||

| Healthcare Services | 33 | 3.52 | 2.49 | |||

| Financial Services | 56 | 4.96 | 2.55 | |||

| Other | 28 | 4.14 | 2.46 | |||

| Environmental Performance | Wholesale and Retail Trade | 38 | 13.66 | 5.64 | 1.140 | 0.340 |

| Agriculture | 13 | 11.08 | 8.00 | |||

| Healthcare Services | 33 | 11.12 | 9.38 | |||

| Financial Services | 56 | 11.18 | 7.19 | |||

| Other | 28 | 9.89 | 8.08 | |||

| Labor Practices and Decent Work | Wholesale and Retail Trade | 38 | 7.74 | 3.74 | 2.734 | 0.031 * |

| Agriculture | 13 | 5.15 | 4.34 | |||

| Healthcare Services | 33 | 8.94 | 3.68 | |||

| Financial Services | 56 | 8.73 | 4.53 | |||

| Other | 28 | 7.25 | 3.93 | |||

| Human Rights | Wholesale and Retail Trade | 38 | 2.53 | 2.90 | 1.331 | 0.261 |

| Agriculture | 13 | 1.31 | 2.21 | |||

| Healthcare Services | 33 | 3.15 | 3.42 | |||

| Financial Services | 56 | 2.95 | 3.27 | |||

| Other | 28 | 2.04 | 2.13 | |||

| Society | Wholesale and Retail Trade | 38 | 2.37 | 1.99 | 4.171 | 0.003 * |

| Agriculture | 13 | 3.00 | 3.83 | |||

| Healthcare Services | 33 | 3.79 | 2.97 | |||

| Financial Services | 56 | 4.61 | 3.01 | |||

| Other | 28 | 3.14 | 2.17 | |||

| Product Responsibility | Wholesale and Retail Trade | 38 | 3.74 | 2.70 | 2.116 | 0.081 |

| Agriculture | 13 | 2.77 | 2.83 | |||

| Healthcare Services | 33 | 4.64 | 2.79 | |||

| Financial Services | 56 | 4.70 | 2.62 | |||

| Other | 28 | 3.57 | 3.11 | |||

| Social Performance (Overall) | Wholesale and Retail Trade | 38 | 16.37 | 9.63 | 2.723 | 0.031 * |

| Agriculture | 13 | 12.23 | 12.44 | |||

| Healthcare Services | 33 | 20.52 | 11.41 | |||

| Financial Services | 56 | 20.98 | 11.87 | |||

| Other | 28 | 16.00 | 10.10 |

| Scale | Year Report Published | n | Mean | SD | F | p |

|---|---|---|---|---|---|---|

| Economic Performance | 2014 | 15 | 3.67 | 2.41 | 0.504 | 0.733 |

| 2015 | 37 | 4.30 | 2.73 | |||

| 2016 | 49 | 4.27 | 2.63 | |||

| 2017 | 51 | 4.10 | 2.59 | |||

| 2018 | 16 | 3.38 | 2.73 | |||

| Environmental Performance | 2014 | 15 | 12.33 | 7.93 | 0.251 | 0.909 |

| 2015 | 37 | 11.32 | 8.11 | |||

| 2016 | 49 | 11.49 | 7.02 | |||

| 2017 | 51 | 11.90 | 7.65 | |||

| 2018 | 16 | 9.94 | 8.28 | |||

| Labor Practices and Decent Work | 2014 | 15 | 7.53 | 4.81 | 0.222 | 0.926 |

| 2015 | 37 | 8.30 | 4.14 | |||

| 2016 | 49 | 8.18 | 4.22 | |||

| 2017 | 51 | 8.04 | 4.19 | |||

| 2018 | 16 | 7.31 | 3.81 | |||

| Human Rights | 2014 | 15 | 2.27 | 2.37 | 0.433 | 0.785 |

| 2015 | 37 | 3.14 | 3.26 | |||

| 2016 | 49 | 2.47 | 2.61 | |||

| 2017 | 51 | 2.61 | 3.11 | |||

| 2018 | 16 | 2.19 | 3.82 | |||

| Society | 2014 | 15 | 3.67 | 3.02 | 0.357 | 0.839 |

| 2015 | 37 | 3.89 | 3.03 | |||

| 2016 | 49 | 3.57 | 2.74 | |||

| 2017 | 51 | 3.53 | 2.74 | |||

| 2018 | 16 | 2.88 | 3.16 | |||

| Product Responsibility | 2014 | 15 | 3.67 | 2.77 | 0.552 | 0.698 |

| 2015 | 37 | 4.54 | 2.74 | |||

| 2016 | 49 | 4.22 | 2.82 | |||

| 2017 | 51 | 4.10 | 2.82 | |||

| 2018 | 16 | 3.44 | 3.12 | |||

| Social Performance (Overall) | 2014 | 15 | 17.13 | 11.62 | 0.408 | 0.803 |

| 2015 | 37 | 19.86 | 11.65 | |||

| 2016 | 49 | 18.45 | 10.53 | |||

| 2017 | 51 | 18.27 | 11.26 | |||

| 2018 | 16 | 15.81 | 13.28 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

|---|---|---|---|---|---|---|---|

| Economic | 1 | 0.654 * | 0.786 * | 0.590 * | 0.699 * | 0.783 * | 0.818 * |

| Environmental | 1 | 0.700 * | 0.625 * | 0.644 * | 0.634 * | 0.745 * | |

| Labor Practices and Decent Work | 1 | 0.656 * | 0.698 * | 0.736 * | 0.903 * | ||

| Human Rights | 1 | 0.750 * | 0.636 * | 0.856 * | |||

| Society | 1 | 0.698 * | 0.884 * | ||||

| Product Responsibility | 1 | 0.866 * | |||||

| Social (Overall) | 1 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yakar Pritchard, G.; Çalıyurt, K.T. Sustainability Reporting in Cooperatives. Risks 2021, 9, 117. https://doi.org/10.3390/risks9060117

Yakar Pritchard G, Çalıyurt KT. Sustainability Reporting in Cooperatives. Risks. 2021; 9(6):117. https://doi.org/10.3390/risks9060117

Chicago/Turabian StyleYakar Pritchard, Gamze, and Kıymet Tunca Çalıyurt. 2021. "Sustainability Reporting in Cooperatives" Risks 9, no. 6: 117. https://doi.org/10.3390/risks9060117

APA StyleYakar Pritchard, G., & Çalıyurt, K. T. (2021). Sustainability Reporting in Cooperatives. Risks, 9(6), 117. https://doi.org/10.3390/risks9060117